Disseminated on behalf of SolarBank Corporation

The U.S. House of Representatives proposes rollbacks to key clean energy programs, which raises questions across the sector. Among the targeted provisions are the residential solar tax credit and funding elements of the Inflation Reduction Act (IRA)—a landmark climate package that helped spark record investment in clean energy over the past two years.

The proposal suggests ending the 30% federal residential solar tax credit by the end of 2025. This is nearly 10 years sooner than expected. This policy change could greatly affect companies in the solar industry.

Understanding the Proposed Policy Change

The residential solar tax credit, or Solar Investment Tax Credit (ITC) is Section 25D of the U.S. Tax Code. It lets homeowners claim 30% of the cost of installing solar panels. This credit appears on their federal tax returns.

The credit, part of the Inflation Reduction Act, was to last until 2032. It will start to decrease gradually in 2033. The schedule is below. However, the new proposal aims to terminate this credit by December 31, 2025.

Experts warn that this sudden change might raise costs for consumers. It could also lower demand for residential solar installations and lead to job losses in the sector. Small solar installation businesses often rely on credit for competitive pricing. This makes them especially vulnerable.

The solar industry has expressed strong opposition to the proposed cuts. Many stakeholders say the tax credit has helped grow residential solar. It creates jobs and promotes energy independence.

The Solar Energy Industries Association says the residential solar market has grown 10x in the last ten years. The tax credit has played a big part in this growth.

The proposal passed the House Ways and Means Committee. However, it still has many hurdles to clear before it can become law. Some lawmakers, including Republicans from areas that benefit from clean energy investments, are worried about the possible negative effects of the cuts.

The final outcome will depend on negotiations in both the House and Senate.

Policy Uncertainty and Its Limits

For many solar developers, these changes could signal uncertainty and disruption. For SolarBank, a developer focused on community and commercial-scale solar (as opposed to residential solar installations), the path forward remains steady. This is due to careful planning, strategic focus, and a shift in business model that favors long-term sustainability.

The company’s CEO, Dr. Richard Lu, says the company’s business model is largely shielded from this turbulence, saying:

“Over the next several years we are not expecting any major changes or challenges from the potential changes to federal solar tax incentives. Support for our community solar projects comes at a state level, and we only focus on the 22 states that have community solar policy.”

This is a key distinction. SolarBank focuses on commercial, industrial, and community solar projects. Unlike residential solar companies, it benefits from strong state mandates and incentives.

Moreover, the timeline for scaling back federal tax credits for commercial solar systems doesn’t begin until 2028 or 2029. SolarBank has already factored that into its long-term planning. Dr. Lu emphasized this, noting:

“We work with industrial and commercial large-scale solar projects, and not residential. The schedule to reduce tax incentives… has already been included in our operations to mitigate the effect.”

Resilience Through Integration

SolarBank isn’t shaken by the headlines. Instead, it is strengthening its operations. Its resilience comes from a vertically integrated model. This model covers development, construction, and long-term operations and maintenance.

This structure helps the company control costs, speed up deployment, and rely less on uncertain external factors. Dr. Lu stated:

“We have a vertically integrated system… which gives us the capability to manage our costs and simplify our process. This is really where our lean set up is competitive.”

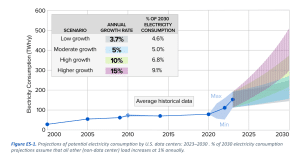

That competitiveness is especially important in a rapidly evolving energy market. AI data centers, electric vehicles, and digital industries are driving high electricity demand.

Data center power use in the U.S. will grow twofold in 2030 due to AI. Meanwhile, traditional energy systems are having a tough time keeping up.

SolarBank sees this mismatch as an opportunity. The company can meet rising energy needs by staying agile and keeping costs in check, that is faster than many big, slower competitors.

Shifting from Build-to-Sell to Build-to-Own

In response to both market evolution and policy unpredictability, SolarBank is also adjusting its core business strategy. Once focused on a build-to-sell model, the company is now emphasizing build-to-own projects.

The CEO noted that this shift aims to create a more stable revenue base, making SolarBank less reliant on one-off transactions and external funding sources. He said:

“This will boost our long-term recurring revenue. It makes it easier to take on new projects with less external funding.”

This change also helps the company hedge against potential federal funding shortfalls. SolarBank can continue to grow by attracting private investment and forming strategic partnerships. This will help, even with solar tax credit challenges.

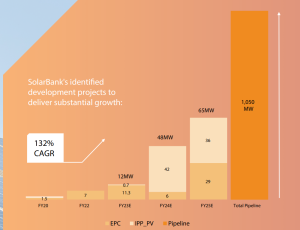

A recent collaboration with Qcells, involving the use of U.S.-manufactured solar modules, is one example of how the company is preparing for multiple future scenarios. SolarBank has the following project pipeline that will bring significant growth to the company:

A Message for Policymakers

The company is confident in its own path. However, Dr. Lu emphasized the broader value of maintaining federal support for clean energy—especially for community solar and distributed energy systems. He remarked:

“Consistent and long-term support… is not just an investment in clean energy but also in social equity and economic resilience.”

Community solar programs are especially important for expanding access to renewable energy among low- and moderate-income households, renters, and underserved communities. Without strong policy support, these groups risk being left behind in the clean energy transition.

Dr. Lu added:

“Stable policies and incentives are crucial for planning and investment. By supporting these initiatives, policymakers can drive job creation, foster local economic development, and advance national goals for carbon reduction and climate resilience.”

What’s The Future for Solar?

SolarBank’s calm response shows its strong position, even if the headlines are unsettling. The company is ready to succeed by using state support, seeking private investment, and adjusting its business model. This approach helps it thrive despite federal uncertainty.

Still, the broader industry faces real questions. Will Congress follow through with proposed rollbacks? Can community solar continue to grow if the tax credits vanish? And what does this mean for energy equity in the U.S.?

For now, SolarBank believes that its focus on fundamentals, policy-savvy expansion, and forward-thinking leadership will carry it through.

- READ MORE: SolarBank and CIM Group Announce $100M Financing to Power 97 MW of U.S. Renewable Energy Projects

This report contains forward-looking information. Please refer to the SolarBank press release entitled “SolarBank Announces Third Quarter Results” for details of the information, risks and assumptions.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

The post SolarBank Stays Strong as Trump’s Clean Energy Rollbacks Loom appeared first on Carbon Credits.

For most businesses, the emissions that matter most sit outside their own walls. Scope 3 emissions, everything generated across your value chain, from the suppliers who make your inputs to the customers who use your products, typically make up the majority of a company’s total carbon footprint. Under the Corporate Sustainability Reporting Directive (CSRD), those value-chain emissions now have to be measured and disclosed with a rigour that spend-based estimates alone struggle to satisfy. This guide sets out how to improve Scope 3 data accuracy for CSRD: the calculation methods open to you, how to move from estimates to verified supplier data, and how to govern that data so it holds up to audit.

![]()

A carbon credit is a commitment that extends well into the future. The tonne of CO₂ compensated for today from a nature-based carbon project must remain out of the atmosphere for good, which means the forest behind the credit has to remain standing long after the transaction is complete. For any buyer, this raises a defining question: What ensures that the forest endures?

![]()

What replaced the cheap REDD credit on the boardroom slide deck, and why procurement is leading the rewrite.

Three years ago, a corporate slide showing a portfolio of cheap REDD+ credits could carry a board meeting. The number was big, the price was low, and the press release wrote itself. Today, that same slide gets sent back with questions. The questions are uncomfortable, the answers are unclear, and your general counsel is suddenly in the room.

Conventional carbon offsets are not dead. The voluntary carbon market retired 202 million tonnes in 2025, and the Morgan Stanley Institute for Sustainable Investing survey published in January 2026 confirmed that interest from corporate buyers remains substantial. What changed is the credibility threshold. The integrity floor has risen, the disclosure scrutiny has tightened, and the buyer profile has shifted. This article tracks what changed, what sophisticated buyers now ask before signing, and what serious corporates are putting on the board slide instead.

What boards used to buy, and why it stopped working

The 2020 to 2022 model was simple: buy a large tranche of avoidance credits at low single-digit prices, retire them against the company footprint, announce the carbon-neutral claim, and move on. Most of those credits came from REDD+ projects, renewable energy installations in countries where the renewable energy was already economic, or methane projects with thin documentation.

Several things broke that model. Academic research published in 2023, including a widely cited Science paper, found that the majority of REDD+ credits issued under the most common methodologies did not represent additional reductions when tested against rigorous counterfactuals. The Voluntary Carbon Markets Integrity Initiative published its Claims Code of Practice, which sets requirements for what companies can credibly claim from credit use. The European Union finalised its Green Claims Directive, restricting how companies can describe products as climate-neutral. France’s Décret 2022-539 already restricts carbon neutrality advertising. California’s AB 1305 imposes disclosure requirements on any company making net-zero or carbon-neutral claims while doing business in the state.

The collective effect: the cheap credit no longer buys the announcement, and the announcement now carries litigation risk.

The integrity reset: ICVCM, VCMI, and what changed

The Integrity Council for the Voluntary Carbon Market published the Core Carbon Principles in 2023 and began assessing methodologies against them in 2024. The first methodologies received the CCP label later that year. The point of the label is to give corporate buyers a defensible quality screen they can cite in disclosure.

The Voluntary Carbon Markets Integrity Initiative complements this on the demand side. Its Claims Code of Practice defines what a buyer can say (Silver, Gold, or Platinum claims, with associated requirements) based on the quality of credits used and the underlying decarbonisation strategy. Together, CCP and VCMI build a quality stack: CCP on the supply, VCMI on the claim, with the science-based target sitting underneath both.

The reset is not a ban on offsets. It is a ratchet. Credits that meet the new bar continue to clear; credits that do not, do not. The Morgan Stanley survey found that 61% of current buyers like the CCP label concept but that supply of labelled credits remains limited. That supply constraint is now visible in pricing.

What sophisticated buyers ask before they sign

The questions on the procurement scorecard have changed. A 2022 buyer might have asked about price, vintage, and project type. A 2026 buyer asks five different questions before any of those.

- What does the counterfactual look like, and who validated it.

- What is the permanence regime, and what is the buffer pool exposure.

- What is the leakage risk, and how is it mitigated.

- What rating has the project received from the independent ratings agencies (Sylvera, BeZero, Calyx Global), and what was the rationale.

- What is the documentation discipline that survives an audit four years from now when the procurement team that signed the contract has moved on.

If the vendor cannot answer those five questions on a first call, the conversation ends. Conversely, if the vendor can answer them with documented specificity, the conversation often expands beyond a single transaction toward a multi-year engagement.

Where this leaves your near-term commitments

You probably have near-term commitments that pre-date the integrity reset. Public targets to be carbon neutral by 2025 or 2030. Product-level claims that ran in last year’s marketing. Disclosed reduction trajectories that assumed continued access to cheap credits.

You have three workable paths. The first is to re-baseline your strategy, replacing the most exposed credits with higher-quality alternatives and adjusting the public language to match what you can defend. The second is to shift the underlying spend from offsetting outside your value chain to investing inside your value chain, where reductions count against Scope 3 directly and the audit trail is cleaner. The third is to keep the strategy and absorb the risk, which is increasingly the most expensive option once you price in litigation, restatement, and reputational exposure.

Most serious buyers are choosing the second path. It moves the carbon spend from a compliance cost to a procurement and resilience investment, and it removes the central failure point of the legacy model: the disconnect between where the emissions occurred and where the reductions sat. Nature-based supply chain investments, structured under the GHG Protocol Land Sector and Removals Standard and aligned to the SBTi FLAG Guidance, are the asset class that fits this brief. They generate inventory-grade reductions, they produce audit-grade documentation, and they survive the new claim restrictions because the carbon math sits inside the value chain that the disclosure already covers.

If you are reassessing a carbon strategy under the new integrity bar, or rebuilding a board narrative that has to survive a more skeptical audience, the carbon and sustainability experts at Carbon Credit Capital can help. The Dual-Value Model gives you a defensible alternative to legacy offset purchases, with the documentation and operational integration that survives the procurement scorecard and the audit. Schedule a consultation.

Most “zombie credits” locked out of new UN carbon market after China and India snub

How to improve Scope 3 data accuracy for CSRD

Debriefed 17 July 2026: UK ‘firewave’ | Fossil-fuelled heat deaths | London’s Natural History Museum spotlights climate

-

Climate Change11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测