Even the most hate-filled and stupid Americans are starting to realize that the United States is being led by a psychopath. If anything can serve as compelling evidence of this, the social media post below just may help to get the job done.

Even the most hate-filled and stupid Americans are starting to realize that the United States is being led by a psychopath. If anything can serve as compelling evidence of this, the social media post below just may help to get the job done.

Venezuela? The country colonized by the Spanish and French? The one that’s been independent for almost 200 years? There are elementary school kids all over the country asking, “WTF?”

Yes, we’re aware that Trump needs to distract us from the many criminal accusations against him, but does he really think this will fly?

The United States Needs a Little More Insanity. Could We Have it, Please?

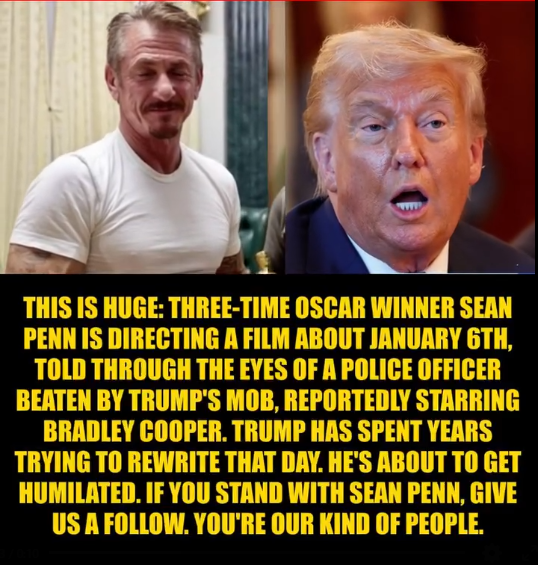

Can’t swear that this is true but hoping so.

Can’t swear that this is true but hoping so.

We must never forget.

The more visibility and the more frequent reminders we can get on this catastrophe in U.S. history the better.

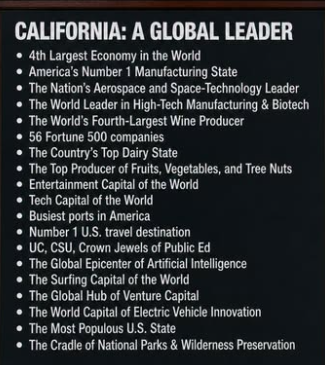

It’s almost funny when we hear that California is a socialist state, or a police state (due to our environmental restrictions), or that people are leaving in droves to go to Texas or Florida. When I come across people who say this, I wonder: have you ever actually been to California?

It’s almost funny when we hear that California is a socialist state, or a police state (due to our environmental restrictions), or that people are leaving in droves to go to Texas or Florida. When I come across people who say this, I wonder: have you ever actually been to California?

Do you know that the garden-variety 3 BR, 2 BA house here lists at about $1.2 million, where, if it were moved to, say, the Midwest, it would be worth perhaps $2500,000? Why do you think that could possibly be? Maybe the law of supply and demand doesn’t apply to the Marxist part of the nation?

Perhaps it’s because Californians are offered fantastic economic opportunities. We develop and implement ideas that improve the lives of everyone on Earth, and that we profit greatly from our undertakings.

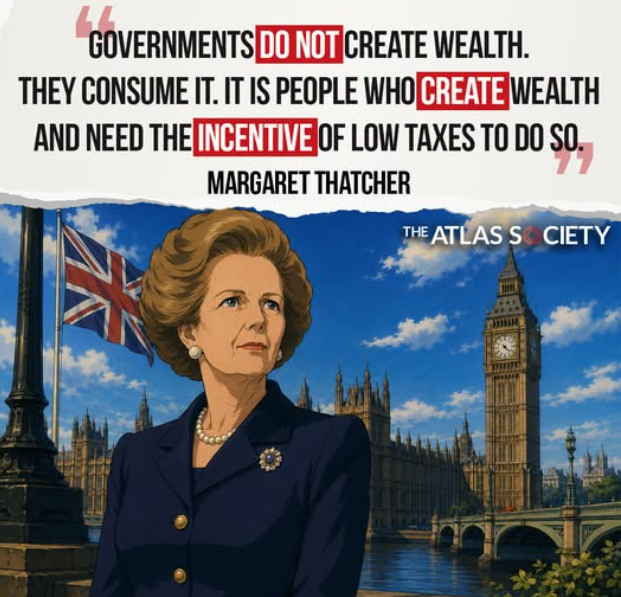

Something for the MAGA crowd to consider.

The main way governments create wealth is by educating people so that they can become productive members of society. They also build roads and airports and maintain law and order so that honest businesses can thrive.

The main way governments create wealth is by educating people so that they can become productive members of society. They also build roads and airports and maintain law and order so that honest businesses can thrive.

Anyone living now who believes that Elon Musk and Jeff Bezos are creating wealth for anyone but themselves is a total fool.

A ton of people bought into the concept expressed here in the mid-20th Century, but no semi-intelligent person today believes that tax breaks for billionaires/trillionaires generates a nickel for the common person.

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测