With almost every nation endorsing the Paris Agreement, the goal is to limit global warming to below 2°C by reducing greenhouse gas (GHG) emissions. However, a significant amount of carbon dioxide has already been accumulated in the atmosphere since the Industrial Revolution. Merely halting emissions would not be enough to reverse climate change.

Climate scientists suggest to remove 10 gigatons of CO2 annually by 2050 and 20 gigatons thereafter to meet the climate target.

In response, professionals and researchers worldwide are actively exploring carbon removal technologies to mitigate the impact of accelerating climate change. Research institutions, in particular, are focusing on curbing their GHG emissions and developing technologies for carbon capture and storage (CCS).

Negative emissions solutions like CCS or carbon capture utilization and storage (CCUS) are gaining importance. Top universities worldwide are actively contributing to this effort, each with specialized research groups focusing on various aspects of carbon capture and utilization. These ranges from capturing CO2 from smokestacks to developing innovative products that use atmospheric CO2 in beneficial ways.

Other top universities are implementing ways on how to directly curb their own carbon emissions and footprint to reach Net Zero goals. Here are the top six universities in the United States and what they’re doing to help in this fight.

Harvard University and Its Zero Goal

Faculty and students from across the Harvard community are working on ways to address climate change and its effects. The university has implemented various sustainability and climate initiatives. Here are some of them:

- Salata Institute for Climate and Sustainability: Established in fall 2022 with a generous $200 million gift from Melanie and Jean Salata, the institute serves as a hub for interdisciplinary collaboration, research, and engagement aimed at addressing the climate crisis.

- Sustainability Management Council (SMC): Senior leaders in operations, facilities, and administration convene regularly to facilitate the sharing of best practices and achieve the University’s sustainability and energy management objectives.

- Council of Student Sustainability Leaders (CSSL): Comprising graduate and undergraduate students involved in sustainability-related groups, the CSSL fosters collaboration, networking, and feedback on Harvard’s sustainability initiatives.

- Climate Solutions Living Lab: This initiative combines pedagogy and applied research to advance climate goals through interdisciplinary student projects focused on solutions for the building and energy sectors.

- Harvard Green Office Program: This program guides staff in creating sustainable workspaces, promoting environmental stewardship across the University.

- Resource Efficiency Program (REPs): Founded in 2002, REPs promotes sustainability within undergraduate housing through peer-driven educational initiatives.

Harvard’s Sustainability Action Plan underscored the university’s unwavering commitment to environmental stewardship and its relentless pursuit of sustainability initiatives both on campus and in broader contexts.

Central to Harvard’s agenda is the acceleration of clean energy adoption and the complete transition away from fossil fuels. Through these efforts, Harvard aims to establish a blueprint for a decarbonized world as shown by its decreasing carbon footprint.

Harvard University Carbon Emissions, 2006-2022

Goal Zero: A Fossil Fuel-Free Harvard

Harvard has set a bold objective to achieve fossil fuel-free status by 2050, surpassing the benchmark of merely attaining “carbon neutrality.”

While carbon neutrality typically involves offsetting emissions through initiatives like renewable energy procurement and tree planting, Goal Zero, as embraced by Harvard, aims for the complete elimination of fossil fuel usage. This approach acknowledges the comprehensive spectrum of harms stemming from fossil fuel consumption, going beyond carbon emissions alone.

Recognizing the manifold negative impacts of fossil fuels, which extend to their role as key components in plastics and toxic chemicals, Harvard also endeavors to curb these dependencies. This multifaceted approach aligns with the university’s broader mission to mitigate waste and foster a healthier, more sustainable value chain.

As an interim measure to progress towards Goal Zero, Harvard has established a short-term target to achieve fossil fuel neutrality by 2026. This entails eliminating campus emissions (both Scope 1 and Scope 2) and investing in initiatives that not only neutralize GHG emissions but also mitigate the adverse health effects of fossil fuel usage, such as air pollution.

By prioritizing human health, social equity, and slashing carbon footprint, Harvard aims to generate positive impacts through its transition to fossil fuel neutrality.

MIT’s Plan for Action on Climate Change

Since the announcement of Massachusetts Institute of Technology’s Plan for Action on Climate Change in October 2015, MIT Energy Initiative (MITEI) has made significant strides in research, education, outreach, and engagement efforts aimed at combating climate change and advancing clean energy solutions.

MITEI established its Carbon Capture, Utilization, and Storage (CCUS) Center in 2006 as part of its commitment to addressing climate change through innovative energy solutions. The center brings together faculty members focused on research in 3 key areas: capture, utilization, and geologic storage of CO2.

Within the CCUS Center, researchers explore a range of technologies and methods, including molecular simulation, materials design, catalytic processes, fluid mechanics, and advanced imaging techniques. They are developing emerging technologies for gas storage and separation.

Geologic storage research investigates the behavior of CO2 in underground reservoirs, including its interactions with pore fluids, and employs advanced imaging techniques to better understand the opportunities and risks associated with storing carbon dioxide underground.

Through these efforts, MIT is contributing to the development of innovative solutions for carbon capture and storage, essential for mitigating climate change. Here are the other key achievements of the university in various aspects of its efforts in cutting carbon emissions:

Research:

- MITEI’s research portfolio focuses on deep decarbonization across four major energy sectors—power, transportation, industry, and buildings—to address climate change and expand access to clean energy.

- The establishment of Low-Carbon Energy Centers has facilitated collaborative research efforts with industry partners to tackle pressing energy challenges. These centers help in advancing projects related to mobility systems, energy storage, carbon capture, and more.

- Major studies and reports, such as “Insights into Future Mobility” and “The Future of Nuclear Energy in a Carbon-Constrained World,” have provided comprehensive analyses of key technologies and sectors, informing policy and business decisions.

Education and Outreach:

- MITEI has been actively involved in educating students and the public about climate change and clean energy solutions through various initiatives, including workshops, seminars, and educational programs.

- The Mobility Systems Center, established as part of MITEI’s research efforts, has contributed to the understanding of individual travel decisions and the importance of sustainable mobility.

Engagement and Collaboration:

- Collaboration with industry partners, including global engineering and energy companies like IHI, Iberdrola, Eni S.p.A., and ExxonMobil, has led to significant advancements in clean energy technologies and policies.

- Membership agreements and collaborations with companies have resulted in substantial financial support for research projects, professorships, and technology development initiatives.

MIT is also joining the race to zero by aiming to eliminate direct emissions by 2050, with a near term milestone of net zero carbon campus emissions by 2026.

The university takes a multifaceted approach to achieve such climate goal. In general, the school will focus on:

- Decarbonizing its on-campus energy systems,

- Enabling large-scale clean energy generation on- and off-campus, and

- Embracing new decarbonization solutions.

These efforts underscore MIT’s commitment to addressing climate change and accelerating the transition to a sustainable energy future.

Yale University’s Center for Natural CO2 Capture

Founded with a transformative donation from FedEx and as a part of Yale’s Planetary Solutions Project, the Yale Center for Natural Carbon Capture is dedicated to exploring the science of natural carbon capture. Its mission is to develop solutions that contribute to addressing some of the most pressing challenges of our time.

The Center introduces fresh and innovative research and researchers to the Yale community, forging connections with relevant research laboratories both on and off-campus. Through funding research projects, workshops, and fellowships, the Center supports initiatives at the University and invests in training the next generation of scientists and practitioners. These efforts revolve around three primary Focus Areas:

- Ecosystem & Biological Capture,

- Geological & Ocean Capture, and

- Industrial Carbon Utilization.

Over the past year, the Center has achieved several notable milestones. Among these, two standout initiatives have emerged: the Yale Applied Science Synthesis Program (YASSP) and significant advancements in enhanced rock weathering (ERW).

YASSP connects academic researchers, policymakers, and those managing lands to answer applied questions about how land management decisions affect the services provided by forests, croplands, wetlands, rangelands, and grasslands.

Yale’s Net Zero Goal

Yale University is dedicated to achieving zero actual carbon emissions by 2050, with an interim objective of reaching net zero emissions by 2035. This goal will primarily be accomplished by reducing campus emissions by 65% below 2015 levels and, if needed, utilizing high-quality, verifiable carbon offsets.

The ultimate aim of zero actual carbon emissions will involve minimizing campus emissions entirely and implementing clean energy technology. The university managed to cut emissions by 28% since 2015, as seen below, despite a huge increase in campus size.

The university’s approach to climate action is comprehensive and encompasses all aspects of its operations. Yale is expanding its educational offerings to address the complexity and magnitude of global climate challenges.

The university’s approach to climate action is comprehensive and encompasses all aspects of its operations. Yale is expanding its educational offerings to address the complexity and magnitude of global climate challenges.

Additionally, investments are being made in campus infrastructure and emerging technologies to mitigate the university’s environmental impact. Yale has also adopted fossil fuel investment principles to facilitate a transition towards a decarbonized energy future.

Yale’s efforts to reduce carbon emissions include:

- Responsible energy use through conservation, efficiency upgrades, and innovative approaches to campus operations.

- Ensuring that energy generation on campus is efficient and environmentally friendly.

- Implementing a greenhouse gas emissions reduction strategy to steadily progress towards zero emissions targets.

- Purchasing and retiring high-quality, verified carbon offsets when necessary to meet emissions goals.

Stanford University Center For Carbon Storage

Stanford University leads global research on carbon sequestration, tackling critical questions on flow physics, monitoring, geochemistry, and more. They study CO2 storage in depleted oil and gas fields, saline reservoirs, and explore policies and techno-economics.

Stanford also focuses on capturing CO2 with engineered and natural applications, and combines bioenergy production with carbon capture to achieve net-negative emissions. Additionally, they research the impact of carbon taxes and cap-and-trade systems on CO2 capture and storage implementation.

The Stanford Center for Carbon Storage is focused on advancing crucial Carbon Capture and Storage (CCS) technologies aimed at capturing greenhouse gas emissions from smokestacks and securely storing them. Their research efforts are directed towards developing cost-effective methods for permanent storage on an industrial scale.

Visit this link to get to know more about the university’s CCS research highlights.

The center is actively addressing fundamental questions related to flow physics, monitoring techniques, geochemistry, and simulation of CO2 transport and behavior once stored underground. Their storage research encompasses a variety of geological formations, including fully-depleted oil fields, saline aquifers, and other unconventional reservoirs.

Stanford’s Path to Net Zero

The university also aims to reach net zero emissions by 2050, following this pathway:

After completing the full year of 100% renewable electricity, Stanford University revealed new goals to get rid of construction and food-related emissions by 2030.

The university is currently monitoring Scope 3 emissions across eight categories, including business and student travel, fuel and energy activities, waste, employee commute, construction, purchased goods and services, leases, and food purchases.

There’s still much work to be done to decrease Stanford’s scope 3 emissions. But with the two emission reduction goals revealed last year, they represent significant progress in the university’s understanding of and ability to reduce these emissions.

These goals underscore climate action as a fundamental value for the departments involved and showcase close collaboration on sustainability initiatives across the university.

Arizona State University: The Center For Negative Carbon Emissions

Arizona State University’s Center for Negative Carbon Emissions is at the forefront of advancing direct air capture (DAC) technologies, crucial for achieving a carbon-negative economy. The center has developed an innovative carbon management cycle focused on capturing carbon dioxide directly from the air.

Their goal is to demonstrate a system that enhances the efficiency and scalability of DAC while reducing costs. Currently, they are testing a prototype technology utilizing “mechanical trees” to extract CO2 from the air. These 10-meter-high structures employ a sorbent, an anionic exchange resin, which absorbs CO2 when dry and releases it when exposed to moisture.

Within just 20 minutes, these “mechanical trees” can capture greenhouse gases brought by the wind. The collected CO2 is then converted into a liquid that can be used to produce carbon-neutral fuel, other products, or sequestered for permanent disposal.

The research on mechanical trees has been ongoing for two decades and was pioneered by Dr. Klaus Lackner, the director of the Center for Negative Carbon Emissions. These trees are remarkably efficient, being a thousand times more effective than natural trees at removing CO2 from the atmosphere.

In addition to technological advancements, the center also examines the economic, political, and social implications of widespread implementation of affordable DAC technology, aiming to lead the way in the field of direct air capture.

ASU Climate Positive Pledge

Since fiscal year 2019, the university has been carbon neutral for scope 1 and 2 emissions through energy efficiency measures, green construction, offsetting, and renewable energy acquisition. The university is working toward achieving the same for its Scope 3 emissions by 2035.

ASU emphasizes energy efficiency and conservation through various initiatives. The university also promotes low-carbon energy sources, with 43% of energy in 2022 coming from such sources.

The school further aims for carbon-neutral transportation by 2035, achieving a milestone with single-occupancy vehicle travel reduced to 59% in 2022. Initiatives include bike parking expansion, ride-sharing incentives, electrification of fleet vehicles, and free intercampus shuttles. ASU also imposes a carbon price on air travel to mitigate emissions.

ASU climate positive commitments are as follows:

- Achieve carbon neutrality for Scope 1 and 2 emissions by FY 2025.

- Update: achieved carbon neutrality for Scope 1 and 2 emissions in FY 2019.

- Achieve carbon neutrality for Scope 3 emissions by FY 2035.

- Update: in progress, reduced 69% since FY 2007.

According to its recent sustainability report, ASU cut net emissions for Scopes 1, 2 and 3 by 91% per 1,000 square feet of building space and 90% per student.

2. Scope 3 emissions primarily occur in third-party commuting and air travel associated with ASU operations.

The post How Top U.S. Universities Cut Their Carbon Emissions to Help Fight Climate Change appeared first on Carbon Credits.

A forest is not just trees. The number of species it holds, from canopy giants to understorey shrubs to soil fungi, directly determines how much carbon it can absorb, and, more importantly, how much it can keep over time. Buyers of carbon credits increasingly ask a reasonable question: Is the carbon in this project long-lasting? The science of biodiversity has a clear answer.

![]()

ChatGPT developer OpenAI has paused its flagship UK data center project, known as “Stargate UK,” citing high energy costs and regulatory uncertainty. The project was part of a broader £31 billion ($40+ billion) investment plan aimed at expanding artificial intelligence (AI) infrastructure in the country.

The initiative was designed to deploy up to 8,000 GPUs initially, with plans to scale to 31,000 GPUs over time. It was aimed to boost the UK’s “sovereign compute” capacity. This means building local infrastructure to support AI development and reduce reliance on foreign systems.

However, the company has now paused development. An OpenAI spokesperson stated that they:

“…support the government’s ambition to be an AI leader. AI compute is foundational to that goal – we continue to explore Stargate UK and will move forward when the right conditions such as regulation and the cost of energy enable long-term infrastructure investment.”

Energy Costs Are Now a Core Constraint

The main issue is energy. AI data centers require large amounts of electricity to run GPUs and cooling systems.

In the UK, industrial electricity prices are among the highest in developed markets. Recent estimates show costs at around £168 per megawatt-hour, compared to £69 in France and £38 in Texas. This gap creates a major disadvantage for large-scale data center investments.

AI workloads are especially power-intensive. A single large data center can consume as much electricity as tens of thousands of homes. As AI adoption grows, this demand is rising quickly.

Globally, the International Energy Agency estimates that data centers could consume over 1,000 terawatt-hours (TWh) of electricity by 2030, up sharply from about 415 TWh in 2024. This growth is largely driven by AI.

The result is clear. Energy is no longer just a cost. It is a key factor in where AI infrastructure gets built.

Regulation Adds Another Layer of Risk

Energy is only part of the challenge. Regulation is also slowing investment. In the UK, uncertainty around AI rules, especially copyright laws for training data, has created hesitation among companies.

Earlier proposals to allow AI firms to use copyrighted content were withdrawn after backlash. This left companies without clear guidance on compliance.

For large infrastructure projects, this uncertainty increases risk. Data centers require billions in upfront investment. Companies need stable rules before committing capital.

Planning delays and grid connection timelines also add friction. These factors increase both cost and project timelines.

Together, energy costs and regulatory uncertainty create a difficult environment for hyperscale AI infrastructure.

OpenAI’s Global Infrastructure Expands, But More Selectively

Despite the pause, ChatGPT-maker is still expanding globally. The company is investing heavily in AI infrastructure through partnerships with Microsoft, NVIDIA, and Oracle. It is also linked to a much larger $500 billion “Stargate” initiative in the United States, focused on building next-generation AI data centers.

At the same time, the company faces rising costs. Reports suggest OpenAI could lose billions of dollars annually as it scales infrastructure to meet demand.

This reflects a broader industry shift. AI is becoming more like energy or telecom infrastructure. It requires large capital investment, long timelines, and stable operating conditions.

The pause also highlights a deeper issue. AI growth is increasing pressure on energy systems and the environment.

The Hidden Carbon Cost Behind Every AI Query

ChatGPT and similar tools rely on large data centers. These facilities already account for about 1% to 1.5% of global electricity use. Projections for their energy use vary widely due to various factors.

Each individual query may seem small. A typical ChatGPT request can use about 0.3 watt-hours of electricity, which is relatively low. However, usage at scale changes the picture.

ChatGPT now serves hundreds of millions of users. Even small energy use per query adds up quickly. Training models is even more energy-intensive. For example, training GPT-3 required about 1,287 megawatt-hours of electricity and produced roughly 550 metric tons of CO₂.

Newer models are even larger. Some estimates suggest training advanced models like GPT-4 could emit up to 15,000 metric tons of CO₂, depending on the energy source.

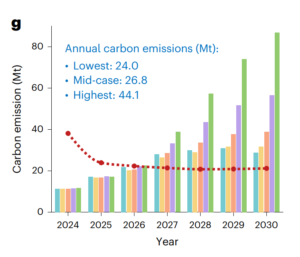

At the system level, the impact is growing fast. AI systems could generate between 32.6 and 79.7 million tons of CO₂ emissions in 2025 alone. By 2030, AI-driven data centers could add 24 to 44 million tons of CO₂ annually.

Looking further ahead, global generative AI emissions could reach up to 245 million tons per year by 2035 if growth continues. These numbers show a clear pattern. Efficiency is improving, but total demand is rising faster.

Big Tech Scrambles to Balance AI Growth and Emissions

OpenAI has not published a detailed standalone net-zero target. However, its operations rely heavily on partners such as Microsoft, which has committed to becoming carbon negative by 2030.

The company has acknowledged that energy use is a real concern. Leadership has pointed to the need for more renewable energy, including nuclear and clean power, to support AI growth.

Across the industry, companies are responding in several ways:

- Improving model efficiency to reduce energy per query

- Investing in renewable energy and long-term power contracts

- Exploring new cooling systems to reduce water and energy use

Efficiency gains are already visible. Some AI systems have reduced energy per query by more than 30 times within a year, showing how quickly technology can improve. Still, total emissions continue to rise because demand is scaling faster than efficiency gains.

The Global AI Infrastructure Race

The pause in the UK highlights a larger trend. AI infrastructure is becoming a global competition shaped by energy, policy, and cost.

Regions with lower energy prices and faster permitting processes have an advantage. The United States and parts of the Middle East are attracting large-scale AI investments due to cheaper power and supportive policies.

At the same time, governments are trying to attract these projects. The UK has pledged billions to support AI growth and improve compute capacity. But this case shows that policy ambition alone is not enough. Companies need reliable energy, clear rules, and predictable costs.

AI’s Next Phase Will Be Decided by Energy, Not Code

The decision by OpenAI does not signal a retreat from AI investment. Instead, it reflects a shift in priorities.

Companies are becoming more selective about where they build infrastructure. They are focusing on locations that offer the right mix of energy access, cost stability, and regulatory clarity.

The UK project may still move forward, but only if conditions improve. For now, the message is clear. The future of AI will not be shaped by technology alone. It will also depend on energy systems, policy frameworks, and long-term investment conditions.

The post OpenAI Hits Pause on $40B UK AI Project: Energy Costs Shake Data Center Economics appeared first on Carbon Credits.

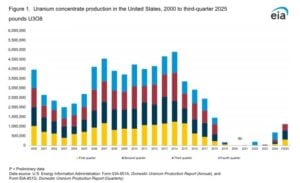

Uranium Energy Corporation (NYSE: UEC) has started production at its Burke Hollow project in South Texas. This is the first new uranium mine to open in the U.S. in over ten years.

The project started production in April 2026 after getting final regulatory approval. This marks a big step for domestic uranium supply. It’s also the world’s newest in-situ recovery (ISR) uranium mine, which shows a move toward less harmful extraction methods.

Burke Hollow was originally discovered in 2012 and spans roughly 20,000 acres, with only about half of the site explored so far. This suggests significant long-term expansion potential as additional wellfields are developed.

The mine’s output will go to UEC’s Hobson Central Processing Plant in Texas. This plant can produce up to 4 million pounds of uranium each year.

A Scalable ISR Platform Expands U.S. Uranium Capacity

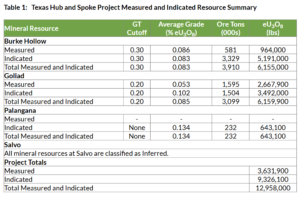

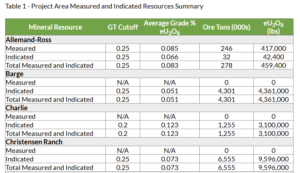

The Burke Hollow launch transforms UEC into a multi-site uranium producer in the United States. The company runs two active ISR production platforms. The second one is at its Christensen Ranch facility in Wyoming; both are shown in the table from UEC.

This “hub-and-spoke” model allows uranium from multiple wellfields to be processed through centralized facilities, improving efficiency and scalability. UEC’s operations in Texas and Wyoming are now active. This gives them a licensed production capacity of about 12 million pounds per year across the U.S.

ISR mining plays a key role in this strategy. Unlike conventional mining, ISR involves circulating solutions underground to dissolve uranium and pump it to the surface. This reduces surface disturbance and can lower environmental impact compared to open-pit or underground mining.

Burke Hollow is the largest ISR uranium discovery in the U.S. in the last ten years. This boosts its long-term value as a domestic resource.

Unhedged Strategy Pays Off as Uranium Prices Rise

UEC’s production launch comes at a time of strong uranium market conditions. The company uses a fully unhedged strategy. This means it sells uranium at current market prices instead of securing long-term contracts.

This approach has recently delivered strong financial results. In early 2026, UEC sold 200,000 pounds of uranium for $101 each. This price was about 25% higher than average market rates. The sale brought in over $20 million in revenue and around $10 million in gross profit.

The strategy allows the company to benefit directly from rising uranium prices, which have been supported by:

- Growing global nuclear energy demand

- Supply constraints in key producing regions

- Increased long-term contracting by utilities

Unhedged exposure raises risk in downturns, but offers more upside in strong markets. UEC is currently taking advantage of this.

Nuclear Energy Growth Is Driving Demand for Uranium

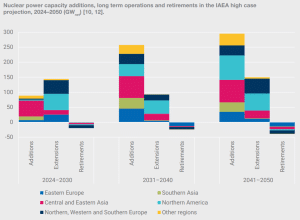

The timing of Burke Hollow’s launch aligns with a broader global shift back toward nuclear energy. Governments are increasingly turning to nuclear power as a reliable, low-carbon energy source.

The International Atomic Energy Agency projects that global nuclear capacity could double by 2050, depending on policy and investment trends. This would require a significant increase in uranium supply.

In the United States, nuclear energy accounts for around 20% of electricity generation. It also produces zero carbon emissions during operations. This makes it a key component of many net-zero strategies.

There are several factors supporting renewed nuclear demand, including:

- Development of small modular reactors (SMRs)

- Extension of existing nuclear plant lifetimes

- Government funding to maintain nuclear capacity

- Rising electricity demand from data centers and electrification

As demand grows, securing a reliable uranium supply becomes increasingly important.

Reducing Import Risk: A Strategic Domestic Supply Push

The Burke Hollow project also addresses a major vulnerability in U.S. energy policy. The country currently imports about 95% of its uranium needs, leaving it exposed to global supply risks.

A large share of uranium production and enrichment capacity is concentrated in a few countries, including Russia and Kazakhstan. This concentration has raised concerns about supply disruptions and geopolitical risk.

By expanding domestic production, UEC is helping to reduce reliance on imports and strengthen the U.S. nuclear fuel supply chain.

The company’s broader strategy includes building a vertically integrated platform covering mining, processing, and, eventually, uranium conversion. This approach aligns with U.S. government efforts to rebuild domestic nuclear fuel capabilities.

Federal programs have allocated billions to boost uranium production and enrichment. This shows how important the sector is.

Two Hubs, One Strategy: Wyoming Supports the Texas Breakthrough

While Burke Hollow is the main focus, UEC’s Christensen Ranch operation in Wyoming remains an important part of its production base.

The Wyoming site has recently received approvals for expanded wellfield development, allowing it to increase output alongside the Texas operation.

Together, the two sites form the foundation of UEC’s dual-hub production model. However, it is the Texas project that marks the first new U.S. uranium mine in over a decade, making it the central milestone in the company’s growth strategy.

Investor Momentum Builds Around Uranium Revival

The restart of U.S. uranium production is drawing strong attention from investors and industry players. Uranium markets have tightened in recent years, driven by rising demand and limited new supply.

UEC’s production launch has already had a positive market impact. The company’s share price rose following the announcement, reflecting investor confidence in its growth strategy.

At the same time, utilities are increasing long-term contracting activity to secure fuel supply. This trend is expected to continue as new nuclear capacity comes online and existing plants extend operations.

Industry forecasts suggest that uranium demand will remain strong through the 2030s, supporting higher prices and increased investment in new production.

Lower Impact Mining, Higher ESG Expectations

The use of ISR mining at Burke Hollow reflects a broader shift toward more sustainable extraction methods. ISR typically reduces land disturbance and avoids large-scale excavation.

However, environmental management remains critical. Key issues include groundwater protection, chemical use, and long-term site restoration.

UEC has emphasized environmental controls and regulatory compliance in its operations. These efforts are important for maintaining social license and meeting ESG expectations.

From a climate perspective, uranium production plays an indirect but important role. Supporting nuclear energy, it helps enable low-carbon electricity generation and reduces reliance on fossil fuels.

The Bottom Line: A Defining Moment for U.S. Uranium Production

The launch of the Burke Hollow mine marks a major milestone for the U.S. uranium sector. It ends a decade-long gap in new mine development and signals renewed momentum in domestic production.

In the short term, it strengthens supply and supports rising uranium markets. In the long term, it highlights the growing role of nuclear energy in global decarbonization strategies.

UEC’s Burke Hollow shows that new uranium projects can advance in today’s market. There are still challenges, like scaling production and handling environmental risks, but progress is possible.

As demand for nuclear energy continues to grow, domestic projects like Burke Hollow will play a key role in shaping the future of energy security and low-carbon power.

The post U.S. Uranium Mining Returns: UEC Launches First New Mine in a Decade appeared first on Carbon Credits.

A Protracted US–Iran War Could Strain Climate Finance From Wealthy Countries to Developing Nations

Illinois Weighs Early Warning System For Pesticide Spraying Near Parks, Schools

The History of Earth Day—and Why It Still Matters

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits