The Voluntary Carbon Market (VCM) has been a vital tool for combating climate change, enabling organizations to offset emissions by funding projects that reduce or remove greenhouse gases (GHGs). Once viewed as a cornerstone for corporate sustainability efforts, the market is now at a critical juncture.

Challenges such as fraudulent practices, questionable project integrity, and waning buyer confidence have sparked concerns about its future. However, amid these setbacks lies an opportunity for transformation. Is the VCM truly on its last leg, or is it evolving to meet the demands of a more discerning global audience?

A Look Back: The Voluntary Carbon Market’s Evolution

What Are Carbon Credits?

Carbon credits represent the reduction or removal of one metric ton of CO₂-equivalent emissions. They are typically achieved through projects such as renewable energy, reforestation, and sustainable agriculture.

These credits are often purchased by companies to offset emissions they cannot reduce internally, allowing them to claim progress toward carbon neutrality.

The VCM differs fundamentally from compliance markets, which are regulated by governments and operate on a cap-and-trade basis. The unregulated nature of the VCM has allowed it to thrive, providing flexibility for buyers and enabling the development of innovative project categories. However, this lack of regulation has also led to vulnerabilities in accountability and standardization.

Exponential Market Growth and Who Drives It

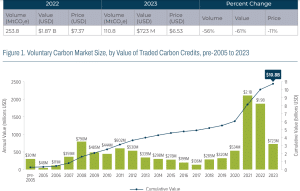

From its origins as a niche market, the VCM has grown exponentially. By 2022, it was valued at $2 billion, driven by rising corporate commitments to net-zero targets.

Projections estimate the market could balloon to up to $25 billion by 2030, representing a 15-fold growth from its current size. This expansion has been fueled by increasing pressure on businesses to address climate change and the growing adoption of sustainability frameworks.

Initially, the VCM emerged as a voluntary alternative to compliance markets, allowing companies to take responsibility for emissions beyond regulated requirements. Over the years, major corporations like Microsoft, Google, and Starbucks have leveraged the VCM to achieve ambitious net-zero goals.

Key participants in the VCM include:

- Project Developers – These entities create carbon credits through verified environmental projects.

- Consumers – Private companies, governments, and individuals purchase credits to offset emissions.

- Retail Traders and Brokers – They bundle and market credits to buyers.

- Third-Party Verifiers – Organizations like Verra and Gold Standard ensure projects meet stringent standards for emissions reduction. These also include carbon rating agencies that provide more transparency and authenticity to carbon projects.

While plenty of companies operate in the VCM, some names stand out because of their major contributions to the space.

For example, Xpansiv operates the world’s largest voluntary carbon exchange through its CBL platform, offering transparent, efficient trading of carbon credits and renewable energy certificates. The platform connects over 1,000 verified projects and partners with major carbon standards like Verra and Gold Standard.

Xpansiv’s technology enables same-day settlement and reduces delivery risks, enhancing market accessibility and liquidity. It also bridges voluntary and compliance markets, facilitating products under programs like the Regional Greenhouse Gas Initiative (RGGI) and California Cap-and-Trade.

Another key player, Laconic Global, operates at the intersection of technology and the VCM, offering solutions that improve transparency and functionality. They utilize their proprietary SADAR Natural Capital Monetization (NCM) platform to provide real-time carbon market data, including live pricing, trade analysis, and portfolio valuation tools.

Natural Capital Monetization (NCM) platform to provide real-time carbon market data, including live pricing, trade analysis, and portfolio valuation tools.

Finally, in the realm of carbon credit ratings, a London-based company, BeZero Carbon offers high specialization. It provides transparency and risk assessments for carbon markets through its BeZero Carbon Ratings. It evaluates the quality and risks of individual carbon credits, covering factors such as additionality, permanence, leakage, and policy risks.

These companies’ works are crucial to keeping the market alive and striving, despite mounting issues and challenges.

VCM’s Current Challenges and Setbacks

Integrity Under Scrutiny

The VCM has faced intense criticism for the questionable integrity of some projects. For example, certain REDD+ initiatives—aimed at reducing deforestation—have been accused of inflating baselines, leading to overestimated carbon savings. High-profile scandals, such as funds from Zimbabwe’s Kariba REDD+ project failing to reach local communities, have further eroded trust.

This scrutiny has translated into financial losses. In 2023, transaction volumes dropped by 56% from the previous year, and the market’s value plummeted to $723 million—a stark contrast to its 2021 peak of $2 billion.

In effect, average credit prices fell to $6.53 per ton, a decline that reflects reduced buyer confidence. The chart below shows dampened market sentiment since 2021 when criticisms began, with number of credits demanded (retired) and produced (issued) decreased.

Media coverage has amplified the market’s vulnerabilities, highlighting instances of greenwashing and low-quality credits. This negative attention has deterred corporate buyers, many of whom fear accusations of insincere climate action. Companies are increasingly seeking transparency and accountability in the credits they purchase, placing additional pressure on the VCM to reform.

Signs of Recovery: Building a Stronger Market

Better Standards, Better Confidence

Despite these challenges, the VCM is evolving. The introduction of integrity frameworks such as the Core Carbon Principles by the Integrity Council for the Voluntary Carbon Market (ICVCM) and the Claims Code by the Voluntary Carbon Markets Integrity Initiative (VCMI) aim to restore buyer confidence.

These initiatives emphasize project transparency, robust verification processes, and adherence to high environmental and social standards.

Standards organizations are addressing past shortcomings. Verra, for example, introduced revised baseline calculations for REDD+ projects in 2023, aimed at resolving overestimation issues. These updates signify a shift toward greater accuracy and accountability, which could help rebuild trust among stakeholders.

More Than Just Carbon: Focus on Co-Benefits

In 2023, 28% of VCM transactions involved projects offering co-benefits such as biodiversity conservation or alignment with Sustainable Development Goals (SDGs). This reflects a growing buyer preference for credits that deliver tangible environmental and social outcomes in addition to carbon reductions.

Why the VCM Still Matters

Amid all the setbacks, the long-term outlook for the VCM remains optimistic.

Echoing this outlook, Xpansiv’s COO Ben Stuart remarked that:

“Despite ongoing challenges in the Voluntary Carbon Market (VCM), recent indicators suggest continued growth and renewed signs of market confidence. Notably, total retirements have increased year-on-year from 2023 to 2024, signaling a steady commitment from existing participants and an increase in new stakeholders engaging with the market.”

He further noted that the VCM is gaining validation through various international frameworks, which is helping to address concerns about market integrity, highlighting:

Last month, at COP29, countries reached a landmark agreement on the adoption of Article 6.4… In parallel, the International Civil Aviation Organization (ICAO) has approved standards…At the national level, the VCM continues to gain traction, with countries such as South Africa, Japan, and Singapore incorporating the VCM into their domestic carbon schemes. These are renewed signs of market confidence…”

Projections indicate a compound annual growth rate (CAGR) of 31% from 2023 to 2028. Key drivers include global net-zero commitments, regulatory alignment under frameworks like the Paris Agreement, and technological advancements in carbon removal.

Technological innovations help the market bounce back as advanced data gathering and sophisticated technologies produce more transparent and reliable verification processes.

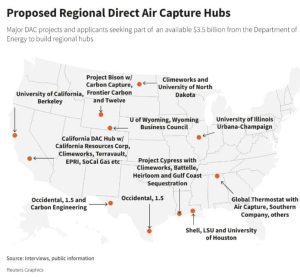

Carbon removal technologies, such as direct air capture, are gaining traction. These solutions, which physically extract CO₂ from the atmosphere, are increasingly favored for their clear and measurable impact.

In 2023, removal credits commanded a 245% price premium over reduction credits, underscoring their value in meeting net-zero targets.

Emerging Trends in the VCM

Increased Demand for High-Quality Credits and Market Integration

Buyers are increasingly prioritizing quality over quantity, focusing on credits that are rigorously verified and offer co-benefits. The share of transactions from projects with co-benefits grew from 22% in 2022 to 28% in 2023, indicating a shift toward more impactful solutions.

Moreover, the VCM is becoming increasingly segmented, with distinct markets emerging for engineered solutions, nature-based projects, and co-benefit-driven initiatives. This differentiation allows buyers to tailor their investments to align with specific climate goals and organizational values.

More notably, as regulatory frameworks under Article 6 of the Paris Agreement are finalized, the boundaries between voluntary and compliance markets are becoming increasingly blurred. This integration offers opportunities for scaling the VCM while addressing systemic issues such as double counting and project accountability.

COP29: A Turning Point for Carbon Markets

The 2024 COP29 in Baku proved pivotal for the future of carbon markets, especially after the uncertainty surrounding the potential re-election of Donald Trump. Despite this looming challenge, the outcomes at COP29 gave a much-needed boost to the climate conversation, particularly following the disappointing results at COP28.

Progress on Article 6.2 and Article 6.4

Article 6 negotiations remained a focal point, with texts on both Article 6.2 and 6.4 evolving through the first week. After extensive deliberations, the final texts were ratified late on the second Saturday of the conference. These decisions provided much-needed clarity and a clear framework for the implementation of carbon markets, marking a significant step forward after COP28’s lack of progress.

One of the most significant achievements was the establishment of clear rules for the transfer and tracking of carbon credits under Article 6.2. This mechanism, which allows for carbon credit trade between countries, is expected to drive substantial investment in climate action, particularly in developing nations.

A Historic Milestone for Carbon Markets

The final adoption of the Article 6 texts was hailed as a historic milestone for climate finance. These decisions provide developers, investors, and countries with much-needed certainty regarding how carbon credits are created and traded. The text’s adoption also set a path for the effective scaling of carbon markets, intending to contribute billions in funding for climate initiatives by the end of the decade.

Despite some pushback from carbon market skeptics, who argue that the system could provide a lifeline for the fossil fuel industry, the global community remains optimistic. The new rules aim to ensure greater transparency, reduce double counting, and enhance the accountability of carbon credits.

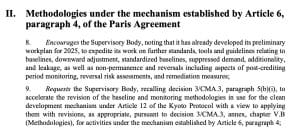

The next major milestone for Article 6 is expected in 2025 when the Supervisory Body for Article 6.4 meets to discuss further refinements. By then, the geopolitical landscape may have shifted, with a new US president potentially influencing the direction of international climate negotiations.

According to some accounts, 2025 will be the “moment of reckoning” for the VCM. Yet, given the past criticisms and current market challenges, the market has to overcome some major hurdles to move forward, as recommended by market experts.

Barriers to Address for Sustained Growth

- Regulatory Alignment: Clearer rules are needed to integrate voluntary and compliance markets seamlessly.

- Market Liquidity: Addressing the low liquidity of certain credit types is essential for maintaining market functionality.

- Trust and Transparency: Rebuilding buyer confidence through improved verification processes and independent oversight is crucial.

- Education: Buyers and the public need greater awareness of the nuances of carbon credits to combat misconceptions and rebuild trust.

Looking Ahead: Is the VCM Dead?

While the VCM has faced undeniable setbacks, it is far from dead. Instead, it is undergoing a critical transformation, driven by the need for enhanced quality and transparency. If integrity initiatives, gain traction, the VCM could emerge stronger and more impactful.

Tommy Ricketts, CEO and Co-Founder of BeZero Carbon, perfectly highlighted this, saying that:

“Carbon markets are restructuring after a turbulent couple of years. Carbon ratings, insurance, and accounting are working together to raise the bar for carbon credit quality…Market actors must recognize carbon credits for what they are: valuable but imperfect mechanisms to channel finance towards climate action. Bolstering the market for credits means buyers and market players must lean on the tools that exist to manage this risk.”

The market’s challenges underscore the importance of vigilance, innovation, and collaboration. As stakeholders refine frameworks and methodologies, the VCM holds the potential to bridge the gap between ambition and action, giving corporations and individuals the tools to fight climate change.

- FURTHER READING: COP29 Breakthrough: UN-Backed Global Carbon Market Takes Shape

The post Is the Voluntary Carbon Market Dead? appeared first on Carbon Credits.

Key takeaways

- SBTi is the default reference point for corporate climate action: 51% of Fortune Global 500 companies now hold net-zero targets, up from 8% in 2020, and over 11,000 organizations worldwide have SBTi-validated targets.

- Net Zero Standard V2 redefines climate leadership as reducing emissions and mitigating ongoing emissions, not reduction alone.

- The new standard adds flexibility through five-year cycles, a “best efforts” standard, and an Asset Transition Method for companies whose path to net-zero doesn’t fit a straight-line trajectory.

- Voluntary carbon credits are formally recognized for the first time, with reduction and removal credits accepted from 2027, and removals required from 2035.

- Companies with 2030 targets keep using V1 for their current cycle and move to V2 in 2028; companies without targets can start using V2 on February 1, 2027.

Why every business needs to understand the SBTi Net-Zero Standard revision

The Science Based Targets initiative (SBTi) has become the default reference point for credible corporate climate action. Net-zero targets are now held by 51% of Fortune Global 500 (FG500) companies, up dramatically from just 8% in 2020, and more than 11,000 organizations worldwide have set SBTi-validated targets.

However, SBTi’s influence extends well beyond the companies formally participating in the program. Every business in the value chain of an SBTi participant will have to reduce its own carbon emissions, and businesses that aren’t SBTi participants themselves still look to the program for guidance on climate action.

In short, SBTi gives every business a credible blueprint for climate action, and companies that follow its principles can pursue climate action with confidence, whether or not they’re formally part of the program.

How will the Net Zero Standard revision affect business climate action?

SBTi participation is expected to grow. Despite strong target-setting participation among the F500, only 17% of companies use the SBTi Net Zero Standard V1 beyond target setting, largely because its rules have been seen as too rigid to apply in practice. Much of the Net Zero Standard revision has focused on creating more flexibility to enable higher participation. Medium and small businesses will also increasingly feel pressure for climate action, since SBTi mandates that its participants reduce carbon emissions across their value chains.

Net Zero Standard V2 also redefines climate leadership: leading climate action now means reducing emissions and mitigating ongoing emissions. Reducing your own emissions while ignoring the emissions you continue to release along the way is no longer considered leadership. Supporting voluntary carbon projects with high-integrity carbon credits is now backed by the leading authority on corporate climate action.

What lessons shaped the Net Zero Standard V2 revision?

The revision reflects a few learnings about what actually drives climate progress, and how SBTi built those lessons into the new standard.

| Net Zero Standard V1 Learnings | Net Zero Standard V2 Implementation |

|---|---|

| Making real short-term progress is more important and more difficult than making big long-term promises | Focus on short-term climate progress |

| Every company has a different path to net zero that doesn’t always fit generalized net-zero rules | Create asset transition plans based on each company’s unique asset lifecycles and capital planning |

| We need to mitigate our ongoing emissions to keep global carbon emissions in check | Reduce global carbon emissions by financing voluntary carbon projects with high-integrity carbon credits |

What are the key changes between the old and new Net Zero Standard?

Both versions of the standard are grounded in net-zero by 2050. However, the old standard treated climate leadership as simply reducing emissions, expected a long-term commitment to net zero, based emission reduction targets on generalized net-zero goals, revoked status from companies that fell behind on targets, and ignored voluntary carbon projects entirely.

The new standard treats climate leadership as reducing emissions and mitigating ongoing emissions. It shifts the focus to short-term progress through five-year cycles, and it bases emission reduction targets on both the net-zero goal and a company’s own asset decarbonization plan. A new Asset Transition Method lets companies set decarbonization targets through asset plans with committed, verifiable steps; an ambitious but achievable path based on a company’s starting point, financial resources, and technology, with multiple pathways to reflect the unique opportunities and constraints of different industries and companies.

Crucially, the new standard moves to a “best efforts” basis that creates real flexibility on progress against targets. Businesses that miss their targets can keep their status if they’ve used “every lever” within their control, and minimum progress rules will be set out in the SBTi Assurance Manual.

Finally, the new standard formally uses voluntary carbon projects to mitigate ongoing emissions. From 2027 through 2034, this mitigation is recognized, and both carbon reduction and removal credits are accepted. From 2035 forward, mitigation with carbon removal credits becomes required, with durability matching between the removal and the emission it offsets.

| Old Net Zero Standard | New Net Zero Standard |

|---|---|

| Grounded in net-zero by 2050 | Grounded in net-zero by 2050 |

| Climate leadership is reducing emissions | Climate leadership is reducing emissions and mitigating ongoing emissions |

| Make a long-term commitment to net-zero | Focus on short-term progress in 5-year cycles |

| Emission reduction targets are based on net-zero goal |

|

| Businesses who fall behind targets lose status |

|

| Ignores voluntary carbon projects |

|

When does the new Net Zero Standard take effect?

Companies with existing 2030 targets should continue using the old Net Zero Standard for their current cycle, and start using the new Net Zero Standard in 2028 to set targets for the next cycle (2030–2035).

Companies that don’t yet have targets can use the new Net Zero Standard starting February 1, 2027.

What are SBTi’s Category A and Category B companies?

The new Net Zero Standard splits companies into two categories, with different requirements attached to each.

Category A covers large companies from all countries and medium-sized companies from high-income countries. A company from any country qualifies if it meets at least one of: net turnover of €450 million or more, or 1,000 or more full-time employees. A company from a high-income country qualifies if its Scope 1 and 2 emissions are 10,000 tCO2e or more, or if it meets at least two of: balance sheet of €25 million or more, net turnover of €50 million or more, or 250 or more full-time employees.

Category B covers small companies from all countries and medium-sized companies from lower-income countries.

How do Scope 1 targets work under Net Zero Standard V2?

Scope 1 targets aim to transition companies to net-zero direct emissions by 2050 or sooner, and companies can choose from three approaches.

- Absolute emissions reduction follows a straight-line emissions trajectory from the target base year to the net-zero year.

- Emissions intensity reduction lets companies follow sector-specific pathways designed to reflect the reduction opportunities available in sectors like steel, cement, or chemicals.

- Asset transition is designed for companies whose capital stock turnover doesn’t follow a linear or sector pathway. These companies design a transition plan to operate existing assets efficiently and replace them with low-carbon assets, using predetermined milestones.

How do Scope 2 targets work under Net Zero Standard V2?

Scope 2 targets address emissions from purchased electricity through three pathways:

- Reducing electricity consumption,

- Reducing grid consumption by installing onsite or direct-line offsite clean energy generation, and

- Cleaning up the regional grid using market-based tools like PPAs, RECs, and GOs that drive clean energy development.

V2 introduces a dual Scope 2 framework requiring two separate targets, with an overall goal of 100% low-carbon electricity by 2040.

The location-based target addresses the carbon intensity of a company’s physical power use, and requires companies to show that their grid consumption is falling and/or that their physical grid use is getting cleaner; in other words, that their market-based solutions are actually making the grid cleaner.

The market-based (or zero-carbon electricity) target tracks a company’s use of low-carbon power generation contracts and Energy Attribute Certificates. It requires geographical matching of these certificates with electricity consumption based on deliverability regions (grid regions); annual matching is allowed, though hourly matching is encouraged. Category A companies with large electricity loads must report the percentage of their Scope 2 electricity consumption matched with low-carbon attributes on an hourly basis, and there’s an optional recognition framework for companies that meet hourly matching thresholds.

How do Scope 3 targets work under Net Zero Standard V2?

Scope 3 targets share the same 2050-or-sooner net-zero goal, but companies set near-term targets only for material emissions sources in their value chain and areas where they have real influence. Long-term Scope 3 targets are generally not required.

Limited, justified exclusions are allowed for near-term targets, including categories that individually account for less than 5% of total Scope 3 emissions, and activities where a company lacks practical influence, like leased assets it doesn’t operationally control, or the processing of sold products. Optional exclusions are also available in specific categories.

Companies can choose from three approaches to near-term Scope 3 targets:

- An overarching emissions reduction target, which follows a linear contraction of emissions from the base year to residual emissions of 10% or less by 2050 or sooner;

- An overarching supplier/customer alignment target, benchmarked against a growing share of tier 1 suppliers and customers reaching net-zero by 2050 or sooner; or

- A category- or activity-specific target, tailored for companies with concentrated emissions in particular Scope 3 categories or high-emitting activities.

What is “ongoing emissions mitigation” under the new SBTi standard?

This is one of the most significant additions in Net Zero Standard V2. Accelerated climate contributions are needed to help the world achieve climate objectives, limit temperature overshoot, mitigate transition risks, and support the scale-up of climate solutions, and V2 formally recognizes that. Ongoing emissions mitigation runs as a parallel track to companies also reducing their own emissions.

The framework is initially voluntary, with recognition available at three contribution levels to encourage early action.

- Engaged companies address more than 1% of total Scope 1, 2, and 3 emissions.

- Advanced companies address more than 10% of total Scope 1, 2, and 3 emissions, including 100% of Scope 1 and 2 emissions.

- Leadership companies address 100% of total Scope 1, 2, and 3 emissions with a contribution budget of $80/tCO2e.

Carbon credits used for this purpose have to meet certain quality standards. They must be ex-post (issued after the mitigation has actually occurred), independently third-party-assured, emissions reductions or removals, measured in tCO2e, that occur within five years prior to the reporting year. They must be sourced from outside the company’s own value chain. Further minimum criteria will be set to align with high-integrity frameworks, with additional details on the recognition program expected in the second half of 2026.

Starting in 2035, carbon removals become mandatory for Category A companies. From that point, the carbon removal coverage requirement rises linearly from 1% of Scope 1–3 emissions to 100% by a company’s net-zero year. Within that, 10% of long-lived GHG emissions must specifically be covered by durable removals, also rising linearly to 100% by the net-zero year.

How must companies neutralize residual emissions?

At a company’s net-zero target year and thereafter, it must reduce its Scope 1, 2, and 3 emissions to zero or to residual levels, and neutralize all residual emissions using eligible carbon removals. Those removals have to meet two conditions: they must occur within the same reporting period as the residual emissions they’re neutralizing, and long-lived GHGs must be neutralized with long-lived removals, matching the durability of the removal to the atmospheric lifetime of the emission being addressed.

What is the SBTi implementation hierarchy?

Net Zero Standard V2 also lays out how companies should prioritize their actions for credible target delivery, in three tiers.

- Direct actions, at the activity level, are actions that reduce emissions at the source within a company’s own operations and value chain; things like efficiency improvements, fuel switching, and engaging suppliers and customers to reduce their emissions.

- Actions within shared systems, or activity pools that reduce the emissions of shared systems like electricity or gas grids. This includes market instruments that convey low-carbon attributes, such as PPAs, RECs, and GOs, all of which must meet minimum integrity criteria that SBTi will elaborate on in future guidance.

- Sector-level actions relate to the same type of activity occurring in a relevant geography or system, in a way that meaningfully reduces the emissions a company is responsible for.

How Terrapass helps businesses meet the new SBTi standard

As the rules around carbon credits become more rigorous, the quality of the credits behind them matters more than ever. Terrapass has expanded our global network of carbon projects: more project types, locations, prices, ICVCM CCPs, and UN SDGs, spanning super-pollutant destruction, nature-based solutions, and durable removals. We offer Green-e® Climate Certification and we only source from third-party-verified projects on ICVCM-Eligible registries.

We also help clients with impact beyond carbon: EACs, RECs, and GOs including Green-e® Certified credits that support leading renewable energy projects; water credits that support water restoration projects; and custom environmental product needs like RNG and SAF. Wherever your organization is on its sustainability journey, we help clients around the world address climate risk, advance their environmental and social goals, and get the most out of their sustainability budgets.

FAQ: SBTi Net-Zero Standard revision

What is the SBTi Net-Zero Standard?

It’s the framework the Science Based Targets initiative publishes for companies that want validated, credible net-zero targets tied to limiting global warming.

What is changing in the SBTi Net Zero Standard V2 revision?

The biggest changes are more flexibility (five-year cycles and a “best efforts” standard), a new Asset Transition Method for companies whose emissions don’t follow a straight-line path, and formal recognition of voluntary carbon credits for mitigating ongoing emissions.

When do companies need to switch to the new SBTi standard?

If your company already has 2030 targets, you keep using V1 for your current cycle and move to V2 in 2028. If you don’t have targets yet, you can start using V2 as of February 1, 2027.

Can companies use carbon credits to meet SBTi targets?

They can. Under V2, high-integrity carbon reduction and removal credits count toward mitigating ongoing emissions from 2027 through 2034. Starting in 2035, only removal credits count, and they need to be durability-matched to the emissions they offset.

What’s the difference between Category A and Category B companies under SBTi?

Category A is large companies everywhere plus medium-sized companies in high-income countries, based on thresholds like revenue, headcount, or emissions. Category B is small companies everywhere and medium-sized companies in lower-income countries.

What happens if a company misses its SBTi target?

Under the old standard, falling behind could cost a company its SBTi status. Under V2’s “best efforts” approach, a company can hold onto its status as long as it’s used every lever within its control, with minimum progress rules coming in the SBTi Assurance Manual.

Sources: This post is based on Terrapass’s internal analysis of the SBTi Corporate Net-Zero Standard V2.0. Facts and figures were checked against SBTi’s official V2.0 announcement, SBTi’s Corporate Net-Zero Standard V2.0 — Chapter 6: Ongoing Emissions Responsibility, Trellis’s coverage of the standard, Trellis’s reporting on Ongoing Emissions Recognition costs, Sylvera’s analysis of what comes next, Anthesis Group’s Fortune 500 net-zero commitments research, and Climate Impact Partners’ seventh annual FG500 analysis, as reported by CarbonUnits.com.

The post SBTi Net-Zero Standard V2: What the Revision Means for Every Business appeared first on Terrapass.

For most businesses, the emissions that matter most sit outside their own walls. Scope 3 emissions, everything generated across your value chain, from the suppliers who make your inputs to the customers who use your products, typically make up the majority of a company’s total carbon footprint. Under the Corporate Sustainability Reporting Directive (CSRD), those value-chain emissions now have to be measured and disclosed with a rigour that spend-based estimates alone struggle to satisfy. This guide sets out how to improve Scope 3 data accuracy for CSRD: the calculation methods open to you, how to move from estimates to verified supplier data, and how to govern that data so it holds up to audit.

![]()

A carbon credit is a commitment that extends well into the future. The tonne of CO₂ compensated for today from a nature-based carbon project must remain out of the atmosphere for good, which means the forest behind the credit has to remain standing long after the transaction is complete. For any buyer, this raises a defining question: What ensures that the forest endures?

![]()

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy10 months ago

Renewable Energy10 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测