Please admit California’s Pajaro Valley to the storehouse of evidence that charging a fee to use scarce resources can stretch those resources, to the benefit of all.

Never heard of Pajaro Valley? Me neither, until I came across NY Times climate reporter Coral Davenport’s compelling end-of-year story, Strawberry Case Study: What if Farmers Had to Pay for Water? Turns out I once hitch-hiked there en route to the spectacular Big Sur coast south of Monterey. But the payoff today is in the story’s subhead: With aquifers nationwide in dangerous decline, one part of California has tried essentially taxing groundwater. New research shows it’s working.

California’s Pajaro Valley, at center of this Google Map, hugs the Pacific Coast midway between Santa Cruz and Monterey and straddles the two counties named for those cities.

What’s working? A charge for groundwater extracted to grow strawberries, raspberries, brussels sprouts, lettuce and kale, administered by the state-chartered Pajaro Valley Water Management Agency to prevent saltwater from the adjacent Pacific Ocean from intruding into underground aquifers. The fee, which began several decades ago at a nominal $30 per acre-foot of water to recover PVWMA’s water-metering costs, now runs as high as $400, according to Davenport.

Lest that rise seem meteoric, and today’s price appear punitive, consider that currently the agency’s total annual water fees, $12 million, equate to barely 1 percent of annual Pajaro Valley crop revenues of $12 million. What’s more, an acre-foot — the standard volumetric for water supply — is enormous: enough to provide 3 million tall glasses of water, by my calculations. Even the projected 2025 price of $500 per acre-foot translates to a mere one-sixtieth of a cent per glass.

To be sure, that calculation is merely illustrative; water for drinking and water for growing crops are two different things. But consider what Pajaro Valley growers get from paying for water.

First, their payments are helping assure increased supplies of crop-worthy water. Revenue from the water fees enabled PVWMA to undertake a $6 million project that captures excess rainwater from a creek near the ocean and injects it into underground wells to be used for irrigation, and a $20 million water recycling plant that cleans 5 million gallons of sewage a day and pipes it to farm fields. Next up, Davenport tells us, is an $80 million system to capture and store more rainwater for irrigation. By replenishing and “stretching’ supplies of groundwater, these investments help ensure that brackish water from the ocean doesn’t seep into Pajaro Valley wells.

Just as importantly, the growers receive a potent incentive to use available water supplies more efficiently. “Gone were the days of sprinklers that drenched fields indiscriminately,” Davenport writes. “To save money, many Pajaro farmers invested in precision irrigation technology to distribute carefully measured water exactly where it was needed.” (See text box.) Though the article doesn’t mention it, these investments by dozens of individual growers might not have materialized had not all growers been subject to the same incentives to conserve as well.

Just as importantly, the growers receive a potent incentive to use available water supplies more efficiently. “Gone were the days of sprinklers that drenched fields indiscriminately,” Davenport writes. “To save money, many Pajaro farmers invested in precision irrigation technology to distribute carefully measured water exactly where it was needed.” (See text box.) Though the article doesn’t mention it, these investments by dozens of individual growers might not have materialized had not all growers been subject to the same incentives to conserve as well.

Economics

Undergirding Davenport’s upbeat reporting is a 2023 working paper, The Dynamic Impacts of Pricing Groundwater, by three economists at U-C Berkeley’s Dept. of Agricultural and Resource Economics. In academic parlance, “dynamic” doesn’t connote a Marvel superhero, it refers to changes over time. By examining changes in water usage over time, the authors conclude that each “21% price increase led to a … 22% reduction in average annual groundwater extraction” by Pajaro Valley growers.

The implied price-elasticity is roughly negative 1.3. (The paper helpfully reports that “The reduction in annual water use doubles between the first year and the fifth year after the tax, with the implied price elasticity of demand ranging from negative 0.86 to negative 1.97.) This empirically-derived price sensitivity is far greater than the price elasticities assumed in CTC’s carbon-tax model, befitting not only the greater salience of water use for growers vis-a-vis energy use for consumers and even most businesses, but the greater agency of Pajaro Valley growers who, Davenport’s reporting suggests, over time have increasingly bought into PVWMA’s groundwater fee in both theory and execution.

After reading Davenport’s article I reached out to hydrologist, climatologist and water sustainability expert Peter Gleick, whose latest book, The Three Ages of Water: Prehistoric Past, Imperiled Present, and a Hope for the Future, was published last year by Hachette / Public Affairs. Peter praised the article while preferring to denote the PVWMA groundwater charge “not [as a] tax but a fee or simply a price for a commodity.” He added, “When we pay for something, we’re more conscious of how we use it. When something is free, we’re more likely to misuse and abuse it. That’s certainly been the case historically for California groundwater.”

After reading Davenport’s article I reached out to hydrologist, climatologist and water sustainability expert Peter Gleick, whose latest book, The Three Ages of Water: Prehistoric Past, Imperiled Present, and a Hope for the Future, was published last year by Hachette / Public Affairs. Peter praised the article while preferring to denote the PVWMA groundwater charge “not [as a] tax but a fee or simply a price for a commodity.” He added, “When we pay for something, we’re more conscious of how we use it. When something is free, we’re more likely to misuse and abuse it. That’s certainly been the case historically for California groundwater.”

Carbon Taxes?

A number of posts in this space have touted — we might say “flogged” — other instances of resource or externality pricing, as possible templates for large-scale carbon pricing. In 2016 we wrote about Berkeley’s soda tax, actually a tax on the sugar content of soft drinks, and summarized research showing that sales of sugar-sweetened beverages fell 21% in that city while rising 4% in “control groups,” i.e., neighboring municipalities where soft drinks continued untaxed. Last year we explained why Congestion pricing, coming soon to New York City, could bode well for carbon-taxing — a message we previously broadcast several times in 2019 as the enabling legislation was being enacted in Albany, in March and in April.

We also dug deep in 2017, writing about an incipient NYC nickel fee on carryout bags dispensed at supermarkets, grocery and convenience stores. (The fee was a month away from taking effect, and though we haven’t yet seen before/after comparisons, anecdotal evidence suggests that trees in New York City are today far less encumbered by what we referred to then as “gossamer debris stuck, like tumors, to our half-a-million street trees.”) We can also go back half a century, to 1972, when NYC environmental officials conjured a “dirty oil surcharge” that forced petroleum suppliers to cough up a fee for each barrel of high-sulfur oil they brought into the city, a remarkably successful (but little known) instance of externality pricing that I memorialized in a 2009 post for Grist, Pollution Taxes Work.

Needless to say, none of these fees — not the soda tax, not congestion charging, not the carryout bag fee, and not the dirty oil surcharge — has paved the way for full-on carbon pricing. While each of them has been or will be a resounding success, their scale is far too local and the stakes far too small to translate automatically to national or even state-level carbon pricing. The same will hold for California’s Pajaro Valley groundwater fee. Indeed, California water districts are wrestling today with the hard work of fulfilling a state mandate requiring every part of the state to devise a plan to conserve groundwater.

Happily, Davenport notes that PVWMA officials and even some growers are advising their statewide counterparts to emulate their approach, including “local control” rather than state or even county governance. Less happily, she reports that the Westlands Water District, which serves the state’s giant Central Valley breadbasket, is pushing a plan “that would allow growers to pay for credits to use groundwater above a certain allocation.” The growers “could buy and sell the credits, starting at about $200 a credit,” Davenport notes. While this scheme certainly improves on the status quo of charging little or nothing for groundwater use, it’s complicated and drenched in market ideology, much as carbon cap-and-trade systems needlessly encumber what could and should be straightforward carbon pricing.

Let’s not end on that dour note, however. These instances of resource charging — whether to stretch a limited resource or to internalize pollution or other externality costs — make it easier to build support for enacting new ones. Davenport’s story — here’s the link again — is both brilliant reporting and cause for optimism.

We close with a snap of the story opening and photo as they appeared on the front page of today’s (Jan. 4, 2024) Times, above the fold. Below it are calculations in which we derived figures in the first part of this post.

Calculation #1: Glasses of water in an acre-foot.

- One acre = 43,560 ft^2, so one acre-foot = 43,560 ft^3.

- One ft^3 (cubic foot) contains 957.5 fluid oz. (per inchcalculator.com; that figure jibes with the 62.4 lb weight of one cubic foot of water).

- A tall water glass contains 14 fluid oz. Thus, one ft^3 of water can fill 957.5/14 = 68.4 tall glasses.

- One acre-foot then contains enough water to fill 43,560 x 68.4 = 2.98 million tall glasses, which we round to 3 million.

Calculation #2: Groundwater-use price-elasticity inferred from empirical finding that a 21 percent price increase evokes a 22 percent decrease in usage.

- It is tempting to reduce this roughly 1-to-1 relationship to a (negative) 1.0 price-elasticity. However, that would ignore the law of diminishing returns and, mathematically, the convex relationship between changes in price and changes in usage.

- The price-elasticity is derived by solving for e in the equation, (1 + 0.21)^e = (1 minus 0.22).

- Using base-10 logarithms, we have: e times log 1.21 = log 0.78, which (omitting one or two steps) leads to e = negative 1.3.

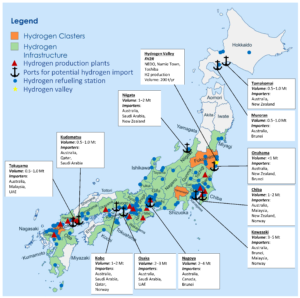

Japan has taken a major step in clean shipping. A consortium led by Japan Engine Corporation and Kawasaki Heavy Industries has successfully tested the world’s first hydrogen-fueled main engine for a large commercial vessel.

This engine is designed for deep-sea cargo ships, not just small vessels. That makes it a key milestone. Most earlier hydrogen ship projects focused on ferries or short routes.

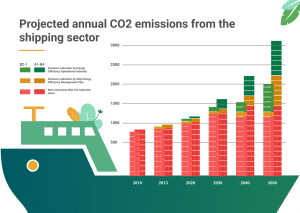

The 3% Problem: Shipping’s Emissions Challenge

The engine is a low-speed, two-stroke design. This is the standard for large ocean-going ships. It can run mainly on hydrogen fuel. In tests, it achieved about 95% hydrogen use at full load, showing stable performance.

The engine will be installed on a 17,500-deadweight-ton multipurpose vessel. The ship is expected to be delivered in 2027. It will then undergo a three-year demonstration period starting in 2028.

Shipping is a major source of global emissions. The sector produces about 2–3% of global greenhouse gas emissions, based on data from the International Maritime Organization (IMO).

Most ships today use heavy fuel oil or marine diesel. These fuels produce high emissions. As global trade grows, shipping emissions could increase without new solutions.

Hydrogen is one option. When used as a fuel, it produces no carbon dioxide at the point of use. This makes it attractive for long-term decarbonization.

However, scaling hydrogen for large ships has been difficult. Key challenges include fuel storage, engine design, and safety. Japan’s latest engine test shows that progress is being made.

How Hydrogen Engines Work in Large Vessels

Hydrogen-powered ships can use fuel cells or combustion engines. Japan’s new system uses combustion. This means hydrogen burns inside the engine, similar to diesel. This approach allows easier integration with existing ship systems. It also reduces the need for full redesigns of vessels.

The engine uses liquid hydrogen fuel and advanced injection systems. Engineers have focused on stable combustion and material strength. Hydrogen burns faster than traditional fuels, so precision is critical.

The project includes partners such as Mitsui O.S.K. Lines (MOL), Onomichi Dockyard, and ClassNK. These groups support design, safety checks, and future operations.

The move is part of Japan’s Green Innovation Fund. The Ministry of Economy, Trade, and Industry has funded the program with about 2 trillion yen to help the country reach carbon neutrality by 2050.

Japan’s Net Zero Strategy and Hydrogen Push

This hydrogen engine project fits into Japan’s broader climate strategy. The country has pledged to reach net-zero greenhouse gas emissions by 2050. This goal was announced by former Prime Minister Yoshihide Suga in 2020.

Japan sees hydrogen as a key part of its energy transition. Under its Basic Hydrogen Strategy, the government aims to expand hydrogen use across power, transport, and industry.

Japan plans to increase its hydrogen supply to 20 million tonnes per year by 2050, up from much lower current levels. The country is also investing in hydrogen imports, storage, and infrastructure.

Shipping plays a major role in this plan. Japan depends heavily on imports of energy and raw materials. Decarbonizing shipping is important for both climate and energy security.

- RELATED: Maritime Decarbonization: Japanese Shipping Giant NYK Partners with 1PointFive for DAC Credits

Projects like the hydrogen engine help link domestic policy with global action. They support Japan’s goal to build a full hydrogen value chain, from production to transport and end use.

Current Hydrogen Ferries in Operation

Japan has already started using hydrogen-powered ferries on real routes. One example is the Hanaria. This hybrid ship uses hydrogen fuel cells, lithium-ion batteries, and biodiesel. It began service in Kitakyushu in April 2024.

The ship can cut carbon dioxide emissions by 53% to 100% compared to regular vessels. It was built for a unit of Mitsui O.S.K. Lines and uses fuel cell technology developed with parts from Toyota.

Another example is the Mahoroba, built by Iwatani Corporation. This is a zero-emission hydrogen catamaran that can carry up to 150 passengers. It started commercial service in April 2025, transporting visitors to the Osaka-Kansai Expo.

In October 2025, the Tokyo Metropolitan Government agreed to bring the vessel to Tokyo Bay. It is expected to start operating there in fiscal year 2026. It will support environmental education and international events.

Japan has also invested in hydrogen transport systems. One example is the Suiso Frontier, which was launched to carry liquefied hydrogen across long distances. These efforts show that Japan is not only testing technology but also building the systems needed to scale hydrogen use globally.

From Ferries to Freighters: Scaling Hydrogen at Sea

Japan is part of a wider global shift. Many countries are testing hydrogen and other clean fuels for shipping.

For example, Norway launched the MF Hydra in 2023. Belgium introduced the Hydrotug 1 in 2024.

However, most of these vessels are small or operate on short routes. Japan’s project targets large cargo ships, which are more complex and more impactful for emissions.

Governments are also exploring hydrogen shipping corridors. These are planned routes where hydrogen-powered vessels can operate with proper fueling infrastructure. This global activity shows that hydrogen is moving from early testing to larger applications.

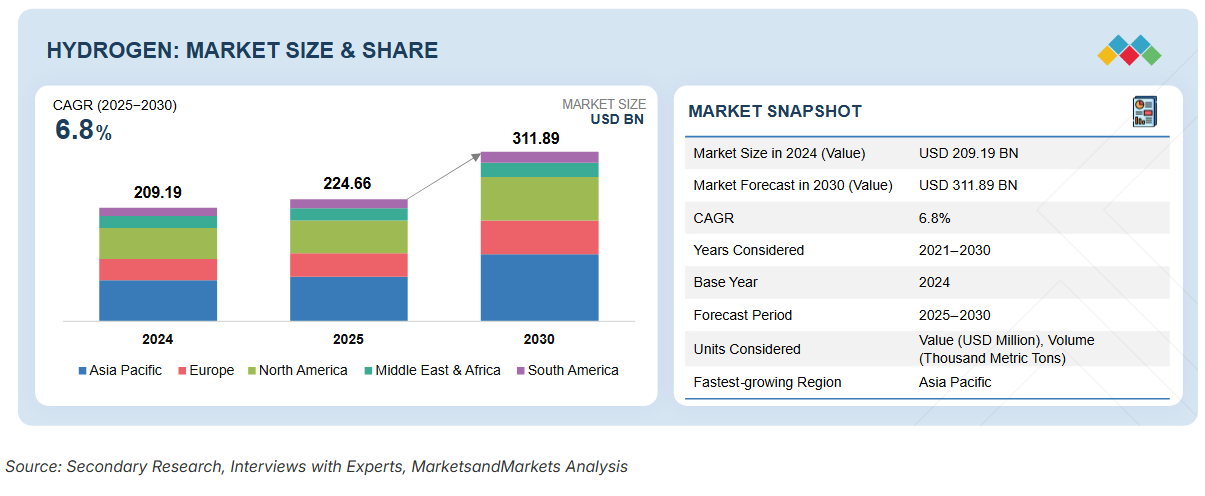

A $300B Hydrogen Market Meets Maritime Demand

The hydrogen economy is expanding quickly. Global demand is rising as industries look for low-carbon solutions.

Industry estimates suggest the global hydrogen market could exceed US$300 billion by 2030. Growth is driven by energy, transport, and industrial use.

In shipping, hydrogen competes with other fuels like ammonia and methanol. Each has strengths and challenges. Hydrogen stands out for its zero carbon emissions at the point of use.

Cost, Storage, and Infrastructure Barriers

Still, hydrogen has limits. Several barriers remain before hydrogen ships become common:

- High costs compared to traditional fuels,

- Limited supply of green hydrogen,

- Lack of port infrastructure, and

- Strict safety requirements.

Despite these issues, investment is growing. Governments and companies are funding research, pilot projects, and infrastructure.

Japan’s demonstration project will help address those gaps. The planned three-year trial will provide real-world data on performance, safety, and costs. If successful, hydrogen engines could become a practical option for large vessels. This would help reduce emissions from global shipping.

Can Hydrogen Power the Future of Global Trade?

Japan’s hydrogen engine test marks a key moment for the shipping industry. It shows that hydrogen can power not only small vessels but also large commercial ships.

The link to Japan’s net-zero strategy makes this development even more important. It connects national policy with global climate goals.

The coming years will shape how fast hydrogen shipping grows. With strong policy support and continued innovation, hydrogen could play a major role in building a low-carbon maritime sector.

The post Japan Unveils First Hydrogen Engine for Large Ships appeared first on Carbon Credits.

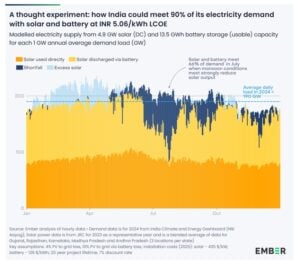

The post Solar Plus Batteries Can Meet 90% of India’s Electricity Needs, Says Ember appeared first on Carbon Credits.

Carbon Footprint

Bioleaching Breakthrough in Canada: How MIRARCO’s Pilot Facility Turns Mine Waste into Critical Minerals

A new wave of innovation is reshaping how the mining industry approaches waste. CBC News, Canada, reported that researchers in Sudbury, northern Ontario, are developing a bacteria-based technology called bioleaching, which uses naturally occurring microbes to extract valuable metals such as nickel, cobalt, and copper from old mine tailings.

Led by MIRARCO Mining Innovation, the team recently opened a pilot facility in October 2025 to scale up this process, aiming to transform mining waste into a source of critical minerals while cutting emissions, reducing environmental risks, and unlocking billions of dollars in untapped resources.

Sudbury Moves Toward Commercial Bioleaching

Sudbury has a long history of mining, leaving behind massive piles of tailings—the leftover rock and sediment from ore extraction. These materials still hold billions of dollars’ worth of metals, but until now, recovering them was difficult, energy-intensive, and expensive. The bioleaching technology changes that. By using bacteria that naturally digest minerals, scientists can release metals from waste rock without relying on harsh chemicals or high temperatures.

According to Nadia Mykytczuk, CEO of MIRARCO, the new pilot facility represents a shift toward sustainable mining. She precisely mentioned that,

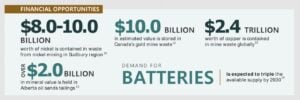

In Sudbury alone, the tailings contain $8 billion to $10 billion worth of nickel. With this facility, we are shaping a new era of mining innovation—one that focuses on clean technology, critical minerals, and preparing the workforce of tomorrow.

The facility connects research, industry, and community partners, creating a hub for applied research in bioleaching and bioprocessing.

Before moving to the new facility, MIRARCO operated within Laurentian University, and the long-standing partnership continues. The pilot center allows researchers to handle larger samples of mine waste and test how bioleaching works at a scale closer to industrial operations. This is essential for proving that the process can be commercially viable in Canada.

Bioleaching Breakthrough: Turning Tailings into Critical Minerals

- The process starts by grinding the mine tailings and mixing them with a nutrient-rich liquid. Scientists then introduce specialized bacteria into the mixture.

- These microbes feed on the minerals, producing chemical reactions that dissolve metals into the liquid.

- The resulting slurry moves through a series of reactors, where the process continues, and metals are eventually collected in a liquid form.

Early experiments are promising. Scientists at MIRARCO have noted that the process can recover 98–99 percent of nickel from the tested tailings. The value surpasses traditional methods that often leave large amounts of valuable minerals behind.

In separate research, scientists are growing and refining the bacteria. Different microbes target specific minerals. Some thrive in acidic conditions, ideal for breaking down sulfide tailings, while others focus on iron oxides or silicate rocks.

This flexibility allows scientists to extract not only common metals like nickel and copper but also rare earth elements and lithium, which are critical for batteries and renewable energy technology.

Environmental and Carbon Benefits

Traditional metal extraction uses energy-intensive methods, including high-temperature processing, chemical treatments, and heavy machinery. This approach produces substantial carbon emissions and generates more waste. Bioleaching operates at ambient temperature and pressure, reducing energy use by an estimated 30–40 percent.

It also tackles the challenge of storing mining waste. Canada produces around 650 million tons of mine tailings every year. Much of this material sits in ponds behind dams, which can be unstable and pose long-term environmental risks.

Significantly, tailings may generate acid or release metals into the environment, and dam failures can have serious consequences. The 2014 Mount Polley mine tailings dam failure incident in British Columbia is a stark reminder of these dangers.

By turning tailings into a source of metals, bioleaching reduces the volume of waste requiring storage, cutting both environmental risk and the legacy costs of old mining sites.

Overcoming Challenges

While promising, the technology is not without hurdles. Processing tailings can be costly, and the bacteria require careful monitoring and specific growth conditions. Scaling up from pilot operations to full commercial production will also need investment in infrastructure and specialized equipment.

Environmental experts, such as MiningWatch Canada, note that tailings can behave unpredictably. They may chemically react over time or shift physically, posing stability concerns. Effective containment and monitoring are critical to ensure the process remains safe at larger scales.

Despite these challenges, researchers are optimistic. Early pilot studies indicate that the bacterial method could recover 65–80 percent of minerals left behind by conventional processing. This is a significant improvement that makes further investment worthwhile.

Fueling Canada’s Clean Energy Future

The technology comes at a crucial time. Global demand for critical minerals is rising as electric vehicles, wind turbines, and solar panels become more widespread. Canada has identified 31 minerals essential for the energy transition, but many are currently imported from regions with supply risks. Bioleaching offers a way to unlock domestic resources while reducing dependence on imports.

The process could provide materials for electric vehicle batteries, grid infrastructure, and industrial applications. Lithium and cobalt can power EVs, rare earth elements like neodymium and dysprosium support wind turbines and other clean energy systems, and copper and nickel are essential for electrical grids.

By recovering these from tailings, Canada could strengthen its supply chains while reducing environmental impact.

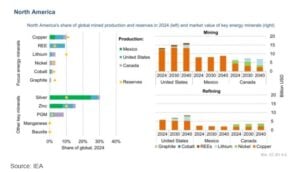

By 2040, the IEA expects the value of North America’s energy minerals to grow to around USD 30 billion for mining and USD 14 billion for refining. Mining growth will mainly come from copper in the United States and Mexico, and from lithium and nickel in Canada.

For refining, the region could make up about 4% of the global market, led by copper and lithium refining in the United States and copper and nickel refining in Canada.

Moving Toward Commercial Deployment

MIRARCO aims to transition from pilot testing to full-scale operations in the next two to three years. Globally, bioleaching is already in use at around 30 mining sites, but Canada has yet to deploy it commercially. The pilot facility in Sudbury is helping bridge that gap by testing continuous processing and demonstrating commercial viability.

Government support is also playing a key role. CBC further highlighted that funding through Canada’s Clean Technology Program and provincial innovation grants is helping advance research and development. The technology aligns with national goals to position Canada as a global leader in sustainable critical minerals production by 2030.

Overall, industry analysts predict bioextraction could become commercially viable within three to five years for specific minerals, with broader adoption following as operational experience grows.

The post Bioleaching Breakthrough in Canada: How MIRARCO’s Pilot Facility Turns Mine Waste into Critical Minerals appeared first on Carbon Credits.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits