The Brazilian COP30 presidency has published a “Baku to Belém roadmap” on how climate finance could be scaled up to “at least $1.3tn” a year by 2035.

The idea for the roadmap was a late addition to the outcome of COP29 last year, following disappointment over the formal $300bn-per-year climate-finance goal agreed in Baku.

The new document, published ahead of the UN climate talks in Belém, Brazil, says it is not designed to create new financing schemes or mechanisms.

Instead, the roadmap says it provides a “coherent reference framework on existing initiatives, concepts and leverage points to facilitate all actors coming together to scale up climate finance in the short to medium term”.

It details suggested actions across grants, concessional finance, private finance, climate portfolios, capital flows and more, designed to drive up climate finance over the next decade.

Despite geopolitical uncertainty, there is hope that this roadmap can lay out a pathway to the “trillions” in climate finance that developing countries say they need to meet their climate targets.

Countries have divergent views on how to get there, but some notable trends have emerged from the roadmap, which was spearheaded by the Azerbaijani and Brazilian COP presidencies.

Below, Carbon Brief details what the Baku to Belém roadmap is, why it was launched and what the key points within it are.

- Why was the ‘Baku to Belém roadmap’ launched?

- What is the goal of the roadmap?

- What are different countries’ views on climate finance?

- What are the solutions that the roadmap has identified?

- What happens next?

Why was the ‘Baku to Belém roadmap’ launched?

A mounting body of evidence shows that developing countries will need trillions of dollars in the coming years if they are to achieve their climate goals.

While much of this finance will likely be sourced domestically within those countries, a large slice is expected to come from international actors.

This climate finance is part of the “grand bargain” at the heart of the Paris Agreement, whereby developing countries agree to set more ambitious climate plans if they receive financial support from developed countries.

Ahead of COP29, developing countries hoped that the post-2025 climate finance target – known as the new collective quantified goal (NCQG) – would reflect their full “needs and priorities”, as set out in the Paris Agreement.

They also pushed for developed-country parties such as the EU, the US and Japan to contribute a large portion of this finance, preferably on favourable terms such as grants.

They were left largely disappointed, with a final target that fell well short of what many developing countries had been proposing.

The central target agreed at COP29 was “at least” $300bn a year by 2035, with an expectation that developed countries would “take the lead” in providing these funds from “a wide variety of sources”, including private finance.

This goal – which was effectively the successor to the previous $100bn-per-year target – was far short of what developing countries had wanted. However, another key part of the text agreed in Baku alludes to their ambitions, with a loose request that “all actors” scale up finance to at least $1.3tn per year by 2035:

“[The COP] calls on all actors to work together to enable the scaling up of financing to developing country parties for climate action from all public and private sources to at least $1.3tn per year by 2035.”

In contrast to the $300bn target, this $1.3tn figure, which first appeared in a proposal by the African Group in 2021, reflects developing-country demands and needs. It also aligns with influential analysis of developing-country needs by the Independent High-Level Expert Group on Climate Finance (IHLEG).

Yet, this part of the text lacked binding language and detail on who precisely would be responsible for providing these funds. It has therefore been described by civil-society groups as more of an aspirational “call to action” than a target.

(“Calls on” is the weakest form of words in which UN legal texts can make a request.)

However, the COP29 text contained another relevant decision, added as negotiations drew to a close. It mentioned a “Baku to Belém roadmap to $1.3tn” – a report that could flesh out ways to scale up finance further and help developing countries achieve their climate targets.

The Azerbaijani COP29 presidency and the incoming Brazilian presidency were tasked with assembling this roadmap ahead of COP30 in 2025.

In the months that followed, the presidencies engaged with governments, civil-society groups, businesses and other relevant actors. They gathered information to build a “library of knowledge and best practices”, which could boost climate finance for developing countries.

What is the goal of the roadmap?

The roadmap comes at a difficult time for climate finance, with a particularly “bleak” outlook for public funding from developed countries. Major donors – particularly the US – have made large cuts to their aid budgets, threatening climate spending overseas.

At the same time, private investment has also faltered, with successive economic shocks raising the cost of capital for clean-energy projects in developing countries.

For years, finance experts and development leaders have talked of a “billions to trillions” agenda, suggesting that public money could help to “mobilise” trillions of dollars of private investments that could be used to build low-carbon infrastructure in the global south.

Yet, the “billions to trillions” concept has also faced growing scrutiny, with even the World Bank chief economist Indermit Gill branding it “a fantasy”. Critics have highlighted wider issues constraining developing countries, such as high levels of debt.

The NCQG text from COP29 set out the roadmap’s overarching goal of scaling up annual climate finance to $1.3tn, through means including “grants, concessional and non-debt-creating instruments, and measures to create fiscal space”.

On the current trajectory, financial sources potentially covered by the target could hit around $427bn for developing countries a year by 2035, less than a third of the goal, according to analysis by the thinktank NRDC.

Achieving $1.3tn of finance relies on what one report calls “yet-to-be-defined mechanisms”, which go beyond the ones covered by the $300bn target.

Countries and other relevant parties were asked by the presidencies for their views on “short-term” – actions by 2028 and “medium-to-long term” actions beyond 2028 that could ramp up finance further. They were asked about new sources of finance and thoughts on scaling up adaptation finance, in particular.

There have already been numerous ideas and programmes put forward for scaling up international climate finance. These include G20-led reforms of the multilateral development banks (MDBs), this year’s International Conference on Financing for Development, as well as UN sovereign debt restructuring efforts.

Accordingly, the Baku to Belém roadmap was also given a remit to “tak[e] into account relevant multilateral initiatives as appropriate”. Parties were also asked for suggestions of organisations and initiatives that should be involved.

Rebecca Thissen from Climate Action Network (CAN) International tells Carbon Brief:

“The roadmap could support the UNFCCC to be sending strong signals to the international community…But also using the convening power that the UNFCCC could have, so bringing those different actors to the table in a more structured and predictable way.”

What are different countries’ views on climate finance?

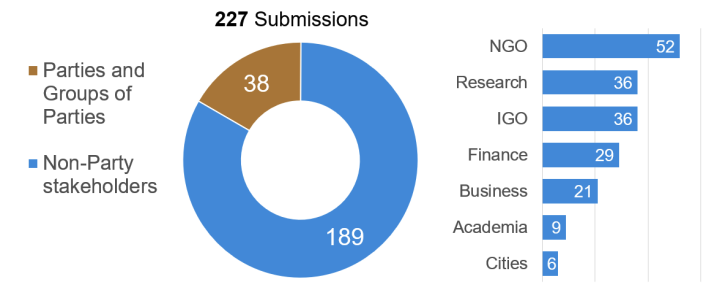

There were over 227 submissions into the Baku to Belém roadmap, including 38 from countries and party groupings. The remainder came mainly from NGOs, businesses, financial experts and researchers, as shown in the figure below.

The submissions partly reflect what the thinktank C2ES describes as the “pockmarked baggage of the climate finance negotiations”, with many parties demonstrating the same entrenched, often opposing views on climate finance that they have held for decades.

Carbon Brief has captured the submissions by countries and party groupings in the interactive table below, comparing their views on key issues.

There is broad agreement among countries that the roadmap should not reopen the NCQG discussions or involve a new, negotiated outcome at COP30.

However, some parties still call for more accountability in achieving the existing goals.

Latin American countries within the AILAC grouping call for the roadmap to “define concrete milestones for scaling up climate finance”. Egypt goes further, proposing that developed countries alone commit “at least $150bn annually in public concessional finance by 2028”, mainly as grants.

A key divergence in submissions is on which governments and institutions, precisely, should be responsible for scaling finance up to $1.3tn.

Several developing-country groups stress the importance of centring developed countries as the primary contributors, referencing Article 9.1 of the Paris Agreement.

The Like-Minded Developing Countries (LMDCs) group, which includes India, China and Saudi Arabia, states that “the roadmap must place Article 9.1 as its central pillar”. The G77 and China – a group representing all developing countries – stresses the “additional role developed countries will play in the context of Article 9.1, which is additional to the $300bn”.

Meanwhile, many developed countries focus on what Canada refers to as “a necessary broadening of climate finance” within the roadmap. In practice, this often amounts to a greater push for private finance, as well as “innovative” new sources such as global levies.

While developing countries do not often outright oppose such sources, some of them propose tighter limits. For example, China says “purely commercial investment flows should not be included” in the $1.3tn, which should only count funds “mobilised through public interventions”.

A related dispute centres on the roadmap’s scope, with the EU suggesting it should “extend beyond the UNFCCC framework”.

Parties such as India reject the idea of involving other multilateral fora, such as the G20. This would involve moving beyond the UN climate process, where developed countries have traditionally been the ones responsible for channelling climate finance.

The submissions also show notable differences among developing-country groupings. On the topic of defining what should be counted as “climate finance”, the Alliance of Small Island States (AOSIS) opposes the inclusion of funding for fossil-fuel projects, while the Arab Group says it does not support “any exclusionary criteria”.

There is coalescence between parties around other issues, albeit with various subtle differences.

Areas of broad agreement include the importance of more funding for climate adaptation, dealing with “barriers” to funding in developing countries and improving the transparency of climate-finance provision.

The roadmap details some of the potential sources of finance identified within the submissions.

This includes direct budget contributions, which the submissions suggest could generate an additional $197bn in financing; improved rechanneling and new issuances of special drawing rights ($100-500bn per year); carbon pricing ($20-4,900bn, dependent on rate and geographies); and fees on aviation or maritime transport($4-223bn).

Additionally, a range of taxes were identified as candidates for raising new climate finance. These include taxes on specific goods such as luxury fashion, technology and military goods ($34-112bn), financial transactions taxes ($105-327bn), minimum corporate taxes ($165-540bn) and wealth taxes ($200-1,364bn).

In a statement, Rebecca Newsom, global political expert at Greenpeace International, said:

“It’s notable that the roadmap recognises new taxes and levies as key to unlocking public climate finance. Given reported profits from just five international oil and gas giants over the last decade reached almost $800bn, taxing fossil fuel corporations is clearly a huge opportunity to overcome national fiscal constraints.

“The roadmap’s recognition that the UN tax convention provides an opportunity to raise new sources of concessional climate finance is also highly welcome, and is an opportunity governments must now seize.”

What are the solutions that the roadmap has identified?

The roadmap sets out “five action fronts” for reaching $1.3tn by 2035.

These are designed to “help deliver on the at-least-$1.3tn aspiration by strengthening supply, making demand more strategic, and accelerating access and transparency”.

The report titles these five action fronts as “replenishing, rebalancing, rechanneling, revamping and reshaping”.

Within each of these, the roadmap lays out key points to help “transform scientific warning into a global blueprint for cooperation and tangible results”.

The first, “replenishing”, refers to grants, concessional finance and low-cost capital, including multilateral climate funds and MDBs.

It notes that there is a “growing role” for MDBs in advancing climate action, as well as a need for developed countries to achieve “manyfold increases in the delivery of grants and concessional climate finance, including through bilateral and multilateral channels”.

Access to grants and concessional finance is a key enabling factor for an “efficient” flow of public funding, the roadmap notes.

The roadmap calls for coordination in the international finance system, bilateral finance that is concessional and low-cost, multilateral climate funds, innovative sources of concessional finance with simplified access pathways and more.

This coordination could be key, with Sarah Colenbrander, director of ODI’s climate and sustainability programme, telling Carbon Brief:

“The bigger risk is probably that some countries will allocate their climate finance differently, so that they can report more money going out the door without a commensurate increase in fiscal effort. For example, they might shift from grants to concessional loans, and from concessional loans to market-rate loans. If the money will be repaid, there is less lift for taxpayers at home.

“Alternatively, countries might focus on using public finance to mobilise private finance that can also count towards the $300bn goal. Private finance has a very important role to play in both mitigation and adaptation, but it is very unlikely to meet the needs of the most vulnerable communities, given their high adaptation investment needs and very limited ability to pay.”

In particular, the roadmap suggests MDBs “intensify their engagement on climate finance through a strategic approach that recognises and amplifies their catalytic role in providing and mobilising capital”.

Second, “rebalancing” refers to fiscal space and debt sustainability. The roadmap calls on creditor countries, the International Monetary Fund (IMF) and MDBs to work together to “alleviate onerous debt burdens faced by developing countries”.

The roadmap notes that external debt servicing costs of developing countries have more than doubled since 2014, to $1.7tn per year in 2023.

Developing countries’ net interest payments on public debt reached $921bn in 2024, a 10% increase compared to 2023, it adds.

The roadmap notes the need to “remove barriers and address disenablers faced by developing countries in financing climate action”. It adds that developing countries face at least two- to four-times the borrowing costs of developed countries.

It points to a number of “promising” solutions already being implemented, such as climate-resilient debt clauses and “debt-for-climate swaps” and debt restructuring.

In particular, MDBs, the IMF, UN agencies and regional UN economic commissions could work together to create a “one-stop shop” for assistance in these areas, the roadmap says.

Third, “rechannelling” refers to “transformative” private finance and affordable cost of capital.

It notes that mobilisation of private finance has been “stubborn to scale”: The level of private finance leveraged by official development interventions has grown by 7% per year from 2016 to 2019 and then 16% per year from 2020 to 2023, to reach $46bn.

The roadmap says that “blended finance” can play a role in scaling up climate finance and that private finance for the implementation of “nationally determined contributions” to cutting global emissions (NDCs) and national adaptation plans (NAPs) has “significant potential for growth”.

“Innovative instruments” are listed as a key approach to improving private finance, including “catalytic equity”, guarantees, foreign exchange risk management, securitisation platforms and more.

To support this, the roadmap calls for target-setting and data transparency, along with increasing, coordinating and harmonising guarantee offerings and channelling concessional finance into long-term foreign exchange hedging facilities, along with other actions.

Relying heavily on private finance could pose a risk, Jan Kowalzig, senior policy adviser for climate at Oxfam Germany, tells Carbon Brief, adding:

“The much larger problem, however, is the plan to massively rely on private finance in the future. While private finance has a key role to play to transform economies, [it] cannot replace much-needed public finance, especially for adaptation and for responding to loss and damage.

“Interventions in these sectors often do not generate return to satisfy investors’ expectations. Forcing projects to become profitable can come at great social cost for frontline communities struggling to survive in the worsening climate crisis.”

The roadmap suggests financial institutions move towards “originate-to-distribute” and “originate-to-share” business models, support the development of climate-aligned domestic financial systems and expand investor bases and diverse sources of capital, amongst other proposals.

Fourth is “revamping”, referring to capacity and coordination for scaled climate portfolios. This “demands institutions to manage risks locally, develop project pipelines, ensure country ownership and track progress and impact”.

It notes that “whole-of-government” approaches to the transition can be strengthened, with NDCs and NAPs integrated throughout national investment strategies. Additionally, it points to country-led coordination or platforms as a route for improving investment.

The roadmap suggests readiness support and project preparation as routes to “revamp” climate finance, alongside support to scale, coordinate and tailor capacity building, the development of country platforms and the provision of “predictable and flexible support for investment frameworks”.

The final “R” is “reshaping”, focused on systems and structures for capital flows. It highlights a number of barriers that still remain for capital flows through developing countries, including outdated clauses in investment treaties.

It recommends prudential regulation, interoperability of taxonomies, climate disclosure frameworks and investment treaties, as key actions to support the reshaping of capital flows.

Additionally, the roadmap suggests that credit rating agencies further refine their methodologies, that jurisdictions adopt voluntary disclosure of climate-related financial risks of financial institutions and that climate stress-test requirements are gradually embedded in supervisory reviews and bank risk management.

Beyond the “five [finance] action fronts”, the roadmap sets out five thematic areas, noting that “where and how finance is directed” matters.

These are: adaptation and loss and damage; clean-energy access and transitions; nature and supporting its guardians; agriculture and food systems; and just transitions.

Within each, it sets out some of the key challenges and suggests routes for financial support.

What happens next?

The Baku to Belem roadmap is not a formal part of COP30 negotiations, but there will be a major launch event at the summit.

Beyond that, the final section of the roadmap sets out that this is the “beginning [of] the journey”. It and details suggested short-term contributions (2026-2028), to serve as “initial, practical steps to inform and guide the early implementation of the roadmap”.

This includes the Azerbaijani and Brazilian presidencies convening an expert group tasked with refining data and developing “concrete financing pathways” to get to $1.3bn in 2035. This will build on the action fronts set out in the roadmap, with the first such report due by October 2026.

Throughout 2026, the presidencies will convene dialogue sessions with parties and stakeholders to discuss how to progress the action fronts over the medium to long term.

The roadmap suggests that to improve predictability, developed countries “could consider” working together on a delivery plan to outline how they expect to achieve the at-least $300bn goal by 2030, as well as other elements of the NCQG.

Additional suggestions in the roadmap are listed in the table below.

(Notably, almost all of these suggestions are made using loose, voluntary language. For example, the roadmap says that developed countries “could” create a delivery plan for their NCQG pathways.)

| Who | What | When |

|---|---|---|

| COP29 and COP30 presidencies | Convene an expert group to develop “concrete financing pathways” | October 2026 |

| COP29 and COP30 presidencies | Convene dialogue sessions with parties and stakeholders | 2026 |

| Developed countries | Creating a delivery plan to set out intended contributions and pathways for NCQG targets | End of 2026 |

| Parties to the Paris Agreement | Request the Standing Committee on Finance to provide an aggregate view on pathways for NCQG | 2027 |

| Governments | Request UN entities to examine and review collaboration options | October 2026 |

| Multilateral climate funds | Report annually on the implementation of their “operational framework” on complementarity and coherence, to enhance cross-fund collaboration. | Annually |

| Multilateral climate funds | Develop monitoring and reporting frameworks and coordination plans, explaining their operations by region, topic and sector | October 2027 |

| Multilateral development banks | Collective report on achieving a new aspirational climate finance target for 2035 | October 2027 |

| Multilateral development banks | Adopt “explicit, ambitious and transparent targets for adaptation and private capital mobilisation” | October 2027 |

| International Monetary Fund | Conduct an assessment of the costs, benefits and feasibility of a new issuance of “special drawing rights” | October 2027 |

| UN regional economic commissions | Develop a study on the potential for expanding debt-for-climate, debt-for-nature and sustainability-linked finance | End of 2027 |

| UNSG-convened working group | Propose a consolidated set of voluntary principles on responsible sovereign borrowing and lending. | October 2026 |

| Crediting rating agencies | Develop a structured dialogue platform with ministries of finance to make progress on refinements to credit rating methodologies. | October 2027 |

| Philanthropies | Expand funding of knowledge hubs | October 2026 |

| UN treaty executive secretariats | Develop a joint report with proposals on economic instruments to support co-benefits and efficiencies | End of 2027 |

| Insurance Development Forum and the V20 | Establish a plan for achieving cheaper and more robust insurance and pre-arranged finance mechanisms for climate disasters | October 2026 |

| Financial Stability Board, the Basel Committee on Banking Supervision and the International Association of Insurance Supervisors | Conduct a joint assessment of whether and how barriers to investment in developing countries could be reduced | October 2027 |

| World’s 100 largest companies | Report annually on how they are contributing towards the implementation of NDCs and NAPs | Annually |

| World’s 100 largest institutional investors | Report annually on how they are contributing towards the implementation of NDCs and NAPs | Annually |

COP29 president Mukhtar Babayev and COP30 president André Aranha Corrêa do Lago conclude in the foreword of the report that while the $1.3bn “journey” is beginning amid “turbulent times”, they are confident that “technological and financial solutions exist”. They add:

“Communities and cities are acting. Families and workers are ready to roll up their sleeves and deliver more action. If resources are strategically redirected and deployed effectively – and if the international financial architecture is reset to fulfil its original purpose of ensuring decent prospects for life – the $1.3tn goal will be an achievable global investment in our present and our future. We are optimistic.”

The post COP30: What does the ‘Baku to Belém roadmap’ mean for climate finance? appeared first on Carbon Brief.

COP30: What does the ‘Baku to Belém roadmap’ mean for climate finance?

Big cuts in generating capacity are coming as the Colorado River struggles to meet demand.

Some day in the next 12 months—maybe in late August, maybe not until next spring— Lake Mead will drop below the critical threshold of 1,035 feet above sea level.

Climate Change

DeBriefed 12 June 2026: El Niño begins | COP31 hosts eye electrification | Atlantic current monitoring at risk

Welcome to Carbon Brief’s DeBriefed.

An essential guide to the week’s key developments relating to climate change.

This week

El Niño begins

‘DOMINO WEATHER’: The natural weather phenomenon El Niño, which can raise global heat and “bring domino weather effects across the planet”, is now underway, the US National Oceanic and Atmospheric Administration (NOAA) declared on Thursday, reported the Washington Post. The Japanese Meteorological Administration also identified the start of El Niño on Wednesday, said Bloomberg. According to the Japanese weather agency, the event is “expected to intensify in the coming months and become very strong later in the year, persisting into at least December”, reported the outlet.

‘SUPER EVENT’: BBC News reported that “many forecasts suggest this could end up as a so-called ‘super’ El Niño” and be “among the strongest ever recorded”. It added: “Coming on top of decades of human-caused warming, it could bring another record-hot year – most likely in 2027 – with disruption to weather, food supplies and economies running well into that year.”

COP31 hosts eye electrification

‘35 BY 35’: COP31 hosts Turkey and Australia have called for countries to support a target of electrifying 35% of global energy use by 2035, reported Politico. Speaking at climate talks in Bonn, Germany, Turkish minister Murat Kurum said that electrification would be a “flagship priority” at the COP31 summit, noted the publication. Kurum added that “electrifying daily life, from transport to buildings and industry” could “protect families and businesses from volatile energy markets”, said the outlet.

WASTE AND BUILDINGS: Climate Home News reported that electrification was one of three priorities unveiled by the COP31 hosts, with the other two being waste and buildings. On buildings, the COP31 hosts “quietly overhauled [their] goal”, Climate Home News said. It reported: “An initial press statement on Monday set out a target ‘to achieve at least a 25% increase in energy efficiency in buildings by 2035’. But…on Tuesday, that was replaced with a different goal to ‘reduce energy consumption intensity in the building sector by at least 25% by 2035’.”

‘HARDEST’ CHALLENGE: Elsewhere in Bonn, UN climate chief Simon Stiell said “governments must stop revisiting climate commitments and start delivering on them”, South Africa’s Mail and Guardian reported. It quoted Stiell as saying: “Tackling the global climate crisis is the hardest but most important thing humanity has ever tried to do together…We are not yet where we need to be. But we are somewhere we have never been before.”

Around the world

- ETS EXTRA: The EU has agreed “stronger” price controls on “ETS2”, its planned trading system for heating and transport emissions, according to Reuters.

- OCEAN STRESS: The rate of sea level rise has doubled in 10 years amid “severe and accelerating” pressures on oceans, said a UN report covered by Time.

- CLIMATE MIGRANTS: Donald Trump’s “immigration crackdown is largely targeting people from the countries most vulnerable to displacement from climate-driven disasters”, according to Guardian analysis.

- ULTRA-RICH: Investments by the world’s ultra-rich in 2022 are linked to nearly $1tn in climate damages, according to a Greenpeace Africa analysis covered by BusinessGreen.

Two

The number of bidders for Trump’s auction for drilling rights in an Arctic wildlife refuge, with big oil companies “sitting out the sale”, reported Bloomberg.

Latest climate research

- As the Arctic warms, increased iceberg activity could “reshape” deep-sea habitats and “elevate” navigational hazards as maritime traffic expands | Nature

- Around 11% of the population of the world’s “rarest great ape”, the Tapanuli orangutan, is estimated to have perished in an extreme rainfall event in Indonesia in 2025 | Current Biology

- Canada’s forests are shifting from a carbon sink to a carbon source, due to “wildfires disturbances” | Global Change Biology

(For more, see Carbon Brief’s in-depth daily summaries of the top climate news stories on Monday, Tuesday, Wednesday, Thursday and Friday.)

Captured

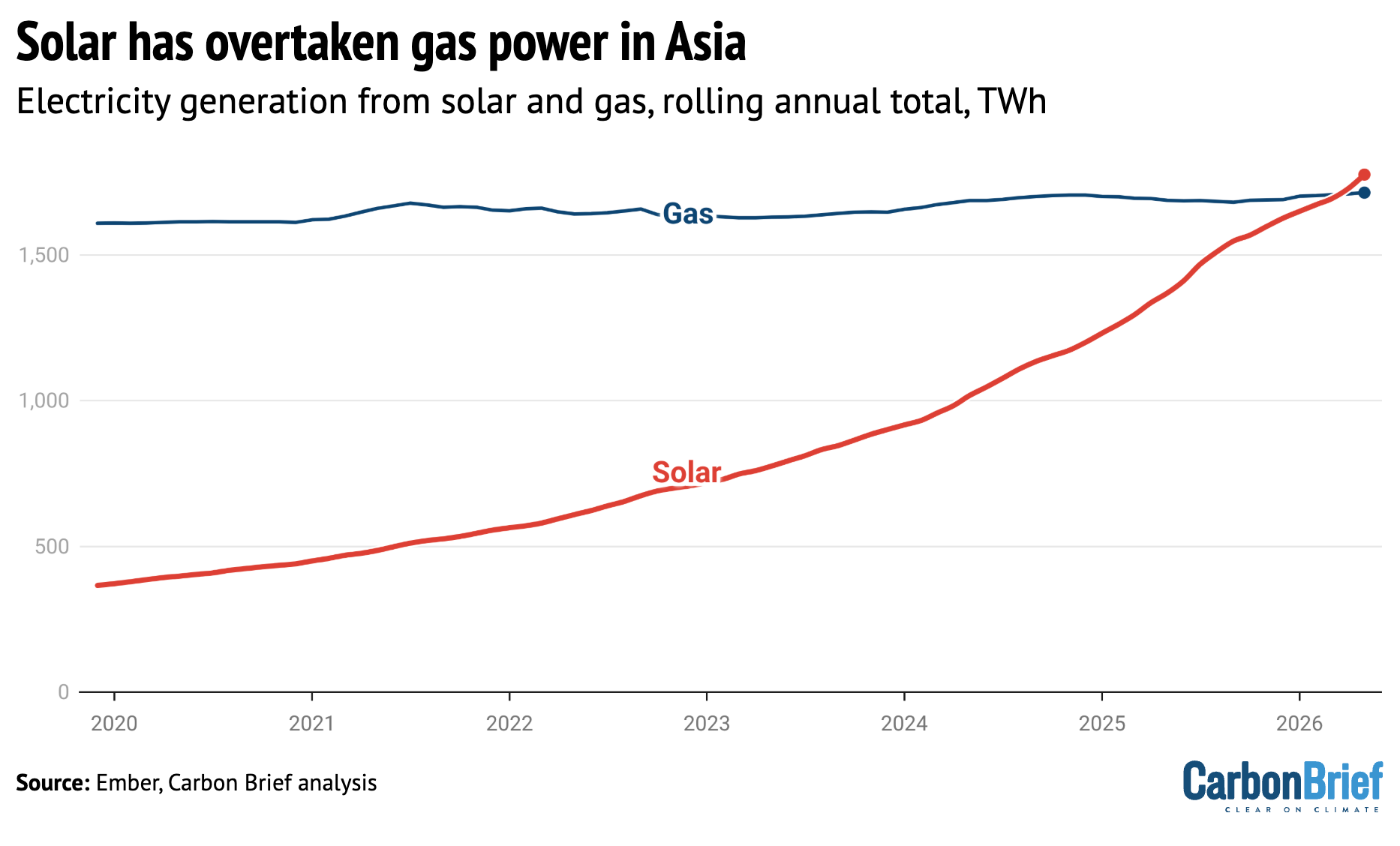

Solar power has overtaken gas in Asia to become the region’s third largest electricity source behind coal and hydropower, according to Carbon Brief analysis of data from the thinktank Ember. Solar became the third largest electricity source for Asia on an annual basis in April 2026, according to the analysis. In the year to April 2026, solar generated 1,727 terawatt hours (TWh), while gas generated 1,711TWh, it added.

Spotlight

Atlantic current monitoring at risk

This week, Carbon Brief reports on how Trump plans could disrupt efforts to track a major ocean current.

The Irminger Sea, a patch of frigid ocean east of Greenland, plays an outsized role in the Earth’s climate.

Here, surface water that has travelled thousands of kilometres from the tropics grows cold and dense enough to sink to the ocean’s depths – a transformation that must occur for the water to begin a long journey back to the southern hemisphere.

This makes the Irminger Sea an “action centre” for the mighty Atlantic Meridional Overturning Circulation (AMOC), the vast system of ocean currents that keeps temperatures in Europe mild.

Last week, the US government announced plans to dismantle ocean moorings installed in the Irminger Sea which, among other things, collect data on the health of the AMOC.

This came as part of a programme to “descope” the Ocean Observatories Initiative, a $368m network of ocean sensors installed in the Pacific and Atlantic oceans.

Two of the moorings earmarked for removal in the Irminger Sea form part of an internationally funded, trans-Atlantic AMOC monitoring array, known as OSNAP, that stretches from Canada to Scotland.

Experts told Carbon Brief the move by the Trump administration highlights the vulnerability of AMOC observation systems around the world. These deep-sea moorings – scattered across the Atlantic – collect real-time data on, among other things, ocean current, temperature, pressure and biochemistry.

Prof Penny Holliday, chief scientific officer of the UK National Oceanography Centre, told Carbon Brief that the OSNAP array, as well as the RAPID array at 26N, are “entirely dependent” on research grants that have to be “continually reapplied for”.

“Funding is perilous all the time,” she said.

A report prepared last month by scientists for Nordic ministers exploring the security of funding for AMOC observing systems warned that RAPID and OSNAP were in “critical condition” and faced “material exposure over an 18-month horizon”. Meanwhile, other key basin-wide and global components of the global AMOC observing system were rated as “at risk”.

It is not just US funding that is uncertain. The report notes, for example, that the five-yearly funding the UK provides to RAPID and OSNAP is “at risk from 2027 due to year-on-year budget reductions” at the Natural Environmental Research Council.

(RAPID is funded by the US and UK, whereas OSNAP is backed by five different countries, with the US contributing half of the total financial support.)

Report co-author Dr Femke de Jong from the Royal Netherlands Institute for Sea Research told Carbon Brief that “continued AMOC observations” are under pressure in “multiple countries”. She said:

“While the risk of a declining AMOC to society is starting to be recognised, there is not yet a system or institution in place to guarantee a way to monitor it.”

AMOC monitoring arrays are still in their infancy – RAPID, the oldest, was launched in 2004. Two decades of data captured so far shows that the AMOC is slowing down. However, scientists will need many more years of data to be able to confidently link the decline to climate change, rather than natural variability in the ocean.

NOC’s Holliday points to the disconnect between scientific and funder timelines:

“The timescale of observations needed in order to be able to detect a climate change signal from the very naturally variable ocean is around 40-60 years…. [And yet], in the Netherlands, they have to apply for a new grant for their ocean moorings every two years. They are going to have to do that for 40 years.

“This is a very inefficient way of getting funding for what should be critical infrastructure.”

This spotlight first appeared in Cited, Carbon Brief’s new fortnightly newsletter focused on climate research. Sign up for free.

Watch, read, listen

‘BEYOND GROWTH’: A group of economists set out a “roadmap for eradicating poverty beyond growth” in the Guardian.

OIL CAMPAIGN: Politico reported on how “oil industry allies” are campaigning against attribution science, including by working to discredit a US National Academies report that “will examine research into the ways corporate climate pollution is intensifying natural disasters”.

‘FIGHT BACK’: For the Apocalyptic Optimist podcast, Dr Dana Fisher spoke to historian and author Dr Naomi Oreskes about how to “fight back” against climate misinformation.

Coming up

- 8-18 June: Bonn climate talks, Bonn, Germany

- 16-18 June: 11th Our ocean conference, Mombasa, Kenya

- 18 June: International Energy Agency Global Hydrogen Review 2026 report launch

Pick of the jobs

- S-Curve Economics, head of road transport | Salary: £75,000-£80,000. Location: Remote (UK)

- UK Department for Energy Security and Net-Zero, speechwriter to the secretary of state | Salary: £62,595-£69,765. Location: London (hybrid)

- Basque Centre for Climate Change, postdoctoral researcher for JustBioSolar project | Salary: €27,040-€34,320. Location: Bilbao, Spain

- Boston Globe climate science and environment reporter | Salary: Unknown. Location: Boston, US

DeBriefed is edited by Daisy Dunne. Please send any tips or feedback to debriefed@carbonbrief.org.

This is an online version of Carbon Brief’s weekly DeBriefed email newsletter. Subscribe for free here.

The post DeBriefed 12 June 2026: El Niño begins | COP31 hosts eye electrification | Atlantic current monitoring at risk appeared first on Carbon Brief.

Solar has overtaken gas power in Asia to become the continent’s third-largest source of electricity, according to new analysis by Carbon Brief.

The rapid expansion of solar power in nations such as China, India and Pakistan has seen its annual output increase nearly fourfold since 2020.

Asia accounts for around 60% of the world’s solar-power growth in this period, putting the continent at the heart of the global solar boom.

Coal and hydropower remain Asia’s largest sources of electricity, generating roughly 52% and 12% of the continent’s power each year, respectively.

Yet despite expectations that gas power would undergo “explosive growth” in the region, output has stalled due to supply disruptions, relatively high gas prices and growth in clean alternatives.

In contrast, solar has surged, generating some 1,727 terawatt hours (TWh) of electricity in the 12 months to April 2026.

As the chart below shows, this pushes it just ahead of gas, which generated 1,711TWh over the same period and has remained roughly flat for the past several years.

The milestone reflects wider trends in the global electricity mix, with monthly generation from both wind and solar surpassing gas generation globally for the first time in April 2026.

Asia’s solar expansion has been driven largely by China, which accounts for nearly three-quarters of the growth in the region’s output since 2020.

Record installations in 2025 took China’s cumulative installed capacity to 1.2 terawatts (TW) by the end of the year.

China also dominates global solar supply chains, hosting more than 80% of solar manufacturing capacity.

This means it has played an important role in enabling solar deployment in other Asian countries through cheap solar-panel exports. Amid the energy crisis sparked by the Iran war, Chinese solar exports to Asia doubled to reach a record 39 gigawatts (GW) in March 2026.

Meanwhile, Asian countries have faced a number of challenges in expanding gas-power capacity. Most of these nations are reliant on imported liquified natural gas (LNG) to support their gas-power projects.

Around 81GW of planned gas capacity in Asia was cancelled in 2022 and 2023, amid LNG supply disruptions and price spikes following Russia’s invasion of Ukraine.

LNG import terminals and pipelines have faced delays and cancellations in south Asia and South Korea as a result of rising fuel and construction costs, as well as weak demand for gas power.

Global gas turbine shortages have also delayed plans to build new gas-power plants in Vietnam and the Philippines.

While Asia’s gas-power capacity increased by 22% between 2019 and 2024, gas-fired generation has only increased by a modest 6% over the same period. Existing gas plants are not always operating at high capacities, as gas is outcompeted by other fuels.

These trends are not uniform across the region, with increased generation in some countries – such as China and Taiwan – being offset by declines in others – such as Japan and India.

Although China has nearly doubled its gas -power generation in the past decade, gas supply issues and high prices make it less competitive than coal and renewables.

The expansion of clean energy has also reduced the need for gas-fired generation in many Asian countries. Pakistan’s widely reported “boom” in rooftop solar is one notable example of this trend.

According to the International Energy Agency (IEA), the latest energy crisis has “renewed gas supply reliability and affordability concerns” among gas-importing countries in Asia, many of which are highly dependent on gas flows through the strait of Hormuz.

Methodology

The figures in this article are based on Ember’s monthly and annual electricity data for Asia.

Annual data was used for the year-end data points, as the coverage is more complete compared to the monthly data.

Rolling annual totals based on monthly data were used to interpolate between the annual data points.

The figures in the chart are based on Ember’s definition of Asia, which covers the following countries: Afghanistan, Armenia, Azerbaijan, Bangladesh, Bhutan, Brunei, Cambodia, China, Georgia, Hong Kong, India, Indonesia, Japan, Kazakhstan, North Korea, Kyrgyzstan, Laos, Macao, Malaysia, Maldives, Mongolia, Myanmar, Nepal, Pakistan, the Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Tajikistan, Thailand, Timor-Leste, Turkmenistan, Uzbekistan and Vietnam.

This does not include some countries that are part of the continent of Asia and that use relatively large amounts of gas, such as Iran, Saudi Arabia, the United Arab Emirates (UAE) and Russia.

The post Analysis: Solar overtakes gas power in Asia for first time ever appeared first on Carbon Brief.

Analysis: Solar overtakes gas power in Asia for first time ever

-

Climate Change10 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases10 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy8 months ago

Renewable Energy8 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases11 months ago

嘉宾来稿:探究火山喷发如何影响气候预测