Tungsten, a critical mineral with unmatched heat resistance and strength, is gaining global attention. It’s dense, brittle, and grayish-white, with the highest melting point and tensile strength of any pure metal. These traits make it vital for high-performance applications. and industries needing extreme durability.

With China controlling most of the supply, the U.S. and allies are racing to secure domestic sources and diversify supply chains. Let’s deep dive into the complete outlook of the tungsten market below:

Demand Drivers: Why Tungsten Keeps Rising in Importance

The tungsten market expanded from USD 6.04 billion in 2024 to USD 6.50 billion in 2025. It is projected to grow at a CAGR of 7.95%, reaching USD 11.16 billion by 2032.

Its demand is rising due to industrial and defense needs. Key drivers include:

- Electronics & Semiconductors: Vital for high-performance chips and circuits.

- Defense & Aerospace: Used in rocket nozzles and armor-piercing ammunition. It also strengthens steel alloys for aerospace and defense.

- Tungsten is used in turbine blades and as a lead substitute in ammunition.

- Industrial Tools: Crucial for cutting and drilling in mining, construction, lighting, welding, and manufacturing.

- Green technology and electrification: Increasing use of tungsten in electric vehicle batteries, energy storage, and renewable energy technologies

Industry experts are indicating that global tungsten demand is expected to rise in 2025 and the next few years. With geopolitical tensions increasing, the U.S. and allies anticipate further growth as supply diversification becomes essential.

China’s Tight Grip on Tungsten Supply

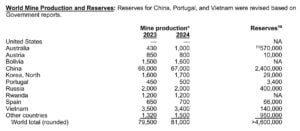

Tungsten is found worldwide, but most supply comes from China. It produces over 80% of global tungsten and holds more than half of the known reserves. Vietnam and Russia follow, contributing only a small share. Other producers like Spain, Austria, Bolivia, and Rwanda account for just 1% to 2% each.

Interestingly, other countries own about 35% of global reserves but produce only 1%. This gap shows growth potential but highlights challenges like high costs and long permitting times.

China also controls production. In late 2024, Beijing introduced new export licensing rules for tungsten, tightening supply further. Analysts view these controls as part of China’s strategy in global trade.

Global Push for Supply Chain Resilience

China’s dominance has raised concerns. Countries are diversifying their tungsten supply chains. New projects in Australia, South Korea, Canada, and Africa show promise, but scaling up will take years.

Vietnam, Russia, and Spain are boosting production. Smaller nations like Rwanda are gaining attention for their resources. However, these efforts face high costs and technical challenges.

China’s market control is expected to last until the early 2030s, but momentum is shifting toward more resilient supply options.

U.S. Tungsten Dependence: A Strategic Risk for Defense

As per the U.S. Geological Survey, the U.S. has not mined/ tungsten since 2015. It relies mostly on imports, especially from China. Notably, in 2023 U.S. imported over 10,000 metric tons of tungsten.

Most U.S. tungsten is used in cemented carbide parts for construction, mining, and drilling. The rest goes to specialty steels, defense alloys, electronics, and chemicals.

This dependence poses serious risks as tungsten is vital for defense applications, including armor-piercing munitions and missile systems. Thus, supply disruptions could threaten U.S. military readiness and high-tech industries.

DoD’s Big Investments and New Rules

The U.S. Department of Defense (DoD) is boosting efforts to secure tungsten, a critical metal for defense systems. Since last year, it has directed millions toward U.S. and allied projects.

In July 2025, it awarded $6.2 million under the Defense Production Act to Golden Metal Resources for the Pilot Mountain project in Nevada, the largest undeveloped tungsten deposit in the U.S.

The project aims to restore domestic production, reduce reliance on China’s 80% market share, and prepare for the 2027 ban on China- and Russia-sourced tungsten in defense contracts.

Procurement Rules

A new U.S. law prevents the Pentagon from sourcing tungsten, magnets, and other critical materials from adversarial nations like China, Russia, Iran, and North Korea. By January 2027, these rules will also cover the mining stage. This means tungsten mined in these countries can’t enter U.S. defense supply chains.

Thus, the U.S. Department of Defense now views tungsten as a national security issue. In summary, its strategy focuses on:

- Diversifying supply chains beyond China.

- Funding domestic exploration and allied projects.

- Expanding metallurgical testing and engineering studies.

- Tightening procurement rules to phase out adversarial tungsten by 2027.

This effort demonstrates a strong commitment to boosting domestic tungsten production for new defense systems and advanced manufacturing. Additionally, it also aims to build secure supply partnerships with allies.

Top Tungsten Stocks Gaining Investor Attention

In 2025, tungsten stocks are attracting attention as the metal becomes essential across industries. Rising demand and tight supply make these stocks appealing. Investors value tungsten for its strategic role in technology and its relatively stable prices compared to other critical minerals.

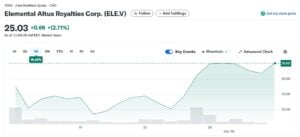

Elemental Altus Royalties Corp. (ELE.V) Rises on Strong Momentum

Canada-based Elemental Altus trades around $15.76 USD (OTC) and CAD 24.37 (TSX Venture) as of October 2025. Its shares climbed nearly 47% in six months, outperforming peers, with a market cap of $388 million USD. Analysts set the TSX target price at CAD 25.92, signaling upside potential.

In September 2025, it merged with EMX Royalty to form Elemental Royalty Corp. Tether Investments backed the deal with $100 million USD to buy 75 million shares at CAD 1.84 each. The capital fuels growth, acquisitions, and expansion in tungsten, rare earths, and other critical minerals.

Elemental Altus leads in the critical minerals’ royalty space, with strong stock momentum and strategic investments positioning it for growth.

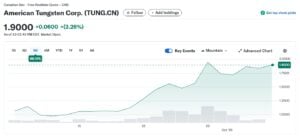

American Tungsten (TUNG) Fuels U.S. Supply Revival

American Tungsten Corp. (TUNG) is gaining attention as a pure-play tungsten stock. In February 2025, it hit an all-time high of CA$2.37, reflecting strong investor confidence in the company’s efforts to develop domestic tungsten resources.

Currently, it is trading at around CAD 1.84 per share. Analysts forecast the stock to rise through the rest of 2025 and into 2026.

With a market capitalization of roughly CAD 25.72 million, the stock has experienced some volatility. This was influenced by critical minerals sector trends and tungsten market dynamics.

However, the company’s performance remains closely tied to progress in U.S. tungsten projects, government support, and global supply-demand trends.

In March, the company announced that its application to join the U.S. Defense Industrial Base Consortium (DIBC) had been approved. The consortium, managed by Advanced Technology International (ATI) for the Department of Defense (DoD), connects private-sector companies with the U.S. Government to strengthen the defense supply chain.

Another key development is the IMA Mine Project in Lemhi County, Idaho, a major step in restoring U.S. tungsten production. This critical mineral supports tank armor, hypersonic weapons, submarine hulls, and semiconductors.

The Rise of Tungsten Juniors

However, this year, several junior mining companies focusing on tungsten in the U.S. are also gaining attention, particularly those developing critical mineral resources to strengthen domestic supply chains.

One such example is Patriot Critical Minerals. It owns100% of the MEGA Deposit in Elko County, Nevada, a strategically located resource that could help close the domestic tungsten supply gap.

The deposit contains approximately 19 million tonnes of mineralized material, with about 32,300 tonnes of contained tungsten trioxide.

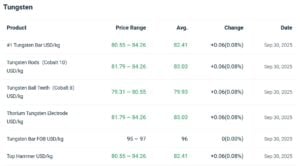

Tungsten Prices Stay High Amid Tight Supply

In September 2025, tungsten bar FOB prices held steady at USD 95–97 per kg. Meanwhile, tungsten concentrates (scheelite and wolframite) traded at RMB 284,000 per ton. This marked a 1.1% drop from peak levels but doubled the price from early 2025, showing strong market volatility.

However, global prices continue to fluctuate due to Chinese export restrictions, production issues, and rising demand in defense, aerospace, and electronics. At the same time, supply-demand gaps, geopolitical tensions, and stockpiling keep prices elevated.

In conclusion, rising demand, tight global supply, and national security concerns make tungsten a strategic mineral. Consequently, U.S. projects and companies like Elemental Altus, American Tungsten, and Patriot Critical Minerals are actively reducing reliance on China.

As production ramps up, tungsten will play an increasingly vital role in defense, technology, and industrial applications.

The post U.S. Tungsten Revival: Rising Demand, Tight Supply, and Top Stocks to Watch in 2025 appeared first on Carbon Credits.

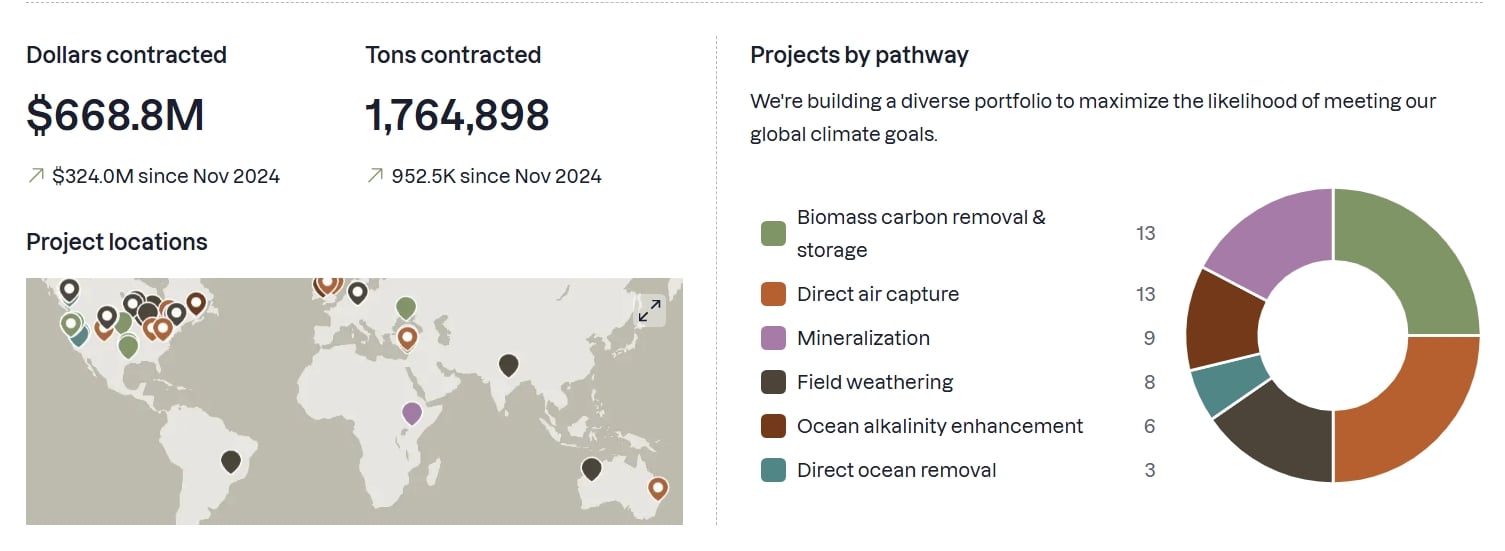

Google, Meta, and McKinsey & Company have made a major move in corporate climate action. They signed a long-term deal to remove carbon from the air in Appalachia. The project is run by Living Carbon and focuses on restoring forests on degraded lands. Under this deal, the companies will remove 131,240 tonnes of CO₂ over the next ten years.

A New Deal for Climate

The effort targets a much larger problem. Across the United States, about 1.6 million acres of abandoned mine land remain damaged by past mining. These lands often have poor soil, erosion, toxic metals, and invasive species that block natural regrowth.

In addition, around 30 million acres of degraded agricultural land could be restored through reforestation. Appalachia is one of the hardest-hit regions due to decades of coal mining.

The deal is backed by the Symbiosis Coalition, a group of buyers that funds high-quality carbon removal projects. The coalition is an advance market commitment (AMC) launched in 2024 by Google, Meta, Microsoft, and Salesforce.

The group has pledged to contract up to 20 million tonnes of carbon removal credits by 2030. This commitment aims to create strong market demand and support the growth of high-impact, science-based restoration projects that can help advance global climate goals.

The agreements they have give developers a steady demand. They also help unlock financing and allow projects to scale.

Symbiosis selected the Appalachian project after a strict review process. It looked at data, field conditions, and long-term risks. The group follows key standards such as durability, transparency, ecological integrity, and community impact. This helps ensure that every credit represents real and measurable carbon removal.

Julia Strong, Executive Director of the Symbiosis Coalition, remarked:

“Our support of Living Carbon reflects our belief that effective nature-based carbon removal requires both strong science and solid execution. Their project stands out for its rigor and for its thoughtful and scalable approach shaped around the needs of local communities, ecosystems, and economies in Appalachia.”

Why Appalachia Matters: From Coal Hubs to Carbon Heroes

The Appalachia region, in the eastern United States, was once a center of coal mining. Today, many of these lands remain unused and degraded. Living Carbon is working to restore them by planting native hardwood and pine trees on former mine sites and damaged farmland.

The project uses a mix of careful site preparation, invasive species control, and strategic planting. This helps trees grow in areas where nature cannot easily recover on its own. The goal is not just to plant trees, but to rebuild entire ecosystems and support long-term carbon storage.

The benefits go beyond carbon removal. Restoring forests improves soil health, water quality, and biodiversity. Native trees help rebuild habitats for local plants and wildlife. These changes can also reduce erosion and improve land stability over time.

The project also creates real economic value. Landowners earn lease payments from land that was once unproductive. Local workers are hired for planting and land restoration.

-

In some cases, old mining equipment is reused to support ecological recovery. This helps turn former industrial sites into productive carbon sinks.

Community engagement is a key part of the project. Living Carbon works closely with landowners, local groups, and government agencies. This helps build long-term support and ensures the project fits local needs. Strong local partnerships also improve the chances that the forests will be maintained over time.

The project stands out for its strong science and clear execution plan. It uses careful monitoring and conservative estimates to ensure carbon removal is real. It also applies new methods for tracking results, including advanced baselines and lifecycle analysis.

This type of approach shows that high-quality nature-based carbon removal can deliver more than climate impact. It can restore ecosystems, support local economies, and scale across similar regions. In places like Appalachia, it offers a way to turn damaged land into a long-term climate solution.

Big Business Bets on Carbon Credits

More corporations are now buying carbon removal credits to meet climate goals. For example, Microsoft bought 45 million tonnes of carbon removal in fiscal year 2025. This is nearly double the amount from 2024 and nine times what they bought in 2023.

These purchases are part of a broader climate strategy. Companies are combining emissions reductions with long-term removal commitments. Durable carbon removal credits, which permanently store CO₂, are becoming more important. Businesses feel pressure to deal with emissions that they cannot completely eliminate.

A major supporter of these deals is Frontier, launched in 2022 by Stripe, Alphabet (Google’s parent company), Meta, Shopify, and McKinsey Sustainability. Frontier wants to boost early demand and funding for promising carbon removal technologies.

The company does this through long-term purchase agreements. Its initial goal was $1 billion in purchases by 2030, sending a strong signal to the market about future demand.

By 2025, Frontier signed contracts for various technologies. These include bioenergy with carbon capture and storage (BECCS), direct air capture (DAC), and enhanced weathering. Several contracts are worth tens of millions of dollars. These agreements help developers survive the early “valley of death,” when financing is hardest to secure.

Market Trends: From Niche to Necessity

The carbon removal market is still small compared with global climate goals, but it is evolving quickly. Industry forecasts say that demand for durable carbon removal credits might hit 100 million tonnes of CO₂ each year by 2030.

This growth is fueled by corporate commitments and government purchases. This is roughly double the supply currently announced, showing a large gap between demand and delivery.

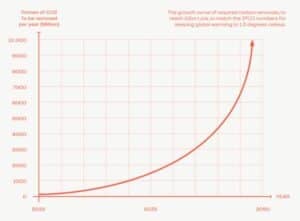

Globally, carbon removal is still a tiny fraction of what is needed. Scientific assessments show that to meet the Paris Agreement, carbon removal needs to increase. By 2050, it should reach 7–9 billion tonnes of CO₂ each year. This is about 4,000 times more than what we do now.

Market projections show strong growth in the next decade. A report by Oliver Wyman and the UK Carbon Markets Forum estimates that the global carbon removal market could grow from $2.7 billion in 2023 to $100 billion per year by 2030–2035, provided policies and standards evolve to support it.

Local and Global Wins

The Appalachia project highlights how carbon removal can benefit both the climate and communities. Restoring degraded lands improves water filtration, soil health, and wildlife habitats. Communities also gain jobs and income through forest management.

Nature-based projects, including reforestation and forest management, currently dominate removal activity. However, they do not offer the same permanence as engineered removals like BECCS or DAC, which store carbon for centuries or longer. Still, both approaches are necessary to scale the carbon removal market.

From Milestones to Market Momentum

The Google, Meta, and McKinsey deal is a milestone for corporate climate action. Long-term agreements help projects secure funding and expand. They also send strong signals to developers and investors. These deals can shift the market from short-term offsets to long-term, permanent carbon removal solutions.

The industry must grow significantly to meet global climate targets. Expanding beyond early adopter companies is essential. Continued policy support, strong standards, and wider sector participation will help scale removals.

In the next decade, how fast carbon removal technologies grow and the amount of credits produced will be key to achieving net-zero goals. Deals like the Appalachia reforestation project are early steps in building a foundational, long-term carbon removal industry.

The post Google, Meta and McKinsey Lead Carbon Removal Boom and Turn Appalachia Green appeared first on Carbon Credits.

The sustainability landscape is increasingly complex. More and more carbon-capture solutions are entering the market, and innovation is a constant thread running through the carbon market. With more possibilities, buyers are faced with more considerations than simply offsetting carbon. In this sphere, two main directions are taking shape—nature-centred or tech-focused.

![]()

Nasdaq has backed one of the first carbon removal credit deals licensed under European Union rules. The project is based in Stockholm and is designed to generate high-quality carbon removal credits under a formal EU framework.

This marks a key shift. For years, carbon markets have relied on voluntary standards with mixed credibility. Now, the European Union has developed a regulated system to define what counts as a valid carbon removal. This move aims to build trust and attract large investors into a market that is still in its early stages.

The deal shows growing interest from major companies. It also reflects rising demand for reliable ways to remove carbon from the atmosphere.

Inside the Stockholm Carbon Removal Project

The removal project is run by Stockholm Exergi. It uses a process called BECCS, or bioenergy with carbon capture and storage. This method burns biomass, such as wood waste and agricultural residues, to produce heat and electricity. At the same time, it captures the carbon dioxide released and stores it underground.

The captured CO₂ will be transported and stored deep beneath the North Sea in rock formations. Over time, it will turn into solid minerals. This makes the carbon removal long-lasting and more secure than many nature-based solutions.

The facility is expected to start operating in 2028. Once active, it will generate carbon removal credits that companies can buy to balance their remaining emissions.

Beccs Stockholm is one of the world’s largest carbon removal projects. In its first ten years, the project could remove about 7.83 million tonnes of CO₂ equivalent. This makes it a key tool for helping the European Union reach climate neutrality by 2050.

The project also aims to scale carbon removal by building a full CCS value chain in Northern Europe and supporting a growing market for negative emissions credits.

This project is important because it is one of the first to follow the EU’s new carbon removal certification rules. These rules define how carbon removal should be measured, verified, and reported. They also aim to reduce risks like double-counting and weak accounting.

EU Certification: Building Trust in a Fragile Market

The European Commission has introduced a framework, also called Carbon Removals and Carbon Farming (CRCF) Regulation, to certify carbon removal activities. This includes technologies like BECCS, direct air capture with carbon storage, and biochar.

The goal is to create a trusted system that investors and companies can rely on. It also established the first EU-wide certification framework for carbon farming and carbon storage in products, not just removals.

Until now, the voluntary carbon market (VCM) has faced criticism. Concerns about transparency and “greenwashing” have made some companies cautious. Many buyers want stronger proof that credits represent real and permanent carbon removal.

The EU framework tries to solve this problem. It sets clear rules for:

- Measuring how much carbon is removed.

- Verifying results through independent checks.

- Ensuring long-term storage of CO₂.

This structure may help standardize the market. It could also make carbon removal credits easier to compare and trade across borders. The Commission states that the goal of having the framework is:

“to build trust in carbon removals and carbon farming while creating a competitive, sustainable, and circular economy.”

Corporate Demand Is Growing—but Still Limited

Large companies are starting to invest in carbon removal. However, the market remains small compared to what is needed.

One major buyer is Microsoft. It currently holds about 35% of all global carbon removal credits, making it a dominant player in the market. In fact, it is responsible for 92% of purchased removal credits in the first half of 2025.

Other companies, including Adyen, a Dutch payments provider, have also joined the Stockholm project. These early buyers aim to secure a future supply of high-quality carbon credits as demand grows.

Ella Douglas, Adyen’s global sustainability lead, said in an interview with the Wall Street Journal:

“This project does exactly that [“catalytic impact” to the VMC] while also building key market infrastructure in collaboration with the European Commission.”

Still, many firms remain cautious. Carbon removal technologies are often expensive and not yet proven at a large scale. Some companies also worry about reputational risks if projects fail to deliver real climate benefits.

This creates a gap. Demand is rising, but the supply of trusted credits is still limited.

- SEE event: Carbon Removal Investment Summit 2026

A Market Set for Rapid Growth

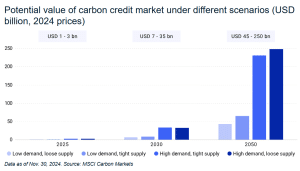

Despite these challenges, the long-term outlook for carbon removal is strong. Estimates suggest the market could reach $250 billion by mid-century, according to MSCI Carbon Markets.

Several factors drive this growth:

- First, global climate targets require large-scale carbon removal. The Intergovernmental Panel on Climate Change estimates that the world may need to remove around 10 billion metric tons of CO₂ per year by 2050 to limit warming.

- Second, many companies have set net-zero goals. These targets often include removing emissions that cannot be avoided, especially in sectors like aviation, shipping, and heavy industry.

- Third, new regulations are pushing companies to disclose and manage emissions more clearly. This increases demand for credible carbon solutions.

However, the current supply falls far short of what is needed. Only a small share of the required carbon removal credits has been developed or sold so far.

Balancing Removal and Emissions Cuts

While carbon removal is gaining attention, experts stress that it cannot replace emissions reductions. Removing carbon from the atmosphere is often more expensive and complex than avoiding emissions in the first place.

Groups like the European Environmental Bureau warn that over-reliance on credits could delay real climate action. They argue that companies should set separate targets for reducing emissions and for removing carbon.

The EU framework reflects this concern. It treats carbon removal as a tool for addressing residual emissions, not as a substitute for cutting pollution at the source. This distinction is important. It helps ensure that carbon markets support, rather than weaken, overall climate goals.

From Concept to Market Infrastructure

The Stockholm project marks a turning point for carbon removal. It shows how rules, strong verification, and corporate backing can bring structure to a fragmented market.

With support from players like Nasdaq, carbon removal is moving closer to becoming a mainstream financial asset. At the same time, the European Union’s certification system is setting the foundation for a more credible and scalable market.

The path ahead remains complex. Technologies must scale. Costs must fall. Trust must grow. But the direction is clear.

Carbon removal is no longer a niche idea. It is becoming a key part of the global climate economy, with the potential to shape investment flows for decades to come.

The post Nasdaq Invests in First EU-Certified Carbon Removal Credits from Stockholm Exergi appeared first on Carbon Credits.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits