Developing countries want rich nations to give them hundreds of billions of dollars for climate action, suggesting this could be raised by taxing defence, technology and fashion companies, as well as financial transactions.

At UN talks on a new post-2025 climate finance goal in the German city of Bonn, the umbrella group for 134 developing countries said wealthy governments could raise $1.1 trillion a year, needed by poorer nations to curb emissions, adapt to climate change and deal with the damage it causes.

An unpublished position paper by the G77+China, seen by Climate Home, maintains that rich countries would “only” need to spend 0.8% of their GDP per year to raise $441 billion. That would mobilise enough private finance to reach $1.1 trillion a year, it adds.

It notes that 0.8% of GDP is much less than the 6.9% of GDP developing countries currently spend paying interest on their debt.

The paper says developed countries can raise $441 billion “without compromising spending on other priorities entirely by adopting targeted domestic measures” such as a “financial transaction tax”, a defence company tax, a fashion tax and a “Big Tech Monopoly Tax”.

It argues that “the matter in question is not whether the resources exist, it is whether there is political will to prioritise climate change”.

Bolivian negotiator Diego Pacheco, who often speaks for the influential Like-Minded Developing Countries group, told Climate Home that rich countries were trying to pass their responsibility to provide climate finance onto the private sector and development banks that mainly offer loans.

“The [argument of a] lack of public finance is not true,” he said. “There is a lot of finance available and political will is lacking.”

He suggested that developed countries should shift military budgets towards tackling climate change or tax luxury products “because luxurious patterns of consumption are also a driver of the climate crisis”.

Innovative sources

Referring to the document in talks on the new finance goal yesterday, Saudi Arabia’s negotiator justified a tax on arms manufacturers by saying that military emissions of planet-heating gases represent 5% of global historical emissions.

“One… potential idea is to have a tax on defence companies in developed countries,” he said, suggesting it could be put forward. “We also realise that a financial transaction tax can actually generate a lot of revenue as well.”

At the COP28 climate summit last November, France and Kenya launched a taskforce to look into innovative levies that could raise money for climate action. They said they planned to examine taxes on international shipping – which has already agreed to introduce one – aviation, fossil fuels and financial transactions but did not refer to fashion, technology or defence companies.

Global brands targeted

According to the document, a financial transaction tax would raise about $240 billion a year over a decade through a 0.5% tax on trades, 0.1% on bonds and 0.005% on derivatives “only for Wall Street”.

About $57 billion a year could be raised from a 5% tax on the annual sales of the top seven technology firms, it says. Those would include Amazon, Apple and Google. “The ‘Big Tech’ firms hold a global monopoly on technologies, upon which developing countries have been reliant,” the paper argues.

About $34 billion a year could come from a 5% tax on the annual sales of the roughly 80 top fashion firms in developed countries, it says. This would hit brands like Louis Vuitton, Dior and Nike.

The G77+China group adds that the fashion sector comes behind only fossil fuels and agriculture in the size of its emissions – “however, unlike fossil fuels and agriculture, high-end brands are not critical for food and energy security”.

Around $21 billion a year could come from a 5% tax on the annual sales of the top 80 defense firms in developed countries, the paper says. This would include US firms like Lockheed Martin, Northrop Grumman and Boeing, the UK’s BAE Systems and France’s Thales.

All these measures would result in finance flows mainly from developed to developing countries, the document notes, except for the technology tax where “flows would be mixed as consumer[s] would shoulder the cost”.

Pacheco said the proposals originated within the Arab Group, before winning support from the wider G77+China group. Developed countries have yet to publicly respond to the ideas.

Under the UN climate change process, the group of developed countries defined back in 1992 have so far had the sole responsibility to provide climate finance to developing nations.

Developed-country governments are now pushing hard to change this, so that wealthier and high-emitting developing countries like Saudi Arabia would also contribute towards the new post-2025 finance goal.

This is one of the divisive issues government negotiators will wrangle over this week and next in Bonn to prepare the ground for an expected agreement on the finance goal at COP29 in Baku in November.

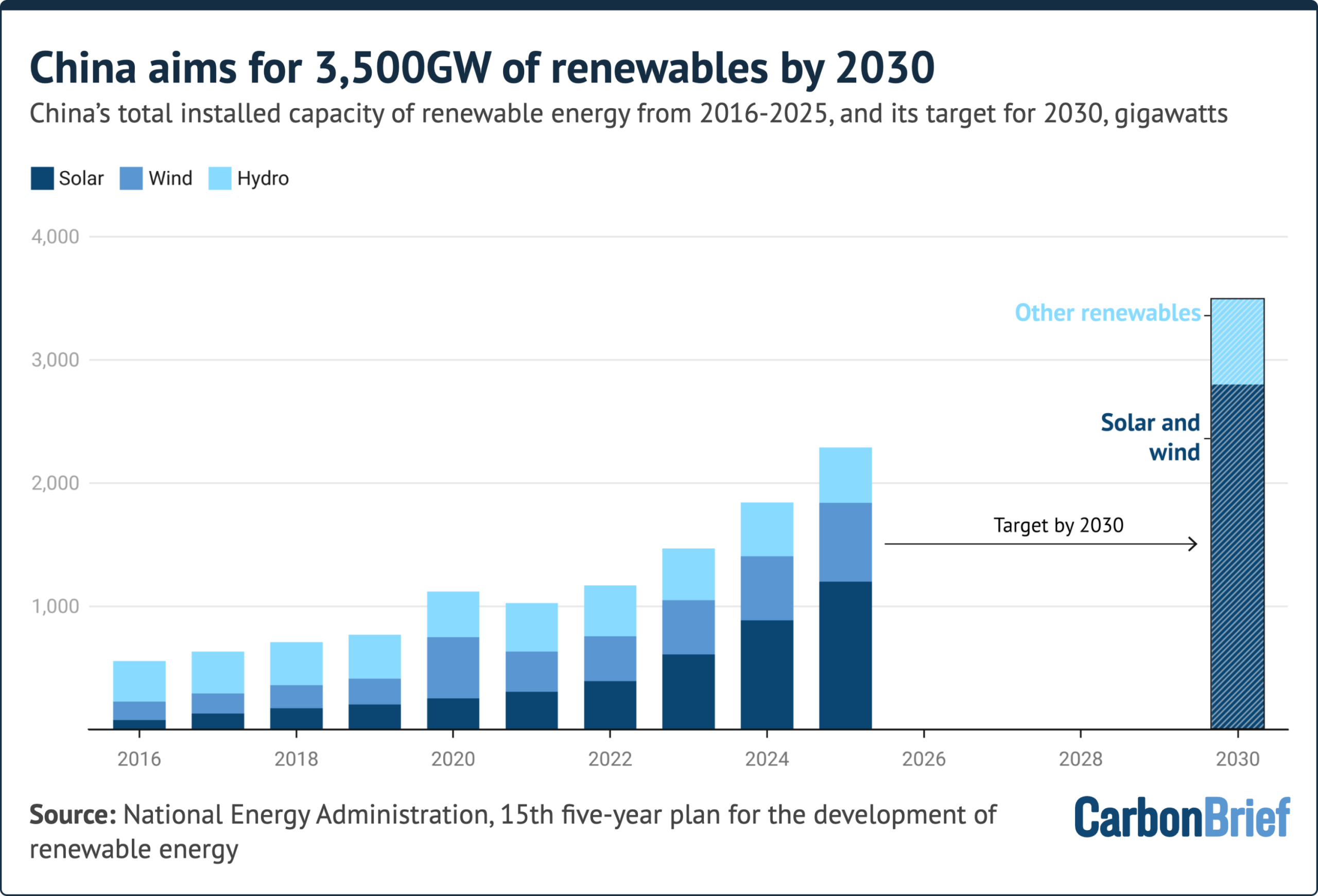

China has released its “15th five-year plan for the development of renewable energy”, outlining key targets and policies for the sector in 2026-2030.

A key focus of the plan is boosting renewable generation and consumption as a share of China’s overall energy mix.

It calls for continued capacity additions of wind and solar – albeit at lower levels than previous years – as well as hydropower, biomass and other clean-energy sources.

Specifically, China will aim to install 3,500 gigawatts (GW) of renewables capacity by 2030, 2,800GW will be wind and solar.

The country had previously pledged to install 1,200GW of wind and solar by 2030, a goal that China met six years early.

Another major theme is the provision of wind and solar supply that is “dependable” and “grid-friendly”.

Setting a target for “dependable output” from wind and solar could help to entrench their role as a provider of “energy security”, according to analysts.

The government also aims to boost renewables consumption by developing non-power uses of renewable energy, in sectors such as steel and chemicals.

Below, Carbon Brief examines the key targets and policies outlined in the five-year plan and what they mean for China’s energy transition.

Five-year plans are key to China’s political system. An overarching plan, covering all socioeconomic issues of importance to policy leaders, is published at the beginning of each five-year cycle.

The plan for the 15th five-year period (2026-2030) was published in March 2026.

It includes what the government considers to be the most important targets and policy signals for climate and energy. For example, binding targets for carbon intensity, the share of non-fossil energy in total energy consumption and total energy production capacity.

Following this overarching document, five-year plans focused on specific sectors or themes are then published over the course of the five-year plan period.

This year, the government has already published several five-year plans related to energy and climate change. One covers the development of the “new-type” energy sector more broadly. Another wraps climate goals together with other environmental targets under the “Beautiful China” programme.

By contrast, the renewables five-year plan focuses specifically on the development of hydropower, wind, solar, biomass, geothermal and wave energy.

It covers topics including capacity and generation targets, as well as efforts to increase integration and reliability of wind and solar. It also has policies to encourage “non-power use” of renewable energy and ways to strengthen innovation of clean-energy technologies.

What overarching renewables targets are in the plan?

China will aim to install 3,500 gigawatts (GW) of renewables capacity by 2030, according to the five-year plan.

Of this, 2,800GW will be wind and solar – a pledge reiterated from China’s action plan for peaking carbon emissions, which was released earlier this month.

The goal more than doubles a previous 2030 target for wind and solar to reach 1,200GW, which China met six years early.

As of June 2026, the country has installed just under 2,000GW of wind and solar capacity, as well as 454GW of hydropower. Biomass, geothermal and wave energy hold very small shares of the overall energy mix.

As such, China would need to build 160GW of wind and solar each year – and just under 220GW of renewable capacity in total – to meet the targets.

The country installed 277GW of new solar alone in 2024 – and 315GW in 2025.

China’s total installed capacity of renewable energy from 2016-2025, and its target for 2030. Source: National Energy Administration, Carbon Brief.

A key part of meeting the targets will be the development of large-scale clean-energy bases in China’s northern regions. These will generate power to be exported elsewhere via ultra-high voltage lines. The plan also encourages greater “local consumption” and installations of distributed energy (see below).

The plan says that further research will be directed at increasing the renewable share of electricity generated by these large-scale energy bases to 100%.

A recent report by the thinktank Global Energy Monitor (GEM) finds that output from these bases “continues to be paired with coal-fired generation in the name of balancing and system flexibility”. It says that currently, coal generates 42% of the power transmitted to the rest of the country from these bases.

China will also add more hydropower, says the plan, with capacity rising from 448GW in 2025 to 570GW in 2030. Some 160GW of this will be pumped-storage hydropower.

Meanwhile, the plan sets a target for renewable power generation to reach 6,000 terawatt-hours (TWh), 4,000TWh of which would come from wind and solar.

This would be a 50% increase in five years as renewables generated just under 4,000TWh of electricity in 2025, according to the National Energy Administration.

By 2030, the plan says that total consumption of renewable energy will stand at 1.8bn tonnes of coal equivalent (Gtce).

This would be up from 1.2Gtce in 2025, which represented about one-fifth of China’s total energy consumption of 6.2Gtce that year.

The renewable targets in the plan are lower than those suggested in a recent study by high-profile Chinese scholars.

The study, from the department of energy and power engineering and the Institute of Climate Change and Sustainable Development at Tsinghua University in Beijing, assessed the “likelihood of China attaining its carbon peak” under different pathways.

It found that, in order to meet its climate commitments, China would need to either install more than 4,000GW of “non-fossil energy capacity” before 2030, or to “maintain a total energy consumption” below 6.5Gtce.

The table below outlines some of the key renewables targets for 2030, as specified in the plan.

Key targets for 2030, adapted from 15th five-year plan for renewable energy

Type

2025

2030

Percentage change

Renewable energy use

1.2Gtce

1.8Gtce

53%

Total renewables capacity

2,340GW

3,500GW

50%

Wind and solar capacity

1,840GW

More than 2,800GW

52%

Of which: Solar thermal

1.8GW

15GW

733%

Hydro capacity

450GW

570GW

27%

Of which: Pumped storage hydropower

66GW

160GW

142%

Wave energy

–

0.4GW

–

Renewable generation

4,000TWh

6,000TWh

50%

Of which: Wind and solar

2,300TWh

4,000TWh

74%

Non-electricity use

60Mtce

150Mtce

150%

Renewable hydrogen

0.25Mt

2Mt

700%

Why does the plan focus on ‘firm capacity’ for renewables?

As well as increasing the overall size of China’s renewable power supply, the country must also maintain an “uninterrupted and reliable power supply”, officials from the NDRC and NEA told state news agency Xinhua in coverage of the new plan.

To support this goal, the plan says that the development of renewables will “enter a new stage”. This will mean that “improving quality and serving as a reliable alternative” to fossil fuels will be as important as “expanding scale”.

The plan, therefore, proposes targets for the “firm capacity” from wind and solar (置信出力). This is the amount plants or grids can be relied on to produce during critical supply periods, in conjunction with on-site storage.

The target for wind is a firm capacity of at least 11% of total installed capacity by 2030, while the equivalent goal for solar is 6%.

Wind and solar will also be expected to supply more than 20% of total demand in peak periods during the summer and winter evenings, says the plan. It expects “reliable peak-shaving capacity from renewable sources” to reach more than 300GW.

The new targets are a “positive move”, says Yao Zhe, global policy advisor at Greenpeace East Asia, as it “only applies during peak load and critical supply periods, when coal power is typically used to stabilise the power supply”.

She adds that this could, theoretically, “prevent the construction of new coal-fired power projects that are proposed and approved for the reason of meeting peak demand”.

The new metrics mark a change in focus, says Lyu Wenbin, director general of the Energy Research Institute – a state thinktank under the NDRC – in an “explanatory reading” posted on BJX News. He says it “marks a shift in renewable energy development from the mere pursuit of installed capacity to…also taking into account system support capabilities”.

The plan pledges to “accelerate the construction of grid-friendly wind and solar power stations”. It says this will enhance “reliable peak-load generation” and strengthen renewables’ ability to ensure “safe and stable operation” of the grid.

It says this will particularly be a focus in the energy-hungry east, central and south areas of China.

It sets out a slightly different focus for areas that already have a high share of renewables in their power mix, such as north-west China. Here, the aim will be to develop wind and solar parks that are “capable of providing voltage, frequency and inertia support”.

“This is a real challenge”, says James Norman, research analyst at GEM. He says these challenges are particularly acute in some circumstances:

“[For example], when the share of wind and solar is very high, relatively few synchronous generators (like coal) are online or large volumes of electricity are being transferred through high voltage DC lines.”

The plan mentions many technological solutions to address the problem, he tells Carbon Brief. However, he adds, there are no quantitative details for the issue. For example, he notes there is no target for “how many gigawatts of wind and solar must gain grid-forming capability”. This is in contrast to the goals for overall renewables capacity or generation.

Norman was a co-author on the recent GEM report, which identified further barriers to renewable uptake. It said these include transmission bottlenecks, alongside systemic features such as dispatching and power-contract mechanisms.

As a result, said the report, renewable power – especially solar – is increasingly being “curtailed”, particularly in north-western and northern provinces.

Yao also notes that the plan does not “spell out specific measures to address systemic constraints” around the electricity grid and the role of coal in the power sector.

“I interpret this as evidence that the vested interests are still strong in the policy debate,” she adds.

What does the plan say about ‘distributed’ energy?

Alongside gigawatt-scale clean-energy megabases, China also aims to expand construction of “distributed” energy. This means smaller-scale installations, such as rooftop solar.

More than 300GW of “distributed new energy” is to be added over 2026-30, some 60GW per year.

The plan aims for distributed new energy to be adopted in sectors such as industry, transport, buildings and agriculture.

Applications include the use of distributed solar and wind in industrial parks, coal mines and oilfields, as well as encouraging residents to install solar panels on buildings and developing rural clean-energy grids.

In some regions, distributed solar and wind is “likely to meet a large proportion of local demand”, says Prof Pan Jiahua at the Hong Kong University of Science and Technology (Guangzhou). He tells Carbon Brief that micro- and mini-grids using such resources will be particularly important in central and coastal China.

The 60GW annual target for new distributed energy is not “overly ambitious”, says Isadora Wang, head of China at the thinktank Transition Asia. She tells Carbon Brief that distributed solar additions, alone, exceeded 100GW in both 2024 and 2025.

Cosimo Ries, analyst at the consultancy Trivium China, agrees that the target is reachable. The biggest question mark, he tells Carbon Brief, is whether it will continue to make sense for industry and utilities to build distributed power at the volumes seen during the 14th five-year plan period.

He adds that market conditions for distributed solar have deteriorated sharply over the past two years. He says a range of factors have hit investor confidence:

“[Distributed solar faces] growing exposure to market trading, worsening returns in spot markets, growing risks of curtailment and new policies limiting or forbidding the selling of power back to the grid.”

What does the plan say about non-electricity use of renewables?

The plan also sets goals for renewable energy’s role in “non-electricity use”.

This means using renewable energy for purposes other than generating electricity, through converting it to other forms, such as heat or mechanical energy.

The government is aiming for non-power use to nearly triple from 60m tonnes of coal equivalent (Mtce) in 2025 to 150Mtce in 2030.

Ries tells Carbon Brief that he thinks this target is “one of the main highlights” of the plan. However, he notes that limited available data means it is hard to assess the level of its ambition. He adds that, given the relative conservatism of China’s other recent clean-energy targets, this one may also be met relatively easily.

Key applications for non-power use of renewables include “green hydrogen, ammonia and methanol”, says the plan. It also points to using wind and solar for heat, as well as to biomass and geothermal for heating and cooling.

Green hydrogen, ammonia and methanol are the “centrepiece” of the non-power push, according to state-owned newspaper Economic Information Daily.

For hydrogen alone, China plans to scale up renewable hydrogen production to 2m tonnes in 2030, up from 250,000 tonnes in 2025.

Today, non-power use of renewables accounts for only around 1% of China’s total energy consumption, NEA and NDRC officials said in a Q&A. They added that there is “considerable room for growth” in sectors such as industry, transport and buildings.

Potential new applications include the use of wind and solar for heat. This could see the use of centralised wind and solar heating stations in the chemicals, textiles, pharmaceuticals, papermaking and food sectors.

New projects in the steel and cement sectors should use locally-generated wind and solar to power electric-arc furnaces and kilns, adds the plan.

Wang tells Carbon Brief that she believes the naming of individual sectors is a “clear indication” that they will be included in China’s renewable consumption quotas. These already cover aluminium and other heavy industry sectors.

She adds that power and heat demand from the named sectors may help absorb distributed renewable energy. It will also serve as a testing ground for matching demand with supply through increased grid flexibility and power price reforms.

To Ries, the growing focus on non-power use signals that China’s decarbonisation efforts are “now entering deeper waters”. That means regulators are turning from easier-to-abate sectors, such as aluminium, to more challenging industries, such as steel.

The plan could create a “second growth curve” for the new-energy industry, says He Zhao, in a commentary for China Power News Net. He, the vice-president of the China Electric Power Planning and Engineering Institute (EPPEI). says this might begin with non-power use, before shifting to fuel, feedstock and heat substitution.

What does the plan say about China’s cleantech dominance?

The next five years is a prime opportunity for China to “consolidate our leading position across the entire industrial chain” for clean-energy technologies, says the plan.

It adds that the government will “strengthen technological innovation” and accelerate the roll-out of new applications of artificial intelligence in China’s renewable-energy system.

A particular focus for new R&D will be “cutting-edge, original and disruptive technologies”. It also points to technologies that “enhance the reliability of renewable energy” as a substitute for fossil fuels.

The plan names technologies for further development. For wind power, these include “reliable and low-cost” blades, ultra-tall towers and new types of floating platforms. It also mentions the development of “high-altitude wind power”. For solar, it points to the development of perovskite and other “high efficiency” solar cells, as well as space-solar technologies.

The plan also pledges to develop a power market that supports the “full entry” of renewable-energy companies. It underscores that companies should plan for an increasingly market-based and competitive environment.

Meanwhile, the government will also deepen cooperation with other countries on clean energy and “advance” global climate cooperation, it says.

A priority will be “strengthening” international coordination on investment and development in “green energy projects”. Another is “actively promoting the free circulation of China’s high-quality green technologies and products in global markets”.

Chinese exports of clean-energy technologies have been surging, especially since the closure of the strait of Hormuz.

At the same time, Chinese investment in clean-energy projects in Belt and Road Initiative member states totalled $20bn in the first half of 2026. This is also driven by the crisis.

The US, EU and others have launched tariffs and pricing mechanisms to curb imports of Chinese cleantech. This has contributed to pushback from China, against what it and others refer to as “unilateral trade measures”.

China is transitioning from a “major energy nation” (能源大国) to an “energy powerhouse” (能源强国), writes the Energy Research Institute’s Lyu in his explanatory reading. He says this will enable China to increasingly shift to building “systemic” advantages in developing clean-energy technologies.

He continues that, from 2026-2030, China will “move to the very forefront of the global stage” on clean energy, “venturing into uncharted territory”. This will create both “major new challenges and significant opportunities” for the country, he adds.

Interview: Dr Sun Yixian on his new database tracking Chinese climate ‘leadership’

SYDNEY/KINGSTON, Wednesday 29 July — The future of deep sea mining will be a focus for world leaders this week as the International Seabed Authority (ISA) Assembly takes place in Kingston, Jamaica.

Country delegates and members from Pacific Civil Society have come together to discuss a deep sea mining code, while the call for a moratorium grows. It follows the ISA’s contentious decision last week to extend The Metals Company subsidiary Nauru Ocean Resources Inc’s (NORI) exploration contract, despite its support for the pursuit of unlawful deep sea mining via US unilateralism.

The Assembly’s agenda was agreed to yesterday, with a science item put forward by Vanuatu to be heard on Thursday local time. Overnight, Mozambique and Mauritius joined the call for a global moratorium.

Rae Bainteiti, Pacific Political Coordinator at Greenpeace Australia Pacific, said from the ISA in Kingston:

“As we move into the General Assembly this week, the fundamental issue remains that there is not enough science to guarantee the safety and protection of the ocean in a world where deep sea mining is allowed. As trustees of the ocean, the common heritage of humankind, our Pacific governments must stand firm against corporate interests that are pushing to move ahead with deep-sea mining outside the ISA framework. If deep sea mining goes ahead, Pacific communities will suffer the economic, cultural and social consequences. We continue to call on all States to support a moratorium as the principled and responsible pathway to protect the ocean.”

Currently, 45 countries, including seven Pacific nations, support a moratorium or precautionary pause on deep sea mining. Last week, Australia’s Labor National Conference committed to supporting a moratorium, but the government has yet to make an official comment.

More of Germany’s electricity came from wind and solar power than fossil fuels for the first time ever in 2025.

Together, wind and solar power generated 225 terawatt hours (TWh) of electricity – accounting for 44% of the total in 2025 – with just 217TWh (43%) coming from fossil fuels.

Solar and onshore wind have grown rapidly under Germany’s “Energiewende” strategy over the past two decades, as the nation transitions away from both coal and nuclear power.

Renewables have recently faced mounting opposition from the far-right Alternative for Germany (AfD) party and the current coalition government has been trying to develop new gas-power plants.

Nevertheless, Carbon Brief analysis of Energy Institute data – shown in the chart below – illustrates how wind and solar have continued growing, emerging as the nation’s largest power source.

The success of renewables in Germany mirrors the EU as a whole, which also saw wind and solar overtake fossil-fuel power generation in 2025 for the first time.

“Other renewables” includes hydropower, bioenergy, geothermal and other renewable sources not otherwise stated. Source: Energy Institute Statistical Review of World Energy, 2026.

Germany has various targets in place that require a rapid expansion of wind and solar power, including cutting economy-wide emissions to net-zero by 2045.

The nation is also aiming to increase renewables’ share of electricity consumption to 80% by 2030 to achieve a “largely climate neutral” power system by 2035. It aims to decarbonise its electricity entirely once coal power has been phased out, which has a deadline of “no later than” 2038.

(The renewables targets also include electricity generated from hydropower and bioenergy. The latter produces a relatively large share of Germany’s power – roughly a tenth in 2025.)

Germany has to rely on renewables more than neighbours, such as France and the UK, to achieve its climate goals. This is due to its phaseout of nuclear power, which is a key part of the “Energiewende” strategy.

Nuclear power has long faced widespread public opposition in Germany. This year, the centre-right chancellor Friedrich Merz described the nuclear phaseout as a “strategic mistake”, but the government has ruled out a return to conventional nuclear power.

The country has an official coal phaseout date of 2038, but experts say the country is on track to eliminate coal from its power supply years earlier. This is despite some pressure to temporarily slow the transition away from coal during the recent energy crisis.

(Very few outside the AfD are calling to scrap the coal phaseout altogether, but the government will publish a review of the timelines in August.)

While coal generation has fallen quickly, even as nuclear was being phased out, some argue that coal could have been cut more quickly if nuclear had remained.

Gas-power expansion has also been framed by the government in recent years as an essential component of Germany’s transition away from coal and nuclear power, to support a renewables-heavy grid.

The current government under Merz has tried to boost gas and recently adopted a law to provide state support for new gas-fired power plants. The plan is for these plants to be converted to run on “green hydrogen” by 2045, in order to meet the climate-neutrality goal.

Germany aims to install 115 gigawatts (GW) of onshore wind by 2030 and approved a record 20.8GW of new capacity in 2025.

Meanwhile, solar generation has reached unprecedented levels during the hot summer of 2026.

However, the government’s planned grid reforms have been criticised by the renewables industry for risking slowing down the energy transition. Under the proposals, renewables developers would only be granted automatic grid connections in areas with limited grid capacity if they waive compensation for future curtailed generation.

Interview: COP31 president says electrification is ‘surest way to protect citizens’