Carbon credit projects are gaining significant attention as businesses aim to reduce greenhouse gas (GHG) emissions while maintaining profitability. These projects offer a pathway for companies to offset emissions, improve sustainability, and tap into new revenue streams.

But how do they do that? This guide explores the types, benefits, challenges, and future trends of carbon credit projects, helping businesses navigate this critical climate solution.

5 Key Types of Carbon Credit Projects

Carbon credit projects include a range of activities designed to either reduce or capture GHG emissions. Here are the five primary types, each with specific mechanisms and benefits:

1. Reforestation & Afforestation

Reforestation involves replanting trees in deforested areas, while afforestation refers to planting trees in regions that have not been forested for extended periods. These projects sequester carbon dioxide (CO₂) from the atmosphere as trees absorb CO₂ during photosynthesis, storing carbon in their biomass and soil.

Reforestation and afforestation projects continue to play a crucial role in carbon sequestration. Some large-scale reforestation projects are financially backed by multinational corporations such as this Amazon reforestation initiative by Mombak.

However, there are also a lot of small nature conservation projects worldwide that need funding to scale up. Some of them are still in the development stage but offer innovative approaches to reforesting degraded lands.

One example in Asia is a re-greening project that aims to reforest hectares of deforested land. Using innovative seed ball technology and drone deployment, the project will disperse seeds across vast areas, promoting large-scale forest restoration. This initiative will not only sequester CO₂ but also support local biodiversity and provide economic opportunities for surrounding communities.

Reforestation and afforestation projects are pivotal in global carbon sequestration efforts. According to the Food and Agriculture Organization (FAO), forests absorb approximately 2.6 billion tonnes of CO₂ annually. This figure offsets about ⅓ of the CO₂ released from burning fossil fuels. Such projects also contribute to biodiversity conservation, soil preservation, and the enhancement of water resources.

2. Renewable Energy Projects

Renewable energy projects involve the development of energy sources that do not emit GHGs during operation. Common examples are wind, solar, and hydroelectric power. By replacing fossil fuel-based energy generation, these projects significantly reduce CO₂ emissions.

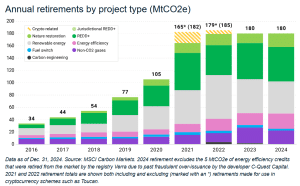

Renewable energy projects remain a significant source of carbon credits. In 2024, renewable energy credits represented 31% of total retirements, with 51.1 million credits retired. This result indicates a continued commitment to clean energy initiatives.

For instance, one of the world’s largest solar energy projects, the Noor Ouarzazate Solar Complex in Morocco covers 3,000 hectares. It has a total capacity of 580 MW, supplying power to over a million people. The project reduces CO₂ emissions by approximately 760,000 tonnes annually.

The Gansu Wind Farm in China is another example. It is one of the world’s largest wind power projects, with a planned capacity of 20 GW. Located in the Gobi Desert, it currently produces over 8 GW of electricity, powering millions of homes. The project reduces CO₂ emissions by millions of tonnes annually and plays a crucial role in China’s renewable energy expansion.

Since 2010, over 750 million voluntary carbon credits have been issued by over 1,700 renewable energy projects worldwide. Wind projects contribute 40% of these credits, followed by hydro (30%) and solar (15%). These projects play a crucial role in diversifying energy portfolios and reducing reliance on fossil fuels.

3. Methane Capture & Destruction

Methane (CH₄) is a potent GHG with a global warming potential about 28 times greater than that of CO₂ over a 100-year period. Projects that capture methane aim to collect and use or destroy methane emissions from sources like landfills, agricultural activities, and wastewater treatment facilities.

In the U.S., numerous landfill gas-to-energy projects have been established to capture methane produced by decomposing organic waste. The captured methane is then used to generate electricity or heat, thereby reducing GHG emissions and providing a renewable energy source.

As of 2024, the U.S. Environmental Protection Agency (EPA) reports 542 operational landfill gas (LFG) energy projects nationwide. These projects harness methane emissions from landfills to generate energy, thereby reducing GHG emissions and providing a renewable energy source.

One company, Zefiro Methane, focuses on sealing abandoned oil and gas wells across the U.S. to prevent methane leaks. By capping and properly decommissioning these wells, Zefiro reduces emissions and generates carbon credits that can be traded in voluntary markets. Their work supports climate goals while addressing the millions of abandoned wells contributing to methane pollution.

The Global Methane Pledge, launched in 2021, aims to reduce global methane emissions by at least 30% from 2020 levels by 2030. Achieving this target could reduce warming by at least 0.2°C by 2050, demonstrating the significant impact of methane capture initiatives.

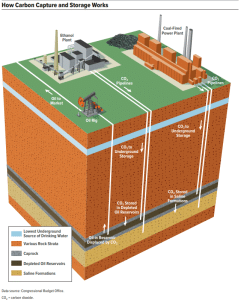

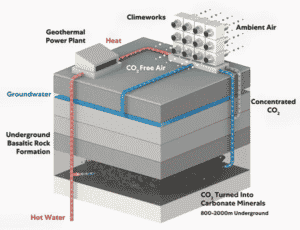

4. Carbon Capture & Storage (CCS)

Carbon Capture and Storage (CCS) involves capturing CO₂ emissions from industrial processes or directly from the atmosphere and storing them underground in geological formations. This technology prevents CO₂ from entering the atmosphere, thereby mitigating climate change.

CCS technologies have seen advancements, with increased investments in projects aimed at capturing CO₂ emissions from industrial processes. In 2024, significant policy developments, including breakthroughs on Article 6 at COP29, are expected to shape the global market for carbon credits, potentially influencing the implementation of CCS projects.

A popular example of CCS is Northern Lights, a joint venture by Equinor, Shell, and TotalEnergies. It is a large-scale carbon capture and storage project in Norway.

- SEE MORE: The “Northern Lights” Shines: Shell, Equinor, and TotalEnergies JV Powers the Norway CCS Project

It captures CO₂ emissions from industrial sources, liquefies them, and transports them for permanent storage under the North Sea. The project aims to store up to 1.5 million tons of CO₂ annually in its first phase, with expansion plans for up to 5 million tons per year, helping industries decarbonize while generating carbon credits.

As of 2024, the global CCS landscape has seen significant growth. There are now 50 operational CCS facilities worldwide, capturing around 50 million tonnes of CO₂ annually. Additionally, 44 facilities are under construction, and 534 are in various stages of development, indicating a robust expansion in CCS initiatives.

The International Energy Agency (IEA) emphasizes that to achieve net-zero emissions by 2050, CCS capacity needs to increase to 1.6 billion tonnes of CO₂ annually by 2030.

5. Community & Land Management Initiatives

These projects focus on sustainable land use practices, conservation, and community-driven efforts to enhance carbon sequestration and support local economies.

Community-driven projects focusing on sustainable land management have been instrumental in generating carbon credits. These initiatives often involve agroforestry and conservation efforts that not only sequester carbon but also provide socio-economic benefits to local communities.

A great example is the Kasigau Corridor project protects over 200,000 hectares of dryland forest in southeastern Kenya. By preventing deforestation and promoting sustainable land management, the project has generated over 1 million carbon credits. It also provides employment opportunities, supports education, and funds community development initiatives, benefiting approximately 100,000 local people.

Community and land management projects are integral to the Reducing Emissions from Deforestation and Forest Degradation (REDD+) program under the United Nations Framework Convention on Climate Change (UNFCCC). These initiatives sequester carbon as well as promote biodiversity conservation and enhance the livelihoods of local communities

4 Benefits of Carbon Credit Projects for Businesses

Environmental Impact & Carbon Reduction

Participating in carbon credit projects enables businesses to offset their carbon footprint effectively. In 2023, global carbon pricing revenues reached a record $104 billion, reflecting increased corporate engagement in emission reduction initiatives.

Beyond compliance, carbon credit projects play a crucial role in meeting global climate goals. According to the IEA, the world must cut emissions by 45% by 2030 to limit global warming to 1.5°C. Businesses that invest in high-quality credits contribute to this target while mitigating their own climate risks and cutting carbon emissions.

Additionally, some programs, like REDD+ help protect biodiversity and improve land-use practices, making them doubly beneficial.

Financial Benefits & Revenue Streams

The carbon credit market has become a substantial financial avenue for businesses. In 2024, credits worth a total of $1.4 billion were utilized by corporations, underscoring the market’s potential for generating additional revenue streams.

Companies not only purchase credits to offset emissions but also develop their own projects to sell verified carbon offsets.

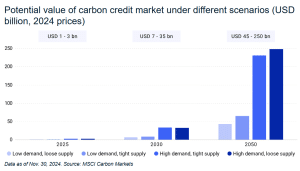

For instance, major corporations like Microsoft and Shell invest in carbon capture projects to generate high-value credits. According to Allied Market Research, the global voluntary carbon market is projected to reach $100 billion by 2030, presenting lucrative opportunities for businesses that engage early. While MSCI data suggests that voluntary carbon credit market could reach up to $250 billion by 2050.

Enhancing Corporate Reputation

Engaging in carbon credit projects enhances a company’s reputation by demonstrating a commitment to sustainability. This proactive approach improves brand image and fosters customer loyalty, as consumers increasingly prefer environmentally responsible companies.

A 2023 survey by IBM found that 70% of consumers are willing to pay a premium for sustainable brands, highlighting the competitive advantage of climate-conscious business strategies.

Moreover, ESG (Environmental, Social, and Governance) investing has surged, with global ESG assets expected to surpass $40 trillion by 2025. Companies that actively reduce their carbon footprint through verified credit projects are more likely to secure funding from institutional ESG-focused investors.

Regulatory Compliance & Market Demand

With the implementation of stricter environmental regulations worldwide, carbon credits assist businesses in complying with emission targets. The expansion of carbon pricing instruments, now totaling 75 globally, indicates a growing market demand for sustainable practices.

Governments are tightening emission policies, making carbon credits a crucial tool for avoiding hefty fines and maintaining operations.

The European Union’s Carbon Border Adjustment Mechanism (CBAM), set to be fully implemented by 2026, will require importers to pay for embedded emissions in products like steel and cement. Similarly, the U.S. Inflation Reduction Act (IRA) includes billions in incentives for clean energy projects and carbon capture. These policies create a clear incentive for companies to invest in carbon credits to maintain regulatory compliance and gain a competitive edge.

3 Steps To Implementing A Successful Carbon Credit Project

If you’re planning or simply thinking about how to have a carbon credit project that emerges successfully, here are the three major steps to follow:

1. Identifying Project Scope & Goals

Start by defining your carbon credit project’s objectives. What are you aiming to achieve? This could range from reducing carbon emissions to generating new revenue streams or ensuring compliance with regulatory frameworks. Each objective should be clear and measurable to track progress.

Once your goals are set, choose the right project type. Whether it’s reforestation, renewable energy generation, or methane capture, aligning your project’s nature with your goals is essential. For instance, if emission reductions are a priority, a renewable energy project may be the best fit. Careful selection of the project type will streamline efforts and maximize impact.

2. Verifying Carbon Offset Credits & Certification

Next, focus on obtaining certification for the carbon credits you generate. Certification from established, recognized standards—such as the Gold Standard or Verra—validates the legitimacy of your carbon credits. Stick to proven methodologies and ensure full transparency in your project’s implementation.

Rigorous monitoring and reporting will ensure that your carbon credits are verified correctly and gain credibility in the marketplace. Remember, the higher the standard of certification, the more trustworthy your credits will appear to buyers, enhancing their marketability.

3. Market Engagement & Carbon Credit Trading

Finally, engage with carbon credit trading platforms to bring your credits to market. Established marketplaces, such as those launched by governments or private entities, allow for easy buying and selling of carbon credits. For example, Indonesia’s entry into the global carbon market in 2024 was a significant step toward green energy funding.

By listing your credits on such platforms, you can contribute to the global effort against climate change while monetizing your efforts. The carbon trading landscape is growing, making it crucial for businesses to stay informed and ready to leverage these platforms for maximum impact.

5 Challenges in Managing Carbon Credit Projects

After knowing the benefits of and the steps needed to implement a carbon credit project, it’s also wise to learn the challenges involved.

-

Ensuring Project Validity & Monitoring

Rigorous monitoring and validation are necessary to maintain project integrity and avoid issues like double counting. This ensures that emission reductions are genuinely achieved.

-

Avoiding Double Counting

Implementing robust tracking systems is crucial to prevent the same carbon credit from being counted multiple times, preserving the credibility of carbon offset claims.

-

Managing Volatile Market Prices

The carbon credit market can experience price fluctuations, impacting the financial sustainability of projects. Staying informed about market trends and diversifying project portfolios can help mitigate these risks. Go over this carbon price page to stay informed.

-

Meeting Strict Regulatory Standards

Compliance with evolving environmental regulations requires businesses to stay updated. Engaging with policy developments, like the breakthroughs in Article 6 at COP29 in 2024, ensures projects align with international standards.

-

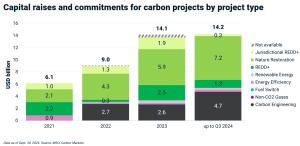

Securing Long-Term Financing

Attracting and maintaining investment for carbon credit projects can be challenging. However, by the end of the third quarter of 2024, $14 billion had been raised or committed, reflecting increasing investor interest and confidence in the market.

3 Future Trends in Carbon Credit Projects

Finally, it helps to know what trends are unfolding in the market and learn how to leverage them, namely:

Innovations in Carbon Capture Technologies

As carbon capture technologies evolve, they are expected to significantly improve the efficiency and scalability of emission reduction efforts. Innovations like Direct Air Capture (DAC) are poised to capture carbon dioxide directly from the atmosphere, making it easier to offset emissions from difficult-to-decarbonize sectors.

These advancements will drive the development of high-quality carbon credit projects that can scale rapidly to meet global climate goals. The global carbon capture market could reach $7.3 billion by 2030, highlighting its growing potential as a major player in carbon credit generation.

Expansion of Carbon Credit Marketplaces

The emergence of new carbon credit marketplaces is a key trend shaping the future of carbon trading. Platforms like Indonesia’s IDX Carbon, launched in 2024, are increasing global participation in emission reduction initiatives. Such marketplaces are making carbon credit trading more accessible, especially for emerging economies looking to fund sustainability projects through carbon sales.

There are over 60 carbon trading platforms now active worldwide. The expansion of these digital platforms is expected to drive greater liquidity and efficiency in the carbon market, enabling more businesses to engage in carbon offsetting.

Increasing Focus on Quality & Additionality

Looking ahead, the carbon credit market will place an increasing emphasis on the quality of credits and additionality. Additionality ensures that carbon reduction projects would not have happened without the credit system, proving their real-world impact.

The Integrity Council for the Voluntary Carbon Market (ICVCM) is leading efforts to create new benchmarks for high-quality carbon credits. As sustainability-conscious investors and businesses seek reliable offsets, there will be a stronger demand for verified, additional, and impactful carbon credit projects.

Conclusion

Carbon credit projects are vital tools for achieving sustainability and profitability in today’s business landscape. By understanding the different types, benefits, and challenges, companies can effectively implement these projects to reduce their carbon footprint, meet regulatory standards, and enhance their market position. With innovations and growing market opportunities, these projects would be pivotal in the global effort to combat climate change.

- FURTHER READING: Is the Voluntary Carbon Market Dead?

The post How Carbon Credit Projects Contribute To Sustainability and Profitability appeared first on Carbon Credits.

Key takeaways

- SBTi is the default reference point for corporate climate action: 51% of Fortune Global 500 companies now hold net-zero targets, up from 8% in 2020, and over 11,000 organizations worldwide have SBTi-validated targets.

- Net Zero Standard V2 redefines climate leadership as reducing emissions and mitigating ongoing emissions, not reduction alone.

- The new standard adds flexibility through five-year cycles, a “best efforts” standard, and an Asset Transition Method for companies whose path to net-zero doesn’t fit a straight-line trajectory.

- Voluntary carbon credits are formally recognized for the first time, with reduction and removal credits accepted from 2027, and removals required from 2035.

- Companies with 2030 targets keep using V1 for their current cycle and move to V2 in 2028; companies without targets can start using V2 on February 1, 2027.

Why every business needs to understand the SBTi Net-Zero Standard revision

The Science Based Targets initiative (SBTi) has become the default reference point for credible corporate climate action. Net-zero targets are now held by 51% of Fortune Global 500 (FG500) companies, up dramatically from just 8% in 2020, and more than 11,000 organizations worldwide have set SBTi-validated targets.

However, SBTi’s influence extends well beyond the companies formally participating in the program. Every business in the value chain of an SBTi participant will have to reduce its own carbon emissions, and businesses that aren’t SBTi participants themselves still look to the program for guidance on climate action.

In short, SBTi gives every business a credible blueprint for climate action, and companies that follow its principles can pursue climate action with confidence, whether or not they’re formally part of the program.

How will the Net Zero Standard revision affect business climate action?

SBTi participation is expected to grow. Despite strong target-setting participation among the F500, only 17% of companies use the SBTi Net Zero Standard V1 beyond target setting, largely because its rules have been seen as too rigid to apply in practice. Much of the Net Zero Standard revision has focused on creating more flexibility to enable higher participation. Medium and small businesses will also increasingly feel pressure for climate action, since SBTi mandates that its participants reduce carbon emissions across their value chains.

Net Zero Standard V2 also redefines climate leadership: leading climate action now means reducing emissions and mitigating ongoing emissions. Reducing your own emissions while ignoring the emissions you continue to release along the way is no longer considered leadership. Supporting voluntary carbon projects with high-integrity carbon credits is now backed by the leading authority on corporate climate action.

What lessons shaped the Net Zero Standard V2 revision?

The revision reflects a few learnings about what actually drives climate progress, and how SBTi built those lessons into the new standard.

| Net Zero Standard V1 Learnings | Net Zero Standard V2 Implementation |

|---|---|

| Making real short-term progress is more important and more difficult than making big long-term promises | Focus on short-term climate progress |

| Every company has a different path to net zero that doesn’t always fit generalized net-zero rules | Create asset transition plans based on each company’s unique asset lifecycles and capital planning |

| We need to mitigate our ongoing emissions to keep global carbon emissions in check | Reduce global carbon emissions by financing voluntary carbon projects with high-integrity carbon credits |

What are the key changes between the old and new Net Zero Standard?

Both versions of the standard are grounded in net-zero by 2050. However, the old standard treated climate leadership as simply reducing emissions, expected a long-term commitment to net zero, based emission reduction targets on generalized net-zero goals, revoked status from companies that fell behind on targets, and ignored voluntary carbon projects entirely.

The new standard treats climate leadership as reducing emissions and mitigating ongoing emissions. It shifts the focus to short-term progress through five-year cycles, and it bases emission reduction targets on both the net-zero goal and a company’s own asset decarbonization plan. A new Asset Transition Method lets companies set decarbonization targets through asset plans with committed, verifiable steps; an ambitious but achievable path based on a company’s starting point, financial resources, and technology, with multiple pathways to reflect the unique opportunities and constraints of different industries and companies.

Crucially, the new standard moves to a “best efforts” basis that creates real flexibility on progress against targets. Businesses that miss their targets can keep their status if they’ve used “every lever” within their control, and minimum progress rules will be set out in the SBTi Assurance Manual.

Finally, the new standard formally uses voluntary carbon projects to mitigate ongoing emissions. From 2027 through 2034, this mitigation is recognized, and both carbon reduction and removal credits are accepted. From 2035 forward, mitigation with carbon removal credits becomes required, with durability matching between the removal and the emission it offsets.

| Old Net Zero Standard | New Net Zero Standard |

|---|---|

| Grounded in net-zero by 2050 | Grounded in net-zero by 2050 |

| Climate leadership is reducing emissions | Climate leadership is reducing emissions and mitigating ongoing emissions |

| Make a long-term commitment to net-zero | Focus on short-term progress in 5-year cycles |

| Emission reduction targets are based on net-zero goal |

|

| Businesses who fall behind targets lose status |

|

| Ignores voluntary carbon projects |

|

When does the new Net Zero Standard take effect?

Companies with existing 2030 targets should continue using the old Net Zero Standard for their current cycle, and start using the new Net Zero Standard in 2028 to set targets for the next cycle (2030–2035).

Companies that don’t yet have targets can use the new Net Zero Standard starting February 1, 2027.

What are SBTi’s Category A and Category B companies?

The new Net Zero Standard splits companies into two categories, with different requirements attached to each.

Category A covers large companies from all countries and medium-sized companies from high-income countries. A company from any country qualifies if it meets at least one of: net turnover of €450 million or more, or 1,000 or more full-time employees. A company from a high-income country qualifies if its Scope 1 and 2 emissions are 10,000 tCO2e or more, or if it meets at least two of: balance sheet of €25 million or more, net turnover of €50 million or more, or 250 or more full-time employees.

Category B covers small companies from all countries and medium-sized companies from lower-income countries.

How do Scope 1 targets work under Net Zero Standard V2?

Scope 1 targets aim to transition companies to net-zero direct emissions by 2050 or sooner, and companies can choose from three approaches.

- Absolute emissions reduction follows a straight-line emissions trajectory from the target base year to the net-zero year.

- Emissions intensity reduction lets companies follow sector-specific pathways designed to reflect the reduction opportunities available in sectors like steel, cement, or chemicals.

- Asset transition is designed for companies whose capital stock turnover doesn’t follow a linear or sector pathway. These companies design a transition plan to operate existing assets efficiently and replace them with low-carbon assets, using predetermined milestones.

How do Scope 2 targets work under Net Zero Standard V2?

Scope 2 targets address emissions from purchased electricity through three pathways:

- Reducing electricity consumption,

- Reducing grid consumption by installing onsite or direct-line offsite clean energy generation, and

- Cleaning up the regional grid using market-based tools like PPAs, RECs, and GOs that drive clean energy development.

V2 introduces a dual Scope 2 framework requiring two separate targets, with an overall goal of 100% low-carbon electricity by 2040.

The location-based target addresses the carbon intensity of a company’s physical power use, and requires companies to show that their grid consumption is falling and/or that their physical grid use is getting cleaner; in other words, that their market-based solutions are actually making the grid cleaner.

The market-based (or zero-carbon electricity) target tracks a company’s use of low-carbon power generation contracts and Energy Attribute Certificates. It requires geographical matching of these certificates with electricity consumption based on deliverability regions (grid regions); annual matching is allowed, though hourly matching is encouraged. Category A companies with large electricity loads must report the percentage of their Scope 2 electricity consumption matched with low-carbon attributes on an hourly basis, and there’s an optional recognition framework for companies that meet hourly matching thresholds.

How do Scope 3 targets work under Net Zero Standard V2?

Scope 3 targets share the same 2050-or-sooner net-zero goal, but companies set near-term targets only for material emissions sources in their value chain and areas where they have real influence. Long-term Scope 3 targets are generally not required.

Limited, justified exclusions are allowed for near-term targets, including categories that individually account for less than 5% of total Scope 3 emissions, and activities where a company lacks practical influence, like leased assets it doesn’t operationally control, or the processing of sold products. Optional exclusions are also available in specific categories.

Companies can choose from three approaches to near-term Scope 3 targets:

- An overarching emissions reduction target, which follows a linear contraction of emissions from the base year to residual emissions of 10% or less by 2050 or sooner;

- An overarching supplier/customer alignment target, benchmarked against a growing share of tier 1 suppliers and customers reaching net-zero by 2050 or sooner; or

- A category- or activity-specific target, tailored for companies with concentrated emissions in particular Scope 3 categories or high-emitting activities.

What is “ongoing emissions mitigation” under the new SBTi standard?

This is one of the most significant additions in Net Zero Standard V2. Accelerated climate contributions are needed to help the world achieve climate objectives, limit temperature overshoot, mitigate transition risks, and support the scale-up of climate solutions, and V2 formally recognizes that. Ongoing emissions mitigation runs as a parallel track to companies also reducing their own emissions.

The framework is initially voluntary, with recognition available at three contribution levels to encourage early action.

- Engaged companies address more than 1% of total Scope 1, 2, and 3 emissions.

- Advanced companies address more than 10% of total Scope 1, 2, and 3 emissions, including 100% of Scope 1 and 2 emissions.

- Leadership companies address 100% of total Scope 1, 2, and 3 emissions with a contribution budget of $80/tCO2e.

Carbon credits used for this purpose have to meet certain quality standards. They must be ex-post (issued after the mitigation has actually occurred), independently third-party-assured, emissions reductions or removals, measured in tCO2e, that occur within five years prior to the reporting year. They must be sourced from outside the company’s own value chain. Further minimum criteria will be set to align with high-integrity frameworks, with additional details on the recognition program expected in the second half of 2026.

Starting in 2035, carbon removals become mandatory for Category A companies. From that point, the carbon removal coverage requirement rises linearly from 1% of Scope 1–3 emissions to 100% by a company’s net-zero year. Within that, 10% of long-lived GHG emissions must specifically be covered by durable removals, also rising linearly to 100% by the net-zero year.

How must companies neutralize residual emissions?

At a company’s net-zero target year and thereafter, it must reduce its Scope 1, 2, and 3 emissions to zero or to residual levels, and neutralize all residual emissions using eligible carbon removals. Those removals have to meet two conditions: they must occur within the same reporting period as the residual emissions they’re neutralizing, and long-lived GHGs must be neutralized with long-lived removals, matching the durability of the removal to the atmospheric lifetime of the emission being addressed.

What is the SBTi implementation hierarchy?

Net Zero Standard V2 also lays out how companies should prioritize their actions for credible target delivery, in three tiers.

- Direct actions, at the activity level, are actions that reduce emissions at the source within a company’s own operations and value chain; things like efficiency improvements, fuel switching, and engaging suppliers and customers to reduce their emissions.

- Actions within shared systems, or activity pools that reduce the emissions of shared systems like electricity or gas grids. This includes market instruments that convey low-carbon attributes, such as PPAs, RECs, and GOs, all of which must meet minimum integrity criteria that SBTi will elaborate on in future guidance.

- Sector-level actions relate to the same type of activity occurring in a relevant geography or system, in a way that meaningfully reduces the emissions a company is responsible for.

How Terrapass helps businesses meet the new SBTi standard

As the rules around carbon credits become more rigorous, the quality of the credits behind them matters more than ever. Terrapass has expanded our global network of carbon projects: more project types, locations, prices, ICVCM CCPs, and UN SDGs, spanning super-pollutant destruction, nature-based solutions, and durable removals. We offer Green-e® Climate Certification and we only source from third-party-verified projects on ICVCM-Eligible registries.

We also help clients with impact beyond carbon: EACs, RECs, and GOs including Green-e® Certified credits that support leading renewable energy projects; water credits that support water restoration projects; and custom environmental product needs like RNG and SAF. Wherever your organization is on its sustainability journey, we help clients around the world address climate risk, advance their environmental and social goals, and get the most out of their sustainability budgets.

FAQ: SBTi Net-Zero Standard revision

What is the SBTi Net-Zero Standard?

It’s the framework the Science Based Targets initiative publishes for companies that want validated, credible net-zero targets tied to limiting global warming.

What is changing in the SBTi Net Zero Standard V2 revision?

The biggest changes are more flexibility (five-year cycles and a “best efforts” standard), a new Asset Transition Method for companies whose emissions don’t follow a straight-line path, and formal recognition of voluntary carbon credits for mitigating ongoing emissions.

When do companies need to switch to the new SBTi standard?

If your company already has 2030 targets, you keep using V1 for your current cycle and move to V2 in 2028. If you don’t have targets yet, you can start using V2 as of February 1, 2027.

Can companies use carbon credits to meet SBTi targets?

They can. Under V2, high-integrity carbon reduction and removal credits count toward mitigating ongoing emissions from 2027 through 2034. Starting in 2035, only removal credits count, and they need to be durability-matched to the emissions they offset.

What’s the difference between Category A and Category B companies under SBTi?

Category A is large companies everywhere plus medium-sized companies in high-income countries, based on thresholds like revenue, headcount, or emissions. Category B is small companies everywhere and medium-sized companies in lower-income countries.

What happens if a company misses its SBTi target?

Under the old standard, falling behind could cost a company its SBTi status. Under V2’s “best efforts” approach, a company can hold onto its status as long as it’s used every lever within its control, with minimum progress rules coming in the SBTi Assurance Manual.

Sources: This post is based on Terrapass’s internal analysis of the SBTi Corporate Net-Zero Standard V2.0. Facts and figures were checked against SBTi’s official V2.0 announcement, SBTi’s Corporate Net-Zero Standard V2.0 — Chapter 6: Ongoing Emissions Responsibility, Trellis’s coverage of the standard, Trellis’s reporting on Ongoing Emissions Recognition costs, Sylvera’s analysis of what comes next, Anthesis Group’s Fortune 500 net-zero commitments research, and Climate Impact Partners’ seventh annual FG500 analysis, as reported by CarbonUnits.com.

The post SBTi Net-Zero Standard V2: What the Revision Means for Every Business appeared first on Terrapass.

For most businesses, the emissions that matter most sit outside their own walls. Scope 3 emissions, everything generated across your value chain, from the suppliers who make your inputs to the customers who use your products, typically make up the majority of a company’s total carbon footprint. Under the Corporate Sustainability Reporting Directive (CSRD), those value-chain emissions now have to be measured and disclosed with a rigour that spend-based estimates alone struggle to satisfy. This guide sets out how to improve Scope 3 data accuracy for CSRD: the calculation methods open to you, how to move from estimates to verified supplier data, and how to govern that data so it holds up to audit.

![]()

A carbon credit is a commitment that extends well into the future. The tonne of CO₂ compensated for today from a nature-based carbon project must remain out of the atmosphere for good, which means the forest behind the credit has to remain standing long after the transaction is complete. For any buyer, this raises a defining question: What ensures that the forest endures?

![]()

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测