More than 60 global companies, including Apple, Amazon, BYD, Salesforce, Mars, and Schneider Electric, are pushing back against proposed changes to global emissions reporting rules. The group is calling for more flexibility under the Greenhouse Gas Protocol (GHG Protocol), the most widely used framework for measuring corporate carbon footprints.

The companies submitted a joint statement asking that new requirements, especially those affecting Scope 2 emissions, remain optional rather than mandatory. Their letter stated:

“To drive critical climate progress, it’s imperative that we get this revision right. We strongly urge the GHGP to improve upon the existing guidance, but not stymie critical electricity decarbonization investments by mandating a change that fundamentally threatens participation in this voluntary market, which acts as the linchpin in decarbonization across nearly all sectors of the economy. The revised guidance must encourage more clean energy procurement and enable more impactful corporate action, not unintentionally discourage it.”

The debate comes at a critical time. Corporate climate disclosures now influence trillions of dollars in capital flows, while stricter reporting rules are being introduced across major economies.

The Rulebook for Carbon: What the GHG Protocol Is and Why It’s Being Updated

The Greenhouse Gas Protocol is the world’s most widely used system for measuring corporate emissions. It is used by over 90% of companies that report greenhouse gas data globally, making it the foundation of most climate disclosures.

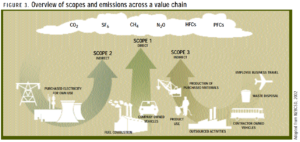

It divides emissions into three categories:

- Scope 1: Direct emissions from operations

- Scope 2: Emissions from purchased electricity

- Scope 3: Emissions across the value chain

The current Scope 2 rules were introduced in 2015, but energy markets have changed since then. Renewable energy has expanded, and companies now play a major role in funding clean power.

Corporate buyers have already supported more than 100 gigawatts (GW) of renewable energy capacity globally through voluntary purchases. This shows how influential the current system has been.

The GHG Protocol is now updating its rules to improve accuracy and transparency. The revision process includes input from more than 45 experts across industry, government, and academia, reflecting its global importance.

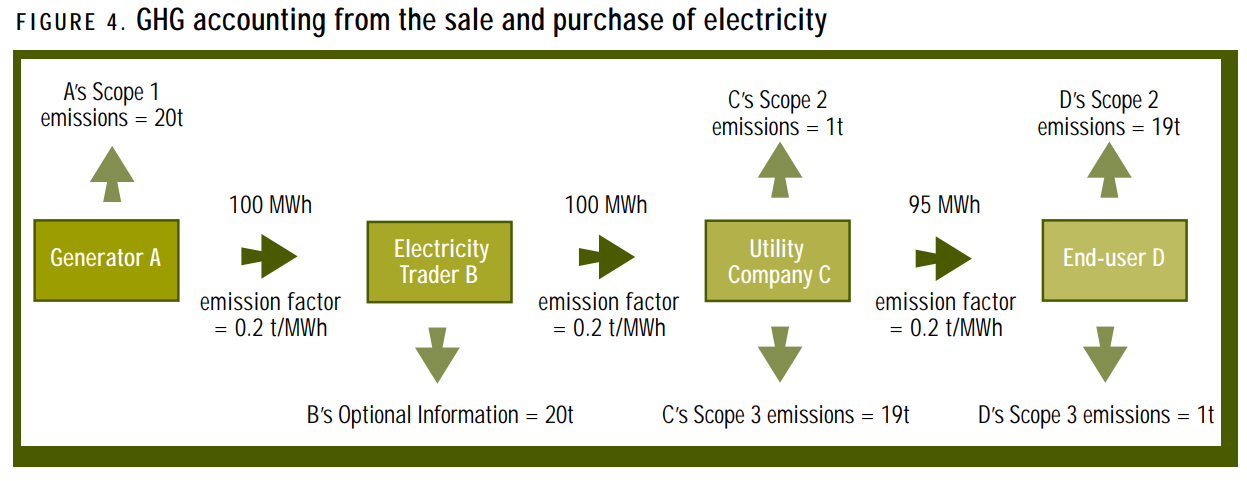

Scope 2 Shake-Up: The Battle Over Real-Time Carbon Tracking

The proposed update would shift how companies report electricity emissions. Instead of using flexible systems like renewable energy certificates (RECs), companies would need to match their electricity use with clean energy that is:

- Generated at the same time, and

- Located in the same grid region.

This is known as “24/7” or hourly or real-time matching. It aims to reflect the actual impact of electricity use on the grid. Companies, including Apple and Amazon, say this shift could create challenges.

According to industry feedback, stricter rules could raise energy costs and limit access to renewable energy in some regions. It can also slow corporate investment in new clean energy projects.

The concern is that many markets do not yet have enough renewable supply for real-time matching. Infrastructure for tracking hourly emissions is also still developing.

This creates a key tension. The new rules could improve accuracy and reduce greenwashing. But they may also make it harder for companies to scale clean energy quickly.

The outcome will shape how companies measure emissions, invest in renewables, and meet net-zero targets in the years ahead.

Why More Than 60 Companies Oppose the Changes

The companies argue that stricter rules could slow climate progress rather than accelerate it. Their main concern is cost and feasibility. Many regions still lack enough renewable energy to support real-time matching. For global companies, aligning energy use across different grids is complex.

In their joint statement, the group warned that mandatory changes could:

- Increase electricity prices,

- Reduce participation in voluntary clean energy markets, and

- Slow investment in renewable energy projects.

They argue that current market-based systems, such as RECs, have helped scale clean energy quickly over the past decade. Removing flexibility could weaken that momentum.

This reflects a broader tension between accuracy and scalability in climate reporting.

Big Tech Pushback: Apple and Amazon’s Climate Progress

Despite their push for flexibility, both companies have made measurable progress on emissions reduction.

Apple reports that it has reduced its total greenhouse gas emissions by more than 60% compared to 2015 levels, even as revenue grew significantly. The company is targeting carbon neutrality across its entire value chain by 2030. It also reported that supplier renewable energy use helped avoid over 26 million metric tons of CO₂ emissions in 2025 alone.

In addition, about 30% of materials used in Apple products in 2025 were recycled, showing a shift toward circular manufacturing.

Amazon has also set a net-zero target for 2040 under its Climate Pledge. The company is one of the world’s largest corporate buyers of renewable energy and continues to invest heavily in clean power, logistics electrification, and low-carbon infrastructure.

Both companies argue that flexible accounting frameworks have supported these investments at scale.

The Bigger Challenge: Scope 3 and Digital Emissions

The debate over Scope 2 reporting is only part of a larger issue. For most large companies, Scope 3 emissions account for more than 70% of total emissions. These include supply chains, product use, and outsourced services.

In the technology sector, emissions are rising due to:

- Data centers,

- Cloud computing, and

- Artificial intelligence workloads.

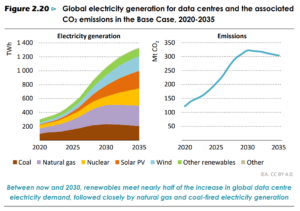

Global data centers already consume about 415–460 terawatt-hours (TWh) of electricity per year, equal to roughly 1.5%–2% of global power demand. This figure is expected to increase sharply. The International Energy Agency estimates that data center electricity demand could double by 2030, driven largely by AI.

This creates a major reporting challenge. Even with cleaner electricity, total emissions can rise as digital demand grows.

Climate Reporting Rules Are Tightening Globally

The pushback comes as climate disclosure requirements are expanding and becoming more standardized across major economies. What was once voluntary ESG reporting is steadily shifting toward mandatory, audit-ready climate transparency.

In the European Union, the Corporate Sustainability Reporting Directive (CSRD) is now active. It requires large companies and, later, listed SMEs, to share detailed sustainability data. This data must match the European Sustainability Reporting Standards (ESRS). This includes granular reporting on emissions across Scope 1, 2, and increasingly Scope 3 value chains.

In the United States, the Securities and Exchange Commission (SEC) aims for mandatory climate-related disclosures for public companies. This includes governance, risk exposure, and emissions reporting. However, some parts of the rule face legal and political scrutiny.

The United Kingdom has included climate disclosure through TCFD requirements. Now, it is moving toward ISSB-based global standards to make comparisons easier. Similarly, Canada is progressing with ISSB-aligned mandatory reporting frameworks for large public issuers.

In Asia, momentum is also accelerating. Japan is introducing the Sustainability Standards Board of Japan (SSBJ) rules that match ISSB standards. Meanwhile, China is tightening ESG disclosure rules for listed companies through updates from its securities regulators. Singapore has also mandated climate reporting for listed companies, with phased Scope 3 expansion.

A clear trend is forming across jurisdictions: climate disclosure is aligning with ISSB global standards. There’s a growing focus on assurance, comparability, and transparency in value-chain emissions.

This regulatory tightening raises the bar significantly for corporations. The challenge is clear. Companies must:

- Align with multiple evolving disclosure regimes,

- Ensure emissions data is verifiable and auditable, and

- Expand reporting across complex global supply chains.

Balancing operational growth with compliance is becoming increasingly complex as climate regulation converges and intensifies worldwide.

A Turning Point for Global Carbon Accounting

The outcome of this debate could shape global carbon accounting standards for years.

If stricter rules are adopted, emissions reporting will become more precise. This could improve transparency and reduce greenwashing risks. However, it may also increase compliance costs and limit flexibility.

If the proposed changes remain optional, companies may continue using current accounting methods. This could support faster clean energy investment, but may leave gaps in reporting accuracy.

The new rules could take effect as early as next year, making this a near-term decision for global companies.

The push by Apple, Amazon, and other companies highlights a key tension in climate strategy. On one side is the need for accurate, real-time emissions reporting. On the other is the need for flexible systems that support large-scale clean energy investment.

As digital infrastructure expands and energy demand rises, how emissions are measured will matter as much as how they are reduced. The next phase of climate action will depend not just on targets—but on the systems used to track them.

The post Apple, Amazon Lead 60+ Firms to Ease Global Carbon Reporting Rules appeared first on Carbon Credits.

Carbon Footprint

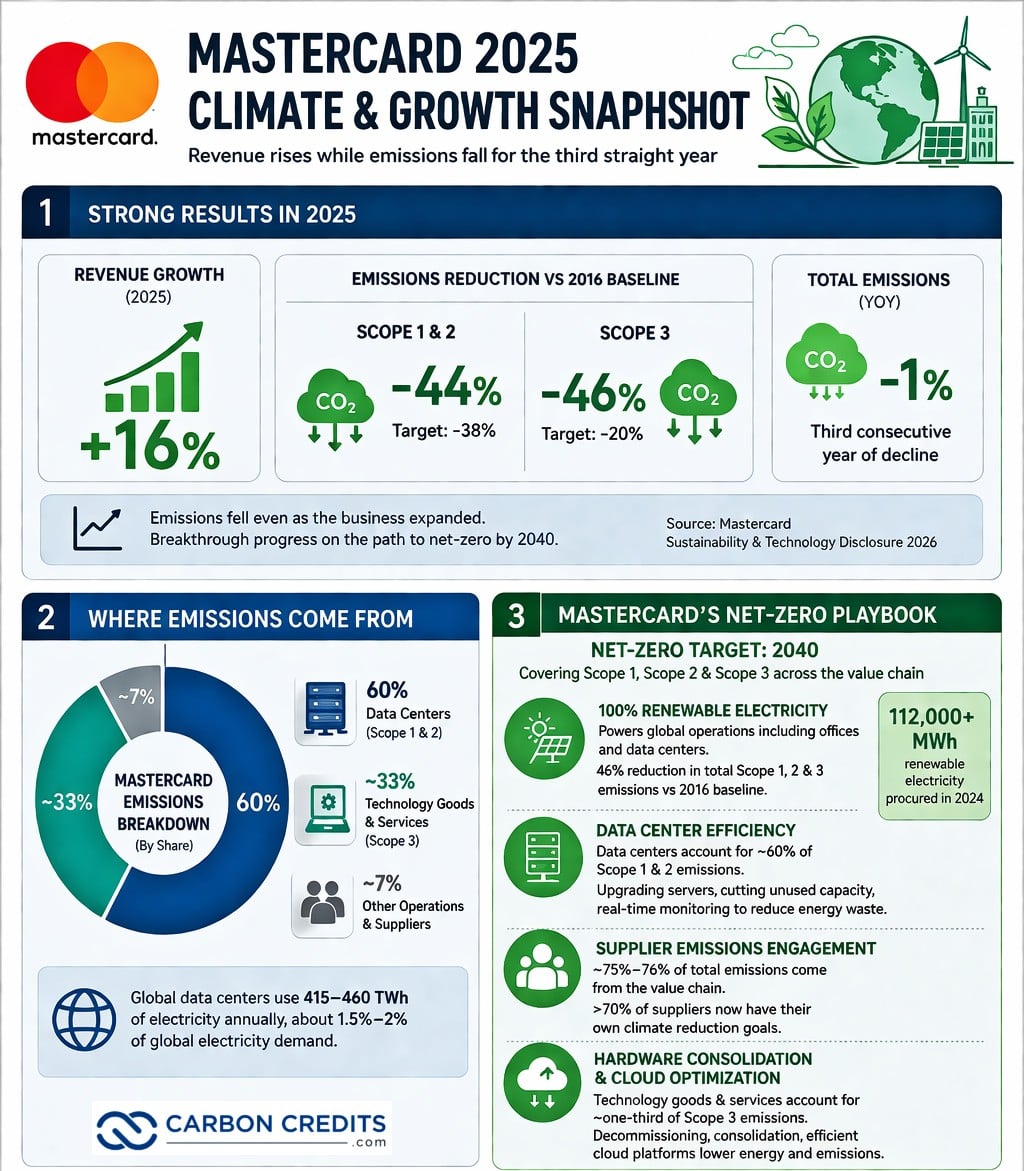

Mastercard Beats 2025 Emissions Targets as Revenue Rises 16%, Breaking the Growth vs Carbon Trade-Off

Mastercard says it has exceeded its 2025 emissions reduction targets while continuing to grow its global business. The company reduced emissions across its operations even as revenue increased strongly in 2025.

The update comes from Mastercard’s official sustainability and technology disclosure published in 2026. It confirms progress toward its long-term goal of net-zero emissions by 2040, covering its full value chain.

The results are important for the financial technology sector. Digital payments depend heavily on data centers and cloud systems, which are energy-intensive and linked to rising global emissions.

Breaking the Pattern: Emissions Fall While Revenue Rises

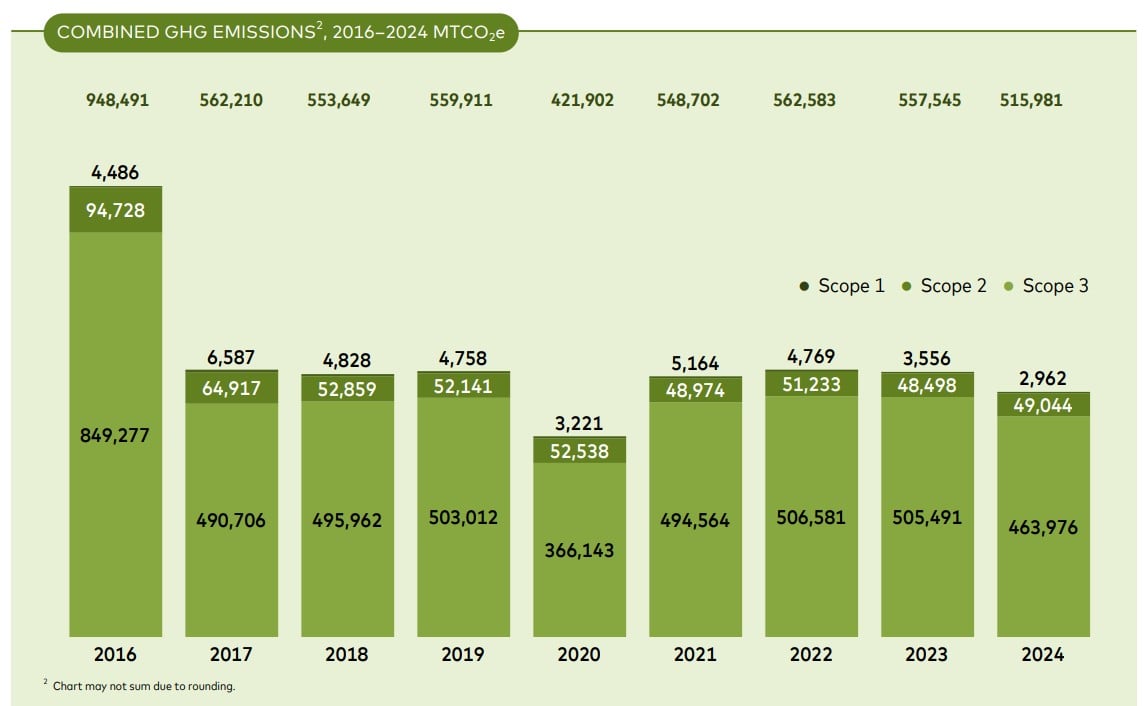

In 2025, Mastercard surpassed its interim climate targets compared with a 2016 baseline. The company reported a 44% reduction in Scope 1 and Scope 2 emissions, beating its target of 38%. It also achieved a 46% reduction in Scope 3 emissions, far exceeding its 20% target.

At the same time, Mastercard recorded 16% revenue growth in 2025. This shows that emissions reductions continued even as the business expanded. Mastercard Chief Sustainability Officer Ellen Jackowski and Senior Vice President of Data and Governance Adam Tenzer wrote:

“These results reflect a comprehensive approach built on renewable energy investment and procurement, supply chain engagement, and embedding environmental sustainability into everyday business decisions.”

The company also reported a 1% year-on-year decline in total emissions, marking the third consecutive year of emissions reduction. This is important because digital payment networks usually grow with higher computing demand.

Mastercard says this trend reflects improved efficiency across its operations, better infrastructure use, and increased reliance on cleaner energy sources.

The Hidden Footprint: Why Data Centers Drive Mastercard’s Emissions

A large share of Mastercard’s emissions comes from its digital infrastructure. According to the company’s sustainability report, data centers account for about 60% of Scope 1 and Scope 2 emissions. Technology-related goods and services make up roughly one-third of Scope 3 emissions.

This reflects how modern financial systems operate. Digital payments, fraud detection, and AI-based analytics require a large-scale computing infrastructure.

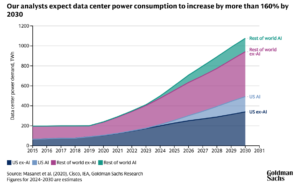

Global data centers already consume about 415–460 TWh of electricity per year, equal to roughly 1.5%–2% of global electricity demand. This number is expected to rise as AI usage expands.

Mastercard’s challenge is similar to that of other digital companies. Higher transaction volume usually leads to greater computing needs. This can raise emissions unless we improve efficiency.

To manage this, the company is focusing on renewable energy procurement, hardware consolidation, and more efficient software systems.

Carbon-Aware Technology Becomes Core to Operations

Mastercard is integrating sustainability directly into its technology systems rather than treating it as a separate reporting function. Since 2023, the company has developed a patent-pending system that assigns a Sustainability Score to its technology infrastructure. This system measures environmental impact in real time.

It tracks factors such as:

- Energy use in kilowatt-hours,

- Regional carbon intensity of electricity,

- Server utilization rates,

- Hardware lifecycle efficiency, and

- Data processing location.

This allows engineers to design systems with lower carbon impact.

The company also uses carbon-aware software design. This means computing workloads can be adjusted to reduce energy use when carbon intensity is high in certain regions.

This approach reflects a wider trend in the technology and financial sectors. More companies are now including carbon tracking in their main infrastructure choices. They no longer see it just as a reporting task.

Powering Payments: Mastercard’s Net-Zero Playbook

Mastercard has committed to reaching net-zero emissions by 2040, covering Scope 1, Scope 2, and Scope 3 emissions across its value chain. The target is aligned with science-based climate pathways and includes operations, suppliers, and technology infrastructure.

To achieve this, the company is focusing on four main areas.

-

Increasing renewable energy use in operations

Mastercard already powers its global operations with 100% renewable electricity. This covers offices and data centers in multiple regions.

The company has also achieved a 46% reduction in total Scope 1, 2, and 3 emissions compared to its 2016 baseline. It continues to use renewable energy purchasing to maintain this progress.

In 2024, Mastercard procured over 112,000 MWh of renewable electricity, supporting lower emissions from its global operations.

-

Improving energy efficiency in data centers

Data centers account for about 60% of Mastercard’s Scope 1 and 2 emissions. To reduce this, Mastercard is upgrading servers, cutting unused computing capacity, and improving workload efficiency. It also uses real-time monitoring to reduce energy waste.

These improvements helped keep operational emissions stable in 2024, even as computing demand increased. Efficiency gains combined with renewable energy use supported this outcome.

-

Working with suppliers to reduce emissions

Around 75%–76% of Mastercard’s total emissions come from its value chain. This includes cloud providers, technology partners, and hardware suppliers.

To address this, Mastercard works with suppliers to set emissions targets and improve reporting. More than 70% of its suppliers now have their own climate reduction goals.

-

Upgrading and consolidating hardware systems

Mastercard is reducing emissions by improving its hardware systems. It decommissions unused servers, consolidates infrastructure, and shifts to more efficient cloud platforms.

Technology goods and services account for about one-third of Scope 3 emissions. By reducing unnecessary hardware and extending equipment life, Mastercard lowers both energy use and manufacturing-related emissions while maintaining system performance.

Renewable energy procurement is central to its strategy. It’s crucial for powering data centers, as they account for most of their operational emissions.

Mastercard works with suppliers because a large part of emissions comes from the value chain. This includes technology manufacturing and cloud services. By 2025, the company exceeded several short-term climate goals. This shows early progress on its long-term net-zero path.

ESG Pressure Hits Fintech: The New Rules of Digital Finance

Mastercard’s results come during a period of rising ESG pressure across the financial sector. Banks, payment networks, and fintech companies must now disclose emissions. This is especially true for Scope 3 emissions, which cover supply chain and digital infrastructure impacts.

Several global trends are shaping the industry:

- Growing regulatory focus on climate disclosure,

- Rising investor demand for ESG transparency,

- Expansion of digital payments and cloud computing, and

- Increased energy use from AI and data processing.

Data centers are becoming a major focus area because they link financial services to energy consumption. In Mastercard’s case, they are the largest source of operational emissions.

At the same time, financial institutions are expected to align with net-zero targets between 2040 and 2050. This depends on regional regulations and climate frameworks. Mastercard’s early progress places it ahead of many peers in meeting short-term emissions goals.

Decoupling Growth From Emissions

One of the most important signals from Mastercard’s 2025 results is the separation of business growth from emissions.

The company achieved 16% revenue growth while reducing total emissions by 1% year-on-year. This marks a continued pattern of emissions decline alongside business expansion.

Mastercard attributes this to improved system efficiency, renewable energy use, and better infrastructure management. In simple terms, the company is processing more transactions without a matching rise in emissions.

This trend is important because digital payment systems normally scale with computing demand. Without efficiency gains, emissions would typically rise with business growth.

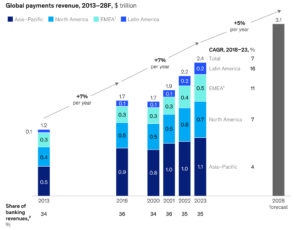

Looking ahead, demand will continue to grow. Global payments revenue is projected to reach around $3.1 trillion by 2028, according to McKinsey & Company, growing at close to 10% annually.

Global data center electricity demand might double by 2030. This rise is mainly due to AI workloads, says the International Energy Agency. Mastercard’s results show that tech upgrades can lower the carbon impact of digital finance. This is true even as global usage rises.

The Takeaway: Fintech’s Proof That Growth and Emissions Can Split

Mastercard’s 2025 sustainability performance shows measurable progress toward its net-zero goal. At the same time, major challenges remain. Data centers continue to be the largest emissions source, and global digital activity is still expanding rapidly due to AI and cloud computing.

Mastercard’s approach shows how financial technology companies are adapting. Sustainability is no longer a separate goal. It is becoming part of how digital systems are designed and operated.

The next test will be whether these efficiency gains can continue to outpace the rapid growth of global digital payments and AI-driven financial systems.

The post Mastercard Beats 2025 Emissions Targets as Revenue Rises 16%, Breaking the Growth vs Carbon Trade-Off appeared first on Carbon Credits.

China is backing a Beijing-based startup called Orbital Chenguang with about 57.7 billion yuan ($8.4 billion) in credit lines to build space-based data centers, according to media reports. The funding comes from major state-linked banks and signals one of the largest known investments in orbital computing infrastructure.

The move highlights a growing global race to build computing systems in space. It also puts China in direct competition with companies like SpaceX, which is exploring space-based data infrastructure, too.

Orbital Chenguang Builds State-Backed Space Computing System

Orbital Chenguang is a startup in Beijing supported by the Beijing Astro-future Institute of Space Technology. This institute works with the city’s science and technology authorities.

The company has received credit line support from major Chinese financial institutions, including:

- Bank of China,

- Agricultural Bank of China,

- Bank of Communications,

- Shanghai Pudong Development Bank, and

- CITIC Bank.

These are credit lines, not fully deployed cash. But the scale shows strong institutional backing.

The project is part of a wider national strategy focused on commercial space, AI infrastructure, and advanced computing systems.

China’s state space contractor, CASC (China Aerospace Science and Technology Corporation), has shared plans under its 15th Five-Year Plan. These include ideas for large-scale space computing systems, aiming for gigawatt power.

Space Data Center Plan Targets 2035 Gigawatt Capacity

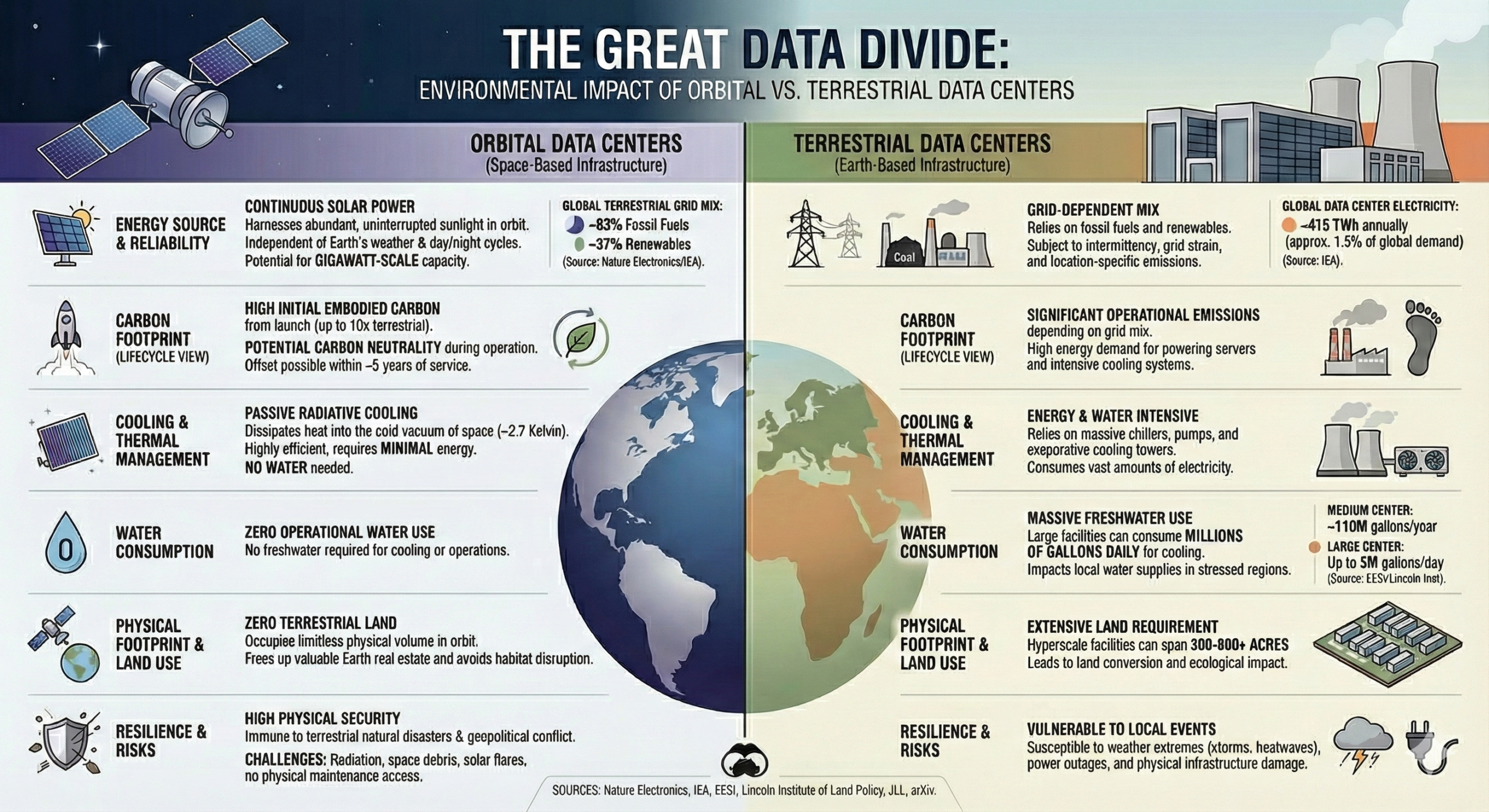

According to Chinese media reports, Orbital Chenguang plans to build a constellation in a dawn-dusk sun-synchronous orbit at 700–800 km altitude. The long-term target is a gigawatt-scale space data center by 2035.

The development plan is divided into phases:

- 2025–2027: Launch early computing satellites and solve technical barriers.

- 2028–2030: Link space-based systems with Earth-based data centers.

- 2030–2035: Scale toward large orbital computing infrastructure.

The design relies on continuous solar energy and natural cooling in space. These features could reduce reliance on land-based power grids and cooling systems.

China has proposed two satellite constellations to the International Telecommunication Union (ITU). These plans include a total of 96,714 satellites. This shows China’s long-term goals for space infrastructure and spectrum control.

The AI Energy Crunch Pushing Computing Into Orbit

The push into orbital data centers is closely linked to rising AI demand. Global data centers consumed about 415–460 terawatt-hours (TWh) of electricity in 2024, equal to roughly 1.5%–2% of global power use. This figure is rising quickly due to AI workloads.

Some industry projections show demand could exceed 1,000 TWh by 2026, nearly equal to Japan’s total electricity consumption.

AI systems require massive computing power, which increases energy use and cooling needs. In many regions, electricity supply—not hardware—is now the main constraint on AI expansion.

China’s strategy aims to address this by moving part of the computing load into space, where solar energy is more stable and continuous.

Carbon Impact: Earth vs Space Computing Trade-Off

Data centers already create a large carbon footprint. In 2024, they emitted about 182 million tonnes of CO₂, based on global electricity use of roughly 460 TWh and an average carbon intensity of 396 grams of CO₂ per kWh. This is according to the International Energy Agency report, as shown in the chart below.

Future projections show even faster growth. The sector could generate up to 2.5 billion tonnes of CO₂ emissions by 2030, driven by AI expansion. This is where orbital systems come in. They aim to reduce emissions during operation by using:

- Continuous solar energy,

- Passive cooling in vacuum conditions, and

- Reduced dependence on fossil-fuel grids.

However, space systems also introduce new emissions. Rocket launches used about 63,000 tonnes of propellant in 2022, producing CO₂ and atmospheric pollutants. Lifecycle studies suggest that over 70% of emissions from space systems typically come from manufacturing and launch activities.

In addition, hardware in orbit often has a lifespan of only 5–6 years, which increases replacement cycles and launch frequency. This creates a key trade-off:

- Lower operational emissions in space, and

- Higher lifecycle emissions from launches and manufacturing.

Research suggests that, in some scenarios, orbital computing could produce up to 10 times higher total carbon emissions than terrestrial systems when full lifecycle impacts are included.

China’s Expanding Space-Tech Ecosystem

Orbital Chenguang is not operating alone. Several Chinese companies are working on similar in-orbit computing systems, including ADA Space, Zhejiang Lab, Shanghai Bailing Aerospace, and Zhongke Tiansuan.

These firms are developing satellite-based computing and AI processing systems. This shows that orbital computing is not a single project. It is part of a broader national push across government, industry, and research institutions.

China’s space strategy combines commercial space growth with national technology planning. It aims to build integrated systems that connect satellites, cloud computing, and terrestrial networks.

The Space-AI Arms Race: China vs SpaceX vs Google

China is not alone in exploring space-based computing. Companies in the United States are also developing orbital data infrastructure concepts. These include early-stage research and private sector projects by firms such as SpaceX and Google.

However, these systems face major challenges:

- High launch costs,

- Heat and thermal control issues,

- Limited data transmission bandwidth, and

- Hardware durability in space.

Despite these challenges, interest is growing because AI demand is rising faster than Earth-based infrastructure can scale. The competition is now moving toward who can solve energy and computing limits first—on Earth or in space.

Market Outlook: AI, Energy, and Space Infrastructure Converge

The global data center industry is entering a period of rapid expansion. Electricity demand from data centers could double by 2030, driven mainly by AI workloads and cloud computing growth. Power supply is becoming a limiting factor in many regions.

At the same time, the global space economy is expanding into a multi-hundred-billion-dollar industry, supported by satellites, communications, and emerging technologies like orbital computing.

- Orbital data centers sit at the intersection of three major trends: rapid AI growth, rising energy constraints, and expansion of space infrastructure.

China’s $8.4 billion credit-backed push through Orbital Chenguang signals confidence in this convergence. However, key barriers remain, such as high cost of launches, engineering complexity, short satellite lifespans (5-6 years), and regulatory uncertainty in orbital systems.

Because of these limits, orbital data centers are unlikely to replace Earth-based systems in the near term. Instead, they may form a hybrid system where some workloads move to space while most remain on Earth.

Space Is Becoming the Next Data Center Frontier

China’s investment in Orbital Chenguang marks one of the most significant moves yet in the emerging field of space-based computing. Backed by major Chinese banks, municipal science institutions, and national space contractors like CASC, the project shows how seriously China is treating orbital infrastructure.

The strategy connects AI growth, energy demand, and climate pressures into a single long-term vision. But the trade-offs are complex. Orbital data centers may reduce operational emissions, but they also introduce high lifecycle carbon costs and major technical challenges.

The global race is now underway. With companies like SpaceX, Google, and Chinese tech firms exploring similar ideas, space is becoming a new frontier for digital infrastructure. The outcome will depend on whether orbital systems can scale efficiently—and whether their carbon benefits can outweigh the emissions cost of building them.

The post China’s $8.4B Orbital Data Center Push Sets Up Space-Based AI Showdown With SpaceX appeared first on Carbon Credits.

-

Climate Change9 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases9 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits