The world’s fossil-fuel use is still on track to peak before 2030, despite a surge in political support for coal, oil and gas, according to data from the International Energy Agency (IEA).

The IEA’s latest World Energy Outlook 2025, published during the opening days of the COP30 climate summit in Brazil, shows coal at or close to a peak, with oil set to follow around 2030 and gas by 2035, based on the stated policy intentions of the world’s governments.

Under the same assumptions, the IEA says that clean-energy use will surge, as nuclear power rises 39% by 2035, solar by 344% and wind by 178%.

Still, the outlook has some notable shifts since last year, with coal use revised up by around 6% in the near term, oil seeing a shallower post-peak decline and gas plateauing at higher levels.

This means that the IEA expects global warming to reach 2.5C this century if “stated policies” are implemented as planned, up marginally from 2.4C in last year’s outlook.

In addition, after pressure from the Trump administration in the US, the IEA has resurrected its “current policies scenario”, which – effectively – assumes that governments around the world abandon their stated intentions and only policies already set in legislation are continued.

If this were to happen, the IEA warns, global warming would reach 2.9C by 2100, as oil and gas demand would continue to rise and the decline in coal use would proceed at a slower rate.

This year’s outlook also includes a pathway that limits warming to 1.5C in 2100, but says that this would only be possible after a period of “overshoot”, where temperature rise peaks at 1.65C.

The IEA will publish its “announced pledges scenario” at a later date, to illustrate the impact of new national climate pledges being implemented on time and in full.

(See Carbon Brief’s coverage of previous IEA world energy outlooks from 2024, 2023, 2022, 2021, 2020, 2019, 2018, 2017, 2016 and 2015.)

World energy outlook

The IEA’s annual World Energy Outlook (WEO) is published every autumn. It is regarded as one of the most influential annual contributions to the understanding of energy and emissions trends.

The outlook explores a range of scenarios, representing different possible futures for the global energy system. These are developed using the IEA’s “global energy and climate model”.

The latest report stresses that “none of [these scenarios] should be regarded as a forecast”.

However, this year’s outlook marks a major shift in emphasis between the scenarios – and it reintroduces a pathway where oil and gas demand continues to rise for many decades.

This pathway is named the “current policies scenario” (CPS), which assumes that governments abandon their planned policies, leaving only those that are already set in legislation.

If the world followed this path, then global temperatures would reach 2.9C above pre-industrial levels by 2100 and would be “set to keep rising from there”, the IEA says.

The CPS was part of the annual outlook until 2020, when the IEA said that it was “difficult to imagine” such a pathway “prevailing in today’s circumstances”.

It has been resurrected following heavy pressure from the US, which is a major funder of the IEA that accounts for 14% of the agency’s budget.

For example, in July Politico reported “a ratcheted-up US pressure campaign” and “months of public frustrations with the IEA from top Trump administration officials”. It noted:

“Some Republicans say the IEA has discouraged investment in fossil fuels by publishing analyses that show near-term peaks in global demand for oil and gas.”

The CPS is the first scenario to be discussed in detail in the report, appearing in chapter three. The CPS similarly appears first in Annex A, the data tables for the report.

The second scenario is the “stated policies scenario” (STEPS), featured in chapter four of this year’s outlook. Here, the outlook also includes policies that governments say they intend to bring forward and that the IEA judges as likely to be implemented in practice.

In this world, global warming would reach 2.5C by 2100 – up marginally from the 2.4C expected in the 2024 edition of the outlook.

Beyond the STEPS and the CPS, the outlook includes two further scenarios.

One is the “net-zero emissions by 2050” (NZE) scenario, which illustrates how the world’s energy system would need to change in order to limit warming in 2100 to 1.5C.

The NZE was first floated in the 2020 edition of the report and was then formally featured in 2021.

The report notes that, unlike in previous editions, this scenario would see warming peak at more than 1.6C above pre-industrial temperatures, before returning to 1.5C by the end of the century.

This means it would include a high level of temporary “overshoot” of the 1.5C target. The IEA explains that this results from the “reality of persistently high emissions in recent years”. It adds:

“In addition to very rapid progress with the transformation of the energy sector, bringing the temperature rise back down below 1.5C by 2100 also requires widespread deployment of CO2 removal technologies that are currently unproven at large scale.”

Finally, the outlook includes a new scenario where everyone in the world is able to gain access to electricity by 2035 and to clean cooking by 2040, named “ACCESS”.

While the STEPS appears second in the running order of the report, it is mentioned slightly more frequently than the CPS, as shown in the figure below. The CPS is a close second, however, whereas the IEA’s 1.5C pathway (NZE) receives a declining level of attention.

US critics of the IEA have presented its stated policies scenario as “disconnected from reality”, in contrast to what they describe as the “likely scenario” of “business as usual”.

Yet the current policies scenario is far from a “business-as-usual” pathway. The IEA says this explicitly in an article published ahead of the outlook:

“The CPS might seem like a ‘business-as-usual’ scenario, but this terminology can be misleading in an energy system where new technologies are already being deployed at scale, underpinned by robust economics and mature, existing policy frameworks. In these areas, ‘business as usual’ would imply continuing the current process of change and, in some cases, accelerating it.”

In order to create the current policies scenario, where oil and gas use continues to surge into the future, the IEA therefore has to make more pessimistic assumptions about barriers to the uptake of new technologies and about the willingness of governments to row back on their plans. It says:

“The CPS…builds on a narrow reading of today’s policy settings…assuming no change, even where governments have indicated their intention to do so.”

This is not a scenario of “business as usual”. Instead, it is a scenario where countries around the world follow US president Donald Trump in dismantling their plans to shift away from fossil fuels.

More specifically, the current policies scenario assumes that countries around the world renege on their policy commitments and fail to honour their climate pledges.

For example, it assumes that Japan and South Korea fail to implement their latest national electricity plans, that China fails to continue its power-market reforms and abandons its provincial targets for clean power, that EU countries fail to meet their coal phase-out pledges and that US states such as California fail to extend their clean-energy targets.

Similarly, it assumes that Brazil, Turkey and India fail to implement their greenhouse gas emissions trading schemes (ETS) as planned and that China fails to expand its ETS to other industries.

The scenario also assumes that the EU, China, India, Australia, Japan and many others fail to extend or continue strengthening regulations on the energy efficiency of buildings and appliances, as well as those relating to the fuel-economy standards for new vehicles.

In contrast to the portrayal of the stated policies scenario as blindly assuming that all pledges will be met, the IEA notes that it does not give a free pass to aspirational targets. It says:

“[T]argets are not automatically assumed to be met; the prospects and timing for their realisation are subject to an assessment of relevant market, infrastructure and financial constraints…[L]ike the CPS, the STEPS does not assume that aspirational goals, such as those included in the Paris Agreement, are achieved.”

Only in the “announced pledges scenario” (APS) does the IEA assume that countries meet all of their climate pledges on time and full – regardless of how credible they are.

The APS does not appear in this year’s report, presumably because many countries missed the deadlines to publish new climate pledges ahead of COP30.

The IEA says it will publish its APS, assessing the impact of the new pledges, “once there is a more complete picture of these commitments”.

Fossil-fuel peak

In recent years, there has been a significant shift in the IEA’s outlook for fossil fuels under the stated policies scenario, which it has described as “a mirror to the plans of today’s policymakers”.

In 2020, the agency said that prevailing policy conditions pointed towards a “structural” decline in global coal demand, but that it was too soon to declare a peak in oil or gas demand.

By 2021, it said global fossil-fuel use could peak as soon as 2025, but only if all countries got on track to meet their climate goals. Under stated policies, it expected fossil-fuel use to hit a plateau from the late 2020s onwards, declining only marginally by 2050.

There was a dramatic change in 2022, when it said that Russia’s invasion of Ukraine and the resulting global energy crisis had “turbo-charged” the shift away from fossil fuels.

As a result, it said at the time that it expected a peak in demand for each of the fossil fuels. Coal “within a few years”, oil “in the mid-2030s” and gas ”by the end of the decade”.

This outlook sharpened further in 2023 and, by 2024, it was saying that each of the fossil fuels would see a peak in global demand before 2030.

This year’s report notes that “some formal country-level [climate] commitments have waned”, pointing to the withdrawal of the US from the Paris Agreement.

The report says the “new direction” in the US is among “major new policies” in 48 countries. The other changes it lists include Brazil’s “energy transition acceleration programme”, Japan’s new plan for 2040 and the EU’s recently adopted 2040 climate target.

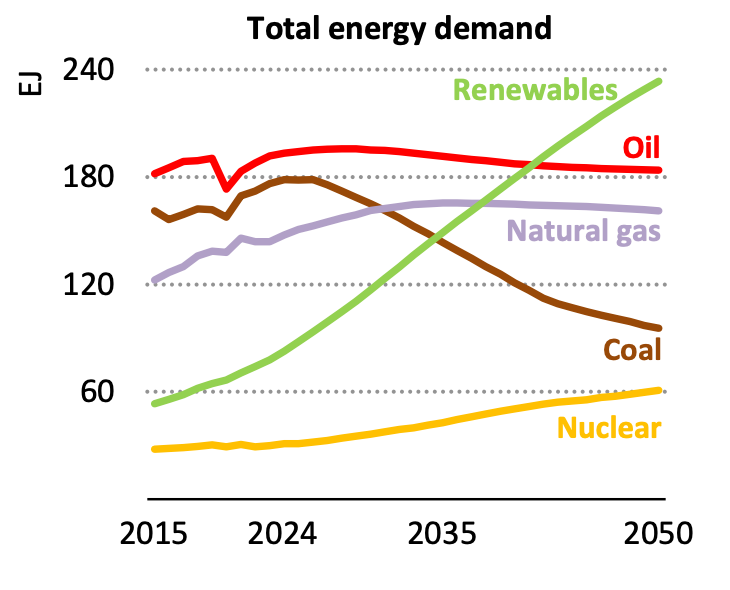

Overall, the IEA data still points to peaks in demand for coal, oil and gas under the stated policies scenario, as shown in the figure below.

Alongside this there is a surge in clean technologies, with renewables overtaking oil to become the world’s largest source of energy – not just electricity – by the early 2040s.

In this year’s outlook under stated policies, the IEA sees global coal demand as already being at – or very close to – a definitive peak, as the chart above shows.

Coal then enters a structural decline, where demand for the fuel is displaced by cheaper alternatives, particularly renewable sources of electricity.

The IEA reiterates that the cost of solar, wind and batteries has respectively fallen by 90%, 70% and 90% since 2010, with further declines of 10-40% expected by 2035.

(The report notes that household energy spending would be lower under the more ambitious NZE scenario than under stated policies, despite the need for greater investment.)

However, this year’s outlook has coal use in 2030 coming in some 6% higher than expected last year, although it ultimately declines to similar levels by 2050.

For oil, the agency’s data still points to a peak in demand this decade, as electric vehicles (EVs) and more efficient combustion engines erode the need for the fuel in road transport.

While this sees oil demand in 2030 reaching similar levels to what the IEA expected last year, the post-peak decline is slightly less marked in the latest outlook, ending some 5% higher in 2050.

The biggest shift compared with last year is for gas, where the IEA suggests that global demand will keep rising until 2035, rather than peaking by 2030.

Still, the outlook has gas demand in 2030 being only 7% higher than expected last year. It notes:

“Long-term natural gas demand growth is kept lower than in recent decades by the expanding deployment of renewables, efficiency gains and electrification of end-uses.”

In terms of clean energy, the outlook sees nuclear power output growing to 39% above 2024 levels by 2035 and doubling by 2050. Solar grows nearly four-fold by 2035 and nearly nine-fold by 2050, while wind power nearly triples and quadruples over the same periods.

Notably, the IEA sees strong growth of clean-energy technologies, even in the current policies scenario. Here, renewables would still become the world’s largest energy source before 2050.

This is despite the severe headwinds assumed in this scenario, including EVs never increasing from their current low share of sales in India or the US.

The CPS would see oil and gas use continuing to rise, with demand for oil reaching 11% above current levels by 2050 and gas climbing 31%, even as renewables nearly triple.

This means that coal use would still decline, falling to a fifth below current levels by 2050.

Finally, while the IEA considers the prospect of global coal demand continuing to rise rather than falling as expected, it gives this idea short shrift. It explains:

“A growth story for coal over the coming decades cannot entirely be ruled out but it would fly in the face of two crucial structural trends witnessed in recent years: the rise of renewable sources of power generation, and the shift in China away from an especially coal-intensive model of growth and infrastructure development. As such, sustained growth for coal demand appears highly unlikely.”

The post IEA: Fossil-fuel use will peak before 2030 – unless ‘stated policies’ are abandoned appeared first on Carbon Brief.

IEA: Fossil-fuel use will peak before 2030 – unless ‘stated policies’ are abandoned

Climate Change

“Next year is too late for regulations”: Beetaloo Energy’s 2GW gas-powered AI data centre a “disaster proposal” destined to cause climate chaos

SYDNEY, Wednesday 22 July 2026 — Beetaloo Energy has secured land from the NT Government for a massive $40 billion “hyperscale” AI data centre near Darwin, which would be powered by 2 gigawatts (GW) of gas power fracked directly from the Beetaloo basin, prompting calls from Greenpeace for urgent federal legislation.

The proposal marks a dangerous escalation in the AI data centre industry’s expansion, which threatens to entrench fossil fuel infrastructure for decades and put immense pressure on the region’s fragile water resources — while continuing to be unregulated.

Joe Rafalowicz, Head of Climate and Energy at Greenpeace Australia Pacific, said: “This disaster proposal for a 2GW gas-powered AI data centre in the NT is a shocking example of the unchecked expansion of hyperscale data centres in Australia. It is also, critically, more evidence for the urgent need for a moratorium on all new data centres until strong, binding regulations are put in place to protect our communities and climate.

“This proposal mirrors the frenzied, unchecked expansion currently wreaking havoc on communities in the US. We are seeing cowboy data centre operators treat Australia like a playground, steam-rolling ahead with projects that would lock down precious water resources and spike emissions, despite the overwhelming community opposition.

“Every day, more councils, communities and environmental groups are joining Greenpeace’s call for a moratorium on data centres, yet as of today there is still no system of safeguards or rules in place to regulate these companies.

“While Beetaloo Energy and the NT Government prepare to bulldoze ahead with this climate and water disaster, the Prime Minister is asleep at the wheel, promising to legislate a vague set of standards next year.

“Next year is too late, and anything less than mandating data centres cover their own energy demand, and then some, with new renewable energy is not enough.”

-ENDS-

Media contact

Lucy Keller on 0491 135 308 or lucy.keller@greenpeace.org

Reports of human rights and environmental abuses linked to Chinese companies’ overseas investments in the mining and refining of minerals needed for the clean energy transition are on the rise, research by a monitoring group has found.

The number of recorded allegations of harm at projects tied to Chinese firms have increased every year since 2021, rising to 148 in 2025, according to the Business and Human Rights Centre (BHRC). On Wednesday it released new data showing that a total of 434 allegations of abuse were made against Chinese-backed projects over the five-year period in projects across the world.

The world’s top cleantech manufacturer, China is also the leading financier of critical minerals projects worldwide. The country has committed more than $120 billion in foreign direct investment into mineral mining and processing since 2023, Australian think-tank Climate Energy Finance recently found.

“China plays a central role in global transition mineral supply chains, and as such has a unique opportunity to raise the bar on human rights and community engagement at every stage of mining,” said Michael Clements, BHRC’s executive director.

“While there have been encouraging developments, from stronger regulations to more company engagement, there remains a gap between human rights commitment and action,” he said.

The report comes as communities affected by Chinese-backed mineral projects have filed the first two cases to a Beijing-based mediation mechanism intended to bring willing Chinese companies to the discussion table with affected communities.

Allegations of harms on the rise

BHRC’s latest analysis – including data for the period 2023-2025 – covered mining, smelting and refining projects for 11 minerals considered key to manufacturing clean energy technologies such as batteries, EVs and solar panels needed to move away from climate-heating fossil fuels.

The highest number of abuses was recorded in Indonesia, the world’s largest producer of nickel, which is used to make EV batteries. After the Indonesian government banned exports of raw nickel, Chinese firms invested billions of dollars to develop a large-scale nickel smelting and processing industry in the Southeast Asian country, largely powered by coal.

Other countries with a high number of recorded harms include the Democratic Republic of Congo, where Chinese firms dominate cobalt and copper production; Myanmar, where unregulated rare earths mining has caused widespread environmental destruction; Serbia, where Chinese-backed mining of some of Europe’s most significant copper and gold deposits is swallowing land and homes, and Zimbabwe, where Chinese investments have turned the nation into Africa’s top lithium producer.

Growing risks for people and nature

Allegations tracked by BHRC included negative impacts on local livelihoods, health and land rights, workers’ health and safety and work-related deaths, as well as water pollution and environmental contamination. In addition, 18 people were attacked for raising concerns about Chinese transition mineral projects between 2023 and 2025.

The report shows that 10 Chinese companies, including Zijin Mining, Tsingshan Group and Zhejiang Huayou Cobalt, accounted for nearly two-thirds of all allegations recorded in the last five years. It found that some Chinese companies “still appear to turn a blind eye to these issues” but noted that several others have been more responsive to allegations of abuse. However, even among companies with human rights policies, implementation remains a challenge, BHRC warned.

-

India looks to untapped graphite riches for slice of critical minerals boom

Clean energy demand for battery-grade graphite is surging, but India faces hurdles as it positions itself to compete with China’s grip on the supply chain -

Indonesia turns traditional Indigenous land into nickel industrial zone

Indonesia supplies the EV industry with critical battery materials but the sector’s rapid expansion is infringing the rights of Indigenous peoples -

Recycling could meet half of Europe’s critical mineral needs by 2050

A new report by an EU-funded research project says the bloc could harness its “urban mines” to reduce its dependence on China for energy transition minerals

Zijin Mining and Zhejiang Huayou Cobalt repeatedly responded to the allegations of harm by saying they take environmental and social risks seriously and adhere to international standards. Tsingshan Group never responded to BHRC’s requests for comment.

Platform for dialogue between communities and Chinese firms

At the same time, Chinese authorities have made “significant progress” on introducing a more specific framework for managing environmental and social risks in overseas investment, BHRC said.

This includes global consultation on a draft Sustainable Mining Code, adherence to UN guiding principles on business and human rights, and greater emphasis on oversight of companies operating overseas.

The China Chamber of Commerce of Metals, Minerals & Chemicals Importers & Exporters (CCCMC) set up a mediation and consultation mechanism intended to provide a platform for dialogue between affected communities or civil society groups that have raised concerns and Chinese companies.

More than three years since its launch, the mechanism has now received its first two complaints from local communities and many more are considering filing a case, Margaux Day, executive director at the nonprofit Accountability Counsel, told an event hosted by Climate Home News last month.

“This is incredibly exciting in that it fills a governance and accountability gap where often communities who are seeking to protect their rights and the environment can’t reach someone who will respond to them,” she told the panel discussion at London Climate Action Week.

Climate Home News understands that the complaints were filed by communities in Latin America and Southeast Asia over labour rights and resettlement issues. No information about the cases has yet been made public. The mechanism’s secretariat did not respond to Climate Home News’ questions.

The mechanism was set up after the Chinese regulator for banks and insurers called on investor-level institutions to establish complaints bodies to hear from communities outside of China. But whether the new initiative will prove effective in tackling grievances remains an open question.

“Real potential” for better mining practices

Participation in the mechanism is voluntary for Chinese firms and it doesn’t have a fact-finding function, nor can it impose provisions for compensation or compliance with human rights standards.

But Day told Climate Home News that, if successful, it could bring companies to negotiate an outcome that is better for people and the planet and leads to more sustainable mining practice.

Chen Yu, an independent China advisor for campaign group Global Witness, agreed that the mechanism holds “real potential”.

“There exists nothing else at a similar level to promote dialogue between communities and Chinese mining companies in particular,” she said.

For companies, the mechanism opens “a channel for problem-solving and dialogue with communities”, she added, as “Chinese companies often remain cautious of approaching affected communities directly, afraid of making the problem bigger”.

However, Chen said the mechanism remains at an early stage of development, faces resourcing challenges and is not yet sufficiently understood by communities in mining areas or Chinese firms.

To help it address some of these challenges, the secretariat is currently seeking technical support from a range of organisations, including civil society groups. But, Chen said, “it will take time for the mechanism to show its value”.

The post Allegations of harms at China-backed transition minerals projects rise appeared first on Climate Home News.

Allegations of harms at China-backed transition minerals projects rise

Andreas Sieber is head of political strategy at 350.0g. Cat Abreu is director of the International Climate Politics Hub.

From the US abduction of Venezuela’s president at the start of this year to the Iran war which rumbles on, disruption is the new normal for global geopolitics, more often than not linked to conflict over supplies of oil and gas.

Events so far in 2026 – driven largely by the desire of the Trump administration to grab control of fossil fuels around the world – show that the climate community’s approach to energy diplomacy will have to evolve if we are to operate effectively and push for climate action in such a volatile landscape.

Today’s climate and energy governance must be able to cope with trade wars, genocide, fascism, spiralling inequality and challenges to multilateralism. The increasingly dominant paradigms of economic competitiveness, energy security and green industrialisation can help drive the transition but they also challenge our collective mission to deliver an equitable green shift.

US-China rivalry dominates

Longer-term geopolitical trends that are seeing power move from West to East and North to South have fuelled a US–China “superpower rivalry”, which is pulling the global economy apart and reining in trade.

A key question will be how the fracture “lines” are drawn: by the US and China, or also by other countries or blocs? Many governments will try to remain “in the middle” between the two giants to capture economic gains from both sides. Yet despite the language of “strategic autonomy”, Washington and Beijing may be in a position to force choices via market access, export controls and sanctions.

-

Top maritime court rejects bid to halt UN deep-sea mining inquiry

Two subsidiaries of The Metals Company sought to block the probe into potential contract breaches launched after the firm’s application for US-sponsored permits

At first glance, this may not seem particularly relevant for climate and energy politics. But Huawei’s exclusion from 5G operations across the political West and India following the so-called Clean Network Campaign by the US government serves as a warning of what could happen to climate green tech.

And the recent debate to cut out Chinese inverters from European markets follows the same pattern – US security forces perceive a risk and start encouraging their allies to drop Chinese technology.

The new drivers: competition and security

Despite this fracturing geopolitical and economic context, energy transition is still happening. To ensure it is effective and equitable, we need to understand what is driving it and how to adapt climate politics so that it better responds to these drivers.

Put simply, China is supplying the world with low-cost renewables (roughly 60% of critical wind and 80% of solar components), batteries, EVs and other key elements. Other countries now also want their piece of the green tech pie and are forming industrial policies to get it.

It is this new competitiveness-driven logic that will shape the quest for decarbonisation, which has shifted from cooperating around the cost of tackling climate change to rivalry for the benefits of climate action.

Over 90% of new renewables projects are now cheaper than fossil alternatives. Gas-fired power is 3–4 times more expensive than solar and wind. In 2015, most decarbonisation policies were “traditional” emissions-cutting strategies like carbon pricing or net zero dates, whereas green industrial policies now underpin the majority.

Iran war could boost fossil fuel phase-out push, says Colombian minister

Meanwhile, security has become a central driver of energy politics. We are living through the second major fossil fuel crisis in just four years. Elevated oil and gas prices will impose up to $1 trillion in additional costs on the global economy by the end of the year if disruption continues in the Strait of Hormuz. Fossil fuel supply chains have exposed countries to conflict, coercion and brutal price shocks.

Fossil fuel volatility destabilises whole economies – higher fuel costs drive up food prices, increase political instability, and push millions into poverty and hunger. This incentivises governments to shield themselves from global shocks, especially in countries that are net fossil fuel importers and home to roughly three-quarters of the world’s population.

Yet security fears can cut both ways. The same instability that makes fossil fuel dependence untenable is also sharpening concern over China’s dominance of critical clean technologies and supply chains.

Equity, cooperation and the opportunity for change

Developing countries benefit from the rapid uptake of renewables enabled by low-cost Chinese technologies. But significant fiscal space and public investment is needed for the electricity grids and infrastructure required to fully unleash the energy transition, as well as for green industrialisation to diversify revenue streams.

Despite this, industrial-scale domestic production and ownership often remain out of reach for too many countries that lack the fiscal space to allow green supply chains to flourish and compete with their traditional industrial base. But more just and diversified green tech supply chains could be achieved with concomitant support.

Can giant batteries unlock Africa’s green industrial future?

For the first time in decades, the international order is being substantially reshaped. If within this context, decarbonisation is increasingly driven by green industrial policy, energy security and competitiveness, the climate policy community must better anticipate where these debates are moving. We must speak the same language, and enter the forums where decisions are made, including security, trade and bilateral or trilateral spaces.

We should build on an enlightened self interest recognising that cooperation remains essential and beneficial. This includes using the UN climate process differently: less as an ever-expanding negotiation machine, and more as a space for norm-setting, political alignment and deal-making. In an age of fragmentation, effective cooperation must not only be framed as necessary but thought of as a strategically compelling source of resilience and shared advantage.

The post Energy transition policymaking must evolve to fit an age of rupture appeared first on Climate Home News.

Energy transition policymaking must evolve to fit an age of rupture

“Next year is too late for regulations”: Beetaloo Energy’s 2GW gas-powered AI data centre a “disaster proposal” destined to cause climate chaos

Allegations of harms at China-backed transition minerals projects rise

Plant-Based Meat Takes Unusual Marketing Tack

-

Climate Change11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测