2024年对中国的能源和气候发展而言是重要的一年。二氧化碳(CO2)排放量增长全年都徘徊在2023年水平附近,这使得中国在2030年前实现碳达峰的可能性增加。

中国可再生能源的快速发展将煤电占比推至历史最低水平,同时全国碳市场覆盖的行业范围也进一步扩大。

在全球层面,中国在阿塞拜疆巴库举办的COP29联合国气候谈判上发挥了重要作用。然而,由于中美贸易关系日趋紧张,此前给全球气候行动带来希望的两国合作受到威胁。

在即将上任的特朗普政府的领导下,美国在气候谈判中的影响力预计将减弱,因此中国在气候雄心方面的表态——例如其计划在2025年发布的国际气候承诺——将成为决定国内外脱碳进程速度的重要因素。

Carbon Brief向10位顶尖专家询问了他们对中国未来一年的期待。他们的回答已经过编辑,以保证简洁明了。

杨木易博士(Dr Muyi Yang)

Ember高级电力政策分析师

2025年,中国需要在保持经济增长与推进脱碳议程之间找到微妙的平衡。要实现这一平衡,不仅需要扩大风能、太阳能和储能等可再生能源的规模,还需要对长期以来在中国能源安全和经济活动中占据核心地位的煤电进行重大转型。

这不仅仅是关闭少数几家燃煤电厂那么简单,而是要处理好煤电生态系统衰退所带来的更广泛的紧张关系和冲突。这些影响将波及电企、物流公司、采矿企业、设备制造商以及煤化工行业,以及围绕它们建立的社会经济体系。

随着中国临近关键的转折点——预计在2026年开始的“十五五规划”内实现煤炭消费的绝对减少——中国现在就需开始为这一转型进行规划。在维护经济稳定、确保能源安全和履行气候承诺的同时,成功驾驭这一复杂过程将是中国在2025年及以后取得成功的关键。

林伯强教授(Prof Boqiang Lin)

中国能源政策研究院院长

2025年,中国能源和气候发展的重点是通过几项关键举措推进“双碳”目标。“新能源”的部署将加速,海上风电、分布式光伏和分散式风电预计将显著增长。新增风电和光伏装机容量预计将至少达到200GW。(去年新增装机超过300GW)。核电将稳步推进,预计到2025年底,核电运行装机容量将达到65GW。同时,促进“煤炭清洁高效利用”工作也将取得进展,更清洁和灵活的煤电系统将继续支持风电和光伏的快速增长。

储能技术和智能电网将进一步扩展,从而促进可再生能源的大规模并网,而虚拟电厂和大规模车网互动试点的发展也将提升电网效率与能源交互能力。电动汽车(EV)配套基础设施将受到更多关注,以支持电动汽车普及率的快速提高。碳市场有望扩大到更多领域,碳价格也将逐步提高。

姚喆(Zhe Yao)

绿色和平东亚分部全球政策顾问

今年将是一个重要的里程碑。作为“十四五规划”的最后一年,我们将看到中国能否回到实现既定能源和碳强度目标的轨道上来。中国未来十年的气候计划(即新的国家自主贡献)也将发布,其雄心也将接受考验。

这也是我们或可确认中国能源消费结构转变的一年,其标志着碳达峰是否到来。这一趋势的关键指标是可再生能源能否满足所有新增电力需求。

一个更为严峻的考验是,气候方面的当务之急能否以及如何应对地缘政治的挑战。中国将面对白宫易主,以及来自欧盟在清洁产业领域日益激烈的竞争,因此中国与其传统气候伙伴之间的关系需要重塑。希望到2025年,新的气候伙伴关系能够适应不断变化的经济和地缘政治环境。

陈志斌(Zhibin Chen)

阿德菲(Adelphi)碳市场与定价高级经理

展望2025年,我认为中国碳市场的发展在几个方面大有可为。其中包括:

- 显著扩大全国碳排放权交易市场(ETS)的覆盖范围,正式纳入钢铁、水泥和铝行业;

- 在自愿碳市场上启动中国核证自愿减排量(CCER)证书的签发、交易和使用,以履行合规义务;

- 转变全国碳排放权交易市场结构,使其从基于(生产单位排放)强度的限额转变为基于总量(以二氧化碳吨数计)的绝对限额;

- 允许交易员和投资者参与全国碳排放权交易市场中的碳排放配额(CEA)交易。

其中,前两点几乎可以确定将在2025年实现,我希望其能顺利实施。后两点已被生态环境部的政策制定者提及,我希望政府能为其制定明确的时间表和实施路线图。

麦怡瑞(Dr Ilaria Mazzocco)

战略与国际研究中心中国商业与经济理事会主席、高级研究员

我关注的是中国如何应对日益紧张的对外商业关系,以及国际上对中国海外直接投资需求的增长。清洁技术——尤其是太阳能、锂电池和电动汽车这“新三样”——处于这些紧张关系的核心。

围绕气候技术制造和贸易未来的全球竞争正在酝酿,而这在很大程度上取决于中国产业的发展,包括国内需求和中国企业的盈利能力。同样重要的是,包括美国在内的中国的贸易伙伴(在未来的对华政策中)将倾向于何种类型的权衡和交易。

陈凯欣(Kyle Chan)

普林斯顿大学博士后研究员

2025年将是中国电动汽车发展的关键一年。中国国内市场的激烈竞争将进一步压低价格,激励先进驾驶辅助系统等功能上的创新,并使中国继续从燃油车向电车过渡。值得关注的是,中国出现的趋势是否会成为全球趋势的先兆,比如增程式(混合动力)电动车的流行和电池更换技术的改进。

在国际市场,中国的电动车和电池制造商正在开拓新市场,并通过在欧洲和东南亚等地大规模投资海外工厂来应对不断上升的贸易壁垒。一个重大问题是,这些投资能否得到回报,或这些市场的电动车需求是否会因当地充电基础设施不足等其他因素而受到制约。另一个关键问题是,其他国家将在多大程度上选择融入中国的电动车供应链,亦或尝试在中国周围建立供应链。

徐安琪博士(Dr Angel Hsu)

北卡罗来纳大学公共政策、环境、生态与能源副教授

我对中美在气候与能源政策上继续开展次国家层面合作的前景充满期待,尤其是两国在COP29上表现出强烈的兴趣。华盛顿州与中国代表团之间的多次技术交流等……都是令人鼓舞的发展。在过去一年所取得进展的基础上,我们已经制定了将这一对话持续到2025年的计划。

我尤其关注第三方国家和地区能否作为中立平台促进合作。例如,随着美国可能退出气候合作,中方与东盟的合作机会显著增加。中国在COP29上的积极行动,尤其是其在自愿气候融资方面的努力,使其有望在支持东南亚国家脱碳方面发挥领导作用,为区域可持续发展创造双赢局面。

弗朗顿·齐耶穆拉博士(Dr Frangton Chiyemura)

英国开放大学国际发展教育讲师

2025年,中国在能源和气候方面的若干发展值得关注。国务院在2024年设定了新目标,标志着中国朝2060年实现碳中和这一更广泛目标迈出重要一步。

这些国内政策正在影响中国的国际投资。我们可以预见,中国将加大在全球南方的小规模可再生能源项目的投资,这反映了其自身在可再生能源发展中的经验。

这一战略还包括加强与富含能源转型所需重要矿产的国家的合作,尤其是非洲国家。2025年1月,中国外长王毅展开了自2013年以来对非洲的第57次访问。他访问了乍得、刚果共和国、纳米比亚和尼日利亚,突显了这一重点,这些国家都拥有丰富的能源转型所需的矿产资源。

总体而言,这些进展表明中国正在全球气候行动和能源转型中,扮演更积极的领导角色。

刘爽(Shuang Liu)

世界资源研究所中国金融项目主任

随着在巴库举行的COP29会议设定了“新气候融资集体量化目标”,中国可通过南南合作,继续支持发展中国家的低碳和韧性转型。我们的研究显示,中国已是气候融资的重要提供者,2013年至2022年间年均提供近45亿美元。

数据显示,疫情后中国在海外的气候融资有所下降,但在过去三年一直在缓慢回升。未来气候融资增长的一个重要驱动力可能是中国及其利益相关方在发展中国家清洁能源转型中的持续投资。最近的一个例子是,在印度尼西亚总统普拉博沃·苏比安托(Prabowo Subianto)去年11月访问北京期间,中国和印尼签署了关于清洁能源生产和基础设施的协议。这类合作有助于能源转型,创造更多就业机会,并有助于全球南方实现其他可持续发展目标。

王珂礼(Dr Christoph Nedopil)

亚格里菲斯大学亚洲研究中心主任、经济学教授

2025年,在伙伴国日益增长的能源转型需求的驱动下,中国在绿色能源领域的参与可能通过“一带一路”倡议进一步发展。例如,印尼总统普拉博沃在2024年12月的G20会议上宣布加速绿色能源计划,并与中国签署新协议,突显了(与中国的)针对性合作在解决本地能源的优先事项方面的作用。这不仅包括对可再生能源的投资,还涉及电池制造等关键技术。

我也希望在以下三方面取得进展:一是加速低碳能源投资的同时逐步减少化石燃料投资;二是让本地员工更多地从绿色能源转型中获益,尤其是在西方对中国绿色科技产品实施更多贸易限制的情况下;三是如何在“一带一路”倡议中加快工业和自备能源的绿色转型。未来几年的一个特别之机是与亚洲其他许多能源国企分享中国国企在电力行业的经验教训。

The post 专家:中国2025年能源与气候行动将有哪些期待? appeared first on Carbon Brief.

CANBERRA, Tuesday 31 March 2026 — Greenpeace Australia Pacific has welcomed the Parliament’s ratification of the Global Ocean Treaty, creating the opportunity for world-first high seas ocean sanctuaries.

Environment Minister Murray Watt today announced the treaty, the most significant global nature protection agreement in a decade, will be ratified by the Australian parliament. The bill has now passed the Senate and House of Representatives with support from the major parties, clearing the final hurdle towards ratification.

David Ritter, CEO at Greenpeace Australia Pacific, said: “Ratifying the Global Ocean Treaty is genuinely historic. At a time of unprecedented pressure from destructive industrial fishing, severe climate impacts, plastic pollution and mining, Australia has chosen to join the global effort to protect our magnificent oceans.”

Australia was one of the first countries to sign its intent to ratify the treaty in 2023, and we have a long and distinguished history of leadership on global ocean protection. Under the new treaty Australia has the necessary legal tools to drive the creation of high seas ocean sanctuaries.

“The Global Ocean Treaty is the most significant global nature agreement for many years, and has the power to protect the world’s high seas and safeguard precious and endangered wildlife,” Ritter added.

“With the Treaty now in force, Australia has an important opportunity to drive the creation of ocean sanctuaries on the high seas that are fully protected, no-take zones, which will allow wildlife populations to recover and thrive.

“We thrill at the whales and albatross, and all of the animals of the deep wild oceans, great and small–and now the world has the legal ability to protect them by creating high seas sanctuaries; massive parks at sea where nature can thrive.

“We are an island nation of ocean lovers, and all Australians are entitled to expect that our government will take this incredible new opportunity to protect the ocean.”

Greenpeace is calling on the Australian government to build on our national legacy by ensuring that this landmark agreement delivers lasting protection for our precious oceans.

“We’re calling on Minister Watt to create five high seas sanctuaries in our region, starting with a large ocean sanctuary in the Tasman Sea, between Australia and Aotearoa-New Zealand.”

Currently, less than 1 per cent of the global ocean is highly or fully protected. Closing the High Seas protection gap from under 1 per cent to 30 per cent in four years, to meet the globally-agreed 30×30 target, will require governments to protect ocean areas larger than entire continents and to do so faster than any conservation effort in history. Australia will now have a seat at the table for the very first Oceans COP, due before February 2027, where nations will discuss the design and implementation of the treaty.

—ENDS—

For more information or to arrange an interview, please contact Vai Shah on +61 452 290 082 or vai.shah@greenpeace.org

High res images and footage of Australia’s oceans can be found here

Ocean Treaty passes Australian Parliament, a “historic moment” for nature protection

Climate Change

Looking to Jesus and Buddha, a Kentucky Passionist Priest Finds Hope Amid an Enveloping Global Environmental Crisis

Father Joe Mitchell works to create a “new story” that recognizes the interconnectedness of people and nature.

LOUISVILLE, Ky.—Father Joe Mitchell, a Passionist priest, returned home here in 2004 to create a nonprofit center that focuses on what he saw as two major disconnects.

Extreme weather events around the world, such as wildfires and storms, were the major driver behind $107bn in insured losses in 2025, according to industry data.

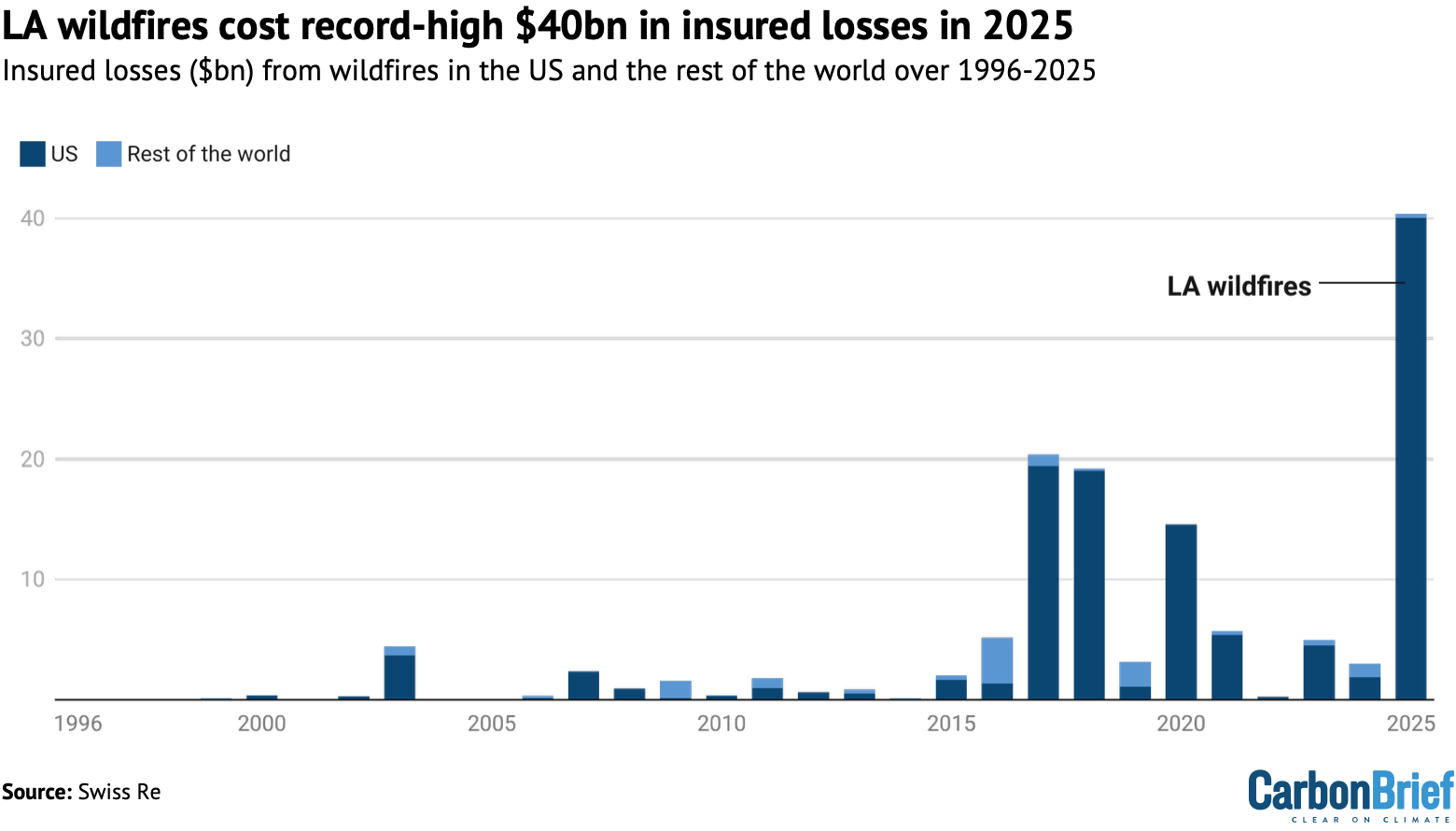

The Los Angeles wildfires alone caused record-high $40bn in insured losses from fires, says a new report from reinsurance company Swiss Re.

The report notes that, while overall insured losses in 2025 were lower than previous years, this was due to a “[luck] rather than a reduction in risk”, partly due to no major hurricanes hitting the US.

Insured losses refer to damages that are compensated for by insurance companies.

Despite lower losses in 2025 than the trend over recent years, they are still rising by an average of 5-7% each year since 1996, accounting for inflation, says Swiss Re.

The report itself does not explicitly discuss the role of human-caused climate change in the events driving these losses.

But the extensive ways in which climate change exacerbates and drives extreme weather are well established in scientific literature.

Other reports and media coverage also show how some parts of the world hit by frequent and intense extreme weather now face the possibility of becoming “uninsurable” due to unaffordable premiums or insurers pulling out of the market.

Below, Carbon Brief outlines three charts from the new Swiss Re report that highlight the role climate extremes had on insured economic losses in 2025.

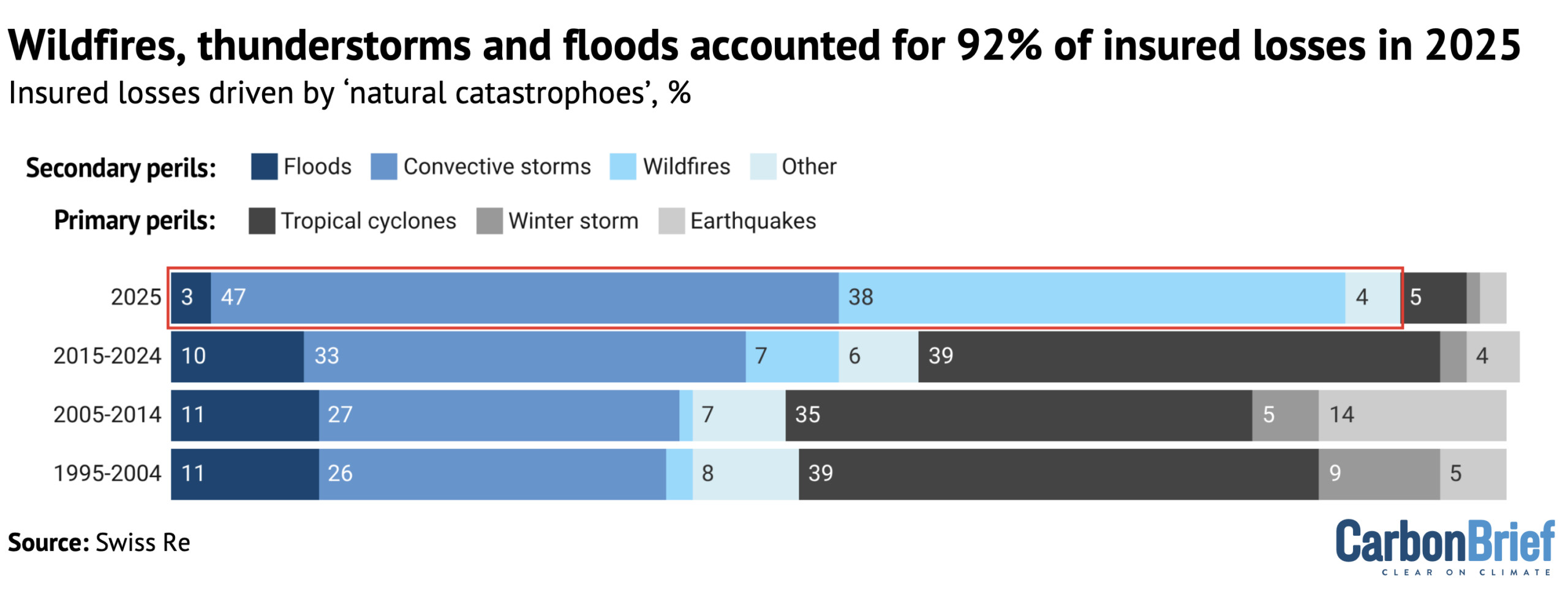

- Most insured losses came from wildfires, storms and floods

- Wildfire losses soared to record-highs in 2025 due to the Los Angeles fires

- Losses are rising from thunderstorms – partly due to cost of replacing damaged rooftop solar panels

Most insured losses came from wildfires, storms and floods

The report finds that wildfires, floods and other “secondary perils” accounted for 92% of the $107bn in insured losses from “natural catastrophes” in 2025.

This is an all-time high for “secondary peril” losses and an increase from 56% over 2015-24 on average.

Secondary perils refer to more frequent, but typically less-damaging events, such as thunderstorms, floods, droughts, wildfires and snow. “Primary perils” are less frequent, but highly-damaging events, such as earthquakes and tropical cyclones.

Secondary events have been the fastest-growing category of insured losses from “natural” catastrophes over the past 55 years, according to the report.

The scientific field of “attribution” shows how global warming is making many of these events occur more frequently and/or with greater severity.

Thunderstorms, wildfires and floods are causing “rapidly growing insured losses with widely varying drivers worldwide”, says the Swiss Re report.

Although overall insured losses decreased to $107bn in 2025 from $137bn in 2024, the report forecasts that they could increase to $148bn in 2026, if the year aligns with long-term trends – or $320bn, if major events occur.

Insured losses only account for part of the wider economic losses from weather events, however, with less than half of losses being covered by insurance, the report says.

It adds that emerging economies have the largest gaps in insurance protection.

One contributing factor to the drop in insured losses between 2024 and 2025 was that no major hurricane made landfall in the US, where many people have insurance coverage for their homes or businesses.

Tropical cyclones accounted for 39% of these losses on average over 2015-24, compared to just 5% in 2025.

Hurricanes did cause destruction in other countries with lower insurance protection in 2025, however, such as Hurricane Melissa in Jamaica.

The US has the largest insurance market in the world, in part due to the predominance of high-value assets when compared to other countries. As such, a hurricane not making landfall in the US brings down the overall total insurance losses more significantly than it would in other countries.

Globally, “growth in exposure” contributes to more than 80% of the increase in weather-related insurance losses since 1970, says Swiss Re. This is the term used by the insurance industry to refer to increasing vulnerability to losses amid rising risks.

The report adds that better modelling and improved adaptation and mitigation measures are “crucial” to reduce losses and maintain insurability in vulnerable areas.

Dr Balz Grollimund, who leads the company’s catastrophe model development, told a press briefing:

“We need to continue reviewing our models, our risk views and updating them so they are not anchored in the past. We want them to be anchored in the present day [and] the next couple of years, so we can really anticipate the risk that we are facing.”

Despite the known link between increasing extreme weather and climate change, the new Swiss Re report only mentions climate change in footnotes or in reference to climate modelling.

In contrast, the company’s 2025 “natural catastrophes” report explicitly mentioned climate change compounding losses and heightening extreme weather events at least six times.

Wildfire losses soared to record-highs in 2025 due to the Los Angeles fires

The Palisades and Eaton wildfires that ripped through parts of Los Angeles in January 2025 resulted in almost $40bn of insured losses – “by far the largest global insured wildfire loss events to date”.

The majority of insured losses from wildfires almost always come from the US, as the chart above shows.

Globally, wildfires burned at least 3.7m square kilometres of land – an area larger than India – over 2024-25, Carbon Brief previously reported.

Extreme events occurred in South American and African rainforests during this time, but these would not rank in insurance industry figures due to low or non-existent insurance cover.

The report notes that “high hazard intersects with high-value assets” in many parts of California, which contributed to the record-high losses in the state.

Typically, extreme weather events in global north countries cost more for insurance companies due to higher levels of insurance protection.

Insurance company Mapfre estimated that around 17% of losses from “natural” disasters are covered by insurance in Asia and 19% in Latin America. This compares to almost 57% in North America.

The total economic losses from the Los Angeles fires were estimated to cost $250bn-275bn, said the UN Office for Disaster Risk Reduction. Other impacts from the fires include job losses, health impacts from the smoke and damage to ecosystems, they noted.

The weather conditions that drove the Los Angeles fires were estimated to be 6% more intense and 35% more likely as a result of human-caused climate change, according to World Weather Attribution.

Losses from wildfires have risen “markedly” over the past decade, notes Swiss Re. Global insured losses from fires are increasing by around 12% each year.

The report adds that wildfires have accounted for an average of 10% of global annual “natural” catastrophe insured losses since 2015, compared to just 2% before 2015.

It also finds that the risk of wildfire losses in the US has been heightened by patterns of population growth. The increase in population in high-risk wildfire zones has been three times higher than the wider US since 1975, says the report.

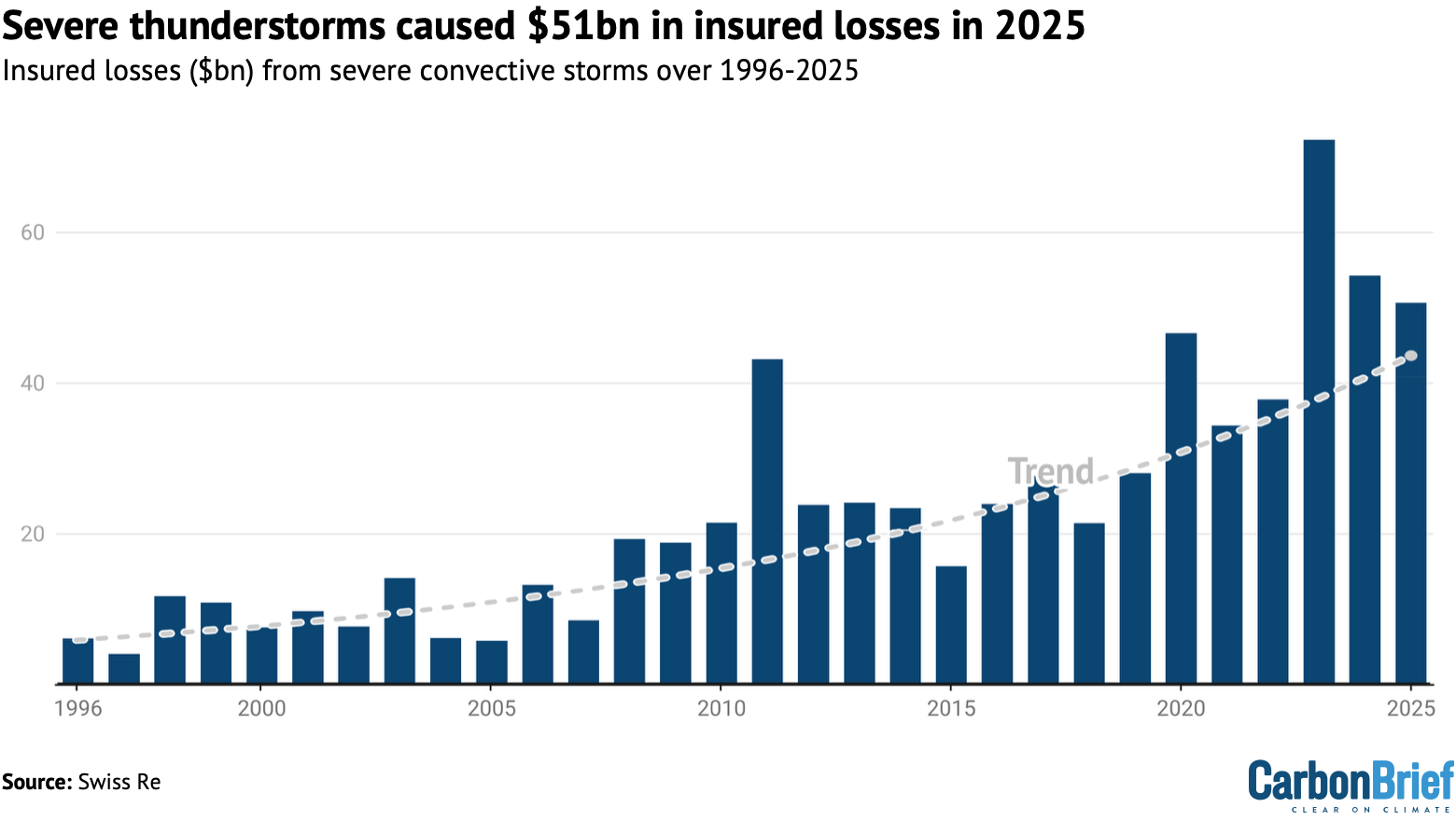

Losses are rising from thunderstorms – partly due to cost of replacing damaged rooftop solar panels

Severe convective storms – also known as thunderstorms – resulted in $51bn of insured losses in 2025, Swiss Re finds, which is above the long-term trend.

These storms are severe events that can bring thunder, lightning, heavy rainfall, hailstones, strong winds and sudden temperature changes, according to the Royal Meteorological Society.

The rain from these storms tends to be very intense and localised in one area, the organisation notes, which can lead to “devastating” floods.

Climate attribution studies have shown that storms have often been made more severe or likely to occur due to climate change, as Carbon Brief’s interactive map reveals.

However, attribution of highly localised convective storms is “extremely difficult”, notes the Intergovernmental Panel on Climate Change. It adds that there is “limited evidence” that extreme rainfall associated with these storms has increased “in some cases” as a result of climate change.

This type of storm has caused up to €50bn ($58bn) in economic losses in the EU since 2000, with Germany, France and Ireland worst-affected, according to a recent report from property data company Cotality.

Globally, 2025 was the third-costliest year for these storms, says Swiss Re, after 2023 ($72bn) and 2024 ($54bn).

One notable contributing factor to this $51bn cost is repairing damage to rooftop solar panels after hailstorms, the report says.

In 2024, the Guardian reported that large hailstones threaten solar infrastructure, with hail in Italy and Germany up to 10cm in size – large enough to “dent a car, smash greenhouses and break a solar panel”.

Grollimund from Swiss Re said that major hail incidents with “tennis ball-sized” hailstones appear to be increasing.

The report says that hail events with stones larger than 5cm are increasing most intensely in Europe, especially in northern Italy. This is driven by “rising low-level moisture and increasing atmospheric instability”, it says.

Hailstones can crack the front glass on a solar panel and cause other damage that can reduce its lifespan and yield, according to a 2019 report from researchers at VU Amsterdam.

The post How wildfires and storms drove insurance losses in 2025 – in three charts appeared first on Carbon Brief.

How wildfires and storms drove insurance losses in 2025 – in three charts

Ocean Treaty passes Australian Parliament, a “historic moment” for nature protection

All About False Killer Whales

Looking to Jesus and Buddha, a Kentucky Passionist Priest Finds Hope Amid an Enveloping Global Environmental Crisis

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits