The amount of foreign aid the UK spends on climate action reached a record high of around £3bn last year, according to government figures obtained by Carbon Brief.

However, Carbon Brief analysis shows that more than £500m of this sum comes from controversial changes in the way the UK calculates its climate aid for developing countries.

By leaning on private-sector investment and including existing aid projects in the total, the government is able to inflate its figures without providing as much new climate funding.

Including this money puts the UK on track for its five-year goal of providing £11.6bn by 2026 to support climate action in developing countries, even as it cuts the overall aid budget.

Climate aid – which is often referred to as “international climate finance” (ICF) – will likely still need to rise above £3bn in 2025, if the UK is to achieve its target over the next year.

The new data, released to Carbon Brief via freedom-of-information (FOI) requests, covers provisional 2024-25 spending across the three major government departments that fund climate projects overseas.

This analysis is the latest in a series of articles by Carbon Brief documenting the UK’s ICF contributions since 2011.

Key findings from the most recent year include:

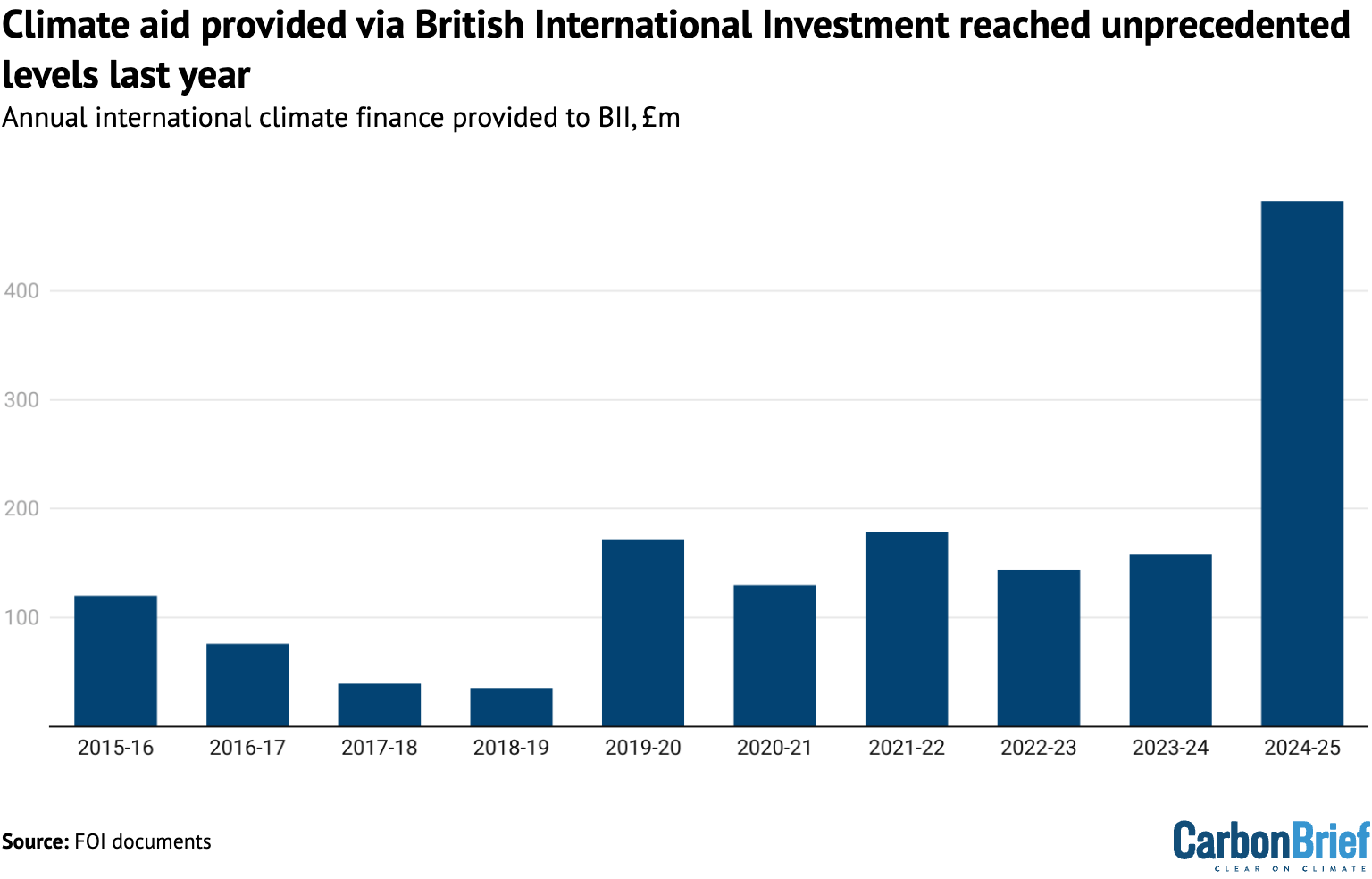

- By far the largest payment last year was a £482.3m contribution to boost British International Investment’s (BII) private-sector interests in developing countries.

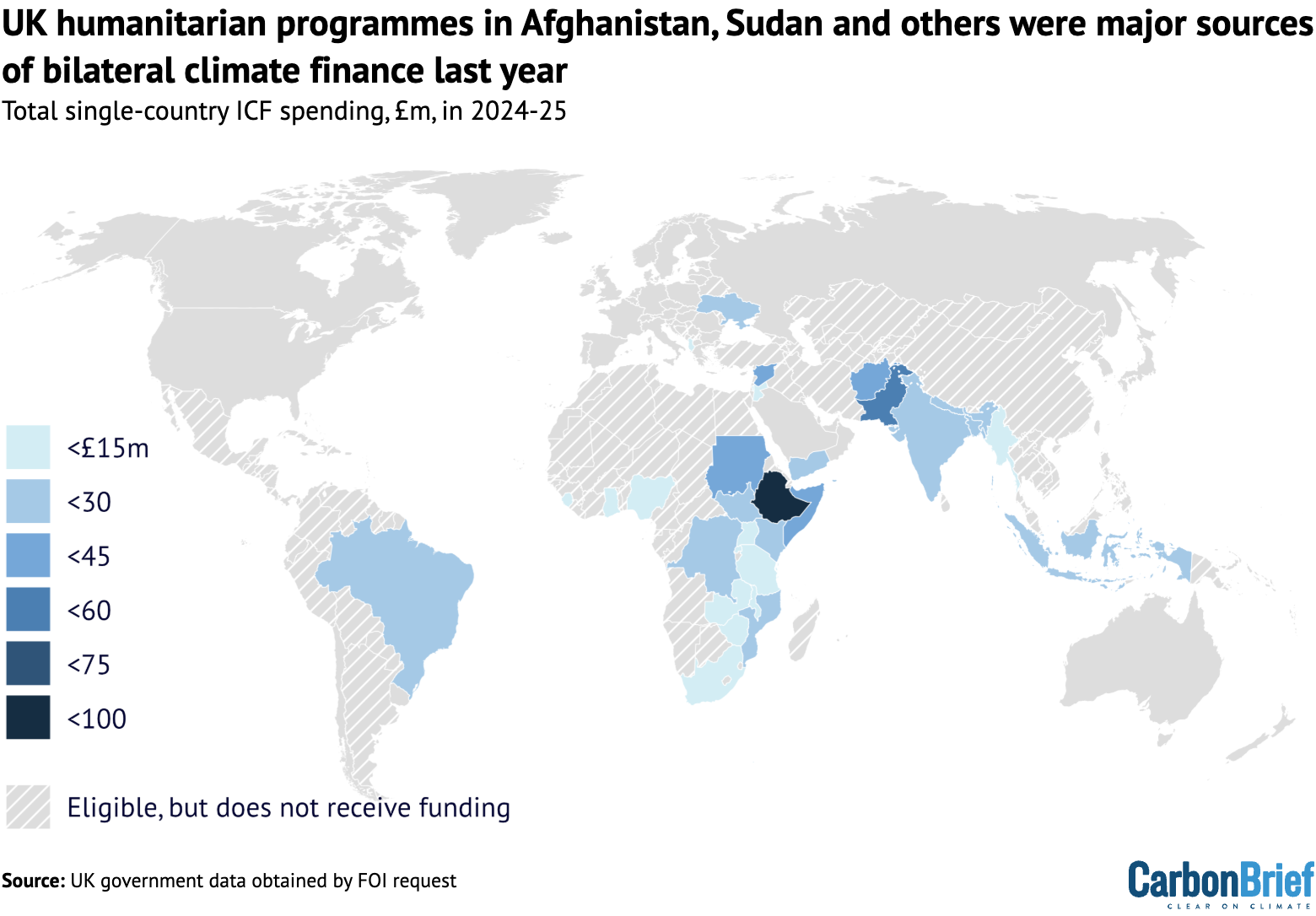

- Ethiopia was the largest recipient of bilateral climate finance (£92.3m). Other major recipients include Pakistan (£55.8m), Afghanistan (£43.7m) and Sudan (£41.1m).

- The biggest single project to receive funding was a World Bank initiative helping developing countries to sell carbon offsets, which received £153.9m.

- Large portions of climate finance also went to the Green Climate Fund (£227m) and the Global Environment Facility (£64.8m).

- Without the government’s changes, which mimic the looser accounting used by some other countries, climate finance would have needed to increase 78% this year. With the changes, climate finance only has to increase by 2%.

- Around £1.3bn – nearly a sixth of the UK’s ICF over the past four years – can be linked to the government’s accounting changes.

Target achieved?

After it was elected last year, Labour confirmed that it would honour the previous government’s pledge to provide £11.6bn of climate finance over the five-year period ending in 2025-26.

This money is the UK’s contribution, under the Paris Agreement, to help developing countries cut emissions and protect themselves from the threat of climate change.

Since the goal was first announced in 2019, experts have regularly voiced doubts that it can be achieved due to major cuts to the foreign-aid budget by successive governments.

More uncertainty followed the announcement in February that the Labour government would cut aid further – from 0.5% of gross national income to 0.3% – ostensibly to fund defence spending. (The government insisted that the remaining aid would “prioritise” climate.)

Despite these changes and uncertainty, the figures provided to Carbon Brief via FOI reveal that the UK is, in fact, on track to meet its £11.6bn target.

Climate-finance spending reached a record high of just under £3bn in the financial year 2024-25, more than £700m higher than the previous year.

(Note that these figures are “provisional” and subject to revision. Due to methodology changes, the final figures for UK climate finance in 2023-24 were much higher than those provided to Carbon Brief via a previous FOI. See the Methodology for more details.)

Assuming the provisional figures for 2024-25 are accurate, the UK would still need to raise its climate finance to £3.1bn in 2025-26 in order to meet the £11.6bn target, as shown in the figure below.

This level of climate finance would need to be maintained, even as the government scales back its overall aid budget in 2025.

When asked at a recent committee hearing whether there would be any new money for the £11.6bn goal, international development minister Baroness Chapman spoke frankly:

“I think the search for new money at the moment is going to be pretty fruitless…Is there going to be any new money for climate in a world where we have just gone from 0.5% to 0.3%? I think you can probably work that out.”

Instead of new funding, the upward trajectory of climate aid has been largely driven by the UK expanding what it counts towards the total. These changes were initially made under the Conservatives, but Labour has retained them.

By relabelling existing funding for multilateral development banks (MDBs), humanitarian aid and private-sector investments via BII as “climate finance”, the UK has inflated the figures without allocating genuinely new funds, making the £11.6bn goal easier to achieve.

Based on data acquired through successive FOIs, Carbon Brief estimates that £528m, or 18% of climate finance provided in 2024-25, can be linked to these accounting changes.

Since 2021, the running total of climate finance resulting from these changes is more than £1.3bn, Carbon Brief analysis suggests, amounting to nearly a sixth of spending to date.

Experts have pointed out that this amounts to a real-world cut in climate aid, as it means less additional funding than was originally pledged.

Without the accounting changes, UK climate finance would only have reached around £2.5bn last year, as the chart below shows.

To achieve the £11.6bn goal from this position, climate finance would have needed to increase by 78% this year, nearly doubling from a year earlier. In comparison, the accounting changes mean it only has to increase by 2%.

The government says that its accounting changes merely brought it in line with other countries. A Foreign, Commonwealth and Development Office (FCDO) spokesperson tells Carbon Brief:

“We will continue to account for all of our international climate finance using internationally agreed OECD guidelines. Meeting our £11.6bn commitment by March 2026 remains our ambition and it is only right that we accurately reflect the funding going to support this aim.”

In response, NGOs and aid experts have argued the UK should have retained its former position as a leader in climate-finance accounting standards, rather than aligning with the looser methodologies used by many others, such as Germany and France.

Moreover, the £11.6bn goal was meant to be a doubling of the government’s previous £5.8bn target, which was based on the original accounting methodology. If the previous target had also been based on a broader definition of climate aid, then the current £11.6bn target would have needed to be higher to represent a doubling.

As the UK nears the end of its third five-year ICF target, it is expected to announce another goal covering the period 2026-27 onwards. This will feed into the $300bn global climate finance target that nations agreed at the COP29 climate summit last year.

Amid the aid cuts, climate NGOs say that the accounting changes should be reversed and the UK should turn to “polluter-pays” measures to generate the required public funds. Catherine Pettengell, executive director of Climate Action Network UK, tells Carbon Brief:

“Our main concern is that we now have the spending review, but there is still no clarity – or vision – on current or future climate finance from the UK.”

Big investments

The UK is now leaning heavily on private-sector investments to achieve its climate-finance goals, according to Carbon Brief’s analysis.

By far the largest climate-finance input last year was a £482m contribution to the UK’s development finance institution, BII.

This is the biggest climate-finance contribution the UK has ever made in a single year, according to the data that Carbon Brief has collected in recent years.

It also amounted to nearly a fifth of the total climate finance last year and almost three times more than the UK has ever channelled into BII before.

BII is a publicly owned, for-profit company that largely supports itself with its £7.3bn portfolio of investments in developing countries, but it also receives regular injections of aid money.

The surge in BII climate finance last year can be attributed to two things.

First, the government now counts more of its BII investments as climate finance than it did previously, following the accounting changes. It argues that this more accurately reflects BII’s expanding focus on investing in clean-energy projects overseas.

The government also decided to invest an extra £400m – largely from underspending on housing asylum seekers in the UK – into BII, bringing its total budget for the year up to £881m.

Prior to these changes, the government expected BII climate finance to be worth £126m in 2024-25, according to forecasts previously obtained by Carbon Brief.

It has, therefore, added an extra £356m to BII’s contribution. Carbon Brief estimates that £218m of this can be attributed to the accounting changes, rather than the increase in funding. (See: Methodology.)

Critics argue that BII, which focuses on loans and equity finance rather than grants, is not capable of supporting climate action in the poorest and most climate-vulnerable nations. (Separately, it has also been criticised for continuing to support fossil-fuel developments.)

Last week’s spending review provided the FCDO with at least £300m annually out to 2029-30 for BII and similar organisations, even as billions are cut from its aid budget. In this context, Ian Mitchell, a senior policy fellow at the Center for Global Development, tells Carbon Brief:

“BII looks set to become the government’s main climate-finance vehicle. Though, whether this is compatible with its historic focus on Africa and the poorest countries remains to be seen.”

Meanwhile, the biggest single project to receive funding from the UK last year was the World Bank initiative titled: “Scaling Climate Action by Lowering Emissions (SCALE).” The government provided it with an initial contribution of £154m.

SCALE aims to help around 20 countries generate carbon credits that can be sold by companies on the voluntary offset market or internationally via Article 6 carbon markets.

According to the UK government, one aim is to “maximise the mobilisation of additional finance through the sale of carbon credits”.

Selling carbon offsets has long been touted as a way to channel climate finance into developing countries, but the practice has faced intense scrutiny and accusations of “greenwashing” in recent years.

Accounting changes

Other large portions of funding in the UK’s 2024-25 climate-finance budget can also be attributed to changes in the government’s accounting methodology.

For example, as of 2023, the UK started counting portions of its “core” payments into MDBs as climate finance, significantly inflating its climate-aid total.

This money is used by the banks to issue loans and – to a lesser extent – grants for projects in developing countries. While many of these projects will be climate-related, relabelling some of the UK’s contributions as “climate finance” does not result in any additional funds being distributed.

In 2024-25, this relabelling accounted for at least £103m of the total climate finance, including £84m for the African Development Bank (AfDB), £11m for the Asian Development Bank (ADB) and £8m for the Caribbean Development Bank (CDB) Special Development Fund.

In terms of bilateral aid from the UK, several of the projects with the largest share of climate finance last year were in nations facing war, famine and natural disasters.

This can partly be attributed to accounting changes that mean 30% of all humanitarian funding in the most climate-vulnerable countries – including Afghanistan, Sudan and Somalia – is now automatically counted as climate finance within government accounting.

Some of these nations have, therefore, risen to be top recipients of bilateral “climate aid” from the UK – as shown in the figure below – through programmes such as Sudan Humanitarian Preparedness and Response.

(Such programmes tend to involve the UK supporting NGOs rather than providing funds to governments. For example, FCDO has two “flagship” humanitarian programmes in Afghanistan – both with an ICF component – but does not provide funds to the Taliban.)

This accounting change was viewed by the previous Conservative government as a way to avoid a “trade-off” between climate and humanitarian projects, amid aid budget cuts.

As the map above shows, Ethiopia remained the largest recipient of UK climate finance via single-country projects last year, with £92.3m in total. This has been the case for more than a decade.

The finance largely comes from two programmes, which aim to improve climate resilience in regions of Ethiopia that have been afflicted by drought and flooding. The country has faced years of regional conflicts that have been exacerbated by climate shocks.

Rather than directly supporting individual projects in individual countries, most UK climate finance is distributed to international bodies and initiatives that serve many countries.

Some of the biggest payments are to well-established international grant providers. These include £227m for the Green Climate Fund, £64m for the Global Environment Facility and £26m for the Global Biodiversity Framework Fund (GBFF).

Other large payments went to long-running initiatives to help “build financial markets and institutions” in Africa and “mobilise private investment in infrastructure” in developing countries.

Methodology

This analysis is the latest part of Carbon Brief’s efforts to assess the UK’s ICF contributions by financial year. Detailed data underpinning these contributions is not released publicly, but is required to track progress towards the UK’s ICF targets.

Total ICF figures for the years 2011-12 to 2023-24 are based on summary public statements made by the government. Ministers have quoted different figures on different occasions, but Carbon Brief is using a March statement from FCDO minister Stephen Doughty for the 2011-12 to 2023-24 period, as this is understood to be the most up-to-date.

The figures for 2024-25 are based on FOI responses from the three major departments responsible for the UK’s overseas climate-related aid projects: FCDO, the Department for Energy Security and Net Zero (DESNZ) and the Department for Environment Food and Rural Affairs (Defra). Around 80% of climate finance provided by the UK is overseen by the FCDO.

All three of these departments provided the data for 2024-25, stressing that it is provisional. This means it is “subject to year-end accounting and audit adjustments, which are still being processed”. Carbon Brief also received the final (i.e. non-provisional) figures for 2023-24, having been given the provisional figures last year.

(The provisional figures released to Carbon Brief in 2023-24 last year were significantly lower than the final figures – amounting to £1.8bn rather than £2.3bn. This is almost entirely due to the provisional data not factoring in most of the accounting methodology changes described in this article. The provisional figures for 2024-25 appear to have factored in these methodology changes already.)

The Department for Science, Innovation and Technology (DSIT) also oversees a small number of ICF projects overseas. Unlike the other departments, DSIT rejected Carbon Brief’s FOI requests. Carbon Brief understands that its projects were worth £42m in 2023-24, roughly 1% of the total. For the sake of this analysis, Carbon Brief assumes that this amount remained the same in 2024-25.

Carbon Brief relied on previous FOI results to calculate how much of the UK’s climate finance derives from accounting changes in recent years:

- BII: According to an internal document, under its old methodology, the government originally forecast 30% of BII core capital to be climate finance in 2024-25, amounting to £126m. The final figure provided to Carbon Brief, which is also based on a higher core capital figure, is £482m. If the government had counted 30% of the higher core capital contribution as ICF, under its old methodology, the total would be £264.3. This suggests the remaining £218m of the £482m could be attributed to the methodology changes.

- MDBs: The FOI results provided to Carbon Brief show contributions to the AfDB, ADB and CDB amounting to £103m.

- Humanitarian projects: Carbon Brief has used the estimates from an internal document showing how much climate finance the government expects humanitarian aid projects to provide, including £69m in 2024-25. This may be an underestimate, as some of the projects listed in this document have higher ICF totals in the new FOI data released to Carbon Brief.

- “Scrubbed” projects: The government also asked civil servants to reappraise the existing aid portfolio in order to identify any extra ICF that could be counted. Carbon Brief has obtained an incomplete list of these projects, which states that £138m was added to the 2024-25 total in this way.

Together, these changes add up to £528m. The actual figure may be higher, as these are provisional figures.

Carbon Brief’s estimate of the cumulative impact of the accounting changes by 2024-25 – some £1.3bn – aligns with an estimate of £1.72bn for the entire five-year period out to 2025-26, made by the Independent Commission for Aid Impact (ICAI). The final figure may be higher, as ICAI’s calculation was based on government documents that did not, for example, include the increased capital contribution to BII in 2024-25.

The post Analysis: UK climate aid to hit £11.6bn goal – but only due to accounting rule change appeared first on Carbon Brief.

Analysis: UK climate aid to hit £11.6bn goal – but only due to accounting rule change

Australia’s network of marine parks is the largest in the world, covering more than half (52%) of Australia’s Commonwealth waters. You could be forgiven for assuming that a marine park is much like a national park on land: a highly protected place where people can enjoy nature while conservation efforts help habitats recover and wildlife thrive. You wouldn’t expect someone to bulldoze a national park, so why should they be allowed to bottom trawl in a marine park?

The reality is that not all marine parks are equally protected. Australia’s Marine Parks Network is divided into different zoning categories, with each zone determining which activities are permitted and the level of protection provided.

More than half of the Commonwealth Marine Parks Network allows industrial activities like oil and gas mining, and industrial fishing.

Our survival, and the survival of our planet, depends on the ocean. The ocean produces more oxygen than all of our forests combined, sustains communities and regulates the earth’s temperature. It’s home to wondrous wildlife and important ecosystems like coral reefs and kelp forests.

We love our big blue backyard

Australia’s ocean is teeming with life that is found nowhere else on earth. Schools of colourful fish, vibrant coral reefs, endemic shark nurseries, pods of dolphins, families of whales, playful seal pups and threatened Jurassic-era turtles call Australian waters home.

Since time began, from the turquoise waves to the deep blue, the ocean has connected our shorelines and communities, fed us, guided us and grounded us. We are intrinsically connected to our big blue backyard – more than 85% of us live within 50km of the shoreline. For tens of thousands of years, people have lived in harmony with the ocean and the wildlife within it, caring for and being sustained by its rich waters. Australia’s waters are some of the most unique and abundant places on Earth but our Marine Parks Network is falling short to properly protect them.

Australia’s marine parks aren’t living up to their name

The Australian Commonwealth Marine Parks Network covers commonwealth waters 5.5km from the coast. The network is divided into 7 regional management areas, overall the network contains 60 marine parks. Zoning types determine what activities are allowed in each area. Over half of the network allows industrial activities, risking our most precious and threatened ocean wildlife.

Within many of our marine parks, destructive industries are allowed to fish, trawl, dig and mine using barbaric and cruel methods. Here are some of the zones explained:

- Bottom Trawling: Special Purpose (trawl) zones allow bottom trawling. This covers 10 marine parks totalling almost 13 million hectares. Bottom trawlers bulldoze the seafloor with weighted nets, deforesting our underwater forests; a cruel, indiscriminate and inefficient way to fish.

- Other Industrial Fishing: Includes “Habitat Protection Zones, ““Multi Use Zones” and “Special Purpose Zones.” Fishing methods vary from park to park but many marine parks in these zones allow industrial fishing like longlining. Longlining involves setting lines that can be 100km long, bristling with deadly hooks designed to catch a specific fish species. But longlining is not a selective method of fishing – significant numbers of sharks, rays, turtles, dolphins and seabirds can be harmed or killed as bycatch in the process.

- Oil and Gas Mining: Many “Special Purpose” and “Multi Use” zones allow seismic blasting and oil and gas mining. 30 marine parks or 65 million hectares of Australia’s highest conservation value areas for ocean wildlife are open for mining and exploration of oil and gas.

- Ocean Sanctuaries: National Park and Sanctuary zones are fully and highly protected marine parks designed to conserve wildlife and their habitat, where fishing, mining, and other industrial activities are not allowed.

Industrial fishing is one of the biggest threats to the ocean

")

In May, Greenpeace Australia Pacific sailed our campaigning vessel Oceania through some of Australia’s most beautiful and threatened marine parks. Our crew visited Jervis and Hunter marine parks to document their beauty, showcase what’s at risk and aim to expose the industrial fishing activities in these protected waters. Both of these marine parks allow bottom trawling and longlining methods of industrial fishing.

Industrial fishing is ripping the ocean apart across the planet. Longlining, also known as longline fishing, is an industrial fishing method that involves the use of a fishing line with thousands of baited hooks. These fishing lines can stretch over 100 kilometers in length and are set to capture a fish species, often tuna or billfish species. But it is not a selective method of fishing and often results in significant bycatch. This includes a range of non-target species like sharks, rays, sea turtles, marine mammals, and seabirds which are often injured or killed as bycatch.

Bottom trawling involves dragging heavy weighted nets along the ocean floor. This fishing method is popular with commercial fishing companies, because it makes it easy to catch large quantities of fish in one go. But it also damages the seafloor, releasing carbon and can kill or injure non-target ocean life like coral, fur seals, dolphins and seabirds. You may have watched the reality of bottom trawling (and the benefits of ocean sanctuaries) in Ocean with David Attenborough, if not, add it to your watch list!

Fully protected ocean sanctuaries that ban industrial fishing and mining can protect ocean wildlife and underwater wonderlands for generations to come. Vast, robust sanctuaries create blue havens where ocean wildlife are safe from nets and hooks, and can truly rest, recover, thrive and replenish out into the surrounding waters. Ocean sanctuaries ensure a healthy ocean full of life.

A once-in-a-decade chance to fix what’s falling short

We have a unique opportunity to turn the tide.

The Australian Government is asking for your feedback on how our Commonwealth Marine Parks Network is managed. This is our once-in-a-decade chance to protect ocean wildlife, ban industrial fishing and create more ocean sanctuaries.

As part of the review the Government is asking for submissions from the public to hear from you on what improvements are needed to better protect our vast network of marine parks. Writing a submission is a powerful way to influence government decisions and create real change.

This is the moment to ban industrial activities like bottom trawling and oil and gas mining. But only if they hear from YOU. Add your name!

Greenpeace is calling on the Australian government to:

1. Ban industrial activities from Australia’s Marine Parks Network: Ban industrial activities, such as industrial fishing, seismic blasting and oil and gas mining, from Australia’s marine parks.

2. Create more ocean sanctuaries: Increase fully protected sanctuaries in Australia’s marine parks based on science principles.

3. Connect Australia’s Marine Parks Network to the High Seas: mCreate seascape connectivity by linking Australian marine parks to new high seas ocean sanctuaries.

References

Substantiation that more than half of the Marine Parks Network permits industrial activity comes from a peer-reviewed systematic literature review (Phillips et al. 2025, PLOS One, https://doi.org/10.1371/journal.pone.0307324). The study found that within the Commonwealth Marine Parks Network specifically, “all zones are considered partially protected areas, meaning areas where extractive activities are permitted, except ‘Pink zones’ (Preservation Zones; IUCN Ia) and ‘Green Zones’ (IUCN II).” In other words, every Commonwealth marine park zone type other than the network’s strict no-take sanctuary and national park zones (IUCN Ia and II) permits some form of extractive industrial activity. Since no-take zones are the minority zone type across the network by area, this supports the conclusion that the majority of the network’s area is zoned to permit industrial activity.

DCCEEW Australian Marine Parks spatial dataset (https://fed.dcceew.gov.au/datasets/erin::australian-marine-parks/explore), filtered by zone type. This confirms that 38.43% of the network’s area is zoned as Sanctuary or National Park zones (IUCN Ia and II). These are the no-take categories excluded from the peer-reviewed study’s definition of partially protected/industrial-permitting zones. The remaining 61.57% of the network falls within the zone categories the study classifies as permitting industrial activity (per The MPA Guide definition of “industrial” applied in Phillips et al. 2025), directly corroborating the peer-reviewed finding with current Commonwealth-specific spatial data.

For further information on activities permitted within the Marine Parks Network Zoning, you can refer to the Management Plans zoning and rules for each Marine Parks Network area, for example: Temperate East, Coral Sea, North.

A new report from Greenpeace Australia Pacific advocates for the closure of bottom trawling in Australia’s Commonwealth Marine Parks Network. Bottom trawling continues to be a pervasive threat to ocean life in Australia, with 10 marine parks totalling almost 13 million hectares, allowing bottom trawling.

Australia’s network of marine parks, which is the biggest in the world, covers more than half (52%) of Australia’s Commonwealth domestic waters, but not all parks are created equal. Australia’s Marine Parks Network is divided into different zoning categories, with each zone determining which activities are permitted and the level of protection provided. More than half of the Marine Parks Network allow industrial activities like industrial fishing and oil and gas mining. This includes zoning types that allow destructive fishing by longliners and bottom trawlers, who pillage underwater wonderlands, rip up coral and indiscriminately and violently catch any animal in their path, including turtles, seals and dolphins, all within areas labelled a marine park.

The Federal government has commenced a review into the majority of Australia’s Commonwealth Marine Parks Network management plans. This presents an opportunity to ban industrial activities from our marine parks and create more ocean sanctuaries.

© Harriet Spark / Grumpy Turtle Film / Greenpeace

The banner drop is a distinctive part of the Greenpeace repertoire.

The moment of the unfolding is intrinsically dramatic. It is the reveal; when the moral and scientific truth of a situation is unveiled to the world. The wrong is being labelled—not through a written submission, or a social media post, or a statement in a meeting—but in words emblazoned in real physical space, chosen and occupied with precision, for all to see. There is jeopardy and transgression. And there are consequences—for the activists and for Greenpeace, as well as for the target of the communication. One of the reasons the banner remains such an effective tool in our toolbox is because of its undeniable clarity in cutting through, driving change and accountability in a way that few other tactics can. It is naming the wrong: in giant, clear letters.

We’ve hung these massive messages at environmental crime scenes, corporate headquarters, and iconic landmarks; on government buildings, ships and planes—in locations all around the world, for years.

My own memories unfurl even as I write this, but because the campaign to stop Woodside at Scott Reef is so pressing, what immediately springs to mind are two of our banners in that campaign: one on a crane outside their Perth HQ, and another on some of their corroding industrial junk at sea. What about you? Is there a particular banner that you picture when you think of Greenpeace?

The banners can attract global attention, but they have quiet beginnings. Each one is made by hand, often by volunteers. It is the invisible labour behind each spectacular public moment. One of the key pieces of equipment in our workshop at Rainbow Warrior House is the sewing machine. Sometimes our workshop is full of people and noise; at others it is quiet, the only sound being the gentle, purposeful, whir and buzz of a banner being sewn. It is usually our warehouse manager, Kieran Holmes, on the tools, head over the machine, carefully pouring over the raw canvas or tarp as the banner takes shape. Kieran’s one of those people who seems to be able to turn his hand to almost anything, but you wouldn’t know it because he’s old-school modest. In addition to being incredibly skilled, Kieran’s an all-round beaut human to have in the heart of our headquarters; never too busy to take the time to show a newcomer, or curious visitor, around his domain.

Once the banner is sewn up, the lettering needs to be outlined. This is done on a magnetic wall—a fit-for-purpose feature at Rainbow Warrior House, where the banner is held up with magnets, and the edges of the letters neatly traced from a projection.

Next comes the painting. It usually starts late in the afternoon, sometimes going into evenings and weekends, with volunteers, staff, mates crowded around, brushes in hand. It is a calming meditative feeling of shared purpose, giving each letter its visual heft, the colour building power and presence with each stroke.

Then you stand back, stretch, and look at the message, now ready.

S A V E S C O T T R E E F

Throughout history, every great push for social change has required some form of invisible labour; preparation in the form of quiet things seldom seen, but vital. It is the enabling work of love instantiated in action. And of course, so much of the time it has been women who have done this labour, so that the men could get the chance to make the speeches and stand on the podiums. The inaugural Greenpeace voyage to stop nuclear testing in 1971 had a male-only crew, but wouldn’t have happened without the ideas and work of women behind the scenes.

It is what we do together, after all, that changes the world. Sometimes that work happens on a stage, a ship on the wild seas, or up the side of a building. But mostly, it is the hidden diligence of those who care and contribute to all the enabling work that makes a change once thought impossible, inevitable. It is Kieran at his sewing machine. It was Dorothy Stowe doing the administrative work of the ‘Don’t Make A Wave Committee’ that became Greenpeace.

When we think of social change, it is the sturm and drang that we remember. The drop of the banner, the chant of the crowd, the raising of the new flag. But look behind the curtain, and there’ll be a crew of people who are taking responsibility for the administration, the sewing and the painting, making the food, checking the bus timetables, getting stuff done. And behind them are even more handsinvisibly donating time and trust; the financial, material and expert resources that make it all possible. There’s love, camaraderie and know-how at every stage.

We are social and cooperative creatures by nature. And we human beings have been stitching for millenia, sewing the possibilities of our common future. Political and corporate bullies and algorithmically manipulative platforms would have us forget this, and abandon who we are. But we should be in no doubt that the brighter prospects for ourselves and life on earth continue to be stitched and painted; collaboratively and with love, by the diligent hands of millions of people who care, each day, in every community and city across the world.

With Love,

David

Q & A

I always get great questions when interviewing prospective new team members. One that came up again recently was: “Is Greenpeace actually one organisation?”

Around the world, people know Greenpeace by our one global name, united by a shared mission: securing an Earth capable of nurturing life in all its magnificent diversity, with a particular focus on climate and biodiversity. Behind the scenes, though, we’re organised as a network of 25 legally autonomous national and regional offices, including Greenpeace Australia Pacific, working alongside Greenpeace International.

That structure gives us the best of both worlds: we work together leveraging the power of a global network on the issues that matter most, while each office remains legally independent and deeply connected to the communities, cultures and political realities where we’re embedded. Local knowledge informs global action, and global collaboration strengthens and supports local campaigns.

It’s a model that has enabled Greenpeace to take on some of the world’s biggest challenges for over five decades–while withstanding challenges and attacks from governments and corporations. Global enough to tackle global problems, local enough to understand our communities and the natural places we love.

If you’re curious to learn more, you can read about the Greenpeace Global Network structure here.

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy10 months ago

Renewable Energy10 months agoSending Progressive Philanthropist George Soros to Prison?

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits