The average UK winter has become around 1C warmer and 15% wetter over the past century, new Carbon Brief analysis shows.

The analysis covers more than 100 years of data on temperature, rainfall, wind speed and snow, to assess how UK winters have changed.

The data show that extremely warm and wet winters are becoming more common. Six of the 10 warmest winters on record were in the 21st century, and four of these also rank in the top 10 wettest years on record.

Despite the trend towards milder conditions, extreme cold snaps still hit the UK. The winter of 2009-10, for example, was dubbed the “Big Freeze of 2010” and clocked in as the UK’s least-windy, second-snowiest and eighth-coldest winter on record.

However, extreme cold periods are becoming less common. On average, the UK saw more than 12 snow days each winter in 1971-2000. This dropped to 9.5 snow days each winter by 1991-2020.

As the climate continues to warm, the UK can expect winters to continue getting warmer and wetter. Met Office projections suggest that, under an emissions pathway in line with current global policies, the average UK winter by 2080-99 will be 2C warmer and 11% wetter than they were in 1981-2000.

Warmer winters

The UK Met Office has been collecting meteorological data from thousands of weather stations across the UK since the 1880s. Using this data, it has produced a gridded dataset called HadUK, which provides complete coverage across the UK for a range of climate variables – including rainfall, temperature, snow days and wind speed – on a one-square-kilometre grid.

Carbon Brief has analysed the data for meteorological winters – defined as December, January and February – to determine how weather conditions have changed since records began.

The plot below shows a timeseries of annual winter average temperature (dark blue) over 1884-2021. These are shown as anomalies – that is, the difference compared to a baseline, which in this case is the average winter temperature over 1991-2020.

(Winters are shown on graphs in this article according to the year in which December falls. For example, the winter of December 2021 to February 2022 is shown as 2021.)

The Met Office, in line with the World Meteorological Organisation, uses 30-year averages to assess changes in UK climate. The table below shows average absolute UK winter temperatures for overlapping 30-year time periods across the full data record.

| Time period | Average temperature | Maximum temperature | Minimum temperature |

|---|---|---|---|

| 1881-1910 | 2.96* | 5.77* | 0.18* |

| 1891-1920 | 3.29 | 6.06 | 0.53 |

| 1901-1930 | 3.50 | 6.21 | 0.80 |

| 1911-1940 | 3.51 | 6.21 | 0.83 |

| 1921-1950 | 3.41 | 6.12 | 0.73 |

| 1931-1960 | 3.29 | 6.05 | 0.56 |

| 1941-1970 | 3.09 | 5.84 | 0.35 |

| 1951-1980 | 3.17 | 5.91 | 0.46 |

| 1961-1990 | 3.22 | 5.94 | 0.51 |

| 1971-2000 | 3.65 | 6.40 | 0.91 |

| 1981-2010 | 3.75 | 6.58 | 0.94 |

| 1991-2020 | 4.12 | 6.97 | 1.28 |

Average, maximum and minimum winter temperatures for overlapping 30-year time periods, from 1881 to 2020, using the December-February average of mean monthly temperatures. An asterisk (*) indicates that a full 30 years was not available for this average.

The average UK winter in 1991-2020 was 0.9C warmer than during 1961-90. The most recent 30-year period also includes the warmest maximum, minimum and average temperatures since Met Office records began.

In addition, with an average winter temperature of 4.64C, the most-recent decade (2013-22) – not shown in the table – has seen a further temperature increase of 0.52C above the 1991-2020 average.

Warmer winters are already impacting UK wildlife. For example, Grahame Madge – senior press officer for the Met Office – told the Guardian that animals including hedgehogs, bats and butterflies are emerging from hibernation too early:

“Abnormal warm spells during winter can encourage species out of hibernation. Butterflies such as red admirals and small tortoiseshells and other insects can be particularly challenged as they can emerge largely without access to life-saving food sources like nectar. If the warm spell is followed by a return to colder conditions, the hibernating individuals will have used up valuable energy reserves without being able to replace them, possibly with disastrous consequences.”

Meanwhile, the National Trust says warmer winters have “particularly devastating impacts for trees”, as cold snaps are often not long enough to kill off harmful diseases and pests.

Looking at individual years gives a more detailed picture. The graphic below shows the warmest and coldest 10 winters in the UK since 1884. The dark blue line shows average UK winter temperature, and red and blue dots indicate the warmest and coldest individual winters, respectively. The table below shows the dates and temperatures of these winters.

| Warmest winters | Coldest winters | |||

|---|---|---|---|---|

| Years | Temperature (C) | Years | Temperature (C) | |

| 1 | 1988-99 | 5.76 | 1962-63 | -0.31 |

| 2 | 2006-07 | 5.53 | 1894-95 | 0.42 |

| 3 | 2015-16 | 5.43 | 1946-47 | 0.75 |

| 4 | 1997-98 | 5.40 | 1978-79 | 1.13 |

| 5 | 2019-20 | 5.28 | 1939-4 | 1.23 |

| 6 | 1974-75 | 5.22 | 1916-17 | 1.33 |

| 7 | 2021-22 | 5.20 | 1928-29 | 1.46 |

| 8 | 2013-14 | 5.19 | 2009-10 | 1.63 |

| 9 | 1934-35 | 5.13 | 1885-8 | 1.65 |

| 10 | 2018-19 | 5.09 | 1940-41 | 1.80 |

Warmest and coldest 10 winters in the UK since 1884. The dark blue line shows average UK winter temperature, and red and blue dots indicate the warmest and coldest individual winters. The table beneath shows the dates and temperatures of these winters. Credit: Chart by Carbon Brief, based on the Met Office HadUK dataset.

The graph shows that six of the 10 warmest winters on record have occurred in the 21st century. Conversely, only one of the UK’s coldest 10 winters were in the 21st century – the winter of 2009-10.

The Met Office also provides country-level data for different parts of the UK. The plot below shows 10-year rolling average winter temperature for England (dark blue), Scotland (red), Northern Ireland (light blue) and Wales (yellow).

The plot shows that Scotland consistently sees the coldest winters, while England, Wales and Northern Ireland experience winter temperatures that are an average of around 1.5-2C warmer.

Snow days

As average temperatures rise across the UK, extremely cold days are becoming less common, while record-breaking warm days are becoming more frequent.

Five of the top 10 warmest days ever recorded during UK winters occurred during a single week February 2019.

Carbon Brief analysed the warmest maximum and coldest minimum temperature on record for each UK winter. The table below shows the years with the warmest (red) maximum daily temperatures and coldest (blue) minimum daily temperatures since 1960.

| Warmest maximum temperatures | Coldest minimum temperatures | |||

|---|---|---|---|---|

| Temperature (C) | Year | Temperature (C) | Year | |

| 1 | 16.1 | 2018-19 | -10.2 | 1986-87 |

| 2 | 14.3 | 1997-98 | -10.1 | 1962-63 |

| 3 | 14.0 | 2015-16 | -10.0 | 1981-82 |

| 4 | 13.8 | 1989-90 | -9.9 | 1978-79 |

| 5 | 13.6 | 2003-04 | -9.5 | 1971-72 |

| 6 | 13.5 | 1985-86 | -9.3 | 2010-11 |

| 7 | 13.4 | 2011-12 | -9.1 | 1995-96 |

| 8 | 13.3 | 2016-17 | -8.9 | 1969-70 |

| 9 | 13.3 | 2021-22 | -8.7 | 2009-10 |

| 10 | 13.2 | 1994-95 | -8.7 | 1968-69 |

Years with the 10 warmest (red) maximum temperatures, and coldest (blue) minimum temperatures, based on individual winter days since 1960. Credit: Chart by Carbon Brief, based on the Met Office HadUK dataset.

Most of the warmest winter extremes on record were in the 21st century. Meanwhile, most of the coldest extremes were in the 20th century.

One way of measuring the change in extreme cold days is to count the number of “frost days” – days with a minimum temperature below 0C – recorded throughout the winter. Another way is to count the number of “snow days”, when snow can be seen on the ground at 9am.

Dr Mark McCarthy is the head of the Met Office National Climate Information Centre, which manages the UK’s climate records. He explains that to calculate snow days, an individual looks at a “representative patch of ground” at 9am in the morning, and if at least half of it is covered in snow, then it is counted as “snowy”.

These results are averaged across hundreds or thousands of observations. This means that, for example, “an average of five days of snow might mean that half of that region had 10 days and half the region had no days”, he explains.

The plot below shows the number of frost days since 1960 (red) and snow days since 1971 (blue) over winter. The black lines show the 10-year running average.

The table below shows the total number of first and snow days during UK winters for four overlapping 30-year time periods.

| Time period | Frost days | Snow days |

|---|---|---|

| 1961-1990 | 38.43 | – |

| 1971-2000 | 35.07 | 12.29 |

| 1981-2010 | 35.17 | 11.73 |

| 1991-2020 | 32.75 | 9.54 |

Total number of frost and snow days for 30-year time periods, from 1931 to 2020, using the December-February average of mean monthly temperatures. An asterisk (*) indicates that a full 30 years was not available for this average.

The plot shows that air frost and snow days are closely linked. Snow will generally not form if the ground temperature is above 5C, and in the UK, the heaviest snowfalls tend to occur when the air temperature is between 0C and 2C.

On average, the UK saw 12.3 snow days each winter over 1971-2000. This dropped to 9.5 snow days each winter by 1991-2020.

There is also regional variation in snow days. Over the entire 1971-2020 dataset, Scotland received 18.6 days of snow per winter on average, while the UK, Northern Ireland and Wales received between 7.2 and 8.8.

“Significant and widespread lying snow might have been considered fairly typical for a UK winter of several decades ago,” says the Met Office’s latest State of the UK climate report. However, it adds that “this type of event has become increasingly unusual in a warming climate over the last two or three decades”.

The graph below shows the UK winters with the greatest (light blue dots) and smallest (red dots) number of snow days since 1971.

| Snowiest winters | Least snowy winters | |||

|---|---|---|---|---|

| Years | Snow days | Years | Snow days | |

| 1 | 1978-79 | 35.62 | 2019-20 | 2.12 |

| 2 | 2009-10 | 30.59 | 1991-92 | 2.39 |

| 3 | 1981-82 | 26.90 | 2007-08 | 2.97 |

| 4 | 1985-86 | 23.69 | 1988-89 | 3.15 |

| 5 | 2010-11 | 23.13 | 2021-22 | 3.35 |

| 6 | 1984-85 | 21.54 | 1997-98 | 3.45 |

| 7 | 1976-77 | 20.77 | 2013-14 | 3.49 |

| 8 | 1977-78 | 18.54 | 2016-17 | 3.57 |

| 9 | 1995-96 | 18.43 | 2005-06 | 3.72 |

| 10 | 1990-91 | 18.13 | 1974-75 | 3.90 |

Snowiest and least snowy 10 winters in the UK since 1884. The dark blue line shows seasonal “snow days”, and red and blue dots indicate the snowiest and least snowy individual winters. The table beneath shows the dates and number of snow days of these winters. Credit: Chart by Carbon Brief, based on the Met Office HadUK dataset.

While the climate is becoming milder and snow is becoming less common, very cold and snowy winters can still happen. For example, the winter of 2009-10, dubbed the “Big Freeze of 2010” in parts of the UK media, was the least-windy, second-snowiest and eighth-coldest winter on record in the UK.

Severe snowfall that winter caused “very significant disruption across the UK”, according to the UK Met Office, which adds that “transport was particularly badly affected with snowfalls causing numerous road closures, and train and flight cancellations”.

On 18 December 2009, five Eurostar trains got stuck in the Channel Tunnel after cold temperatures caused electrical failures, trapping 2,000 people for 16 hours. All Eurostar services were cancelled for the next three days.

In January that winter, BBC News reported that “heavy snow and freezing temperatures has caused chaos across Scotland over the past three weeks, with hundreds of schools closed and motorists facing hazardous conditions on the roads”.

Research from the UK Met Office indicates that the odds of the UK having a winter as cold as the one in 2009-10 will drop to less than 1% by the end of the century as global temperatures continue to rise.

Wetter winters

The total volume of rainfall recorded during UK winters is also rising. The plot below shows total winter rainfall in mm over 1836-2021 (blue) and the 10-year rolling average (black).

The table below shows average UK winter rainfall totals for a series of overlapping 30-year time periods across the full data record.

| 30-year period | Average annual winter rainfall (mm) |

|---|---|

| 1831-1860 | 254.69* |

| 1841-1870 | 276.00 |

| 1851-1880 | 284.28 |

| 1861-1890 | 287.46 |

| 1871-1900 | 281.51 |

| 1881-1910 | 279.06 |

| 1891-1920 | 300.55 |

| 1901-1930 | 311.07 |

| 1911-1940 | 314.51 |

| 1921-1950 | 305.00 |

| 1931-1960 | 298.76 |

| 1941-1970 | 290.82 |

| 1951-1980 | 293.23 |

| 1961-1990 | 301.82 |

| 1971-2000 | 329.22 |

| 1981-2010 | 330.01 |

| 1991-2020 | 346.98 |

Average winter rainfall over overlapping 30-year time periods, from 1831 to 2020, using the December-February average of mean monthly temperatures. An asterisk (*) indicates that a full 30 years was not available.

Between 1961-90 and 1990-2020, the UK winters became 15% wetter on average – increasing from around 300mm of rainfall to almost 350mm. The more recent decade of 2012-21 – not shown in the table – has seen further increases, with average winter rainfall of 380mm.

The Met Office also provides country-level rainfall data. The plot below shows 10-year rolling average winter temperature for England (dark blue), Scotland (red), Northern Ireland (light blue) and Wales (yellow).

The graph shows that rainfall is increasing across all four regions of the UK, but remains consistently the lowest in England and the highest in Scotland and Wales.

Looking at the wettest and driest years across the UK shows that individual rainfall extremes are becoming more common. In a ranking going back to 1884, seven of the driest years were in the 19th century, while three were in the 20th. None of the driest years on record have been in the 21st century.

Meanwhile, four of the rainiest winters have been in the 21st century. The graph below shows the wettest (blue dots) and driest (red dots) winters since 1884.

| Rainiest winters (mm) | Least rainy winters (mm) | |||

|---|---|---|---|---|

| Years | Winter rainfall | Years | Winter rainfall | |

| 1 | 2013-14 | 540.3 | 1963-64 | 121.3 |

| 2 | 2015-16 | 505.7 | 1890-91 | 141.4 |

| 3 | 1994-95 | 498.2 | 1844-45 | 164.6 |

| 4 | 1989-90 | 482.2 | 1933-34 | 170.4 |

| 5 | 2019-20 | 474.5 | 1846-47 | 171.3 |

| 6 | 1876-77 | 458.0 | 1962-63 | 171.5 |

| 7 | 1914-15 | 450.7 | 1857-58 | 176.6 |

| 8 | 1868-69 | 439.6 | 1840-41 | 179.6 |

| 9 | 2006-07 | 435.8 | 1937-38 | 186.9 |

| 10 | 1993-94 | 431.4 | 1854-55 | 189.1 |

Wettest and driest 10 winters in the UK since 1884. The dark blue line shows total winter rainfall, and blue and red dots indicate the driest and wettest snowy individual winters. The grey dashed lines the volume of rainfall recorded during the rainiest and least rainy winters on record. The table beneath shows the dates and total rainfall in mm of these winters. Credit: Chart by Carbon Brief, based on the Met Office HadUK dataset.

The fact that UK winters are getting wetter makes sense, McCarthy tells Carbon Brief, because as the atmosphere heats up, it is able to hold more moisture, which can then fall as rain. According to the Clausius-Clapeyron equation, the air can generally hold around 7% more moisture for every 1C of temperature rise.

However, he adds that the observed trend in UK winter rainfall is “somewhat larger than can be explained purely through the thermodynamic process”, and explains that natural variability is also very important when discussing changes in UK winter rainfall.

“We’re in a particularly wet regime at the moment,” McCarthy explains, “so we are seeing lots of winter rainfall records and wetter winters, but it’s the combination of variability and climate change”.

For example, December 2015 topped the charts as the UK’s wettest month on record, after Storm Desmond swept across the UK, bringing very heavy rainfall and gale-force winds to much of northern England, southern Scotland and Ireland. The resulting floods left many homes inundated and at least 60,000 without power.

The winter of 2015-16 was also the third warmest on record. Preliminary analysis conducted at the time suggested that the exceptional rainfall totals were 40% more likely because of rising global temperatures.

The jet stream

The graph below shows the relationship between temperature and rainfall, where warm and wet winters are shown in the top right, while cool and dry winters are in the bottom left. Darker dots indicate more recent years.

The UK’s winter weather regime is strongly linked to the strength of the jet stream. This thin, fast flowing ribbon of air in the troposphere – the lowest layer of the earth’s atmosphere – acts to steer weather systems towards the UK.

A strong jet stream brings warm and damp winds to the UK from the west, resulting in a warm and wet winter.

For example, the winter of 2023-24 has already been dominated by a series of storms. Storm Jocelyn, which swept across the UK at the end of January 2024, was the 10th named storm of the season. “The storms have mainly been driven by a powerful jet stream,” BBC News reported.

Similarly, during the winter of 2013-14, a series of storms brought record-breaking rainfall to the UK, clocking in as the wettest and eighth-warmest winter on record in the UK. Intense rainfall led to “remarkably widespread and persistent flooding”, according to the Met Office. Around 18,700 insurance claims related to flooding were filed across the UK in the aftermath of the storms, costing an estimated £451m.

One study suggests that climate change made the sustained wet and stormy weather seen around 43% more likely, and put an extra 1,000 houses at risk of flooding along the River Thames.

The study attributes about two-thirds of the increase in likelihood to the atmosphere being able to hold more moisture because the world is warming up and the remaining third to the position of the jet stream.

Conversely, a weak jet stream allows cold air from the Arctic and mainland Europe to enter from the east and north. “A slower, more buckled jet stream can cause areas of higher pressure to take charge, which typically brings less stormy weather, light winds and dry skies,” the Met Office says.

This was the case in the winter of 2009-10, which clocked in as the eighth-coldest and least-windy UK winter on record.

Sometimes, the jet stream can even get “stuck” – a phenomenon called blocking – and instead of shunting weather systems from west to east, it can allow a spell of cold, dry weather to sit over the UK for many days.

While there is a clear trend of UK winters getting warmer and wetter, the data on wind speed is less clear-cut. However, cool weather in the UK is often associated with low speeds, while warm weather is often brought by strong gusts.

The plot below shows average UK winter wind speed over 1969-2021 in knots. The darker line shows the 10-year rolling average, and the most and least windy years are shown by red and blue dots, respectively.

| Windiest winters | Least windy winters | |||

|---|---|---|---|---|

| Years | Average windspeed (knots) | Years | Average windspeed (knots) | |

| 1 | 1973-74 | 13.08 | 2009-10 | 7.90 |

| 2 | 1989-90 | 12.77 | 2010-11 | 8.62 |

| 3 | 1974-75 | 12.72 | 2005-06 | 8.81 |

| 4 | 1994-95 | 12.71 | 2008-09 | 9.03 |

| 5 | 2013-14 | 12.47 | 1984-85 | 9.04 |

| 6 | 1982-83 | 12.41 | 1976-77 | 9.31 |

| 7 | 1980-81 | 12.24 | 2018-19 | 9.32 |

| 8 | 1999-2000 | 12.11 | 2000-01 | 9.54 |

| 9 | 1988-89 | 12.11 | 1986-87 | 9.59 |

| 10 | 2019-20 | 12.08 | 2016-17 | 9.68 |

Windiest and least windy 10 winters in the UK since 1969. The dark blue line shows winter average wind speed, and red and blue dots indicate the windiest and least windy individual winters. The grey dashed lines the average wind speed during the windiest and least windy winters on record. The table beneath shows the dates and wind speeds of these winters. Credit: Chart by Carbon Brief, based on the Met Office HadUK dataset.

The table below shows average UK wind speed totals for three overlapping 30-year time periods.

| 30-year averages | Average wind speed (knots) |

|---|---|

| 1971-2000 | 11.06 |

| 1981-2010 | 10.60 |

| 1991-2020 | 10.55 |

Average winter wind speed for overlapping 30-year time periods, from 1971 to 2020, using the December-February average of mean monthly temperatures.

McCarthy tells Carbon Brief that there has been a notable decline in UK wind speed when looking at annual data, which is consistent with the trend of “stilling” – a slowdown in near surface wind speeds – measured globally. However, he says that this trend is less obvious in the winter-only data.

Meanwhile, the UK State of the Climate report 2022 states that there are no compelling trends in storminess when considering maximum gust speeds over the last four decades.

A range of other atmospheric circulation patterns can also impact UK winters.

The North Atlantic Oscillation (NAO) is a large-scale atmospheric pressure see-saw in the North Atlantic region, which describes the difference in air pressure between the high pressure sitting over the Azores, to the west of Portugal, and the low pressure over Iceland.

When the NAO is “positive” and the pressure difference is stronger than usual, the jet stream shifts towards the poles, bringing mild, wet and windy weather to North American and Eurasian winters and leaving the Arctic very cold.

When it is “negative” and the pressure difference weakens, storm tracks shift towards the equator, bringing cold, dry and calm winters to Europe.

Another mechanism is the “stratospheric polar vortex”. This low-pressure weather system sits around 50km above the Arctic in the stratosphere – the layer of the atmosphere above the troposphere. Its main feature is the strong west-to-east winds which encircle the north pole. These winds are known as the “polar night jet” because they only appear during the dark Arctic winter.

As with the jet stream in the troposphere, the polar night jet forms a boundary between the very cold Arctic air and the warmer air over the mid-latitudes. However, if something disrupts the stratospheric polar vortex it can weaken, reverse direction and even split into two. This can trigger a “sudden stratospheric warming” event where air collapses in over the Arctic, causing a spike in temperatures in the stratosphere – by as much as 50C in just a couple of days.

This allows the cold air the polar vortex was holding in to spill out into the mid-latitudes during the weeks that follow. This is what caused the “Beast from the East” snowstorm that hit the UK in 2018. (This is not well reflected in the UK winter data, as the brunt of the storm hit in March 2018 after the end of meteorological winter.)

In general, however, the UK has experienced a run of mild, wet winters in the most recent decade, including the very wet winters of 2013, 2015 and 2019. These are consistent with a positive phase of the NAO and strong polar vortex, according to the latest State of the UK Climate report.

Projections

As the planet continues to warm, the UK’s climate will shift “towards warmer, wetter winters and hotter, drier summers”, the Met Office says.

The UK Climate Projections 2018 (UKCP18) is a series of climate change projections for the UK produced by the UK Met Office, taking advantage of the latest observed data and climate models

The projections include temperature and rainfall changes – for averages and extremes – for each month and season of the year, and for different emissions scenarios and future time periods throughout this century.

The maps below show the probabilistic projections for summer average temperature (top) and winter precipitation (bottom) in the 2080s under the RCP4.5 emissions pathway, relative to a 1961-90 baseline. In this pathway, global temperatures are projected to rise by around 2.7C of warming above pre-industrial levels by 2081-2100, which is broadly in line with the trajectory under current global policies.

The three percentiles (10th, 50th and 90th) reflect the likelihood of those temperatures and rainfall anomalies occurring. The 50th percentile (middle maps) is the “central estimate” across the models, while the 10th (left) and 90th (right) percentiles reflect the lowest 10% and highest 10% of the model results.

The table below shows UKCP18 projections for changes in average UK winter temperature and precipitation under RCP4.5, under the 10th, 50th and 90th percentile, for 2080-99, compared to a 1981-2000 baseline.

| 10th percentile change | 50th percentile change | 90th percentile change | |

|---|---|---|---|

| Change in average winter temperature (C) | +0.7 | +2.0 | +3.5 |

| Change in average winter precipitation (%) | -2.0 | +11.0 | +25.0 |

Source: UKCP18 Key results spreadsheet

As a central estimate, these projections suggest that by 2080-99, UK winters will be 2C warmer and 11% wetter than they were in 1981-2000.

However, the picture is more complex for wind speed. The Met Office explains that storms in the UK are influenced by factors including sea surface temperatures, Arctic sea ice melt and the jet stream.

It says that “under climate change some of these influences will strengthen storms and others weaken them, as well as potentially change the parts of the world that storms affect”.

It adds:

“UKCP18 projected an increase in near surface wind speeds over the UK for the second half of the 21st century for the winter season when more significant impacts of wind are experienced. However, the increase in wind speeds is modest compared to natural variability from month to month and season to season, so confidence is low.”

The post Analysis: How UK winters are getting warmer and wetter appeared first on Carbon Brief.

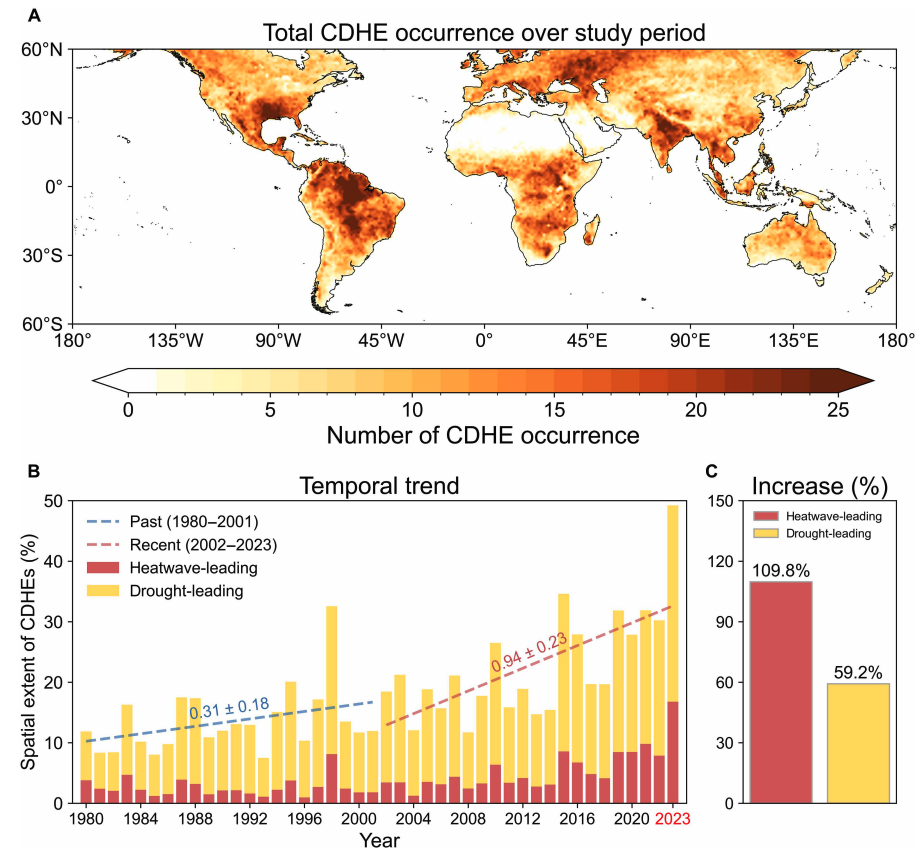

Drought and heatwaves occurring together – known as “compound” events – have “surged” across the world since the early 2000s, a new study shows.

Compound drought and heat events (CDHEs) can have devastating effects, creating the ideal conditions for intense wildfires, such as Australia’s “Black Summer” of 2019-20 where bushfires burned 24m hectares and killed 33 people.

The research, published in Science Advances, finds that the increase in CDHEs is predominantly being driven by events that start with a heatwave.

The global area affected by such “heatwave-led” compound events has more than doubled between 1980-2001 and 2002-23, the study says.

The rapid increase in these events over the last 23 years cannot be explained solely by global warming, the authors note.

Since the late 1990s, feedbacks between the land and the atmosphere have become stronger, making heatwaves more likely to trigger drought conditions, they explain.

One of the study authors tells Carbon Brief that societies must pay greater attention to compound events, which can “cause severe impacts on ecosystems, agriculture and society”.

Compound events

CDHEs are extreme weather events where drought and heatwave conditions occur simultaneously – or shortly after each other – in the same region.

These events are often triggered by large-scale weather patterns, such as “blocking” highs, which can produce “prolonged” hot and dry conditions, according to the study.

Prof Sang-Wook Yeh is one of the study authors and a professor at the Ewha Womans University in South Korea. He tells Carbon Brief:

“When heatwaves and droughts occur together, the two hazards reinforce each other through land-atmosphere interactions. This amplifies surface heating and soil moisture deficits, making compound events more intense and damaging than single hazards.”

CDHEs can begin with either a heatwave or a drought.

The sequence of these extremes is important, the study says, as they have different drivers and impacts.

For example, in a CDHE where the heatwave was the precursor, increased direct sunshine causes more moisture loss from soils and plants, leading to a drought.

Conversely, in an event where the drought was the precursor, the lack of soil moisture means that less of the sun’s energy goes into evaporation and more goes into warming the Earth’s surface. This produces favourable conditions for heatwaves.

The study shows that the majority of CDHEs globally start out as a drought.

In recent years, there has been increasing focus on these events due to the devastating impact they have on agriculture, ecosystems and public health.

In Russia in the summer of 2010, a compound drought-heatwave event – and the associated wildfires – caused the death of nearly 55,000 people, the study notes.

The record-breaking Pacific north-west “heat dome” in 2021 triggered extreme drought conditions that caused “significant declines” in wheat yields, as well as in barley, canola and fruit production in British Columbia and Alberta, Canada, says the study.

Increasing events

To assess how CDHEs are changing, the researchers use daily reanalysis data to identify droughts and heatwaves events. (Reanalysis data combines past observations with climate models to create a historical climate record.) Then, using an algorithm, they analyse how these events overlap in both time and space.

The study covers the period from 1980 to 2023 and the world’s land surface, excluding polar regions where CDHEs are rare.

The research finds that the area of land affected by CDHEs has “increased substantially” since the early 2000s.

Heatwave-led events have been the main contributor to this increase, the study says, with their spatial extent rising 110% between 1980-2001 and 2002-23, compared to a 59% increase for drought-led events.

The map below shows the global distribution of CDHEs over 1980-2023. The charts show the percentage of the land surface affected by a heatwave-led CDHE (red) or a drought-led CDHE (yellow) in a given year (left) and relative increase in each CDHE type (right).

The study finds that CDHEs have occurred most frequently in northern South America, the southern US, eastern Europe, central Africa and south Asia.

Threshold passed

The authors explain that the increase in heatwave-led CDHEs is related to rising global temperatures, but that this does not tell the whole story.

In the earlier 22-year period of 1980-2001, the study finds that the spatial extent of heatwave-led CDHEs rises by 1.6% per 1C of global temperature rise. For the more-recent period of 2022-23, this increases “nearly eightfold” to 13.1%.

The change suggests that the rapid increase in the heatwave-led CDHEs occurred after the global average temperature “surpasse[d] a certain temperature threshold”, the paper says.

This threshold is an absolute global average temperature of 14.3C, the authors estimate (based on an 11-year average), which the world passed around the year 2000.

Investigating the recent surge in heatwave-leading CDHEs further, the researchers find a “regime shift” in land-atmosphere dynamics “toward a persistently intensified state after the late 1990s”.

In other words, the way that drier soils drive higher surface temperatures, and vice versa, is becoming stronger, resulting in more heatwave-led compound events.

Daily data

The research has some advantages over other previous studies, Yeh says. For instance, the new work uses daily estimations of CDHEs, compared to monthly data used in past research. This is “important for capturing the detailed occurrence” of these events, says Yeh.

He adds that another advantage of their study is that it distinguishes the sequence of droughts and heatwaves, which allows them to “better understand the differences” in the characteristics of CDHEs.

Dr Meryem Tanarhte is a climate scientist at the University Hassan II in Morocco, and Dr Ruth Cerezo Mota is a climatologist and a researcher at the National Autonomous University of Mexico. Both scientists, who were not involved in the study, agree that the daily estimations give a clearer picture of how CDHEs are changing.

Cerezo-Mota adds that another major contribution of the study is its global focus. She tells Carbon Brief that in some regions, such as Mexico and Africa, there is a lack of studies on CDHEs:

“Not because the events do not occur, but perhaps because [these regions] do not have all the data or the expertise to do so.”

However, she notes that the reanalysis data used by the study does have limitations with how it represents rainfall in some parts of the world.

Compound impacts

The study notes that if CDHEs continue to intensify – particularly events where heatwaves are the precursors – they could drive declining crop productivity, increased wildfire frequency and severe public health crises.

These impacts could be “much more rapid and severe as global warming continues”, Yeh tells Carbon Brief.

Tanarhte notes that these events can be forecasted up to 10 days ahead in many regions. Furthermore, she says, the strongest impacts can be prevented “through preparedness and adaptation”, including through “water management for agriculture, heatwave mitigation measures and wildfire mitigation”.

The study recommends reassessing current risk management strategies for these compound events. It also suggests incorporating the sequences of drought and heatwaves into compound event analysis frameworks “to enhance climate risk management”.

Cerezo-Mota says that it is clear that the world needs to be prepared for the increased occurrence of these events. She tells Carbon Brief:

“These [risk assessments and strategies] need to be carried out at the local level to understand the complexities of each region.”

The post Heatwaves driving recent ‘surge’ in compound drought and heat extremes appeared first on Carbon Brief.

Heatwaves driving recent ‘surge’ in compound drought and heat extremes

Greenhouse Gases

DeBriefed 6 March 2026: Iran energy crisis | China climate plan | Bristol’s ‘pioneering’ wind turbine

Welcome to Carbon Brief’s DeBriefed.

An essential guide to the week’s key developments relating to climate change.

This week

Energy crisis

ENERGY SPIKE: US-Israeli attacks on Iran and subsequent counterattacks across the Middle East have sent energy prices “soaring”, according to Reuters. The newswire reported that the region “accounts for just under a third of global oil production and almost a fifth of gas”. The Guardian noted that shipping traffic through the strait of Hormuz, which normally ferries 20% of the world’s oil, “all but ground to a halt”. The Financial Times reported that attacks by Iran on Middle East energy facilities – notably in Qatar – triggered the “biggest rise in gas prices since Russia’s full-scale invasion of Ukraine”.

‘RISK’ AND ‘BENEFITS’: Bloomberg reported on increases in diesel prices in Europe and the US, speculating that rising fuel costs could be “a risk for president Donald Trump”. US gas producers are “poised to benefit from the big disruption in global supply”, according to CNBC. Indian government sources told the Economic Times that Russia is prepared to “fulfil India’s energy demands”. China Daily quoted experts who said “China’s energy security remains fundamentally unshaken”, thanks to “emergency stockpiles and a wide array of import channels”.

‘ESSENTIAL’ RENEWABLES: Energy analysts said governments should cut their fossil-fuel reliance by investing in renewables, “rather than just seeking non-Gulf oil and gas suppliers”, reported Climate Home News. This message was echoed by UK business secretary Peter Kyle, who said “doubling down on renewables” was “essential” amid “regional instability”, according to the Daily Telegraph.

China’s climate plan

PEAK COAL?: China has set out its next “five-year plan” at the annual “two sessions” meeting of the National People’s Congress, including its climate strategy out to 2030, according to the Hong Kong-based South China Morning Post. The plan called for China to cut its carbon emissions per unit of gross domestic product (GDP) by 17% from 2026 to 2030, which “may allow for continued increase in emissions given the rate of GDP growth”, reported Reuters. The newswire added that the plan also had targets to reach peak coal in the next five years and replace 30m tonnes per year of coal with renewables.

ACTIVE YET PRUDENT: Bloomberg described the new plan as “cautious”, stating that it “frustrat[es] hopes for tighter policy that would drive the nation to peak carbon emissions well before president Xi Jinping’s 2030 deadline”. Carbon Brief has just published an in-depth analysis of the plan. China Daily reported that the strategy “highlights measures to promote the climate targets of peaking carbon dioxide emissions before 2030”, which China said it would work towards “actively yet prudently”.

Around the world

- EU RULES: The European Commission has proposed new “made in Europe” rules to support domestic low-carbon industries, “against fierce competition from China”, reported Agence France-Presse. Carbon Brief examined what it means for climate efforts.

- RECORD HEAT: The US National Oceanic and Atmospheric Administration has said there is a 50-60% chance that the El Niño weather pattern could return this year, amplifying the effect of global warming and potentially driving temperatures to “record highs”, according to Euronews.

- FLAGSHIP FUND: The African Development Bank’s “flagship clean energy fund” plans to more than double its financing to $2.5bn for African renewables over the next two years, reported the Associated Press.

- NO WITHDRAWAL: Vanuatu has defied US efforts to force the Pacific-island nation to drop a UN draft resolution calling on the world to implement a landmark International Court of Justice (ICJ) ruling on climate, according to the Guardian.

98

The number of nations that submitted their national reports on tackling nature loss to the UN on time – just half of the 196 countries that are part of the UN biodiversity treaty – according to analysis by Carbon Brief.

Latest climate research

- Sea levels are already “much higher than assumed” in most assessments of the threat posed by sea-level rise, due to “inadequate” modelling assumptions | Nature

- Accelerating human-caused global warming could see the Paris Agreement’s 1.5C limit crossed before 2030 | Geophysical Research Letters covered by Carbon Brief

- Future “super El Niño events” could “significantly lower” solar power generation due to a reduction in solar irradiance in key regions, such as California and east China | Communications Earth & Environment

(For more, see Carbon Brief’s in-depth daily summaries of the top climate news stories on Monday, Tuesday, Wednesday, Thursday and Friday.)

Captured

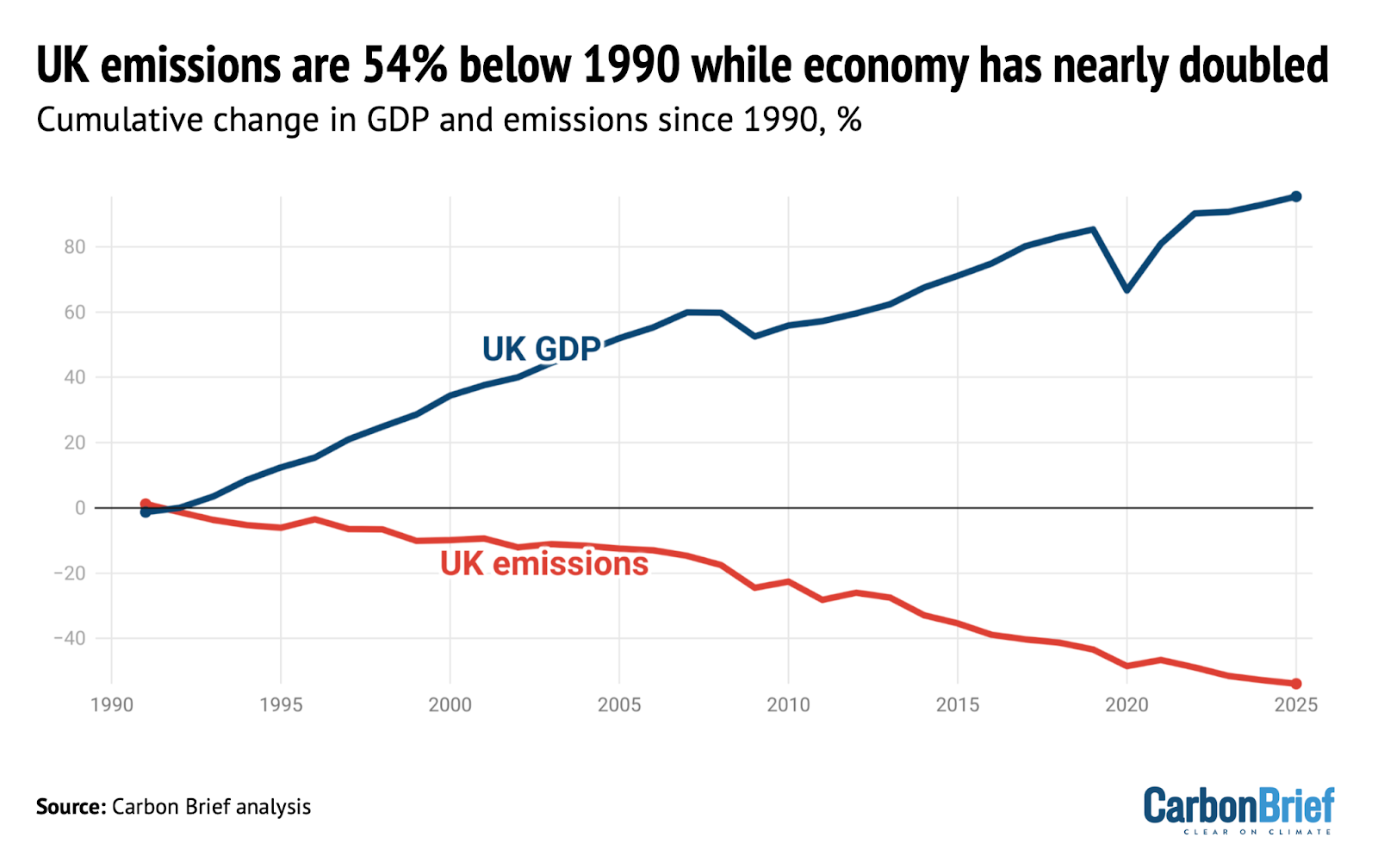

UK greenhouse gas emissions in 2025 fell to 54% below 1990 levels, the baseline year for its legally binding climate goals, according to new Carbon Brief analysis. Over the same period, data from the World Bank shows that the UK’s economy has expanded by 95%, meaning that emissions have been decoupling from growth.

Spotlight

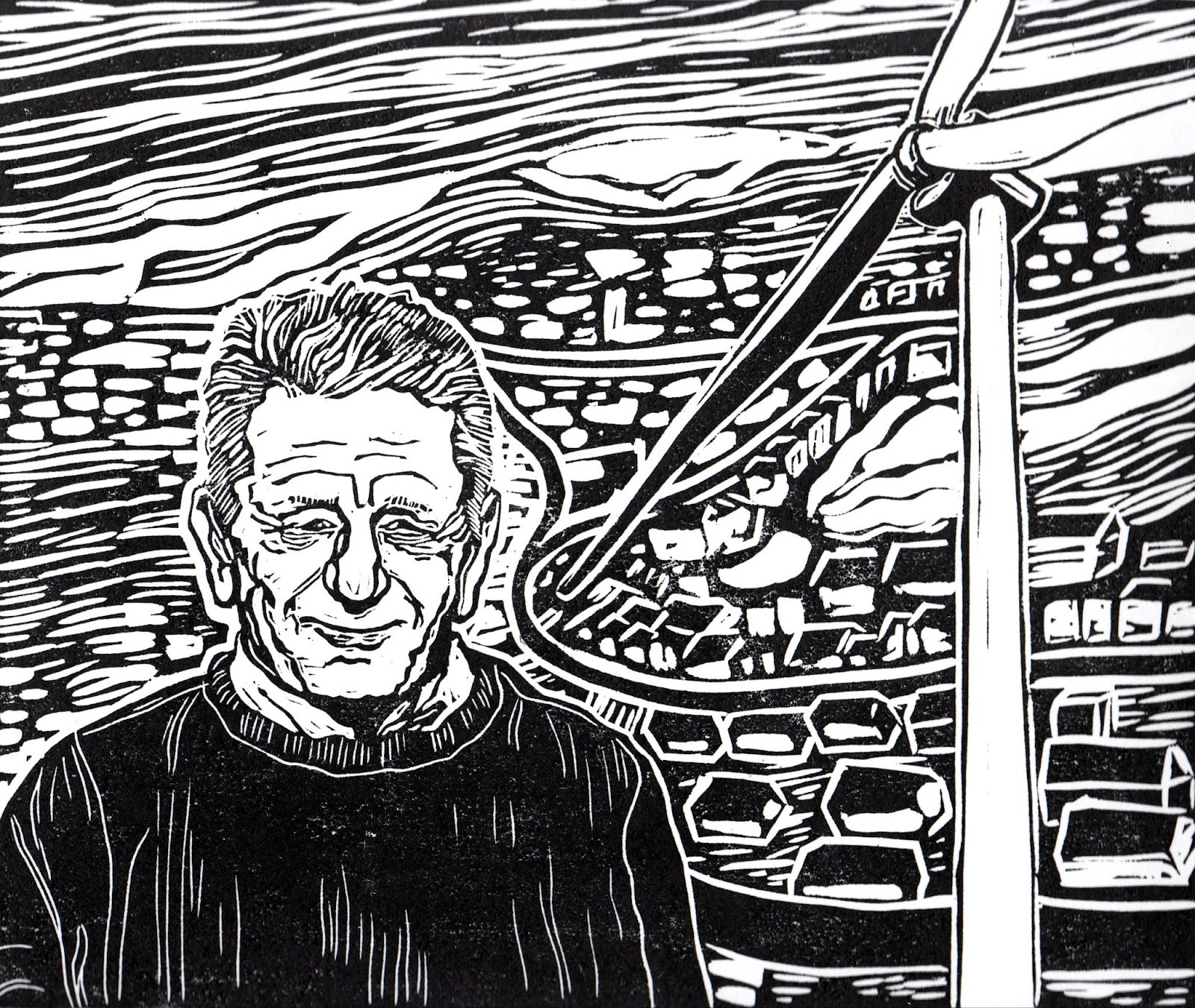

Bristol’s ‘pioneering’ community wind turbine

Following the recent launch of the UK government’s local power plan, Carbon Brief visits one of the country’s community-energy success stories.

The Lawrence Weston housing estate is set apart from the main city of Bristol, wedged between the tree-lined grounds of a stately home and a sprawl of warehouses and waste incinerators. It is one of the most deprived areas in the city.

Yet, just across the M5 motorway stands a structure that has brought the spoils of the energy transition directly to this historically forgotten estate – a 4.2 megawatt (MW) wind turbine.

The turbine is owned by local charity Ambition Lawrence Weston and all the profits from its electricity sales – around £100,000 a year – go to the community. In the UK’s local power plan, it was singled out by energy secretary Ed Miliband as a “pioneering” project.

‘Sustainable income’

On a recent visit to the estate by Carbon Brief, Ambition Lawrence Weston’s development manager, Mark Pepper, rattled off the story behind the wind turbine.

In 2012, Pepper and his team were approached by the Bristol Energy Cooperative with a chance to get a slice of the income from a new solar farm. They jumped at the opportunity.

“Austerity measures were kicking in at the time,” Pepper told Carbon Brief. “We needed to generate an income. Our own, sustainable income.”

With the solar farm proving to be a success, the team started to explore other opportunities. This began a decade-long process that saw them navigate the Conservative government’s “ban” on onshore wind, raise £5.5m in funding and, ultimately, erect the turbine in 2023.

Today, the turbine generates electricity equivalent to Lawrence Weston’s 3,000 households and will save 87,600 tonnes of carbon dioxide (CO2) over its lifetime.

‘Climate by stealth’

Ambition Lawrence Weston’s hub is at the heart of the estate and the list of activities on offer is seemingly endless: birthday parties, kickboxing, a library, woodworking, help with employment and even a pop-up veterinary clinic. All supported, Pepper said, with the help of a steady income from community-owned energy.

The centre itself is kitted out with solar panels, heat pumps and electric-vehicle charging points, making it a living advertisement for the net-zero transition. Pepper noted that the organisation has also helped people with energy costs amid surging global gas prices.

Gesturing to the England flags dangling limply on lamp posts visible from the kitchen window, he said:

“There’s a bit of resentment around immigration and scarcity of materials and provision, so we’re trying to do our bit around community cohesion.”

This includes supper clubs and an interfaith grand iftar during the Muslim holy month of Ramadan.

Anti-immigration sentiment in the UK has often gone hand-in-hand with opposition to climate action. Right-wing politicians and media outlets promote the idea that net-zero policies will cost people a lot of money – and these ideas have cut through with the public.

Pepper told Carbon Brief he is sympathetic to people’s worries about costs and stressed that community energy is the perfect way to win people over:

“I think the only way you can change that is if, instead of being passive consumers…communities are like us and they’re generating an income to offset that.”

From the outset, Pepper stressed that “we weren’t that concerned about climate because we had other, bigger pressures”, adding:

“But, in time, we’ve delivered climate by stealth.”

Watch, read, listen

OIL WATCH: The Guardian has published a “visual guide” with charts and videos showing how the “escalating Iran conflict is driving up oil and gas prices”.

MURDER IN HONDURAS: Ten years on from the murder of Indigenous environmental justice advocate Berta Cáceres, Drilled asked why Honduras is still so dangerous for environmental activists.

TALKING WEATHER: A new film, narrated by actor Michael Sheen and titled You Told Us To Talk About the Weather, aimed to promote conversation about climate change with a blend of “poetry, folk horror and climate storytelling”.

Coming up

- 8 March: Colombia parliamentary election

- 9-19 March: 31st Annual Session of the International Seabed Authority, Kingston, Jamaica

- 11 March: UN Environment Programme state of finance for nature 2026 report launch

Pick of the jobs

- London School of Economics and Political Science, fellow in the social science of sustainability | Salary: £43,277-£51,714. Location: London

- NORCAP, innovative climate finance expert | Salary: Unknown. Location: Kyiv, Ukraine

- WBHM, environmental reporter | Salary: $50,050-$81,330. Location: Birmingham, Alabama, US

- Climate Cabinet, data engineer | Salary: hourly rate of $60-$120 per hour. Location: Remote anywhere in the US

DeBriefed is edited by Daisy Dunne. Please send any tips or feedback to debriefed@carbonbrief.org.

This is an online version of Carbon Brief’s weekly DeBriefed email newsletter. Subscribe for free here.

The post DeBriefed 6 March 2026: Iran energy crisis | China climate plan | Bristol’s ‘pioneering’ wind turbine appeared first on Carbon Brief.

China’s leadership has published a draft of its 15th five-year plan setting the strategic direction for the nation out to 2030, including support for clean energy and energy security.

The plan sets a target to cut China’s “carbon intensity” by 17% over the five years from 2026-30, but also changes the basis for calculating this key climate metric.

The plan continues to signal support for China’s clean-energy buildout and, in general, contains no major departures from the country’s current approach to the energy transition.

The government reaffirms support for several clean-energy industries, ranging from solar and electric vehicles (EVs) through to hydrogen and “new-energy” storage.

The plan also emphasises China’s willingness to steer climate governance and be seen as a provider of “global public goods”, in the form of affordable clean-energy technologies.

However, while the document says it will “promote the peaking” of coal and oil use, it does not set out a timeline and continues to call for the “clean and efficient” use of coal.

This shows that tensions remain between China’s climate goals and its focus on energy security, leading some analysts to raise concerns about its carbon-cutting ambition.

Below, Carbon Brief outlines the key climate change and energy aspects of the plan, including targets for carbon intensity, non-fossil energy and forestry.

Note: this article is based on a draft published on 5 March and will be updated if any significant changes are made in the final version of the plan, due to be released at the close next week of the “two sessions” meeting taking place in Beijing.

- What is China’s 15th five-year plan?

- What does the plan say about China’s climate action?

- What is China’s new CO2 intensity target?

- Does the plan encourage further clean-energy additions?

- What does the plan signal about coal?

- How will China approach global climate governance in the next five years?

- What else does the plan cover?

What is China’s 15th five-year plan?

Five-year plans are one of the most important documents in China’s political system.

Addressing everything from economic strategy to climate policy, they outline the planned direction for China’s socio-economic development in a five-year period. The 15th five-year plan covers 2026-30.

These plans include several “main goals”. These are largely quantitative indicators that are seen as particularly important to achieve and which provide a foundation for subsequent policies during the five-year period.

The table below outlines some of the key “main goals” from the draft 15th five-year plan.

| Category | Indicator | Indicator in 2025 | Target by 2030 | Cumulative target over 2026-2030 | Characteristic |

|---|---|---|---|---|---|

| Economic development | Gross domestic product (GDP) growth (%) | 5 | Maintained within a reasonable range and proposed annually as appropriate. | Anticipatory | |

| ‘Green and low-carbon | Reduction in CO2 emissions per unit of GDP (%) | 17.7 | 17 | Binding | |

| Share of non-fossil energy in total energy consumption (%) | 21.7 | 25 | Binding | ||

| Security guarantee | Comprehensive energy production capacity (100m tonnes of standard coal equivalent) |

51.3 | 58 | Binding |

Select list of targets highlighted in the “main goals” section of the draft 15th five-year plan. Source: Draft 15th five-year plan.

Since the 12th five-year plan, covering 2011-2015, these “main goals” have included energy intensity and carbon intensity as two of five key indicators for “green ecology”.

The previous five-year plan, which ran from 2021-2025, introduced the idea of an absolute “cap” on carbon dioxide (CO2) emissions, although it did not provide an explicit figure in the document. This has been subsequently addressed by a policy on the “dual-control of carbon” issued in 2024.

The latest plan removes the energy-intensity goal and elevates the carbon-intensity goal, but does not set an absolute cap on emissions (see below).

It covers the years until 2030, before which China has pledged to peak its carbon emissions. (Analysis for Carbon Brief found that emissions have been “flat or falling” since March 2024.)

The plans are released at the two sessions, an annual gathering of the National People’s Congress (NPC) and the Chinese People’s Political Consultative Conference (CPPCC). This year, it runs from 4-12 March.

The plans are often relatively high-level, with subsequent topic-specific five-year plans providing more concrete policy guidance.

Policymakers at the National Energy Agency (NEA) have indicated that in the coming years they will release five sector-specific plans for 2026-2030, covering topics such as the “new energy system”, electricity and renewable energy.

There may also be specific five-year plans covering carbon emissions and environmental protection, as well as the coal and nuclear sectors, according to analysts.

Other documents published during the two sessions include an annual government work report, which outlines key targets and policies for the year ahead.

The gathering is attended by thousands of deputies – delegates from across central and local governments, as well as Chinese Communist party members, members of other political parties, academics, industry leaders and other prominent figures.

What does the plan say about China’s climate action?

Achieving China’s climate targets will remain a key driver of the country’s policies in the next five years, according to the draft 15th five-year plan.

It lists the “acceleration” of China’s energy transition as a “major achievement” in the 14th five-year plan period (2021-2025), noting especially how clean-power capacity had overtaken fossil fuels.

The draft says China will “actively and steadily advance and achieve carbon peaking”, with policymakers continuing to strike a balance between building a “green economy” and ensuring stability.

Climate and environment continues to receive its own chapter in the plan. However, the framing and content of this chapter has shifted subtly compared with previous editions, as shown in the table below. For example, unlike previous plans, the first section of this chapter focuses on China’s goal to peak emissions.

| 11th five-year plan (2006-2010) | 12th five-year plan (2011-2015) | 13th five-year plan (2016-2020) | 14th five-year plan (2021-2025) | 15th five-year plan (2026-2030) | |

|---|---|---|---|---|---|

| Chapter title | Part 6: Build a resource-efficient and environmentally-friendly society | Part 6: Green development, building a resource-efficient and environmentally friendly society | Part 10: Ecosystems and the environment | Part 11: Promote green development and facilitate the harmonious coexistence of people and nature | Part 13: Accelerating the comprehensive green transformation of economic and social development to build a beautiful China |

| Sections | Developing a circular economy | Actively respond to global climate change | Accelerate the development of functional zones | Improve the quality and stability of ecosystems | Actively and steadily advancing and achieving carbon peaking |

| Protecting and restoring natural ecosystems | Strengthen resource conservation and management | Promote economical and intensive resource use | Continue to improve environmental quality | Continuously improving environmental quality | |

| Strengthening environmental protection | Vigorously develop the circular economy | Step up comprehensive environmental governance | Accelerate the green transformation of the development model | Enhancing the diversity, stability, and sustainability of ecosystems | |

| Enhancing resource management | Strengthen environmental protection efforts | Intensify ecological conservation and restoration | Accelerating the formation of green production and lifestyles | ||

| Rational utilisation of marine and climate resources | Promoting ecological conservation and restoration | Respond to global climate change | |||

| Strengthen the development of water conservancy and disaster prevention and mitigation systems | Improve mechanisms for ensuring ecological security | ||||

| Develop green and environmentally-friendly industries |

Title and main sections of the climate and environment-focused chapters in the last five five-year plans. Source: China’s 11th, 12th, 13th, 14th and 15th five-year plans.

The climate and environment chapter in the latest plan calls for China to “balance [economic] development and emission reduction” and “ensure the timely achievement of carbon peak targets”.

Under the plan, China will “continue to pursue” its established direction and objectives on climate, Prof Li Zheng, dean of the Tsinghua University Institute of Climate Change and Sustainable Development (ICCSD), tells Carbon Brief.

What is China’s new CO2 intensity target?

In the lead-up to the release of the plan, analysts were keenly watching for signals around China’s adoption of a system for the “dual-control of carbon”.

This would combine the existing targets for carbon intensity – the CO2 emissions per unit of GDP – with a new cap on China’s total carbon emissions. This would mark a dramatic step for the country, which has never before set itself a binding cap on total emissions.

Policymakers had said last year that this framework would come into effect during the 15th five-year plan period, replacing the previous system for the “dual-control of energy”.

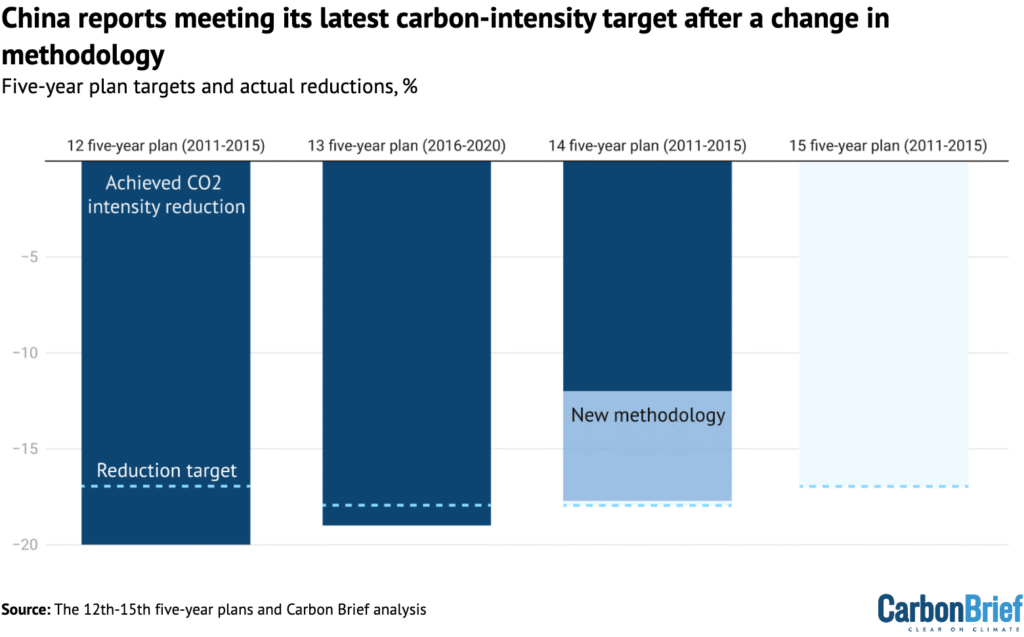

However, the draft 15th five-year plan does not offer further details on when or how both parts of the dual-control of carbon system will be implemented. Instead, it continues to focus on carbon intensity targets alone.

Looking back at the previous five-year plan period, the latest document says China had achieved a carbon-intensity reduction of 17.7%, just shy of its 18% goal.

This is in contrast with calculations by Lauri Myllyvirta, lead analyst at the Centre for Research on Energy and Clean Air (CREA), which had suggested that China had only cut its carbon intensity by 12% over the past five years.

At the time it was set in 2021, the 18% target had been seen as achievable, with analysts telling Carbon Brief that they expected China to realise reductions of 20% or more.

However, the government had fallen behind on meeting the target.

Last year, ecology and environment minister Huang Runqiu attributed this to the Covid-19 pandemic, extreme weather and trade tensions. He said that China, nevertheless, remained “broadly” on track to meet its 2030 international climate pledge of reducing carbon intensity by more than 65% from 2005 levels.

Myllyvirta tells Carbon Brief that the newly reported figure showing a carbon-intensity reduction of 17.7% is likely due to an “opportunistic” methodological revision. The new methodology now includes industrial process emissions – such as cement and chemicals – as well as the energy sector.

(This is not the first time China has redefined a target, with regulators changing the methodology for energy intensity in 2023.)

For the next five years, the plan sets a target to reduce carbon intensity by 17%, slightly below the previous goal.

However, the change in methodology means that this leaves space for China’s overall emissions to rise by “3-6% over the next five years”, says Myllyvirta. In contrast, he adds that the original methodology would have required a 2% fall in absolute carbon emissions by 2030.

The dashed lines in the chart below show China’s targets for reducing carbon intensity during the 12th, 13th, 14th and 15th five-year periods, while the bars show what was achieved under the old (dark blue) and new (light blue) methodology.

The carbon-intensity target is the “clearest signal of Beijing’s climate ambition”, says Li Shuo, director at the Asia Society Policy Institute’s (ASPI) China climate hub.

It also links directly to China’s international pledge – made in 2021 – to cut its carbon intensity to more than 65% below 2005 levels by 2030.

To meet this pledge under the original carbon-intensity methodology, China would have needed to set a target of a 23% reduction within the 15th five-year plan period. However, the country’s more recent 2035 international climate pledge, released last year, did not include a carbon-intensity target.

As such, ASPI’s Li interprets the carbon-intensity target in the draft 15th five-year plan as a “quiet recalibration” that signals “how difficult the original 2030 goal has become”.

Furthermore, the 15th five-year plan does not set an absolute emissions cap.

This leaves “significant ambiguity” over China’s climate plans, says campaign group 350 in a press statement reacting to the draft plan. It explains:

“The plan was widely expected to mark a clearer transition from carbon-intensity targets toward absolute emissions reductions…[but instead] leaves significant ambiguity about how China will translate record renewable deployment into sustained emissions cuts.”

Myllyvirta tells Carbon Brief that this represents a “continuation” of the government’s focus on scaling up clean-energy supply while avoiding setting “strong measurable emission targets”.

He says that he would still expect to see absolute caps being set for power and industrial sectors covered by China’s emissions trading scheme (ETS). In addition, he thinks that an overall absolute emissions cap may still be published later in the five-year period.

Despite the fact that it has yet to be fully implemented, the switch from dual-control of energy to dual-control of carbon represents a “major policy evolution”, Ma Jun, director of the Institute of Public and Environmental Affairs (IPE), tells Carbon Brief. He says that it will allow China to “provide more flexibility for renewable energy expansion while tightening the net on fossil-fuel reliance”.

Does the plan encourage further clean-energy additions?

“How quickly carbon intensity is reduced largely depends on how much renewable energy can be supplied,” says Yao Zhe, global policy advisor at Greenpeace East Asia, in a statement.

The five-year plan continues to call for China’s development of a “new energy system that is clean, low-carbon, safe and efficient” by 2030, with continued additions of “wind, solar, hydro and nuclear power”.

In line with China’s international pledge, it sets a target for raising the share of non-fossil energy in total energy consumption to 25% by 2030, up from just under 21.7% in 2025.

The development of “green factories” and “zero-carbon [industrial] parks” has been central to many local governments’ strategies for meeting the non-fossil energy target, according to industry news outlet BJX News. A call to build more of these zero-carbon industrial parks is listed in the five-year plan.

Prof Pan Jiahua, dean of Beijing University of Technology’s Institute of Ecological Civilization, tells Carbon Brief that expanding demand for clean energy through mechanisms such as “green factories” represents an increasingly “bottom-up” and “market-oriented” approach to the energy transition, which will leave “no place for fossil fuels”.

He adds that he is “very much sure that China’s zero-carbon process is being accelerated and fossil fuels are being driven out of the market”, pointing to the rapid adoption of EVs.

The plan says that China will aim to double “non-fossil energy” in 10 years – although it does not clarify whether this means their installed capacity or electricity generation, or what the exact starting year would be.

Research has shown that doubling wind and solar capacity in China between 2025-2035 would be “consistent” with aims to limit global warming to 2C.

While the language “certainly” pushes for greater additions of renewable energy, Yao tells Carbon Brief, it is too “opaque” to be a “direct indication” of the government’s plans for renewable additions.

She adds that “grid stability and healthy, orderly competition” is a higher priority for policymakers than guaranteeing a certain level of capacity additions.

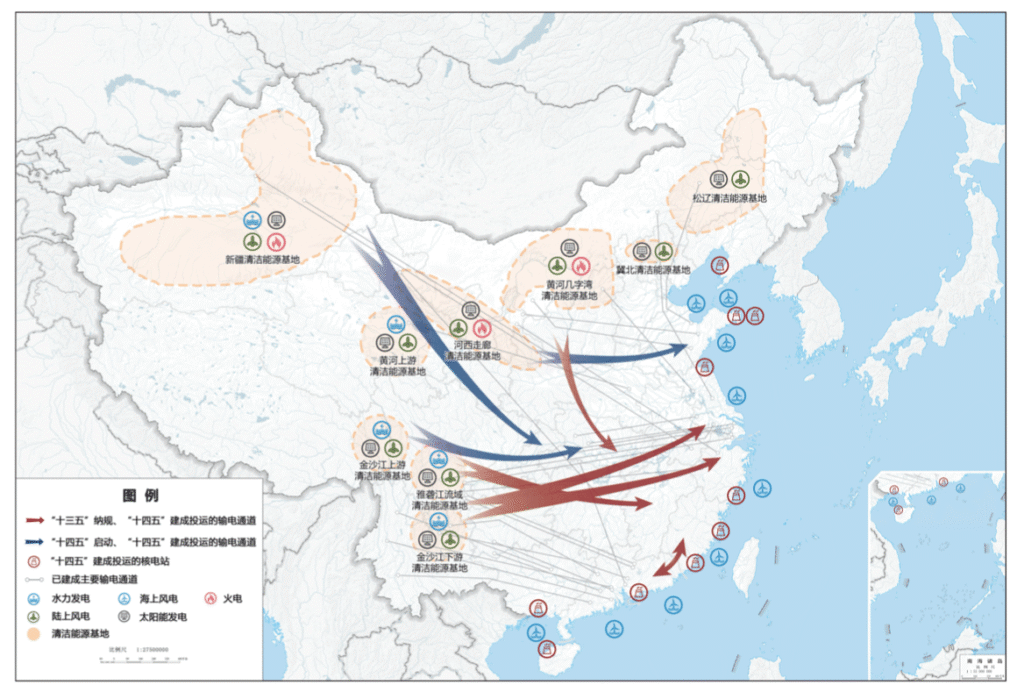

China continues to place emphasis on the need for large-scale clean-energy “bases” and cross-regional power transmission.

The plan says China must develop “clean-energy bases…in the three northern regions” and “integrated hydro-wind-solar complexes” in south-west China.

It specifically encourages construction of “large-scale wind and solar” power bases in desert regions “primarily” for cross-regional power transmission, as well as “major hydropower” projects, including the Yarlung Tsangpo dam in Tibet.

As such, the country should construct “power-transmission corridors” with the capacity to send 420 gigawatts (GW) of electricity from clean-energy bases in western provinces to energy-hungry eastern provinces by 2030, the plan says.

State Grid, China’s largest grid operator, plans to install “another 15 ultra-high voltage [UHV] transmission lines” by 2030, reports Reuters, up from the 45 UHV lines built by last year.

Below are two maps illustrating the interlinkages between clean-energy bases in China in the 15th (top) and 14th (bottom) five-year plan periods.

The yellow dotted areas represent clean energy bases, while the arrows represent cross-regional power transmission. The blue wind-turbine icons represent offshore windfarms and the red cooling tower icons represent coastal nuclear plants.

The 15th five-year plan map shows a consistent approach to the 2021-2025 period. As well as power being transmitted from west to east, China plans for more power to be sent to southern provinces from clean-energy bases in the north-west, while clean-energy bases in the north-east supply China’s eastern coast.

It also maps out “mutual assistance” schemes for power grids in neighbouring provinces.

Offshore wind power should reach 100GW by 2030, while nuclear power should rise to 110GW, according to the plan.

What does the plan signal about coal?

The increased emphasis on grid infrastructure in the draft 15th five-year plan reflects growing concerns from energy planning officials around ensuring China’s energy supply.

Ren Yuzhi, director of the NEA’s development and planning department, wrote ahead of the plan’s release that the “continuous expansion” of China’s energy system has “dramatically increased its complexity”.

He said the NEA felt there was an “urgent need” to enhance the “secure and reliable” replacement of fossil-fuel power with new energy sources, as well as to ensure the system’s “ability to absorb them”.

Meanwhile, broader concerns around energy security have heightened calls for coal capacity to remain in the system as a “ballast stone”.

The plan continues to support the “clean and efficient utilisation of fossil fuels” and does not mention either a cap or peaking timeline for coal consumption.

Xi had previously told fellow world leaders that China would “strictly control” coal-fired power and phase down coal consumption in the 15th five-year plan period.

The “geopolitical situation is increasing energy security concerns” at all levels of government, said the Institute for Global Decarbonization Progress in a note responding to the draft plan, adding that this was creating “uncertainty over coal reduction”.

Ahead of its publication, there were questions around whether the plan would set a peaking deadline for oil and coal. An article posted by state news agency Xinhua last month, examining recommendations for the plan from top policymakers, stated that coal consumption would plateau from “around 2027”, while oil would peak “around 2026”.

However, the plan does not lay out exact years by which the two fossil fuels should peak, only saying that China will “promote the peaking of coal and oil consumption”.

There are similarly no mentions of phasing out coal in general, in line with existing policy.

Nevertheless, there is a heavy emphasis on retrofitting coal-fired power plants. The plan calls for the establishment of “demonstration projects” for coal-plant retrofitting, such as through co-firing with biomass or “green ammonia”.

Such retrofitting could incentivise lower utilisation of coal plants – and thus lower emissions – if they are used to flexibly meet peaks in demand and to cover gaps in clean-energy output, instead of providing a steady and significant share of generation.

The plan also calls for officials to “fully implement low-carbon retrofitting projects for coal-chemical industries”, which have been a notable source of emissions growth in the past year.

However, the coal-chemicals sector will likely remain a key source of demand for China’s coal mining industry, with coal-to-oil and coal-to-gas bases listed as a “key area” for enhancing the country’s “security capabilities”.

Meanwhile, coal-fired boilers and industrial kilns in the paper industry, food processing and textiles should be replaced with “clean” alternatives to the equivalent of 30m tonnes of coal consumption per year, it says.

“China continues to scale up clean energy at an extraordinary pace, but the plan still avoids committing to strong measurable constraints on emissions or fossil fuel use”, says Joseph Dellatte, head of energy and climate studies at the Institut Montaigne. He adds:

“The logic remains supply-driven: deploy massive amounts of clean energy and assume emissions will eventually decline.”

How will China approach global climate governance in the next five years?

Meanwhile, clean-energy technologies continue to play a role in upgrading China’s economy, with several “new energy” sectors listed as key to its industrial policy.

Named sectors include smart EVs, “new solar cells”, new-energy storage, hydrogen and nuclear fusion energy.

“China’s clean-technology development – rather than traditional administrative climate controls – is increasingly becoming the primary driver of emissions reduction,” says ASPI’s Li. He adds that strengthening China’s clean-energy sectors means “more closely aligning Beijing’s economic ambitions with its climate objectives”.

Analysis for Carbon Brief shows that clean energy drove more than a third of China’s GDP growth in 2025, representing around 11% of China’s whole economy.

The continued support for these sectors in the draft five-year plan comes as the EU outlined its own measures intended to limit China’s hold on clean-energy industries, driven by accusations of “unfair competition” from Chinese firms.

China is unlikely to crack down on clean-tech production capacity, Dr Rebecca Nadin, director of the Centre for Geopolitics of Change at ODI Global, tells Carbon Brief. She says:

“Beijing is treating overcapacity in solar and smart EVs as a strategic choice, not a policy error…and is prepared to pour investment into these sectors to cement global market share, jobs and technological leverage.”

Dellatte echoes these comments, noting that it is “striking” that the plan “barely addresses the issue of industrial overcapacity in clean technologies”, with the focus firmly on “scaling production and deployment”.

At the same time, China is actively positioning itself to be a prominent voice in climate diplomacy and a champion of proactive climate action.

This is clear from the first line in a section on providing “global public goods”. It says:

“As a responsible major country, China will play a more active role in addressing global challenges such as climate change.”

The plan notes that China will “actively participate in and steer [引领] global climate governance”, in line with the principle of “common,but differentiated responsibilities”.

This echoes similar language from last year’s government work report, Yao tells Carbon Brief, demonstrating a “clear willingness” to guide global negotiations. But she notes that this “remains an aspiration that’s yet to be made concrete”. She adds:

“China has always favored collective leadership, so its vision of leadership is never a lone one.”

The country will “deepen south-south cooperation on climate change”, the plan says. In an earlier section on “opening up”, it also notes that China will explore “new avenues for collaboration in green development” with global partners as part of its “Belt and Road Initiative”.

China is “doubling down” on a narrative that it is a “responsible major power” and “champion of south-south climate cooperation”, Nadin says, such as by “presenting its clean‑tech exports and finance as global public goods”. She says:

“China will arrive at future COPs casting itself as the indispensable climate leader for the global south…even though its new five‑year plan still puts growth, energy security and coal ahead of faster emissions cuts at home.”

What else does the plan cover?

The impact of extreme weather – particularly floods – remains a key concern in the plan.

China must “refine” its climate adaptation framework and “enhance its resilience to climate change, particularly extreme-weather events”, it says.

China also aims to “strengthen construction of a national water network” over the next five years in order to help prevent floods and droughts.

An article published a few days before the plan in the state-run newspaper China Daily noted that, “as global warming intensifies, extreme weather events – including torrential rains, severe convective storms, and typhoons – have become more frequent, widespread and severe”.

The plan also touches on critical minerals used for low-carbon technologies. These will likely remain a geopolitical flashpoint, with China saying it will focus during the next five years on “intensifying” exploration and “establishing” a reserve for critical minerals. This reserve will focus on “scarce” energy minerals and critical minerals, as well as other “advantageous mineral resources”.

Dellatte says that this could mean the “competition in the energy transition will increasingly be about control over mineral supply chains”.

Other low-carbon policies listed in the five-year plan include expanding coverage of China’s mandatory carbon market and further developing its voluntary carbon market.

China will “strengthen monitoring and control” of non-CO2 greenhouse gases, the plan says, as well as implementing projects “targeting methane, nitrous oxide and hydrofluorocarbons” in sectors such as coal mining, agriculture and chemicals.

This will create “capacity” for reducing emissions by 30m tonnes of CO2 equivalent, it adds.

Meanwhile, China will develop rules for carbon footprint accounting and push for internationally recognised accounting standards.

It will enhance reform of power markets over the next five years and improve the trading mechanism for green electricity certificates.

It will also “promote” adoption of low-carbon lifestyles and decarbonisation of transport, as well as working to advance electrification of freight and shipping.

The post Q&A: What does China’s 15th ‘five-year plan’ mean for climate change? appeared first on Carbon Brief.

Q&A: What does China’s 15th ‘five-year plan’ mean for climate change?

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits