Welcome to Carbon Brief’s Cropped.

We handpick and explain the most important stories at the intersection of climate, land, food and nature over the past fortnight.

This is an online version of Carbon Brief’s fortnightly Cropped email newsletter. Subscribe for free here.

Key developments

Amazon affairs

DRY SPELL: Climate change made last year’s agricultural drought in the Amazon around 30 times more likely to occur, according to a new rapid attribution study covered by Mongabay. The El Niño climate pattern “played a much smaller role” than many had assumed, the outlet said. World Weather Attribution scientists analysed data from the Amazon region between June and December last year, finding that both El Niño and climate change “contributed to reduced rainfall” during these months. But climate change “also led to high temperatures, significantly increasing water evaporation from plants and soils”, the outlet added. The report authors “predict that dry spells in the Amazon will become more frequent and harsher” under continued warming, Mongabay said.

CRIME COOPERATION: A $1.8m Amazon rainforest security centre will open in Manaus, Brazil in the coming months, Climate Home News reported. The centre is financed through the Amazon Fund and will “bring together Amazon nations in policing the rainforest, sharing intelligence and chasing criminals”, the outlet said. Climate Home News quoted Humberto Freire, head of the Brazil federal police’s environment and Amazon department, who said the centre will “fight drug trafficking and the smuggling of timber, fish and exotic animals, as well as deforestation and other environmental crimes”. It will also focus on illegal gold mining on Indigenous land, the outlet said.

LAND CONFLICT: Meanwhile, Brazil’s president, Luiz Inácio Lula da Silva, said the federal government will “help resolve” a land conflict between Indigenous people and farmers that led to the fatal shooting of a tribal leader, Reuters reported. Maria Fatima de Andrade was shot and killed after 200 land owners tried to “evict an Indigenous community” from a farm in the state of Bahia and take the land, which is claimed by the Pataxó tribe, the newswire said. Another leader was also shot and brought to hospital, Reuters said, noting that the incident “underlines years of tensions between Brazil’s Indigenous peoples and agricultural settlers over land rights”. The country’s minister for Indigenous peoples, Sonia Guajajara, said the attack was “unacceptable”, the newswire added.

Offsets scrutinised

EU BAN: Labelling products and services as “climate neutral” or “climate positive” based on the use of carbon offsets will be banned in the EU from 2026, the Guardian reported. Carbon offsets involve a polluting entity, such as an airline, paying for emissions to be reduced elsewhere, such as by preventing deforestation. Companies often use carbon-offsetting to make claims that their products are “net-zero” or “environmentally friendly”, but evidence – previously set out in detail by Carbon Brief – shows these can be exaggerated or misleading. On 17 January, members of the European parliament voted to outlaw the use of terms such as “environmentally friendly”, “natural”, “biodegradable”, “climate neutral” or “eco” without evidence. The European parliament also introduced a total ban on using carbon-offsetting to back up such claims, the Guardian reported. The NGO Carbon Market Watch called the move “a big step towards more honest commercial practices and more informed European consumers”.

GUYANA CREDITS: Elsewhere, the Financial Times reported on Guyana’s plans to generate $3bn from forest carbon offset schemes by the end of the decade. Forests currently cover 85% of the South American country’s land surface, the FT said, with the government estimating they could generate credits representing 19.5bn tonnes of CO2 – more than the annual emissions of China. However, offsetting plans could be put at risk by conflict with neighbouring Venezuela, which has threatened to annex more than half of Guyana’s territory, the FT said. It added that most of Guyana’s forests are in the mineral-rich region of Essequibo, “a tract of Amazon jungle that would be a prime target for Venezuelan loggers and miners in the event of a takeover”.

COOKSTOVE CONTROVERSY: Finally, Heatmap was among several publications covering a new study finding that carbon offset schemes using so-called “clean” cookstoves are “kind of bogus”. Clean cookstove schemes involve the distribution of more efficient cooking equipment, with the goal of cutting reliance on traditional fuels, such as firewood – leading to lower emissions. The study from researchers at the University of California, Berkeley, found that cookstove projects have generated, on average, nine times more carbon credits than they should have, Heatmap reported. The research was published in the journal Nature Sustainability.

Spotlight

French farmers and the far right

In this spotlight, Carbon Brief looks at the ongoing EU farmer protests and how far-right political groups could latch on to the outrage ahead of the European parliament elections in June.

Farmers have used tractors to blockade the streets of Berlin, Brussels and Bucharest in recent weeks. Farmers across the EU have been protesting against “competition from cheaper imports”, tightening environmental rules and rising production costs, according to Reuters.

This week, the French farmer protests escalated. Hundreds of tractors blocked off major roads into the country’s capital in what has been dubbed the “siege of Paris” by many media outlets, including BBC News. President Emmanuel Macron is “scrambling to end an escalating political and social crisis”, the Times said.

According to Le Monde, farmers are raising issues around “pesticides, free-trade agreements and wages”. France is an EU agricultural powerhouse, producing huge amounts of meat, dairy and wheat each year.

The nation’s newly appointed prime minister, Gabriel Attal, announced some concessions to farmers, including simplified technical procedures and a “progressive end to diesel fuel taxes for farm vehicles”, the Associated Press reported.

But the two main farmers’ unions said these measures did not go far enough and vowed to continue the protests.

The protests are the “first big test” of Attal’s leadership, Bloomberg noted. And, just months out from the European parliament elections, Euractiv said they are also the “first major political test for EU election candidates in France”.

Ahead of these elections, Politico said that right-wing parties in countries – such as France, Italy, the Netherlands and Germany – are “piggybacking on farmers’ noisy outrage”. Recent polling has suggested that there could be a “sharp turn to the right” in the June vote, Deutsche Welle reported.

Dr Gilles Ivaldi, a politics researcher at Sciences Po who has examined the far right in Europe, said that right-wing groups may use the farmer protests to “boost their electoral support” in France and elsewhere. He told Carbon Brief:

“What we see, particularly in France, is that the far right is seeking to capitalise on public discontent with the impact of the green transition, not only among farmers but also in social groups affected most by the economic cost of environmental policies.”

He said the French far right is “clearly trying to instrumentalise” the farmer protests to “mobilise against the government and the EU”. Sky News said the protests “are being seized upon by various groups”, including Marine Le Pen’s right-wing Rassemblement National party.

But Ivaldi noted that the far right’s EU election focus will mostly remain on topics such as immigration, the economy, the future of the EU and the bloc’s Green Deal. The “main factors” behind a potential right-wing surge will not come from agriculture alone. He added:

“Far-right parties are currently capitalising on the economic crisis and rise in prices, on the immigration issue, particularly growing concerns about the massive influx of refugees in Germany and, more broadly, the many anxieties caused by the war in Ukraine and geopolitical instability.”

News and views

LET’S EAT BALANCED’: A £4m advertising campaign aimed at convincing young people to eat more meat and dairy has been released in the UK, with support from the government, DeSmog reported. Timed to coincide with Veganuary (a popular challenge where people go vegan for January), the “Let’s Eat Balanced” campaign – voiced by British comedian Richard Ayoade – targets cinema screens, TVs, newspapers, social media channels and major supermarkets, DeSmog said. The campaign attempts to communicate the health benefits of eating meat and dairy, which “flies in the face of science”, experts told DeSmog. It was developed by the PR agency Ogilvy, which counts BP as a former client, and is run by the Agriculture and Horticulture Development Board, a UK government-appointed board funded by farmers’ levies.

AT SEA: Chile and Palau became the first countries to officially sign off on the High Seas Treaty, Euronews Green reported. Palau was the first to ratify the treaty governing the sustainable use and conservation of international waters since it was agreed last March, the outlet said. The Chilean senate “unanimously” voted in favour of ratification, which will become official “once it is published in the government’s official journal”. The outlet quoted Rebecca Hubbard, director of the High Seas Alliance, who said she hopes Palau “inspires” others to “redouble their efforts to ratify the treaty without delay so that it can enter force as soon as possible” once 60 nations sign off.

COLOMBIA FIRES: Colombia, due to host the biodiversity summit COP16 later this year, is currently battling intense fires in the mountains around the capital city of Bogotá, as dozens of other blazes have burned across the country, the New York Times reported. The president, Gustavo Petro, has declared a national disaster and asked for international help fighting the fires amid the country’s hottest January in three decades, according to the publication. It comes after the UN Convention on Biological Diversity announced that six cities in Colombia have expressed interest in hosting COP16. It is not yet clear if the fire emergency could affect Colombia’s ability to host the summit.

TAKE OFF: The world’s first plant using ethanol partly made with corn to produce “sustainable aviation fuel” opened in the US, Bloomberg reported. The $200m facility in Georgia plans to use the ethanol made from “American-grown corn, as well as from advanced technologies”, the outlet said. The facility’s opening spurred industry groups in Iowa – the US state that produces the most corn – to warn farmers and ethanol producers that they risk “missing out on the chance to significantly profit from the developing market for sustainable aviation fuel”, the outlet said. A 2022 study found that corn-based ethanol is likely more carbon-intensive overall than petrol, Reuters previously reported.

HUNT FOR POWER: Climate Home News investigated lithium mining in Zimbabwe, where Chinese companies have “flocked” to secure supplies of the lightweight metal, which is crucial for electric vehicle batteries. Lithium mining “brought the promise of jobs and a better life” for some, the piece outlined, but the country’s “poor progress on establishing robust resource governance” could prevent local communities from “seeing any of the benefits”. The country’s president, Emmerson Mnangagwa, “aspires to turn Zimbabwe into a battery manufacturing hub” to help “catapult the country into an upper-middle-income economy by 2030”, the outlet said.

CAMBODIA DEFORESTATION: A Mongabay investigation alleged that a vast forested wildlife sanctuary in Cambodia is being put at risk by mining concessions granted by the government to a “timber baron” who has previously been sanctioned over corruption in relation to natural resource extraction. In 2023, the Cambodian government announced a ban on extractive practices inside the Prey Lang Wildlife Sanctuary, a “sprawling carbon sink” home to 250,000 Indigenous peoples, according to Mongabay. However, the government made an exemption for companies that had already been awarded contracts, it added. This included the mining company of Try Pheap, “a powerful tycoon and adviser to the previous prime minister”, Mongabay said. Mongabay was unable to make contact with the Cambodian government or representatives of Try Pheap, despite repeated attempts.

Watch, read, listen

TREE GRIEF: Al Jazeera spoke to Palestinians who are grieving the loss of their olive trees, which have long been a symbol of the Palestinian spirit, amid Israel’s assault on Gaza.

HIT THE WAVES: The Climate Question, a BBC podcast, looked towards Northern Ireland and South Korea to see why tidal power is not more commonly used in renewable energy.

TINY WILD CAT: A long read by Mongabay explored how conservationists are working to save the guina, the Americas’ smallest wild cat species, native to Chile and Argentina.

‘BLACK MOSS’: The South China Morning Post examined the Chinese new year staple “fat choy” and how its overharvesting has turned parts of China “into desert”.

New science

Atmospheric CO2 emissions and ocean acidification from bottom-trawling

Frontiers in Marine Science

Bottom-trawling – the fishing practice where nets are scraped along the seabed – could have caused the release of up to 370m tonnes of CO2 between 1996 and 2020, a new study found. As well as being harmful for wildlife living near the bottom of the ocean, bottom-trawling disturbs carbon that was previously locked up for millenia, the researchers said. They used a combination of satellite data tracking fishing events and carbon cycling modelling to examine how bottom-trawling could cause CO2 emissions. The researchers also found that, in heavily trawled seas, the volume of carbon released is likely to be enough to drive ocean acidification – known to be harmful to a range of ocean wildlife, from coral reefs to fish.

Multi-decadal trends of low-clouds at the tropical montane cloud forests

Ecological Indicators

New research suggested that low-cloud cover is declining over tropical montane cloud forests because of climate change, posing an existential threat to these unique mountain ecosystems. The study used climate data to study changes to the proportion of sky covered by cloud cover and other climate variables in 521 tropical montane cloud forests across the world from 1997 to 2020. The researchers found that proportional cloud cover has declined at 70% of these sites, with cloud forests in central and South America and south-east Asia most affected. Decreases in cloud cover were associated with increases in surface temperature and decreases in soil moisture, “revealing that the tropical montane cloud forests’ climate is changing”, the researchers added.

Livestock increasingly drove global agricultural emissions growth from 1910-2015

Environmental Research Letters

Emissions from agriculture in 2015 were more than three times bigger than they were around one century prior, a study found. Scientists developed a dataset of global emissions from the agriculture sector across 10 time periods between 1910 and 2015. They found that agriculture emissions from livestock, soil management and fossil energy inputs “increased continuously” during this time by an overall factor of 3.5, with methane accounting for the majority of these emissions. The study said that reduced emissions intensity, especially for livestock, “partly counterbalanced” the overall rise in emissions to varying degrees. The researchers wrote that the findings “underscore the large potential of reducing livestock production and consumption for mitigating the climate impacts of agriculture”.

In the diary

- 6 February: European Commission to publish 2040 emissions-reduction target recommendations

- 12-17 February: Fourteenth meeting of the Conference of the Parties to the Convention on the Conservation of Migratory Species of Wild Animals | Samarkand, Uzbekistan

- 14 February: Indonesian general election

Cropped is researched and written by Dr Giuliana Viglione, Aruna Chandrasekhar, Daisy Dunne, Orla Dwyer and Yanine Quiroz. Please send tips and feedback to cropped@carbonbrief.org

The post Cropped 31 January 2024: French farmers and the far right; Amazon affairs; EU offsetting ban appeared first on Carbon Brief.

Cropped 31 January 2024: French farmers and the far right; Amazon affairs; EU offsetting ban

Low-income Indian workers, many of them migrants from rural areas hit by climate change, are paying for worsening extreme heat through lost working days and health complications, with the cost equivalent to 2% of national GDP per year, new research shows.

The International Institute of Environment and Development (IIED), a London-based think-tank, worked with local organisations to survey around 540 households of informal workers in three Indian cities: Ajmer, Delhi and Agra. Most had migrated from rural areas to find work in industries such as construction, brick-making, garment manufacturing and food packaging.

The survey found them struggling through long working days with little access to shade, cooling, rest or water, as well as few toilets for women. And even when they go home, many live in makeshift shelters or airless cramped rooms with barely a single fan, bringing almost no respite.

Outdoor workers are losing about 24 days of work a year due to heat, costing them nearly a tenth of their annual earnings, while indoor workers sacrifice roughly 15 days. On top of losing income, they are also bearing the cost of health problems like heat exhaustion, psychological stress and kidney damage brought on by repeated dehydration.

If the survey’s findings are extrapolated to a national level, the IIED researchers estimate that the decline in productivity and effects of kidney disease combined add up to lost wages of $78 billion each year.

-

Top maritime court rejects bid to halt UN deep-sea mining inquiry

Two subsidiaries of The Metals Company sought to block the probe into potential contract breaches launched after the firm’s application for US-sponsored permits -

Most “zombie credits” locked out of new UN carbon market after China and India snub

Fears of a flood of environmentally-dubious carbon credits have faded, with most old projects not able to transition to new UN market

Vishram Meena, 45, from Alwar in Rajasthan, has worked on construction sites in Ajmer for more than a decade, toiling for 10 to 12 hours a day carrying materials and mixing cement in the full sun.

In May 2024, on one of the hottest days, he collapsed after feeling dizzy and suffering a nosebleed. His wife and colleagues managed to get him to hospital where he was diagnosed with heat stroke. He has since returned to the same building work because the family needs the money.

“I went back because what else could I do? We are not machines. We are human beings. The heat is killing us slowly,” he was quoted as saying in a report on the survey’s findings.

“Victorian-era” conditions

Ritu Bharadwaj, IIED’s director of climate resilience, finance and loss and damage, described some of the stories from workers about their experiences of extreme heat as “genuinely horrifying”.

Kusum, a tailor at a garment manufacturing and export unit in Kapashera, Delhi, recounted how the machines for ironing finished garments are in the same tiny room where workers are making the clothes, with steam and hot air building up through her shift.

Fans are too far apart to move the air and nothing has changed in over a decade, she said, adding that “in summer, the unit feels like a furnace”.

“These are Victorian-era working conditions and they’re completely unacceptable in the 21st century,” said Bharadwaj. She called for stepped-up social protection from the government to pay people for days they are unable work due to heat, as well as micro-insurance schemes with payouts triggered by temperature measurements.

This money would help families buy food and pay medical bills when their income dips if they fall ill or cannot work their usual hours due to soaring temperatures.

Climate change-driven heatwaves hit Delhi’s Red Fort market traders

The aim of the IIED study, Bharadwaj added, is to get policy-makers’ attention by showing the scale of damage extreme heat is doing to India’s GDP in an economy whose growth relies on service-led industries. “If the workers within them start falling sick, you know it’s the economic growth which is going to get impacted,” she told a webinar to present the research.

“Whether [policymakers] care about the workers or not, at least they would care about the GDP, and therefore then invest in their care,” she explained.

Labour code leaves out heat

However, Bharadwaj noted that a 2026 reform to India’s labour law bringing a range of regulations together in one code does not include heat-related protections for workers and only applies to businesses above a certain size. She urged the government to introduce a temperature threshold above which all workers would be able to stop their activities.

IIED and its partners have also carried out a similar study in Bangladesh which will be published later this month, showing that extreme heat is costing its workforce the equivalent of nearly 1.4% of GDP.

Shakirul Islam, chairperson of the Ovibashi Karmi Unnayan Program (OKUP) in Bangladesh, said the government had introduced stricter safety policies for garment-making companies after the Rana Plaza complex collapsed in 2013. But, he said, these rules are rarely followed by manufacturers, especially at the level of smaller subcontractors.

The workers’ welfare centres that do exist are open mainly during work hours so they are difficult to visit. Some companies also make saline water available for heat stress, which is no good for those with high blood pressure, he noted.

For Indian women workers, a just transition means surviving climate impacts with dignity

Archana Shukla Mukherjee, CEO of India’s Change Alliance, which also partnered with IIED on the survey, said it was time to hold both the government and businesses accountable for finding solutions to the intensifying problem of extreme heat’s effects on workers.

She said that employee state insurance schemes should identify heat stroke as an occupational disease while companies along the whole supply chain should start putting in place heat protection measures, including for informal workers and migrants.

If the tools and mechanisms available to help workers do not reach the most vulnerable and marginalised people, “then I think we are not doing something right,” she said.

The post Extreme heat costing India’s poorest workers 2% of GDP, survey finds appeared first on Climate Home News.

Extreme heat costing India’s poorest workers 2% of GDP, survey finds

A United Nations investigation into deep-sea mining firms will continue after the world’s top maritime court rejected their bid to suspend the inquiry triggered by a US-backed push to extract critical minerals from the ocean floor.

In two orders issued on Saturday, the International Tribunal for the Law of the Sea (ITLOS) declined to halt an inquiry launched by the International Seabed Authority (ISA) into whether permit holders, including Tonga Offshore Mining Ltd (TOML) and Nauru Ocean Resources Inc (NORI), have breached their obligations under UN exploration contracts.

The two companies are subsidiaries of Canadian firm The Metals Company (TMC), which earlier this year sought permits from the United States to commercially mine the deep seabed in an area already covered by its UN exploration licences, bypassing the ISA’s regulatory process.

The inquiry was opened after TMC’s move raised questions over whether its subsidiaries had complied with their contractual obligations to the ISA, which regulates mining in international waters under the UN Convention on the Law of the Sea. TOML and NORI sued the ISA last June for allegedly targeting them “in breach of due process” and without “good faith”.

-

UN seabed regulator defends authority as mining firms seek to halt inquiry

Campaigners accused deep-sea mining frontrunner The Metals Company of obstructing an inquiry into its subsidiaries. The firm says it is being targeted without procedural basis -

Flood deaths in West African cities raise fraught issue of slum evictions

Deadly floods expose poor urban planning, over-population and spread of informal settlements on disaster-prone land – a problem authorities are struggling to manage -

Most “zombie credits” locked out of new UN carbon market after China and India snub

Fears of a flood of environmentally-dubious carbon credits have faded, with most old projects not able to transition to new UN market

While allowing the inquiry to proceed, the court ordered the ISA to ensure the companies receive due process. Judges said the regulator must explain the factual and legal basis of its inquiry, clarify the procedures being followed and provide TOML and NORI with a meaningful opportunity to respond.

The companies seeks to mine an area called the Clarion-Clipperton Zone, which holds vast reserves of critical minerals like nickel, manganese and rare earths but is also home to a little-studied deep ocean ecosystem with thousands of unnamed species.

In response to the court’s ruling, the ISA welcomed the decision, saying the inquiry “remains in effect” and would continue “with due regard to all applicable legal requirements”.

Last week, during an annual meeting of its member governments, ISA secretary-general Leticia Carvalho said the resources in the ocean floor are “the common heritage of humankind” and upheld the agency’s role as “more important than ever”.

TMC also welcomed the court decision in a statement and claimed that judges ruled to “protect the rights of TMC subsidiaries”.

“Contractors like NORI and TOML, who have together spent hundreds of millions of dollars on the promise of a fair regulatory framework, should be informed of the factual and legal basis of any non-compliance inquiries, understand the procedure being applied, and receive a meaningful opportunity to respond,” said Gerard Barron, CEO of The Metals Company.

Environmental groups said the ruling allows scrutiny of the companies’ actions to continue.

Louisa Casson, deep-sea mining campaigner with Greenpeace, said the “entire litigation has been an egregious waste of time and money”, which was part of the industry’s “textbook distraction tactic” meant to delay the consequences of the inquiry.

“If the inquiry confirms that TMC’s subsidiaries are breaching their contracts, governments must send the strongest possible signal that complicity in unlawful deep sea mining will not be tolerated,” she said.

While investigation is still ongoing, NORI’s contract is set to expire this week and is up for review. Governments asked the ISA to report back and make “make appropriate recommendations” by the next ISA assembly, its main decision-making body set to take place next week from July 27 to 31.

The court ordered both the ISA and TMC to submit a report on how they complied with the ruling by August 31, and called on both to “cooperate and refrain from any action that might lead to

aggravating the dispute”.

The post Top maritime court rejects bid to halt UN deep-sea mining inquiry appeared first on Climate Home News.

Top maritime court rejects bid to halt UN deep-sea mining inquiry

The European Commission has put forward new plans to cut emissions under the EU carbon market more slowly, from 2031 onwards.

On 17 July, the commission presented its long-awaited proposal for reform of the EU’s Emissions Trading System (ETS).

It recommended a number of changes, including giving companies free allowances to cover their emissions for longer than previously planned, conditional on climate investment plans.

The proposal offers a more business-friendly and “savvy” approach, argued EU climate commissioner Wopke Hoekstra in a press conference.

But critics believe it could “weaken” the system and put EU climate targets at risk.

Alongside the proposal, the commission also announced a new target for electricity to make up 46% of energy consumption by 2040, doubling the current rate of 23%.

This could cut EU spending on imported fossil fuels by €260bn annually, according to the commission.

In this Q&A, Carbon Brief outlines the details of the new ETS proposal – which is subject to negotiation with member states – and explores what it could mean for climate action.

- What is the EU Emissions Trading System?

- What did companies and countries want from the ETS review?

- What is in the new proposal from the European Commission?

- What could the changes mean for greenhouse gas emissions?

- How was the proposal received?

- What is ‘ETS2’?

- What happens next?

What is the EU Emissions Trading System?

The EU ETS is a carbon market, which puts a price on the greenhouse gas emissions of companies in power generation, industry, aviation and other sectors.

It covers everything from electricity generation to steel production, as well as flights within the EU and a handful of other European countries.

Emissions in these sectors have halved since the ETS launched in 2005, according to the European Commission.

A European parliament briefing describes the system as a “cornerstone” of EU climate policy, covering around 40% of the bloc’s overall emissions.

It applies to emissions in all 27 EU countries alongside Iceland, Liechtenstein, Norway and electricity generation in Northern Ireland. (The UK established its own ETS after Brexit.)

The ETS operates as a “cap and trade” system, which puts a limit on the amount of carbon dioxide equivalent (CO2e) that can be emitted within the sectors it covers.

The “cap” on emissions gradually decreases each year until, eventually, they are expected to reach zero.

The currency of trade within the system is “allowances”. One allowance is equal to one tonne of CO2-equivalent emissions.

At present, around 57% of these allowances are bought by companies in auctions. The EU generated around €43bn in revenue from these auctions in 2025.

The remaining 43% of allowances are given to companies for free, to cover some or all of their emissions.

This is intended to prevent “carbon leakage” – the idea that companies operating in countries with strict climate policies will relocate to countries with looser rules.

The amount of free allowances varies by sector, depending on factors including the level of competition with overseas firms that do not face a carbon price.

What did companies and countries want from the ETS review?

Countries and companies have been divided on how they wanted the ETS to evolve.

Some pushed for more ambition to help meet European climate goals. Others called for it to be rolled back, amid rising costs for businesses.

In March, 10 countries including Italy, Hungary and Poland wrote a letter to the commission calling the ETS an “existential risk” for key industrial sectors, reported Euronews.

Italy had earlier even called for the system to be suspended outright.

France and other countries favoured introducing a slower descent towards bringing the emissions cap to zero by 2039.

Some steel and chemical companies also criticised the cost burden of the ETS.

Other organisations focused on calls for stability and predictability in the system.

In recent weeks, Spain, the Netherlands and five other countries called on the commission to “resist gutting” the ETS in its review, said E&E News. They said the ETS should be strengthened to “ensure long-term investment predictability and regulatory stability”.

Weakening the system could “undermine investment signals and leave Europe more exposed to fossil-fuel shocks”, said a March 2026 briefing from climate thinktank E3G.

Another E3G briefing said the “risk” is that politicians weaken the system as a short-term economic fix, “undermining one of the EU’s main tools for delivering on its industrial transformation ambitions”.

Dozens of investment organisations called on EU countries to facilitate a “robust and predictable” ETS. They said that “policy stability is the cheapest investment stimulus available to the EU”.

In its list of priorities for ETS reform, the NGO Carbon Market Watch said that “now is not the time to backslide” on its aims and terms.

What is in the new proposal from the European Commission?

The commission’s proposal outlines a number of changes to the ETS, to bring it in line with the EU’s climate goal to cut emissions to 90% below 1990 levels by 2040.

The review will “bring relief to industry”, the commission says, while also continuing the ETS’ “essential” role in climate action.

However, others are more sceptical about the impacts it could have on climate action.

Below, Carbon Brief details the main aspects of the proposal.

Free allowances extended

The European Commission proposes to extend free allowances beyond a previously agreed date.

Free allocations were due to reduce from this year and be fully removed by 2034.

However, the commission has proposed to extend this to 2038, on the condition that companies receiving free allowances set out how they will invest in decarbonising their EU operations.

It proposes that from 2031 onwards, 80% of free allowances in the system would be given to companies that have submitted plans for investment in EU decarbonisation.

The remaining 20% of free allowances would only be allocated to those that can prove they followed through with planned investments and achieved the emissions reductions they had previously outlined.

This move is a “step in the right direction”, says Dr Kirsten Scholl, the director for EU affairs at thinktank Epico, but it must not “impose excessive administrative burdens”.

The EU’s carbon border adjustment mechanism (CBAM) was designed to replace the existing system of free allowances in the ETS.

It is a tax applied to certain imported goods, based on the amount of CO2 emissions released during their production. It began to be phased in at the start of 2026.

As a result, free allocation is being gradually phased out from 2026-38.

However, the commission has proposed that 15% of free allocations due to be removed because of CBAM should be reintroduced from 2028, to “reduce the speed at which CBAM is phased-in and mitigate the remaining carbon leakage risk”.

The commission says that preventing carbon leakage “remains a crucial element” of the ETS.

Pushing back the phase-out of free allowances and the full implementation of CBAM “risks squandering the EU’s credibility with investors and trading partners alike”, says Francesco Lombardi Stocchetti, a policy advisor on sustainable economy at the Bellona Foundation, an environmental NGO.

“Europe cannot lead the clean industrial transition just by moving the goalposts,” he adds in a statement.

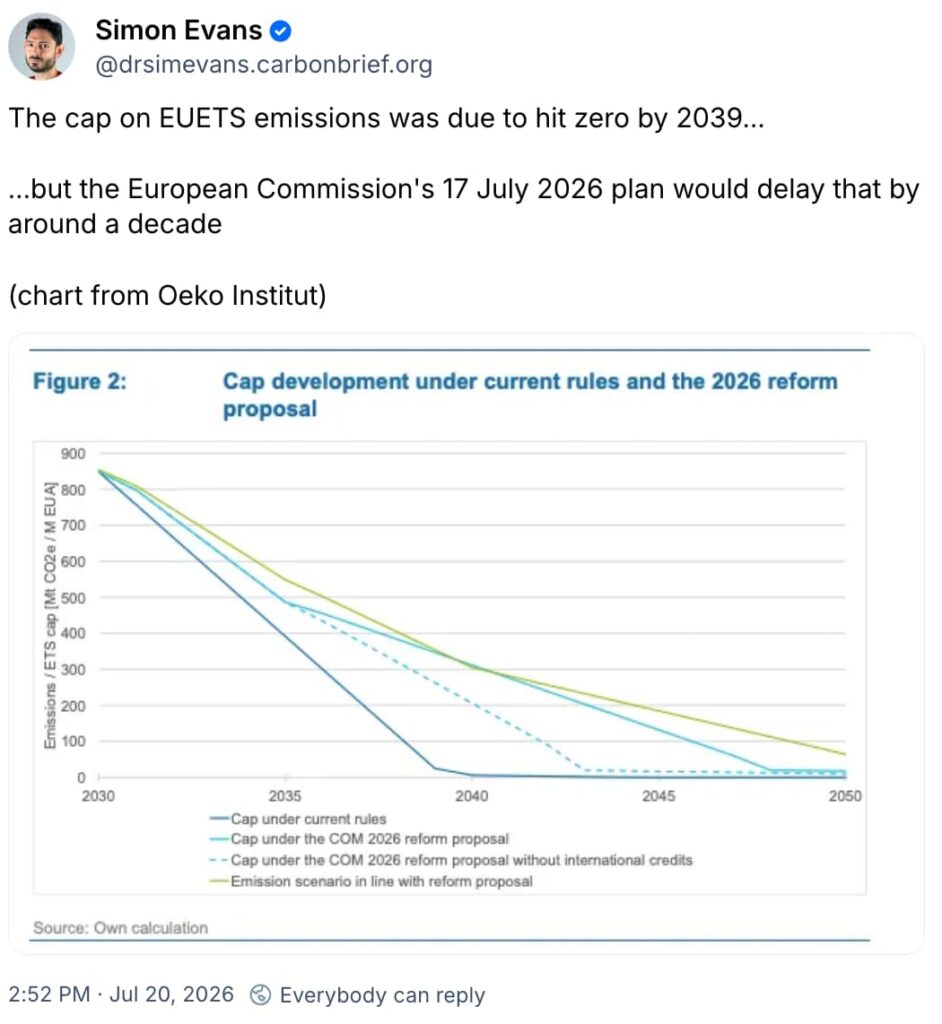

Slowing path to reach zero emissions by a decade

The commission has proposed to cut emissions in the ETS more slowly from 2031 onwards.

This could mean new allowances are able to enter the scheme into the 2040s, instead of ending in 2039 as previously planned.

But the planned changes are still “aligned” with the EU’s 2040 climate target and net-zero requirement by 2050, says the commission.

The overall ETS cap on emissions was reduced by 1.7% each year up to 2020 and then by 2.2% annually since 2021.

It is then agreed to drop by 4.3% over 2024-27 and 4.4% from 2028 onwards.

Maintaining similar rates after 2030 would not be “realistic”, says the commission’s proposal.

Instead, it suggests that the cap should fall by 3.7% per year over 2031-35 and by just 1.7% annually over 2036-40.

This will make the path to zero emissions within the ETS “more gradual and aligned with domestic climate ambition level”, claims the commission.

But WWF says that the proposal would allow an extra 2bn tonnes of CO2e to be emitted. (See: What could the changes mean for greenhouse gas emissions?)

Aviation

The commission has proposed plans to incorporate more airline emissions into the ETS.

The plan outlines that, from 2029, all flights departing from the European Economic Area (EU, Iceland, Liechtenstein and Norway) and landing in other countries within 5,000km of a point in central Europe should be added to the ETS.

This distance means that the changes would not apply to flights landing in China or the US. (Both the US and China have opposed the expansion of ETS coverage for flights.)

The commission also proposes including emissions from private jets and other “business flights” in the ETS.

It notes that aviation currently accounts for 14% of EU transport emissions. This is expected to skyrocket to around 90% by 2050, given it is more difficult to decarbonise than other modes of transport.

Some aviation emissions have been included in the ETS since 2012. This included emissions from air travel within the EEA and flights departing from Switzerland and the UK.

The airline industry did not respond favourably to reports of plans to expand beyond this scope.

On 8 June, the biggest airlines in Europe urged commission president Ursula von der Leyen not to extend the ETS to cover international flights, saying that it would raise ticket prices.

A study commissioned by Carbon Market Watch found that the ETS encompassing all flights departing from the EEA, not just those within it, would result in a “very small impact on ticket prices and passenger demand”.

Auction money

Under the proposed changes, EU countries would need to funnel half of the money they receive from ETS auctions towards decarbonising sectors covered by the system.

This would amount to more than €100bn in investment for decarbonisation before 2030, says the commission.

Around three-quarters of the money generated by the ETS has been allocated to EU countries since 2013, the proposal notes.

Since 2023, countries have been required to spend all of this money on climate and energy-related activities – at least on paper.

But the proposal says the “transparency and effectiveness” of this mechanism has been “insufficient”.

Currently, only around 5% of the ETS money “directly supports industrial decarbonisation in sectors such as steel, chemicals and fertilisers”, it adds.

Going forward, the proposal says that 50% should be put towards actions aiding clean-energy plans, industrial decarbonisation and improved waste management, as some examples.

A briefing by thinktank Institut Montaigne noted that the money generated within the system for EU countries to help finance the energy transition should be “at the heart” of ETS discussions, amid budget constraints in many EU countries at the moment.

CO2 removals

The commission has proposed integrating permanent carbon removals into the ETS to “give additional flexibility” for certain sectors that struggle to decarbonise. This action was previously agreed within the terms of the EU’s 2040 climate target.

“Permanent” removals refer to direct air capture with carbon storage and similar measures, rather than temporary removals such as planting trees.

The removals would be integrated into the system by increasing the allowance cap by an amount equivalent to the number of removals purchased.

This will set up “additional emission space” for hard-to-abate sectors and also support the “scale-up of the carbon removals industry”, outlines the proposal.

It also proposes that certain companies, such as shipping and aircraft operators, could compensate for their emissions with their own certified carbon removals.

These emissions would not be permitted to “go beyond zero”, adds the proposal.

Sven Harmeling, the head of climate at Climate Action Network (CAN) Europe, says that adding carbon removals “would weaken the ETS impact, undermine the carbon price and create new loopholes for polluters instead of accelerating the transition away from fossil fuels”.

The proposal “fails to ensure that only high-integrity removal technologies would be considered”, he adds in a statement.

However, the director of the Potsdam Institute for Climate Impact Research, Prof Ottmar Edenhofer, describes the move as “an important step”, saying:

“For the first time, it creates a credible and long-term investment framework for carbon-removal technologies in Europe.”

International credits

The commission proposes that firms covered by the ETS could make use of “high-integrity” credits bought on the global carbon market from 2036 onwards.

This relates to the EU’s 2040 climate target, in which up to 5% of the 90% reduction in GHGs can come from global carbon credits.

Amélie Laurent, a policy advisor in carbon accounting at the Bellona Foundation, says in a statement that these credits “should be in a strategic last resort reserve, not an excuse to avoid doing our homework”.

Aurora D’Aprile, the EU policy director at the International Emissions Trading Association, notes in a statement:

“For international credits, early preparation on governance and procurement and greater certainty around a pilot from 2031, will be essential to establish a credible demand signal.”

Other sectors extended

The commission has outlined plans to expand the inclusion of the maritime sector in the ETS.

Maritime accounts for around 4% of the EU’s total emissions. The new proposals for the sector include adding certain small ships of 400-5,000 tonnes to the system.

The proposal also outlines plans to incorporate more waste incineration into the ETS on a gradual basis from 2031.

Since 2024, some waste-burning companies have been required to monitor and report their emissions under the ETS. But they did not have to purchase credits.

Now, the commission proposes introducing the sector on a gradual basis.

Under the proposals, companies would require allowances for 25% of their emissions in 2031, 50% in 2032, 75% in 2033 and 100% from 2034 onwards.

Market stability reserve review

The market stability reserve was added to the ETS in 2019 to help stabilise the flow of allowances.

It acts like an overflow container holding extra allowances. If the number of allowances in the market falls below a certain threshold, more are brought out from the reserve to balance things out.

Equally, if the market is flooded with too many allowances, depressing prices, then some are removed and put into the reserve.

The commission has proposed a reform of the reserve, including changing the upper and lower limits for when allowances are released or removed.

It wants to reduce the rate at which allowances are withdrawn from auctions when they exceed a certain threshold from 24% to 12% from 2028.

This means that the permits would be able to stay in the market for longer.

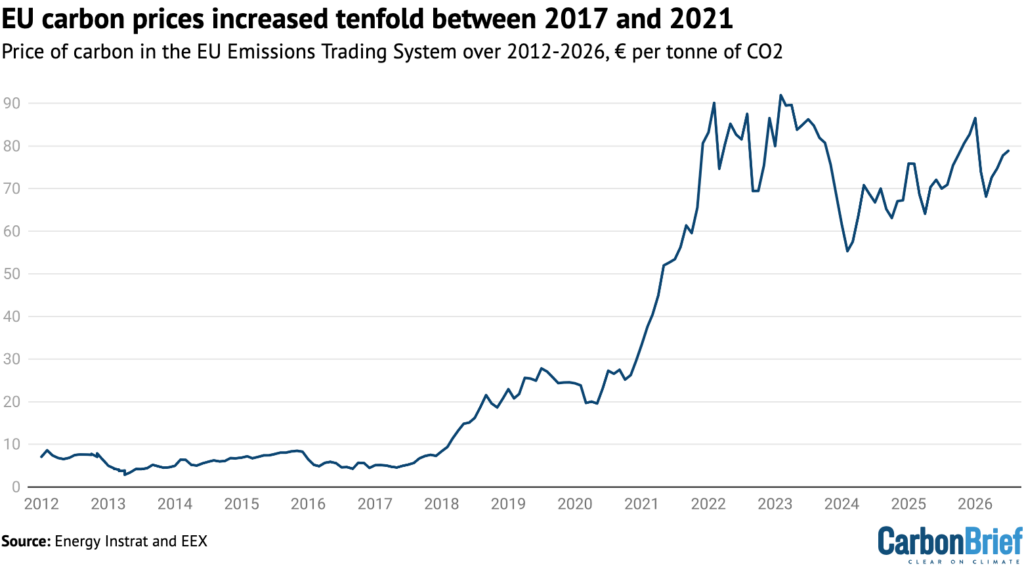

As shown in the chart below, the price of carbon in the EU increased tenfold over 2017-2021, exceeding €80 (£68) per tonne of CO2.

Nevertheless, the commission proposal says the reserve was “effective in mitigating price shocks” on the ETS caused by the Covid-19 pandemic and the surge in energy prices after Russia invaded Ukraine in 2021.

UK-EU ties

The EU and UK have agreed in principle to link their carbon markets, but the commission’s proposal says negotiations are still “under progress”.

It adds that the commission “foresees” future financial contributions from the UK to the EU’s ETS, if a final agreement is reached.

Many companies have called for the systems to be linked. In June, dozens of carbon-capture organisations and industry groups signed a letter calling for greater certainty on EU-UK links to ensure cross-border carbon-capture and storage projects are covered, for example.

Switzerland’s ETS has been linked to the EU since 2020.

What could the changes mean for greenhouse gas emissions?

The European Commission says the ETS plays a “crucial role” in meeting its climate targets “cost-effectively”.

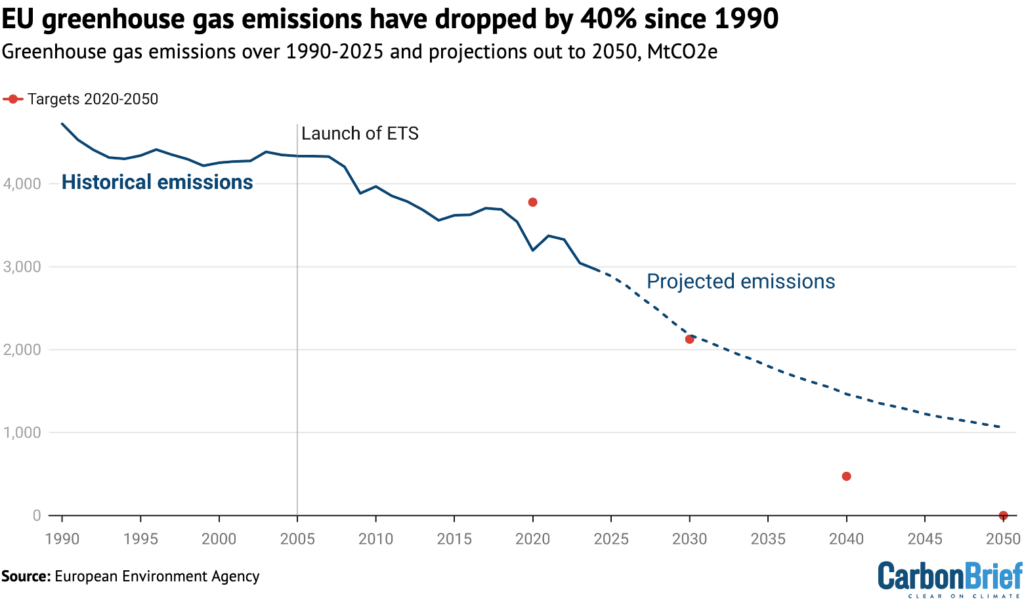

The system contributed to a 41% reduction in EU industrial emissions over 2021-23, a decrease of around 800m tonnes of CO2 per year, according to recent analysis from the London School of Economics.

As highlighted in the chart below, the EU’s overall GHG emissions have dropped by 40% since 1990.

Climate commissioner Hoekstra told a press briefing that the proposal is “fully aligned” with the EU’s target to cut GHGs to 90% below 1990 levels by 2040. He called the plan “completely climate-law proof”.

He also noted that no other EU policy has contributed to reducing emissions on the scale of the ETS, describing it as a “phenomenal asset”.

But campaigners and experts are concerned that the proposed changes could slow decarbonisation and put the EU’s climate goals at risk.

Carbon Market Watch says the plans would “severely weaken” the ETS and “risk undermining the achievement of the EU’s 2040 and 2050 climate targets”.

The proposals “would represent a major setback for EU climate ambition, weakening incentives to cut emissions, extending reliance on fossil fuels and putting the 2040 climate target at risk”, says a statement from WWF.

WWF estimates that 2bn extra tonnes of CO2 would be emitted if the proposals were approved in the EU.

Michael Bloss, a German member of the European parliament (MEP) for the European Greens, says the plans would release around 1.4bn tonnes of extra CO2. He describes the proposal as “climate vandalism”.

Chiara Martinelli, the director of CAN Europe, says:

“Every extra tonne of CO2 allowed under the ETS makes Europe’s climate challenge harder and more expensive. Weakening the ETS now is a gift to polluters that have prioritised shareholder payouts instead of investing in cleaner production.”

How was the proposal received?

The European Commission’s new ETS proposal has been met with a mixed response.

Scholl from Epico says the proposal has “important flexibilities that can help address competitiveness challenges and provide greater certainty for industrial investment”. But she adds in a statement:

“Concerns remain about whether the proposed changes preserve the long-term investment signal of the ETS and sufficiently recognise companies that have already committed to ambitious decarbonisation pathways.”

Edenhofer from the Potsdam Institute for Climate Impact Research adds that the proposals provide “clarity on the contribution that emissions trading is intended to make towards the 2040 climate target”.

Elisa Giannelli, a programme lead at E3G, says in a statement:

“Today’s proposal might please some, but it risks increasing both the long-term cost and the time needed to deliver the EU’s growth strategy.”

Pepe Escrig, a senior researcher, also at E3G, adds that the commission held onto some of the ETS’ “essential foundation”, but “yielded to political pressure to weaken it as a quick fix to broader challenges”.

This has left the plan “pull[ing] in two directions: strengthening support for industrial investment while weakening parts of the framework meant to drive it”, says Escrig.

Andrea Spignoli, the policy manager of sustainable markets at Bellona Europa, says the proposal risks “weakening green investments” and putting a larger decarbonisation burden onto other sectors that are not covered by the ETS.

Greg Van Elsen, a senior industrial policy coordinator at CAN Europe, says in a statement:

“Free pollution permits were never meant to become a permanent subsidy. Extending them until 2038 rewards delay instead of industrial decarbonisation.”

Lobby groups also had mixed reactions to different aspects of the proposal.

The International Air Transport Association says it is “deeply frustrated” with the proposal.

The organisation’s director general, Willie Walsh, claims the consequences will be “harmful”, “sowing acrimony over extraterritoriality, slowing global decarbonisation and sapping European competitiveness”.

WindEurope says the proposal risks “slowing decarbonisation and failing to channel billions in ETS revenues to industrial electrification”.

BusinessEurope’s director general, Markus J Beyrer, says some aspects “raise concerns”. For example, he says the “new conditionalities for free allocations risk increasing bureaucratic complexity and the uncertain role for international carbon credits”.

What is ‘ETS2’?

ETS2 is a separate emissions trading system to the main ETS. It is due to take effect in 2028 and is not affected by the current ETS review or resultant proposals.

It will operate under a similar system as the existing ETS, covering emissions from transport, buildings and smaller industries in other sectors.

One key difference, however, is that ETS2 will not provide any allowances for free. They will all be auctioned and bought by companies.

On 15 July, 10 countries, including Italy and Poland, had urged the commission to also reconsider the ETS2 during this review. They were unsuccessful.

Similar to the original ETS, the commission believes the carbon price under the new ETS2 system will “provide a market incentive for investments in building renovations and low-emissions mobility”.

However, in June, member-state governments and the European parliament agreed on a number of “safeguards” to support price stability.

For example, if allowance costs under the ETS2 exceed €45 per tonne of CO2, they agreed that 40m allowances will be put into the system from a reserve to normalise the supply – double the amount previously agreed.

A European Environment Agency briefing said the ETS2 will “affect fuel prices and mobility costs” and that money will be syphoned into a social climate fund to “support vulnerable households and investments”.

What happens next?

EU countries will now negotiate over the terms of the commission’s proposal before it goes to a vote in the European parliament.

Ireland, which recently took over the six-monthly rotating presidency of the Council of the EU, has stated that it wants the ETS proposals to be signed off by the end of this year.

A previous document from the council, which represents member-state governments, outlined a target to agree a deal by the first quarter of 2027.

Clean Energy Wire says that this would be an “unusually ambitious timetable for one of the bloc’s most technically complex pieces of climate legislation”.

Politico notes that “months of arguing” is likely to occur.

The post Q&A: What the EU’s carbon market review means for climate action appeared first on Carbon Brief.

Q&A: What the EU’s carbon market review means for climate action

-

Climate Change11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测