ExxonMobil published its updated 2030 Corporate Plan, which keeps the company’s “dual challenge” approach. The oil giant says it will supply reliable energy while cutting emissions. The update raises lower-emission spending, while also forecasting higher oil and gas production to 2030.

Billions in Motion: ExxonMobil’s Financial and Production Targets

ExxonMobil plans about $20 billion of lower-emission capital between 2025 and 2030. It says the $20 billion targets carbon capture and storage (CCS), hydrogen, and lithium projects.

The company projects ~5.5 million oil-equivalent barrels per day (Moebd) of upstream production by 2030. Exxon also forecasts ~$25 billion of earnings growth and ~$35 billion of cash-flow growth by 2030 versus 2024 on a constant price-and-margin basis.

The oil major gives a range for cash capex. It shows $27–29 billion for 2026 and $28–32 billion annually for 2027–2030. The updated plan highlights about $100 billion in major investments planned for 2026–2030. It notes these projects could bring in around $50 billion in total earnings during that time.

Low-Carbon Plan: $20B for CCS, Hydrogen and Lithium

ExxonMobil describes the $20 billion as focused on three business lines:

- CCS networks and hubs for third parties.

- Hydrogen production and integrated fuels.

- Lithium supply for batteries.

The company says roughly 60% of the $20 billion will support lower-emissions services to third-party customers. It estimates new low-carbon businesses could deliver ~$13 billion of earnings potential by 2040 if markets and policies develop as expected.

Exxon’s updated Corporate 2030 Plan lists current and contracted CCS volumes. The company reports about 9 million tonnes per annum (MTA) of CO₂ capture capacity under contract for its U.S. Gulf Coast network. Key project entries include:

- Linde — Beaumont, TX: ~2.2 MTA CO₂, start-up 2026.

- CF Industries — Donaldsonville, LA: ~2.0 MTA, start-up 2026.

- NG3 (Gillis, LA): ~1.2 MTA, start-up 2026.

- Lake Charles Methanol II: ~1.3 MTA, start-up 2030.

- Nucor — Convent, LA: ~0.8 MTA, start-up 2026.

The plan also highlights a proposed 1.0 GW low-carbon power/data center project paired with ~3.5 MTA capture, with a planned final investment decision in 2026. Exxon calls its Gulf Coast network an “end-to-end CCS system” and says scale depends on permitting and supportive policy.

- SEE MORE: ExxonMobil’s (XOM Stock) Wild Ride: Gas Discovery, $14M Pollution Fine, and Carbon Storage Push

Counting Carbon: How Exxon Tracks Methane and Emissions Cuts

ExxonMobil says it is making measurable progress on emissions. The company reports faster-than-expected cuts in several intensity metrics. It states it has already met key 2030 intensity milestones and now expects to meet its methane-intensity target by 2026, four years early.

The company repeats its long-term net-zero framing for operated assets. Exxon’s plan targets Scope 1 and Scope 2 net-zero for its operated assets by 2050. It also sets a nearer target of net-zero Scope 1 and 2 for its operated Permian assets by 2035.

These commitments focus on emissions the company directly controls. They do not include a Scope 3 net-zero pledge for customer use of sold products. Exxon underscores that these goals depend on technology, markets, and supportive policy.

On operational achievements, Exxon highlights large cuts in routine flaring and improved equipment standards. The new plan states that the company reduced corporate flaring intensity by over 60% from 2016 to 2024.

- As shown in the chart below, ExxonMobil’s operated-basis greenhouse gas profile shows a clear decline in Scopes 1 and 2 between the 2016 baseline and 2024.

Also, by 2024, Scope 1 emissions dropped to 91 million metric tons CO₂e. Scope 2 emissions (location-based) reached 9 million metric tons CO₂e. Together, this totals 100 million metric tons CO₂e. This is about a 15% reduction from 2016 based on operations.

For the same period, Exxon’s Scope 1+2 emissions intensity dropped from 27.5 to 22.6 metric tons CO₂e per 100 metric tons produced. This shows they are decarbonizing operations, even as production has changed.

The company also hit other flaring and GHG intensity goals ahead of schedule. These outcomes came from replacing old equipment, tightening operations, and limiting routine venting and flaring.

Exxon lists four categories of near-term reduction actions it is scaling up:

- Methane control: wider deployment of leak-detection and infrared cameras, more frequent inspections, and accelerated repairs.

- Flaring reduction: operational changes and stricter shutdown protocols to cut routine flaring.

- Efficiency and asset management: project design improvements, digital optimization, and selective asset sales or retirements to lower average carbon intensity.

- CCS and low-carbon services: building capture hubs (about 9 MTA of contracted CO₂ capacity on the U.S. Gulf Coast) and contracting capture services for industrial customers.

The plan also names specific technology and program investments. Exxon highlights advanced sensor networks and real-time emissions monitoring. They also focus on expanding data systems to track and verify reductions. It expects these tools to improve measurement accuracy and speed up corrective action.

Limits and caveats appear repeatedly. Exxon links its long-term net-zero goal to several factors. These include market formation, policy incentives like tax credits and carbon pricing, and permitting timelines. The company warns that total emissions and some asset outcomes will change with production levels and energy demand.

In the near term, key metrics to watch include:

-

2026 methane-intensity and flaring disclosures.

-

Volumes of CO₂ captured and stored as Gulf Coast CCS projects launch.

-

The pace of FID and execution for the 1.0 GW / 3.5 MTA low-carbon power and capture project.

These will show whether Exxon’s claimed progress converts into sustained emissions declines.

Fueling the Future: Rising Oil & Gas Output Through 2030

Exxon projects higher hydrocarbon output even as it invests in low-carbon businesses. The plan targets ~5.5 Moebd by 2030. The company expects ~65% of production to come from advantaged assets such as the Permian Basin, Guyana, and select LNG.

Permian growth is a core part of the supply outlook. Exxon expects roughly 2.5 Moebd from the Permian by 2030, up materially from 2024 levels. Guyana’s Stabroek Block is another major growth driver.

Exxon plans multiple new offshore start-ups in Guyana before 2030. The company argues that these barrels deliver lower operational carbon intensity compared with many older fields.

Critics say rising production risks locking in fossil reliance. Environmental groups, including the Sierra Club, called the plan inconsistent with a 1.5°C pathway. Exxon responds that the world will need oil and gas for decades and that its strategy balances supply security with emissions reduction. Reuters reported split investor and market reactions when the plan surfaced.

- MUST READ: Oil Giants Under Fire: ExxonMobil Fights Climate Laws as TotalEnergies Found Guilty of Greenwashing

Investor Radar: Metrics to Track Exxon’s Low-Carbon Rollout

ExxonMobil links the pace of low-carbon roll-out to policy, permitting, and market formation. Key near-term items to watch include:

- Final investment decision and execution of the 1.0 GW / 3.5 MTA project in 2026.

- Gulf Coast CCS volumes will actually be placed into service in 2026–2030.

- Methane-intensity disclosures in 2026 to confirm earlier achievement claims.

Market analysts noted Exxon’s plan targets improved earnings and cash flow through 2030 while retaining tight capital discipline. Some news channels highlighted that the company raised its earnings and cash-flow outlook to 2030 without raising total capital allocation.

The post ExxonMobil’s $20B Low-Carbon Bet in 2030 Plan: Big Emissions Cuts, Bigger Oil Production appeared first on Carbon Credits.

As electricity demand rises and renewable energy grows in the U.S., battery storage is key. Waymo has launched a battery repurposing program to give retired electric vehicle (EV) batteries a new purpose in the power sector.

Waymo is working with B2U Storage Solutions to turn used batteries from its all-electric fleet into large-scale energy storage systems. Instead of recycling these batteries after use, Waymo will repurpose them to store electricity and support local power grids.

This program reflects a commitment to the circular economy, keeping products useful before recycling.

Adam Lenz, Head of Sustainability & Environment at Waymo, said:

“Our shared fleet of EVs provide a massive opportunity to support the growth of clean energy on the electricity grid while expanding the circular economy. Through this partnership, we can repurpose our batteries for local grid storage and ensure our batteries continue to provide economic and environmental value to the community long after they’ve retired from the road.”

Turning Old EV Batteries Into Energy Assets

EV batteries often retain significant storage capacity after their driving days. While their performance may drop for vehicles, many can still serve well in energy storage projects.

The press release says that retired Waymo batteries will join grid-connected energy storage systems through this partnership. These systems will store electricity from renewable sources like solar and wind.

During peak renewable generation, especially when solar production is high, the batteries will absorb excess electricity. Later, when demand increases in the evening, this stored energy can flow back into the grid.

This process helps balance electricity supply and demand, making renewable energy more reliable.

B2U specializes in second-life battery storage technology. They will manage the batteries during their second use and ensure proper recycling when they reach the end of their life.

Here’s a picture to show how B2U’s storage works.

This collaboration creates a complete lifecycle pathway for EV batteries—from vehicle use to energy storage and finally recycling.

Supporting Growing Demand for Battery Storage

This initiative comes at a time of rapid growth in renewable energy and battery storage in the U.S.

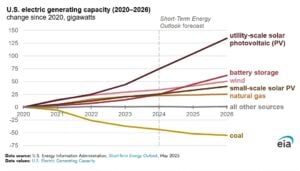

- According to the U.S. Energy Information Administration (EIA), developers plan to add 86 gigawatts (GW) of new utility-scale electricity generation capacity by 2026. If completed, it would be a record increase.

Solar energy will account for over half of these additions, with battery storage the second-largest category. Wind energy also plays a significant role in this growth.

In 2025, the U.S. power sector added 53 GW of new capacity, the highest since 2002. Meanwhile, battery storage installations keep increasing.

- They also expect to add about 24 GW of utility-scale battery storage in 2026, surpassing the previous record of 15 GW installed in 2025. Over the last five years, more than 40 GW of battery storage capacity has been added to the grid.

Texas, California, and Arizona are expected to account for around 80% of the planned battery storage in 2026.

The Grid Advantage of Reusing EV Batteries

Repurposing EV batteries offers crucial benefits for power systems and communities.

First, it extends the useful life of battery materials. Making lithium-ion batteries requires a lot of critical minerals and energy. Second-use batteries maximize the value of those materials.

Second, second-life batteries can lower energy storage costs. Since the batteries have already served in transportation, utilities can access storage capacity at lower costs than buying new systems.

Third, repurposing helps reduce electronic waste. Companies can keep batteries in use for several more years, easing pressure on waste management.

- Most importantly, battery storage boosts grid reliability. Renewable sources like solar and wind don’t produce electricity constantly. Energy storage systems fill this gap by storing power when production is high and delivering it when demand rises.

As renewable energy grows, these storage systems will be vital for stable electricity networks.

Freeman Hall, CEO of B2U Storage Solutions, said:

“This agreement marks a significant milestone in B2U’s mission to provide integrated repurposing services to the automotive industry. By extending the use of these batteries as grid storage, we are monetizing the full potential of EV batteries, now providing crucial stability to the power grid as energy demand continues to grow.”

First Deployments Planned for Texas and California

The first battery storage projects in the Waymo-B2U partnership will focus on Texas and California. Waymo already provides public autonomous ride-hailing services in these states.

Both states lead in renewable energy deployment. California increasingly relies on clean electricity and often has periods where renewable generation exceeds demand. Texas continues to lead the nation in new solar installations.

Waymo plans to repurpose old EV batteries into stationary storage systems. This will help manage renewable energy growth and improve local electricity infrastructure.

The company believes this initiative could deploy hundreds of megawatts of storage capacity in these regions. As autonomous EVs retire, their batteries could continue to provide value long after leaving the road.

This partnership shows how transportation electrification and clean energy can work together. Instead of viewing used EV batteries as waste, Waymo and B2U are transforming them into valuable energy assets. These assets support grid reliability, renewable energy integration, and a sustainable circular economy.

Waymo’s Broader Sustainability Efforts

The battery repurposing program is part of Waymo’s larger sustainability strategy. The company operates one of the largest fleets of fully autonomous electric vehicles, providing over 500,000 paid EV trips each week. These trips help cut emissions by replacing conventional vehicles with electric ones.

- Waymo estimates that every 500,000 weekly trips prevent about 530 tons of carbon dioxide emissions.

It also measures emissions avoided through its autonomous electric service. This framework evaluates the environmental benefits of electric, autonomous, and shared mobility solutions.

Additionally, the company reports its greenhouse gas emissions through parent company Alphabet as part of broader environmental efforts.

The post Waymo and B2U Unlock a Second Life for EV Batteries with Grid-Scale Storage appeared first on Carbon Credits.

Carbon removal is moving beyond pilot projects. A new agreement between JPMorgan Chase and Charm Industrial shows how the sector is entering a new phase. The deal combines carbon removal credit purchases with financing support, helping expand future supply while reducing project risk.

Under the agreement, JPMorgan will purchase 61,500 metric tons of carbon removal credits from Charm Industrial. The bank will also provide financing support to help the company grow its operations.

The deal highlights a broader trend. Large financial institutions are starting to view carbon removal not only as a climate tool but also as a market with long-term growth potential.

As net-zero deadlines approach, demand for high-quality carbon removal credits is rising. Companies are looking for solutions that deliver measurable climate benefits and long-term carbon storage.

Taylor Wright, Head of Operational Sustainability at JPMorganChase, remarked:

“Our initial purchase with Charm marked an important step as we expanded our ambition in carbon removal and refined how we assess quality and deliver real impact across our portfolio. This new purchase—bringing our total to 90,000 tons—together with financial support from our business, reflects how our portfolio has matured over time and Charm’s track record of delivering measurable, durable outcomes across its projects.”

Carbon Removal Becomes a Bigger Part of Net Zero

Carbon dioxide removal (CDR) is different from traditional carbon offsets. Many offsets focus on avoiding emissions. Carbon removal takes carbon dioxide out of the atmosphere and stores it for the long term.

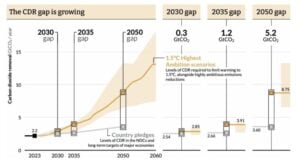

Most climate experts agree that emissions cuts alone will not be enough to meet global climate goals. According to the Intergovernmental Panel on Climate Change (IPCC), most pathways that limit warming to 1.5°C require large-scale carbon removal.

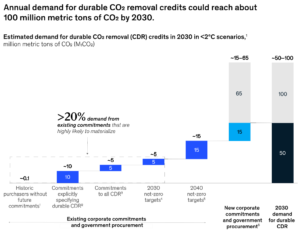

Today, the novel technological market remains small. Global demand for these engineered carbon removals is still below 10 million metric tons per year, according to CDR.fyi.

However, the State of Carbon Dioxide Removal Report shows that total global removals—mostly from forestry—already sit at 2.2 billion tons. Looking forward, IPCC climate pathways project that total global demand will need to reach billions of tons annually by mid-century to meet net-zero targets.

That growth is expected to come from sectors such as aviation, steel, cement, and shipping. These industries are difficult to fully decarbonize and will likely need carbon removal to address remaining emissions. Thus, investors and financial institutions are paying closer attention to the sector.

Inside JPMorgan’s Growing Climate Strategy

The agreement also fits JPMorgan’s broader climate strategy. The bank has committed to aligning key parts of its financing portfolio with net-zero emissions by 2050. It has also set emissions reduction targets across sectors including power generation, oil and gas, aviation, shipping, and automotive manufacturing.

In addition, JPMorgan has pledged to finance and facilitate more than $2.5 trillion toward sustainable development initiatives by 2030. That includes $1 trillion dedicated to climate action and green solutions. Carbon removal is becoming an important part of those efforts.

Many companies can reduce most of their emissions through clean energy, efficiency improvements, and new technologies. However, some emissions are likely to remain. Carbon removal is expected to help address these residual emissions.

The structure of the JPMorgan-Charm deal is also notable. Instead of only purchasing carbon credits, the bank is helping support future production capacity. This approach gives developers access to capital while helping buyers secure future carbon removal supply.

Peter Reinhardt, CEO and Co-Founder of Charm Industrial, stated:

“JPMorganChase is helping build the infrastructure for a permanent carbon removal industry. Having a sophisticated, mission-aligned financial institution come back for a second, larger purchase while also stepping up with growth capital is exactly the kind of validation that tells us we’re on the right path.”

Charm’s Way: Turning Farm Waste Into Permanent Carbon Storage

Charm Industrial uses a process known as biomass carbon removal and storage. The company collects agricultural waste, including crop residues that would otherwise decompose or be burned. It converts this material into a carbon-rich bio-oil through a process called fast pyrolysis.

The bio-oil is then injected deep underground for long-term storage. This method is designed to keep carbon locked away for hundreds or even thousands of years.

One advantage is that the process can use existing energy infrastructure. Storage wells, transportation systems, and other equipment already used in the energy sector can often be adapted for carbon storage.

Charm has become one of the leading companies in the sector. The company says it has already delivered more than 150,000 metric tons of carbon removal to customers, making it one of the world’s largest suppliers of durable carbon removal credits.

While the technology continues to develop, many experts see biomass carbon removal as one of the more mature engineered carbon removal pathways available today.

The Carbon Removal Supply Crunch Is Emerging

Corporate demand for carbon removal continues to increase. Technology companies have been among the biggest buyers. Many have net-zero goals and are looking for ways to address emissions that cannot be eliminated through renewable energy or operational improvements.

Programs such as Frontier have also helped accelerate the market. The initiative, backed by major technology companies, commits funding to help scale carbon removal technologies.

Yet, supply remains limited. Novel or engineered solutions contribute only 0.1%, roughly 2.2 million metric tons, to the physical supply.

Analysts at McKinsey estimate global demand for carbon removals could reach 100 million metric tons per year by 2030 and grow 100-fold by 2050. Current delivery volumes are only a small fraction of that level. CDR.fyi data shows only 1.5 million metric tons were delievered as of June 2026.

This gap between supply and demand is pushing buyers to sign long-term agreements years before credits are delivered. That trend is creating new opportunities for financing and investment.

Why Capital Could Unlock the Next Wave of Growth

One of the most important aspects of the JPMorgan-Charm agreement is the financing component.

Carbon removal projects often need large upfront investments. Companies must build infrastructure, secure storage sites, and establish monitoring systems before generating significant revenue.

New financing models are helping address this challenge. These include:

- Long-term carbon removal purchase agreements,

- Advance market commitments,

- Project financing backed by future credit deliveries, and

- Blended finance structures that combine different sources of capital.

The approach resembles the early growth of renewable energy. Long-term power purchase agreements helped wind and solar developers secure financing and expand rapidly.

Many industry observers believe carbon removal could follow a similar path. The involvement of a major institution like JPMorgan suggests the market is beginning to mature.

From Climate Niche to Investable Market

The JPMorgan-Charm Industrial agreement shows how climate finance is evolving. Companies are no longer focused only on buying carbon credits. Increasingly, they are investing in the systems needed to produce those credits at scale.

Most net-zero pathways still require large amounts of carbon removal to balance emissions from hard-to-abate industries. The challenge now is building enough capacity to meet future demand.

Technology is advancing. Corporate demand is growing. Financing is becoming more available. Together, these trends are helping move carbon removal from a niche climate solution toward a larger and more established market.

The post JPMorgan Backs Carbon Removal Growth With New Charm Industrial Deal appeared first on Carbon Credits.

Carbon Footprint

SMRs Set for Breakout: Global Nuclear Capacity Forecast to Jump Nearly Sixfold by 2030

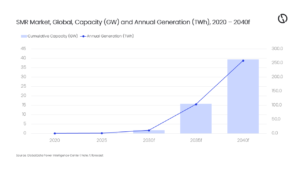

Small modular reactors (SMRs) are moving from concept to commercial reality. A new forecast from GlobalData suggests global SMR capacity could increase nearly sixfold between 2025 and 2030.

The projection reflects rising confidence in advanced nuclear technology as countries search for reliable, low-carbon electricity. This demand is being driven by electrification, artificial intelligence (AI), data center growth, and industrial decarbonization.

For years, SMRs were seen as a long-term idea. That view is now shifting. Governments are updating nuclear policies. Regulators are speeding up licensing reviews. Utilities are forming partnerships with technology developers.

At the same time, electricity demand is rising sharply, strengthening the case for firm power sources capable of operating 24/7. This momentum comes as countries try to meet net-zero targets while also ensuring stable and affordable energy supplies.

Why SMRs Are Gaining Momentum

SMRs are nuclear reactors that typically produce up to 300 megawatts (MW) of electricity per unit. Unlike large nuclear plants, they are designed to be built in factories and assembled on site.

Supporters say this modular approach can reduce construction time, improve cost control, and make deployment more flexible. SMRs can also be added in phases, depending on demand growth.

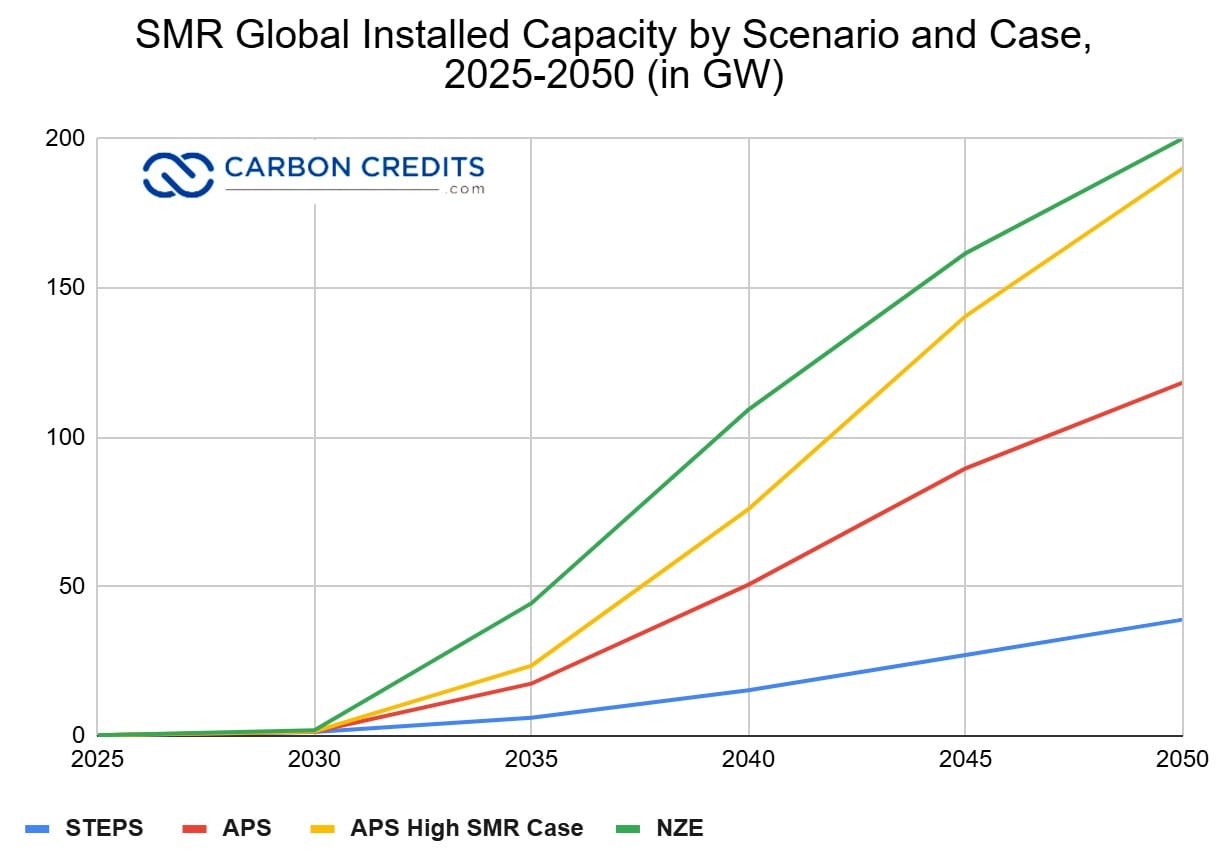

GlobalData’s forecast reflects a wider revival in nuclear energy. The firm expects global nuclear capacity to grow steadily over the next decade, by almost sixfold from 2025 to 2030. That increase could even reach a hundredfold by 2040. Cleaner energy goals, policy backing, and increasing demand for stable baseload electricity will support this growth.

The International Energy Agency (IEA) also expects strong long-term growth. In its Announced Pledges Scenario, the IEA predicts over 1,000 SMRs to be used worldwide by 2050. This would add up to about 120 gigawatts (GW) of capacity. It also estimates SMR investment could rise from about $5 billion today to more than $25 billion by 2030.

Meanwhile, major SMR projects are moving forward. GE Hitachi’s BWRX-300 design will be used at Ontario Power Generation’s Darlington site in Canada. This is one of the most advanced SMR projects currently in planning.

Holtec International is also advancing plans to install SMR-300 reactors at the Palisades site in Michigan. The company has outlined a long-term vision that could scale SMR capacity across North America to as much as 10 GW in the coming decades.

These early projects are important. They will test cost, speed, and performance. Their results will help determine how quickly SMRs can scale globally.

Nuclear Power’s Quiet Climate Comeback

As countries move toward net-zero targets, nuclear energy is receiving renewed attention as a low-emissions power source.

According to the IEA, nuclear is the world’s second-largest source of low-emissions electricity after hydropower. In 2024, more than 410 reactors in over 30 countries supplied about 9% of global electricity. Nuclear also generated more low-carbon electricity than wind and significantly more than solar.

- Since 1971, nuclear power has helped avoid roughly 72 gigatonnes of carbon dioxide emissions by reducing reliance on fossil fuels.

This climate contribution is becoming more important as electricity demand rises and countries retire coal plants. The IEA expects global nuclear generation to reach a record high in 2025, supported by reactor restarts in Japan, maintenance work in France, and new builds in Asia.

More than 60 reactors are currently under construction worldwide, adding over 70 GW of new capacity.

SMRs could strengthen this role further. Their smaller size makes them suitable for regions where large nuclear plants are not practical. They may also replace aging coal plants by using existing grid infrastructure.

In addition, SMRs are being considered for industrial uses such as hydrogen production, mining, and heavy manufacturing, where steady heat and power are required.

Big Tech and Data Centers Drive New Power Demand

One of the strongest drivers for SMR growth is the rapid expansion of artificial intelligence and data centers. AI systems require large amounts of electricity. Training and operating these systems depend on high-performance computing infrastructure that runs continuously. This is pushing electricity demand higher in key technology hubs.

Goldman Sachs has raised its forecast for AI-related capital spending by major hyperscalers. The bank now expects Meta, Microsoft, Amazon, and Alphabet to invest about $5.3 trillion between 2025 and 2030, up from a previous estimate of $4.5 trillion. A large share of this spending will go into AI infrastructure, data centers, and supporting energy systems.

Moreover, Goldman Sachs Research estimates global data center electricity demand could increase by as much as 165% by 2030 compared with 2023 levels.

This surge in demand is changing energy planning. While renewable energy remains central to corporate climate strategies, many technology companies are also looking for stable, round-the-clock power sources.

SMRs are increasingly viewed as a potential solution because they can provide constant power without weather dependence. Unlike wind or solar, nuclear plants can operate day and night continuously. This reliability is becoming more important as AI workloads grow and grids face higher stress.

As a result, several SMR developers are now targeting data center operators as future customers, alongside traditional utilities.

The First Wave of SMR Projects Breaks Ground

The SMR industry is now entering a more practical phase, with several flagship projects moving toward construction and deployment.

In Canada, Ontario Power Generation is advancing the first commercial deployment of GE Hitachi’s BWRX-300 reactor at the Darlington site. This project is widely seen as a key test case for SMR commercialization in North America.

In the United States, TerraPower continues development of its Natrium reactor in Wyoming. The project, backed by Bill Gates, combines nuclear generation with advanced energy storage. This design aims to improve flexibility and help balance electricity grids with growing renewable energy penetration.

These developments mark an important shift. The industry is moving beyond design and licensing discussions and into construction, financing, and real-world deployment.

The Roadblocks on the Nuclear Revival Path

Despite strong momentum, SMRs still face major challenges.

- Cost remains the most important issue. Early projects must prove that factory-based construction can reliably reduce total costs compared with traditional nuclear plants.

- Regulatory approval is another barrier. Even though licensing frameworks are improving, nuclear projects still require long review timelines in most countries.

- Fuel supply is also a concern. Many advanced SMR designs depend on high-assay low-enriched uranium (HALEU), but global supply chains are still limited.

- There are also broader concerns around nuclear waste management and public acceptance, which continue to influence project timelines in several regions.

These challenges explain why some analysts remain cautious about near-term deployment, even while long-term forecasts are becoming more positive.

Outlook: A Defining Decade for SMRs

The next five years could be decisive for SMRs. Global momentum is being driven by several overlapping trends. Electricity demand is rising. AI growth is accelerating. Countries are committing to net-zero targets. Energy security has become a national priority. At the same time, nuclear technology is improving.

GlobalData’s forecast of a nearly sixfold increase in SMR capacity by 2030 reflects growing confidence that the sector is approaching commercial scale.

While SMRs are still in the early stages of deployment, progress in Canada, the United States, China, and other regions suggests the industry is moving closer to wider adoption.

If current projects succeed, SMRs could become an important part of the global low-carbon energy mix. They may help support grid stability, reduce reliance on fossil fuels, and provide the steady power needed for a more electrified and digital economy.

The post SMRs Set for Breakout: Global Nuclear Capacity Forecast to Jump Nearly Sixfold by 2030 appeared first on Carbon Credits.

-

Climate Change10 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases10 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy8 months ago

Renewable Energy8 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases11 months ago

嘉宾来稿:探究火山喷发如何影响气候预测