The UK’s new Labour government must urgently reinstate the net-zero plans shelved by its predecessor in order to “limit the damage” caused by Conservative policy rollbacks, according to official advisors at the Climate Change Committee (CCC).

In its latest annual progress report, the CCC issues some frank words about the “confusing and inconsistent” behaviour of the previous government.

The Conservatives only brought in “credible” policies to cover one-third of the emissions cuts required to hit the UK’s 2030 climate target, the committee finds.

Despite being “insufficient”, the CCC notes that this is a slight improvement on last year. Since then, a requirement for carmakers to sell electric models and a deal to help decarbonise heavy industry both boosted the credibility of the UK’s climate strategy, it says.

Nevertheless, the committee criticises former prime minister Rishi Sunak’s decision to roll back key net-zero policies, notably delaying bans on the sale of new gas boilers and non-electric cars. It says that, contrary to his claims, there was “no evidence” the delays would save people money.

The committee points to a general need to scale up emissions cuts across the economy. It says almost none of the UK government efforts to scale up low-carbon technologies or invest in nature-based solutions are on track.

With this in mind, the progress report lays out a selection of “priority” actions that the new Labour government should take to “make up lost ground” so the UK can achieve its climate goals.

- New government

- Policy gap

- Road transport

- Buildings

- Industry

- Fossil fuels and hydrogen

- Electricity

- Agriculture and land use

- Aviation and shipping

- CO2 removal

- Waste and F-gases

- Adaptation

New government

A lot has changed in UK climate politics since the CCC’s last annual progress report was published in June 2023.

Earlier this month, Labour won a landslide election victory ending 14 years of Conservative rule. The party triumphed with a manifesto full of climate-related policies, including a pledge to decarbonise the nation’s electricity supplies by 2030.

Under the Conservatives, the CCC had issued a series of progress reports in which it warned, again and again, that the UK was not on track to meet its future climate goals.

Rather than heeding these warnings, the government led by Sunak announced a rollback of net-zero policies last September, citing “unacceptable costs” for British people. This included delaying the phaseout of both gas boilers and petrol and diesel cars.

The CCC’s latest report acknowledges some positive progress made under Sunak’s leadership. However, it is also quite critical of the outgoing Conservative government, which it says “undermined” the government’s own climate efforts with “confusing and inconsistent messaging and actions”. The report states:

“[The previous government] claimed to be acting in the long-term interests of the country, but there was no evidence backing the claim that dialling back ambition would reduce costs to citizens.”

The new report was prepared before the election, but it says the new government must “act fast to hit the country’s commitments”. It highlights the reinstatement of the weakened net-zero policies as a priority, noting that “damage can be limited”, if the government does so “quickly”.

Interim CCC chair Prof Piers Forster told journalists in a briefing that the new Labour government, which has hired former CCC chief executive Chris Stark to lead its clean power by 2030 “Mission Control”, has already made some progress. He said:

“They’ve done some quite good things in their first 10 days…They have concentrated their announcements on decarbonising energy.”

However, to achieve the UK’s broader climate goals, he added that the new government would “have to go much wider than energy”, with efforts to cut emissions “right across the economy”.

In the coming months, the Labour government must produce a new net-zero strategy, following a second successful legal challenge, which concluded that the existing UK plan was not credible.

It is also obliged to produce a new international climate pledge (nationally determined contribution, NDC) under the Paris Agreement, laying out the UK’s ambition for cutting emissions out to 2035.

The government will also have to legislate in 2025 for the seventh carbon budget, covering 2038-2042, following advice from the CCC due early next year. The CCC describes the seventh carbon budget period as a “stepping stone” on the path to net-zero by 2050.

(See Carbon Brief’s “Interactive: Labour government’s in-tray for climate change, energy and nature”.)

Policy gap

UK greenhouse gas emissions have been falling steadily for years, largely driven by the phaseout of coal and the growth of renewable power. Last year was no exception, the CCC says – confirming Carbon Brief analysis published in March.

The nation’s emissions dropped by 5.4% from 415m tonnes of carbon dioxide equivalent (MtCO2e) in 2022 to 393MtCO2e in 2023, excluding emissions from international aviation and shipping.

This marked an increase in the rate of emissions cuts, resulting predominantly from a fall in gas demand that “may in part reflect continuing high gas prices”, as well as a return to normal levels of imports of clean electricity from overseas.

The UK also comfortably achieved its third carbon budget, which ran for the period 2018 to 2022, the CCC confirms. It notes that, rather than due to deliberate climate policy, this can partly be attributed to the UK’s “lower-than-expected GDP”, which, in turn, is linked to the economic impact of Brexit and the Covid-19 pandemic.

However, for years the CCC has been warning of a looming gap between the government’s net-zero policies and its future emissions targets.

Only one third of the emissions reductions required to achieve the UK’s 2030 NDC goal under the Paris Agreement of cutting emissions 68% by 2030 are covered by plans the CCC deems “credible”.

There is an even larger credibility gap on the sixth carbon budget for 2033-2037, with only a quarter of the cuts needed covered by “credible” policies.

The chart below shows the distance between these credible policies (dark blue) and the “delivery pathway” that the government has set out for achieving its net-zero target (red).

Policies with “some” (light blue) or “significant” risk (purple) close part of the gap to getting on track, but around one fifth of the emissions cuts needed are either covered by plans that are “completely insufficient” or have no plans in place at all.

The CCC notes a “slight improvement” in credible policies, which only covered a quarter of the 2030 emissions cuts last year. This is due primarily to the introduction of the zero-emission vehicle mandate and a deal for the electrification of heavy industry.

This is illustrated in the figure below, which shows the change in expected emissions in 2030 based only on “credible” policies. The dots on the left show what the CCC expected in its 2023 progress report, while those on the right show its latest estimates.

While the committee now expects emissions from road transport and industry to be slightly lower, the outlook for some sectors – notably buildings – has worsened following the Conservatives’ rollback of net-zero policies.

One of the ways in which the committee monitors government progress towards net-zero is with 28 “key indicators”. Of the 22 that have a fixed benchmark or target, only five are currently on track, including a reduction in distances driven by cars and a drop in battery prices.

None of the CCC’s 12 indicators for the uptake of low-carbon technologies and nature-based solutions are classed as “on track”, except for the expansion of public electric vehicle charging stations.

The CCC also set out 27 specific “priority recommendations” in last year’s progress report for the previous government to implement.

It says only two of these recommendations have seen “good progress” over the past year and 12 have seen no progress at all. Nine of the priorities where no progress was seen were the responsibility of the Department for Energy Security and Net Zero (DESNZ), which oversees most of the policies in question.

Progress was also “too slow” in the devolved administrations of Scotland, Wales and Northern Ireland, the CCC notes, with limited headway on their priority recommendations.

While there are “almost” enough credible policies in place to achieve the upcoming fourth carbon budget, between 2023 and 2027, the CCC warns that this should not lead to complacency.

Both the fourth and fifth budgets are relatively unambitious because they were set before the UK had a net-zero target, when the goal was an 80% cut in emissions by 2050. Both must be overachieved in order to remain on a “sensible path” to net-zero, it says.

The emissions drop in 2023 of 22.3MtCO2e was much higher than the average annual emissions cut seen in the seven years prior to this, which was 13.8 MtCO2e each year. The CCC notes that “a similar pace of reduction will need to be maintained throughout the rest of the decade” in order to meet future climate targets.

However, while emissions cuts to date have been dominated by the electricity system, other sectors will need to start contributing in the coming years.

As the chart below shows, three quarters of the emissions cuts over the next three carbon budgets are expected to come from transport, buildings and other sectors.

The CCC sets out various “priority actions” across the report in order to “make up lost ground” and get the UK back on track for its climate targets.

These include sector-specific targets, described in the sections below. They also include broader goals, such as making planning policy consistent with net-zero, publishing a just transition plan for workers and improving public engagement on low-carbon choices.

Road transport

Despite an increase in the miles driven on UK roads last year, emissions from cars and other road transport fell by 0.9%, according to the progress report.

The CCC says this marks the “first time that the uptake of electric vehicles has had a meaningful impact on the direction of emissions trends”. At least one million UK cars – 2.8% of the total fleet – are now electric.

In addition, the CCC notes that the number of miles being driven in cars remains roughly 6% below pre-Covid levels, indicating a persistent shift in travel patterns following the pandemic. (This is not the case for vans, which are being driven 11% more miles than before.)

Yet transport remains the largest source of emissions in the UK economy. The CCC stresses that emissions from cars, vans and trucks will have to drop four times faster than the 2023 rate each year this decade, in order to meet the country’s climate targets.

The report recommends various policies to achieve this. It welcomes the zero-emission vehicle mandate – which sets targets for car manufacturers to sell a certain share of electric models – as one of the few recent successes of the previous government.

However, it says that electric cars’ market share did not grow in 2023, after years of having exceeded the CCC’s expectations. It also notes that electric van sales have been stalling.

With this in mind, the CCC’s “priorities” for the Labour government includes a reinstatement of the 2030 phaseout date for petrol and diesel cars, after Sunak’s government delayed this to 2035. (Labour pledged to do so in its election manifesto.)

It also says ministers should remove planning barriers for electric vehicle chargers and develop new policies to promote electric van uptake.

The report welcomes the rapid drop in electric-vehicle battery prices, which have fallen far ahead of the CCC’s expectations, as the chart below shows. Their continued decline will play a “key role” in making these vehicles “more cost-effective”, it says.

Finally, the CCC recommends that the UK and devolved governments should publish various plans to guide local authorities in setting out local transport strategies, promote charging infrastructure and reduce the use of cars.

Buildings

In 2023, emissions from buildings fell by 7.2% due to reduced demand for gas. This continued a trend seen in 2022, which was driven in part by mild winter months and high fuel prices leading to behavioural change, such as people using their heating less.

However between 2015 and 2022, the average reduction in emissions in the buildings sector was below the pace needed for the rest of the decade to reach 2030 targets, the CCC says.

The reductions over the last two years were also not driven by sustained programmes to scale up low-carbon technologies, such as heat pumps, which the CCC says will be needed for “deeper decarbonisation of the economy”.

As such, progress must now be sped up, enabled by programmes of support to roll-out key technologies over the next seven years, the CCC says.

In 2023, the number of heat pumps installed only increased by 4% compared to the previous year, up from 58,000 to 60,000.

This indicator is “significantly off track” from the rate the CCC says is required. Installation rates in residential buildings will need to increase tenfold from 2023 levels by 2028 to meet the government’s 600,000 a year target.

However, the committee says there have been some “promising signs” in the first few months of 2024.

Applications under the Boiler Upgrade Scheme – which provides financial support for switching from a gas boiler to a heat pump – rose 62% in the first four months of the year compared to the same period in 2023. This follows a decision by the Conservative government to increase the grants available under the scheme from £5,000 to £7,500.

Meanwhile, measures to improve the energy efficiency of buildings are “moving in the wrong direction”. Rates of home insulation fell in 2023, having already been “significantly off track” in 2022, the CCC states.

Overall, the CCC’s assessment of policies to decarbonise buildings for the 2030 NDC has worsened over the last year. It points to the Conservative government’s decision to delay the phaseout of fossil-fuelled boilers, abandon plans to enforce energy efficiency improvements in rental properties and push back the introduction of the “clean heat market mechanism”.

The committee recommends reversing recent policy rollbacks as a priority. It also says the government should introduce a comprehensive programme to decarbonise public sector buildings, remove planning barriers for heat pumps and make electricity cheaper to support the electrification of home heating. (See: Electricity.)

Broadly, one of the priorities set out by the CCC is rolling out heat pumps faster, supported by strong and credible signals that policies such as the Boiler Upgrade Scheme will continue to be fully funded.

Additionally, the committee says the government should “narrow the scope” of the strategic decision on hydrogen for heat, ahead of its current deadline in 2026. The government has been set to make a decision on what the role of hydrogen will be within the heating system in Britain, however, multiple pilot schemes have now closed bringing the role of the technology into question. Ahead of this decision, the CCC suggests “prohibiting connections to the gas grid for new buildings from 2025”.

Industry

Emissions from industry fell by 8.1% in 2023. These reductions were largely the result of site closures in the chemicals sector, with high gas prices potentially a contributing factor, the CCC says. There was also a reduction in emissions in the iron and steel sector.

As with buildings, the sector’s annual emissions reductions over the previous seven years were not at a sufficient pace to achieve the UK’s 2030 climate target, the report says.

Moreover, last year’s fall was not the result of sustained decarbonisation action. The CCC says emissions cuts will need to speed up, supported not by factory closures but by the rollout of low-carbon technologies.

Between 2008 and 2022, direct industrial and fuel supply emissions fell from 140.8MtCO2e to 87.1MtCO2e, as shown in the chart below. This was “considerably faster” than the CCC expected in its 2008 advice.

This was mostly due to a fall in emissions-intensive industries’ outputs, in particular for steel and chemicals. The overall demand for steel saw a “big drop” from 2008 to 2009, and the sector has shrunk due to a lack of competitiveness internationally.

Additionally the EU emissions trading scheme (ETS) contributed significantly to abatement by encouraging further emissions reductions, the CCC notes.

The share of industrial energy use that comes from electricity has stayed relatively consistent, at 26%, since 2020. However, the CCC expects this to increase, as various industries electrify their processes to reduce emissions. As an indicator therefore, industrial electrification is off track, the report adds.

Risks to the decarbonisation of industry include British Steel’s plan to replace its blast furnace in Scunthorpe with two electric arc furnaces (EAF), which is dependent on as-yet unapproved government support.

The CCC notes that the previous government’s £500m deal with Tata Steel to shift production at its Port Talbot site to EAFs has lowered the risk of industry missing its decarbonisation targets.

However, this transition will mean up to 2,800 job losses. The CCC notes that it has “long been clear that the site would need to adapt to remain competitive, for economic reasons largely unrelated to decarbonisation, yet successive governments have failed to develop a long-term economic strategy to develop alternative high-quality employment in the area”.

It further advises that the government should be more proactive and ambitious when it comes to engaging with communities affected by the transition to net-zero. Not doing so risks long-term harm to communities, which could undermine support for net-zero.

The CCC says there has been progress with tightening the cap under the UK’s emissions trading system (UK ETS), which includes industry. However, it notes that the cap is still far looser than in the “central” trajectory in the government’s net-zero strategy. This means that other parts of the economy will need to cut emissions more quickly in order to keep the UK on track overall.

The new UK ETS cap is expected to lead to higher production costs, the CCC notes. While some industries will be protected if the government introduces a carbon border adjustment mechanism (CBAM) in 2027 as planned, this “could lead to offshoring in the absence of further supporting policy to develop alternative low-carbon options”, the report notes..

It says priorities for the new Labour government to tackle industry emissions therefore include strengthening the UK ETS to ensure that its price is sufficient to drive decarbonisation and implementing a CBAM effectively to protect against offshoring.

It also says the government should act to make electricity cheaper, develop policies to address barriers to industrial electrification and implement resource efficiency plans.

Fossil fuels and hydrogen

The CCC also weighs in on the question of whether the UK should continue to exploit its domestic fossil fuel resources, including those in the North Sea.

Specifically, it says that UK policy should be aligned with the COP28 deal on “transitioning away” from fossil fuels, as well as the guiding principle for international climate action of “common but differentiated responsibilities”. It says:

“As a developed country with a binding commitment to transition to net-zero, the UK should reassess whether further exploration for new sources of fossil fuels is aligned to the UNFCCC principle of common but differentiated responsibility and the global stocktake.”

The outgoing Conservative government had argued that domestic fossil fuels bolstered energy security, attempting to make this into a “wedge issue” with the now-ruling Labour Party, which ran on a pledge to end new licensing for North Sea oil and gas extraction.

To drive this point home, the Conservatives had introduced an offshore petroleum licensing bill that would have required the North Sea Transition Authority to run annual licensing rounds for new exploration. (The Conservatives failed to pass the bill before the election.)

In contrast, the CCC report notes that one of the key reasons why UK energy bills have remained so high during and after the global energy crisis is due to the country’s dependence on fossil fuels. This dependence will be reduced in the shift to net-zero, it notes.

The shift to domestic renewables will also bolster energy security, the CCC says:

“British-based renewable energy is the cheapest and fastest way to reduce vulnerability to volatile global fossil fuel markets. The faster we get off fossil fuels, the more secure we become.”

One “welcome” point of progress has been that in February 2024, the UK formally withdrew from the controversial Energy Charter Treaty, which provides protection to companies investing in fossil fuel developments, the CCC notes.

Beyond fossil fuels, the UK government has continued to target a strategic role for hydrogen. It published a hydrogen production delivery roadmap, a transport and storage networks pathway, and a business model for the first hydrogen allocation round in December 2023.

As a priority, the government should also publish a “strategic spatial energy plan” and identify low-regret infrastructure investments, including for hydrogen infrastructure that can proceed now, the committee says.

Electricity

Emissions from the electricity system fell by 22.2% in 2023. This large drop reflects falling gas generation as part of the longer-term rise of renewables, combined with a return to the UK’s normal status as a net electricity importer.

Electricity generation is the only sector to have sustained emissions cuts in line with the 2030 target over multiple years, the CCC notes.

With electrification of the economy a key enabler for wider emissions cuts, one of the CCC’s priority actions for the remainder of 2024 is for the government to make electricity cheaper, by removing policy costs from electricity bills.

This would support industrial electrification, the uptake of electric cars and ensure lower running costs of heat pumps compared to fossil fuel boilers, it says.

Electricity decarbonisation to date has been aided by massive cost reductions for technologies including wind and solar power, the CCC says. It adds that lower costs lay the groundwork for continued rapid uptake of low-carbon technologies.

Indeed, it says that renewable energy will need to be built even faster than it has been to date. Annual installation of offshore wind will need to more than treble, onshore wind more than double and solar increase five-fold between 2023 and 2035.

For example, the UK had 15 gigawatts (GW) of offshore wind at the end of 2023 and will need to add more than 5GW every year to reach 50GW by 2030. This is more than three times the rate added over the past three years.

The technology hit a stalling point in 2023, when no offshore wind was contracted in the contracts for difference (CfD) scheme due to failure to respond to supply chain cost increases.

The CCC says it has “some confidence” that contracts coming through under the CfD scheme will lead to capacity increases, “but these are not enough and significant additional capacity beyond this will be required”.

The CCC “welcomes” updates to the next CfD auction, including the 66% increase in the maximum price for offshore wind and an increase in the notional “budget” that includes £800m for the technology

Onshore wind capacity in 2023 was 15GW, however only 0.5GW of new capacity was installed last year. This was considerably below the peak of 1.8GW in 2017.

Total solar capacity was 16GW in 2023. For the UK to achieve the previous government’s ambition of hitting 70GW of capacity by 2035, more than 4GW would need to be installed each year, the CCC notes – more than five times the average amount added over the past three years.

Within its first week, the new Labour government has moved to make the development of renewables easier, including removing the de facto ban on onshore wind in England and approving three major solar farms.

Other key areas of development have been “positive steps” made by the previous government around whole-system strategic planning of the future energy system, the report says.

The CCC calls for rapid decisions to be made following the second consultation on the “review of electricity market arrangements”, which was published in March,.

The government should publish a strategy for the full decarbonisation of electricity by 2035 at the latest, the CCC recommends. (The report was prepared prior to the election. The new Labour government is targeting clean power by 2030.)

This strategy should cover the strategic and policy requirements, milestones and timeline for delivery, as well as contingencies addressing key risks, the CCC suggests.

Additionally, the government should ensure electricity network capacity is growing to meet requirements. This should include fully implementing the “connections action plan” and “transmission acceleration action plan” at pace.

Agriculture and land use

Agriculture and land use are the source of some major gaps in the previous government’s net-zero plans, the CCC states.

Emissions from agriculture have remained virtually unchanged for nearly two decades. Planting trees and restoring peatland could absorb some of the emissions from high-emitting sectors, but efforts to expand these activities have faltered.

The UK has committed to cut its methane emissions 30% from 2020 levels by 2030. In order to do this, the pace of reductions compared to recent years would need to double over this decade.

Cattle and sheep produce around half of the UK’s methane emissions. Given the slow rate of change over recent years, the rate of methane cuts from agriculture would need to increase roughly eightfold in order to meet the UK’s methane target by 2030.

The CCC notes that livestock numbers fell between 2017 and 2020, but since then the trend has remained flat. It notes that there has been a small amount of progress in the promotion of methane-suppressing feed products for livestock.

The committee also points out that the Welsh government has paused its plans to reduce emissions from farming “following substantial resistance”. It warns that any delay to its sustainable farming scheme “could have significant impacts”.

The report says both the UK government and devolved governments should prioritise funding and support to ensure the UK-wide tree planting target of 30,000 hectares per year by the 2024-25 period is met.

It also says there should be a “delivery mechanism” for peatland restoration, which is supposed to reach 32,000 hectares per year by 2026, but is not on track to do so. (The CCC notes that even this target is “significantly less ambitious” than its own recommendation.)

The final priority highlighted for the sector by the CCC is the publication of the long-awaited land-use framework. This plan has been repeatedly delayed, and could help to align the sector with other issues such as using land to build energy infrastructure or adapt to climate change.

Aviation and shipping

Aviation was the only sector that saw a substantial leap in emissions in 2023. They rose by 15.5% as demand “continued to rebound from the pandemic”, and the CCC says there is “a risk” that demand for flights may rise higher than pre-Covid levels next year.

The government’s pathway to net-zero allows for some growth in both aviation and shipping emissions out to 2030. (While domestic journeys are included, international aviation and shipping are not part of the 2030 NDC target. However, they will feature in the UK’s carbon budgets from the sixth period onwards.)

The CCC says more detail of policies for curbing aviation emissions was provided last year – specifically the sustainable aviation fuel (SAF) mandate. However, it says “delivery concerns” mean this sector continues to “attract some risks”.

It notes that the SAF targets the previous government set were “ambitious”, but cautions that the volume of SAFs available to meet this target is “highly uncertain”.

The CCC has frequently highlighted the need to manage demand for flights as well as implementing technological solutions to decarbonise travel. As recent Carbon Brief analysis demonstrates, any emissions cuts from the SAF mandate in the coming years will be entirely wiped out by the expected rise in demand for flights.

In the new report, the committee says a priority for the Labour government should be pausing any new airport expansions until there is a UK-wide “capacity management framework” in place.

This would assess aviation emissions and ensure there is no overall expansion “unless the carbon intensity of aviation is outperforming the government’s emissions reduction pathway”.

Shipping, which accounts for one of the smallest shares of annual emissions, is not highlighted as a priority area for the new government.

CO2 removal

The CCC says the previous Conservative government’s plans to develop technologies that remove CO2 from the atmosphere are “behind schedule”.

This makes the ambition to remove at least 5MtCO2 per year by 2030 – which is required to meet the UK’s NDC target under current plans – “increasingly challenging”, according to the committee.

Moreover, despite the publication of some business models for the sector, all of the government’s plans carry “significant risk”, the CCC warns. This is notable, as the removals sector is expected to contribute 11% of emissions cuts by the end of the sixth carbon budget in 2037.

The key priority the report highlights for the new Labour government is finalising business models for engineered CO2 removals and “opening these to the market to enable projects to get underway”.

A related piece of advice highlighted by the CCC is that the government should publish guidance for businesses on how to use carbon offsets. It says firms should only use them to claim “net-zero” once nearly all their emissions are cut, and “the remaining emissions are neutralised by high-quality permanent removals”.

Waste and F-gases

The CCC says there has been “very little progress” in cutting waste emissions. It highlights insufficient progress in capturing methane from landfills, recycling and composting.

Waste is largely a devolved issue and the CCC makes recommendations to the governments of Scotland, Wales and Northern Ireland accordingly.

The key priority that the report highlights for the new Labour government for this sector is the need to address rising emissions from waste-to-energy facilities, which have “substantially increased”. It calls for a “moratorium” on new plants until there is a government review of capacity needs and how these facilities align with climate plans.

Fluorinated gases (F-gases), which make up a tiny fraction of UK emission, are subject to steadily declining quotas for importers and producers of the devices that emit them. They are not targeted as a priority in the new report.

Adaptation

The previous Conservative government published its third National Adaptation Plan (NAP3) in 2023, covering the period out to 2028. This is the nation’s statutory plan to ensure the UK is prepared for a warmer world.

It has faced intense criticism from the CCC, and campaigners have taken the government to court, citing the plan’s failure to adequately protect people from climate change.

In its new report, the CCC says NAP3 “lacks the pace and ambition to address growing climate risks which we are already experiencing”. It says the plan needs “clear objectives and targets”, and this should include stronger links with the next spending review.

The report also says the government should reorganise so that adaptation “becomes a fundamental aspect and is embedded in other national policy objectives” across departments. This includes prioritising it in other national priorities, including nature restoration, infrastructure development, economic growth and health.

The post CCC: Labour must ‘make up lost ground’ to hit UK climate goals appeared first on Carbon Brief.

CCC: Labour must ‘make up lost ground’ to hit UK climate goals

SYDNEY, Monday 27 July 2026 — In response to an announcement that Woodside’s Browse to North West Shelf (Browse) Project was declared a State Significant Project by the WA Government, the following comments can be attributed to Senior Campaigner at Greenpeace Australia Pacific, Hannah Schuch:

“The WA Government must not ignore the significant risks clearly associated with Woodside’s plans to drill for gas at the pristine Scott Reef — to endangered marine life, our oceans, and our climate — all of which are valued and relied upon by Western Australians.

“The WA Environmental Protection Authority has already found Woodside’s plans to drill at Scott Reef would have unacceptable impacts on the environment without considering the climate impacts of 1.6 billion tonnes of carbon pollution associated with this disastrous proposal.

“Woodside’s gas drilling plans, including seismic blasting and carbon dumping in the heart of a precious ecosystem, pose potentially fatal risks to pygmy blue whales and genetically unique green sea turtles, and could cause a catastrophic oil spill.

“If the WA and federal governments are concerned with the prosperity of WA, they must reject Woodside’s nature and climate-wrecking proposal to drill for gas at Scott Reef.”

—ENDS—

High res images and footage of Scott Reef can be found here.

For more information or to arrange an interview, please contact Emma Sangalli on 0431 513 465 or emma.sangalli@greenpeace.org

Cook Government must recognise risks posed by Woodside’s Scott Reef drilling plans

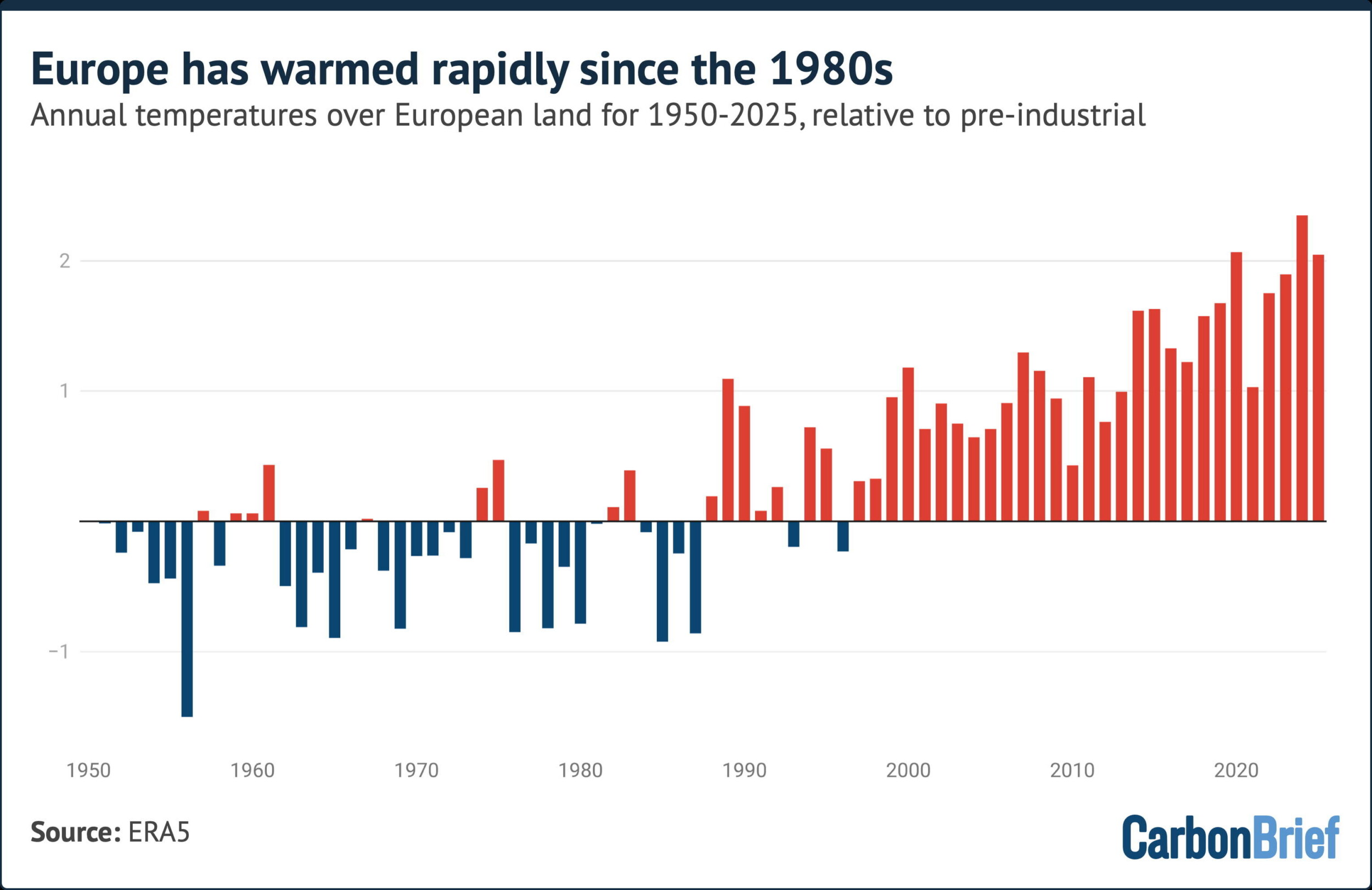

This summer has seen Europe suffer through a series of record-breaking heatwaves.

Amid widespread media coverage of the number of deaths and the influence of climate change, the UK’s Daily Telegraph reported on new research with the incorrect headline: “Heatwaves caused by fall in pollution.”

The article was shared on social media by Richard Tice – deputy leader of the hard-right, climate-sceptic Reform UK party – along with a number of prominent rightwing commentators.

Tice claimed that “net stupid zero is contributing to rising temperatures, not helping”, adding that “we have been gaslit and lied to”.

GB News followed up with its own article, incorrectly headlined: “Britain’s scorching heatwaves caused by falling pollution levels, researchers find.”

Scientists tell Carbon Brief that the framing of heatwaves being “caused” by declining air pollution is “wrong”.

While a drop in pollution has reduced the cooling impact it has had in the past, the scientists say, Europe’s summer heatwaves are primarily becoming more extreme “as a result of greenhouse-gas-induced warming”.

Another scientist adds that “any attempt” to link this research to net-zero policies is “simply wrong”.

Fast warming

The extensive reporting around Europe’s heatwaves in recent months has often mentioned that Europe is the world’s fastest-warming continent.

The new study in question aims to unpack why Europe’s summer temperatures are rising more quickly than other regions of the northern hemisphere’s mid and high latitudes.

The research – published in Geophysical Research Letters – explores the role of air pollution and, specifically, how it affects circulation patterns in the atmosphere.

(The study focuses on long-term trends in European summers and does not include the very recent heatwaves.)

Human-caused emissions of aerosols – tiny, light‑scattering particles produced mainly by burning fossil fuels – have long acted to “mask” global warming. This is largely because they absorb or reflect incoming sunlight and influence the formation and brightness of clouds.

To understand how the climate of Europe – or any region – is changing, scientists need to take into account a whole range of factors, says Prof Bjørn Samset, a research professor at Norway’s Center for International Climate Research (CICERO), who was not involved in the work.

This includes “greenhouse gases, aerosols, land-use change, natural variability and how they all interact”, he says, adding:

“The effects of air pollution on circulation, which is the topic here, has long been difficult to pin down.”

As European countries improved their air quality through the second half of the 20th century, the cooling effect of aerosols has gradually been removed.

This can boost heatwaves in two ways – directly, by letting more sunlight reach the land surface and, indirectly, by influencing the jet stream.

Using hundreds of simulations from nine climate models, the new study finds that a decline in aerosols is resulting in more frequent “quasi-stationary Rossby waves”.

Rossby waves are huge meanders in the jet stream. Occasionally, they become slow-moving – or “quasi-stationary” – which allows weather systems to get stuck over one region, leading to prolonged heatwaves.

These circulation changes have contributed to Europe’s rapidly warming summers.

However, while Europe’s heatwaves are being influenced by declining aerosols, it is “wrong” to say they are being “caused” by them, says Prof Erich Fischer, a climate scientist at ETH Zurich.

Fischer, who was not involved in the study, tells Carbon Brief:

“Heatwaves are caused by high-pressure systems and are now much more frequent and intense because they are happening in a climate that is much warmer than 100 years ago as a result of greenhouse-gas-induced warming.

“The paper shows that the greenhouse-gas-induced summer warming had been temporarily masked by air-polluting aerosols. The full extent for European summers only becomes visible now as the air-polluting aerosols have declined.”

Samset adds:

“Air pollution never causes or removes global warming, it only temporarily moderates it.”

Study lead author Dr Pedro Roldán‐Gómez, an associate researcher at the Barcelona Supercomputer Centre, is quoted in the Daily Telegraph saying that “most” of the “excess warming” in Europe, beyond that of comparable regions in the northern hemisphere, can be linked to declining aerosols.

But, earlier in the article, the newspaper interprets this as, simply, “most of the extra heat experienced in Britain and Europe” is down to air pollution.

GB News uses a similar phrasing, reporting that “much of the additional warming across Britain and western Europe since the 1980s is linked to the sharp decline in airborne particles known as aerosols”.

This is “misleading”, says Fischer, while Roldan-Gomez tells Carbon Brief that this is a “tricky point”, which “could lead to wrong interpretations if not properly explained”. He adds:

“The contribution of greenhouse gases is, in any case, the most important factor.”

Cleaner air

The Daily Telegraph’s article was seized upon by Reform’s Richard Tice to claim that “cleaner air” was causing higher temperatures, rather than CO2.

This continued his position – refuted by long-established climate science – that CO2 does not drive global warming.

Tice also claimed in his post that net-zero policies are “contributing to rising temperatures”. Tice appears to be linking declining air pollution to a shift from fossil fuels to renewable energy.

Samset points out that net-zero became a goal “decades later” than the cumulative efforts to reduce air pollution since the 1980s and that it is “simply wrong” to link it to the study.

“The scientific community will keep working to understand how greenhouse gas warming and air pollution interact,” he says, but “nothing we do will change the fact that the consequences of global warming are due to human-induced CO2 emissions”.

Fischer adds:

“Let us not forget that cleaning up air-polluting aerosols is highly desirable. According to the World Health Organisation, 7 million people still die prematurely every year due to air pollution.”

Clean air legislation

Finally, the Daily Telegraph article and the study itself both attribute Europe’s declining air pollution from the 1980s onwards to the Montreal Protocol.

This is a “glaring error”, Samset says, and it is “surprising that it wasn’t picked up” in the peer-review process for the study. He explains:

“The Montreal Protocol did not deal with air pollution. It dealt with ozone-depleting gases and has been an extremely successful multi-national effort against environmental damage. “

Clean air legislation was already in place in many European countries by the time the Montreal Protocol was signed in 1987, says Samset.

In response, Roldán‐Gómez says that while the protocol did not target aerosols specifically, it “boosted the clean air policies”.

The post Factcheck: No, Europe’s heatwaves are not being ‘caused’ by declining air pollution appeared first on Carbon Brief.

Factcheck: No, Europe’s heatwaves are not being ‘caused’ by declining air pollution

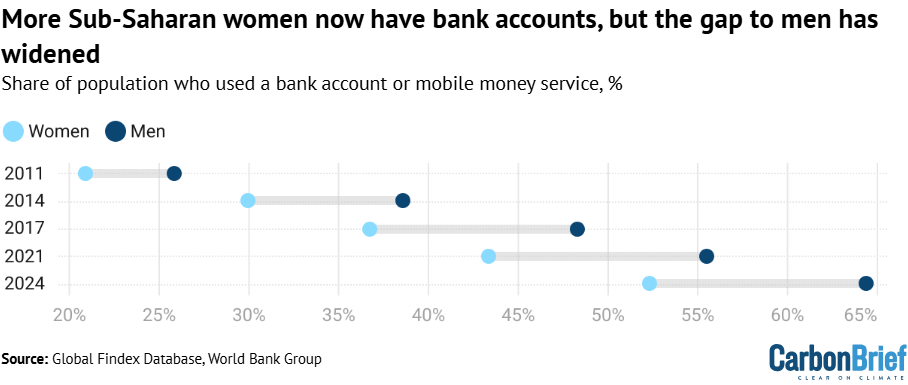

Empowering women through greater access to finance could “strengthen” households’ resilience to “climate shocks”, according to a new study.

Published in Climate Risk Management, it analyses the impact of financial access on “women-headed households” in sub-Saharan Africa.

The study finds that where women had formal financial access – such as through owning a bank account – households were more able to withstand short-term shocks.

It adds that “climate shocks”, such as extreme weather events and the impacts of climate change, can cause economic crises, which destabilise communities and households.

However, the authors say that in order to protect households from long-term climate vulnerabilities – including “droughts, floods and sea-level rise” – financial access would need to be paired with wider efforts to tackle gender inequality.

They add that the findings could have important implications for policy in sub-Saharan Africa, where many countries and households are vulnerable to climate disasters.

Financial inclusion

The study highlights that entrenched gender disparities mean many women still have unequal access to financial services in sub-Saharan Africa

For example, women are still less likely to have their own bank accounts and instead are often dependent on male relatives for access to finance.

The number of women with access to an account in the region had risen to 52% as of 2024, according to data from World Bank Group.

However, as shown in the chart below, the gap between men and women has also increased, rising from just under 5 percentage points in 2011 to 12 in 2024.

Using survey data from Afrobarometer, the new study analyses 25,511 women-headed households across 37 sub-Saharan countries.

The authors use the Organisation for Economic Co-operation and Development’s (OECD) framework to measure “financial inclusion”. This looks at factors such as having a bank account, owning a mobile phone and having internet access.

Francis Anaisie, a co-author on the study, tells Carbon Brief the researchers were motivated by the UN’s sustainable development goals (SDGs). Anaisie, an economist at the University of Cape Coast, Ghana, says the study specifically looked at SDGs five and 13, on gender equality and addressing climate issues. He adds:

“Financial inclusion is one of the key policy tools for empowering women or for empowerment. But as to whether this actually translates into better climate outcomes for women is not known or is limited; this study seeks to address that gap.”

The study finds households with higher levels of financial access for women had higher levels of women’s empowerment, when this is defined as the ability to make choices and have control over economic and social outcomes.

This was checked by cross-comparing financial access against different measures of women’s empowerment, such as financial security, voting rights and connection to communities.

In particular, the study found that “financially included” women had greater political and economic empowerment, such as financial security and voting rights. On some measures of social empowerment, however, the link was weaker – financial access alone was not enough to erase cultural and social barriers to gender equality.

Women and climate change

It has been well documented that women are more vulnerable to the impacts of climate change than men.

Environmental shocks affect women disproportionately due to a range of factors. These include income disparities, higher rates of displacement and unequal access to land.

Financial inequality and barriers to economic resources, such as needing internet access to make digital payments, play a key role in climate vulnerability, says Tracy Kajumba. She is director for the Least Developed Countries initiative for Effective Adaptation and Resilience (LIFE-AR) interim secretariat at the International Institute for Environment and Development (IIED).

Kajumba, who was not involved in the study, explains to Carbon Brief:

“Women are on the front line doing farming, planting, harvesting and these things that are all impacted [by climate change]. If they don’t have the income to invest either in drought-resistant crops or water-saving technologies, it becomes difficult for households to adapt.”

Calculating climate resilience

The new study measures the impact of financial inclusion on women’s empowerment and, in turn, on climate resilience.

It evaluates a household’s ability to withstand and recover from “shocks and stressors” by using a UN Food and Agriculture Organization metric for “resilience index measurement and analysis” (RIMA).

For example, questionnaires are used to gather information about households in certain areas. The data is then used, together with key indicators, to quantify a household’s resilience to food insecurity, climate variability and economic crisis, amongst other risks.

The 25,511 households surveyed across sub-Saharan Africa were found to be relatively resilient overall and had a high capacity to bounce back from climate shocks. However, they had much lower ability to adapt, in order to build protective capacity in advance of extreme events.

In addition, the study finds that women’s financial empowerment had a positive impact on a household’s ability to “absorb” a climate shock, suggesting that financial access is critical for responding to climate change.

Increased empowerment through financial access enables women to make decisions about planting crops, to access credit in emergencies and to buy or sell food at a better price, the study notes.

For example, it says increased financial access and women’s empowerment help households to deal with the immediate consequences of an extreme weather event, such as a drought. This could be through building community mutual-support networks and by enabling access to savings, to keep the household running.

Anaisie says the study shows women’s empowerment has a significant impact on climate resilience. He tells Carbon Brief:

“If we include women in the financial system, in the case of any climate issue they can save, they can be independent, they can rely on investment to absorb these shocks. This empowerment will help them to be more resilient to climate shocks…We can make progress because SDG goals are all about inclusiveness. It’s all about inclusive growth.”

However, the study notes that financial access does not necessarily create long-term change, which would make the household less vulnerable to extreme weather in the first place.

The authors suggest that lasting structural and cultural change is important for bringing about long-term resilience. They say that policies to address gender inequalities would help bring this about.

They say such policies could include gender-sensitive agricultural credit schemes, subsidised climate insurance for women farmers in drought-prone regions, joint land-titling programmes and quotas for women in local climate-adaptation committees.

Such policies would have helped women impacted by recent severe floods in Ghana to protect their savings, Anaisie explains. He tells Carbon Brief:

“Women are engaged in economic activities, especially informal activities. They have resources and money, but when the flood came in, many women lost that. If they had access to insurance, this flood wouldn’t have cost them that much.

“So, if the government comes out with financial initiatives, training, civic education and gender-focused initiatives, leadership training, women will be empowered and this will translate into their resilience with regards to climate change.”

Addressing climate vulnerability in sub-Saharan Africa

The study could have policy implications for sub-Saharan Africa, a region particularly vulnerable to the effects of climate change. The region faces increasingly extreme weather, heatwaves, droughts, wildfires and floods, as well as food scarcity and threats to crops.

The study suggests that policies to address structural and cultural barriers to women’s financial autonomy could be a key way to build climate resilience across the region.

However, it recognises that even where financial access is expanded, gender norms and cultural constraints continue to shape women’s social empowerment. This, in turn, affects their ability to adapt to climate change in the long term.

Ultimately, addressing structural inequalities is needed to minimise climate vulnerability, says Kajumba. She adds that supporting adaptation with financial access can allow households to absorb shocks without falling into poverty – and to rebuild after climate impacts.

Kajumba says that supporting adaptation with women’s financial access can allow households to absorb shocks without falling into poverty – and to rebuild after climate impacts. She adds:

“When they are supported [with] microloans, savings and all that, you will see change in income, change in households, change in health and education for the children as well.”

However, Kajumba notes that structural inequalities still “amplify” women’s vulnerability to climate impacts and make it harder for them to exercise agency and leadership. She adds:

“The tools that are being used are not always favourable for women…When we look at women in leadership and participation, you cannot lead or you cannot participate unless you have some level of income.”

The post Access to finance ‘strengthens climate resilience’ among sub-Saharan women appeared first on Carbon Brief.

Access to finance ‘strengthens climate resilience’ among sub-Saharan women

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测