Donald Trump has overseen more retirements of coal-fired power stations than any other US president, according to Carbon Brief analysis.

His administration’s latest efforts to roll back US climate policy have been presented by interior secretary Doug Burgum as an opportunity to revive “clean, beautiful, American coal”.

The administration is in the process of attempting to repeal the 2009 “endangerment” finding, which is the legal underpinning of many federal climate regulations.

On 11 February, the White House issued an executive order on “America’s beautiful clean coal power generation fleet”, calling for government contracts and subsidies to keep plants open.

On the same day, Trump was presented with a trophy by coal-mining executives declaring him to be the “undisputed champion of beautiful clean coal”.

These words are in sharp contrast to Trump’s record in office, with more coal-fired power plants having retired under his leadership than any other president, as shown in the figure below.

This is because coal plants have been uneconomic to operate compared with cheaper gas and renewables – and because most of the US coal fleet is extremely old.

In total, some 57 gigawatts (GW) of coal capacity has already been retired during Trump’s first and second terms in office, compared with 48GW under Obama’s two full terms and 41GW under Biden’s single term.

Even in relative terms, the US has lost a larger proportion of its remaining coal fleet for each year of Trump’s presidencies than for either of his recent predecessors.

Trump’s record hints at the many practical and economic factors that have driven US coal closures, regardless of the preferences of the president of the day.

Indeed, Trump made variousefforts to prop up coal power during his first term in office. These were ultimatelyunsuccessful, as the figure below illustrates.

Coal plants have been retiring in large numbers over the past 20 years because they were uneconomic relative to cheaper sources of electricity, including renewables and gas.

These unfavourable market conditions, alongside air pollution regulations unrelated to climate change, have resulted in a steady parade of coal closures under successive presidents.

By 2024, wind and solar were generating more electricity in the US than coal.

More recently, analysis from the US Energy Information Administration shows that surging power prices have improved the economics of both coal and gas-fired power plants.

These rising prices have been driven by increasing demand, including from data centres, and by higher gas prices, due to increasing exports at liquefied natural gas (LNG) terminals.

These factors saw coal-power output increase by 13% year-on-year in 2025, only the second rise in a decade of steady decline for the fuel, according to the Rhodium Group.

Nevertheless, many utilities have still been looking to shutter their ageing coal-fired power plants.

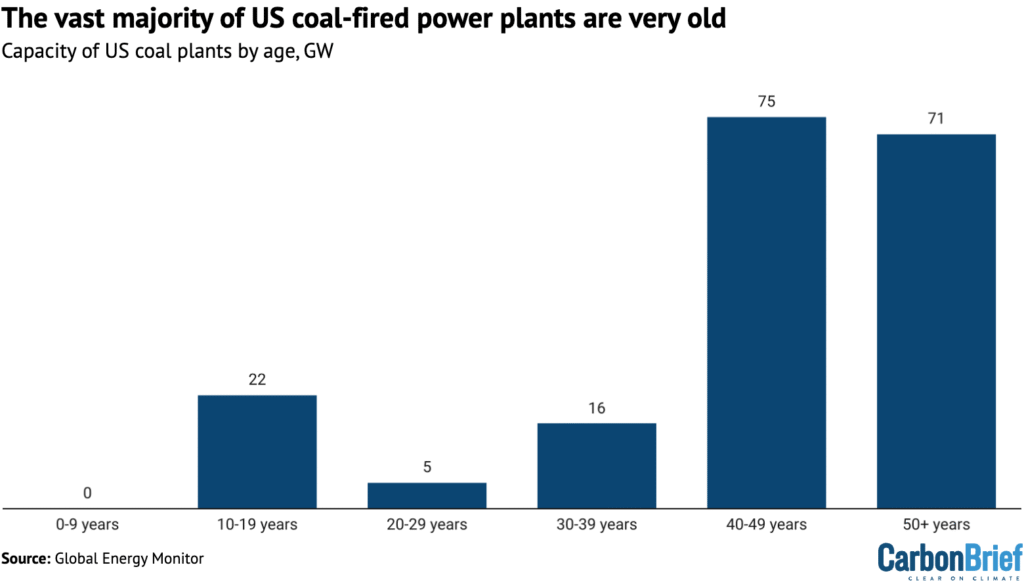

The vast majority of US coal plants are nearing retirement. Three-quarters of US coal capacity is more than four decades old and only 14% is less than 20 years old, as shown in the figure below.

In response, the Trump administration has recently invoked legislation designed for wartime emergencies to force a number of uneconomic coal plants to remain open.

Despite Trump’s efforts, clean energy made up 96% of the new electricity generation capacity added to the US grid in 2025. None of the new capacity came from coal power.

The post Analysis: Trump has overseen more coal retirements than any other US president appeared first on Carbon Brief.

Analysis: Trump has overseen more coal retirements than any other US president

Researchers say fossil fuel burning and other human activities caused nearly all the rapid warming of the past decade.

Former federal climate experts warn that atmospheric carbon dioxide concentrations hit a record high in May and that the monthly average global temperature this summer could rise as much as 3.5 degrees Fahrenheit (1.9 degrees Celsius) above the pre-industrial benchmark used to measure the heating from greenhouse gases.

Scientists Warn of Summer Heat Spikes as Global Warming Edges Toward 2C

Climate Change

A Sloth Exhibitor Shut Down by New York Wants a Florida Comeback—and Florida Licensed Him

Larry Wallach’s commercial exotic animal business was shuttered by New York courts and federal regulators declined his application to exhibit animals. Now he’s pitching a new sloth encounter business in Florida.

An exotic animal exhibitor whose sloth-encounters business was shuttered by New York courts is attempting to relaunch his operations in Florida, right as the state grapples with the fallout from sloth deaths at a different tourist attraction.

A Sloth Exhibitor Shut Down by New York Wants a Florida Comeback—and Florida Licensed Him

Grand Staircase-Escalante National Monument has been targeted for downsizing and protection rollbacks for years. But the latest attempt to overturn its management plan in Congress has stalled.

GRAND STAIRCASE-ESCALANTE NATIONAL MONUMENT, Utah—When Autumn Gillard first visited this national monument in southern Utah’s red rock country, she hiked to the top of a plateau. Her heart was broken there.

Utah National Monument Survives Attempt to Rescind its Management Plan

-

Climate Change10 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases10 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy8 months ago

Renewable Energy8 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases11 months ago

嘉宾来稿:探究火山喷发如何影响气候预测