Lithium producers are facing challenges due to the low prices of lithium, prompting them to take measures to cut costs and protect profits. The drop in lithium prices has been significant, driven by increased supply and a slowdown in electric vehicle (EV) sales.

In response to these market conditions, lithium producers are reducing production, scaling back expansion plans, and focusing on cost-saving initiatives. The world’s biggest provider of lithium for EV batteries, Albemarle, announced additional cost-saving measures, reducing capex by delaying planned lithium investments.

Albemarle’s Cost-Cutting Measures

Albemarle outlined plans to cut capital expenditures for 2024 by $300 million to $500 million compared to 2023.

Moreover, the company aims to slash costs by about $100 million, with over $50 million targeted for the current year. They’ll be implementing measures such as reducing headcount and decreasing spending on contracted services.

The leading lithium producer’s Q4 2023 financial report showed a significant decline in adjusted EBITDA. It has a net loss of $315 million, representing a 125.3% decrease year-over-year. Net sales totalled $2.36 billion, down 10.1% compared to the previous year.

Looking ahead to 2024, Albemarle has identified strategic investments and projects for slow down in response to current market dynamics.

Albemarle’s Chairman and CEO Jerry Masters noted that new greenfield projects, particularly in the West, are not economically feasible at current lithium prices.

Construction and engineering work at the Richburg, SC, MegaFlex conversion facility has been halted until prices improve. But permitting activities will continue at the company’s Kings Mountain site in North Carolina.

In terms of future initiatives, Albemarle will prioritize large, high-return projects that are nearing completion or in startup stages. Meanwhile, they’ll be limiting mergers and acquisitions activity.

Projects that will continue development include the commissioning of the Maison lithium conversion facility and the expansion of the Kemerton lithium conversion facility in Western Australia.

The Rise and Fall of Lithium: From EV Boom to Market Downturn

During 2020 and 2021, the electric vehicle (EV) market experienced significant growth, leading to a surge in demand for lithium, a key component in EV batteries. EV sales saw remarkable increases, with a 45.9% jump in 2020 and a further 100% increase in 2021. This led to a total of EVs sold at 9.78 million units.

This surge in demand created a deficit in lithium supplies in 2021, quickly turning into a surplus of 40,000 metric tons of lithium carbonate equivalent by 2022. Despite the surplus, market expectations continued to drive lithium prices upwards.

However, the boom in the lithium market was short-lived as the global economy weakened and EV sales slowed down, particularly in Mainland China, due to the repeal of EV subsidies. This led to a significant downturn in the lithium market in 2023.

-

As more lithium production capacity comes online, the surplus of lithium is expected to widen further, reaching 100,000 Mt of LCE in 2024.

Australia remains the largest producer of lithium, followed by Chile and China. The U.S. lagged far behind, at the 8th spot after Canada.

Production of lithium is forecasted to increase by 35.7% in 2024 compared to the previous year. Analysts anticipate that lithium prices will stabilize and reach a cyclical bottom in 2024 as inventory build ups are relieved.

The current market conditions are particularly challenging for lower-grade spodumene concentrate and lepidolite producers. These producers are feeling the brunt of the downturn, as they are more susceptible to price changes and are typically the first to reduce output when prices drop too low.

For instance, Pilbara Minerals, an Australian spodumene producer, announced that it’s unlikely to pay an interim dividend for the first half of fiscal year 2024 to preserve its balance sheet.

Similarly, some spodumene producers have been considering changes to pricing settlement terms to prevent buyers from relying on inventories. For example, IGO Ltd. modified the offtake pricing model for spodumene from the Greenbushes deposit, the world’s largest lithium spodumene deposit. The company also announced a reduction in production for the second half of 2024.

Core Lithium Ltd., another Australian producer, halted mining operations at the Grants open pit to slow output and alleviate oversupply. Analysts anticipate that Australian lithium miners will continue to curtail supply in the near term due to uncertain prices.

What Lithium Producers and Investors Can Expect

As some lithium miners reduce production, investors in lithium projects are grappling with whether to proceed or postpone project development. Analysts anticipate that projects may face delays, with a particular impact on unfunded greenfield projects. They also foresee more higher-cost and pure-play lithium producers exiting the market or postponing their projects due to the current challenging conditions.

With lithium projects facing financial challenges, analysts also expect an increase in merger and acquisition (M&A) activity. Major producers with positive cash flow may seek deals in the market, while junior companies may attempt to sell projects, especially given the scarcity of private capital compared to previous years. But this isn’t the case with Li-FT Power (LIFT; LIFFF), the fastest developing North American lithium junior.

Li-FT Power‘s strategy centers on consolidating and advancing hard rock lithium pegmatite projects in Canada, focusing on established lithium districts. The company is well-financed to advance its projects, underscoring its dedication to exploring and developing top-tier lithium assets in Canada.

The tumultuous journey of lithium producers reflects the cyclical nature of commodity markets, where booms are often followed by busts. As Albemarle and other key players in the industry adapt to the challenges posed by plummeting lithium prices, their resilience and strategic responses will shape the future landscape of the lithium market.

Disclosure: Owners, members, directors and employees of carboncredits.com have/may have stock or option position in any of the companies mentioned: LIFFF

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involve risks which could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

The post Lithium Producers Adapt to Price Plummet, Cut Costs and Delay Investments appeared first on Carbon Credits.

Google has taken a major step in reshaping how large energy users interact with the power grid. The company has secured 1 gigawatt (GW) of demand response capacity across its U.S. data center operations with several utility partners. This allows Google to cut or shift electricity use during high demand. It helps stabilize the grid and reduce system costs.

The scale is significant. One gigawatt is roughly enough to power about 750,000 U.S. homes for a year. Demand response helps reduce peak power needs, which can cut grid strain during extreme heat or cold. It also reduces the need for expensive “peaker” plants that run only a few hours per year.

The company noted:

“Demand response enables our data centers to be valuable assets for the power grid. Our ability to shift or reduce our energy demand can help utility companies balance supply and demand and plan for future capacity needs. These agreements create a smart solution to make the electricity systems that serve our data centers more affordable and reliable.”

Demand Response: Turning Data Centers into Flexible Grid Assets

Google’s move reflects a growing challenge. U.S. electricity demand is rising fast. Data centers, especially those running artificial intelligence (AI) and cloud computing, are among the fastest‑growing power loads.

At the same time, building new power supply and grid infrastructure can take five to ten years or more. Google’s strategy bridges this gap by making demand more flexible instead of only increasing supply.

Demand response is a system where large electricity users reduce or shift power use during peak periods. Instead of running at full capacity all the time, facilities adjust operations based on grid conditions. This helps balance supply and demand in real time.

Google applies this by managing its data center workloads. It can delay or shift energy‑intensive tasks, especially machine learning and batch computing, to times when electricity demand is lower. This reduces energy use during peak grid stress without affecting performance.

It also turns data centers into flexible energy assets rather than fixed loads. Traditionally, grids treat demand as constant. Google’s model changes that assumption.

The company has built this system through agreements with multiple U.S. utilities, including:

- Tennessee Valley Authority (TVA)

- Indiana Michigan Power

- Entergy Arkansas

- Minnesota Power

- DTE Energy

These partnerships let grid operators ask Google to cut demand during stressful times, like heat waves or winter peaks. This helps keep the system reliable without just depending on backup generation.

Why Peak Demand Matters for Costs and Reliability

The timing of this move is critical. The U.S. Department of Energy projects that electricity demand could grow 20% or more by 2030, driven by electrification and digital services.

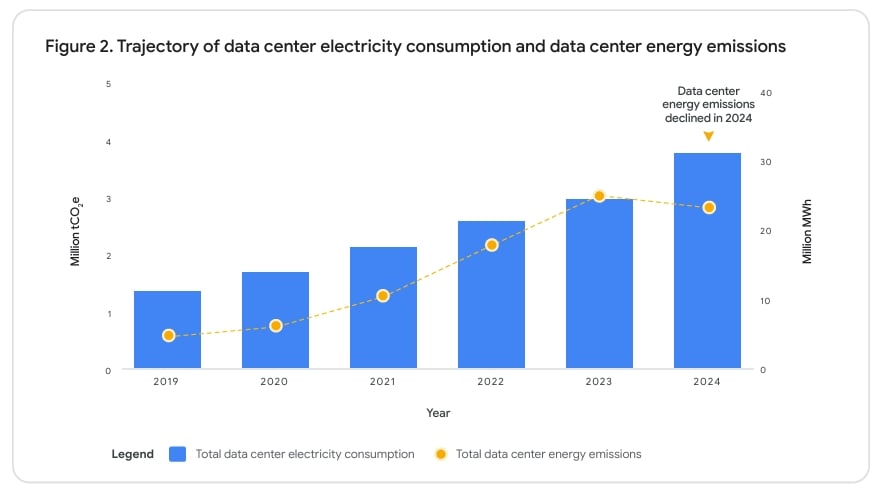

Data centers are a major part of this growth. With AI workloads increasing rapidly, total data center energy use rose over 20% between 2020 and 2025 in the U.S., according to industry studies.

At the same time, grid expansion faces delays. Building new transmission lines or power plants can take years or even decades due to permitting, siting, and cost challenges. Demand response offers a faster solution that can be deployed now.

Google notes that flexible demand can help utilities:

- Balance supply and demand in real time,

- Avoid building rarely used “peaker” plants,

- Reduce stress on transmission systems, and

- Lower wholesale electricity prices during peaks.

Even small flexibility gains can have large system‑wide effects. Research from the Electric Power Research Institute (EPRI) suggests that demand response programs could reduce peak load by 10–20% in many regions, leading to significant savings in infrastructure costs.

This is because peak demand drives infrastructure spending. Power systems are often built to meet only a few hours of extreme demand each year. Reducing those peaks can delay or avoid costly investments in generation and transmission.

Cost Savings and Reliability Gains

Google’s demand response strategy targets two key outcomes: lower costs and improved reliability.

- First, cost reduction. Peak demand periods often coincide with the highest wholesale electricity prices. By lowering demand during those hours, both Google and utilities can save money. These savings can help stabilize electricity prices for businesses and households alike.

- Second, reliability. Power grids face increasing pressure from extreme weather, electrification of transport and buildings, and higher loads from digital infrastructure. Demand response adds flexibility that helps prevent outages when supply is tight.

Google’s system allows it to cut the load quickly when needed. This gives grid operators more tools during tight supply conditions. It also reduces the risk of blackouts and emergency calls for conservation.

Importantly, this approach does not reduce overall energy use over time. Instead, it shifts when energy is used. This makes the system more efficient without limiting long‑term growth in data center activity or other demand.

SEE MORE:

- Google Taps Earth’s Heat in 150MW Geothermal Deal with Ormat Technologies to Power Data Centers

- Google Pledges $50M to Fight Superpollutants by 2030: A Near-Term Climate Game Changer

A Shift in Energy Strategy for Big Tech

Google’s move reflects a broader shift across the technology sector. Large tech companies are no longer just energy consumers. They are becoming active participants in energy systems.

This change is driven by several trends:

- Rapid growth in AI workloads that require large computing resources;

- Rising energy costs that pressure operating margins;

- Corporate climate targets tied to investor and public expectations; and

- Pressure to secure a reliable power supply amid grid uncertainty.

Demand response is now joining renewable energy procurement as a core strategy. Google has already invested heavily in solar, wind, geothermal, and energy storage. The company regularly ranks among the top corporate buyers of renewable energy, which helps avoid emissions.

Other industries have used demand response for years, including manufacturing and heavy industry. However, its use in data centers is still new. The scale of Google’s 1 GW deployment signals that this model could expand quickly and be adopted by other large energy users.

Linking Demand Response to Google’s 24/7 Carbon-Free Goals

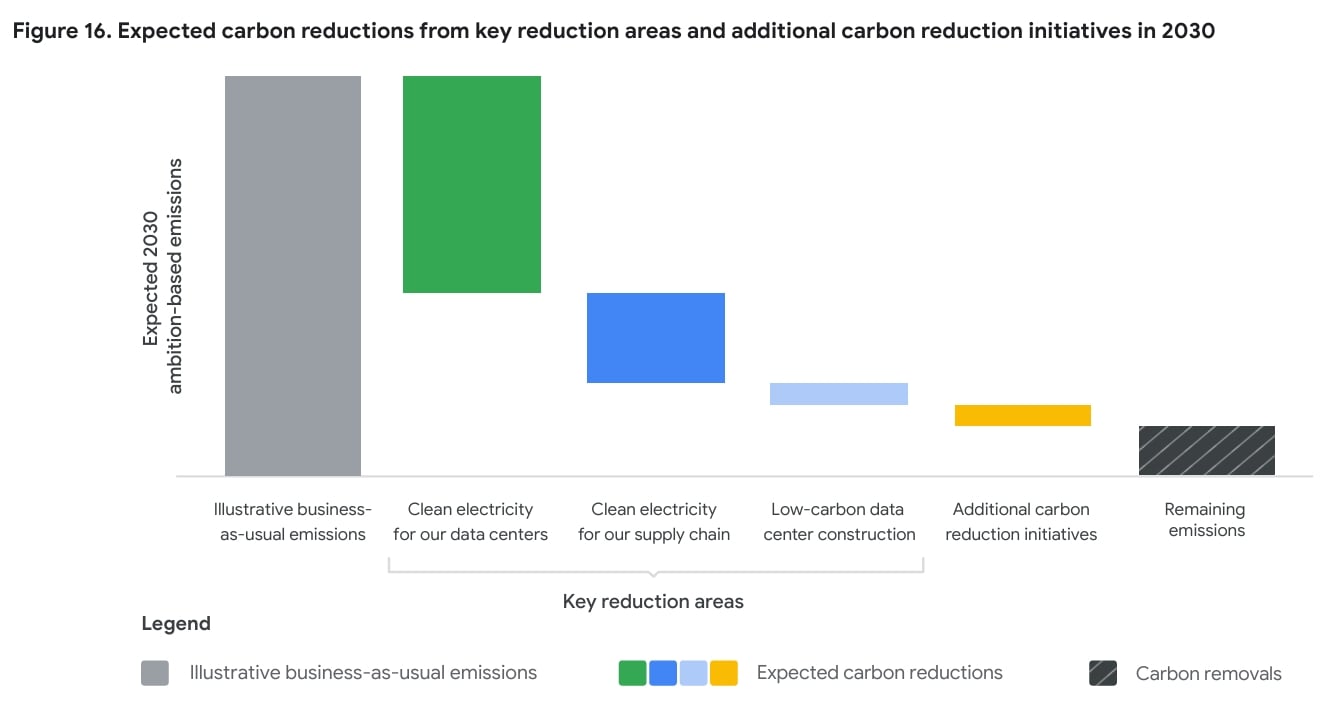

Google’s demand response move also supports its wider clean energy and climate strategy. The company aims to run on 24/7 carbon‑free energy by 2030 and reach net‑zero emissions across its operations and value chain by 2030.

Progress is ongoing. In 2024, Google matched about 66% of its electricity use with carbon‑free energy on an hourly basis, even as power demand rose due to a 27% increase in workload from AI and cloud services.

At the same time, Google added 2.5 GW of new clean energy capacity to the grids serving its operations and cut data center energy emissions by 12% compared with baseline years.

Demand response helps close the remaining gap. By shifting when electricity is used, Google can better match operations with clean energy supply. This improves its ability to run on carbon‑free power every hour of the day.

The Future of Demand Response in AI and Cloud Operations

The demand response market is expected to grow as grids become more complex. Several trends support this outlook.

- Rising demand: U.S. data center growth will drive much of the new electricity use over the next decade. Digital services continue to push the load higher.

- Renewables growth: Wind and solar are cheap but variable, making flexible demand more important for grid stability.

- Grid limits: U.S. interconnection queues include thousands of gigawatts of projects, far more than the grid can handle quickly, causing delays.

Demand response can help manage these constraints. It acts as a “virtual power plant” by reducing demand instead of increasing supply. Studies suggest that flexible demand could unlock large amounts of additional grid capacity and reduce the need for costly transmission upgrades.

This makes demand response one of the fastest and most cost‑effective tools available for grid management.

A Cost-Effective Tool for Modern Grids

As electricity demand continues to grow, this energy model may become more common. Utilities, regulators, and companies are already exploring ways to expand demand‑side flexibility.

In the coming years, the success of these programs will depend on technology, policy support, and market design. However, the direction is clear. Flexible demand is becoming a core part of modern energy systems. Google’s latest move provides a real‑world example of how this transition can work at scale.

The post Google Turns Data Centers Into Grid Assets With 1 GW Flex Power Deal appeared first on Carbon Credits.

Tesla may be getting ready for one of the biggest solar manufacturing moves in America. Reuters reports that the company is looking at buying about $2.9 billion worth of equipment from Chinese suppliers to make solar cells and solar panels in the United States.

If the plan moves forward, it could help Tesla build up to 100 gigawatts of solar manufacturing capacity on American soil by the end of 2028. That is a huge number. It also shows how serious Elon Musk may be about turning solar into a much bigger part of Tesla’s future.

But the report also reveals a bigger problem for the U.S. clean energy sector. Even when companies want to manufacture in America, they still often depend on Chinese tools, machinery, and supply chains to make it happen.

Tesla’s Solar Dream Is Getting Bigger

According to Reuters, Tesla is in talks with several Chinese companies that make solar manufacturing equipment. Suzhou Maxwell Technologies is one of the main names in the discussion. The company is known as the world’s biggest maker of screen-printing equipment used in solar cell production.

Other possible suppliers include Shenzhen S.C New Energy Technology and Laplace Renewable Energy Technology, Reuters said, citing people familiar with the matter.

Some of the equipment may need export approval from China’s commerce ministry before it can be shipped. Reuters reported that the companies were asked to deliver the machinery before autumn, and two sources said the equipment would likely head to Texas.

These details suggest Tesla’s plan is not just an idea or a long-term goal. The company seems to be preparing for a major manufacturing buildout in the U.S. However, the company has not publicly confirmed the reported order. The Chinese suppliers and China’s commerce ministry also did not respond to Reuters’ requests for comment, according to the report.

In January, Musk said solar power could meet all of America’s electricity needs, including rising demand from data centers. Reuters also noted that Tesla job postings said the company wants to deploy 100 GW of “solar manufacturing from raw materials on American soil before the end of 2028.”

The Cost Gap Keeps China in Charge of Solar Supply Chains

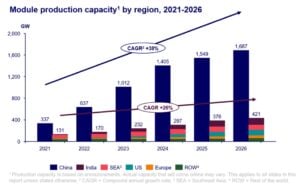

After years of heavy investment, China controls most of the world’s solar manufacturing chain. According to Wood Mackenzie, China is expected to hold more than 80% of global polysilicon, wafer, cell, and module manufacturing capacity from 2023 to 2026.

Wood Mac also said a solar module made in China is about 50% cheaper than one made in Europe and 65% cheaper than one made in the United States. That price gap makes it hard for U.S. factories to compete, especially in the early stages.

So even when U.S. companies want to build locally, they still often need Chinese equipment and expertise. Reuters pointed out that the Biden administration excluded solar manufacturing equipment from tariffs in 2024 after U.S. solar companies said they had no real alternative source for the machines needed to launch domestic factories. That exemption has since been extended by the Trump administration.

In other words, America’s solar manufacturing push still depends, at least in part, on Chinese technology.

- READ MORE: Two Solar Stories, Two Different Directions: Why China Builds Faster as the U.S. Hits Pause

Why Tesla May Be Making This Move Now

Tesla’s reported plan is about much more than one company. It highlights a major challenge for the United States as it tries to build a stronger clean energy economy.

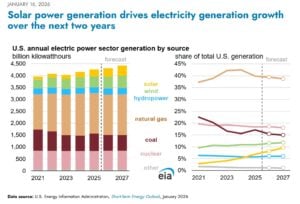

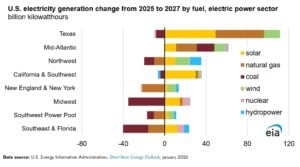

U.S. electricity demand is rising again, and solar is growing fast. The Energy Information Administration said U.S. power use hit its second straight record high in 2025. It also expects demand to keep rising in 2026 and 2027.

At the same time, solar is becoming one of the country’s fastest-growing power sources. In its latest outlook, the EIA said utility-scale solar generation in the U.S. is expected to grow from 290 billion kilowatt-hours in 2025 to 424 billion kilowatt-hours by 2027.

The EIA also said nearly 70 GW of new solar capacity is scheduled to come online in 2026 and 2027. That would increase U.S. solar operating capacity by 49% compared with the end of 2025.

Texas Solar Capacity Supports Tesla and SpaceX

Texas is expected to lead much of that growth. Solar generation in the ERCOT grid is forecast to rise from 56 billion kilowatt-hours in 2025 to 106 billion kilowatt-hours by 2027. Battery storage is also growing to help balance solar power throughout the day.

This helps explain why Texas is such an important part of Tesla’s reported plan. The state already plays a big role in Tesla’s manufacturing footprint. It is also one of the hottest solar markets in the country.

For Tesla, building solar equipment or solar products in Texas could support more than just the grid. Reuters said Musk plans to use much of the capacity for Tesla itself, while some could also help power SpaceX satellites.

That would turn solar into a strategic asset across Musk’s wider business empire. It would also tie clean power more closely to Tesla’s long-term growth story, especially as energy demand from artificial intelligence and data infrastructure keeps rising across the country.

Snapshot of US Solar Imports

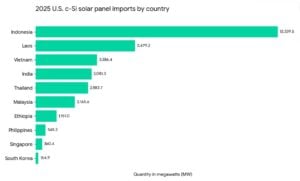

Even with more local manufacturing, the U.S. solar market still depends heavily on imported parts. Solar Power World reviewed U.S. International Trade Commission data and found that the United States imported 33 GW of silicon solar panels in 2025. It also imported 21 GW of silicon solar cells.

That cell figure is especially important because it shows that U.S. panel assembly is growing faster than domestic cell production. America may be building more panels at home, but it still imports many of the core components needed to make them.

The report said the U.S. has around 50 GW of silicon panel assembly capacity, but less than 5 GW of domestic cell manufacturing output. That means plenty of cells still have to be imported. Notably, most imported cells came from Indonesia and Laos in 2025, while South Korea was also a major supplier.

This is where Tesla could make a difference. If it builds large-scale solar cell and panel manufacturing in the U.S., it could help close one of the biggest gaps in the domestic solar supply chain.

Still, there is an irony here. To reduce America’s dependence on foreign solar products, Tesla may first need to buy Chinese machines.

A Massive Opportunity, But Also a Huge Challenge

If the deal happens, it would be a major win for Chinese solar equipment companies. Many of them have faced weak domestic demand because China has already built too much manufacturing capacity.

For Tesla, the order could lay the foundation for a giant U.S. solar platform. It could support the company’s long-term energy strategy at a time when America needs more electricity, more solar, and more battery storage.

But the challenge is enormous.

Building 100 GW of solar manufacturing capacity in just a few years would be a staggering task. Tesla would need factories, workers, permits, raw materials, logistics, and smooth equipment delivery. It would also need stable trade rules and a supportive policy environment.

The company has already faced supply chain setbacks before. Reuters previously reported that production preparations for the Cybertruck and Semi in the U.S. were disrupted last year after component shipments from China were suspended following higher tariffs on Chinese goods. This history shows how exposed U.S. manufacturing can still be to trade tensions.

If speculations are true, Musk appears to be thinking far beyond electric vehicles, i.e., building a larger clean energy system around solar, batteries, manufacturing, and power demand from new technologies like AI.

For now, Reuters’ report shows a simple reality. The U.S. wants a homegrown solar industry. Tesla may want to help build one. But China still holds many of the tools needed to make that goal real.

The post Is Tesla Building a 100 GW U.S. Solar Giant With Chinese Equipment? appeared first on Carbon Credits.

Carbon Footprint

EU Plans Major Carbon Pricing Overhaul and €30B Clean Tech Boost to Drive Decarbonization

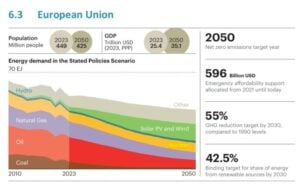

The European Union is preparing to make large changes to its carbon pricing system. EU Commission President Ursula von der Leyen announced that the bloc will revise its Emissions Trading System (ETS) and launch a new €30 billion cleantech investment fund. These moves aim to support the bloc’s climate goals and help industry cope with shifting energy markets.

The announcements came after a summit of EU leaders focused on energy prices and economic challenges. Rising global energy prices and geopolitical pressures are affecting Europe’s economy and industry.

The new proposals aim to improve the EU’s carbon pricing system. They will also encourage investment in clean technology throughout the bloc.

Von der Leyen said:

“The Emissions Trading System is working. It has massively reduced gas consumption. Because of that, it has reduced our dependency on imports of fossil fuels, and it has reduced our vulnerability. And it has driven major investments in the energy transition in the low-carbon energy sources like renewables and nuclear that are homegrown and give us independence. But we need to modernise it and make it more flexible.”

What Is the EU Emissions Trading System and Why Change It?

The EU’s Emissions Trading System is the bloc’s main carbon pricing tool. It was set up in 2005 to reduce greenhouse gas emissions from major industrial sectors. These include electricity and heat generation, steel, cement, chemicals, and commercial aviation.

Under the ETS, companies must buy permits for each ton of carbon dioxide they emit. The total number of permits is capped to reduce emissions over time.

Over nearly two decades, the ETS has helped reduce Europe’s dependence on fossil fuels and encouraged investment in cleaner energy. It is often viewed as a cornerstone of the EU’s climate policy.

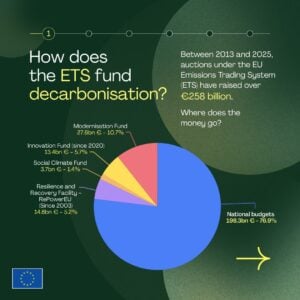

The EU ETS continues to generate large revenues that fund climate action across Europe. In 2025, total ETS auction revenues exceeded €43 billion, with about €24 billion going directly to EU member states.

The remaining funds were allocated to EU-level programs such as the Innovation Fund, Modernisation Fund, and the Social Climate Fund. Overall, ETS revenues since 2013 have surpassed €258 billion, making it one of the world’s largest carbon market funding sources.

However, rising energy costs are pressuring European industries. They started with the war in Ukraine and are now impacted by conflicts in the Middle East. Some member states have asked for a review of the ETS to ease short‑term burdens.

Planned changes “in the next days” may include:

- Updating benchmarks for free allowances given to the industry.

- Strengthening the Market Stability Reserve, which manages the supply of carbon allowances to stabilize prices.

Future changes will seek a “more realistic trajectory.” They may also extend free allocation for some industries past 2034.

Carbon Pricing in Europe: The Stakes and the Context

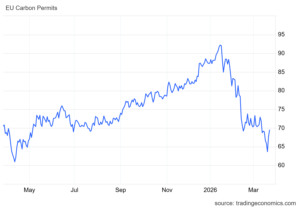

Carbon pricing has been a key driver of investment in clean energy. ETS prices influence how companies weigh fossil fuels versus low‑carbon options. In recent weeks, ETS prices have fluctuated, partly in response to talks about reform and broader energy market volatility.

Recent reports noted that benchmark EU carbon prices jumped almost 10% after policy statements from EU leadership.

Market stability is a core concern. The ETS’s design includes mechanisms to support consistent carbon prices, especially during times of economic stress. A strong and predictable carbon price can help investors commit to long‑term clean energy projects. Conversely, sudden changes can raise costs for industrial players and weaken investment incentives.

At the same time, formal industry and civil society groups have called for regulatory certainty. They say stable carbon pricing is key for planning big clean energy projects. It also helps the EU keep its role as a leader in global climate efforts. These groups emphasize that unpredictable policy shifts could slow clean industrial growth and raise risk for new projects.

A New €30 Billion Cleantech Fund to Boost Decarbonization

Alongside ETS reform, von der Leyen announced plans for a €30 billion ETS Investment Booster. This new fund will support decarbonization and clean technology projects across Europe. It will be financed by revenues from the ETS, meaning carbon pricing will help fund climate action directly.

The booster fund will operate on a “first-come, first-served” basis to support ready‑to‑deploy projects. Von der Leyen said that the fund will ensure access for lower‑income member states. This is intended to promote fairness across the EU and help balance regional disparities in clean technology investment.

The new fund complements existing EU climate finance mechanisms. The Innovation Fund has backed many projects. These include renewable energy, energy storage, and industrial decarbonization.

In 2024, the Innovation Fund provided €4.8 billion in grants. This supported 85 innovative net-zero projects. These efforts helped reduce nearly 476 million tonnes of CO₂ in the first decade.

Expanding funding sources for clean industrial investments reflects a broader EU trend. The Clean Industrial Deal, launched in 2025, plans to raise over €100 billion. This funding will support clean technology manufacturing, create jobs, boost energy efficiency, and promote circular economy solutions.

Renewables, Baseload, and Energy Market Trends in Europe

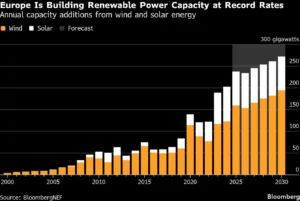

The EU’s net‑zero journey sits against a backdrop of changing energy markets. Renewable energy deployment in Europe continues to grow rapidly.

Wind and solar now make up an increasing share of electricity generation in many member states. These technologies are expected to gain further market share as costs fall and grid integration improves.

However, the need for stable and resilient power systems has grown. Renewable sources like wind and solar are variable by nature. This increases interest in baseload options like geothermal, hydropower, nuclear, and storage paired with renewables.

Meanwhile, global energy prices have remained volatile. Brent crude prices rose above $110 per barrel due to geopolitical tensions. This increase is driving up electricity and heating costs in Europe. These price swings can influence industrial competitiveness and household energy bills.

EU leaders view carbon pricing and investment in decarbonization as key to reducing long-term risks from unstable fossil fuel markets. Policymakers want to use ETS revenues for clean technologies. This will help reduce the need for imported fuels and boost energy independence.

Industry Reaction: Balancing Flexibility and Climate Signals

The proposed changes have drawn mixed reactions. Some industry groups welcomed the updates to the ETS. They said the funding support could help reduce short-term cost pressures. Others warn that too much flexibility could weaken long‑term climate signals and reduce investment certainty.

Civil society organizations have stressed the importance of maintaining carbon pricing integrity. They believe a strong, predictable ETS is key. It will boost investment in electrification, renewables, energy efficiency, and circular economy solutions. Maintaining the market’s rules‑based design, supporters say, will help the EU stay on track with its 2030 and 2040 climate targets.

The European Council has invited the Commission to present a formal ETS review by July 2026 at the latest. This timeline reflects the urgency of balancing climate goals with current economic pressures.

Looking Ahead: Combining Policy and Investment for Climate Goals

The post EU Plans Major Carbon Pricing Overhaul and €30B Clean Tech Boost to Drive Decarbonization appeared first on Carbon Credits.

-

Climate Change7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?