In this era of sustainability, the battery metals market plays a key role in the energy transition. Lithium, nickel, and cobalt drive demand for electric vehicles (EVs), renewable energy storage, and electronics. Now confining to lithium, its compounds namely lithium carbonate and lithium hydroxide power the battery cathodes for highly efficient storage.

Beyond batteries, lithium has diverse uses in glass, lubricants, ceramics, and pharmaceuticals. In 2025, the top battery-grade lithium producers are focusing on sustainability and making efforts to stabilize the supply chains to meet growing demand.

Lithium’s Contribution to Reduced Automotive Life Cycle Emissions

The industry is further transforming through mergers and partnerships, enhancing resource access and supply chains to meet global needs. However, challenges remain. Rising demand risks supply chain strain, stricter environmental rules push for greener practices, and most significantly the fluctuating prices affect profits.

To thrive in this turbulent market, these top producers are constantly innovating and collaborating, ensuring they overcome obstacles while driving the global energy shift. So who are the top lithium producers fueling the battery market in 2025? Find out…

1. Albemarle Corporation: The Lithium Powerhouse

Albemarle Corporation, with a market cap of $11.08 billion in January 2025, leads the lithium industry. Based in Charlotte, North Carolina, it plays a key role in the clean energy transition.

The company supplies lithium to major EV manufacturers worldwide. Its operations in Chile, Australia, and the U.S. make it a global leader. In Kings Mountain, North Carolina, Albemarle runs one of the world’s most advanced lithium facilities. This site focuses on cutting-edge technology and development, reinforcing its industry leadership.

Innovating for a Sustainable Future

Albemarle leads in innovation with technologies like lithium sulfide and ultra-thin lithium anodes. These advancements increase energy density, reduce battery weight, and extend EV range. The company has invested heavily in new facilities to boost lithium hydroxide production, essential for EV batteries.

Collaborations with Tesla and General Motors highlight Albemarle’s role in the EV ecosystem. The company is committed to sustainability, and reducing carbon emissions during lithium production. These efforts align with global green energy goals and reinforce Albemarle’s industry leadership.

Albemarle’s focus on innovation and sustainability keeps it ahead in the growing lithium market. As the world shifts to cleaner energy, Albemarle ensures it remains a key player in powering the future.

2. Sociedad Química y Minera de Chile (SQM): A Lithium Giant with a Sustainable Focus

As of January 2025, Sociedad Química y Minera (SQM) boasts a market cap of $11.04 billion, solidifying its position as one of the largest lithium producers globally. The Chilean company leverages the country’s vast lithium reserves in the Atacama Desert. SQM plays a pivotal role in the global lithium supply chain with its vertically integrated operations and cost-efficient production methods,

The company sources raw materials like brine and caliche from its operations in Chile’s Salar de Atacama. This brine is used to produce key battery materials such as lithium carbonate, potassium chloride, and potassium sulfate.

S&P Global reported SQM is ramping up production to meet surging demand, with plans to reach 230,000 metric tons of lithium in 2025.

Expansion efforts in Australia, Chile, and China, including a new conversion plant in China, underpin this growth. Despite declining lithium prices, SQM remains optimistic, driven by a projected 20% increase in global lithium demand, especially from electric vehicle (EV) markets in China.

Sustainability and Strategic Partnerships

SQM is committed to sustainable practices to lower brine extraction rates and integrate renewable energy into its operations. The company also engages local communities, promoting social well-being while minimizing its environmental impact.

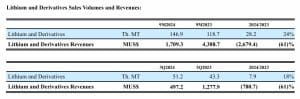

Strategic partnerships further bolster SQM’s market position. Agreements with LG Energy Solution and SK On enhance its role in the EV supply chain and ensure steady demand for its lithium. Additionally, lithium and its derivatives now contribute 79% of SQM’s gross margin, highlighting their significance in the company’s portfolio.

SQM aligns with global sustainability goals and meets the growing need for battery metals by focusing on “Green Lithium” production and investing in innovative technologies.

3. Ganfeng Lithium: China’s Lithium Leader

As of January 2025, Ganfeng Lithium, headquartered in Jiangxi, China, has a market cap of HKD 64.83 billion. As one of the world’s largest lithium producers, Ganfeng has a robust supply chain that supports competitive pricing and high production volumes.

The company supplies premium lithium hydroxide products to leading lithium battery and EV manufacturers, earning its reputation for technological excellence and reliable quality.

Sustainably Sourcing Lithium

Notably, EVs using Ganfeng’s lithium salt products traveled over 129 billion kilometers between 2015 and 2022. This achievement reduced CO2 emissions by 32.26 million tons which aligned with the environmental benefits of EV adoption.

Furthermore, Ganfeng’s lithium batteries play a crucial role in energy storage. They store solar and wind energy, ensuring renewable energy is reliable and accessible. By reducing the reliance on fossil fuels, these batteries help lower carbon emissions and support global clean energy goals.

The company’s sustainability goals revolve around battery recycling which is a critical part of the EV supply chain. The company’s recycling projects recover valuable materials like lithium, nickel, cobalt, and manganese from retired batteries.

These efforts reduce resource waste and support the transition to renewable energy. Ganfeng’s lithium batteries are also used in energy storage systems, helping store solar and wind energy while cutting fossil fuel usage and lowering carbon emissions.

Lithium Capacity Boost by 2025

However, the company faces challenges as its production capacity has outpaced project development. To address this, Ganfeng plans to boost its annual lithium compounds capacity to 300,000 tonnes LCE by 2025, aiming for 70% self-sufficiency.

Ganfeng also announced last year a joint feasibility study with Pilbara Minerals Limited highlights to expand its lithium production. Its innovation in recycling and its dominance in China’s lithium market make it a key player in the global clean energy transition.

4. Tianqi Lithium: An Expanding Global Player

With a market cap of 49.33 billion CNY, Tianqi Lithium stands out as a major force in the lithium industry. The company has a strong presence in China and Australia, thanks to its joint venture with Albemarle at the Greenbushes lithium mine. This mine, located in Western Australia, is one of the largest and highest-grade lithium resources globally.

High-Quality Resources

Tianqi relies on top-tier lithium resources to drive its business. The Greenbushes mine and the Cuola mine in Sichuan ensure a stable, cost-effective supply of high-quality lithium raw materials. This stability enhances efficiency, flexibility, and reliability in Tianqi’s downstream chemical production.

Notably, the Greenbushes mine, managed through Talison Lithium, has been in operation for over 30 years. Recent expansions have boosted its annual production capacity to 1.62 million tonnes of lithium concentrate, cementing its critical role in the global market.

Strategic Investments for Growth

Tianqi is investing heavily in downstream processing, including lithium hydroxide facilities. These efforts aim to add value to the battery supply chain and meet surging demand for premium lithium products. With its strategic partnerships and focus on innovation, Tianqi is well-positioned for growth in the competitive battery metals market.

5. Mineral Resources: Australia’s Rising Star

With a market cap of A$7.28 billion, Mineral Resources Limited (MinRes) is a top diversified resources company headquartered in Perth, Australia. Its operations span lithium, iron ore, energy, and mining services across Western Australia, making it a major player in the mining industry.

World-Class Lithium Assets

MinRes manages some of the world’s most prominent lithium projects, including the Wodgina and Mount Marion mines. The Wodgina mine, one of the largest known hard rock lithium deposits, is a joint venture with Albemarle Corporation, with MinRes overseeing all mining activities. It includes a spodumene concentrate processing plant with an annual capacity of 900,000 tonnes (SC5.5).

Mount Marion, another key operation, produces up to 600,000 tonnes (SC6 equivalent) of spodumene concentrate annually. This project is co-owned with Jiangxi Ganfeng Lithium. The spodumene is transported to the Port of Esperance for export, serving global markets.

Expanding Operations and Sustainability

MinRes acquired the Bald Hill mine in 2023, boosting production by adding 150,000 tonnes (SC6 equivalent) of spodumene annually. Located near Mount Marion, this site leverages shared infrastructure.

Apart from supporting decarbonization, MinRes Australian operations add strategic value to global supply chains.

Recent cuts in lithium investments and project expansions may lead to supply shortages. Albemarle predicts that these constraints could disrupt the market in the mid-term, emphasizing the need for increased production and sustainable sourcing.

However, as the energy transition accelerates, the role of these battery-grade lithium producers will become even more critical to stabilize the lithium market.

________________________________________________________________________

Li-FT Power: Exploring & Developing Hard Rock Lithium Deposits in Canada

Li-FT Power Ltd. (TSXV: LIFT) recently announced its first-ever National Instrument 43-101 (NI 43-101) compliant mineral resource estimate (MRE) for the Yellowknife Lithium Project (YLP), located in the Northwest Territories, Canada.

An Initial Mineral Resource of 50.4 Million Tonnes at Yellowknife.

This maiden estimate is a major milestone for the company and marks a significant step forward in the project’s development. Li-FT Power’s upcoming mineral resource is expected to further solidify Yellowknife as one of North America’s largest hardrock lithium resources.

Click to Learn More about Lithium and Li-FT Power Ltd. >>

The post Top 5 Lithium Producers Powering the Battery Market in 2025 appeared first on Carbon Credits.

What replaced the cheap REDD credit on the boardroom slide deck, and why procurement is leading the rewrite.

Three years ago, a corporate slide showing a portfolio of cheap REDD+ credits could carry a board meeting. The number was big, the price was low, and the press release wrote itself. Today, that same slide gets sent back with questions. The questions are uncomfortable, the answers are unclear, and your general counsel is suddenly in the room.

Conventional carbon offsets are not dead. The voluntary carbon market retired 202 million tonnes in 2025, and the Morgan Stanley Institute for Sustainable Investing survey published in January 2026 confirmed that interest from corporate buyers remains substantial. What changed is the credibility threshold. The integrity floor has risen, the disclosure scrutiny has tightened, and the buyer profile has shifted. This article tracks what changed, what sophisticated buyers now ask before signing, and what serious corporates are putting on the board slide instead.

What boards used to buy, and why it stopped working

The 2020 to 2022 model was simple: buy a large tranche of avoidance credits at low single-digit prices, retire them against the company footprint, announce the carbon-neutral claim, and move on. Most of those credits came from REDD+ projects, renewable energy installations in countries where the renewable energy was already economic, or methane projects with thin documentation.

Several things broke that model. Academic research published in 2023, including a widely cited Science paper, found that the majority of REDD+ credits issued under the most common methodologies did not represent additional reductions when tested against rigorous counterfactuals. The Voluntary Carbon Markets Integrity Initiative published its Claims Code of Practice, which sets requirements for what companies can credibly claim from credit use. The European Union finalised its Green Claims Directive, restricting how companies can describe products as climate-neutral. France’s Décret 2022-539 already restricts carbon neutrality advertising. California’s AB 1305 imposes disclosure requirements on any company making net-zero or carbon-neutral claims while doing business in the state.

The collective effect: the cheap credit no longer buys the announcement, and the announcement now carries litigation risk.

The integrity reset: ICVCM, VCMI, and what changed

The Integrity Council for the Voluntary Carbon Market published the Core Carbon Principles in 2023 and began assessing methodologies against them in 2024. The first methodologies received the CCP label later that year. The point of the label is to give corporate buyers a defensible quality screen they can cite in disclosure.

The Voluntary Carbon Markets Integrity Initiative complements this on the demand side. Its Claims Code of Practice defines what a buyer can say (Silver, Gold, or Platinum claims, with associated requirements) based on the quality of credits used and the underlying decarbonisation strategy. Together, CCP and VCMI build a quality stack: CCP on the supply, VCMI on the claim, with the science-based target sitting underneath both.

The reset is not a ban on offsets. It is a ratchet. Credits that meet the new bar continue to clear; credits that do not, do not. The Morgan Stanley survey found that 61% of current buyers like the CCP label concept but that supply of labelled credits remains limited. That supply constraint is now visible in pricing.

What sophisticated buyers ask before they sign

The questions on the procurement scorecard have changed. A 2022 buyer might have asked about price, vintage, and project type. A 2026 buyer asks five different questions before any of those.

- What does the counterfactual look like, and who validated it.

- What is the permanence regime, and what is the buffer pool exposure.

- What is the leakage risk, and how is it mitigated.

- What rating has the project received from the independent ratings agencies (Sylvera, BeZero, Calyx Global), and what was the rationale.

- What is the documentation discipline that survives an audit four years from now when the procurement team that signed the contract has moved on.

If the vendor cannot answer those five questions on a first call, the conversation ends. Conversely, if the vendor can answer them with documented specificity, the conversation often expands beyond a single transaction toward a multi-year engagement.

Where this leaves your near-term commitments

You probably have near-term commitments that pre-date the integrity reset. Public targets to be carbon neutral by 2025 or 2030. Product-level claims that ran in last year’s marketing. Disclosed reduction trajectories that assumed continued access to cheap credits.

You have three workable paths. The first is to re-baseline your strategy, replacing the most exposed credits with higher-quality alternatives and adjusting the public language to match what you can defend. The second is to shift the underlying spend from offsetting outside your value chain to investing inside your value chain, where reductions count against Scope 3 directly and the audit trail is cleaner. The third is to keep the strategy and absorb the risk, which is increasingly the most expensive option once you price in litigation, restatement, and reputational exposure.

Most serious buyers are choosing the second path. It moves the carbon spend from a compliance cost to a procurement and resilience investment, and it removes the central failure point of the legacy model: the disconnect between where the emissions occurred and where the reductions sat. Nature-based supply chain investments, structured under the GHG Protocol Land Sector and Removals Standard and aligned to the SBTi FLAG Guidance, are the asset class that fits this brief. They generate inventory-grade reductions, they produce audit-grade documentation, and they survive the new claim restrictions because the carbon math sits inside the value chain that the disclosure already covers.

If you are reassessing a carbon strategy under the new integrity bar, or rebuilding a board narrative that has to survive a more skeptical audience, the carbon and sustainability experts at Carbon Credit Capital can help. The Dual-Value Model gives you a defensible alternative to legacy offset purchases, with the documentation and operational integration that survives the procurement scorecard and the audit. Schedule a consultation.

The World’s Biggest Game Is Coming

Every four years, the world stops to watch football. Billions of fans tune in, millions travel, and for a few glorious weeks the sport unites people across language, culture, and geography in ways almost nothing else can.

The 2026 FIFA World Cup is set to be the most ambitious tournament in the history of the sport. For the first time ever, 48 national teams will compete across 16 host cities in three countries: the United States, Canada, and Mexico. From Atlanta to Toronto, from Guadalajara to New York, the tournament will span an entire continent and draw an estimated five to six million visitors.

That scale is extraordinary. It is also an invitation.

When an event this large takes shape, its environmental footprint grows alongside it. More teams mean more matches. More host cities mean more travel. More fans mean more flights, more hotel stays, more food, and more waste. But scale also means influence, and that is exactly where the opportunity lies.

The 2026 World Cup arrives at a moment when awareness of climate responsibility is higher than it has ever been. Fans, sponsors, cities, and governing bodies are increasingly asking: how do we celebrate something we love while taking better care of the planet we share? The good news is that the answer is not about sacrifice. It is about small, intentional choices made by millions of people acting together.

This article breaks down the environmental footprint of the tournament, explains what FIFA and host cities are doing to reduce it, and offers practical ways for every fan to participate in something bigger than the beautiful game itself.

What Is the Environmental Impact of the 2026 FIFA World Cup?

Quick Answer: The 2026 FIFA World Cup will generate greenhouse gas emissions through international and domestic air travel, ground transportation, hotel stays, stadium operations, food and beverage consumption, and event logistics. Fan travel, especially long-haul flights, typically represents the largest share of a major sporting event’s total carbon footprint.

A tournament the size of the World Cup generates emissions across nearly every category of human activity. Understanding where those emissions come from is the first step toward reducing them.

The primary sources of World Cup emissions include:

- International flights: Fans traveling from Europe, Asia, South America, Africa, and beyond generate significant aviation emissions. Long-haul flights are among the most carbon-intensive activities an individual can undertake.

- Domestic flights: With 16 host cities spread across three countries, fans attending multiple matches will likely fly between venues within North America.

- Ground transportation: Rental cars, taxis, rideshares, and buses connecting airports to stadiums and hotels all add to the overall footprint.

- Hotel stays: Millions of nights of lodging consume electricity, water, and heating and cooling energy at scale.

- Stadium operations: Lighting, cooling, sound systems, and food service at each venue require significant energy.

- Food and beverage: Catering at scale, with meat-heavy menus and single-use packaging, contributes both direct emissions and substantial waste.

- Event logistics: Equipment transport, broadcasting infrastructure, and official travel all factor in.

No single estimate exists yet for the 2026 tournament’s total footprint, but context from past events is instructive. FIFA’s own sustainability reports acknowledge that major tournaments generate hundreds of thousands to millions of metric tons of CO2-equivalent emissions when fan travel is included. The 2022 FIFA World Cup in Qatar drew considerable scrutiny for its construction-related emissions and for the long-haul flights required to reach a single Middle Eastern host nation.

The 2026 tournament’s multi-country, multi-city format presents different challenges and, importantly, different opportunities.

Why Sports Matter in the Fight Against Climate Change

Quick Answer: Global sporting events like the World Cup reach billions of people and have a unique power to inspire behavior change at scale. That makes them one of the most important platforms for communicating and normalizing climate-conscious choices.

Sport occupies a rare space in public life. It commands attention from people who may not read policy papers, follow environmental news, or consider themselves particularly engaged with climate issues. A single World Cup final draws a television audience measured in the hundreds of millions. That kind of reach is genuinely extraordinary.

The United Nations Sports for Climate Action Framework, launched in 2018, recognizes this explicitly. The framework calls on sports organizations to use their platforms to raise awareness, reduce their own emissions, and inspire broader action among fans and communities. As of 2024, more than 300 sports organizations have signed on, including national football associations and major leagues across multiple disciplines.

When sports organizations commit to climate action, they do not just reduce their own footprint. They send a signal to fans, sponsors, broadcasters, and host cities that sustainability is a shared priority. When a stadium installs solar panels, it normalizes renewable energy. When a league actively promotes public transit, it makes that choice feel obvious rather than inconvenient. When a tournament takes accountability for its unavoidable emissions, it shows that responsibility is possible even at enormous scale.

The 2026 World Cup has the potential to reach more people with that message than almost any other platform on earth.

Why Transportation Is the Largest Source of Emissions

Quick Answer: Transportation, especially aviation, typically accounts for the majority of a major sporting event’s total carbon footprint. It involves millions of individuals making high-emission journeys that are genuinely difficult to avoid or replace with lower-carbon alternatives today.

When sustainability researchers analyze the footprint of a mega sporting event, one category consistently dominates: how people get there.

Aviation is among the most carbon-intensive modes of travel per mile. A single round-trip transatlantic flight, say from London to New York, generates roughly 1 to 1.5 metric tons of CO2-equivalent per passenger depending on the aircraft, seat class, and routing. For a fan flying from Buenos Aires or Tokyo, that figure climbs considerably higher.

The 2026 World Cup will draw fans from every continent. Many will travel internationally. Some will attend matches in multiple cities and need additional domestic flights between venues. Ground transportation adds further emissions once fans arrive at each destination.

Hotels come in as the second major source. With millions of visitors needing accommodation across dozens of cities over several weeks, the aggregate energy consumption of lodging is substantial.

This concentration of travel-related emissions is why transportation is the category most often targeted by sustainability strategies at major events. It is also the area where individual fan choices can have the most meaningful real-world impact.

Existing Stadiums Help Reduce Environmental Impact

Quick Answer: Most 2026 World Cup venues are existing stadiums, which significantly reduces the construction-related emissions that have contributed to the environmental footprint of past tournaments.

One of the most meaningful and often underappreciated sustainability advantages of the 2026 World Cup is the decision to use venues that are largely already built.

Stadium construction is enormously carbon-intensive. Concrete, steel, and the energy required to assemble them at scale contribute millions of metric tons of emissions before a single match is played. Using existing infrastructure eliminates that category of impact from the outset.

Many 2026 host venues, including AT&T Stadium in Arlington, MetLife Stadium in New Jersey, Levi’s Stadium in Santa Clara, and SoFi Stadium in Los Angeles, are large, established facilities with existing transportation connections, utilities, and operational infrastructure. Similar existing stadiums anchor the schedule in Canada and Mexico.

Host cities are also using the tournament as an opportunity to invest in improvements that will benefit communities long after the final whistle:

- Public transit expansions: Several host cities are upgrading rail and bus infrastructure to handle increased tournament traffic. Those improvements will remain useful to residents for decades.

- Renewable energy integration: Some venues are increasing their use of solar, wind, and other clean energy sources in preparation for the event.

- Waste diversion programs: Enhanced composting, recycling, and single-use plastic reduction efforts are being built into venue operations.

- Water conservation: Stadiums in drier climates are adopting more efficient irrigation and water management systems.

None of this erases the footprint of the event entirely. But it does mean the 2026 World Cup is starting from a more sustainable foundation than tournaments that required massive new construction.

FIFA’s Sustainability Strategy

Quick Answer: FIFA has developed a Sustainability and Human Rights Strategy that includes environmental commitments around emissions reduction, responsible sourcing, and legacy planning for host communities. Independent oversight and third-party verification remain important to ensuring those commitments translate into real outcomes.

FIFA’s approach to sustainability has evolved meaningfully over the past decade. The organization’s current Sustainability and Human Rights Strategy covers several interconnected areas.

On the environmental side, FIFA has committed to reducing greenhouse gas emissions across its operations, promoting sustainable venue management, and encouraging host nations to integrate sustainability into their planning. The strategy also addresses responsible procurement, supply chain transparency, and waste reduction.

Legacy planning sits at the center of the framework. FIFA works with host cities and nations to ensure that infrastructure investments, community programs, and environmental improvements outlast the tournament itself. The goal is that hosting the World Cup leaves communities measurably better off, with improved transit, upgraded facilities, and stronger environmental standards.

It is worth noting that large international sports organizations operate under significant public scrutiny, and sustainability commitments are most meaningful when supported by independent verification and transparent reporting. Fans and stakeholders are right to ask for accountability alongside ambition.

For the full details of FIFA’s approach, readers can consult the official FIFA Sustainability and Human Rights Strategy and the associated FIFA World Cup 26 sustainability documentation.

How Fans Can Reduce Their Carbon Footprint

Quick Answer: Fans attending or following the 2026 World Cup can reduce their environmental impact by choosing lower-carbon transportation, staying in sustainable accommodations, reducing waste at venues, and offsetting unavoidable emissions through verified carbon offset programs.

The most powerful lever in World Cup sustainability is not a stadium design or a transit system. It is the combined weight of millions of individual choices made by fans who care.

Here is a practical guide to making yours count:

Getting There

- Choose direct flights when possible. Takeoffs and landings are the most fuel-intensive parts of any flight, so fewer of them means less fuel burned.

- Consider train travel for shorter distances between host cities, particularly in the U.S. Northeast corridor or within Mexico.

- Use public transit from the airport to your hotel and to the stadium. Most host cities have rail and bus connections to venues, and several are expanding those networks specifically for the tournament.

- If you need to rent a car, opt for an electric or hybrid vehicle.

- Share rides with other fans when driving is unavoidable.

At the Hotel

- Book accommodations that have earned recognized green certifications. Look for LEED, Green Key, or similar credentials as a starting point.

- Reuse towels and linens, take shorter showers, and turn off lights and air conditioning when you leave the room.

- Choose hotels within walking or transit distance of the stadium rather than driving in from farther away.

At the Match

- Bring a reusable water bottle. Many venues will have refill stations available.

- Choose plant-based food options when they are available. Food production is a meaningful contributor to greenhouse gas emissions, and the menu choices of millions of fans add up.

- Use the designated recycling and composting bins at the venue.

- Skip single-use plastics wherever an alternative is offered.

Supporting Local Communities

- Eat at locally owned restaurants rather than large international chains. This keeps economic benefits inside the host community and typically means shorter, less emissions-heavy food supply chains.

- Buy souvenirs from local artisans and makers.

- Be a thoughtful guest in every host city you visit.

Offsetting What You Cannot Eliminate

- Calculate your travel emissions using the Terrapass Carbon Footprint Calculator and balance the portion of your footprint you could not reduce by purchasing carbon credits that support verified climate projects.

What Are Carbon Credits?

Quick Answer: Climate projects are basically carbon reduction factories. They generate one carbon credit every time they reduce or remove one metric ton of CO2-equivalent (CO2e) greenhouse gas emissions from the atmosphere. Individuals and organizations can compensate for their own emissions by purchasing an equivalent amount of carbon credits that fund projects for reducing CO2e.

Carbon offsetting works by balancing the emissions generated in one place with emissions reduced by climate projects somewhere else. When you purchase a carbon credit, you are funding projects that restore and protect nature, accelerate decarbonization, and remove carbon from the atmosphere.

Common types of carbon projects include:

- Forestry and land conservation: Protecting and restoring forests that would otherwise be logged prevents the release of the carbon stored in trees and soil.

- Renewable energy: Projects that build wind, solar, or small hydro capacity in regions that would otherwise rely on coal or other fossil fuels.

- Methane capture: Methane is known as a climate super-pollutant. Capturing methane from landfills, orphaned oil wells, or agricultural operations prevents a particularly potent greenhouse gas from reaching the atmosphere.

- Regenerative agriculture: Farming practices that sequester carbon in soil while improving overall ecosystem health.

Not all carbon credits are created equal, and that distinction matters. High-integrity carbon credits are generated by projects that operate on carbon credit registries like the American Carbon Registry, Climate Action Reserve, Verra, and the Gold Standard which have been approved by the Integrity Council for Voluntary Carbon Markets (ICVCM) for rigorous governance, tracking, transparency, and no double-counting. All carbon credits from these projects go through independent third-party verification to ensure that the emissions reductions claimed by a project are real, measurable, additional (meaning they would not have happened without the carbon credit funding), and permanent.

Carbon offsetting works best as a complement to emission reductions, not a substitute for them. The goal is always to reduce first, then offset what cannot be avoided. You can learn more in the Terrapass Guide to Carbon Credits.

Why Carbon Offsetting Make Sense for World Cup Travel

Quick Answer: Many of the emissions generated by World Cup travel, particularly long-haul international flights, cannot currently be eliminated with available technology. Carbon offsetting give fans a practical way to take responsibility for those unavoidable emissions while supporting verified climate projects around the world.

Aviation remains one of the most difficult sectors to decarbonize. Sustainable aviation fuel exists and is growing, but it currently accounts for a small fraction of global fuel supply and comes at a significant price premium. Electric long-haul aircraft are still years away from commercial viability. For most fans, flying to the World Cup means generating emissions that cannot yet be avoided through any other realistic means.

This is precisely the situation carbon offsetting is designed to address.

By calculating the emissions from your flights, hotel stays, and ground transportation, you can take meaningful financial responsibility for that footprint today, while the world works toward the technologies and systems that will eventually make low-carbon travel universally accessible.

Terrapass makes this process straightforward. The company has been helping individuals and businesses calculate and offset their carbon footprints for more than 20 years, funding verified projects in forestry, renewable energy, methane capture, and other categories. For fans planning to attend the 2026 World Cup, the Terrapass Flight Carbon Calculator provides a clear estimate of travel emissions and purchasing personal carbon offsets takes only a few minutes.

This is not about guilt or restriction. It is about celebrating the sport you love while acknowledging that our choices have consequences, and then actually doing something about it.

The Lasting Legacy of Sustainable Sporting Events

Quick Answer: When sporting events invest in sustainability, the benefits extend well beyond the tournament itself. Infrastructure improvements, cleaner energy systems, stronger transit networks, and community investments all create lasting value for host cities and the people who live in them.

The 2026 World Cup will end. The infrastructure, habits, and standards it helps establish will not.

Host cities that expand their public transit systems for the tournament will keep those systems running after the last match. Stadiums that invest in renewable energy and efficient operations will benefit from lower costs and reduced emissions for years. Communities that build composting and waste diversion programs during the event have the framework to sustain them long afterward.

This is what legacy planning means in practical sustainability terms. The most successful sporting events do not just minimize harm. They leave behind something genuinely valuable.

The tournament also has the potential to accelerate the normalization of sustainable behavior among millions of fans. When people experience public transit that actually works, venues that make recycling easy, and hotels that back up their environmental commitments with real action, those experiences reshape expectations. Fans carry those expectations home with them and apply them to their daily lives.

Climate action at scale is not driven only by policy. It is driven by cultural change, by enough people deciding that this is simply how things are done now. A World Cup can contribute to that shift in ways that are hard to quantify but easy to recognize when you see them.

Sustainable Travel Checklist

Use this as your personal guide for the 2026 World Cup:

Before You Go

- Calculate your travel emissions using the Terrapass Carbon Footprint Calculator

- Purchase verified carbon offsets for your flights and other travel

- Book accommodations with recognized green certifications

- Research public transit options at each host city you plan to visit

- Pack a reusable water bottle, travel mug, and shopping bag

Getting There

- Choose direct flights to reduce fuel burn from multiple takeoffs and landings

- Consider train travel for shorter routes between host cities

- Use public transit from the airport rather than renting a car

- If renting, select an electric or hybrid vehicle

During the Tournament

- Use public transit or walk to the stadium

- Fill your reusable bottle at stadium refill stations

- Sort waste into the correct recycling and composting bins

- Explore plant-based food options at the venue

- Eat at locally owned restaurants

- Buy local souvenirs to support host community economies

- Respect local environmental regulations and natural spaces

When You Get Home

- Share your experience and the sustainable choices you made with friends and family

- Keep the habits you built during the tournament going

- Consider a home energy audit or a renewable energy subscription

Did You Know? Sustainability Facts Worth Sharing

Fact 1: The United Nations Sports for Climate Action Framework has more than 300 signatories from the global sports community, including leagues, clubs, national associations, and event organizers all committed to reducing sports-related emissions.

Fact 2: Reusing existing stadiums avoids the construction-related carbon emissions that have been one of the most criticized aspects of past World Cups and Olympic Games. Building a new stadium can generate hundreds of thousands of metric tons of CO2-equivalent before a single match is played.

Fact 3: A single round-trip transatlantic flight can generate roughly as much CO2-equivalent per passenger as several months of average home energy use, which is why aviation is such an important focus for anyone thinking seriously about their personal carbon footprint.

Fact 4: Verified carbon projects often generate benefits beyond emissions reductions, including biodiversity protection, community employment, cleaner water, and improved public health in project communities.

Fact 5: The 2026 FIFA World Cup will be the first ever to feature 48 teams, meaning the number of matches and participating nations will be larger than at any previous tournament in the sport’s history.

Fact 6: Plant-based food options generate significantly lower greenhouse gas emissions per serving than beef or lamb on average, making menu choices at stadiums a surprisingly meaningful sustainability decision when multiplied across millions of meals.

Fact 7: Renewable Energy Certificates (RECs) allow individuals and businesses to match their electricity consumption with verified renewable energy generation, making it possible to support clean energy even when your local grid still relies on fossil fuels.

Every Goal Counts On and Off the Field

The 2026 FIFA World Cup is going to be extraordinary. Forty-eight teams. Sixteen cities. Three countries. The greatest players in the world are competing for the most coveted prize in sport. Billions of people watching.

It is also a moment.

Moments like this are rare. Occasions when the whole world is paying attention at the same time, when shared experience opens the door to shared action. The players on the pitch will give everything for 90 minutes. Fans in the stands and at home can give something too.

Not perfection. Not sacrifice. Just intention.

Choosing a direct flight. Riding the subway to the stadium. Filling a reusable bottle. Eating a plant-based meal. Staying somewhere that has earned its green credentials. Offsetting the emissions from your journey before you even board the plane.

None of these things are dramatic on its own. Together, across millions of fans in 2026, they add up to something significant.

Terrapass has spent more than 20 years making it easy for people to take genuine responsibility for their carbon footprint. Whether you are attending matches in person, hosting viewing parties, or following the tournament from afar, there are meaningful ways to reduce your impact and offset what you cannot yet eliminate.

Calculate your World Cup travel footprint and offset your emissions at Terrapass.com.

The world is watching. Let’s make this one count.

Frequently Asked Questions

What is the environmental impact of the FIFA World Cup?

The FIFA World Cup generates greenhouse gas emissions across several categories: international and domestic air travel, ground transportation, hotel stays, stadium operations, food service, and event logistics. Fan travel, particularly long-haul flights, typically represents the largest share of total emissions for a sporting event at this scale. The 2026 tournament spans three countries and 16 host cities, making transportation planning especially important for fans who want to minimize their footprint. While exact projections for 2026 are not yet finalized, past tournaments have generated hundreds of thousands of metric tons of CO2-equivalent.

Why does air travel create so many emissions?

Aircraft burn large quantities of jet fuel during flights, releasing CO2 and other climate-warming compounds. Unlike ground vehicles, which can be electrified relatively quickly, long-haul aircraft have very few low-carbon alternatives available on a commercial scale today. Sustainable aviation fuel exists but currently makes up a small fraction of global supply. A single round-trip transatlantic flight can generate roughly 1 to 1.5 metric tons of CO2-equivalent per passenger, comparable to several months of home energy use. Flying in a higher class or on older, less fuel-efficient aircraft increases emissions further.

Are existing stadiums better for the environment?

Generally speaking, yes. Constructing a new stadium requires enormous quantities of concrete, steel, and other materials, all of which carry substantial embedded carbon emissions. Using existing venues avoids those construction-related emissions entirely. The 2026 World Cup benefits significantly from this approach, as most venues, including major NFL and MLS stadiums across the U.S., are already built and operational. This does not eliminate the event’s footprint, but it removes one of the most carbon-intensive categories that has drawn criticism at past tournaments and Olympic Games.

How can I travel more sustainably to the World Cup?

Sustainable travel starts before you leave home. Choose direct flights when possible, since takeoffs and landings are the most fuel-intensive phases of any flight. Use public transit from airports to hotels and stadiums rather than renting a car. If a car is necessary, choose an electric or hybrid option. Book accommodations with recognized environmental certifications. Pack reusable bags, bottles, and utensils. And calculate your unavoidable travel emissions with the Terrapass Flight Carbon Calculator so you can offset them through a verified program before you depart.

What are carbon credits?

Carbon credits are verified units representing the reduction or removal of one metric ton of CO2-equivalent greenhouse gas emissions. When you purchase carbon credits, you fund projects that prevent greenhouse gases from entering the atmosphere, such as protecting forests, building renewable energy capacity, or capturing methane from landfills. High-integrity carbon credits are independently verified under recognized standards organizations, ensuring the emissions reductions claimed are real, measurable, additional, and permanent. Carbon credits work best when used to compensate for emissions that cannot currently be eliminated, not as a substitute for actually reducing your footprint.

Should I offset my flight?

If you are flying to attend the 2026 World Cup, offsetting your flight emissions is one of the most practical and immediate steps available to you. Aviation is among the most carbon-intensive activities most individuals engage in, and the technology to eliminate those emissions on a commercial scale does not yet exist. By calculating your flight’s emissions and purchasing verified carbon credits, you take direct financial responsibility for that footprint and fund climate projects that make a measurable difference. It is not a perfect solution, but meaningful steps taken by millions of people are how real progress gets made. Use the Terrapass Flight Carbon Calculator to get started.

How can fans reduce their carbon footprint at the World Cup?

Fans can reduce their carbon footprint through choices made at every stage of the trip: flying direct, using public transit, staying in sustainable hotels, bringing reusable water bottles, choosing plant-based food options at the venue, sorting waste properly, supporting local businesses, and offsetting unavoidable travel emissions before departure. No single action eliminates a fan’s footprint entirely, but the combined effect of millions of fans making better choices produces a meaningful reduction across the tournament as a whole. The single most impactful individual action is almost always reducing transportation emissions, particularly from flying. Explore personal carbon offset options at Terrapass to cover what you cannot eliminate.

What is sustainable tourism?

Sustainable tourism means travel that minimizes negative environmental and social impacts while contributing positively to host communities. In practice, it means choosing lower-carbon transportation, supporting locally owned businesses, respecting natural environments and local cultures, reducing waste, conserving water and energy, and taking responsibility for unavoidable emissions through verified offset programs. For World Cup fans, it means being a thoughtful guest in each host city, recognizing that the places and communities welcoming the tournament deserve real respect, and that travel itself can be conducted in ways that leave a lighter footprint.

What is FIFA doing to reduce environmental impacts at the 2026 World Cup?

FIFA’s Sustainability and Human Rights Strategy includes environmental commitments around emissions reduction, responsible procurement, sustainable venue management, waste diversion, and legacy planning. For the 2026 tournament, FIFA is working with host associations in the U.S., Canada, and Mexico to incorporate sustainability requirements into venue operations, transportation planning, and community investment. The decision to use largely existing stadiums is itself a significant sustainability choice. Independent stakeholders and advocacy organizations continue to monitor FIFA’s progress against its stated commitments, and transparent reporting will be essential to evaluating the actual outcomes. More details are available at FIFA’s official sustainability pages.

Can sporting events be sustainable?

Mega sporting events cannot be carbon neutral in any simple sense. They involve too much travel, too much energy, and too much logistical complexity. But they can be substantially more sustainable than a business-as-usual approach, and they can generate lasting positive legacies in host communities. The goal is not perfection but meaningful reduction, honest accounting, and genuine investment in the infrastructure and behaviors that make lower-carbon futures possible. The 2026 World Cup has real opportunities in all three categories. Whether those opportunities are fully realized depends on the choices made by FIFA, host cities, sponsors, and the fans themselves.

How can businesses support climate action around the World Cup?

Businesses can use the 2026 World Cup as an occasion to assess and reduce their own operational carbon footprints, offset emissions from employee travel and corporate hospitality, engage customers and partners in sustainability initiatives, and support climate projects through verified carbon programs. Sponsoring or hosting sustainable events, choosing suppliers with credible environmental commitments, and publishing transparent emissions data are all meaningful steps. For companies with significant travel or event-related footprints, working with an established carbon management partner to measure, reduce, and offset those emissions is a practical place to start. Terrapass offers business carbon offset programs and Renewable Energy Certificates to help organizations take concrete action.

Links Reference

Terrapass Internal Links (live throughout article)

- Carbon Footprint Calculator

- Flight Carbon Calculator

- Personal Carbon Offsets

- Business Carbon Offsets

- Renewable Energy Certificates

- Carbon Credit Guide

External Sources

- FIFA World Cup 26 Sustainability Documentation

- FIFA Sustainability

- UN Sports for Climate Action Framework

- United Nations Environment Programme

- IPCC

- American Carbon Registry

- Climate Action Reserve

- Verra / Verified Carbon Standard

- Gold Standard

The post 2026 FIFA World Cup Carbon Footprint: A Sustainability Guide appeared first on Terrapass.

A few months ago I went to a climate change forum at the Center for Brooklyn History. The panel I attended, “Confronting Climate Change: Understanding Deniers,” featured the prominent climate activist, Bill McKibben.

Bill McKibben. Courtesy https://billmckibben.com/.

I was curious to hear McKibben’s take on climate change deniers. I don’t regard the true deniers as a big problem – they’re only 11-15% of our country, according to most polls. Rather, I wondered if McKibben would label as “climate deniers” people who agree that climate change is a significant problem but disagree with his framing and his proposed solutions. I have worked for decades on energy and climate matters as an energy lawyer. Now, more than ever, I believe that to address climate change we need to build a big tent.

In the Q&A I tested where McKibben is on this by asking if he would label as a climate denier someone who subscribes to the main tenets of climate change science yet holds that natural gas has a role to play as a bridge fuel. (Our exchange starts at 1:12:45 of the video.)

This could have been a chance for McKibben to make clear that such a view isn’t climate denialism, even if he feels it’s misguided. But he punted, saying “I don’t care whether they’re deniers or not.” For good measure, he threw in his long-standing refrain that swapping coal for natural gas makes climate change worse, despite coal’s far higher carbon content per unit of energy.

674-MW methane-powered generating station, Salem, MA.

As you can hear in the recording, McKibben’s claim that gas is worse than coal draws on the work of Cornell scientist Robert Howarth. Yet McKibben didn’t mention that Howarth’s work is controversial and disputed by many scientists. The crux of the dispute is whether methane’s impact on warming should be measured with a 20-year or 100-year time frame.

Methane is a relatively short-lived greenhouse gas, with a lifetime of around 10 years, versus the 100-year life applicable to carbon dioxide. But each ton of methane is far more potent while in the atmosphere, trapping roughly 100 times as much heat as a ton of CO2. These cross-cutting facts about atmospheric methane — shorter life but greater potency than CO2 — have resulted in two opposing camps: one insisting on a 20-year timeframe for greenhouse gas accounting, the other adhering to the established 100-year frame. This matters because with a 20-year timeframe, generating electricity with natural gas (which, chemically speaking, is essentially all methane) is more damaging to climate than coal-fired electricity.

McKibben blew past this dispute. To hear him at the Center for Brooklyn History, one would have no inkling that there’s an active disagreement over which timeframe to use, that there are staunch climate activists who favor the 100-year time frame, and that the Intergovernmental Panel on Climate Change (IPCC) generally uses the 100-year timeframe.

McKibben’s latest (2025) book. Published by W.W. Norton & Company.

McKibben also insisted that a discussion about natural gas’s potential role in mitigating climate change as a replacement for coal is irrelevant because solar “is now our cheapest resource.” McKibben’s claim, of course, suffuses “Here Comes the Sun,” his 2025 book that extols solar power as the cheapest solution for all of our energy needs. But this too is questionable, because it’s based on cost comparisons between solar farms and natural gas power plants (or nuclear power plants) that fail to consider that electricity supply and delivery is a complex system of wires and plants rather than individual power plants. Based on his remarks, McKibben is choosing to ignore studies such as the comprehensive 2025 report from the Clean Air Task Force that concluded that plant-level cost comparison “is a good metric to track historical technology cost evolution [but] is not an appropriate tool to use in the context of long-term planning and policymaking for deep decarbonization.” And the task force is not alone in finding that when electricity is treated as a system, solar loses its place as the cheapest low-carbon resource.

The dogmatism McKibben displayed at the Brooklyn meeting was unfortunate. We’re in a time when efforts to combat climate change are in retreat. A unified front is required to turn the tide. Instead of doubling down on absolutist positions, activists like McKibben who seem convinced that the solution to climate change is all-renewables, end of discussion, should be seeking common ground with others who want climate action but believe that nuclear power and natural gas must also play a role.

NYC Climate March, Sept 17, 2023. Photo: C. Komanoff.

Climate change activists need to build a bigger tent, rather than call anyone who disagrees with their positions a climate change denier. It is striking that McKibben stuck to his guns after saying in the same talk that the most important goal for everyone right now is to help climate change realists win more House and Senate seats in this year’s midterms. As some have noted, an absolutist position on natural gas appears less likely to achieve that win and politicians are following that advice.

Will McKibben evolve? He has demonstrated that he knows how to build a national climate movement centered around issues like divestment. Given the current political situation, he should focus on building an even bigger tent by welcoming all of the 85% who believe that we need to address climate change but do not agree with his ideological positions.

Rich Miller is an energy lawyer who has worked for a variety of stakeholders and now gives walking tours in lower Manhattan on the history of electricity.

-

Climate Change11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测