Carbon permits in the European Union have recently climbed to their highest levels since August 2023. The rise reflects tighter supply, policy decisions, and shifting market demand under the EU Emissions Trading System (ETS).

The ETS is the world’s largest cap-and-trade system for greenhouse gas emissions. It mandates large emitters to buy allowances for the carbon dioxide they emit. These allowances are known as EU Allowances (EUAs).

EUAs are now trading at a price over €92 per tonne — the strongest level in about 18 months. This rise shows that companies and markets expect fewer allowances to be available in the future as the EU tightens its emissions cap.

What Is the EU Emissions Trading System?

The EU ETS began in 2005 as a tool to reduce greenhouse gas emissions through market forces. It sets a cap on total emissions from major sectors such as power generation, manufacturing, and aviation. Companies must hold enough allowances to cover their emissions each year.

The cap reduces over time, meaning fewer EUAs are issued. This creates scarcity. As allowances become scarcer, their price tends to rise, which increases costs for polluters. In theory, this pushes companies to reduce emissions or invest in cleaner technology.

In 2026, the system also overlaps with the Carbon Border Adjustment Mechanism (CBAM), a tax on imported carbon-intensive goods. CBAM began to apply in January 2026 and makes carbon costs visible on imports like steel and cement. The measure aims to cut down on “carbon leakage.” This happens when industries move production to areas with cheaper carbon prices.

Recent Price Moves: Highest Since August 2023

In early January 2026, EU carbon permits climbed as high as about €91.82 per tonne on EU markets, up from lower levels earlier in 2025. Now, it’s trading at over €92 per tonne, showing 27% increase from January 2025 prices. The rise represents a fourth consecutive weekly gain in allowances for the December 2026 contract.

The price rise reflects tightening supply — fewer allowances are available through auctions and free allocations. Reduced supply increases competition among companies that must surrender EUAs to match their emissions. This dynamic pushes the price higher.

Market analysts also note that colder weather and more heating needs in winter often boost industrial energy demand. This can lead to higher carbon prices during the season.

Why Prices Have Risen?

The recent uptick in EU carbon prices is driven by several key factors:

- Reduced Supply of Allowances:

The EU continues to tighten its emissions cap and reduce the number of new allowances issued. Estimates from the European Exchange auction calendar and Market Stability Reserve show that auction volumes will drop. They are expected to fall from about 588.7 million EU Allowances in 2025 to around 482.4 million in 2026. A stronger cap reduces the total pool of tradable EUAs, creating scarcity and upward pressure on prices.

- Policy Signals and Reform Expectations:

Investors and companies anticipate future regulatory tightening. The EU’s long-term climate goals include cutting net emissions by 90% by 2040 compared with 1990 levels. Such policy signals can strengthen confidence that carbon costs will rise further.

- Market Confidence and Funds:

Investment funds have increased their holdings of EU carbon futures. Trading positions and speculation can also influence price momentum, especially as market sentiment shifts toward tighter futures.

- Compliance Demand:

Industries covered by the ETS are required to surrender allowances to match their emissions by compliance deadlines. As deadlines near, buying activity can increase, adding short-term upward pressure on prices.

- Carbon Border Adjustment Mechanism:

With CBAM now active, imported products from outside the EU face carbon costs similar to domestic industries. This mechanism can reduce free allowance allocations and tighten supply further.

Looking Back and Ahead: Carbon Price Trends and Forecasts

Carbon prices in the EU ETS have fluctuated over recent years. Prices surged above €100 per tonne in early 2023. Then, they eased back in 2024 and 2025. This decline was due to shifting market conditions and wider economic factors.

In 2024, the average price of EU ETS carbon permits was around €65 per tonne, down from €84 per tonne the year before. High prices in 2023 reflected strong policy signals from the Fit for 55 climate package and global energy disruptions.

Looking ahead, analysts and forecast models expect prices to continue rising over the coming decade:

- A survey of market participants predicts that the average EU ETS carbon price will rise to almost €100 per tonne from 2026 to 2030. This increase will happen as demand exceeds supply.

- Energy market analysts predict that the average price could hit about €126 per tonne by 2030. This rise is due to stricter caps and wider emission coverage.

- Under the EU ETS II framework, starting in 2027, more sectors will be included, like buildings and transport. In some scenarios, prices might average €99 per tonne from 2027 to 2030.

- BNEF’s EU ETS II Market Outlook projects carbon prices reaching €149 per metric ton ($156/t) by 2030, driving substantial emissions reductions.

Overall, these forward estimates imply that allowance prices may continue to rise as the EU strengthens its emissions targets to meet climate goals.

Emissions Reductions Under the ETS

The EU ETS has contributed to measurable emissions reductions. In 2024, emissions under the system were roughly 50% lower than in 2005. This progress is set to help the EU meet its 2030 goal of a 62% reduction from 2005 levels. The decline was driven mainly by cuts in the power sector, with increased renewable energy and a shift away from coal and gas.

Renewable energy growth, including wind and solar, played a role. Increases in renewables helped lower emissions by reducing reliance on fossil fuels.

The drop in emissions may lead to higher demand for allowances in the long run. With fewer emissions, companies will need more allowances to meet the cap.

What Higher Carbon Prices Mean for Industry

Higher carbon prices affect the European economy in many ways. For polluting industries, rising carbon costs increase operating expenses. Companies may invest more in cleaner technologies to reduce their allowance needs. This can accelerate decarbonization technology adoption.

Policy makers face the challenge of balancing climate goals with economic competitiveness. Some EU governments, like France, want price limits in the ETS. This could stop big swings in carbon costs. It would also help industries plan better.

The Market Stability Reserve (MSR), a mechanism to absorb excess allowances, also plays a role. It intends to reduce surplus permits and stabilize prices. Combined with the tightening cap, the MSR tends to push prices higher over time.

The ETS’s expansion to include more sectors — such as maritime transport and potentially buildings and road transport under EU ETS II — expands the share of emissions subject to carbon pricing. This broadening can further tighten supply and push prices up.

Why EU Carbon Prices Matter Beyond Europe

The EU ETS remains the largest carbon market in the world. According to global carbon pricing data, carbon pricing instruments currently cover about 28% of global greenhouse gas emissions, up from about 24% previously. The EU’s system is a key driver of this trend.

Many national and regional carbon markets have prices much lower than the EU’s. This shows differences in climate policies and economic situations. The ETS’s tightening emissions cap, reduced auction volumes, and shifting market sentiment all play roles in supporting higher carbon prices.

Forecasts suggest that prices may continue upward in the years to come, potentially averaging over €100 per tonne by the end of the decade. Meanwhile, the ETS continues to help reduce emissions in key sectors and supports the EU’s broader climate targets.

These price trends and policy developments make the EU carbon market a central piece of Europe’s climate strategy and an important bellwether for global carbon pricing efforts.

The post EU Carbon Prices Hit Highest Since August 2023: What Causes The Surge? appeared first on Carbon Credits.

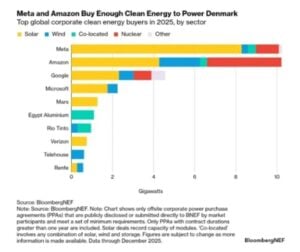

The U.S. is witnessing a surge in utility-scale solar development, driven by growing corporate demand for clean energy. Major tech companies like Meta and Google are securing long-term deals in Texas, combining renewable energy growth with economic and grid benefits.

This trend highlights how corporate commitments are shaping the future of the clean energy transition. Let’s find out.

Zelestra and Meta’s $600 Million Solar Deal

Madrid-based renewable energy firm Zelestra secured a massive $600 million green financing facility, signaling strong investor confidence in utility-scale solar. The funding, backed by Société Générale and HSBC, will support two large solar projects in Texas—Echols Grove (252 MW) and Cedar Range (187 MW).

These projects are not standalone efforts. Instead, they are part of a broader clean energy partnership with Meta, one of the world’s largest corporate renewable energy buyers. Together, they form a portion of a seven-project portfolio totaling 1.2 GW under long-term power purchase agreements (PPAs).

Sybil Milo Cioffi, Zelestra’s U.S. CFO, said:

“This financing marks a significant milestone in the delivery of our largest U.S. solar projects to date. It reflects strong confidence from Societe Generale and HSBC in our strategy and execution capabilities and reinforces our ability to attract first-class capital to support our growth platform in the U.S. market.”

Zelestra is strengthening its presence in the U.S. energy market with innovative solutions for hyperscalers and corporate clients. It is developing around 15 GW of renewable projects across key markets. In February 2026, BloombergNEF ranked Zelestra among the top 10 PPA sellers to U.S. corporations.

Solar Powering Meta’s Climate Strategy

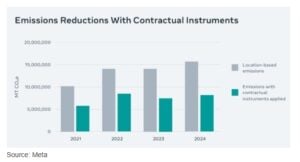

Meta continues to aggressively expand its clean energy footprint. The company has made renewable energy procurement a core part of its climate roadmap—and the numbers clearly reflect that shift.

In 2024, Meta reported emissions of 8.2 million metric tonnes of CO₂e after accounting for clean energy contracts. In comparison, its location-based emissions stood at 15.6 million tonnes. This marked a sharp 48% reduction, largely driven by renewable energy purchases.

Moreover, the company has consistently maintained momentum:

- Since 2020, it has matched 100% of its electricity consumption with renewable energy.

- Over the past decade, it has secured more than 15 GW of clean energy globally.

- Overall, renewable energy procurement has helped cut 23.8 million MT CO₂e emissions since 2021.

As a result, Meta cut operational emissions by around 6 million tonnes in 2024 alone. At the same time, it tackled value chain emissions using Energy Attribute Certificates (EACs), reducing Scope 3 emissions by another 1.4 million tonnes.

Most of these deals were concentrated in the U.S., highlighting the country’s growing importance in corporate decarbonization strategies.

Importantly, this collaboration goes beyond just energy supply. It also aims to deliver broader economic benefits, including:

- Local job creation during construction

- Long-term tax revenue for the region

- Continued investment in local infrastructure

David Lillefloren, CEO at Sunraycer, said:

“These agreements with Google represent a significant milestone for Sunraycer and underscore the strength of our development platform. We are proud to support Google’s clean energy objectives while delivering high-quality renewable infrastructure in Texas.”

Additionally, the deal was facilitated through LevelTen Energy’s LEAP process, which simplifies and speeds up PPA execution. This highlights how innovative platforms are now playing a key role in scaling renewable deployment.

“Google’s data centers are long-term investments in the communities we call home,” said Will Conkling, Director of Energy and Power, Google. “This collaboration with Sunraycer will fuel local economic growth while helping to build a more robust and affordable energy future for Texas.”

Google, like Meta, has built a strong clean energy portfolio over time. Since 2010, it has signed over 170 agreements totaling more than 22 GW of capacity worldwide. Its long-term ambition is even more ambitious—achieving 100% carbon-free energy, every hour of every day, by 2030.

Why Texas Is Becoming the Center of Energy Transformation

All these developments point to one clear trend—Texas is rapidly becoming a global hub for clean energy and data center growth.

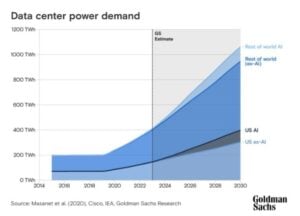

On one hand, the state offers strong solar resources, vast land availability, and a deregulated power market. On the other hand, it is witnessing a surge in electricity demand, especially from data centers and AI-driven workloads.

According to projections from the EIA, U.S. electricity demand could rise by 20% or more by 2030. Data centers are expected to play a major role in this growth. In fact, energy consumption from data centers increased by over 20% between 2020 and 2025.

As a result, energy infrastructure in Texas is facing growing pressure. Rising industrial activity, extreme weather events, and rapid digital expansion are all contributing to grid stress. Yet, at the same time, this demand is driving unprecedented investment in renewable energy.

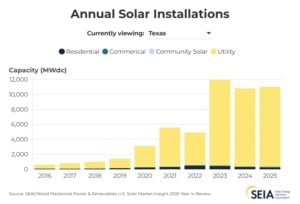

The EIA expects Texas to lead solar expansion in the coming years, accounting for nearly 40% of new solar capacity in the U.S. California will follow closely, and together, the two states will drive almost half of total additions.

Even though the sector has faced temporary slowdowns, the long-term outlook for U.S. solar remains highly positive.

In 2025, the U.S. added 53 GW of new electricity capacity—the highest annual addition since 2002. Notably, wind and utility-scale solar together generated 17% of the country’s electricity, a massive jump from less than 1% two decades ago.

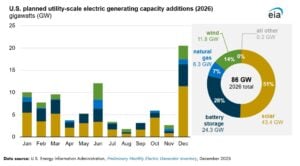

Looking ahead, growth is expected to accelerate again. Developers are planning to add around 86 GW of new capacity in 2026, which could set a new record. Solar alone is projected to account for more than half of this expansion.

Breaking it down further:

- Solar is expected to contribute 51% of new capacity

- Battery storage will make up 28%

- Wind will account for 14%

Utility-scale solar capacity additions could reach 43.4 GW in 2026, marking a 60% increase compared to 2025 levels.

Analysis: Corporate Demand Is Reshaping Energy Markets

Overall, the developments from Zelestra, Meta, Google, and Sunraycer highlight a broader transformation underway in global energy markets.

First, corporate buyers are no longer passive participants. Instead, they are actively shaping energy infrastructure through long-term PPAs. These agreements provide stable revenue for developers while ensuring a clean power supply for companies.

Second, financing is becoming more accessible. Large-scale funding deals, like Zelestra’s $600 million facility, show that banks are increasingly willing to back renewable projects with strong contractual support.

Third, regions like Texas are emerging as strategic energy hubs. The combination of rising electricity demand and favorable renewable conditions is attracting both developers and corporate buyers.

However, challenges remain. Grid reliability, permitting delays, and policy uncertainty could still impact the pace of deployment. Even so, the overall trajectory remains clear.

Clean energy demand is rising fast. Big Tech is leading the charge. And solar power is set to play a central role in meeting future electricity needs.

- READ MORE: Meta, Amazon, Google, and Microsoft Dominate Clean Energy Deals as Global Buying Slips in 2025

The post Texas Solar Market Heats Up with Meta and Google Investments appeared first on Carbon Credits.

A major transaction in the methane market is drawing attention across the energy sector. Xpansiv and MiQ announced the settlement of 3.5 million methane certificates on the Xpansiv CBL exchange. This is one of the largest trades of its kind to date.

The deal involved a European energy buyer and a large integrated energy producer. It covered 3.5 million MMBtu of U.S.-produced natural gas, with emissions verified under the MiQ standard.

The transaction shows that methane certification is moving from pilot programs to real market activity. It also highlights the growing demand for transparent emissions data in global gas supply chains.

What Are Methane Certificates: Tracking Invisible Emissions

Methane certificates track the emissions intensity of natural gas. They provide independently verified data on how much methane is released during production and transport.

Xpansiv CEO John Melby stated:

“We are excited to support the energy sector’s transition to certified natural gas by providing secure and scalable market infrastructure to transact and settle these innovative instruments. This transaction sets a new benchmark for the integration of verified environmental performance in the global energy markets, enhancing precision, rigor, and integrity in responsible natural gas sourcing.”

Methane is a powerful greenhouse gas. According to the International Energy Agency, methane has a much higher warming impact, 80x more than carbon dioxide over the short term. So, reducing methane leaks is one of the fastest ways to cut global warming.

MiQ certificates assign grades based on emissions performance. These grades help buyers choose lower-emission gas. The system creates a financial incentive for producers to reduce methane leaks.

Certification also supports compliance. The European Union Methane Regulation requires companies to measure and report methane emissions using strict standards.

As rules tighten, verified data becomes more valuable. This is driving demand for certified gas and related environmental products.

From Pilot to Market Reality

This transaction is not just large. It also shows how methane markets are evolving.

- First, it demonstrates that market infrastructure is maturing. The trade was settled through Xpansiv’s CBL exchange, which allows secure and transparent transactions without complex bilateral agreements.

- Second, it reflects growing cross-border demand. European buyers are increasingly seeking certified gas to meet regulatory and corporate climate goals.

- Third, it sets a benchmark for scale. Earlier, methane certificate trading was limited. This deal shows that multi-million unit transactions are now possible.

Industry leaders see this as a step toward integrating emissions data into everyday energy trading. It brings methane performance closer to becoming a standard market factor, like price or volume.

Rising Demand from Data Centers and Energy Use

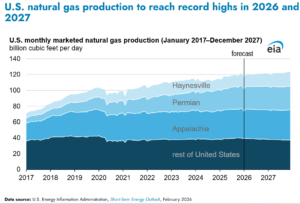

One key driver of methane certificate demand is rising energy consumption. The U.S. Energy Information Administration projects that U.S. natural gas use could increase by up to 7.3% between 2025 and 2027. It is also expected to hit a record-high 122.3 Bcf/d in 2027.

A major reason is data center growth. Artificial intelligence and cloud computing require large amounts of electricity. Many data centers rely on natural gas for reliable power.

Tech companies are now looking at emissions across their energy supply chains. This includes methane emissions from gas production. Methane certificates offer a way to track and manage these emissions.

This trend links digital growth with environmental accountability. As data demand rises, so does the need for cleaner energy sourcing.

A Rapidly Expanding Market and Emerging Trends

Methane certification is part of a broader expansion in environmental markets. Platforms like Xpansiv support trading in:

- Carbon credits

- Renewable energy certificates

- Methane performance certificates

These markets are growing quickly. On Xpansiv’s CBL exchange, trading volumes in environmental commodities have reached millions of tons annually, with strong growth in recent years.

MiQ has grown rapidly since its launch and is now a major player in methane certification. Today, MiQ certifies about 25% of U.S. natural gas production and more than 5% of global gas supply.

The MiQ registry now holds billions of issued certificates, creating a large pool of tradable emissions performance data. This scale shows that methane performance is moving beyond pilot stages and into mainstream markets.

Georges Tijbosch, CEO, MiQ, said:

“Our program gives buyers the trusted, independently verified emissions data they need to make smart choices—raising the bar for openness and accountability in the natural gas industry.”

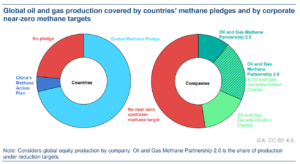

Demand for methane certificates will grow as global regulations tighten. The IEA’s Global Methane Tracker 2025 shows that methane pledges cover about 80% of global fossil fuel production. However, only a small part has enforceable rules. This points to a rising need for verified emissions data.

In the EU, strict laws require ongoing monitoring, reporting, and quick leak repairs. Frameworks like OGMP 2.0 already cover around 42% of global oil and gas production. This pushes companies toward certification based on measurements.

Globally, methane causes about 30% of temperature rise since the Industrial Revolution, reinforcing regulatory urgency. As compliance moves from estimates to verified data, certified methane tracking systems are crucial for market access and trade.

At the same time, many firms are setting stricter climate targets that include methane performance. Investors are also pushing for better emissions data across energy supply chains.

Some industry forecasts suggest that markets for methane performance data and certificates could grow by more than 60% annually in the next several years. Together, these trends are likely to support continued growth in the methane certificate market.

Infrastructure is also improving. Exchanges like CBL help provide price signals and liquidity. Partnerships with firms like S&P Global aim to improve market transparency and data quality.

What This Means for the Energy Transition

The 3.5 million certificate trade highlights a broader shift in energy markets. Emissions data is becoming part of how energy is bought and sold.

Natural gas remains a key fuel in the global energy mix. But buyers are increasingly focused on how it is produced. Lower-emission gas may gain a competitive advantage.

Methane certification offers a practical tool. It allows companies to:

- Track emissions,

- Improve performance,

- Meet regulatory requirements, and

- Support climate targets.

This aligns with wider efforts to reduce greenhouse gas emissions while maintaining energy supply. In the coming years, methane certification could become a standard part of natural gas trading. It may also link more closely with carbon markets and broader climate finance systems.

With this development, the direction is clear. Environmental performance is becoming a measurable and tradable part of energy markets. Deals like this signal that the shift is already underway.

- READ MORE: Shell’s Initiative to Cut Methane in Rice Farming in the Philippines and Create Carbon Credits

The post A Record 3.5M Methane Credits Trade at Xpansiv CBL Signals New Era for Gas Markets appeared first on Carbon Credits.

Carbon tends to sit at the forefront of climate considerations, but there’s another important, interconnected piece of the sustainability puzzle that often gets overlooked: water.

Globally, 4 billion people face severe water scarcity for at least one month out of every year, according to the United Nations University Institute for Water, Environment and Health (UNU-INWEH).

Like with global warming, human activities have had a major impact on water systems. Not only are we often using too much water, but issues like land use change and rising temperatures also stress freshwater ecosystems and the water cycle.

If we ignore these issues, more water systems will be permanently damaged. That likely means more people will live with insufficient access to clean water, agricultural production will become more difficult and expensive, and many businesses will face economic risks, like supply chain delays and shortages.

Fortunately, there are ways to reduce water risks and even improve water systems.

One option is to purchase water credits. Similar to how carbon credits emerged as a solution for offsetting hard-to-avoid greenhouse gas emissions, water credits provide a market-based solution for conserving and restoring water systems.

Here, we’ll take a deeper dive into:

- What are Water Credits?

- How do Water Credit Projects Work?

- Water Credit Project Types and Examples

- Benefits of Water Credits

- Why Individuals and Businesses Should Buy Water Credits

What Are Water Credits?

If you’re familiar with carbon credits, you already get the gist of water credits.

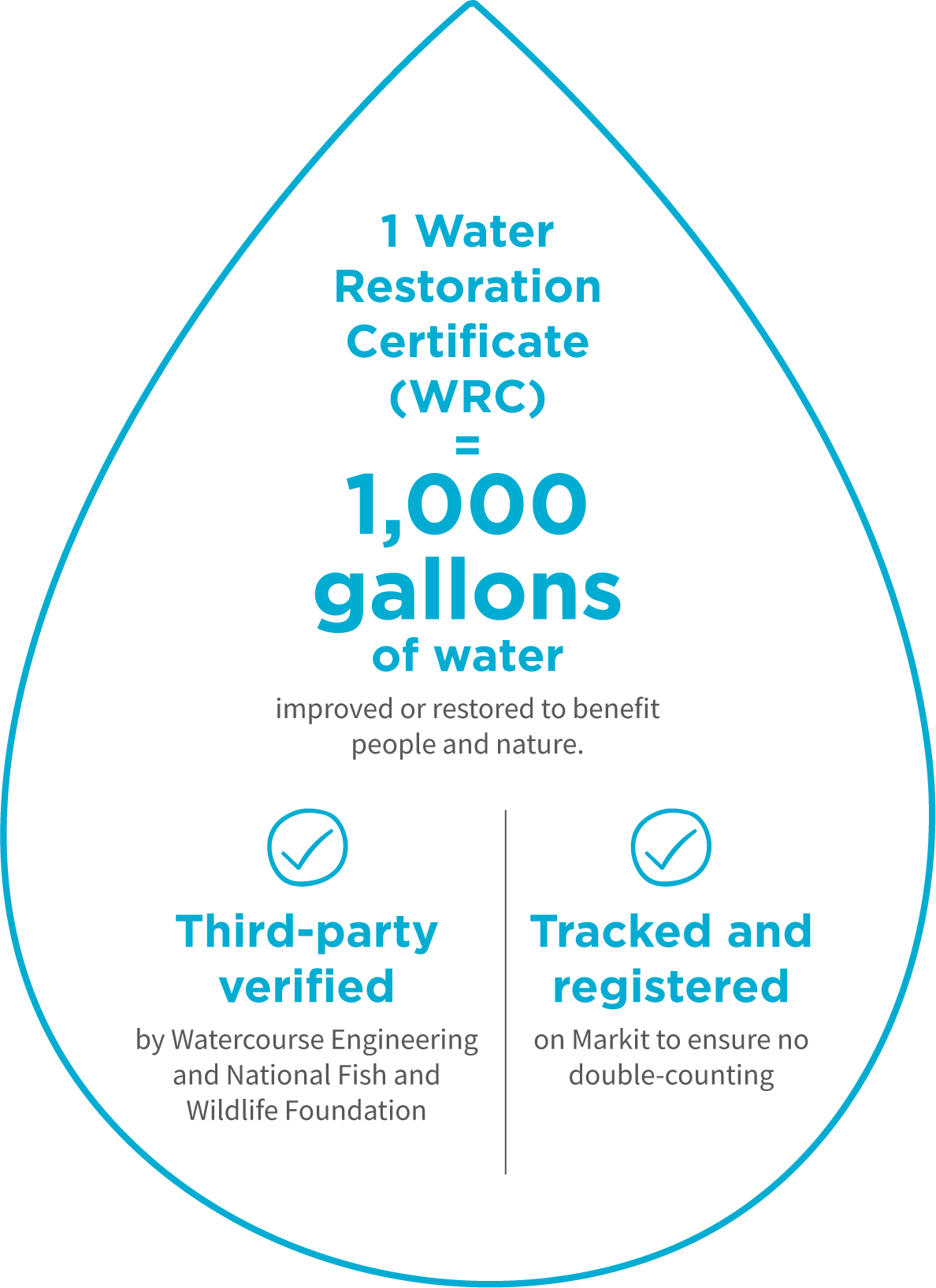

Similar to how one carbon credit represents one metric ton of carbon dioxide equivalent avoided or removed from the atmosphere, one water credit represents 1,000 gallons of natural freshwater flow that has been improved or restored.

Water credit projects involve protecting, restoring, or conserving water flows to ultimately help natural systems like rivers, wetlands, and aquifers, along with the communities that rely on them.

Source: Bonneville Environmental Foundation

For example, leading project developer Bonneville Environmental Foundation (BEF) issues Water Restoration Certificates® that are third-party verified, namely by Watercourse Engineering or the National Fish and Wildlife Foundation. All BEF WRC® projects are also tracked and registered on S&P Global’s Markit registry to avoid double-counting.

Other water credit programs exist, but BEF WRCs® are arguably the most established market-based solution for addressing your water footprint.

Terrapass offers BEF WRC® certificates that support projects like the Middle Deschutes River Flow Restoration project in Oregon, which in turn helps support a healthy ecosystem for local wildlife and communities.

Buy BEF WRCs® through Terrapass today.

How Do Water Credit Projects Work?

Water credit projects work similarly to carbon credit projects in terms of directing financing toward initiatives that support the restoration of natural freshwater flows and ecosystems.

Water restoration project developers like BEF work with farmers, conservation groups, and local irrigation districts to identify these opportunities and manage the projects. Water restoration projects also meet additionality requirements, meaning that without the funding from water credits, the projects would not be possible.

For example, funding might go towards the cost and effort of securing legal agreements that help restore river flows. This is necessary to help overcome challenges like “use it or lose it” water rights policies in the Western U.S. By maintaining a water source for ecological purposes, water rights holders can maintain their water rights while addressing old and inefficient requirements like the obligation to use all of their allotted water.

Note that since water issues are largely regional, best practice is to purchase credits from water restoration projects that help relieve water stress in the same basins where you’re using water. However, water credit projects are mostly concentrated in the Western U.S. where water stress is more severe, so matching projects to your location isn’t always possible. If that’s the case, buying a mixed portfolio of water credits can still compensate for your impact, it just might not directly address water issues in the areas you operate.

Water Credit Timing

Each water credit directly translates to 1,000 gallons of natural freshwater improved or restored over an 18-month cycle.

Note that while these projects might provide long-lasting water benefits, along with other associated environmental and social benefits, best practice is for buyers to only count water credits against their water footprint for the year in which these certificates are purchased.

To address your water footprint for multiple years, buyers can purchase water credits for each year they want to balance their water impact, similar to how you would purchase carbon credits corresponding to each year’s emissions.

Also note that water credits have vintages, which refer to the primary year when the water restoration took place. Like with carbon credits, best practice for water credits is to buy ones with recent vintages — generally within the last five years, but ideally within the past three. However, you don’t have to match vintages with the year of your own water consumption, as you’re still funding water improvements that help balance your own footprint.

Water Credit Project Types and Examples

BEF WRC® projects fall into one of three main categories:

- Restoring Flows: These projects often involve legal transactions like water rights transfers and partnerships with local groups to help keep water flowing in rivers and streams, rather than overly diverted, like for inefficient agricultural practices.

Example — Jordan River Flow Restoration: This project uses Environmental Water Transactions (EWTs) to help secure more water flowing from the Jordan River into the Great Salt Lake in Utah, which helps address the critical shrinking of this lake.

- Restoring Natural Systems: While similar to restoring flows, this project category focuses more on physical interventions to help restore freshwater systems like rivers and wetlands to their natural state, thereby increasing freshwater and potentially providing co-benefits like cleaner water.

Example — Pine Tree Brook Dam Removal: This project removes dams in the Pine Tree Brook in the Boston area to support the movement of local trout and improve water quality. For example, one of the dams on this brook was previously put in place to create a local ice rink, but that was no longer needed due to the 1950s construction of a nearby ice rink facility that does not rely on this water source. So, removing it helped return the brook to more of its natural order.

- Improving Efficiency: Some water credit projects focus more on conservation and efficient water use, which can thereby help retain or restore water in natural systems.

Example — Mason Lane Headgate: In Arizona, the Mason Lane Ditch diverts a tributary of the Verde River to irrigate agricultural land. This project funds the replacement of an inefficient headgate system with a modern, automated one to enable more precise control of the diverted water.

Benefits of Water Credits

In addition to directly supporting freshwater restoration, water credits provide a wide range of co-benefits, such as supporting:

- Groundwater conservation: Projects that minimize groundwater usage not only can improve water volume but also provide benefits like stabilization of river beds. That helps to avoid problems like sinking land and enables water systems to maintain natural filtration capabilities.

- Biodiversity: Water restoration projects often support biodiversity, like providing a healthier habitat for local fish and bird populations. That can provide associated environmental and economic benefits, like supporting pollinators and keeping local fisheries well-stocked.

One example of biodiversity co-benefits can be seen in the Merced County Seasonal Wetland Habitat project, which aims to provide an annual spring habitat for migratory birds in central California.

You can support projects like these by buying BEF WRCs® through Terrapass today.

- Recreation: Maintaining freshwater ecosystems helps provide communities with recreational opportunities, such as fishing, boating, and hiking. That can correlate with economic opportunities for these areas, while also supporting the health of local populations.

- Agricultural economies: The funding from water credits can directly support farmers and ranchers, providing an important income stream that can help mitigate issues like crop shortages. Long term, water credits can also support a more stable water supply that sustains these agricultural businesses season after season, even amidst increasing floods and droughts caused by climate change.

- Community empowerment: Water credits often involve working with tribal groups and other local communities. The economic, ecological, and recreational benefits can help protect these communities’ cultures and rights.

- Lower emissions: While water credits are separate from carbon credits, there can be interconnected benefits. For example, more efficient irrigation systems can use less water and energy. More reliable water supplies can also reduce the need for high-emitting fertilizers.

Why Individuals and Businesses Should Buy Water Credits

Water risk sometimes gets overshadowed by carbon emissions risk, but it’s important for both individuals and businesses to consider their water footprints. Buying water credits enables you to account for the impact of your water usage while supporting a broad range of environmental, economic, and social benefits.

In particular, consider the following:

For Individuals

You likely use far more water than you assume, particularly when accounting for indirect usage, like the water that went into making the jeans you bought. One survey from American Water found that most Americans think they use less than 100 gallons of water per day, when really total usage adds up to over 2,000 gallons daily, based on data from Water Footprint Network.

While it’s important to be mindful of your water usage, we’re all inevitably going to use water throughout our daily lives. So, purchasing water credits helps you take responsibility for the impact of this water usage while funding projects that have a wide range of co-benefits you may value.

For Businesses

Just as many companies acknowledge climate risk and commit to addressing greenhouse gas emissions, water scarcity and overuse can have direct economic effects on businesses, along with creating risks like reputational damage. By 2050, 31% of global GDP is projected to be exposed to high water stress, according to the World Resources Institute.

So, buying water credits can address your company’s direct water footprint and contribute to solving water scarcity and quality issues that can harm your operations going forward. Meanwhile, businesses can potentially increase goodwill with customers, employees, and the local communities where they operate by supporting water credit projects that have meaningful co-benefits.

Buying water credits can also align with other standards and certifications that many businesses value. Some examples include:

- WRI’s Volumetric Water Benefit (VWB) Accounting 2.0: Water credit projects can potentially align with this VWB accounting standard, and Bonneville Environmental Foundation was one of WRI’s partners involved in creating it. Still, consider looking into the details of this accounting standard and project specifics to determine alignment.

- UN Sustainable Development Goals (SDGs): Depending on the specific project, there can be benefits that align with multiple SDGs. For example, a project might align with SDG 6: Clean Water and Sanitation, while also supporting local economic development that aligns with SDG 11: Sustainable Cities and Communities.

- LEED Certification: Water credits can be matched to a building’s annual water usage and counted toward this green building certification.

- 1% for the Planet: BEF is an environmental partner of 1% for the Planet, so buying BEF WRCs® can qualify a company for membership.

- B Corp: Buying water credits can also count toward earning B Corp certification.

Ready to Support Water Restoration?

Terrapass makes it easy for you to balance your water footprint while supporting sustainable ecosystems and community development.

You can directly purchase BEF WRCs® through Terrapass today or reach out to speak with one of our sustainability experts who can help you build a custom portfolio of carbon credits and water credits that align with your sustainability goals.

Talk to a Sustainability Expert

The post The 2026 Complete Guide to Water Credits (WRCs) appeared first on Terrapass.

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?