Weather Guard Lightning Tech

Siemens Gamesa, Vestas, Ørsted Updates: Finances, Fallen Rotors, and Offshore Wind Outlook

This week we analyze recent news from Siemens Gamesa, Vestas, and Ørsted, including financial struggles, layoffs, and plans to regain profitability. The episode also covers offshore wind manufacturing expansion in the U.S., a fallen wind turbine rotor in Norway, and the need for better data sharing among wind farm owners and operators. Plus, if you’re attending ACP O&M in San Diego, sign up for the IntelStor event!

Sign up now for Uptime Tech News, our weekly email update on all things wind technology. This episode is sponsored by Weather Guard Lightning Tech. Learn more about Weather Guard’s StrikeTape Wind Turbine LPS retrofit. Follow the show on Facebook, YouTube, Twitter, Linkedin and visit Weather Guard on the web. And subscribe to Rosemary Barnes’ YouTube channel here. Have a question we can answer on the show? Email us!

Pardalote Consulting – https://www.pardaloteconsulting.com

Weather Guard Lightning Tech – www.weatherguardwind.com

Intelstor – https://www.intelstor.com

Joel Saxum: So Allen is in Denmark at the Leading Edge Symposium DTU in Roskilde there with a lot of really smart people talking about leading edge erosion issues. What are the newest protections out there? What kind of projects going on in the world? From our side of view, how does aerodynamics leading edge roughness affect lightning?

A lot of really cool things going on there. Of course, DTU is always doing great work. But that’s where Allen is today. So this week I’m going to try to be my best Allen. I’m Joel Saxum, the chief commercial officer of Weather Guard Lightning Tech. And I’m here with international renewables expert, Rosemary Barnes.

Plus, wind energy economics and data guru Phil Totaro from IntelStor. This is the Uptime Wind Energy Podcast.

So speaking about offshore wind in the United States and how the IRA bill is interacting and if it’s kicking off manufacturing facilities or what’s actually happening on the ground, today there was an announcement by US Forged Rings Inc. It’d be the USA’s only integrated one stop shop manufacturer for offshore wind towers and steel forging.

What they released today in an article was, or in a press release was, the fact that they’re going to have two factories up and running on the east coast. One by 2026, one by 2027. And they’re going to work together. To build these large scale steel infrastructure that we need for offshore wind in the U.

S. So one of one of the factories is going to output towers. They’re saying a hundred towers per year with a 35 foot diameter on them and the other factory that’s going to be completing 2027. It’s for forging and ring rolling, and they can do up to 40 feet in diameter. So what this will do is be able to help the U.

S. market create its own transition pieces, its own, bearing races, its own caps for the towers and whatnot. But Phil, what are the larger reaching implications of this press release?

Philip Totaro: It’s extremely good for the offshore wind market where, a company is looking to obviously take advantage of the 45x manufacturing tax credits.

What’s interesting about this, though, is that in addition to this serving the offshore wind market, assuming that this factory exists, we don’t actually have a lot of particularly forging capabilities in the United States for anything above, let’s say, like a megawatt onshore turbine. We usually have to import a lot of that stuff from Europe.

Even Asia doesn’t have the, a full capability to do, enormous 6, onshore turbines. A lot of that they’re actually getting from Europe as well. Surprisingly, to, to most. The fact that this, these factories will exist, and, the tower factory with, it’s going to start off at 100 units a year and they said that it’s going to potentially expand to 200 units a year.

We’ll see. Maybe some of those units will actually be dedicated to to some onshore wind turbines as well. If we can get the offshore market really going, then they’ll be fully utilized in building offshore towers and transition pieces. But there is that possibility that we can leverage them for an expansion in the onshore market too.

Joel Saxum: Yeah, some interesting stuff here in their press release, they also are talking about being able to use some of the capabilities that they’ll have for offshore floating turbines, because if you have a spar design or other kind of designs, they need the large tubular pieces, right? This could enable the floating offshore wind in the US.

Of course, we’re looking at that on the West Coast. With the deeper water out there and there is some leases floating around out there on the east coast for further out past what we’ve been talking about lately into deeper water. Also with that forging and ring rolling factory on the other side you’re looking at yaw rings, pitch bearings, main shaft bearings and other large components.

The another thought I have here, Phil or Rosemary for that matter as well. Do you think that the capabilities of this factory could be used for other things than offshore wind, or will it be specifically just offshore wind? Could it be used for other large industrial facilities?

Philip Totaro: I don’t know enough about it to say what else this could be used for, and frankly, why, if we have oil and gas fabrication facilities, why they aren’t Doing something for offshore wind and we’re just like converting something that already exists for oil and gas Maybe they don’t need anything that big.

I don’t but we’ll make use of these factories I’m telling you like whether it’s offshore wind onshore wind, whatever. We’ll make use of these factories.

Joel Saxum: I think the difference there in oil and gas is when you have an oil and gas jacket or Other infrastructure. It’s so specialized That it’s a one off, right?

They’re not building a factory to make these things. They’re either ordering that one piece or that two pieces or whatever it is from somewhere that can already complete it, or they’re piecing them together. I’ve seen a lot of jacket foundations that are not rolled steel. They’re pieces. That are all welded together, right?

So they build a facility and do that custom fab. Not the case when you’re going to scale.

Rosemary Barnes: I think that the unique thing about this facility is the size, like the large diameters that they can do, which means I can do wind turbine towers. And not familiar with absolutely every single thing that’s made out of steel, but I don’t think that anything else needs those really large diameters.

Obviously if you’ve got a factory that’s big enough to make really big stuff, it could make smaller stuff if it wanted to, but yeah, that isn’t such a big challenge and there’d be other competitors that are already filling that need. So I’m guessing it’s going to be fairly specialized.

Philip Totaro: Yeah, the only thing I would think of might be pressure vessels for any various number of applications. The only thing is that’s also a specialized. Fabrication capability, so I’m not quite sure if they’d actually be able to, again I think these factories are intended to be offshore wind.

There is obviously a possibility, as I mentioned, of being able to leverage it for larger onshore wind machines as well either for domestic consumption or frankly, even an export market, because when you contemplate. We could be fabricating parts here in the U. S. for export to China, for instance.

That is a possibility. Or even, actually, Australia, because there’s a lot of projects in Australia that are proposing six and seven and eight megawatt turbines. Unless they’re gonna make it a point to, to build their own localized fabrication facilities. Who knows we could be we could be making some parts for them.

Rosemary Barnes: Yeah, I think I know that there’s plenty of people that have in mind that is a really good entry point into wind turbine manufacturing. It’s 1 of the easier things and. Australia already makes some towers some parts of towers at least. So it’s, not such a stretch that we would move up to that.

We do have a steel industry. It’s not what it used to be, we’ve got all the iron ore. There’s a lot of work now to move towards processing that into steel in Australia and then. Yeah, it’s already I’m not the only one that’s been saying for a decade or more how crazy it is that we take our iron ore, send that to China, they turn it into steel, and then, whatever else they make from the steel and then send that back to us.

It’s. It’s not good for Australia, keeping the real value from our minerals in Australia, the digging up of the mineral is, like the least valuable part of that whole process, values added all the way along through the manufacturing chain. And yeah, aside from it being economically stupid, it’s also environmentally stupid because, obviously if you send the unrefined steel over, if you’ve got like 50% concentrated iron ore, and when that comes back, you’ve got double the volume that you’ve got to send over there compared to what comes back.

So you can save a lot in shipping and. Yeah, so we are, we should have been doing it from the start, but I think, the whole world was really into globalization and just low costs at any non financial costs. We were prepared to, give up nearly anything if the cost of steel or whatever other material was lower and the whole world’s moving away from that now and slower than I would have liked, but Australia has all the pieces in place to.

Like a wind turbine tower should be the very easiest thing that we should definitely be manufacturing in Australia. And yeah, I am hopeful that we will within a few years.

Hey, Uptime listeners, we know how difficult it is to keep track of the wind industry. That’s why we read P. E. S. Wind magazine.

P. E. S. Wind doesn’t summarize the news. It digs into the tough issues. And P. E. S. Wind is written by the experts, so you can get the in depth info you need. Check out the wind industry’s leading trade publications. PESWIND at PESWIND. com

Joel Saxum: So news out of Denmark today, guys. Ørsted is suspending its dividend and cutting some jobs as it changes how it addresses offshore markets. So the wind developer says it needs to create a leaner and more efficient company. This is the words from Mads Nipper today. We’ve prioritized projects within our portfolio and are implementing significant changes in our business, including revising our operational model to reduce risks.

We now present a robust business plan with an uncompromising focus on value creation. Plan to install more than double our current installed capacity of renewable energy by 2030. The thing I like here that he said and I haven’t dug completely into it yet is that we are presenting a robust business plan.

This is something that we haven’t heard of some other players in the wind industry. I. e. Siemens, Gamesa, and whatever that they’re doing, what is their plan? Ørsted has one now. Phil, what does this mean for Ørsted going forward?

Philip Totaro: As they indicated, they’re getting rid of some of the fluff, let’s call it.

Which is going to include some of the Power to X projects that they had on the menu. Some of the hydrogen production, et cetera, et cetera, and focusing on core business, focusing also on core markets. And on. Doubling down in their their view on, offshore wind again, core European markets but also Taiwan and they’re obviously going to continue what they’ve been trying to do in the U.

S. South Fork is still, on on track for coming online this year. And we’ll see what happens with some of the other projects that they’re still pursuing and involved with. They may end up still divesting some of the the projects here in the U. S. Eversource also wants out if both project developers are looking to get out, then that’s potentially an opportunity for someone else to get in.

I think again, as we’ve talked about, it is a good thing that they present a a business plan that provides investors and shareholders more confidence, because that’s the key as far as what was lacking, and it’s we do liken it to other companies like Siemens Gamesa, Ørsted just came out a few months ago and said we have a problem.

But they didn’t really say we have a solution, too, and here’s what it is. It’s just, All they did was diagnose the fact that they have issues. And now they’ve at least put pen to paper and said, Alright, we, here’s how we’re gonna dig ourselves out of the hole. It’s unfortunate that not only the 800 jobs that they’re going to be cutting, but their long time chairman also stepped down as a result.

And, as we’ve also talked about, one would presume that Mad Snipper’s job also isn’t safe, but they’re at least leaving him in his current position until this can, this kind of transition can occur, and then they’ll find someone else to champion the new era of Ørsted.

Joel Saxum: Yeah, interesting here.

They’re the market that some of their plan. Okay. Phil, you mentioned it. They’re cut 800 jobs. They have about 9, 000 people globally. So that means that just under 10 percent of their staff is looking for pink slips. That’s not the best way to be, but. It’s reality. And the markets that they’re going to withdraw from our Norway, Spain and Portugal.

Now, Norway, Spain and Portugal for the most, a lot of that is floating to my knowledge. They’re not as advanced as the projects that they operate right now in the North Sea. But it is interesting as well. The with the chairman stepping down. So Thomas Tuna Anderson has been there for 10 years.

He’s exiting that role. And also we had, this past fall, Daniel Lerup, the chief operating officer. Or the finance chief and then Richard Hunter, the chief operating officer left as well. So there has been, we have talked about how long will Mads Nipper keep his job. But there has been a lot of changes from the board of directors all the way down.

And we’re all hopeful that Ørsted comes out of this thing. A shinier new product because them being healthy is good for the offshore wind energy market as a whole Rosemary, any thoughts on this Ørsted move and them pulling back a little bit, what it means for their future.

Rosemary Barnes: Yeah I think that they had the right idea with their strategy to, get in early with the U S market. A lot of people had that idea and I think that’s why we saw such a, like a feeding frenzy for some of those early auctions. Everybody wanted in, and they got in, but I don’t think people anticipated how I don’t know, wishy washy, is that the right term? The environment in the U. S. was?

Philip Totaro: Yes. Yes, it is.

Joel Saxum: Yeah, it’s perfect.

Rosemary Barnes: Yeah, I think it’s a huge cultural difference between Denmark and the U. S. And I’ve lived in both countries, the U. S. just for one year back in. 20 years ago. So it’s been a while. But Denmark is characterized by just that they’ve got immense trust in, other people and in governments.

I think that they’re like the most trusting country in the world, or at least one of them. Which I think that they might as a, Danish company culturally. They might have been surprised that when you enter into agreements with governments that things don’t, there isn’t a lot of trust going back the other way, so I think that they might’ve been surprised by that relationship and so that the cultural clash might’ve been more than what they’re expecting. But I do still think that it’s the right move, but just that it was too soon. The U. S. isn’t actually ready for all of these European companies to come in and ramp up offshore wind really fast in the U.

S. We all wish that it was true and I wouldn’t have predicted these problems a couple of years ago, but here we are. But that said, I do like the company. It’s just such a great story of a company that went from being an oil and gas company that was literally in their name and now they’re a renewable energy company.

I don’t know if there’s any others in the world that have actually managed to do that. Like I am rooting for them, for the company. I actually, I have a note I sent a reminder in my calendar to buy some Austered stocks once this kind of settled down because it fell so far. And I don’t really believe that there’s anything wrong, anything much has changed with the fundamentals of the company.

I still haven’t done that yet. And just mostly out of forgetfulness, but it’s nice to say that they feel a little bit more because now I can get an extra couple of percent. Since they’re lower don’t take that as stock advice. If you looked at the, returns that I make in my portfolio, then you would certainly not come to me for stock advice.

But yeah, the size of the layoffs was interesting. What is it like nearly 10 percent of their workforce. And I will say. Denmark is brutal, absolutely brutal for stuff like that. People might have the wrong idea that, Denmark is Scandinavia, everybody’s warm and fuzzy. And you might have heard like Swedish people tell you how it’s impossible to fire anyone as culturally similar as Denmark is to Sweden.

It is just absolutely not like that in the workforce. They they call their system. Flex security, I think, like flexible security. The flexibility is just the ability to ruthlessly just slash their workforce by 10 percent for, they don’t have to give that much of a reason or be that generous even in their payout to the staff that they let go of.

But the security is that for Danish people, it’s quite it’s quite secure in the amount of unemployment money that you’ll get for quite a long time while you’re looking for work, as long as you I can’t remember the exact setup. I think you have to be a member of a union or something similar to it, some kind of insurance to get that.

But I will say as a foreigner it’s, there’s no, no security for you there as a foreigner. So all the foreigners that the international workers that got laid off, that’s yeah, that is just as brutal as it sounds. So yeah it, it’s good for the company though, that they can make a big change when they need to better that than that they, limp along for the next decade, trying to scrimp and scrape enough to recover, this way, hopefully they can.

Get it all done in one go and then move forward with the stuff that’s going to be profitable in the near term and have the strength there to get back into the U. S. When the country is ready for it.

Joel Saxum: Rosemary, I don’t want to make you feel bad about your delay in the stock price, but back in the fall, not too long ago, a couple, two, three months ago, when they initially, Hey, we announced these write downs and stuff, their stock dropped to about.

11 and 80 cents us. And it’s already back up to 18.

Rosemary Barnes: There you go. So this is why you shouldn’t trust me for investment advice. I’ve missed the boat. I’m also, I’m very, I’m lazy as well with my investing. I. I do it when it occurs to me. And yeah, I’m definitely not someone that’s looking up stock prices every day and making a lot of trades.

I buy something and then I hold it for, as long as I can.

Joel Saxum: So guys sticking in the financial realm of things, you’re gonna talk about Vestas for a little bit. So Vestas’ return to profitability, however, not going to give a dividend either. And for good reason, their dividend would have been minuscule based on what their profitability was, but they are back in black and their discipline is paying off is what they’re stating in their report for the year.

So I’ll give you some numbers here. They made a full year operating profit before special items of 231 million euros. Compared to a loss of 1. 2 billion euros the year before, so that’s a big turnaround. They adjusted the operating profit in fourth quarter, was 191 million euros versus a loss of 514 million euros the year before.

So they’re beating analysts, they’re doing a bit better. The guidance that they’ve given, Investors forecast revenue this year of 16 to 18 billion euros. And the analysts are looking at 17. So they’re right in that same window with what the, they believe will be. So Henrik Andersen, the CEO has stated continued geopolitical volatility, as well as slow permitting and insufficient grid build out across markets are expected to cause.

Uncertainty in 2024. So Vestas is getting back to better health. This is something that we’ve talked about for the last few years was going to take a little while to happen, but it’s great. However, this is the angle I would like to talk at this one with you guys about, do you believe that some of the downfall of what Siemens has going on and them stopping selling their certain platforms right now in the market has led to an increase in Vestas?

Philip Totaro: Modestly, I’ll say, Joel a lot of this getting the Vestas getting back to profitability has more to do with a recovery in turbine prices, because, as you may recall in prior years, even Vestas came out and said that the average price they were seeing. For turbines was about 700, 000 U.

S. per megawatt. And that’s taking into account, markets where you’re selling turbines for a million a megawatt, but also markets where you’re selling for 600, And so now the average price, according to our own numbers at Intel Store, we’re seeing much higher turbine sale prices for projects that were closed last year, including, a lot of the 18 gigawatts order book that they announced last year.

But they’re quoting much higher now they’re around 900, 000 a megawatt megawatt, if not a little higher now in terms of the price quotes that they’re offering at this point for projects which presumably would be delivered to in the next two to, to three years.

Yes, the downfall of Siemens Gamesa has allowed Vestas to go gain some market share in markets where, they would have been competing with megawatt platform. The only reason I guess I’m hesitating on it is because I feel like, Vestas would have already been leading that.

Those markets anyway because while everybody still thinks that Siemens Gamesa makes a solid product even prior to the quality issues it just wasn’t always the favored turban and I don’t know if that comes down to perception of performance, perception of bankability. The service offerings that, or the quality of the service offering that’s received by an asset owner and operator.

Yeah, there’s there, again good news for Vestas in terms of getting back to profitability. It seems like most of the cost increase that they’ve been able to incur. Or that they’ve had to incur as a result of commodities and raw material costs going up has been passed on to customers i.

e. project developers. That’s good. But again, even with them not issuing a dividend, I think it’s fine from the standpoint of the shareholders in the company who will anticipate getting back to a higher dividend once that. Can presumably occur later on this year.

Lightning is an act of God, but lightning damage is not. Actually, it’s very predictable and very preventable. StrikeTape is a lightning protection system upgrade for wind turbines made by WeatherGuard. It dramatically improves the effectiveness of the factory LPS, so you can stop worrying about lightning damage.

Visit weatherguardwind. com to learn more, read a case study, and schedule a call today.

Joel Saxum: So guys, Siemens Gamesa staff in Aruzury, Navarra will go on strike. We’ve been talking about them possibly going on strike in Spain there for a while. And it sounds like one of the factories has actually pulled the trigger and made it happen.

So what they’re saying is Aruzury is the only center in Navarra that has not adhered to the corporate office agreement with Siemens Gamesa. which is a clear discrimination. It looks like it’s going to affect 62 workers at the plant that they’re going to basically shut it down. So what are the ramifications for this in a plant like that, Rosemary?

Rosemary Barnes: It’s It’s an interruption.

Philip Totaro: This is the sort of thing that, they’ll do this occasionally, Vestas has suffered from temporary factory shutdowns in Spain. GE even had protests, going back a few years, LM factories in Spain as well in the past.

It’s usually like a very modest and temporary interruption. It’s not anything that’s gonna like dramatically impact production per se. But it’s one of those things that it’s, this is like the fourth different location since, Siemens has announced that they’ve had these product quality issues.

This is like the fourth location that said that they’re gonna go on strike and so it’s just culturally, I think they’re just facing a challenge there to provide reassurance, not only to investors and shareholders, but to their own staff to say, look, we’ve got a plan for getting ourselves out of this.

But we all need to pull together to be able to do that. And, obviously these 62 people feel like they’re not being treated equitably.

Joel Saxum: And that so that plan, like we’re saying, Ørsted came out with the, Hey, here’s our plan. Siemens Gamesa has a plan, they’re calling it the Mistral.

Plan to address some of these issues within the inside there. So their, they’ve actually came out now it’s quarterly earnings time, right? We’ve been talking a little stock market, a little finances here. So Siemens energy different, of course, than Siemens Gamesa right now dragging Siemens energy down on their quarterly reports a bit.

It looks if you were to take the quick numbers from Siemens energy. The revenues to 2 billion euros for this past fiscal year but that comes with a loss of or a reported EBITDA, which is basically your loss after everything else you pull out of it, of a negative 900 million.

So pretty tough times to be in the Siemens Comesa finance department. But what is, how does that overall feel affect with Siemens, that if, when you take into consideration Siemens Energy as the parent and Siemens Gamesa looking like this, are they going to have to make some big moves to save this thing financially, Phil?

Philip Totaro: There’s still struggling with a couple of different things at the moment. It sounds like they obviously have their head around what the quality issues are. They haven’t quite effectively communicated that to investors and shareholders because they’re still clamoring for what exactly is the full extent of this?

And management came out even today when they released their numbers. And said, we aren’t expecting anything worse than what we’ve already told you to paraphrase which I guess is good from one perspective, but it’s also unsettling because, people want to either have confidence that you’ve, tied this off and we can move on, or, and get back to selling or it’s something where, oh we were, grossly or disproportionately over predicting what we were going to spend, the 5 billion loss that, that we were going to have, it’s actually not going to be 5 billion.

It’s only going to be 3 or whatever, and it’s oh, my God, that’s great to an extra 2 billion that, that we don’t have to waste on losses. That’s the sort of thing that investors shareholders want to see. And here And they’re still not seeing and hearing that from Siemens Gamesa management and that’s where I think we still have a problem here, they keep trying to provide assurances about the quality issues are, understood and are being dealt with, but again, even from that perspective, I think since the start of this whole thing, Siemens Gamesa has just had A bit of a PR issue with this whole thing.

It’s in, in corporate management, like if you have an, everybody’s going to go through either a product quality issue or some kind of. Business downturn, whatever. But it’s usually, okay, we can see this coming, we have a plan for dealing with it we know, what needs to ha and my point is that before you go out and say anything in public, you’ve dealt with everything that you can possibly deal with internally.

You can’t obviously withhold information, business critical information from shareholders, but you also want to be able to have your arms around what’s happening. And I think in their desire for transparency, and not wanting to be accused of hiding anything, they went forward with, publicly, with a lot of hey, we’ve got an issue here, but there was no road map for okay.

How do you deal with that issue? And then what’s the business strategy moving forward? They’ve just come out and you know been very transparent with the fact that they have an issue and we’re sitting here nine months later You know going on 10 or 11, and it’s you know, we’re still Scratching our heads trying to understand.

Okay, what exactly you know, when can you start selling again? When are you gonna start making money again? There’s it’s You know the things that they’ve said in the past are just unfortunately not convincing. And they’re talking about, oh, we’re going to be back in profitability by 2026.

Not if you’re not selling in 2024. So you best get on top of it. If you’re not already.

Joel Saxum: Yeah, that’s the interesting one, right? Chief executive officer, Christian brush come out. He says we’re going to stick to this prediction that we’re going to break even in 2026. With some of these fixes that we need to do the big spend probably being in 2025.

Which is, it’s such a general vague statement that it, that can’t give anybody a warm fuzzy, but how, however the early shares trading that rose 2. 8% and that adds to 20 percent gains so far this year after they slumped off about 30 percent in value. At the end of last year. So for the, I don’t know, the general investor that’s, they’re still feeling like it’s going to be okay is what it looks like, but I don’t know if from some looking at it as we do from the inside of the industry it’s still on thin ice.

Okay. So shifting gears. Now we’ve been talking about finance for a little bit. We’re going to talk back to O and M and what’s actually going on in the field. So up in Norway, a rotor fell off. Of a Nordic N 1 49 turbine. So this was in, I’m gonna say this wrong, of course, wind Park in Norway. They had an issue with one of the turbines back from the summer back in June.

And since then they corded off the area. They made sure nobody would go in there. They did everything safe there. But as a part of the repair process, they removed the gearbox. So they took some major components out of the inside of the nelle there. And it said, along with the company’s statement says this, along with other special circumstances surrounding the damage and repair work has led to an unusual risk that the rotor falling could, or the rotor falling, failing could fall off the turbine.

And on January 27th, the rotor became loose and fell off the turbine. So the interesting thing here for me is that they knew it could be an issue. They knew it could come off. There did they did some risk analysis and stuff on it, but they didn’t actually do anything about it to remove a major component.

Usually you have to have the gearbox or the gearbox. You have to have a crane there. You also have to have. Or a smaller crane system mobilized to site to even get this thing down. So there had to be something really weird going on with this turbine that they left it in a precarious position without actually just saying, hey, the crane’s here, let’s take the rotor off as well.

What do you heard anything else about this, Phil?

Philip Totaro: It’s a little bit of a strange one because it sounds like they, they needed to reinstall some tooling or other components that was gonna hold everything together, and mitigate some of that risk. But they just didn’t have some of that tooling available, is what they’re saying.

That’s unfortunate because, from that perspective, it’s going to be hard for them to make any kind of a claim, like an insurance claim or whatever, because this sounds like it was entirely the either on the OEM or EPC contractor to not follow a proper procedure, but it’s also a bit distressing because this product platform has had some Teething issues around the world like that.

They also had a rotor issue down in Australia the same model at the more like South wind farm recently. There’s also been a recent report of an issue in for a wind farm in Chile with the same same model, make and model of turbine. And it’s. Maybe this is one of those scenarios where it might be like a Nordex procedure that needs to be re evaluated.

Again, you never want to see a situation like this, but clearly something needs to be done if it’s, not just an isolated incident.

Joel Saxum: Yeah, the interesting, Nordex says They came out right away. This is an isolated incident. There’s no other risk to any other turbines on that wind farm or in the wider fleet.

No worries. And then the asset owner’s yeah, we’re going to do an RCA and figure this out. So there could be some more news that comes out of this rotor falling off of the turbine up in Norway.

Philip Totaro: And it’s also another reason why you need to have asset owners talking to each other and providing information exchange, which is obviously something that we’re trying to do with the.

The data licensing that we’re doing is trying to, shine a light on the fact that there are other asset owners that own the same product that you do, and potentially, they’re, they could also be experiencing issues or potentially operating their asset with the same make and model of product in a better way.

And so that’s the sort of thing that needs to happen within the industry is asset owners have to, and operators have to get. A little more comfortable kind of talking to each other and potentially sharing best practices and information so that things like this don’t reoccur. Because again, Nordex may come out and say, trying to reassure everybody, oh, it’s an isolated incident, but it hasn’t, when you do the root cause, I’m sure it’s going to be You know, something that was specifically different than the issue that they had in, in Australia, more like South or in Chile, as you mentioned, but it’s still, it seeing repeated issues on the same make and model of product.

is never really a good thing. So again, I think from a holistic standpoint, it might need to be a internal investigation into procedures that might need to occur here.

Joel Saxum: Yeah. Phil, we talk about this quite often. The OEMs don’t want to share that much data, which is, trade secrets and whatnot, but the operators can.

Some of them are covered under some contractual agreements to basically NDAs and those kinds of nasty little pieces of paper that can slow industries down. But there is a few working groups. I know there’s a Scandinavian working group that gets together and they talk about, with all the owners and they talk about things.

There is a blades one. I think that’s headed up by some people from Bladina and Burgett Junker that was with RWE. They talk about some blade issues to get together as a little conference. One of the ones I was at a few years ago, the last time they had it in person was the Sandia blade conference.

And there was quite a bit of. Good conversation there about best practices and what’s going on different kind of things. Not at the granular level, right? Not at the, hey, we have this platform with this blade and this and this. It was more like, hey, guys, let’s get together. What are some general things?

That Sandia is going to happen again this year. We saw that and they announced that down in Albuquerque. If you’re into, if you’re into blades and you want to know what’s going on in the. The US wind industry from an academic standpoint, but with a lot of great operators there and engineers, that’s a good conference to go to.

I think last year, last time they had it in person, there was probably 250 to 300 people there. And it was a couple of different tracks all about technical issues. So that one was good. We could see some of these things raised at that conference, but yes fully agree with you, Phil. It would be nice if we had yeah.

I don’t know what we would call it. The wind book, the Facebook of wind, and just everybody could be on there and share all the issues with certain things and maybe a nice forum there. I don’t know. And maybe it’s an IntelStor spinoff. Maybe we’re working on it. So that’s going to be it for the uptime wind energy podcast this week.

If you’re a frequent listener to the podcast, please take a moment and give us a five serving on your podcast platform and subscribe to our weekly newsletter, uptime tech news. And this was a big one. Don’t forget this. If you’re going to be at OMS ACP OMS in San Diego, IntelStor is putting on a perfect little event on Thursday night.

So go to their website or go to their LinkedIn, find the link for that, sign up. It’s going to be free to attend. A lot of good information there. Make sure you hit up that.

Siemens Gamesa, Vestas, Ørsted Updates: Finances, Fallen Rotors, and Offshore Wind Outlook

Can’t swear that this is true but hoping so.

Can’t swear that this is true but hoping so.

We must never forget.

The more visibility and the more frequent reminders we can get on this catastrophe in U.S. history the better.

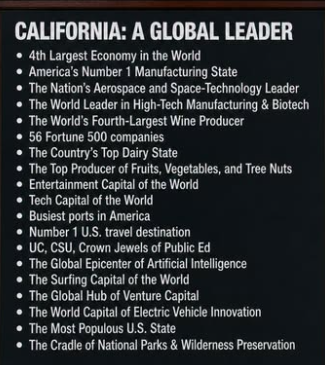

It’s almost funny when we hear that California is a socialist state, or a police state (due to our environmental restrictions), or that people are leaving in droves to go to Texas or Florida. When I come across people who say this, I wonder: have you ever actually been to California?

It’s almost funny when we hear that California is a socialist state, or a police state (due to our environmental restrictions), or that people are leaving in droves to go to Texas or Florida. When I come across people who say this, I wonder: have you ever actually been to California?

Do you know that the garden-variety 3 BR, 2 BA house here lists at about $1.2 million, where, if it were moved to, say, the Midwest, it would be worth perhaps $2500,000? Why do you think that could possibly be? Maybe the law of supply and demand doesn’t apply to the Marxist part of the nation?

Perhaps it’s because Californians are offered fantastic economic opportunities. We develop and implement ideas that improve the lives of everyone on Earth, and that we profit greatly from our undertakings.

Something for the MAGA crowd to consider.

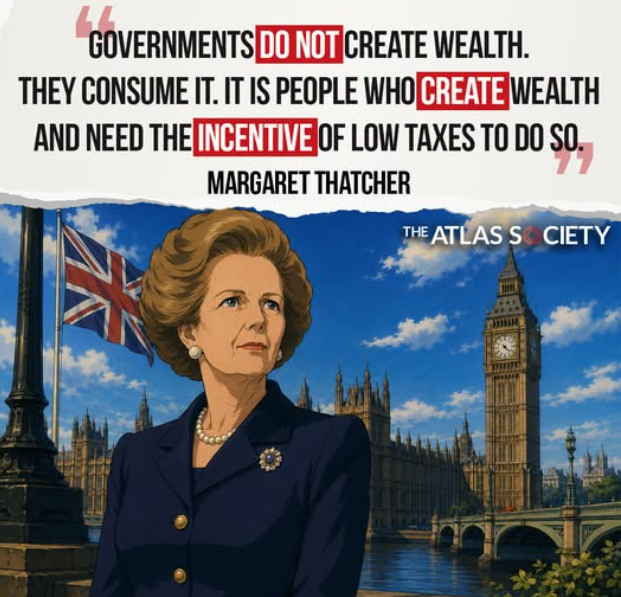

The main way governments create wealth is by educating people so that they can become productive members of society. They also build roads and airports and maintain law and order so that honest businesses can thrive.

The main way governments create wealth is by educating people so that they can become productive members of society. They also build roads and airports and maintain law and order so that honest businesses can thrive.

Anyone living now who believes that Elon Musk and Jeff Bezos are creating wealth for anyone but themselves is a total fool.

A ton of people bought into the concept expressed here in the mid-20th Century, but no semi-intelligent person today believes that tax breaks for billionaires/trillionaires generates a nickel for the common person.

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测