Canadian Solar Inc. (NASDAQ: CSIQ), one of the world’s largest solar technology companies, has taken a major step forward in sustainable solar manufacturing. The company recently announced the launch of its next-generation Low Carbon (LC) modules, which combine cutting-edge wafer innovations with advanced heterojunction (HJT) cell technology.

Designed for utility-scale and commercial & industrial (C&I) markets, the new modules are engineered to deliver one of the lowest carbon footprints in the industry—just 285 kg CO₂eq per kW, setting a new standard for eco-friendly solar power solutions.

Canadian Solar Leads the Way in Low-Carbon Solar Technology

The company revealed that the LC modules are expected to begin deliveries in August 2025 and offer up to 660 Wp output with 24.4% efficiency, helping businesses and utilities deploy high-performance solar systems with a much smaller environmental impact. Canadian Solar’s proprietary improvements across multiple stages of production have enabled these breakthroughs in both efficiency and sustainability.

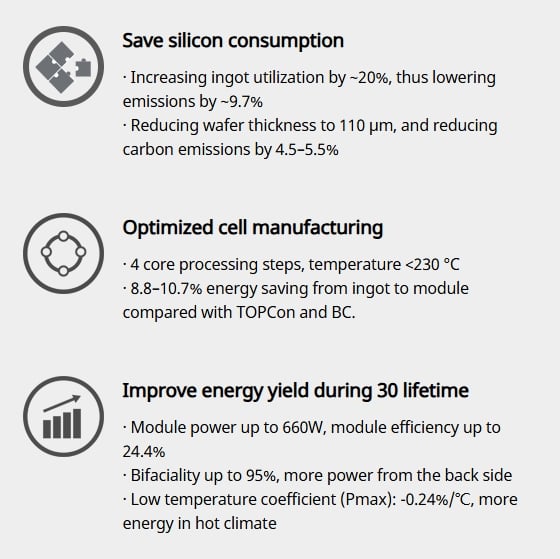

Key advancements include:

- Higher ingot utilization: By increasing ingot use by around 20%, emissions are cut by approximately 9.7% or 30 kg CO₂ per kWp.

- Thinner wafers: Reducing wafer thickness to 110 μm (from 130–135 μm) lowers silicon usage and carbon emissions by 4.5%–5.5% or 14–19 kg CO₂ per kWp.

- Optimized HJT cell production: Streamlining the process to four steps (compared to 10–13 in conventional methods) and lowering operating temperatures from 960°C–1050°C to below 230°C saves 4.2%–5.7% or 14–21 kg CO₂ per kWp.

- Lower total energy consumption: The total energy used in manufacturing is 105.62 MWh/MW, reducing energy use by 8.8%–10.7% versus traditional production.

Collectively, these innovations reduce the carbon payback time by 11% compared to standard N-type silicon-based modules.

Features of Low-Carbon Modules

Power Packed, Planet Friendly

The new LC modules allow customers to achieve two important goals at once: higher energy output and lower environmental impact. This is particularly vital for investors and businesses looking to meet ambitious ESG targets without sacrificing performance or reliability.

Canadian Solar’s modules are fully compatible with their inverter portfolio. Their 350-kW utility inverters with 40 A MPPT DC input current optimize energy capture, even in high-temperature environments up to 45°C, helping customers maximize returns in challenging climates.

Thomas Koerner, Corporate Senior Vice President of Canadian Solar, noted,

“We are proud to introduce our new environmentally friendly, low-carbon modules, marking a key milestone in sustainable solar manufacturing. By combining advanced wafer innovations with heterojunction (HJT) cell technology, we are significantly reducing the carbon footprint of solar energy while maintaining the proven reliability and high efficiency Canadian Solar is known for.”

The LC modules will be showcased at RE+ 2025 in Las Vegas from September 9–11, highlighting the company’s leadership in sustainable solar technology.

Strong Financial Performance Supports Green Goals

Solid financial results back Canadian Solar’s commitment to sustainability. In Q2 2025, the company reported:

- 7.9 GW of solar module shipments, a 14% quarter-over-quarter increase, meeting their guidance of 7.5–8.0 GW.

- 29.8% gross margin, exceeding expectations of 23%–25%.

- $1.7 billion in net revenues, up 42% from the previous quarter and 4% year-over-year, driven by strong battery storage and solar sales.

- $505 million in gross profit, compared to $140 million in Q1 2025 and $282 million in Q2 2024.

The improvements in profitability reflect increased demand for clean energy products and favorable market conditions, including adjustments to U.S. anti-dumping and countervailing duty regulations.

Canadian Solar operates through two main segments:

- CSI Solar: Manufacturing solar modules and battery energy storage solutions.

- Recurrent Energy: Developing and managing utility-scale solar and storage projects.

With nearly 165 GW of solar modules delivered, 13 GWh of battery storage shipped, and a $3 billion contracted backlog, the company’s growth is tightly aligned with global decarbonization efforts.

From Power to Purpose: Canadian Solar’s Path to Net-Zero

Canadian Solar’s mission is to power the world with clean solar energy while applying ESG principles throughout its operations.

The company aims to run on 100% renewable energy by 2030. By 2028, it plans to reach 82% and achieve a carbon payback period of 10 months or less for its solar systems. It also supports circular economy practices to reduce waste and use resources more efficiently.

Its efforts to expand renewable energy sourcing include:

- Signing Power Purchase Agreements (PPAs).

- Leveraging Renewable Energy Certificates (RECs).

- Expanding rooftop solar projects across manufacturing facilities.

Additionally, it has secured Green Electricity Certificates (GECs) for its factories in Inner Mongolia and Qinghai, covering 541,169 MWh of clean power, and bought 42,873 MWh from spot markets. All of its revenue comes from renewable energy, highlighting its leadership in climate action.

Emission Reductions

- By running 147 energy-saving programs, it cut 141,836 tCO₂e in greenhouse gases. This helped lower its emissions intensity to 71 tCO₂e per MWp, a 4% drop from 2023.

Although the company slightly missed its 2024 target of 69 tCO₂e per MWp due to lower factory use, it remains committed to improving processes and technologies to further reduce emissions and support long-term sustainability.

Partnerships and Global Initiatives

In May 2024, it joined the Solar Stewardship Initiative (SSI), a European collaboration that promotes responsible sourcing and sustainable solar production. The company is actively participating in governance, environmental, and labor rights assessments, with audits expected to be published in mid-2025.

Transforming Solar Solutions into Investment Opportunities

For investors, Canadian Solar presents a compelling case. The company’s innovations in low-carbon manufacturing not only enhance its market competitiveness but also align with global ESG priorities. Its steady growth, robust backlog, and proven expertise in delivering high-efficiency solar and storage solutions make it a sound choice for long-term investment.

With the global energy transition accelerating, Canadian Solar’s leadership in sustainable technology, transparent governance, and measurable carbon reductions positions it as a key player in shaping the future of renewable energy.

The post Canadian Solar Launches Low Carbon Modules, Setting New Standards in Sustainable Solar Energy appeared first on Carbon Credits.

Since the Industrial Revolution, human activities have left a significant and growing mark on the natural world. Pollution, carbon emissions, and altered land use have degraded ecosystems, contaminated water supplies, and pushed global temperatures to record highs. These are not distant consequences. They affect the air people breathe, the food they eat, and the stability of the climate every community depends on.

Understanding the environmental effects of industry is the first step toward meaningful change. When we grasp the full picture of how industrial practices damage the planet, we can make better decisions at every level, from individual choices to corporate policy to government regulation.

This guide covers the origins of industrial pollution, its specific environmental impacts, which industries carry the heaviest footprint, and the solutions that are already making a difference. We also highlight companies leading by example and explain how businesses of all sizes can take action today.

How Did the Industrial Revolution Cause Environmental Pollution?

The Industrial Revolution began in England in the 18th century before spreading through Europe and across the world. Nations shifted from agrarian economies to industrial ones, and fossil fuels were burned on a massive scale to power that transition. The environmental deterioration that followed has been compounding ever since.

Land use changed dramatically alongside industrial growth. As factories and urban centers expanded, farmland shrank and agriculture itself became industrialized. Industrial farming introduced fossil-fuel-powered machinery, synthetic fertilizers, pesticides, and concentrated livestock operations. The result was soil deterioration, widespread air and water pollution, and a significant rise in greenhouse gas emissions from the agricultural sector alone.

Deforestation and urbanization compounded the damage by eliminating natural carbon sinks. Forests and wetlands that once absorbed carbon dioxide from the atmosphere were cleared for development, removing the land’s natural ability to absorb carbon and leaving more greenhouse gases concentrated in the air.

The numbers tell the story clearly. Atmospheric CO2 was consistently around 280 parts per million before industrialization began. According to the IEA, CO2 concentrations reached approximately 427 parts per million in 2025, more than 50% above pre-industrial levels, with total energy-related emissions hitting a record high of nearly 38.4 billion tonnes. That figure has risen every decade since the Industrial Revolution began.

Industrialization continues today in developing nations, many of which lack the financial infrastructure to adopt clean energy and rely instead on coal, oil, and petroleum to power their growing economies. Even many developed nations remain heavily dependent on polluting industries, continuing to add to global greenhouse gas concentrations.

What Are the Environmental Impacts of Industry?

Industrial pollution creates environmental damage at every scale, from local waterways to the global atmosphere. The consequences affect ecosystems, human health, and the long-term stability of the climate. Below are the three primary categories of environmental impact driven by industry.

Pollution

Industry causes pollution across water, air, and soil, the three foundations of life on Earth. Each type of pollution carries its own chain of consequences.

Water pollution occurs in both freshwater systems and oceans. Water used in industrial processes becomes contaminated when it contacts metals, chemicals, or radioactive waste, and that water is often discharged into rivers and waterways. The result is contaminated drinking water, damaged aquatic ecosystems, and crops irrigated with polluted water that can become harmful to consume. Globally, 80% of wastewater is still released untreated into the environment.

Air pollution is any physical, biological, or chemical change to the atmosphere that reduces air quality. Gas, smoke, and fine particulate matter from burning coal or natural gas cause respiratory and cardiovascular disease in humans and threaten ecosystems globally. Air pollution now contributes to approximately 7.9 million premature deaths per year worldwide, making it one of the leading environmental causes of mortality. Airborne contaminants also cause acid rain, which ruins crops and acidifies freshwater bodies.

Soil pollution occurs when chemical levels in the ground exceed safe thresholds and present a threat to human health or ecosystems. Soil becomes polluted through industrial waste, chemical pesticides and fertilizers, oil spills, and landfills. Heavy metal contamination from industrial waste currently affects an estimated 20% of global agricultural land. Contaminated soil reduces crop yields, harms wildlife, and can lead to serious health problems in humans and animals living in affected areas.

Ecological Consequences

Pollution and altered land use place severe strain on ecosystems in ways that ripple outward for generations. Three interconnected effects stand out.

Habitat destruction results from deforestation, urban expansion, and industrial development. When natural habitats are destroyed or fragmented, plants and animals lose the environments they need to survive. Species are pushed into shrinking territories, forcing greater competition for resources and raising extinction risks. According to current data, 33% of global soils are degraded due to pollution and erosion, compressing the productive land available to both agriculture and wildlife.

Slower environmental recovery is another consequence of the cumulative strain on ecosystems. Natural disasters like wildfires and hurricanes are growing more frequent and severe as the climate shifts, and ecosystems already weakened by pollution and habitat loss take longer to recover from each new event. Industrial accidents, such as oil spills or chemical leaks, add further damage that can persist in an environment for decades.

Biodiversity loss continues to accelerate as species go extinct at rates far above natural baselines. The combination of habitat destruction, pollution, climate change, and resource depletion creates overlapping pressures that many species cannot adapt to quickly enough.

Atmospheric Changes

Industrial practices release large quantities of greenhouse gases into the atmosphere, driving global warming and climate change. These two phenomena are distinct but deeply linked.

Global warming occurs when greenhouse gases like CO2 and methane accumulate in the atmosphere and trap heat that would otherwise radiate into space. Burning fossil fuels is the primary driver of CO2 buildup. Agricultural practices and landfills release significant quantities of methane, a greenhouse gas with more than 80 times the short-term warming power of CO2.

Climate change is the broader set of consequences that follows from global warming. Rising temperatures shift rainfall patterns, intensify storms, accelerate glacial melting, raise sea levels, and make agricultural conditions less predictable. Every fraction of a degree of additional warming increases these risks. The remaining carbon budget for limiting warming to 1.5 degrees Celsius is now projected to be exhausted by 2029 at current emission rates.

What Industries Have the Largest Environmental Impact?

Some industries carry a disproportionately large environmental footprint. Researchers evaluate environmental impact across six key components: greenhouse gas emissions, water use, waste generation, land and water pollutants, air pollutants, and natural resource use. The industries that dominate these categories are as follows.

Energy and electric utilities are the most polluting sector on Earth, generating approximately 15.83 billion tonnes of greenhouse gas emissions annually. The energy sector ranks highest in four of the six environmental impact categories: greenhouse gas emissions, waste, air pollutants, and natural resource use. As long as coal and natural gas remain central to electricity generation, this sector will continue to lead all others in environmental damage.

Transport is the second most polluting industry globally, responsible for around 8.43 billion tonnes of greenhouse gas emissions each year. Road transport accounts for the majority of that figure, while aviation and shipping contribute significantly. The sector is under growing pressure to electrify and adopt cleaner fuels.

Manufacturing and construction generate approximately 6.3 billion tonnes of emissions annually and consume vast quantities of raw materials including metals, sand, and timber. This sector appears across all six environmental impact categories, reflecting its broad footprint across pollution, resource use, and land disruption.

Food production ranks as the highest non-utility industry in water use and land and water pollutants. Industrial agriculture is responsible for the majority of freshwater withdrawals globally and is a leading driver of deforestation, soil degradation, and chemical runoff into waterways.

How Can the Environmental Impact of Industry Be Reduced?

Meaningful solutions to industrial pollution already exist. The challenge is implementing them at speed and scale. Below are the most impactful approaches available to businesses and industries today.

Better Waste Management

Improperly handled industrial waste is one of the most direct and preventable causes of environmental pollution. When waste is not treated and disposed of correctly, it contaminates waterways, soil, and groundwater. Industries that invest in proper waste treatment and disposal systems can eliminate a significant portion of their local environmental impact. This is also an area where regulation has historically produced measurable results.

Improved Recycling and Water Reuse

Unnecessary pollution occurs when recyclable materials and reusable water are instead discarded. Industrial water recycling, for example, keeps contaminated water within closed systems rather than releasing it into rivers and oceans. Expanding recycling programs across manufacturing sectors reduces both raw material extraction and waste generation, addressing two environmental problems at once.

Greenhouse Gas Mitigation and Carbon Offsetting

Reducing greenhouse gas emissions from industrial processes is the single most important lever for slowing climate change. Switching to renewable or clean energy cuts emissions at the source. Gas capture programs reduce methane and other potent greenhouse gases that would otherwise escape from operations like landfills and agricultural sites. For emissions that cannot yet be eliminated, verified carbon offset programs allow businesses to fund reforestation, methane capture, and renewable energy projects that compensate for their remaining footprint. Understanding the social cost of carbon helps businesses make the case internally for these investments.

Smarter Land Use

Industrial site selection and land management have lasting ecological consequences. Businesses should choose locations that minimize habitat disruption and avoid high-risk areas where accidents like fires or spills could cause catastrophic environmental damage. Reducing resource extraction on sensitive lands and funding environmental restoration projects, including reforestation and wetland rehabilitation, helps offset the land-use impact of ongoing operations. Carbon removal credits are one mechanism businesses can use to support these restoration efforts directly.

Advancing Technology

Older industrial technologies are often energy-inefficient and generate disproportionately high levels of pollution. Upgrading to newer equipment and processes allows industries to reduce emissions and resource consumption simultaneously. Switching to renewable energy, adopting AI-driven energy management, and investing in cleaner production technologies are all practical steps that industries can take now. The companies seeing the most progress are those that have embedded sustainability goals into their technology roadmaps rather than treating them as separate initiatives.

Environmental Awareness and Impact Assessment

Education and measurement underpin all other solutions. Industries that conduct regular environmental impact assessments, track their resource consumption and emissions, and train employees on sustainability practices are better positioned to identify problems early and respond effectively. Measuring and managing your carbon footprint is as essential for businesses as financial reporting, and increasingly, regulators and investors are requiring exactly that.

What Companies Are Reducing Their Environmental Impact?

Several major companies have made substantial commitments to reducing their environmental footprint and serve as benchmarks for the rest of the corporate world. Their progress, and in some cases their setbacks, offer useful lessons for any business navigating the transition to more sustainable operations.

Microsoft has been carbon neutral since 2012 and has set more ambitious targets since then. The company’s 2025 Environmental Sustainability Report outlines its goals to become carbon negative, water positive, and zero waste by 2030. Microsoft charges an internal carbon fee to business units and reinvests those funds into carbon reduction and removal initiatives. The company achieved its goal to protect more land than it uses by 2025 and has invested in renewable energy across 16 countries, including its first large-scale nuclear energy agreement.

Intel aims to be net positive on water use and achieve 100% renewable energy for its global operations by 2030. Intel links a percentage of employee compensation to corporate sustainability metrics, recognizing that achieving environmental goals requires company-wide participation rather than top-down mandates alone.

Alphabet (Google) has made significant progress on data center efficiency, reducing data center energy emissions by 12% in 2024 despite a 27% increase in overall electricity consumption, driven largely by AI workloads. Google’s data centers now provide six times more computing capacity per unit of electricity compared to five years ago. In 2024, Google signed agreements for more than 8 gigawatts of clean energy, the highest annual volume in the company’s history. The company has also pioneered AI-driven cooling systems for its data centers that dramatically reduce energy waste. It is worth noting that all three of these companies face the growing challenge of rising energy demand from AI infrastructure, a reminder that sustainability commitments require continuous adaptation as business models evolve.

Changing the Environmental Impact of Industry

More than two centuries of large-scale industrial activity have given us a clear view of the consequences. Pollution, ecological damage, and atmospheric change are not side effects we can manage around. They are the defining environmental challenge of our time, and the window for meaningful action is narrowing.

The good news is that solutions are no longer theoretical. Renewable energy is now cost-competitive with fossil fuels in most markets. Carbon capture and offset programs are funding real-world emissions reductions. Companies across every sector are finding that sustainable practices often improve efficiency and reduce long-term costs alongside their environmental benefits.

Whether you run a business or simply want to understand your own role in this picture, the path forward starts with knowing where you stand. Visit Terrapass to learn how you can measure your carbon footprint, reduce your emissions, and support verified projects that make a difference.

Brought to you by terrapass.com

The post The Environmental Impact of Industry: Causes, Effects & Solutions appeared first on Terrapass.

Humanity is consuming natural resources faster than the planet can replenish them, and the gap is growing. The result is environmental degradation, economic risk, and a shrinking inheritance for future generations. With the global population still rising and consumption habits in wealthy nations showing little sign of slowing, addressing overconsumption has never been more urgent.

This guide explains what overconsumption of natural resources means, which resources are most at risk, how it harms the environment, and what individuals and industries can do about it.

Key Takeaways

- Earth Overshoot Day 2026 falls on July 30, the point at which humanity exhausts the planet’s entire annual ecological budget with five months still remaining in the year.

- Humanity is currently using nature 73% faster than Earth’s ecosystems can regenerate, the equivalent of consuming 1.73 planets simultaneously. This is the highest level of ecological overshoot ever recorded.

- The two most consumed natural resources on Earth are water and sand.

- North Americans consume an average of 90 kilograms of natural resources per person per day, nine times more than the average African.

- Transitioning to renewable energy, sustainable agriculture, and circular economy practices are the most effective paths forward.

What Is Overconsumption of Natural Resources?

Overconsumption occurs when humans extract or use natural resources faster than the planet can replenish them. When this happens, ecosystems cannot recover from excessive resource extraction, leading to biodiversity loss and long-term deterioration of the natural world. Once a resource is fully depleted from a region, it is often gone permanently.

The logging industry is a clear example. Timber is used for construction, paper manufacturing, and fuel. Billions of people depend on it for shelter, heat, and cooking. But overconsumption of timber leads to deforestation. Since 1990, the world has lost 420 million hectares of forest land, and between 2001 and 2025, total global tree cover loss reached 540 million hectares driven primarily by agricultural expansion, logging, and infrastructure development.

The stakes are not abstract. When essential resources like clean water, fertile land, and building materials disappear, the consequences fall hardest on the most vulnerable communities around the world.

How Does Overconsumption Affect Natural Resources?

Natural resources need time to replenish. Forests must regrow after logging. Fish populations must recover after commercial fishing. Aquifers refill slowly after extraction. When human demand exceeds these regeneration rates, the consequences compound over time.

A useful benchmark is Earth Overshoot Day, the calendar date each year when humanity’s demand for ecological resources exceeds what Earth can regenerate in that same year. In 1972, overshoot day fell on December 31, meaning humanity was living within the planet’s means. By 2026, it falls on July 30, the highest level of ecological overshoot in human history. From that point on, we operate on ecological credit for the rest of the year, drawing down natural capital in forests, fisheries, freshwater systems, and the atmosphere’s capacity to absorb CO₂.

Understanding this dynamic is central to understanding how climate change and resource depletion are connected and why action on both fronts is urgent.

What is an ecological footprint?

An ecological footprint measures the land and water area a human population requires to produce the resources it consumes and absorb the waste it generates. When a nation’s footprint exceeds its biocapacity, it runs an ecological deficit. More than 80% of the global population lives in countries currently running such a deficit.

What Natural Resources Are We Consuming?

Natural resources fall into two broad categories: non-renewable and renewable. Both are under pressure from overconsumption, though for different reasons.

Non-Renewable Resources

Non-renewable resources form over millions of years and cannot be meaningfully replenished on human timescales. They include fossil fuels like oil, coal, and natural gas, as well as mined materials such as metals, ores, diamonds, sand, and other raw materials.

Relying heavily on non-renewables carries serious economic risk. More than 80% of the world’s energy still comes from oil, coal, and natural gas. The consequences of burning fossil fuels extend well beyond supply risk. They include greenhouse gas emissions, air pollution, and accelerating climate change. If fossil fuels became too scarce or expensive to extract, the disruption to the global economy would be severe, with no ready substitute available at the same scale.

Demand for critical minerals like lithium, cobalt, and copper is also expected to surge dramatically in coming decades, driven by the transition to electric vehicles and renewable energy infrastructure. Even the green energy transition has its own resource demands to manage carefully.

Renewable Resources

5")

Renewable resources replenish naturally in a much shorter timeframe. They include solar and wind energy, food crops, fish, animals, and lumber.

Wind and sunlight are effectively limitless as energy sources. We can use them without depleting them, which is why transitioning to sustainable energy sources is such a critical lever for reducing overall resource pressure. Biological renewables like fish populations and forests, however, must be carefully managed to avoid overexploitation.

Fish stocks are a pressing concern. The FAO reported that 35.5% of global fish stocks were overfished in 2025, continuing an upward trend from previous years. Overfishing doesn’t just reduce the catch available today. It disrupts marine food webs, causes biodiversity loss, and threatens the livelihoods of coastal communities worldwide.

Overconsumption also degrades fertile agricultural land. As soil quality deteriorates and water becomes scarcer, the capacity to feed a growing global population comes under increasing strain.

How Does Consumption of Natural Resources Vary by Country?

Resource consumption is closely correlated with national wealth. Wealthier nations consume 10 times more natural resources than developing countries.

North America leads global per-capita consumption. The average North American uses 90 kilograms of resources per day, compared to 45 kilograms for the average European and just 10 kilograms for the average African resident. According to Scientific American, over a single lifetime, one American will consume 53 times as many goods and services as a person from China and as many natural resources as 35 residents of India.

This disparity matters because it shapes where solutions need to be concentrated. High-consumption nations bear disproportionate responsibility for driving global resource depletion and have the greatest capacity to change. Understanding your own carbon footprint is a meaningful first step toward making that change personal.

How Does Overconsumption of Natural Resources Affect the Environment?

The environmental impacts of resource-intensive industries are wide-ranging and interconnected. Some are direct. Deforestation removes habitat and releases stored carbon. Others work through a longer chain, as industries that harvest natural resources generate greenhouse gas emissions that accelerate climate change, which in turn threatens the very resource systems we depend on.

Consider the construction industry. It requires metals mined from the Earth, sand and lumber as building materials, and fossil fuels to power its machinery. Each of these inputs carries its own environmental cost including habitat disruption, water use, and carbon emissions, and they compound across the full supply chain.

Atmospheric greenhouse gas concentrations have risen from 367 parts per million CO₂ equivalent in 1972 to an estimated 547 parts per million in 2026, according to NOAA estimates. The accumulated ecological debt from overshoot since the early 1970s now equals approximately 20.6 years of the planet’s full biological productivity.

Protecting land and ocean ecosystems and transitioning to sustainable energy sources represents humanity’s best opportunity to reverse this trend. For businesses already thinking about their role in this, carbon offsets can support reforestation and emissions reduction projects that directly address the damage overconsumption has caused.

What Are the Most Consumed Natural Resources?

The two natural resources consumed in the greatest quantities globally are water and sand.

Sand

Sand is the world’s second most consumed natural resource, used primarily in concrete for construction. Global urbanization drives an enormous appetite for it, and humanity extracts approximately 50 billion tons of sand each year. The consequences include the deterioration of river systems and ocean habitats as sand is removed in vast quantities.

Water

Water is the most consumed natural resource on Earth. It is essential for drinking, agriculture, cooking, industrial processes, and electricity generation. Despite water covering 70% of the planet’s surface, 97.5% of that water is ocean water. Accessible freshwater is a genuinely finite resource.

The numbers reveal the scale of the problem. About 4 billion people, nearly two-thirds of the global population, experience severe water scarcity for at least one month each year. Agriculture accounts for roughly 70% of all global freshwater withdrawals. According to the BBC, 21 of Earth’s 35 major aquifers are already receding. Climate change is deepening the crisis by intensifying droughts and altering rainfall patterns precisely where demand is growing fastest.

The global carbon cycle is tightly linked to freshwater availability. Warming temperatures and disrupted precipitation patterns are a direct consequence of the same fossil fuel overconsumption that drives resource depletion more broadly.

How Can We Slow the Overconsumption of Natural Resources?

6")

Slowing overconsumption requires action at multiple levels: policy, industry, and individual behavior. The most impactful changes involve moving away from non-renewable resources, improving efficiency across industries, and embracing the principles of a circular economy, in which materials are reused and regenerated rather than consumed and discarded.

Transition to renewable energy. New technologies continue to lower the cost and improve the efficiency of renewable energy sources like wind and solar. Accelerating this transition reduces fossil fuel burning and the extraction pressures that come with it. Renewable Energy Credits (RECs) are one accessible way for households and businesses to support clean power today.

Sustainable agriculture and fisheries management. More efficient food production, better fisheries regulation, and reduced food waste can protect natural lands and fish populations while feeding a growing global population. Reducing meat consumption is one of the highest-impact dietary changes an individual can make.

Water desalination and conservation. Desalination technology can convert ocean water into freshwater suitable for drinking and agriculture, reducing pressure on strained freshwater systems. Conservation measures in agriculture, which is by far the dominant user of freshwater, can make an outsized difference.

Circular economy practices. Designing products for longevity, repairability, and recyclability reduces the total volume of resources extracted and the waste generated. This model is gaining traction across manufacturing, construction, and packaging industries and is increasingly recognized as one of the most commercially viable paths to sustainability.

Carbon offsetting. For emissions and resource use that cannot yet be eliminated, verified carbon offsets fund projects that reduce deforestation, capture methane, and support renewable energy development. Terrapass carbon offset projects include reforestation, REDD+, landfill gas capture, and residential solar installation.

Individual action. Each person can meaningfully reduce their ecological footprint by being conscious of consumption habits. Buying less, choosing durable goods, reducing food waste, and reusing materials wherever possible all add up. Use the Terrapass carbon calculator to understand exactly where your personal footprint comes from and take targeted action.

Frequently Asked Questions

What are the main natural resources being overconsumed?

The most overconsumed resources include freshwater, sand, fossil fuels (oil, coal, and natural gas), timber from forests, and fish stocks. Fertile agricultural land and minerals like lithium and cobalt are also under increasing pressure.

Which country consumes the most natural resources per person?

North Americans, and Americans in particular, consume the most natural resources per capita. The average North American uses 90 kilograms of resources per day, compared to 45 kilograms in Europe and 10 kilograms in Africa.

What is Earth Overshoot Day and why does it matter?

Earth Overshoot Day marks the point in the calendar year when humanity has used up all the ecological resources the planet can regenerate that year. In 2026, it falls on July 30, the highest level of ecological overshoot ever recorded. Everything consumed after that date draws down ecological reserves, accelerating long-term depletion.

How does overconsumption drive climate change?

Overconsumption drives climate change primarily through the extraction and burning of fossil fuels, deforestation (which releases stored carbon), and industrial processes that generate greenhouse gas emissions. Understanding how the carbon cycle works helps explain why reducing consumption and offsetting emissions are two sides of the same solution.

How can individuals reduce their impact?

The most effective individual actions include reducing home energy use, minimizing food waste, consuming less meat, and buying durable goods over disposable ones. Calculating your carbon footprint is a good starting point, and offsetting unavoidable emissions through Terrapass helps fund real-world emissions reductions.

What is a circular economy?

A circular economy is an economic model designed to eliminate waste by keeping materials in use for as long as possible through reuse, repair, remanufacturing, and recycling. It contrasts with the dominant take-make-dispose model that drives overconsumption and is increasingly seen as one of the most practical large-scale responses to ecological overshoot.

Taking Action to Protect Natural Resources

Overconsumption is depleting the natural systems that all human life depends on. The data is stark. In 2026, humanity hit the highest level of ecological overshoot ever recorded, and the real human footprint is still growing.

The solutions exist. Renewable energy, sustainable resource management, and a shift toward circular economic models can collectively move us back toward a world that operates within planetary limits. Technology continues to improve our capacity to do more with less, from precision agriculture to advanced water treatment to verified carbon markets.

Systemic change is essential, but individual choices also matter. A world of responsibly consumed resources is a world of greater health, stability, and opportunity for everyone including future generations.

Learn how Terrapass can help you reduce your carbon footprint and offset your consumption.

Brought to you by terrapass.com

The post Overconsumption of Natural Resources: Causes, Effects & Solutions (2026) appeared first on Terrapass.

As electricity demand rises and renewable energy grows in the U.S., battery storage is key. Waymo has launched a battery repurposing program to give retired electric vehicle (EV) batteries a new purpose in the power sector.

Waymo is working with B2U Storage Solutions to turn used batteries from its all-electric fleet into large-scale energy storage systems. Instead of recycling these batteries after use, Waymo will repurpose them to store electricity and support local power grids.

This program reflects a commitment to the circular economy, keeping products useful before recycling.

Adam Lenz, Head of Sustainability & Environment at Waymo, said:

“Our shared fleet of EVs provide a massive opportunity to support the growth of clean energy on the electricity grid while expanding the circular economy. Through this partnership, we can repurpose our batteries for local grid storage and ensure our batteries continue to provide economic and environmental value to the community long after they’ve retired from the road.”

Turning Old EV Batteries Into Energy Assets

EV batteries often retain significant storage capacity after their driving days. While their performance may drop for vehicles, many can still serve well in energy storage projects.

The press release says that retired Waymo batteries will join grid-connected energy storage systems through this partnership. These systems will store electricity from renewable sources like solar and wind.

During peak renewable generation, especially when solar production is high, the batteries will absorb excess electricity. Later, when demand increases in the evening, this stored energy can flow back into the grid.

This process helps balance electricity supply and demand, making renewable energy more reliable.

B2U specializes in second-life battery storage technology. They will manage the batteries during their second use and ensure proper recycling when they reach the end of their life.

Here’s a picture to show how B2U’s storage works.

This collaboration creates a complete lifecycle pathway for EV batteries—from vehicle use to energy storage and finally recycling.

Supporting Growing Demand for Battery Storage

This initiative comes at a time of rapid growth in renewable energy and battery storage in the U.S.

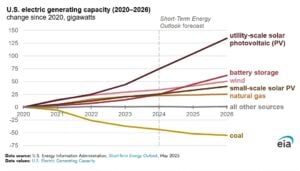

- According to the U.S. Energy Information Administration (EIA), developers plan to add 86 gigawatts (GW) of new utility-scale electricity generation capacity by 2026. If completed, it would be a record increase.

Solar energy will account for over half of these additions, with battery storage the second-largest category. Wind energy also plays a significant role in this growth.

In 2025, the U.S. power sector added 53 GW of new capacity, the highest since 2002. Meanwhile, battery storage installations keep increasing.

- They also expect to add about 24 GW of utility-scale battery storage in 2026, surpassing the previous record of 15 GW installed in 2025. Over the last five years, more than 40 GW of battery storage capacity has been added to the grid.

Texas, California, and Arizona are expected to account for around 80% of the planned battery storage in 2026.

The Grid Advantage of Reusing EV Batteries

Repurposing EV batteries offers crucial benefits for power systems and communities.

First, it extends the useful life of battery materials. Making lithium-ion batteries requires a lot of critical minerals and energy. Second-use batteries maximize the value of those materials.

Second, second-life batteries can lower energy storage costs. Since the batteries have already served in transportation, utilities can access storage capacity at lower costs than buying new systems.

Third, repurposing helps reduce electronic waste. Companies can keep batteries in use for several more years, easing pressure on waste management.

- Most importantly, battery storage boosts grid reliability. Renewable sources like solar and wind don’t produce electricity constantly. Energy storage systems fill this gap by storing power when production is high and delivering it when demand rises.

As renewable energy grows, these storage systems will be vital for stable electricity networks.

Freeman Hall, CEO of B2U Storage Solutions, said:

“This agreement marks a significant milestone in B2U’s mission to provide integrated repurposing services to the automotive industry. By extending the use of these batteries as grid storage, we are monetizing the full potential of EV batteries, now providing crucial stability to the power grid as energy demand continues to grow.”

First Deployments Planned for Texas and California

The first battery storage projects in the Waymo-B2U partnership will focus on Texas and California. Waymo already provides public autonomous ride-hailing services in these states.

Both states lead in renewable energy deployment. California increasingly relies on clean electricity and often has periods where renewable generation exceeds demand. Texas continues to lead the nation in new solar installations.

Waymo plans to repurpose old EV batteries into stationary storage systems. This will help manage renewable energy growth and improve local electricity infrastructure.

The company believes this initiative could deploy hundreds of megawatts of storage capacity in these regions. As autonomous EVs retire, their batteries could continue to provide value long after leaving the road.

This partnership shows how transportation electrification and clean energy can work together. Instead of viewing used EV batteries as waste, Waymo and B2U are transforming them into valuable energy assets. These assets support grid reliability, renewable energy integration, and a sustainable circular economy.

Waymo’s Broader Sustainability Efforts

The battery repurposing program is part of Waymo’s larger sustainability strategy. The company operates one of the largest fleets of fully autonomous electric vehicles, providing over 500,000 paid EV trips each week. These trips help cut emissions by replacing conventional vehicles with electric ones.

- Waymo estimates that every 500,000 weekly trips prevent about 530 tons of carbon dioxide emissions.

It also measures emissions avoided through its autonomous electric service. This framework evaluates the environmental benefits of electric, autonomous, and shared mobility solutions.

Additionally, the company reports its greenhouse gas emissions through parent company Alphabet as part of broader environmental efforts.

The post Waymo and B2U Unlock a Second Life for EV Batteries with Grid-Scale Storage appeared first on Carbon Credits.

-

Climate Change10 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases10 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy8 months ago

Renewable Energy8 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases11 months ago

嘉宾来稿:探究火山喷发如何影响气候预测