A new analysis of jurisdictional REDD+ (JREDD+) in Brazil’s Amazon reveals a big chance. The potential credit sales could reach $10–$20 billion this decade. However, the market faces delays, integrity issues, and a drop in voluntary demand.

The report from the Earth Innovation Institute (EII) outlines the numbers and assumptions. It also offers a roadmap connecting carbon credit sales to real forest results and social safeguards.

The $20B Amazon Question: EII’s JREDD+ Forecast

The Amazon remains a vital carbon reservoir, holding approximately 56.8 billion metric tons of carbon above ground. Brazil alone contains over 32 billion metric tons of this total. This carbon stock equates to more than one and a half times global annual CO₂ emissions in 2023.

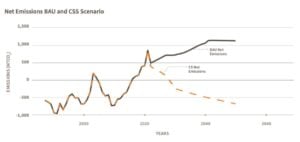

EII’s Amazon Forest Climate Solution (AFCS) expects Amazon emissions from deforestation, fire, and logging to drop by 90% by 2030 from a 2018–2022 baseline. Then, they aim for a 95% reduction by 2040 and a 98% cut by 2050.

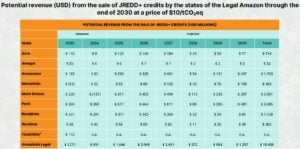

Brazil’s Amazon states could issue around 1.05 billion TREES standard credits. This would be for reductions achieved from 2023 to 2030. At $10–$20 per credit, that equals $10–$20 billion in potential revenue.

Timing matters. EII notes it typically takes two to three years to verify, issue, and sell credits. The four most advanced states—Acre, Mato Grosso, Pará, and Tocantins—might sell around 100 million credits in 2026. This could bring in about $1 billion at $10 per ton. That figure is roughly comparable to the $1.4 billion donated to the Amazon Fund since 2008.

A state-by-state table shows around 1,048.8 MtCO₂e in potential credits by 2030. This could bring in about $10.49 billion at $10 per ton. Pará leads with 348.5 Mt and $3.49 billion, followed by Mato Grosso with 200.1 Mt and $2.00 billion.

Why Billions Haven’t Flowed Yet

Analysts underscore the gap between early promises and actual transactions, while the EII report highlights these bottlenecks:

- No Brazilian state issued credits by June 2025.

- Only Pará and Tocantins signed forward Emissions Reduction Purchase Agreements (ERPAs).

- Acre and Mato Grosso are advancing through pay-for-performance (non-credit) mechanisms.

Meanwhile, the voluntary carbon market retrenched in 2023–2024. Global transactions fell to about 84 MtCO₂e from a 516 MtCO₂e peak in 2021, and forest/land-use project volumes slid from about 227 MtCO₂e to about 37 MtCO₂e. This slump undermines demand just as Brazilian states prepare to sell large volumes.

Put simply, the supply pipeline is maturing faster than demand. Integrity controversies around some project-level REDD+ credits have cooled buyers’ risk appetite.

EII argues that jurisdictional programs, using conservative baselines and including leakage deductions, can tackle many concerns. They also have social safeguards under the TREES standard. However, these programs still need clear policies and buyer confidence to turn modeled volumes into cash.

What Makes JREDD+ More Credible than Old REDD+?

EII emphasizes that JREDD+ credits reward performance at the state or national scale, not farm-by-farm activities. Also, participation is voluntary. The programs are created with Indigenous peoples, traditional communities, and farmers. They do not limit how landholders can use their land. Critically, project-level credits are subtracted from the jurisdictional pool to prevent double-counting.

Under TREES, crediting leaves out some removals, like those from fire-damaged forests. It also tightens baselines every five years. Moreover, there are significant deductions for leakage, uncertainty, and reversals. These choices underestimate climate benefits but aim to raise robustness.

These features are key to EII’s claim. They say JREDD+ can help finance quick emissions cuts now. Meanwhile, longer-term funds like the proposed “Tropical Forest Forever Fund” can grow.

Policy Shifts and Potential Buyers: From Petrobras to China

Converting potential into real revenue hinges on policy and demand signals:

- Domestic regulation:

Brazil’s federal government can explain how states can access Paris Agreement Article 6.2 transactions. This is for those who exceed the national NDC pathway. It could raise carbon prices and volumes for jurisdictional credits. - Corporate demand:

EII floats a COP 30 initiative where Petrobras convenes oil-and-gas peers to buy JREDD+ credits equal to about 1% of the sector’s Scope 3 emissions. This alone would multiply current forest and land-use demand on the voluntary carbon market tenfold. - Trade linkages:

A Brazil–China partnership on “forests, food, and climate” could link trade with local deforestation cuts. It might also direct credit purchases into state JREDD+ programs. Discussions are underway with Brazilian states.

EII believes these steps can shift the market from intent to action. They could also help bridge the multi-billion-dollar funding gaps in law enforcement, fire management, and regenerative land use.

What Success Would Mean for Climate — and the Amazon

The AFCS scenario suggests around 1.5 GtCO₂e in net reductions from 2025 to 2030. This is nearly double what the EU-27 is expected to achieve during that time. This relies on Brazil continuing to reduce deforestation and improving fire prevention and natural regeneration.

About 21% of the cleared land in the Amazon is marginal and turning back into forest. So, targeted incentives could boost natural regeneration at a lower cost than active restoration. This could also help stabilize regional rainfall.

EII connects climate benefits to public health and economic gains. This means fewer smoke-related illnesses and deaths. It also lowers risks for farm and forest investments. Plus, it creates new income streams for Indigenous peoples and smallholders. These include non-timber products, perennials, and aquaculture.

Still, EII’s main claim can be tested soon. If states set benefit-sharing rules, secure Article 6.2 eligibility, and finalize multi-buyer offtakes, then the first $1 billion in 2026 would prove that jurisdictional crediting works at scale.

Signals to Watch Before COP30

The report highlights COP30 in Belém, Brazil, as a pivotal moment for Amazon JREDD+. The country will host global climate negotiators in November 2025. This event will allow states to showcase their programs. They can also finalize pathways for Article 6.2 crediting.

EII believes COP30 can be used to reveal big corporate groups. This includes oil-and-gas or agribusiness buyers who commit to JREDD+ purchases. This event may determine whether modeled revenues of up to $20 billion move from projections to real contracts within the decade.

Some of the key market trends to watch are:

- State milestones: publication of final benefit-sharing frameworks and issuance of first TREES credits.

- Federal signals: Brazil’s alignment of Article 6.2 pathways for subnational programs.

- Buyer coalitions: oil-and-gas Scope 3 purchase commitments and commodity-trade linkages with China.

- Market breadth: whether jurisdictional credits revive voluntary carbon market volumes and pricing after the 2024 slump.

The EII report quantifies a plausible $10–$20 billion revenue pathway for Amazon JREDD+ this decade if governance, integrity, and buyer demand align. That level of financing could speed up Brazil’s forest-climate shift and provide social benefits. But this will only happen if policies and purchase commitments develop as quickly as expected.

The post Amazon’s $20B Carbon Credit Boom? Brazil’s REDD+ Faces Integrity and Demand Test appeared first on Carbon Credits.

Malawi has lost a striking share of its forests over the past three decades. Woodlands that once covered well over a third of the country now cover less than a quarter, and the pressure on what remains is increasing. Behind those figures sit two practical questions: what is driving the loss, and what reverses it?

![]()

Climate change is real, and the evidence is everywhere, from rising sea levels to extreme weather events. While changes in Earth’s climate have occurred naturally over millennia, human activities are now the dominant force behind the current warming trend. Understanding what climate change is, what causes it, and what we can do to stop it is essential for safeguarding our planet and future generations.

Key takeaways

- Human activities, especially burning fossil fuels, are now the dominant driver of climate change, not natural cycles like solar activity.

- Livestock accounts for an estimated 51% of annual global greenhouse gas emissions, while deforestation is the second-largest contributor.

- 2023-2025 was the first three-year period on record to average more than 1.5°C above pre-industrial temperatures.

- Global fossil fuel CO2 emissions hit a record 38.1 billion tonnes in 2025, with no sign yet of a peak.

- Nearly 30% of plant and animal species could be at risk of extinction if global temperatures keep rising.

- Solutions like renewable energy, energy efficiency, carbon offsets, and reduced deforestation can meaningfully slow climate change today.

Climate Change in 2026: The Latest Data

The data keeps confirming the same trend: warming is accelerating, not leveling off. Here’s where things stand as of 2026, based on the most recent findings from NOAA, Copernicus, NASA, and the Global Carbon Project.

2026 climate data snapshot

- Global temperatures: 2025 was the third-warmest year on record, behind 2024 and 2023. The past 11 years (2015–2025) are the 11 warmest ever measured, and 2023–2025 marked the first three-year period to average above 1.5°C over pre-industrial levels.

- CO2 levels: Atmospheric CO2 hit a record monthly high of 430.5 ppm at Mauna Loa in May 2025. Global fossil fuel emissions reached a record 38.1 billion tonnes in 2025, and researchers now say the remaining carbon budget to keep warming under 1.5°C will likely be exhausted before 2030 at current emission rates.

- Extreme weather costs: The U.S. recorded 23 separate billion-dollar weather disasters in 2025, the third-highest annual total on record, costing an estimated $115 billion. The January 2025 Los Angeles wildfires alone caused $61.2 billion in damage, making them the costliest wildfire event in U.S. history.

- Sea level rise: Global mean sea level rose just 0.08 cm in 2025, slowed temporarily by La Niña rainfall patterns, but the long-term rate of sea level rise has more than doubled since 1993, and oceans are up roughly 10 cm (about 4 inches) since satellite records began.

None of this changes the underlying picture: the causes, effects, and solutions below remain the same, they’re just playing out faster and at greater cost each year.

What Is Climate Change?

You’ve likely heard the terms “climate change” and “global warming” used interchangeably. However, they have distinct meanings. Global warming refers specifically to the increase in the planet’s average surface temperature, largely due to greenhouse gas emissions. Climate change, on the other hand, encompasses a broader range of long-term changes in temperature, precipitation, wind patterns, and other aspects of the Earth’s climate system.

Climate change has always been part of Earth’s history, driven by natural interactions between five key systems:

- Atmosphere (air)

- Biosphere (living things)

- Cryosphere (ice and permafrost)

- Hydrosphere (water bodies)

- Lithosphere (Earth’s crust and upper mantle)

Today, the rapid pace and scale of climate change are primarily driven by human activities.

Climate Change (infographic)

What Are the Causes of Climate Change?

Greenhouse Gases

Greenhouse gases (GHGs) trap heat in the Earth’s atmosphere. While some GHGs occur naturally, human activities have sharply increased their concentrations. Major contributors include:

- Carbon dioxide (CO2) – Released by burning fossil fuels, deforestation, and land-use changes.

- Methane (CH4) – Emitted from livestock, landfills, and oil and gas production.

- Nitrous oxide (N2O) – Produced by agricultural activities and fossil fuel combustion.

- Chlorofluorocarbons (CFCs) – Man-made chemicals used in refrigeration and aerosols.

CO2 is the most significant and long-lasting of these gases, making it the primary driver of global warming.

While some of these greenhouse gases, such as water vapor, are naturally occurring, others, such as CFCs, are synthetic. CO2 is released into the atmosphere from both natural and human-made causes and is one of the leading contributors to climate change. CO2 has been increasing at an alarming rate and has the potential to stay in the earth’s atmosphere for thousands of years unless it gets absorbed by the ocean, land, trees, and other sources. As CO2 production has steadily risen, though, the earth’s natural resources to absorb it have also been diminished. This is already occurring in many ways as the earth’s resources are disappearing from things like deforestation. Some studies even predict that plants and soil will be able to absorb less CO2 as the earth continues to warm, possibly accelerating climate change even further.

While some of these greenhouse gases, such as water vapor, are naturally occurring, others, such as CFCs, are synthetic. CO2 is released into the atmosphere from both natural and human-made causes and is one of the leading contributors to climate change. CO2 has been increasing at an alarming rate and has the potential to stay in the earth’s atmosphere for thousands of years unless it gets absorbed by the ocean, land, trees, and other sources. As CO2 production has steadily risen, though, the earth’s natural resources to absorb it have also been diminished. This is already occurring in many ways as the earth’s resources are disappearing from things like deforestation. Some studies even predict that plants and soil will be able to absorb less CO2 as the earth continues to warm, possibly accelerating climate change even further.

Solar Activity

Solar activity, as mentioned above, does play a role in the earth’s climate. While the sun does go through natural cycles, increasing and decreasing the amount of energy that it emits to the earth, it is unlikely that solar activity is a major contributor to global warming or climate change. Since scientists began to measure the sun’s energy hitting our atmosphere, there has not been a measurable upward trend.

Agriculture

There are many significant ways in which agriculture impacts climate change. From deforestation in places like the Amazon to the transportation and livestock that it takes to support agricultural efforts around the world, agriculture is responsible for a significant portion of the world’s greenhouse gas emissions. However, agriculture is also an area that is making tremendous strides to become more sustainable. As productivity increases, less carbon is being emitted to produce more food. Agriculture also has the potential to act as a carbon sink, and could eventually absorb nearly the same amount of CO2 it emits.

Deforestation

Deforestation and climate change often go hand in hand. Not only does climate change increase deforestation by way of wildfires and other extreme weather, but deforestation is also a major contributor to global warming. According to the Earth Day Network, deforestation is the second leading contributor to global greenhouse gasses. Many people and organizations fighting against climate change point to reducing deforestation as one of, if not the most, important issues that must be addressed to slow or prevent climate change.

Human Activity

According to the Environmental Protection Agency, the most significant contributor to climate change in the United States is the burning of fossil fuels for electricity, heat, and transportation. Of these factors, transportation in the form of cars, trucks, ships, trains, and planes emits the largest percentage of CO2, speeding up global warming and remaining a significant cause of climate change.

Livestock

While interconnected to many of the agricultural and deforestation issues we have already touched on, livestock in the form of cattle, sheep, pigs, and poultry play a significant role in climate change. According to one study, “Livestock and Climate Change,” livestock around the world is responsible for 51% of annual global greenhouse gas emissions.

What Are the Immediate Effects of Climate Change?

From melting glaciers to more extreme weather patterns, people everywhere are beginning to take notice of the real impacts of climate change. While some nations around the world are taking action with initiatives such as the Paris Climate Agreement, others are continuing business as usual, pumping millions of tons of carbon into the atmosphere year after year. As the 2026 data above shows, climate change continues to cause extreme weather as well as safety and economic challenges on a global scale, and the costs are climbing every year.

Extreme Weather

Changes to weather are perhaps the most noticeable effect of climate change for the average person, largely because of the financial impact severe weather events can have. In 2025 alone, the U.S. recorded 23 separate billion-dollar weather disasters totaling $115 billion in damages, continuing a run of the three highest years on record (2023, 2024, and 2025). Extreme weather influenced by climate change includes:

- Stronger storms & hurricanes

- Heatwaves

- Wildfires

- More flooding

- Heavier droughts

Safety & Economic Challenges

In 2014 the U.S. Department of Defense released a report that stated climate change posed a severe and immediate threat to national security. According to former Secretary of Defense, Chuck Hagel, rising global temperatures, shifting precipitation patterns, climbing sea levels, and more extreme weather events intensify the challenges of global instability, hunger, poverty, and conflict.

Climate change is also likely to cause continued economic challenges in many parts of the world. Some estimates have the U.S. already spending around $240 billion annually due to human-caused climate change, and the 2025 U.S. billion-dollar disaster total of $115 billion shows those costs remain elevated year after year. Putting an exact number on the real costs of climate change is difficult, though, once you consider the staggering costs of losing natural resources like clean air and water.

What Is the Long-Term Impact of Climate Change?

The long-term impact of climate change could be absolutely devastating to the planet and everyone and everything living on it. If the world continues on its current trajectory, and 2025’s record fossil fuel emissions suggest it is, then we will likely continue to see increasing effects on everyday life.

Health

There are many ways in which climate change could impact people’s health. Depending on age, location, and economic status, climate change is already affecting the health of many and has the potential to impact millions more. According to the Center for Disease Control and Prevention, climate change-related health risks may include:

- Heat-related illness

- Injuries and fatalities from severe weather

- Asthma & cardiovascular disease from air pollution

- Respiratory problems from increased allergens

- Diseases from poor water quality

- Water & food supply insecurities

Negative Impact on Ecosystems

Ecosystems are interconnected webs of living organisms that help support all kinds of plant and biological life. Climate change is already changing seasonal weather patterns and disrupting food distribution for plants and animals throughout the world, potentially causing mass extinction events. Some studies estimate that nearly 30% of plant and animal species are at risk of extinction if global temperatures continue to rise.

Water & Food Resources

Climate change could have a significant impact on food and water supplies. Severe weather and increased temperatures will continue to limit crop productivity and increase the demand for water. With food demand expected to increase by nearly 70% by 2050, the problem will likely only get worse.

Sea Levels Rising

Rising sea levels could have far-reaching effects on coastal cities and habitats. Increasing ocean temperatures and melting ice sheets have steadily contributed to the rise of sea levels on a global scale. Global sea level has risen roughly 10 cm (about 4 inches) since satellite records began in 1993, and the National Oceanic and Atmospheric Administration estimates sea levels will rise by at least 8 inches by 2100, potentially causing increased flooding and a decrease in ocean and wetland habitats.

Shrinking Ice Sheets

While contributing to rising sea levels, shrinking ice sheets present their own set of unique problems, including increased global temperatures and greenhouse gas emissions. Climate change has driven summer melt of the ice sheets covering Greenland and Antarctica to increase by nearly 30% since 1979.

Ocean Acidification

The ocean is one of the main ways in which CO2 gets absorbed. While at first glance that may sound like a net positive, the increasingly human-caused CO2 is pushing the world’s oceans to their limits and causing increased acidity. As pH levels in the ocean decrease, shellfish have difficulty reproducing, and much of the ocean’s food cycle becomes disrupted.

What Are the Solutions for Climate Change?

While the effects of climate change can seem bleak, there is still hope. By taking immediate action to curb climate change, we may never see the worst consequences. Likewise, as the world adopts cleaner, more sustainable energy solutions, there may be millions of new jobs created and billions of dollars of economic benefits. Below are some practical ways you can battle climate change, including:

- Switching to renewable energy (solar, wind, hydro)

- Purchasing Renewable Energy Certificates (RECs) for your home

- Using energy-efficient appliances and insulating buildings

- Offsetting your carbon emissions through verified programs

- Adopting plant-based diets and reducing meat consumption

- Minimizing food waste and single-use plastics

- Protecting and restoring forests and wetlands

- Supporting clean transportation options (EVs, public transit, biking)

Try the Terrapass Flight Carbon Calculator

Traveling by plane? Use the Terrapass Flight Carbon Calculator to estimate your flight emissions and support verified offset projects.

See How Terrapass Can Help Your Business

Companies facing growing pressure to cut emissions, whether from regulation, investors, or customers, can explore Terrapass’s business carbon offset programs to start addressing their footprint today.

Why Climate Change Matters to Everyone

Climate change isn’t just an environmental problem. It’s an everything problem. It touches every aspect of our lives:

- Jobs and the economy: Clean energy sectors are rapidly expanding and could create millions of new jobs worldwide.

- National security: Climate change exacerbates global instability, resource conflicts, and forced migration.

- Public health: Clean air, safe drinking water, and stable food systems are all at risk.

- Justice and equity: Low-income communities and developing nations are often hit hardest despite contributing the least to global emissions.

- Future generations: The choices we make today will shape the legacy we leave behind.

By investing in climate solutions now, we not only avoid catastrophe but also unlock opportunities for innovation, resilience, and shared prosperity.

FAQ: Climate Change

What is climate change?

Climate change refers to long-term shifts in temperature, precipitation, wind patterns, and other aspects of Earth’s climate system, largely driven today by human greenhouse gas emissions.

What is the difference between climate change and global warming?

Global warming specifically means the rise in the planet’s average surface temperature. Climate change is the broader term, covering the shifts in weather patterns, sea levels, and ecosystems that result from it.

What causes climate change?

The main driver is greenhouse gas emissions, especially carbon dioxide from burning fossil fuels, along with deforestation, agriculture, and livestock. Natural factors like solar activity play a much smaller role.

What are the effects of climate change?

Effects include more extreme weather, rising sea levels, shrinking ice sheets, ocean acidification, threats to food and water supplies, and growing risks to public health.

Is climate change getting worse in 2026?

The trend lines are still moving the wrong way. 2025 was the third-warmest year on record, global fossil fuel emissions hit a new record of 38.1 billion tonnes, and 2023–2025 was the first three-year period to average above 1.5°C over pre-industrial levels.

Can climate change be reversed?

It’s generally described as something we can slow and adapt to rather than fully reverse in the near term. Cutting emissions, protecting forests, and shifting to renewable energy can still prevent the worst outcomes.

What can I do to help stop climate change?

Individual actions add up: switching to renewable energy, using energy-efficient appliances, offsetting your carbon emissions, reducing meat consumption, and supporting clean transportation all make a difference.

Brought to you by Terrapass, your trusted partner in carbon offsets and climate education.

Sources:

- Rose, Brian E. “ATM 623: Climate Modeling.” Lecture04 – Climate System Components, atmos.albany.edu.

- “AAAS Reaffirms Statements on Climate Change and Integrity.” American Association for the Advancement of Science, aaas.org.

- “The Causes of Climate Change.” NASA, 6 Sept. 2019, climate.nasa.gov/causes.

- “The Carbon Cycle.” NASA, earthobservatory.nasa.gov/features/CarbonCycle/page5.php.

- Green, Julia K., et al. “Large Influence of Soil Moisture on Long-Term Terrestrial Carbon Uptake.” Nature, vol. 565, no. 7740, 2019, pp. 476–479, nature.com.

- “Is the Sun Causing Global Warming?” NASA, climate.nasa.gov.

- “Agriculture and Greenhouse Gas Emissions.” American Farm Bureau Federation, fb.org.

- “Deforestation and Climate Change.” Earth Day Network, earthday.org/campaigns/reforestation/deforestation-climate-change/.

- “REDD: Protecting Climate, Forests and Livelihoods.” International Institute for Environment and Development, 24 Jan. 2018, iied.org.

- “Sources of Greenhouse Gas Emissions.” EPA, 13 Sept. 2019, epa.gov.

- Goodland, Robert and Anhang, Jeff. “Livestock and Climate Change.” worldwatch.org.

- “Extreme Weather and Climate Change.” Center for Climate and Energy Solutions, 14 Aug. 2019, c2es.org.

- “DoD Releases 2014 Climate Change Adaptation Roadmap.” U.S. Department of Defense, defense.gov.

- “The Economic Case for Climate Action in the United States.” FEUUS, feu-us.org.

- “Climate Change and Public Health.” Centers for Disease Control and Prevention, cdc.gov.

- “Climate Impacts on Ecosystems.” EPA, 22 Dec. 2016, epa.gov.

- Kijne, Jacob W. “Hugh Turral, Jacob Burke and Jean-Marc Faurès: Climate Change, Water and Food Security.” fao.org.

- “Quick Facts on Ice Sheets.” National Snow and Ice Data Center, nsidc.org.

- “Copernicus: 2025 was the third hottest year on record.” Copernicus Climate Change Service, climate.copernicus.eu.

- “Assessing the Global Temperature and Precipitation Analysis in 2025.” NOAA NCEI, ncei.noaa.gov.

- “Fossil Fuel CO2 Emissions Hit Record High in 2025.” Global Carbon Project, globalcarbonbudget.org.

- “2025 in Review: U.S. Billion-Dollar Disasters.” Climate Central, climatecentral.org.

- “NASA Analysis Shows La Niña Limited Sea Level Rise in 2025.” NASA/JPL, jpl.nasa.gov.

The post What Is Climate Change? Causes, Effects & Solutions (2026) appeared first on Terrapass.

We will explore the process of burning fossil fuels and look at why they are burned and what sectors use the energy they supply. Then, we will cover what sort of products and greenhouse gases are released when fossil fuels are burned. Finally, we’ll view alternative energy solutions that are available for energy production.

Key takeaways

- Fossil fuels still supplied about 86% of global energy in 2025, only a slight decline from roughly 87% in 2024.

- Burning fossil fuels releases six main products: carbon dioxide, carbon monoxide, sulfur dioxide, nitrogen oxides, lead, and particulate matter.

- Carbon dioxide accounts for roughly 74% of global greenhouse gas emissions, and burning fossil fuels is the single largest source of it.

- Natural gas is the cleanest-burning fossil fuel, but it’s still primarily methane, a potent greenhouse gas.

- The three adverse effects of burning fossil fuels are air pollution, water pollution, and climate change.

- Renewable energy, nuclear power, and carbon offset programs are all viable ways to reduce reliance on fossil fuels today.

Fossil Fuels in 2026: The Latest Data

Despite years of clean energy investment, fossil fuels haven’t lost much ground yet, they’ve mostly just been joined by more of everything else. Here’s the latest picture, based on the Energy Institute’s 2026 Statistical Review of World Energy and the U.S. Energy Information Administration (EIA).

2026 fossil fuel data snapshot

- Global energy mix: Fossil fuels supplied about 86% of the world’s total energy in 2025, down only slightly from roughly 87% in 2024. Oil provided about a third of global supply, followed by coal and natural gas.

- Coal set a new record: Global coal use hit an all-time high in 2025, even as renewables grew faster in percentage terms, because total global energy demand kept rising alongside it.

- U.S. electricity: About 58% of U.S. utility-scale electricity generation came from fossil fuels in 2025 (down from roughly 60.6% in 2020), with natural gas alone supplying about 41%. Renewables reached nearly 26% of U.S. generation.

- Emissions: Global carbon dioxide emissions from energy rose 1.1% in 2025, with China accounting for roughly 31% of global emissions.

The takeaway: fossil fuel combustion is still growing in absolute terms even as its share of the energy mix inches down, which is why the effects and alternatives covered below remain just as relevant in 2026 as ever.

What Are Fossil Fuels?

Most of the fossil fuels we exploit today are the product of plants and animals that died 540 million to 65 million years ago and were buried in layers of sediment. Over time, the fossils were subjected to increased pressure and heat as the sedimentary rock layers of the earth’s crust continued to develop above them.

Eventually, these fossils turned into kerogen, also known as oil shale. After even more time, the oil shale was subjected to even greater temperatures and ultimately transformed into coal, oil, or natural gas. Fossil fuels consist of energy stores called hydrocarbons that form during exposure to immense heat and pressure.

What Is Fossil Fuel Combustion?

Fossil fuel combustion is the process of burning coal, oil, natural gases, or other fossil fuels to create energy. The use of fossil fuels creates around 80% of the world’s energy. While these fuels are an inexpensive way to produce power, they release large amounts of carbon dioxide and other greenhouse gases when combusted.

Creating electricity through burning fossil fuels utilizes a steam generator to create power. Fossil fuels are burned to heat water in boilers that make large amounts of steam. High pressure from the steam then rotates a turbine in a steam generator and creates power. This power is then transferred into the power supply.

Other forms of fossil fuel combustion come from the transportation sector. Burning fuel to power cars, trucks, and airplanes are all forms of fossil fuel combustion.

What Happens When You Burn Fossil Fuels?

Due to the presence of hydrocarbons, fossil fuels produce a substantial amount of energy per pound when combusted. Hydrocarbon-rich fossil fuels hold a large amount of energy potential that is released in the form of heat when combusted in the presence of oxygen.

However, these hydrocarbons also produce large amounts of carbon dioxide, which contributes to the greenhouse effect and in turn causes global warming. As the hydrocarbon compounds break down during combustion, the carbon dioxide is released alongside the heat energy.

Why Are Fossil Fuels Burned?

Burning fossil fuels creates energy in many different ways for people worldwide. Fossil fuels are responsible for powering the energy sector, transportation sector, and industrial sector.

In the energy sector, people rely on electricity generation for lighting, heating, and cooling in their homes and places of business. As of 2025, about 58% of U.S. utility-scale electricity generation still came from burning fossil fuels, according to the U.S. Energy Information Administration. Natural gas is also commonly used in homes and commercial buildings for heating, cooking, and other needs.

Fossil fuels are also used to power the transportation sector. In 2020, the U.S. transportation sector received 89% of its energy from petroleum fuel sources. People rely on personal vehicles, public transportation, and air travel to get where they need to be. Many of these modes of transportation rely on burning fossil fuels. Fossil fuels also power the transportation of goods around the world. Cargo ships, trucks, and airplanes are often powered with petroleum fuels.

Finally, the industrial sector relies on fossil fuels to create heat for their industrial practices and to create power to manufacture products. The industrial sector uses energy generated by burning fossil fuels to power electrical equipment like motors, lights, computers, and more. The manufacturing industry is responsible for using the most energy within the industrial sector.

What Do Fossil Fuels Release When Burned?

Six products are released due to the burning of fossil fuels. Each of these products affects the environment in different ways.

Carbon Dioxide

Of all the greenhouse gases, carbon dioxide is the most abundant when it comes to human-related emissions. Carbon dioxide is released in large quantities from burning coal, gas, and oil because these fuels are primarily composed of hydrocarbons released in the form of carbon dioxide once combusted. Coal burning is the primary source of carbon dioxide emissions, followed by burning oil, then natural gas.

Carbon Monoxide

Carbon monoxide is released when carbon-based fuel is not completely burned. The primary source of carbon monoxide emissions comes from road vehicles. Non-road vehicles, like boats or construction equipment, also contribute to carbon monoxide emissions.

Sulfur Dioxide

Sulfur dioxide is found in coal and oil. It can be emitted when these fossil fuels are burned and through the process of extracting gasoline from crude oil. When sulfur dioxide dissolves into water vapor and forms sulfuric acid, it interacts with other gases in the air, and sulfates are formed. This can lead to acid rain.

Nitrogen Oxides

Nitrogen oxides are released when fossil fuels are burned at high temperatures in motor vehicles or from other fuel-burning sources in industrial or home settings. Nitrogen dioxide, one common form of nitrogen oxide, creates smog over city centers.

Lead

Lead used to be a more common emission when leaded gasoline was used for vehicles. Today, most lead pollutants can be found in the air around factories that separate metal from ore.

Particulate Matter

Particulate matter is any solid particle or liquid droplet found in the air. Particulate matter is released when fossil fuels are burned and can be found in higher concentrations in regions that burn more fuels, like city centers or power facilities.

Why Is Burning Fossil Fuels a Problem?

The primary issue associated with burning fossil fuels is that the practice releases large quantities of greenhouse gases into the atmosphere. High concentrations of greenhouse gases in the atmosphere increase the global temperature and cause climate change.

Carbon dioxide is the most emitted greenhouse gas, accounting for roughly 74% of global greenhouse gas emissions, according to the Center for Climate and Energy Solutions’ analysis of European Commission emissions data. Burning fossil fuels is the activity responsible for emitting the most carbon dioxide around the world.

As the world continues to rely on fossil fuels for energy production and transportation, carbon emissions will continue to remain high. Global CO2 emissions from energy rose another 1.1% in 2025. If the globe does not mitigate the amounts of carbon dioxide released by burning fossil fuels, then we will continue to see increasing global temperatures and climate change.

What Are 3 Effects of Burning Fossil Fuels?

There are three adverse effects of burning fossil fuels: air pollution, water pollution, and climate change. These effects are caused by the products released when fossil fuels are burned.

Air Pollution

Air pollution occurs when products like sulfur dioxide, carbon monoxide, nitrogen oxides, and particulate matter are released from burning fossil fuels. Air pollution has been found to cause respiratory disease, cardiovascular disease, and cancer. Children, pregnant women, and elderly people are all at higher risk of the negative health effects caused by air pollution.

Water Pollution

Water pollution occurs when sulfur dioxide dissolves into water and creates sulfuric acid. This produces acid rain and can lead to the acidification of freshwater sources like lakes and streams. When these bodies of water become too acidic, life cannot survive in them. Acid rain can also affect local crops and soil acidity levels.

Climate Change

Climate change is a significant threat to ecosystems and human populations worldwide. Carbon dioxide emitted through burning fossil fuels plays a huge role in global warming. As more carbon dioxide is released into the atmosphere, more heat is trapped on earth through the greenhouse effect. Increasing global temperatures can lead to rising sea levels, deforestation, changing climates, and scarcity of food sources.

Which Fossil Fuel Is the Cleanest Burning?

Of the three primary fossil fuels, the cleanest burning fuel is natural gas. Using natural gas to generate energy emits less of all kinds of air pollutants and carbon dioxide than both oil and coal.

While natural gas is cleaner to burn for energy, it consists primarily of methane, a harmful greenhouse gas. Natural gas leaks are a leading cause of methane emissions each year in the United States. What is more, the process of locating natural gas wells and drilling for natural gas can have negative environmental impacts.

What Are Alternatives to Burning Fossil Fuels?

Alternatives to burning fossil fuels include renewable energy sources like hydroelectricity, wind power, and solar energy. Clean energy from nuclear power plants is another alternative to burning fossil fuels.

The benefit of transitioning to clean energy is a significant reduction in emissions. Nuclear energy and renewable energy sources have no emissions, which can slow the effect of climate change around the world.

A switch to entirely renewable energy systems would provide the best alternative to fossil fuels. Fossil fuels are non-renewable, meaning once the natural resource is diminished, we will not be able to continue using it. On the other hand, sustainable energy sources provide us with a supply we can never run out of, meaning increased energy security for future generations.

The Intergovernmental Panel on Climate Change emphasizes that these energy sources are essential for achieving long-term emissions reductions.

Burning Fossil Fuels? Only for the Time Being

Burning fossil fuels provides the majority of global energy. However, this natural resource is not sustainable and releases many harmful emissions when it is burned.

While fossil fuels are cheap and efficient, the globe should move forward to find better solutions on how to create energy. That way, we can avoid the negative effects that come along with burning fossil fuels while still providing the energy our planet relies on.

In the meantime, while the world energy system is still dependent on fossil fuels, you can make a difference by participating in carbon offsetting programs. These programs are designed to mitigate the carbon released from activities that burn fossil fuels.

For example, if you are taking a flight somewhere, you can purchase carbon offset credits that go toward projects that support reducing the amount of carbon in the atmosphere. Visit Terrapass today and view all of our carbon offset programs for individuals and businesses.

FAQ: Burning Fossil Fuels

What happens when you burn fossil fuels?

Burning fossil fuels releases the energy stored in their hydrocarbons as heat, along with six main byproducts: carbon dioxide, carbon monoxide, sulfur dioxide, nitrogen oxides, lead, and particulate matter.

Why are fossil fuels burned in the first place?

They’re burned because they’re an energy-dense, relatively inexpensive way to generate power for electricity, transportation, and industry. Fossil fuels still supplied about 86% of global energy in 2025.

What are the effects of burning fossil fuels?

The three main effects are air pollution, water pollution, and climate change, driven by the carbon dioxide, sulfur dioxide, and other byproducts released during combustion.

Which fossil fuel burns the cleanest?

Natural gas is the cleanest-burning of the three primary fossil fuels, emitting less air pollution and CO2 than coal or oil, though it’s still mostly methane, a potent greenhouse gas.

What are the alternatives to burning fossil fuels?

Renewable sources like solar, wind, and hydroelectric power, along with nuclear energy, are the main zero-emission alternatives. All are considered essential for long-term emissions reductions.

Is the world still relying on fossil fuels in 2026?

Yes. Fossil fuels supplied about 86% of global energy in 2025, and global coal use hit a new record even as renewables grew, because overall energy demand keeps rising.

Brought to you by terrapass.com

The post What Happens When You Burn Fossil Fuels? Effects & Alternatives appeared first on Terrapass.

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy10 months ago

Renewable Energy10 months agoSending Progressive Philanthropist George Soros to Prison?

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits