Extreme weather events, such as heavy rainfall, flooding and heatwaves, have been described as the “new normal” for China.

The country lost almost 12bn yuan ($1.65bn) due to heavy rainfall and floods in April – “the worst in 10 years”. In June, dozens of people were killed and some 33 rivers in China “exceeded warning levels”. The floods in Guilin, capital city of Guangxi province, were the largest in the area since 1998.

It has been less than a year since the Beijing meteorological service recorded 745mm of rain in just five days during July 2023 – roughly the same amount the city usually receives in the whole month.

The province surrounding Beijing, Hebei, also had heavy rainfall at the same time. In July 2023, the county of Lincheng recorded more than one metre of rain, twice its annual average.

In July 2021, Hebei’s neighbouring province Henan had a “one-in-a-thousand-year” rainstorm.

While China has issued more policies to improve its emergency response system and infrastructure, the increasing number of extreme weather events continues to pose challenges.

In this Q&A, Carbon Brief looks at the reasons for China’s recent floods, how the country is adapting and whether it will need to re-examine and future-proof its flood defence systems.

- What are the reasons behind the recent floods?

- What role does human-caused climate change play?

- How is China adapting to increasingly frequent flooding?

- How effective are these measures?

- What can China learn from other cities?

What are the reasons behind the recent floods?

There are various factors behind the frequent heavy rain and flooding in recent years.

Dr Oliver Wing, honorary research fellow at the school of geographical sciences, University of Bristol, tells Carbon Brief that “on the whole, we expect a warming world to be a wetter world due to the Clausius-Clapeyron relationship”.

This relationship dictates that the air can generally hold around 7% more moisture for every 1C of temperature rise, meaning rainfall is likely to be heavier in a warmer climate.

Wing notes that “for sub-daily rainfall, we are seeing even greater scaling than this relationship would suggest. This makes surface water flooding in cities [more likely] due to short-duration, intense, localised rainfall increase”.

In addition, he says, “warming is inducing a rise in sea levels in most places, meaning storm surges have a higher baseline from which to inflict damage”.

In China, “higher than normal temperatures” were behind frequent heavy rainfall in southern coastal provinces, such as Guangdong and Guangxi, since April, says Zheng Zhihai, chief forecaster at the National Climate Centre of the China Meteorological Administration (CMA), and reported in China Daily.

Zheng adds that the El Niño-Southern Oscillation – a natural climate cycle that entered its warmer El Niño phase in mid-2023 – was partly to blame because it raised sea surface temperatures and directed vast amounts of water vapour from the South China Sea and the Bay of Bengal towards southern China.

Dr Faith Chan, head of the school of geographical sciences at the University of Nottingham Ningbo China, tells Carbon Brief that the rainfall pattern in Guangdong during this April was quite similar to the intensive rainstorm on 6-8 September in 2023 after Typhoon Haikui.

Specifically, the intense rainfalls were generated by the low-pressure moist current from the south-east and south Asian monsoon pattern crashing into another low-pressure rain belt from the Philippines and the west Pacific.

Typhoon Haikui had hit Hong Kong with the worst storm in 140 years and caused some of the heaviest rains in the provinces of Guangdong and Fujian.

While these intense rainstorms, in a meteorological sense, are not unusual, they are happening more closely to one another owing to the warming world, Chan says.

Large-scale heavy rainstorms typically occur three times on average in April – the onset of a monsoon season. But, this year, China has been battered by at least eight regional extreme rain events in the month alone, all happening in quick succession.

River floods are commonly seen in the affected regions, such as Chongqing and Hunan. Identifying the causes can be more complicated for river floods in general, says Wing:

“There are many modulating factors. Drier soils in a warming world may enable the land to absorb the increased rainfall, thereby mitigating any flood hazard increase. Many floods are not driven by intense rainfall, but are driven by snowmelt or low-intensity, long-duration rain falling on saturated soils. For this reason, it is not reasonable to extrapolate that increased rainfall in a warming world will lead to increased fluvial flooding.”

Chan says natural reasons “of course” enhanced the wetness, “but human-induced climate change led to the greenhouse effect and caused sea temperature to rise, which caused more storms and low-pressure rain belts. That is a fact”.

Wing agrees that “the thermodynamic impact” of human-led climate change increases the rainfall associated with storms. But, he adds:

“What we do not understand well is how anthropogenic climate change has altered the dynamics of the climate system, and where and how this either compounds or dampens the thermodynamic response.”

What role does human-caused climate change play?

Many studies have found that warmer sea surface temperatures are supercharging high-impact, back-to-back extreme rains.

The sixth assessment report (AR6) from the UN’s Intergovernmental Panel on Climate Change (IPCC) also says that human-induced climate change caused by greenhouse gas emissions contributes to ocean warming and “is likely the main driver of the observed global-scale intensification of heavy precipitation over land regions”.

In east and central Asia, under 1.5C of global warming, extreme annual daily rainfall (Rx1) and five-day accumulated rainfall (Rx5) events are projected to increase by 28% and 15%, respectively, relative to 1971-2000, according to AR6.

Similarly, it says that in China’s urban agglomerations, “an increase in global warming from 1.5C to 2C is likely to increase the intensity of total precipitation of very wet days 1.8 times and double maximum five-day precipitation”.

Prof Yang Chen of the Chinese Academy of Meteorological Sciences at the CMA tells Carbon Brief that human-caused intensification of heavy rainfall over China had been even larger than expected. He explains:

“Human-caused intensification of heavy precipitation over monsoonal China is markedly larger than expected from increases in atmospheric moisture due to warming, because of stronger feedback between latent heat releases and ascending motion within wetter storms in a warmer climate.”

Such feedback, he adds, is particularly evident in eastern China compared to other regions of similar latitudes.

A recent study in Nature also anticipates storm activity over China to become more frequent and intense as a result of warming. By the end of the 21st century, the annual average frequency of tropical cyclones on the east coast of China is anticipated to increase by 16% compared to the present day, according to the study.

Apart from climate change that is caused by human activities, poorly designed and constructed cities, as well as subsidence – caused by groundwater extraction, the weight of buildings as result of urban growth, urban transportation systems and mining activities – could also amplify floods.

Dr Kevin Smiley, assistant professor from the department of sociology of Louisiana State University tells Carbon Brief:

“Climate change is increasing the severity and frequency of extreme weather. Extra rainfall induced by climate change can be the difference between a building’s parking lot hosting puddles on a rainy day compared to floodwaters crossing the threshold of the building and causing thousands of dollars of damages.

“It’s always important to remember: climate change is anthropogenic, so this increased risk also has human-caused roots.”

How is China adapting to increasingly frequent flooding?

China has built a number of large water projects to prevent flooding, such as the south-north water transfer projects in the Yangtze river that was launched in 2002.

In the most recent “national water network construction planning outline” published by the State Council – China’s top administrative authority, the equivalent of central government – constructing “national water networks” by 2035 is among the “backbones” of future flood prevention.

The “backbones” in the document also include large hard-engineered structures on the main rivers, such as embankments, flood gates and channelised river networks, to mitigate flood risks.

Meanwhile, a study published in the journal Ocean & Coastal Management found that “nature-based solutions” have also become popular in China. The restoration and conservation of freshwater swamps, mangroves and wetlands along coastlines and river mouths are being used to provide a buffer for tidal and storm surges.

They include the Chongming Island wetland in Shanghai (Yangtze delta) and the Futian and Mai Po wetlands in Shenzhen Bay (Pearl River delta).

Another concept proposed in the planning document is to “accelerate smart development” by using the internet, data and technology to monitor and prevent floods.

The capital Beijing has incorporated data from high-definition cameras, as well as telescopes, radar maps and satellite cloud images to provide real-time hazard updates, which has improved emergency response times.

Ningbo, a port city on China’s east coast, has worked with mobile companies to analyse big data and disseminate information.

The Ministry of Emergency Management said these measures have reduced the number of deaths and missing people as a result of natural disasters by 54% over 2018-22, compared to 2013-17. The death toll continued to fall in 2023 but the number of destroyed buildings and direct economic losses rose by 97% and 13%, respectively, compared with 2018-22 levels.

In 2015, the sponge city programme (SCP) concept was written into a policy document of the Ministry of Housing and Urban-Rural Development. It was promoted across the country and 30 major cities, such as Wuhan (home to 11 million people) and Zhengzhou (home to 10 million people), were chosen to be the pilot cities.

Those sponge cities are designed to collect, purify and re-use at least 70% of the floodwaters through “green-blue facilities”, such as green roofs, permeable pavements and stormwater parks, in urban areas. The overall system was meant to resolve the issues of urban heating, freshwater scarcity and flooding all at once.

China has improved its recovery process too. In Ningbo, for example, flood victims were able to access financial compensation within an hour, using an improved online documentation process during Typhoon In-Fa in 2021.

How effective are these measures?

Chan tells Carbon Brief that China has “done very well in terms of preparation, response and recovery for flood and drought hazards” – the two most destructive types of natural disasters.

“As a global south country,” he says, referring to China as a developing country, “China has done quite well with the SCP [sponge cities programme] and the ecologically enhanced solutions for addressing climate change”.

However, Wing argues that nature-based solutions, such as SCP, can “get saturated quickly” and so “there’s a risk of their role being overstated”. He continues:

“These types of interventions are most effective for rainfall events which occur relatively regularly at low intensities. They will be quickly overwhelmed during the very intense, rare rainfall events (whose probabilities are changing rapidly in a warming world) that cause the most damage and suffering.”

In 2021, a “historically rare” rain and flood, that affected more than 14 million people and killed 398 in Zhengzhou, a showcase sponge city, highlighted the limitations of the SCP in the face of climate change.

SCP is designed to only withstand one-in-30-year rain events, says the Nature study. On top of that, it can create a false sense of security, which encourages more people to move to high-risk areas, leading to an increase in population and assets in exposed areas that require ever-increasing protection in a cycle referred to as a “levee effect”, says Chan.

The levee effect refers to the paradox whereby the construction of a flood-defence levee leads to a lowered perception of flood risks and a greater likelihood of property owners investing in their property, increasing the potential damages should the levee breach.

The effect, according to the Nature paper, is a key challenge in the densely populated Yellow River delta and Pearl River areas, which both face high risks of flooding.

Smiley says:

“Risk is realised when social vulnerabilities intersect with hazards. Vulnerabilities are social. Flood impacts are greater when social vulnerabilities are greater…Social vulnerabilities are uneven. A household with some wealth and good insurance can recover from a flooding event much faster and more successfully than a household living paycheck-to-paycheck.”

The Chinese government has allocated more than one trillion yuan ($138bn) – via a special government bond – to support the vulnerable citizens and reconstruction of areas hit by natural disasters in March this year. More than half of the funds are used for “the construction of water conservancy projects like flood control,” reported state media outlet the Global Times.

But the delivery of financial support has been questioned in the past. When Typhoon Doksuri hit China in 2023, only $2bn out of roughly $25bn in aggregate losses were underwritten, according to global reinsurer Munich Re.

In addition, the construction of those sponge cities has already cost China 1.5-1.8bn yuan ($210-250m) between 2015 and 2018. And maintenance will make this bill even larger.

The authors of the Nature paper suggest that the government should work on integrating fragmented “grey infrastructure” – built structures such as drains, pipework and pumping stations – into existing green-blue facilities, but should not rely on engineered infrastructure alone.

Dr Lele Shu, a researcher at the northwest institute of eco-environment and resources, Chinese Academy of Sciences, tells the Intellectual magazine that “the [impact of] heavy rain at the current rate cannot be mitigated through traditional engineered approaches alone”.

“Everytime there is heavy rain, the damage it causes will make headlines primarily because there are too many people living in the city,” adds Shu.

The lack of coordination between regional governments and municipalities in flood prone areas also often led to fragmented approaches to disaster management.

In the case of the Yangtze and Pearl deltas, there is a lack of delta-wide plans that “systematically zone land and prioritise investments within one unified hydrological system”, the Nature study adds.

Dr Zheng Yan, a researcher at the Research Institute of Eco-civilisation, China Academy of Social Sciences, noted in the aftermath of the 2023 Beijing flood that government bodies often look after their own jurisdiction and aim only to move the problem and divert the floods quickly, which piled pressure on cities in downstream areas.

Smiley says:

“Floodwaters don’t care about human-created boundaries by municipality, district or province. Effective urban design in one locality may lessen flood risk there, but indirectly increase risk elsewhere. Thinking collectively while centering justice means providing spatially extensive and locally attuned solutions that help all recover effectively instead of exacerbating inequalities.”

What can China learn from other cities?

As flooding is a challenge faced by cities across the world, there is a plethora of ideas and technologies that China can draw on.

The Nature paper suggests that the Yangtze and Pearl deltas, for example, could learn from the Ganges-Brahmaputra-Meghna delta and the Mekong delta to “improve their responses to regional challenges such as subsidence and erosion, by using and aligning with the underlying dynamics of the deltas that are rapidly changing in response to climate change and anthropogenic activities”.

Building a resilient society that is “proactive and forward-looking, with adequate capabilities to limit detrimental flooding impacts and timely return to the pre-disaster state” is also advocated by the paper.

Rotterdam, a Dutch delta city of 600,000 people that is surrounded by water on four sides, has built water storage facilities, such as an underground parking garage with a basin the size of four Olympic swimming pools. It has also installed green roofs and facades to absorb rainwater.

Japan has built an intricate network of concrete tunnels and vaults about 14 storeys beneath the Saitama prefecture in the outskirts of Tokyo, Japan’s capital city, that can hold more than 1,000 Olympic pools of rainwater.

Both cities’ underground flood diversion facilities are often used as a prime example of a viable flood defence system for urban cities on the frontline of climate change.

Hong Kong has a similar underground stormwater storage system beneath the sport pitches of the Happy Valley Racecourse, designed to withstand once-in-50-years flood events.

However, Chan says it is difficult to compare flood mitigation measures as each city is very different in terms of geography, demographic, densities and topography.

He tells Carbon Brief:

“But in my opinion, China’s megacities should think about using underground spaces to store the sudden extreme discharge from super intensive rainstorms…Tokyo and Rotterdam are quite wise (in that regard) for using their underground spaces.”

The post Q&A: How China is adapting to increasingly frequent flooding appeared first on Carbon Brief.

Q&A: How China is adapting to increasingly frequent flooding

More of Germany’s electricity came from wind and solar power than fossil fuels for the first time ever in 2025.

Together, wind and solar power generated 225 terawatt hours (TWh) of electricity – accounting for 44% of the total in 2025 – with just 217TWh (43%) coming from fossil fuels.

Solar and onshore wind have grown rapidly under Germany’s “Energiewende” strategy over the past two decades, as the nation transitions away from both coal and nuclear power.

Renewables have recently faced mounting opposition from the far-right Alternative for Germany (AfD) party and the current coalition government has been trying to develop new gas-power plants.

Nevertheless, Carbon Brief analysis of Energy Institute data – shown in the chart below – illustrates how wind and solar have continued growing, emerging as the nation’s largest power source.

The success of renewables in Germany mirrors the EU as a whole, which also saw wind and solar overtake fossil-fuel power generation in 2025 for the first time.

Germany has various targets in place that require a rapid expansion of wind and solar power, including cutting economy-wide emissions to net-zero by 2045.

The nation is also aiming to increase renewables’ share of electricity consumption to 80% by 2030 to achieve a “largely climate neutral” power system by 2035. It aims to decarbonise its electricity entirely once coal power has been phased out, which has a deadline of “no later than” 2038.

(The renewables targets also include electricity generated from hydropower and bioenergy. The latter produces a relatively large share of Germany’s power – roughly a tenth in 2025.)

Germany has to rely on renewables more than neighbours, such as France and the UK, to achieve its climate goals. This is due to its phaseout of nuclear power, which is a key part of the “Energiewende” strategy.

Nuclear power has long faced widespread public opposition in Germany. This year, the centre-right chancellor Friedrich Merz described the nuclear phaseout as a “strategic mistake”, but the government has ruled out a return to conventional nuclear power.

The country has an official coal phaseout date of 2038, but experts say the country is on track to eliminate coal from its power supply years earlier. This is despite some pressure to temporarily slow the transition away from coal during the recent energy crisis.

(Very few outside the AfD are calling to scrap the coal phaseout altogether, but the government will publish a review of the timelines in August.)

While coal generation has fallen quickly, even as nuclear was being phased out, some argue that coal could have been cut more quickly if nuclear had remained.

Gas-power expansion has also been framed by the government in recent years as an essential component of Germany’s transition away from coal and nuclear power, to support a renewables-heavy grid.

The current government under Merz has tried to boost gas and recently adopted a law to provide state support for new gas-fired power plants. The plan is for these plants to be converted to run on “green hydrogen” by 2045, in order to meet the climate-neutrality goal.

Germany aims to install 115 gigawatts (GW) of onshore wind by 2030 and approved a record 20.8GW of new capacity in 2025.

Meanwhile, solar generation has reached unprecedented levels during the hot summer of 2026.

However, the government’s planned grid reforms have been criticised by the renewables industry for risking slowing down the energy transition. Under the proposals, renewables developers would only be granted automatic grid connections in areas with limited grid capacity if they waive compensation for future curtailed generation.

Interview: COP31 president says electrification is ‘surest way to protect citizens’

Six charts show how clean power was world’s largest source of new energy in 2025

Guest post: How US renewable-energy growth persists despite federal policy uncertainty

CCC: Faster electrification of UK will ‘put money back into people’s pockets’

The post Analysis: Wind and solar power overtake fossil fuels in Germany for first time ever appeared first on Carbon Brief.

Analysis: Wind and solar power overtake fossil fuels in Germany for first time ever

Climate Change

Analysis: 84% of nations miss deadline to identify ‘nature-harming’ subsidies by 2025

Most countries failed to meet a 2025 target to identify all of their subsidies that could be “harmful” to biodiversity, according to Carbon Brief analysis.

The findings also reveal that 32 countries spend an estimated $270bn on biodiversity-harming subsidies and other incentives each year.

This is the “tip of the iceberg”, one expert notes, with “trillions” spent globally.

In 2022, almost every country in the world agreed on a set of “goals” and “targets” aiming to halt and reverse biodiversity loss by 2030.

One of these targets asked countries to identify all subsidies that damage biodiversity by 2025, before phasing out or reforming at least $500bn of these incentives by 2030.

The subsidies can be found in a range of sectors, including fossil fuels, agriculture, forestry, mining and fishing.

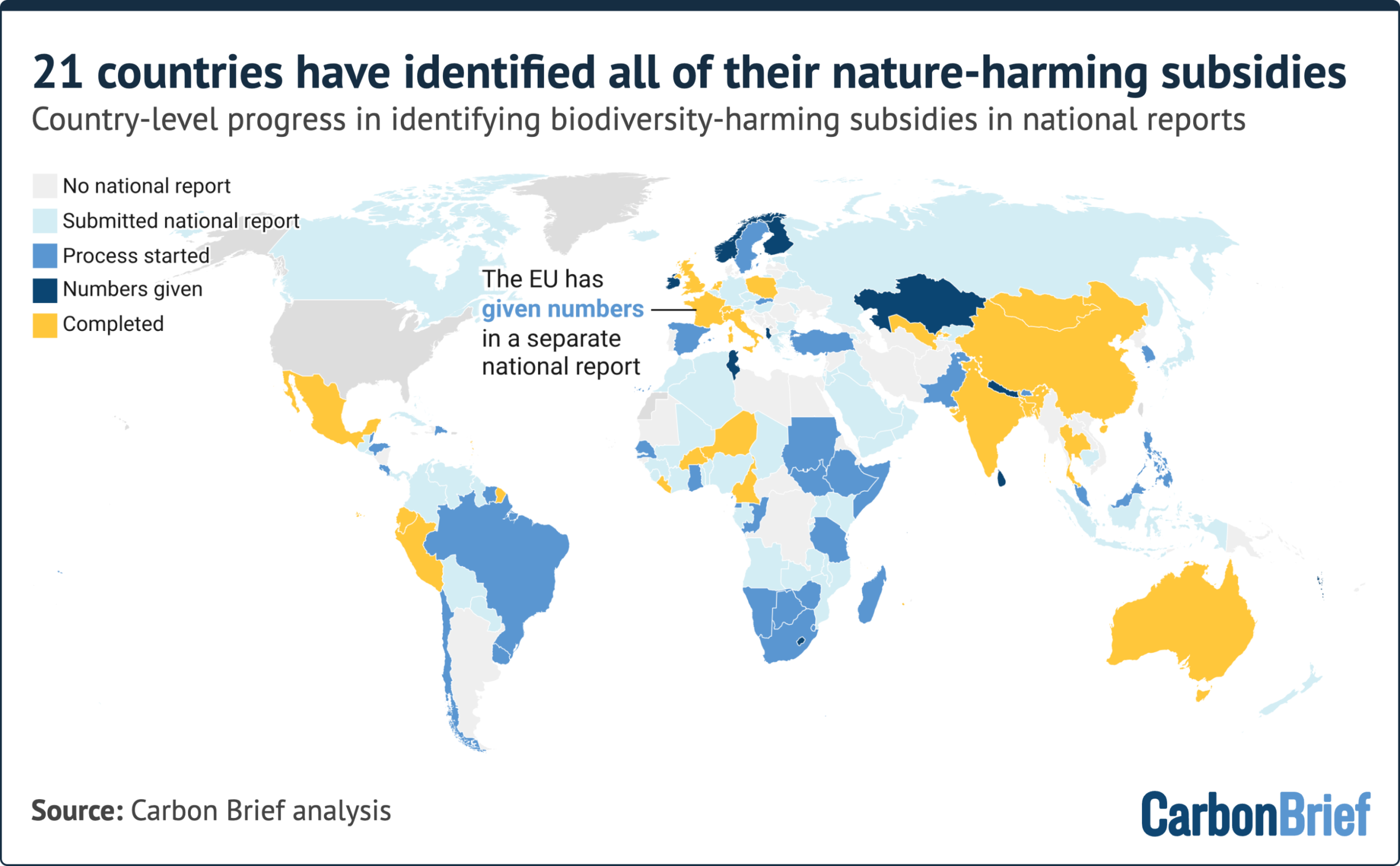

Just 21 countries appear to have met the 2025 goal, Carbon Brief finds, based on analysis of 134 national reports submitted to the UN Convention on Biological Diversity (CBD) by 1 July 2026.

Five of the world’s 17 megadiverse countries were among those that met the deadline.

Country progress

Carbon Brief’s analysis looks at the number of countries that have met the 2025 target to identify their use of nature-harming subsidies.

However, the metrics to determine which countries have “met” this target are not explicitly defined.

Carbon Brief included any country that says it has completed the process of identifying its subsidies. In almost every case, these countries also included a total figure for the value of those subsidies.

The analysis finds that 21 countries say they have identified their harmful subsidies, as shown in the map below (yellow). This amounts to 16% of the countries that have submitted national reports so far.

A further 11 countries, plus the EU, have provided figures for some of their subsidies, such as only those in a specific sector (dark blue).

Of the 134 national reports submitted to the CBD, 66 make reference to beginning the process (medium blue), while the remaining 68 do not (light blue). The final 62 countries party to the CBD have yet to submit a national report (light grey).

(Every country in the world participates in the CBD, except for the US and the Holy See – the governing body of the Catholic church, which is seated in Vatican City.)

The 32 countries that have identified some or all subsidies spend almost $270bn on nature-harming incentives annually, according to Carbon Brief’s analysis.

This is based on a tally of the figures for the most recent available year listed in countries’ national reports, in US dollars using conversion rates at the end of the given year and adjusted for inflation. The analysis also includes figures from other reports cited in the country submissions.

The $270bn reported in country submissions to date is “just the tip of the iceberg”, notes Eva Zabey, the chief executive of Business for Nature. The global figure could be as high as $1.8tn, according to a 2022 estimate from non-profit group, the B Team.

The figures identified by Carbon Brief are a “warning” that the “world is not moving fast enough” to tackle harmful subsidies, Zabey says, adding:

“The positive news is that some countries have shown it can be done and this should embolden others to follow suit…Subsidy reform should be treated as an economic necessity, not an environmental checklist.”

Harmful subsidies are expected to be among the key priorities at the upcoming COP17 UN nature summit, being held in Armenia in October 2026.

Subsidy target

There is no single definition of a “harmful” subsidy. (See: ‘Harmful’ subsidies.)

The aim to identify these subsidies stems from target 18 of the Kunming-Montreal Global Biodiversity Framework (GBF) – the global agreement containing a series of goals and targets for nature.

Target 18 calls on countries to identify subsidies and other incentives that are harmful for biodiversity by 2025.

It also says that nations should “eliminate, phase out or reform” these subsidies in a “proportionate” way, reducing them by at least $500bn per year by 2030.

It says countries should first target the “most harmful” incentives, while simultaneously scaling up positive incentives for nature.

All 2030 targets in the GBF are global – with countries each expected to outline how they will contribute nationally. So far, 169 countries have submitted these national targets.

Only 38% of countries addressed the 2025 aim to identify harmful subsidies in their national targets “to some extent”, according to a draft version of an upcoming progress report.

Countries’ national reports do not “provide a sufficient basis to determine” whether the 2025 milestone was met, says the report, but available evidence “suggests” that it was not.

‘Harmful’ subsidies

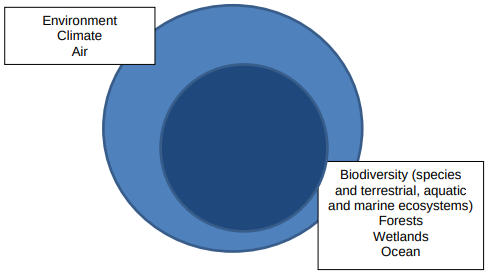

There is no universally agreed-upon definition of a “biodiversity-harmful subsidy” – or how it differs from an environmentally harmful subsidy.

In general, “harmful” environmental subsidies impact humans’ surroundings, whereas those harmful to biodiversity directly affect species and ecosystems. Paul Elton, a PhD candidate at the Australian National University, tells Carbon Brief:

“If you were to do a study that focused on biodiversity-harmful subsidies versus one that focused on environmentally-harmful subsidies, there’d be a Venn diagram where a large percentage would overlap.”

A 2022 working paper on identifying subsidies harmful to biodiversity published by the Organisation for Economic Co-operation and Development (OECD) depicted biodiversity as a subset of the environment, with climate and air falling outside the scope of “biodiversity”.

However, the report also noted that climate change is one of the five key drivers of biodiversity loss, adding:

“As such, subsidies that lead to larger greenhouse gas emissions, for example, will also indirectly impact on biodiversity.”

Prof Jessica Dempsey, a political ecologist at the University of British Columbia, tells Carbon Brief that she would “absolutely” consider fossil-fuel subsidies to be biodiversity-harming – not only as a driver of climate change, but also because the extraction of fossil fuels can cause localised harms to biodiversity. She adds:

“I do think probably it is true that all harmful subsidies are not necessarily biodiversity-related. Some care in that is important, but subsidies to the sectors that are known drivers of biodiversity loss feel very obvious to me.”

Biodiversity-harming subsidies can be either direct or indirect.

Direct subsidies refer to government expenditures that go towards a project that harms nature, such as construction of a new gas-fired power plant. Indirect subsidies could include tax exemptions that encourage a certain behaviour, such as lower tax rates on fuels for agricultural machinery.

Subsidies in agriculture, fishery and energy sectors are most commonly deemed “harmful”, but damage can also be caused by support for forestry, infrastructure, transport, construction, water and other sectors.

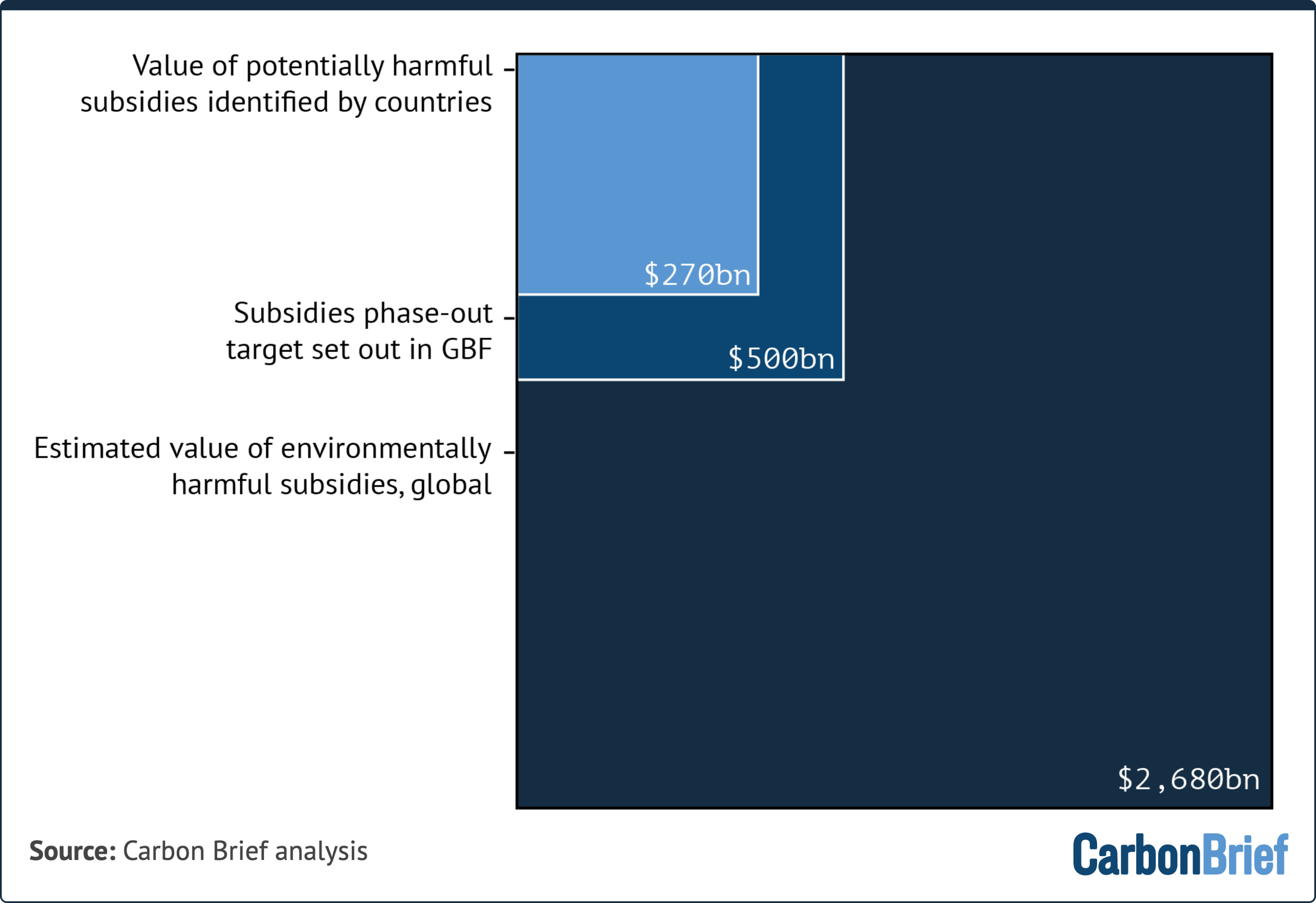

One recent estimate of the global total of biodiversity-harming subsidies put the figure at $1.7-3.2tn annually. An estimate of environmentally harmful subsidies put the figure at $2.6tn.

Elton tells Carbon Brief:

“It’s useful to contextualise the $500bn ambition of the GBF against those global estimates of how big [the total] actually could be, because that underscores the fact that so far, you’ve only got a subset of nations reporting about $250bn by your analysis, which is only half of the [phase-out target].

“It’s a significant lack of accountability.”

The chart below compares the $2.6bn estimated value of harmful subsidies to the $500bn phase-out target set in the GBF and the value of the subsidies identified so far in national reports.

Sectoral breakdown

Many subsidies can have both negative and positive impacts on biodiversity, according to the 2022 OECD working paper.

A subsidy on constructing dams for new hydropower can harm local biodiversity by disrupting water flows and flooding certain areas, for example. But it also reduces fossil-fuel dependence, lowering emissions and leading to a decrease in global warming.

Ronald Steenblik, a subsidies expert and co-author of the report estimating $2.6bn of harmful subsidies, tells Carbon Brief:

“What’s harmful is somewhat in the eye of the beholder.”

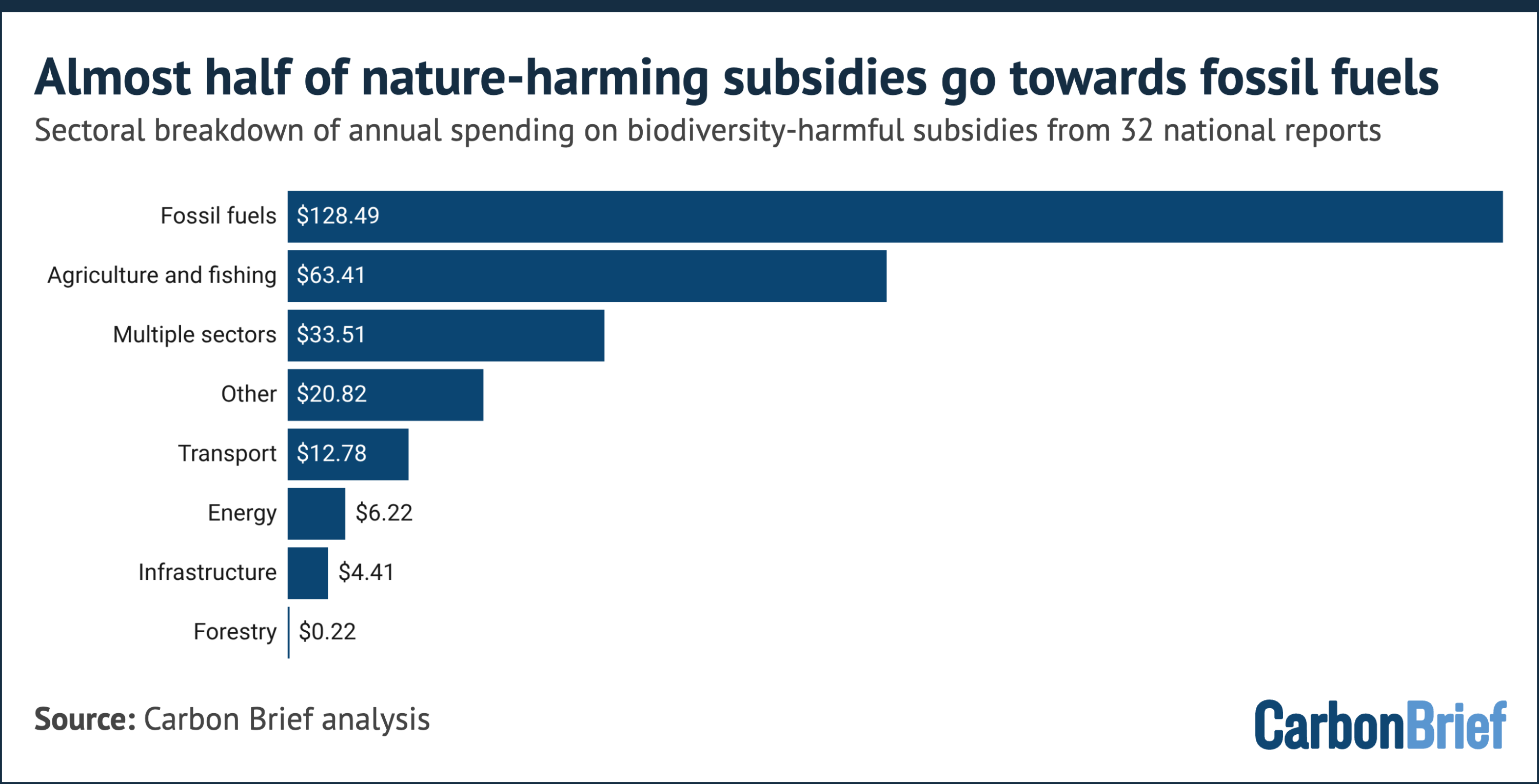

Most experts agree that a few sectors receive the bulk of the world’s biodiversity-harming subsidies: fossil fuels, agriculture and infrastructure, with much smaller contributions from other sectors, such as forestry, mining and fisheries.

Of the subsidies reported to the CBD, almost half were for the fossil-fuel sector, and around one-quarter for agriculture and fishing.

Dempsey says it is “surprising” that mining “didn’t show up” in these figures. (Of the 32 countries that provided subsidy data, only one mentioned mining as an industry that received harmful subsidies.)

Limitations

One limitation of Carbon Brief’s analysis is the lack of standardisation of subsidy data.

The methodology underlying the national reports lists several definitions of environmentally harmful subsidies, adding:

“[T]here is no standardised, globally agreed methodology for assessing the value of subsidies…nor is there a single global dataset providing this information.”

It adds that it is “important” for countries to identify harmful subsidies “within their national context”. Steenblik says:

“When you get down into the details, you can have lots of arguments of where you draw the line. And, so, the big question on this spreadsheet is where countries drew that line.”

For example, China’s national report says the country has already identified all biodiversity-harming subsidies and reformed them entirely.

In Australia, a 2026 study – led by Elton from Australian National University – identified biodiversity-harmful subsidies worth $26.3bn over 2022-23, a number that amounts to just over 1% of the country’s GDP.

However, in its national report, Australia identified $155m worth of subsidies, largely in the agricultural sector. (The national report says that the identified agricultural subsidies are those that are “potentially most harmful to the environment”.)

Elton tells Carbon Brief that this discrepancy underscores the necessity of an independent assessment of harmful subsidies, “rather than this just being seen as a tick-the-box reporting exercise by officials in the environment department”.

When it comes to actually phasing out harmful subsidies, Dempsey says, focusing on the quality of the subsidy – and who benefits from it – is just as important as focusing on the numbers. She adds:

“If we don’t take this lens of understanding the beneficiaries and we only focus on the [numbers], we really risk having policy changes that then lead to increased affordability problems for everyday working people, and backlash.”

Methodology

Carbon Brief analysed national reports submitted to the CBD by 134 parties – 133 countries and the EU – to assess which ones had identified all of their biodiversity-harmful subsidies and therefore met the 2025 deadline.

The reports were submitted in 2026, with the analysis including those submitted by 1 July 2026.

The figures for each country can be found in this spreadsheet. More than three-quarters of reports did not list any figures.

To get the full tally for the amount listed, Carbon Brief used the figures for 2025 (or the nearest available year) and converted the local currency into US dollars, based on conversion rates in the given year using the currency exchange rates calculator from the US Treasury.

These figures were then adjusted for inflation to the year 2025. Numbers were rounded to the nearest $1,000.

In total, this amounted to $269,856,769,000 in subsidies across 32 countries.

Many countries listed the sector that each subsidy is going towards. Carbon Brief standardised these inputs using the following categories:

- Agriculture and fishing

- Energy

- Forestry

- Fossil fuels

- Infrastructure

- Transport

- Other

- Multiple sectors

“Multiple sectors” was assigned when a country provided only a partial sectoral breakdown of their subsidies or none at all.

“Other” was selected to encompass sectors that were named more infrequently, including water, mining, tourism and construction.

The designations employed and the presentation of the material on the map in this article do not imply the expression of any opinion whatsoever on the part of Carbon Brief concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries.

UK withdraws millions in funding from world’s second-largest rainforest in Congo

Q&A: What England’s new ‘land-use framework’ means for climate, nature and food

Analysis: Half of nations meet UN deadline for nature-loss reporting

Brazil’s biodiversity pledge: Six key takeaways for nature and climate change

The post Analysis: 84% of nations miss deadline to identify ‘nature-harming’ subsidies by 2025 appeared first on Carbon Brief.

Analysis: 84% of nations miss deadline to identify ‘nature-harming’ subsidies by 2025

SYDNEY, Monday 27 July 2026 — In response to an announcement that Woodside’s Browse to North West Shelf (Browse) Project was declared a State Significant Project by the WA Government, the following comments can be attributed to Senior Campaigner at Greenpeace Australia Pacific, Hannah Schuch:

“The WA Government must not ignore the significant risks clearly associated with Woodside’s plans to drill for gas at the pristine Scott Reef — to endangered marine life, our oceans, and our climate — all of which are valued and relied upon by Western Australians.

“The WA Environmental Protection Authority has already found Woodside’s plans to drill at Scott Reef would have unacceptable impacts on the environment without considering the climate impacts of 1.6 billion tonnes of carbon pollution associated with this disastrous proposal.

“Woodside’s gas drilling plans, including seismic blasting and carbon dumping in the heart of a precious ecosystem, pose potentially fatal risks to pygmy blue whales and genetically unique green sea turtles, and could cause a catastrophic oil spill.

“If the WA and federal governments are concerned with the prosperity of WA, they must reject Woodside’s nature and climate-wrecking proposal to drill for gas at Scott Reef.”

—ENDS—

High res images and footage of Scott Reef can be found here.

For more information or to arrange an interview, please contact Emma Sangalli on 0431 513 465 or emma.sangalli@greenpeace.org

Cook Government must recognise risks posed by Woodside’s Scott Reef drilling plans

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测