The Global Plastics Treaty is a once-in-a-generation opportunity to solve the plastics crisis. For the sake of our collective future, we cannot waste this moment.

We are in the fifth round and the most critical moment of treaty negotiations. Now is the time to escalate the pressure so that our demands are not ignored: the treaty must cut plastic production and end single-use plastic to solve this global crisis.

Greenpeace’s demands for the Global Plastics Treaty:

- The Global Plastics Treaty must cut total plastic production by at least 75% by 2040 to ensure that we are staying below 1.5° C for our climate and to protect our health, our rights, our communities and our environment.

- This is a battle for our survival. As expected, the petrochemical industry, corporations and some governments are trying to weaken the treaty’s ambition. If they have their way, plastic production will triple by 2050. We can’t let them.

- As we head into the last round of negotiations, blocker countries continue to oppose meaningful provisions. We need high-ambition countries to show more courage and fight for ambition to reach a treaty that will cut plastic production and end single-use plastic.

- The Bridge to Busan declaration, signed by 34 countries, shows there is support for an agreement that cuts global plastic production to limit global temperature increase below 1.5° C. High-ambition countries can show how ambitious they really are by signing on. We cannot solve the pollution crisis unless we turn off the tap.

- The Global Plastics Treaty must be built upon a foundation of human rights. It must reduce inequalities, end waste colonialism, prioritize human health, center justice, and ensure dignity for all.

- An effective treaty must protect biodiversity, safeguard our climate, and ensure a just transition to a reuse-based economy.

A strong and ambitious plastics treaty will deliver a cleaner, safer planet for us all.

We need a major reduction in plastic production to reduce the harm that plastic brings to our health, our biodiversity, and our climate. Given the urgency of this plastics crisis, we need to set a baseline based on an agreed timeline, and then build from there based on newly available science.

The plastics crisis touches every corner of the globe. It is in the deepest parts of our oceans and on the highest mountain peaks and even in our bodies. During the negotiations process, we will show how an unstoppable global movement can achieve an ambitious Global Plastics Treaty that will turn off the plastics tap and finally, end the age of plastic – for our health, our communities, climate, and the planet.

Sign the petition for a strong Global Plastics Treaty

Let’s end the age of plastic – sign the petition for a strong Global Plastics Treaty

SYDNEY, Monday 27 July 2026 — In response to an announcement that Woodside’s Browse to North West Shelf (Browse) Project was declared a State Significant Project by the WA Government, the following comments can be attributed to Senior Campaigner at Greenpeace Australia Pacific, Hannah Schuch:

“The WA Government must not ignore the significant risks clearly associated with Woodside’s plans to drill for gas at the pristine Scott Reef — to endangered marine life, our oceans, and our climate — all of which are valued and relied upon by Western Australians.

“The WA Environmental Protection Authority has already found Woodside’s plans to drill at Scott Reef would have unacceptable impacts on the environment without considering the climate impacts of 1.6 billion tonnes of carbon pollution associated with this disastrous proposal.

“Woodside’s gas drilling plans, including seismic blasting and carbon dumping in the heart of a precious ecosystem, pose potentially fatal risks to pygmy blue whales and genetically unique green sea turtles, and could cause a catastrophic oil spill.

“If the WA and federal governments are concerned with the prosperity of WA, they must reject Woodside’s nature and climate-wrecking proposal to drill for gas at Scott Reef.”

—ENDS—

High res images and footage of Scott Reef can be found here.

For more information or to arrange an interview, please contact Emma Sangalli on 0431 513 465 or emma.sangalli@greenpeace.org

Cook Government must recognise risks posed by Woodside’s Scott Reef drilling plans

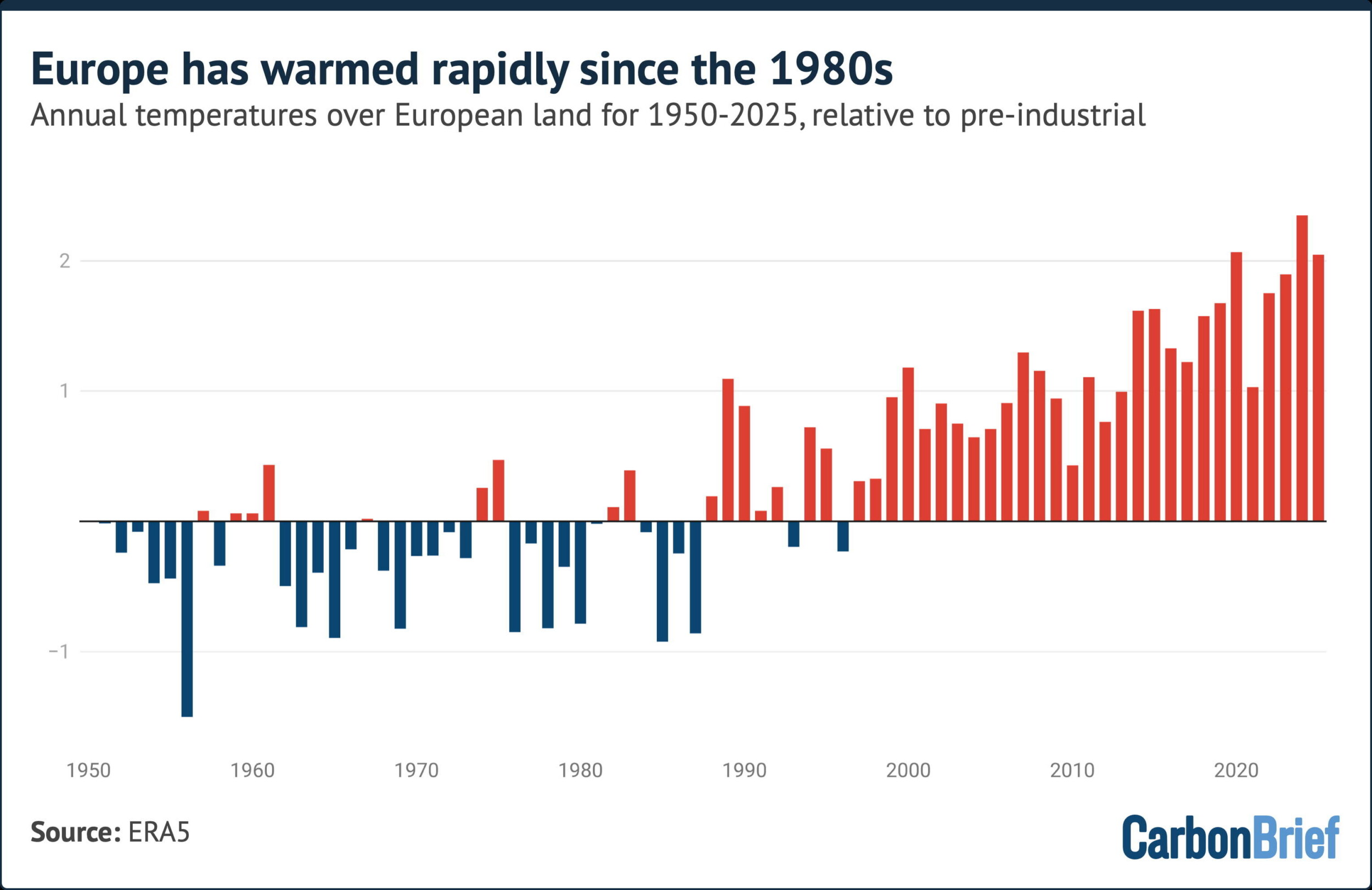

This summer has seen Europe suffer through a series of record-breaking heatwaves.

Amid widespread media coverage of the number of deaths and the influence of climate change, the UK’s Daily Telegraph reported on new research with the incorrect headline: “Heatwaves caused by fall in pollution.”

The article was shared on social media by Richard Tice – deputy leader of the hard-right, climate-sceptic Reform UK party – along with a number of prominent rightwing commentators.

Tice claimed that “net stupid zero is contributing to rising temperatures, not helping”, adding that “we have been gaslit and lied to”.

GB News followed up with its own article, incorrectly headlined: “Britain’s scorching heatwaves caused by falling pollution levels, researchers find.”

Scientists tell Carbon Brief that the framing of heatwaves being “caused” by declining air pollution is “wrong”.

While a drop in pollution has reduced the cooling impact it has had in the past, the scientists say, Europe’s summer heatwaves are primarily becoming more extreme “as a result of greenhouse-gas-induced warming”.

Another scientist adds that “any attempt” to link this research to net-zero policies is “simply wrong”.

Fast warming

The extensive reporting around Europe’s heatwaves in recent months has often mentioned that Europe is the world’s fastest-warming continent.

The new study in question aims to unpack why Europe’s summer temperatures are rising more quickly than other regions of the northern hemisphere’s mid and high latitudes.

The research – published in Geophysical Research Letters – explores the role of air pollution and, specifically, how it affects circulation patterns in the atmosphere.

(The study focuses on long-term trends in European summers and does not include the very recent heatwaves.)

Human-caused emissions of aerosols – tiny, light‑scattering particles produced mainly by burning fossil fuels – have long acted to “mask” global warming. This is largely because they absorb or reflect incoming sunlight and influence the formation and brightness of clouds.

To understand how the climate of Europe – or any region – is changing, scientists need to take into account a whole range of factors, says Prof Bjørn Samset, a research professor at Norway’s Center for International Climate Research (CICERO), who was not involved in the work.

This includes “greenhouse gases, aerosols, land-use change, natural variability and how they all interact”, he says, adding:

“The effects of air pollution on circulation, which is the topic here, has long been difficult to pin down.”

As European countries improved their air quality through the second half of the 20th century, the cooling effect of aerosols has gradually been removed.

This can boost heatwaves in two ways – directly, by letting more sunlight reach the land surface and, indirectly, by influencing the jet stream.

Using hundreds of simulations from nine climate models, the new study finds that a decline in aerosols is resulting in more frequent “quasi-stationary Rossby waves”.

Rossby waves are huge meanders in the jet stream. Occasionally, they become slow-moving – or “quasi-stationary” – which allows weather systems to get stuck over one region, leading to prolonged heatwaves.

These circulation changes have contributed to Europe’s rapidly warming summers.

However, while Europe’s heatwaves are being influenced by declining aerosols, it is “wrong” to say they are being “caused” by them, says Prof Erich Fischer, a climate scientist at ETH Zurich.

Fischer, who was not involved in the study, tells Carbon Brief:

“Heatwaves are caused by high-pressure systems and are now much more frequent and intense because they are happening in a climate that is much warmer than 100 years ago as a result of greenhouse-gas-induced warming.

“The paper shows that the greenhouse-gas-induced summer warming had been temporarily masked by air-polluting aerosols. The full extent for European summers only becomes visible now as the air-polluting aerosols have declined.”

Samset adds:

“Air pollution never causes or removes global warming, it only temporarily moderates it.”

Study lead author Dr Pedro Roldán‐Gómez, an associate researcher at the Barcelona Supercomputer Centre, is quoted in the Daily Telegraph saying that “most” of the “excess warming” in Europe, beyond that of comparable regions in the northern hemisphere, can be linked to declining aerosols.

But, earlier in the article, the newspaper interprets this as, simply, “most of the extra heat experienced in Britain and Europe” is down to air pollution.

GB News uses a similar phrasing, reporting that “much of the additional warming across Britain and western Europe since the 1980s is linked to the sharp decline in airborne particles known as aerosols”.

This is “misleading”, says Fischer, while Roldan-Gomez tells Carbon Brief that this is a “tricky point”, which “could lead to wrong interpretations if not properly explained”. He adds:

“The contribution of greenhouse gases is, in any case, the most important factor.”

Cleaner air

The Daily Telegraph’s article was seized upon by Reform’s Richard Tice to claim that “cleaner air” was causing higher temperatures, rather than CO2.

This continued his position – refuted by long-established climate science – that CO2 does not drive global warming.

Tice also claimed in his post that net-zero policies are “contributing to rising temperatures”. Tice appears to be linking declining air pollution to a shift from fossil fuels to renewable energy.

Samset points out that net-zero became a goal “decades later” than the cumulative efforts to reduce air pollution since the 1980s and that it is “simply wrong” to link it to the study.

“The scientific community will keep working to understand how greenhouse gas warming and air pollution interact,” he says, but “nothing we do will change the fact that the consequences of global warming are due to human-induced CO2 emissions”.

Fischer adds:

“Let us not forget that cleaning up air-polluting aerosols is highly desirable. According to the World Health Organisation, 7 million people still die prematurely every year due to air pollution.”

Clean air legislation

Finally, the Daily Telegraph article and the study itself both attribute Europe’s declining air pollution from the 1980s onwards to the Montreal Protocol.

This is a “glaring error”, Samset says, and it is “surprising that it wasn’t picked up” in the peer-review process for the study. He explains:

“The Montreal Protocol did not deal with air pollution. It dealt with ozone-depleting gases and has been an extremely successful multi-national effort against environmental damage. “

Clean air legislation was already in place in many European countries by the time the Montreal Protocol was signed in 1987, says Samset.

In response, Roldán‐Gómez says that while the protocol did not target aerosols specifically, it “boosted the clean air policies”.

The post Factcheck: No, Europe’s heatwaves are not being ‘caused’ by declining air pollution appeared first on Carbon Brief.

Factcheck: No, Europe’s heatwaves are not being ‘caused’ by declining air pollution

Empowering women through greater access to finance could “strengthen” households’ resilience to “climate shocks”, according to a new study.

Published in Climate Risk Management, it analyses the impact of financial access on “women-headed households” in sub-Saharan Africa.

The study finds that where women had formal financial access – such as through owning a bank account – households were more able to withstand short-term shocks.

It adds that “climate shocks”, such as extreme weather events and the impacts of climate change, can cause economic crises, which destabilise communities and households.

However, the authors say that in order to protect households from long-term climate vulnerabilities – including “droughts, floods and sea-level rise” – financial access would need to be paired with wider efforts to tackle gender inequality.

They add that the findings could have important implications for policy in sub-Saharan Africa, where many countries and households are vulnerable to climate disasters.

Financial inclusion

The study highlights that entrenched gender disparities mean many women still have unequal access to financial services in sub-Saharan Africa

For example, women are still less likely to have their own bank accounts and instead are often dependent on male relatives for access to finance.

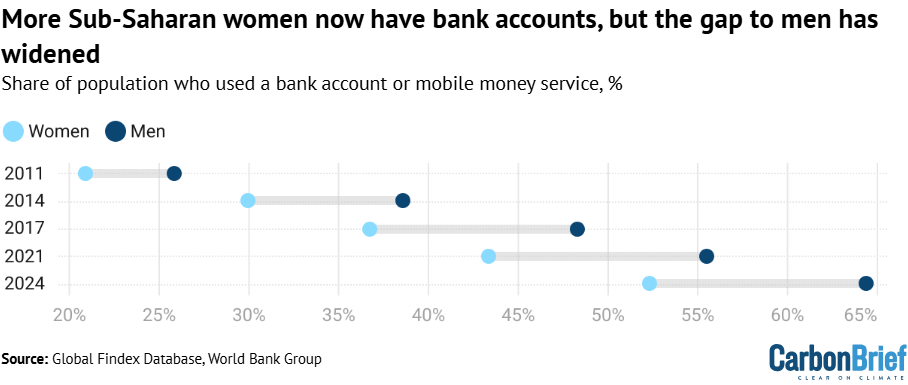

The number of women with access to an account in the region had risen to 52% as of 2024, according to data from World Bank Group.

However, as shown in the chart below, the gap between men and women has also increased, rising from just under 5 percentage points in 2011 to 12 in 2024.

Using survey data from Afrobarometer, the new study analyses 25,511 women-headed households across 37 sub-Saharan countries.

The authors use the Organisation for Economic Co-operation and Development’s (OECD) framework to measure “financial inclusion”. This looks at factors such as having a bank account, owning a mobile phone and having internet access.

Francis Anaisie, a co-author on the study, tells Carbon Brief the researchers were motivated by the UN’s sustainable development goals (SDGs). Anaisie, an economist at the University of Cape Coast, Ghana, says the study specifically looked at SDGs five and 13, on gender equality and addressing climate issues. He adds:

“Financial inclusion is one of the key policy tools for empowering women or for empowerment. But as to whether this actually translates into better climate outcomes for women is not known or is limited; this study seeks to address that gap.”

The study finds households with higher levels of financial access for women had higher levels of women’s empowerment, when this is defined as the ability to make choices and have control over economic and social outcomes.

This was checked by cross-comparing financial access against different measures of women’s empowerment, such as financial security, voting rights and connection to communities.

In particular, the study found that “financially included” women had greater political and economic empowerment, such as financial security and voting rights. On some measures of social empowerment, however, the link was weaker – financial access alone was not enough to erase cultural and social barriers to gender equality.

Women and climate change

It has been well documented that women are more vulnerable to the impacts of climate change than men.

Environmental shocks affect women disproportionately due to a range of factors. These include income disparities, higher rates of displacement and unequal access to land.

Financial inequality and barriers to economic resources, such as needing internet access to make digital payments, play a key role in climate vulnerability, says Tracy Kajumba. She is director for the Least Developed Countries initiative for Effective Adaptation and Resilience (LIFE-AR) interim secretariat at the International Institute for Environment and Development (IIED).

Kajumba, who was not involved in the study, explains to Carbon Brief:

“Women are on the front line doing farming, planting, harvesting and these things that are all impacted [by climate change]. If they don’t have the income to invest either in drought-resistant crops or water-saving technologies, it becomes difficult for households to adapt.”

Calculating climate resilience

The new study measures the impact of financial inclusion on women’s empowerment and, in turn, on climate resilience.

It evaluates a household’s ability to withstand and recover from “shocks and stressors” by using a UN Food and Agriculture Organization metric for “resilience index measurement and analysis” (RIMA).

For example, questionnaires are used to gather information about households in certain areas. The data is then used, together with key indicators, to quantify a household’s resilience to food insecurity, climate variability and economic crisis, amongst other risks.

The 25,511 households surveyed across sub-Saharan Africa were found to be relatively resilient overall and had a high capacity to bounce back from climate shocks. However, they had much lower ability to adapt, in order to build protective capacity in advance of extreme events.

In addition, the study finds that women’s financial empowerment had a positive impact on a household’s ability to “absorb” a climate shock, suggesting that financial access is critical for responding to climate change.

Increased empowerment through financial access enables women to make decisions about planting crops, to access credit in emergencies and to buy or sell food at a better price, the study notes.

For example, it says increased financial access and women’s empowerment help households to deal with the immediate consequences of an extreme weather event, such as a drought. This could be through building community mutual-support networks and by enabling access to savings, to keep the household running.

Anaisie says the study shows women’s empowerment has a significant impact on climate resilience. He tells Carbon Brief:

“If we include women in the financial system, in the case of any climate issue they can save, they can be independent, they can rely on investment to absorb these shocks. This empowerment will help them to be more resilient to climate shocks…We can make progress because SDG goals are all about inclusiveness. It’s all about inclusive growth.”

However, the study notes that financial access does not necessarily create long-term change, which would make the household less vulnerable to extreme weather in the first place.

The authors suggest that lasting structural and cultural change is important for bringing about long-term resilience. They say that policies to address gender inequalities would help bring this about.

They say such policies could include gender-sensitive agricultural credit schemes, subsidised climate insurance for women farmers in drought-prone regions, joint land-titling programmes and quotas for women in local climate-adaptation committees.

Such policies would have helped women impacted by recent severe floods in Ghana to protect their savings, Anaisie explains. He tells Carbon Brief:

“Women are engaged in economic activities, especially informal activities. They have resources and money, but when the flood came in, many women lost that. If they had access to insurance, this flood wouldn’t have cost them that much.

“So, if the government comes out with financial initiatives, training, civic education and gender-focused initiatives, leadership training, women will be empowered and this will translate into their resilience with regards to climate change.”

Addressing climate vulnerability in sub-Saharan Africa

The study could have policy implications for sub-Saharan Africa, a region particularly vulnerable to the effects of climate change. The region faces increasingly extreme weather, heatwaves, droughts, wildfires and floods, as well as food scarcity and threats to crops.

The study suggests that policies to address structural and cultural barriers to women’s financial autonomy could be a key way to build climate resilience across the region.

However, it recognises that even where financial access is expanded, gender norms and cultural constraints continue to shape women’s social empowerment. This, in turn, affects their ability to adapt to climate change in the long term.

Ultimately, addressing structural inequalities is needed to minimise climate vulnerability, says Kajumba. She adds that supporting adaptation with financial access can allow households to absorb shocks without falling into poverty – and to rebuild after climate impacts.

Kajumba says that supporting adaptation with women’s financial access can allow households to absorb shocks without falling into poverty – and to rebuild after climate impacts. She adds:

“When they are supported [with] microloans, savings and all that, you will see change in income, change in households, change in health and education for the children as well.”

However, Kajumba notes that structural inequalities still “amplify” women’s vulnerability to climate impacts and make it harder for them to exercise agency and leadership. She adds:

“The tools that are being used are not always favourable for women…When we look at women in leadership and participation, you cannot lead or you cannot participate unless you have some level of income.”

The post Access to finance ‘strengthens climate resilience’ among sub-Saharan women appeared first on Carbon Brief.

Access to finance ‘strengthens climate resilience’ among sub-Saharan women

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测