Battery storage systems play a crucial role in maintaining grid stability by balancing electricity supply and demand. They store energy from renewable sources like wind and solar, releasing it when needed, which helps to save power during low-demand periods. In this rapidly growing sector, lithium-ion batteries are taking the lead, driving the energy transition with their high efficiency and flexibility.

Utility-scale battery energy storage is booming across the United States. According to the latest report from the U.S. Energy Information Administration (EIA), till July 2024, operators added 5 gigawatts (GW) of new capacity to the U.S. power grid, making a total available battery storage capacity more than 20.7 GW. Notably, developers plan to add 15 GW in 2024 and another 9 GW in 2025.

Source: EIA

A MESSAGE FROM Li-FT POWER LTD.

Lithium Deposits That Can Be Seen From The Sky

Who is Li-FT Power? They are one of the fastest developing North American lithium juniors with a flagship Yellowknife Lithium project located in the Northwest Territories.

Three reasons to consider Li-FT Power:

RESOURCE POTENTIAL | EXPEDITED STRATEGY | INFRASTRUCTURE

Li-FT is advancing five key projects; all located in the extremely safe and friendly mining jurisdiction of Canada.

TXSV: LIFT | OTCQX: LIFFF | FRA: WS0

*** This content was reviewed and approved by Li-FT Power Ltd. and is being disseminated on behalf of Li-FT Power Ltd. by CarbonCredits.com. ***

Lithium-ion batteries Lead the Charge

The U.S. power sector has overwhelmingly adopted lithium-ion batteries for energy storage. These batteries now account for over 90% of the global demand, outpacing their use in personal electronics. As the world transitions from fossil fuels, battery storage is crucial to improving energy efficiency and supporting clean energy adoption.

Energy storage, while not a primary electricity source, provides crucial backup power. It stores electricity generated from the grid or renewable sources, making it a key player in the renewable energy ecosystem. Batteries allow electricity produced during peak generation times to be stored and later supplied during peak demand periods, enhancing grid reliability and reducing energy losses.

Despite impressive growth, the battery storage sector faces several challenges. Supply chain disruptions, inflation, and delays in grid interconnection are slowing the pace of new projects. However, experts like energy analysts and battery enthusiasts expect these issues to improve by the end of this year, leading to an even faster deployment.

Michael Craig, a professor at the University of Michigan, emphasizes the need for rapid technological advancement to meet ambitious carbon-reduction goals. The EIA predicts that utility-scale battery storage will almost double by the end of 2024, a sign that the industry is moving in the right direction.

Battery Storage Set to Drive 60% of CO2 Reductions by 2030: IEA

Battery storage is becoming increasingly attractive as costs continue to fall. Companies like Tesla and Enphase are scaling their battery storage offerings to meet growing demand, driven by the rise of AI and data centers, which are expected to increase energy consumption dramatically.

According to industry projections, the global battery storage market will grow in leaps and bounds with the push for renewable energy adoption. By 2030, electric vehicles are expected to displace millions of barrels of oil daily, further boosting the need for large-scale energy storage solutions in the power sector.

As battery storage continues to expand, it is clear that this technology is a cornerstone of the energy transition, enabling the shift away from fossil fuels and toward a more sustainable, electrified future.

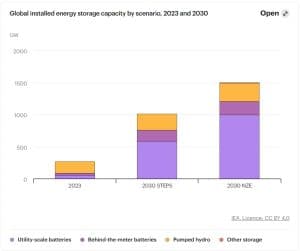

According to the IEA, to triple global renewable energy capacity by 2030, while ensuring electricity security, energy storage must grow six-fold. In the Net Zero Emissions (NZE) Scenario, storage capacity needs to reach 1,500 GW by 2030. Batteries will drive 90% of this expansion, growing 14-fold to 1,200 GW, supported by technologies like pumped storage and compressed air.

Source: IEA

This rapid growth requires battery deployment to rise 25% annually. Batteries are key, as they account for 60% of CO2 reductions in 2030, directly in EVs and solar PV, and indirectly through electrification and renewables.

Low-Cost Cathode Could Slash Lithium Battery Costs

A team led by Hailong Chen at Georgia Tech has developed a low-cost iron chloride (FeCl3) cathode for lithium-ion batteries (LIBs). This breakthrough could reduce electric vehicle (EV) costs, where batteries make nearly half the price. FeCl3 costs just 1-2% of traditional cathode materials like nickel and cobalt while delivering the same energy capacity, making it a game-changer for EVs and energy storage.

The FeCl3 cathode is not only cheaper but also provides higher voltage than popular alternatives like lithium iron phosphate (LiFePO4). Chen’s team aims to push for all-solid-state LIBs, which could improve safety and efficiency. This could also enhance large-scale energy storage and strengthen the power grid.

Chen’s research, which began in 2019, shows FeCl3 as a scalable and eco-friendly option. The team expects the technology to be commercially available within five years, promising to reshape EVs and renewable energy storage with lower costs and greater sustainability.

Source: Hailong Chen and research team, Georgia Tech

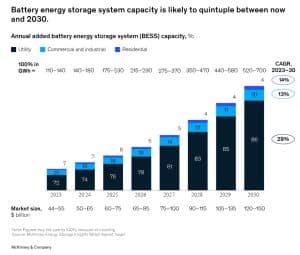

BESS Market Poised for Explosive Growth by 2030, A McKinsey Report

The Battery Energy Storage System (BESS) market is rapidly growing, creating a huge opportunity for investors and companies. In 2022, over $5 billion was invested in BESS, nearly tripling from the previous year.

- According to McKinsey, the global BESS market is projected to grow significantly, reaching between $120 billion and $150 billion by 2030—more than 2x its current size.

Source: McKinsey

Source: McKinsey

Although the BESS market is expanding, it remains fragmented, leaving many companies uncertain about their next move. Now is the time for businesses to pinpoint the best opportunities and secure their position. With rising competition and increasing demand for renewable energy, companies must act swiftly to carve out their share of this booming market.

Key Strategies to Succeed in the BESS Market

McKinsey has come up with innovative solutions for companies to succeed in the dynamic BESS market:

They should focus on filling gaps in the value chain and prioritizing software development. System integrators can explore new opportunities by partnering with battery manufacturers, while battery makers can add integration services to target specific sectors. Additionally, investing in software that optimizes BESS performance will unlock larger markets and drive higher margins.

Strengthening supply chains and staying agile are also crucial. Companies need strategic partnerships and multi-sourcing options to manage supply disruptions. Smaller firms should act quickly, leverage their intellectual property, and take risks to stay competitive against larger players.

With global investments in BESS surging, reaching between $120 billion and $150 billion by 2030, companies need to identify the best opportunities and act decisively.

Source: McKinsey

Can the U.S. Dominate the Battery Energy Storage Market?

EIA has also estimated that U.S. battery storage capacity could increase by 89% by the end of 2024. This growth depends on developers bringing planned energy storage systems online by their intended commercial operation dates.

- Currently, developers aim to expand U.S. battery capacity to over 30 gigawatts (GW) by the end of 2024. This would surpass the capacity of petroleum liquids, geothermal, wood and wood waste, and landfill gas.

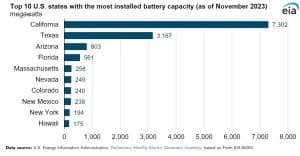

California and Texas dominate the battery storage market. California leads with 7.3 GW of installed battery storage, followed by Texas with 3.2 GW. Significantly, Vistra’s facility in Moss Landing, California, is currently the largest, with 750 megawatts (MW).

By 2025, developers expect to complete over 300 utility-scale battery storage projects across the U.S., with Texas accounting for about 50% of the planned capacity. The five largest battery storage projects set to come online in 2024 or 2025 include:

- Lunis Creek BESS SLF (Texas, 621 MW)

- Clear Fork Creek BESS SLF (Texas, 600 MW)

- Hecate Energy Ramsey Storage (Texas, 500 MW)

- Bellefield Solar and Energy Storage Farm (California, 500 MW)

- Dogwood Creek Solar and BESS (Texas, 443 MW)

Source: EIA

Source: EIA

With ambitious battery storage plans and declining costs, the U.S. is poised to achieve a cleaner, more reliable energy future, rapidly closing the gap with China.

- FURTHER READING: EV Wars and Breakthroughs: BYD to Overtake Tesla, CATL’s New Battery With 1.5M KM Range

The post EIA Expects Explosive Growth in U.S. Battery Storage—Can America Ascend to Dominance? appeared first on Carbon Credits.

Carbon buyers are asking better questions: permanence risk, additionality, co-benefits, and third-party verification, has all become vital considerations. The due diligence applied to nature-based carbon credits has grown sharper and more rigorous over the past few years. Yet one factor consistently sits at the edges of buyer evaluation: Whether the communities living on and around the project land are genuinely embedded in its design, management, and long-term success.

![]()

The artificial intelligence (AI) boom has entered a new phase. It is no longer just about innovation or market dominance. Instead, it is now deeply tied to energy demand, emissions, and capital discipline. As a result, the rapid expansion of AI infrastructure is pushing Big Tech into an uncomfortable position—balancing climate commitments with rising environmental costs.

Data compiled for CNBC by carbon management platform Ceezer shows a sharp rise in carbon credit purchases across the sector. Companies are scaling AI aggressively, yet at the same time, they are leaning more heavily on carbon markets to offset the emissions they cannot yet avoid.

This shift is not happening in isolation. It reflects a broader structural tension between growth, sustainability, and financial performance.

AI Expansion Is Driving Both Emissions and Offsets

Tech giants such as Alphabet, Microsoft, Meta, and Amazon are collectively expected to spend close to $700 billion this year to scale their AI capabilities. This includes building hyperscale data centers, deploying advanced chips, and expanding global cloud infrastructure.

However, these investments come with a high environmental cost. AI systems require vast computing power, which in turn demands continuous electricity and cooling. Water use is also rising, particularly in large data center clusters. Consequently, emissions are increasing even as companies reaffirm their net-zero ambitions.

This is where carbon credits play a growing role. Each credit represents one metric ton of carbon dioxide either reduced or removed from the atmosphere. By purchasing these credits, companies aim to offset emissions that remain difficult to eliminate in the short term.

Yet this approach raises a fundamental question. Are carbon credits acting as a bridge to decarbonization—or becoming a substitute for it?

A Market Surge Signals Structural Dependence

The scale of growth in carbon credit purchases suggests a structural shift rather than a temporary adjustment.

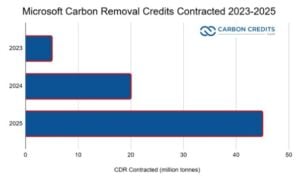

In 2022, permanent carbon removal purchases across these companies stood at just over 14,000 credits. Within a year, that figure jumped dramatically to 11.92 million. The momentum did not slow. Purchases increased to 24.4 million in 2024 and then surged to 68.4 million in 2025.

This exponential rise highlights how quickly AI-driven emissions are feeding into carbon markets. More importantly, it shows that demand for high-quality removal credits is accelerating faster than supply.

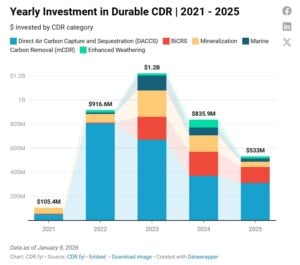

At the same time, companies are not relying on a single solution. Their portfolios include nature-based projects such as forestry and soil carbon, alongside engineered approaches like direct air capture. Long-term offtake agreements are also becoming more common, helping secure future credit supply while supporting project development.

However, the rapid increase in demand raises concerns about market depth. High-integrity carbon removal credits remain scarce, and scaling them is both capital-intensive and time-consuming.

Microsoft Sets the Pace—but Questions Remain

Among its peers, Microsoft has taken a clear lead in carbon removal efforts. The company reported a 247% increase in credit purchases between fiscal 2022 and 2023, followed by a further 337% jump in 2024. Growth continued into the next fiscal year, roughly doubling again.

More notably, Microsoft expanded its carbon removal agreements to 45 million metric tons of CO₂ in 2025, up from 22 million tons the previous year. These agreements span multiple geographies and technologies, reflecting a diversified approach to carbon removal.

The company is now a top climate leader, intending to become carbon-negative by 2030. Its strategy emphasizes reducing emissions first and then removing what cannot be avoided.

However, a key gap remains. It has not explicitly tied its carbon credit strategy to its AI expansion. While the correlation is clear, the lack of direct disclosure leaves room for interpretation.

This ambiguity is not unique to Microsoft. It reflects a broader issue across the sector, where sustainability narratives are evolving faster than reporting frameworks.

- MUST READ: Microsoft Q2 FY26 Earnings: $81B Revenue, AI Momentum, and a 150% Jump in Water Use by 2030

Free Cash Flow Pressures Are Becoming Harder to Ignore

While environmental concerns are rising, financial pressures are also building.

The CNBC report further highlighted that the scale of AI investment is unprecedented. As companies ramp up spending, free cash flow is beginning to decline. The four largest U.S. tech firms generated a combined $237 billion in free cash flow in 2024. That figure dropped to $200 billion in 2025, and further declines are expected.

This trend signals a shift in capital allocation. Companies are prioritizing long-term growth over short-term financial efficiency. However, this comes at a cost. Lower cash generation reduces flexibility and may increase reliance on external financing.

For instance, Alphabet raised $25 billion through a bond sale in late 2025, while its long-term debt rose sharply to $46.5 billion. This move underscores how even cash-rich companies are turning to debt markets to sustain their AI ambitions.

For investors, the implications are significant. The AI story remains compelling, but it now comes with margin pressure, delayed returns, and increased financial risk.

- ALSO READ: Google Bets Big on Next-Gen Nuclear and Carbon Credits from Superpollutants For a Greener AI

Renewables Help Stabilize Emissions—but Not Fully

Despite the rise in emissions, the increase has not been as steep as some feared. This is largely due to the rapid adoption of renewable energy.

Hyperscalers have expanded their clean energy portfolios, securing power purchase agreements and investing in renewable projects. As a result, they have been able to offset part of the additional demand created by AI workloads.

Ceezer’s data suggest that while emissions rose alongside AI growth, the increase was relatively moderate. This indicates that companies are responding quickly by integrating renewable energy into their operations.

However, this strategy has limits. Renewable energy can reduce operational emissions, but it cannot fully eliminate the impact of rapid infrastructure expansion. As AI demand continues to grow, the gap between emissions and reductions may widen.

Stricter Rules Are Reshaping Carbon Credit Use

At the same time, the regulatory landscape for carbon credits is becoming more stringent. New frameworks are redefining how companies can use offsets within their climate strategies.

Initiatives such as the VCMI Scope 3 Action Code now allow limited use of high-quality credits, but only under strict disclosure conditions. Meanwhile, the Science Based Targets initiative (SBTi) continues to refine its guidance, particularly as Scope 3 emissions remain difficult to reduce.

The challenge is substantial. The global Scope 3 emissions gap is estimated at 1.4 billion tonnes and could increase significantly by 2030. This creates pressure on companies to find credible solutions without over-relying on offsets.

In parallel, disclosure frameworks such as CSRD are pushing companies to provide detailed explanations of their carbon credit strategies. This includes justifying project selection, verifying credit quality, and demonstrating measurable impact.

The direction is clear. Carbon credits are no longer a simple compliance tool. They are becoming part of a broader accountability framework.

Carbon Removal Market Expands—but Supply Constraints Persist

The carbon removal market is growing rapidly, yet it remains constrained.

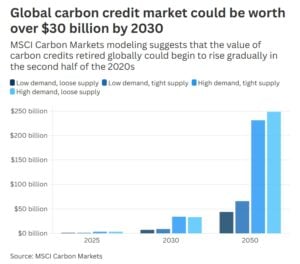

MSCI Projections suggest the global carbon credit market could exceed $30 billion by 2030. Corporate demand for carbon removal credits may surpass 150 million metric tons annually within the same timeframe.

However, supply is struggling to keep pace. High costs remain a major barrier, particularly for advanced technologies such as direct air capture, where prices often exceed $100 per ton.

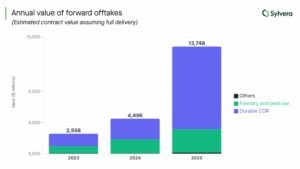

In 2025, offtake agreements reached $13.7 billion, reflecting a strong corporate commitment. Yet these agreements will deliver only 78 million credits over the next decade. Actual durable carbon removal credits retired in the same year remained below 200,000.

This mismatch highlights a key issue. While demand is accelerating, real-world deployment is lagging. As a result, the market faces both growth potential and structural limitations.

The Bottom Line: A Delicate Balancing Act

Big Tech’s AI expansion is reshaping both the digital economy and the carbon market. On one side, companies are investing heavily in future growth. On the other hand, they are navigating rising emissions, tighter regulations, and increasing financial pressure.

Carbon credits are playing a critical role in bridging this gap. However, they are not a long-term solution on their own.

The path forward will require a more balanced approach—one that combines technological innovation with real emissions reductions and transparent reporting. Companies must prove that their climate commitments are more than offset strategies.

At the same time, investors will need to adjust expectations. The AI boom promises strong returns, but it also introduces new risks. Lower cash flow, higher capital intensity, and evolving climate obligations are all part of the equation.

Ultimately, the success of this transition will depend on execution. The companies leading the AI race must now show they can scale responsibly—without compromising either financial stability or climate credibility.

The post AI vs. Climate Reality: Why Big Tech Is Buying Millions of Carbon Credits appeared first on Carbon Credits.

Industrial heat production makes up a large share of global emissions. About 18% of all greenhouse gas emissions come from heat used in factories, plants, and manufacturing processes. This type of heat is hard to decarbonize because it often requires high temperatures that are still powered by fossil fuels like natural gas.

To tackle this challenge, AstraZeneca, together with Secaro and ERM, launched the Clean Heat Program. The initiative helps companies measure, plan, and reduce industrial heat emissions across their supply chains.

Rob Williams, Senior Director of Sustainable Procurement at AstraZeneca, said:

“It’s clear that a programme like this is the fastest and most effective way to decarbonise heat in our supply chain. We are long-term partners with Secaro and ERM, and now we’re expanding relationships with peers, buyers from other industries and suppliers to plan, fund and launch the projects that will make heat decarbonisation a reality.”

Industrial Heat: The Hidden Carbon Giant

Fossil fuels still supply most industrial heat energy today. Cleaner alternatives like electrification, hydrogen, or biofuels often cost more. They also require new technology and infrastructure.

Despite its importance, industrial heat has received less focus than clean electricity or transport. In many industries, heat drives fundamental operations, from making chemicals to processing food. Because of this, experts say improving how heat is produced is key to cutting industrial emissions.

Clean Heat Program: Turning Plans into Action

In March 2026, AstraZeneca teamed up with ERM and Secaro to launch the Clean Heat Program. This initiative aims to help companies reduce emissions tied to industrial heat across their supply chains.

By combining data tools, technical support, and financing options, the program aims to make it easier for industrial facilities to adopt low-carbon heat solutions and accelerate decarbonization.

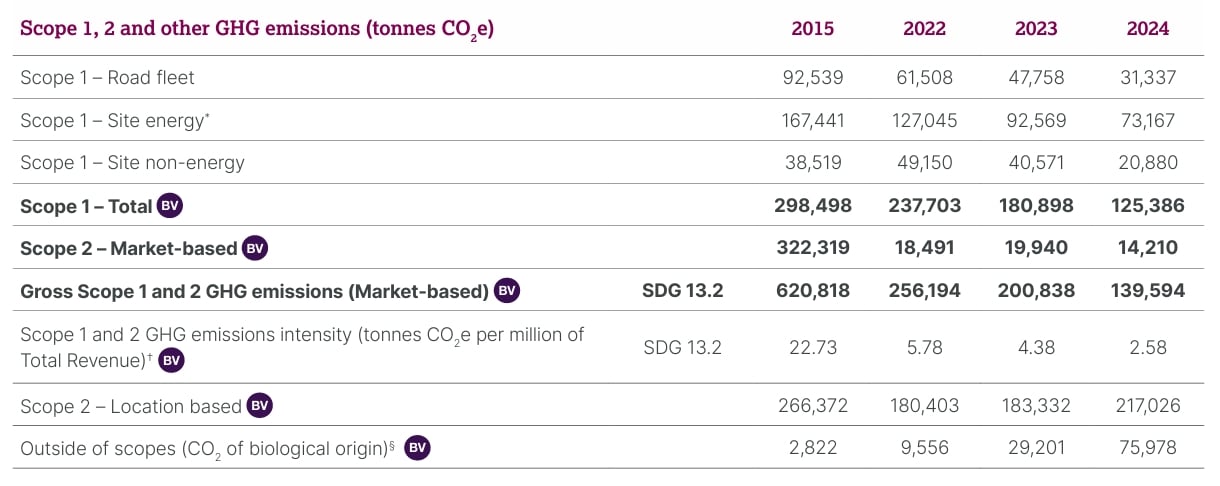

AstraZeneca is joining as a founding partner. The company has its own near‑term climate goals. By 2026, it aims to cut 98% of its Scope 1 and 2 emissions from operations compared to a 2015 baseline.

The pharma giant has already achieved 88.1% reduction by the end of 2025. Its long‑term target is to reach net zero by 2045, including deep cuts in emissions across its suppliers and partners.

The Clean Heat Program is designed to go beyond simple planning. It aims to help companies move from studying options to actually acting on decarbonizing heat.

The program combines:

- Supply chain data tools that show where heat is used and emitted.

- Technical support to find practical ways to reduce emissions.

- Financing options to help companies afford projects that cut heat emissions.

Secaro maps heat emissions across supply chains while ERM designs bankable projects, heat pumps, biomass conversion, and electrification upgrades. Notably, financing leverages EU funds and carbon credit revenue to de-risk upfront costs, moving companies from analysis to implementation.

Unlike many efforts that focus on one plant or site, the program looks at supplier networks. This broader view helps companies pinpoint where changes will have the biggest impact.

Why High-Temperature Heat Is Hard to Replace

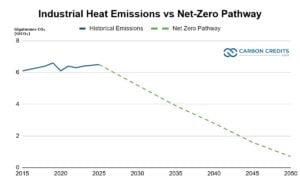

Industrial heat is one of the largest sources of industrial emissions. According to the International Energy Agency, around 70% of industrial energy demand goes to producing heat for processes such as steel, cement, and chemicals.

Estimates from IEA data show that heat-related emissions are about 6.5 gigatonnes of CO₂ each year. This underscores the significant decarbonization needed.

The same analysis suggests that these emissions must drop to less than 1 gigatonne by 2050. This pathway needs quick action from various industries. It also requires strong investment in technology and changes in supply chains to cut emissions in high-temperature processes.

Industrial heat often uses natural gas or other fossil fuels. While electricity can now come from wind or solar, renewable options for high‑temperature heat are still emerging. Solutions such as electrification, biomass fuels, or hydrogen require new equipment and deep planning.

Electrification technologies work for low-temperature heat below 200°C. But industries that need higher heat still rely on fossil fuels. Secaro’s data show that 80% of industrial energy consumption is tied to heat, and 60% of these come from natural gas.

This complexity makes industrial heat one of the hardest parts of decarbonization — even for companies with net‑zero goals. In many cases, heat emissions make up a large share of a company’s direct emissions, known as Scope 1 emissions.

Currently, less than 10% of sites use biofuels or other renewable energy. Industry forecasts suggest that renewable heat may reach only 15% of industrial use by 2028 unless strong action is taken.

Pressure’s On: Regulators, Investors, and Rising Energy Costs

Pressure to cut heat emissions is growing from both regulators and investors. New rules such as the European Union’s Carbon Border Adjustment Mechanism (CBAM) and updated disclosure requirements from the U.S. Securities and Exchange Commission (SEC) require more detailed emissions reporting and climate risk disclosure.

Companies that ignore their emissions might face penalties. They could also lose contracts with buyers who want cleaner supply chains.

Energy price volatility also plays a role. Firms that rely on fossil fuels for heat may face wide swings in energy costs. Decarbonizing heat can help companies stabilize fuel expenses and reduce exposure to price shocks, which investors increasingly watch closely.

Tools and Support for Heat Decarbonisation

Secaro’s data platform is central to the program. It now offers heat-specific insights, which show where emissions are highest and highlight chances for change. The platform links buyers, suppliers, and solution providers to highlight high‑impact decarbonization actions.

ERM steps in with its technical expertise. It helps companies assess options and build project plans to attract investment.

These can include:

- Higher energy efficiency

- Switching to low-carbon fuels

- Installing heat recovery systems

- Adopting new technologies, like high-temperature heat pumps

Financing is also part of the program. Many industrial heat projects stall because of upfront costs. The initiative aims to connect companies with financing options, including funds based in the European Union and other mechanisms that help lower financial barriers.

Markets Are Warming Up: Forecasts for Industrial Decarbonization

Efforts like the Clean Heat Program are significant as the market for industrial decarbonization is growing. A recent market outlook projects that global industrial heat decarbonization could grow steadily over the next decade.

From 2025 to 2033, the market is expected to expand at a compound annual growth rate (CAGR) of about 6%, reaching an estimated $380 billion by 2033.

Technologies such as industrial heat pumps are also gaining traction. These devices can reuse waste heat and reduce energy losses. A market forecast shows that the global industrial heat pump market will rise to over 13,150 units by 2035. Revenues may exceed $9.1 billion by that time.

Even though many low‑carbon heat solutions exist, adoption has been slow. For example, only a small share of industrial sites in some sectors currently use renewable heat sources. Without stronger action, forecasts suggest renewable heat may reach only around 15% of industrial heat use by 2028.

A Clear Path for Companies and Supply Chains

The Clean Heat Program offers companies a way to close the gap between their climate goals and the real challenges of industrial heat. It helps companies move beyond early analysis and toward real projects that reduce emissions, improve energy security, and meet investor and regulatory expectations.

For supply chain partners and smaller suppliers, the program can lower barriers to entry. Many small and mid‑tier suppliers struggle to access data, technical support, or financing. This initiative aims to change that by giving a clearer path to decarbonization. If widely adopted, this approach could help reduce significant emissions from industrial heat worldwide and support broader climate goals.

The post AstraZeneca Turns Up the Heat: New Program Tackles Industry’s Toughest Emissions appeared first on Carbon Credits.

Landmark deal to share Chile’s lithium windfall fractures Indigenous communities

Roadmap launched to restart deadlocked UN plastics treaty talks

Indigenous and local knowledge in carbon projects: why it defines credit quality

-

Greenhouse Gases7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy2 years ago

GAF Energy Completes Construction of Second Manufacturing Facility