Disseminated on behalf of Sierra Madre Gold & Silver Ltd.

Mexico has been a cornerstone of global silver and gold production for centuries, with historic mining regions such as Zacatecas, Durango, and the Sierra Madre belt supplying the world with these precious metals. Mining represents nearly 2.5% of Mexico’s GDP and produces significant export revenue.

However, decades of underinvestment and declining output from aging mines led to a slowdown in production growth. Today, a new wave of modern mining companies is reinvigorating Mexico’s silver and gold industry, bringing capital, modern technology, and strict environmental practices to historic mining regions.

Among these companies, Sierra Madre Gold & Silver Ltd. (TSXV: SM | OTCQX: SMDRF) is emerging as a standout player, spearheading the revival of Mexico’s rich Temascaltepec district with its La Guitarra Mine.

Mexico’s Silver and Gold Renaissance: Strategic Importance

Mexico remains the world’s largest silver producer, contributing roughly 23–25% of global output in 2024, with total production between 5,800 and 6,300 tonnes. The surge in industrial demand for silver is reshaping its role from primarily a jewelry and investment metal to an essential material in the clean energy transition.

- With silver prices stabilizing around US$28 per ounce in 2025 and climbing above $50 in October, mid-tier producers like Sierra Madre stand to increase shareholder value while supporting rural economies.

Each solar panel consumes about 20 grams of silver, while electric vehicles require up to 50 grams. Analysts predict that by 2030, global silver demand will exceed 1.2 billion ounces annually, highlighting the need for stable, modern supply sources.

Mexico’s combination of skilled workforce, supportive regulations, and modern infrastructure makes it an attractive destination for exploration and investment. Sierra Madre’s work at La Guitarra, along with exploration at Tepic, exemplifies how new companies are turning dormant assets into engines of growth for the next decade.

Reviving La Guitarra: History Meets Modern Mining

The La Guitarra Mine has a storied history dating back to colonial times, producing both gold and silver under different owners, most recently First Majestic Silver. After a period of care and maintenance, Sierra Madre acquired the mine in 2023 with a clear strategy: restart production (achieved January 2025) and expand output.

The mine comes equipped with a 500-tonnes-per-day processing plant, permitted underground workings, and nearby infrastructure including roads, water, and power. With C$19.5 million in fresh capital and a skilled technical team, it has achieved a full-scale restart, with commercial production announced in January 2025.

- By 2027, the company aims to up to triple production to 1,500 tonnes per day, leveraging smart mine design and local partnerships to keep costs low while ramping output efficiently.

Furthermore, their leadership blends local mining expertise with strong capital markets knowledge, enabling efficient project execution. La Guitarra’s high-grade veins, clear exploration targets, and straightforward permitting process make it one of Mexico’s most promising silver-gold projects.

Commitment to Responsible Mining

Sierra Madre embodies a new generation of environmentally and socially responsible miners. The company is upgrading waste and water systems to modern standards, reclaiming tailings efficiently, and minimizing water usage. Open communication with local communities, clear permitting, and strong ESG practices reinforce its credibility with stakeholders and investors.

Modernization at La Guitarra is as much about responsible operations as it is about increasing output. This focus on sustainability aligns with global investor expectations while strengthening its long-term partnerships.

Sierra Madre holds one other project in Mexico’s Sierra Madre mineral belt:

- Tepic Project (Nayarit): High-grade epithermal gold-silver deposit with near-surface mineralization and strong exploration upside.

By focusing on assets with existing infrastructure and clear development paths, Sierra Madre reduces operational risk compared with early-stage exploration projects.

Industrial Demand Drives Silver’s Strategic Role

Silver’s function has evolved beyond traditional uses. Its high conductivity and reflectivity make it essential in solar panels, EV batteries, 5G networks, and electronics. Industrial demand is rising sharply: in 2024, industrial silver consumption reached 680.5 million ounces, accounting for over 30% of total usage, and solar energy alone represents a growing share.

The EV market further drives demand, with each vehicle requiring up to 50 grams of silver. Rising industrial requirements, combined with structural supply deficits, position companies like Sierra Madre to benefit from near-term production growth.

Global silver production is struggling to keep pace. In 2024, total output was roughly 819.7 million ounces, barely a 1% increase over the previous year. A projected 117.6 million-ounce supply deficit in 2025 underscores the need for reliable producers in Mexico’s rich silver belt.

Leveraging Gold’s Enduring Value in a Record-Price Era

Gold remains a cornerstone of stability. Prices are expected to hold above US$3,000 per ounce, supported by investment demand, central bank buying, and geopolitical uncertainty. In Q2 2025, total gold demand rose 3% year-over-year, reaching 1,249 tonnes, while mine production matched this growth, reflecting a healthy market balance.

At La Guitarra, underground mining at the high-grade Coloso vein started in April 2025, increasing production potential and improving grades. The company is upgrading milling systems to improve recovery rates and lower costs, capitalizing on record-high gold prices.

Strong Operational and Financial Performance

- In Q2 2025, Sierra Madre sold 173,562 silver-equivalent ounces: 66,011 ounces of silver and 1,048 ounces of gold, generating 168,535 AgEq ounces at an average price of US$30.10 per AgEq ounce.

The Coloso Mine is ramping up to 150 t/d by year-end, while underground development at the Nazareno Mine has already delivered over 700 tonnes of mineralized material to the Guitarra mill, with grades exceeding prior estimates.

The company raised C$19.5 million in mid-2025 to expand throughput, launch a +20,000-meter exploration program across its mineralized belt, and target high-grade zones in the East District. Strong revenue, cash position, and working capital support ongoing operations and exploration, providing a solid financial foundation for growth.

Silver continues to show upside potential. With a gold-to-silver ratio of 70:1, silver is currently undervalued relative to gold. Combined with rising industrial demand and tight supply, this positions Sierra Madre’s dual-metal strategy to capitalize on both growth and stability. Analysts project that silver deficits will persist, reinforcing the value of near-term production assets like La Guitarra.

- ALSO READ: Gold’s Enduring Value: How Sierra Madre Is Advancing Mexico’s Next Generation of Gold Projects

Two Metals, One Growth Strategy

Sierra Madre’s dual-metal approach combines gold’s stability with silver’s growth potential. Gold anchors financial security, while silver leverages rising industrial demand. This strategy enables the company to maximize shareholder value while maintaining operational resilience.

Phased Expansion Plan

Sierra Madre is executing a two-phase expansion at La Guitarra:

- Phase 1 (Q2 2026): Increase capacity to 750–800 t/d with equipment upgrades, including a new cone crusher and ball mill.

- Phase 2 (Q3 2027): Ramp up to 1,200–1,500 t/d with additional crushing circuits, producing finer material and improving recovery rates.

No additional permits are required, and the expansion will be fully funded from existing cash flow, ensuring self-sustained growth.

Final Take: Why Sierra Madre Is Poised to Deliver Silver and Gold

Sierra Madre Gold & Silver is at the forefront of Mexico’s silver and gold revival. With a mix of production-ready assets, exploration upside, and strong financial backing, the company is well-positioned to benefit from rising demand, structural supply deficits, and supportive market dynamics.

La Guitarra combines history, infrastructure, and timing for near-term production, while Tepic offers significant exploration potential. Sierra Madre’s dual-metal strategy balances stability with growth, leveraging gold’s safe-haven value and silver’s industrial demand.

As global demand for clean energy technologies, electric vehicles, and industrial applications rises, Sierra Madre is uniquely equipped to deliver both silver and gold. Its operational asset, responsible mining practices, and strategic expansion plan position it as a leading junior miner in Mexico’s most productive silver-gold belt.

In short, Sierra Madre has not just restarted a mine—it is breathing new life into Mexico’s historic silver and gold heartland while positioning investors to benefit from a transformative decade in precious metals.

- MUST READ: Reviving Mexico’s Silver Belt: How Sierra Madre’s La Guitarra Mine Is Leading the Comeback

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Sierra Madre Gold and Silver Ltd. (“Company”) made a one-time payment of $25,000 to provide marketing services for a term of one month. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2024, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

For more information on the Company, investors should review the Company’s continuous disclosure filings available on SEDAR+ at www.sedarplus.ca.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

The post Sierra Madre: Breathing New Life into Mexico’s Silver and Gold Heartland appeared first on Carbon Credits.

Nasdaq has backed one of the first carbon removal credit deals licensed under European Union rules. The project is based in Stockholm and is designed to generate high-quality carbon removal credits under a formal EU framework.

This marks a key shift. For years, carbon markets have relied on voluntary standards with mixed credibility. Now, the European Union has developed a regulated system to define what counts as a valid carbon removal. This move aims to build trust and attract large investors into a market that is still in its early stages.

The deal shows growing interest from major companies. It also reflects rising demand for reliable ways to remove carbon from the atmosphere.

Inside the Stockholm Carbon Removal Project

The removal project is run by Stockholm Exergi. It uses a process called BECCS, or bioenergy with carbon capture and storage. This method burns biomass, such as wood waste and agricultural residues, to produce heat and electricity. At the same time, it captures the carbon dioxide released and stores it underground.

The captured CO₂ will be transported and stored deep beneath the North Sea in rock formations. Over time, it will turn into solid minerals. This makes the carbon removal long-lasting and more secure than many nature-based solutions.

The facility is expected to start operating in 2028. Once active, it will generate carbon removal credits that companies can buy to balance their remaining emissions.

Beccs Stockholm is one of the world’s largest carbon removal projects. In its first ten years, the project could remove about 7.83 million tonnes of CO₂ equivalent. This makes it a key tool for helping the European Union reach climate neutrality by 2050.

The project also aims to scale carbon removal by building a full CCS value chain in Northern Europe and supporting a growing market for negative emissions credits.

This project is important because it is one of the first to follow the EU’s new carbon removal certification rules. These rules define how carbon removal should be measured, verified, and reported. They also aim to reduce risks like double-counting and weak accounting.

EU Certification: Building Trust in a Fragile Market

The European Commission has introduced a framework, also called Carbon Removals and Carbon Farming (CRCF) Regulation, to certify carbon removal activities. This includes technologies like BECCS, direct air capture with carbon storage, and biochar.

The goal is to create a trusted system that investors and companies can rely on. It also established the first EU-wide certification framework for carbon farming and carbon storage in products, not just removals.

Until now, the voluntary carbon market (VCM) has faced criticism. Concerns about transparency and “greenwashing” have made some companies cautious. Many buyers want stronger proof that credits represent real and permanent carbon removal.

The EU framework tries to solve this problem. It sets clear rules for:

- Measuring how much carbon is removed.

- Verifying results through independent checks.

- Ensuring long-term storage of CO₂.

This structure may help standardize the market. It could also make carbon removal credits easier to compare and trade across borders. The Commission states that the goal of having the framework is:

“to build trust in carbon removals and carbon farming while creating a competitive, sustainable, and circular economy.”

Corporate Demand Is Growing—but Still Limited

Large companies are starting to invest in carbon removal. However, the market remains small compared to what is needed.

One major buyer is Microsoft. It currently holds about 35% of all global carbon removal credits, making it a dominant player in the market. In fact, it is responsible for 92% of purchased removal credits in the first half of 2025.

Other companies, including Adyen, a Dutch payments provider, have also joined the Stockholm project. These early buyers aim to secure a future supply of high-quality carbon credits as demand grows.

Ella Douglas, Adyen’s global sustainability lead, said in an interview with the Wall Street Journal:

“This project does exactly that [“catalytic impact” to the VMC] while also building key market infrastructure in collaboration with the European Commission.”

Still, many firms remain cautious. Carbon removal technologies are often expensive and not yet proven at a large scale. Some companies also worry about reputational risks if projects fail to deliver real climate benefits.

This creates a gap. Demand is rising, but the supply of trusted credits is still limited.

- SEE event: Carbon Removal Investment Summit 2026

A Market Set for Rapid Growth

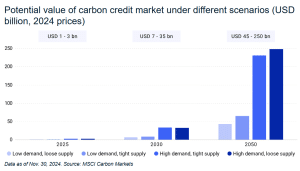

Despite these challenges, the long-term outlook for carbon removal is strong. Estimates suggest the market could reach $250 billion by mid-century, according to MSCI Carbon Markets.

Several factors drive this growth:

- First, global climate targets require large-scale carbon removal. The Intergovernmental Panel on Climate Change estimates that the world may need to remove around 10 billion metric tons of CO₂ per year by 2050 to limit warming.

- Second, many companies have set net-zero goals. These targets often include removing emissions that cannot be avoided, especially in sectors like aviation, shipping, and heavy industry.

- Third, new regulations are pushing companies to disclose and manage emissions more clearly. This increases demand for credible carbon solutions.

However, the current supply falls far short of what is needed. Only a small share of the required carbon removal credits has been developed or sold so far.

Balancing Removal and Emissions Cuts

While carbon removal is gaining attention, experts stress that it cannot replace emissions reductions. Removing carbon from the atmosphere is often more expensive and complex than avoiding emissions in the first place.

Groups like the European Environmental Bureau warn that over-reliance on credits could delay real climate action. They argue that companies should set separate targets for reducing emissions and for removing carbon.

The EU framework reflects this concern. It treats carbon removal as a tool for addressing residual emissions, not as a substitute for cutting pollution at the source. This distinction is important. It helps ensure that carbon markets support, rather than weaken, overall climate goals.

From Concept to Market Infrastructure

The Stockholm project marks a turning point for carbon removal. It shows how rules, strong verification, and corporate backing can bring structure to a fragmented market.

With support from players like Nasdaq, carbon removal is moving closer to becoming a mainstream financial asset. At the same time, the European Union’s certification system is setting the foundation for a more credible and scalable market.

The path ahead remains complex. Technologies must scale. Costs must fall. Trust must grow. But the direction is clear.

Carbon removal is no longer a niche idea. It is becoming a key part of the global climate economy, with the potential to shape investment flows for decades to come.

The post Nasdaq Invests in First EU-Certified Carbon Removal Credits from Stockholm Exergi appeared first on Carbon Credits.

The nuclear energy industry is entering a new phase of transformation. This shift is no longer just about building reactors—it is about building them faster, smarter, and more efficiently.

A recent breakthrough led by the U.S. Department of Energy (DOE), in collaboration with Idaho National Laboratory, Argonne National Laboratory, Microsoft, NVIDIA, Everstar, and Aalo Atomics, highlights that AI tools can streamline the nuclear regulatory process.

AI and DOE’s Genesis Mission: Breaking Bottlenecks in Nuclear Energy Deployment

The work supports President Trump’s Genesis Mission, a national initiative aimed at driving a new era of AI-accelerated innovation and discovery. The mission focuses on using advanced technologies like AI to solve critical national challenges, from energy to healthcare and beyond.

Under the Genesis Mission, DOE recently announced $293 million in competitive funding to tackle twenty-six pressing science and technology challenges, including one dedicated to speeding up nuclear energy deployment.

Rian Bahran, Deputy Assistant Secretary for Nuclear Reactors. said,

“Now is the time to move boldly on AI-accelerated nuclear energy deployment,” “This partnership, combined with the President’s orders, represents more than incremental ‘uplift’ improvements. It has the potential to transform how industry prepares its regulatory submissions and deploys nuclear energy while upholding the highest standards of safety and compliance.”

Simply put, from licensing to construction and operations, AI is now helping eliminate long-standing bottlenecks.

Faster Nuclear Licensing with Advanced Tools

The DOE’s recent announcement is a big step in modernizing nuclear regulation. Normally, preparing licensing documents for nuclear reactors is slow and complicated. It requires reviewing thousands of pages of technical data and making sure everything meets strict rules.

This shows how AI can make nuclear licensing faster and more accurate, helping advanced reactors reach the market sooner. Here’s how AI is simplifying this usually long and complex process.

Kevin Kong, CEO and Founder of Everstar, added:

“Nuclear is poised to solve today’s critical energy challenges,” said “We’re excited to partner with INL to meet the moment, working together to accelerate regulatory review and commercialization.”

Microsoft and NVIDIA Partnership: Building AI Infrastructure for Nuclear Energy

While the DOE demonstration focused on licensing, the broader transformation is being driven by a powerful collaboration between Microsoft and NVIDIA.

Together, they are developing a full-stack AI ecosystem designed specifically for nuclear energy. This platform combines cloud computing, simulation tools, and advanced AI models to streamline every phase of a nuclear project.

Key technologies in this ecosystem include:

- NVIDIA Omniverse for simulation and digital modeling

- NVIDIA CUDA-X and AI Enterprise for high-performance computing

- Microsoft Azure AI for data processing and automation

- Microsoft’s Generative AI tools for permitting and documentation

This integrated system enables developers to manage complex workflows in a unified environment. Instead of working with disconnected tools and datasets, teams can now operate within a single, AI-powered framework.

As a result, nuclear projects become more efficient, transparent, and predictable.

Carmen Krueger, Corporate Vice President, US Federal, Microsoft, further added:

“Our collaborations with DOE, INL, and across the industry are demonstrating how we can effectively bring secure, scalable AI technologies to solve key energy challenges and achieve the broader national and economic security goals envisioned by the Department’s Genesis Mission.”

Aalo Atomics: Cutting Permitting Time and Costs with AI

One of the most compelling real-world examples of AI impact comes from Aalo Atomics.

By leveraging Microsoft’s Generative AI for Permitting solution, Aalo has achieved dramatic improvements in project timelines. The company reported:

- A 92% reduction in permitting time

- Estimated annual savings of $80 million

These results show how AI can address one of the biggest challenges in nuclear development—delays caused by regulatory complexity.

Permitting often takes years and requires extensive documentation. However, AI can automate much of this work, allowing teams to focus on critical decision-making rather than repetitive tasks.

For Aalo, the value goes beyond speed. The technology also improves confidence in project execution by ensuring that all documentation is consistent, complete, and aligned with regulatory expectations.

This video demonstrated further details:

AI-Powered Nuclear Lifecycle: From Design to Operations

The impact of AI is not limited to licensing. It extends across the entire lifecycle of a nuclear plant. In the blog post, written by Darryl Willis, Corporate Vice President, Worldwide Energy and Resources Industry of Microsoft, explained how AI can help nuclear in a broader context.

- Design and Engineering Optimization: AI and digital twins allow engineers to simulate reactor designs in real time. This enables faster iteration and better decision-making. Developers can reuse proven design patterns and instantly evaluate how changes affect performance, safety, and cost.

- Licensing and Permitting Automation: Generative AI handles document drafting, data integration, and gap analysis. It ensures that applications are complete and consistent, reducing delays during regulatory review. This allows experts to focus on safety assessments instead of administrative tasks.

- Construction and Project Delivery: Advanced simulations now include time and cost dimensions. These 4D and 5D models allow developers to track progress, predict delays, and avoid costly rework. AI also enables real-time monitoring, ensuring that construction stays on schedule and within budget.

- Predictive maintenance and Plant Performance: Once a plant is operational, AI continues to add value. Predictive maintenance systems can detect issues early, reducing downtime and improving reliability. Digital twins provide continuous insights into plant performance, helping operators maintain optimal efficiency.

The post AI Solutions from Microsoft and NVIDIA Power DOE’s Nuclear Energy Genesis Mission appeared first on Carbon Credits.

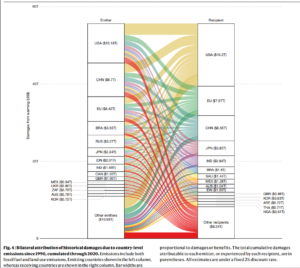

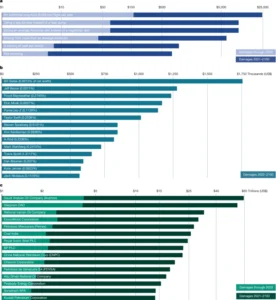

Climate change is not only a physical threat, but it also affects the world’s economy. A major new study published in the journal Nature on March 25, 2026, puts a clear number on this impact. It finds that carbon dioxide (CO₂) emissions from the United States caused about $10.2 trillion in total economic damage worldwide between 1990 and 2020. This makes the U.S. the largest single contributor to climate-related economic loss over that period.

The study shows that emissions slow economic growth in many countries. Rising temperatures cut productivity, lower output, and hurt long-term economic performance around the globe.

Marshall Burke, the lead author of the study, remarked:

“If you warm people up a little bit, we see very clear historical evidence, you grow a little bit less quickly. If you accumulate those effects over 30 years, you just get a really large change by the end of 30 years. It’s like death by a thousand cuts. And you have people being harmed who did not cause the problem, and that feels just fundamentally unfair.”

The researchers focused on carbon dioxide, the most common greenhouse gas. They used data on how temperature affects economic activity and then linked that to how much CO₂ different countries have emitted since 1990. This method links climate science to real economic results, including slower growth, lower productivity, and smaller national outputs.

Counting the Dollars: $10 Trillion in U.S.-Linked Damage

One of the study’s central findings is striking. From 1990 to 2020, U.S. emissions likely caused around $10.2 trillion in global economic damage. This means that warming linked to U.S. emissions has reduced economic production across many countries. The study links these impacts to heat’s long-term effects on labor, agriculture, and overall economic growth.

The damage is not confined to other nations. Roughly 30% of that $10.2 trillion figure is estimated to have occurred within the United States itself. In other words, U.S. emissions have slowed economic growth at home as well as abroad. The remaining impacts are spread across the global economy.

The researchers found that U.S. emissions led to about $500 billion in damage in India and around $330 billion in Brazil during that time. These figures show how carbon released in one area can affect economies far away.

A New Framework for Loss and Damage

The Nature study introduces a new framework for assessing what scientists call “loss and damage.” This term refers to harms that cannot be prevented by reducing emissions or avoided through adaptation alone.

The study uses economic data and climate models. It tracks how temperature changes over the years impact economic output.

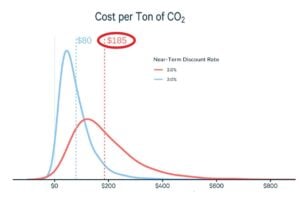

- To put the numbers into context: one tonne of CO₂ emitted in 1990 is estimated to have caused about $180 in global economic damages by 2020.

But that same tonne is projected to cause an additional $1,840 of cumulative damage by 2100, as warming continues and its effects compound over time. This highlights that past emissions still contribute to future economic harm.

The researchers highlight that these estimates focus on economic output, like goods and services. They do not account for all types of climate damage. They do not include costs from loss of life, health impacts, biodiversity collapse, cultural heritage losses, or many kinds of infrastructure damage. These excluded impacts could raise the true total cost of climate change even further.

The Social Cost of Carbon Revisited

This study is part of a broader scientific effort to understand the economic impacts of climate change. Climate and economic models show that rising temperatures are already slowing economic growth. If emissions stay high, this slowdown will get worse in the future.

Analyses by major international institutions and research groups project that climate change could reduce global GDP by a significant percentage by mid-century. This is compared to scenarios with strong mitigation, though exact figures vary by method.

The concept of estimating a “social cost of carbon” (SCC) — a monetary estimate of economic damage per tonne of CO₂ — has been used in policy analysis for years. It helps governments weigh trade-offs in climate policy. For example, they can decide how much to invest in emissions cuts versus adaptation.

However, traditional SCC estimates have been debated. They depend on assumptions about future growth, discount rates, and climate sensitivity. The Nature study advances this approach by tying economic outcomes directly to observed climate impacts.

Economists and climate scientists agree that warming impacts several areas. These include agricultural yields, labor productivity, energy demand, and health outcomes. These effects reduce economic output and increase costs for businesses and governments. The latest research makes these links more explicit by assigning dollar values to the historical impacts of emissions.

Equity and Global Responsibility

The research’s results also highlight important equity questions. Low-income countries often face bigger economic impacts compared to their emissions histories.

For example, nations with warmer climates and more fragile infrastructure may experience greater output losses due to temperature increases. These effects grow over time and can worsen existing development challenges.

At the same time, richer countries with higher historical emissions may take a larger share of responsibility for damage. The Nature study shows it is possible to calculate responsibility in monetary terms. However, turning those numbers into legal or financial obligations is still complex.

Tail Risks and Future Costs

The researchers also point toward the future. It finds that future damages from past emissions are much larger than the losses already accrued.

Since CO₂ remains in the atmosphere for centuries, its warming effects — and the economic damages linked to them — will persist well beyond 2020. This “tail risk” means that the total cost of historical emissions could rise sharply over the rest of this century.

Climate risk is increasingly integrated into economic planning and finance. Governments, businesses, and international institutions are incorporating climate scenarios into investment decisions and risk models.

This includes assessing how rising temperatures may affect infrastructure costs, insurance markets, supply chains, and national budgets. Without strong mitigation and adaptation measures, these economic pressures are expected to grow.

A Shared Reality, Quantified

The Nature study offers a clear and data-based way to think about the economic harms of climate change. Emissions from the United States since 1990 have caused over $10 trillion in global economic damage. This includes harm in the U.S., India, and Brazil.

These findings do not assign legal liability. However, they provide a meaningful picture of how climate change affects the global economy in terms of the social costs of carbon. They show that the costs of climate impacts are measurable and significant.

As the world continues to adapt and respond to climate change, understanding these economic links will be crucial for policymakers, businesses, and communities.

The post $10 Trillion in Carbon Cost? How U.S. Emissions Hit the Global Economy appeared first on Carbon Credits.

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits