The Integrity Council for the Voluntary Carbon Market (ICVCM) published new decisions under its Core Carbon Principles (CCP) program. The update covers three carbon credit methodologies, also called “categories” in ICVCM’s system. One methodology received full approval, and two received conditional approval.

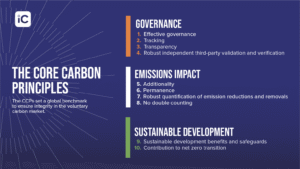

ICVCM’s CCP label is meant to help buyers spot carbon credits that meet a clear, minimum integrity bar. ICVCM uses an Assessment Framework to apply its label. This framework checks how programs and methods handle key issues, including quantification, additionality, monitoring, and verification.

According to Annette L. Nazareth, Chair of the Governing Board, ICVCM

“Demand for CCP-labelled credits has grown steadily, commanding price premiums that reflect buyers’ renewed trust. Policymakers, multilateral institutions, and standard-setters have incorporated the CCPs into their own frameworks, recognising the Integrity Council’s role in building coherence across voluntary and compliance markets.”

The three decisions were:

- Isometric: ISM Reforestation Protocol v1.1 — CCP Approved

- Gold Standard: Methane emission reduction by adjusted water management practice in rice cultivation v1.0 — CCP Approved (Conditional)

- American Carbon Registry (ACR): Improved Forest Management (IFM) on Non-Federal US Forestlands v2.0 — CCP Approved (Conditional)

How the CCP Label Works and When Conditions Apply

A CCP-approved method can earn credits for the CCP label. Projects need to follow the method and the program’s usual rules. In this ICVCM update, the Isometric reforestation method was approved without conditions. This means credits issued under it can get CCP labeling immediately.

A CCP-approved but conditional methodology can still earn the label, but only if specific conditions are met. These conditions can apply to how projects prove additionality. They can also apply to how projects account for risks. Finally, they may apply to how projects set baselines and leakage deductions.

ICVCM also published a market-level snapshot with its February 2026 decisions. It approved eight carbon-crediting programs as CCP-Eligible. It also approved 38 methodologies.

However, 22 methodologies did not meet the requirements. About 105 million credits were approved for the CCP label. Of these, 52 million are available, while 53 million have been retired or canceled. Globally, here’s ICVCM’s carbon credit achievement:

Isometric Sets a First for Nature-Based CCP Credits

ICVCM granted full CCP approval to Isometric’s ISM Reforestation Protocol v1.1, which Isometric published in October 2025. The protocol outlines rules for measuring carbon removals from reforestation. This refers to restoring forest cover on land that was once forested. ICVCM placed it under the broader Afforestation, Reforestation, and Revegetation (ARR) category.

ICVCM said the assessment found the protocol met all relevant criteria in the CCP Assessment Framework. Because the body approved it with no conditions, it stated that all credits issued under the methodology will be eligible for CCP labels.

The Integrity Council also shared early activity indicators for this protocol. It said no credits had been issued yet, but 20 project developers were already registered under the methodology. The organization added that Isometric expects to issue over 4 million credits annually by 2030 under this protocol.

Isometric announced this week that the approval makes its Reforestation Protocol the first nature-based protocol with the CCP label.

- RELATED: Verra Issues First CCP-Labeled IFM Credits Under VM0045: A New Era for Forest Carbon Accounting

Rice Methane Credits Get a Conditional Green Light

ICVCM gave conditional CCP approval to Gold Standard’s method for cutting methane emissions. This method focuses on adjusting water management in rice cultivation (version 1.0). The Integrity Council announced that it published the methodology in July 2023. It is the first approved method for avoiding methane in rice cultivation.

The basic idea behind adjusted water management is simple. Flooded rice fields can produce methane because organic matter breaks down without oxygen. Changing water levels during the growing season can reduce methane formation.

Gold Standard’s documentation states that methane forms in flooded fields with low oxygen. It also notes that the methodology helps water regime changes that reduce methane emissions.

ICVCM also pointed to recent research on the scale of rice methane. A Nature Research Highlight from May 2025 said that a new inventory found rice paddy methane emissions were over 39 million metric tonnes in 2022.

Why Some Credits Qualify, and Others Don’t

The Integrity Council said the rice methodology qualifies for CCP approval only when specific conditions are met. The conditions show how a project proves additionality in some cases. They also explain a rule update about soil organic carbon loss risk in the methodology.

ICVCM also gave credit volume and pipeline estimates. It said about 50,000 credits had been issued under this methodology so far. However, the body understood that none of those credits complied with the first condition. As a result, the organization said those already-issued credits will not be eligible for the CCP label.

ICVCM noted that Gold Standard plans to issue up to 3.2 million credits in the next five years. This is based on its current project pipeline projections. It also listed the main project locations as India, plus activities in Pakistan, Vietnam, Bangladesh, Cambodia, Ghana, Indonesia, Lao PDR, Nepal, and Thailand.

- SEE MORE: Shell’s Initiative to Cut Methane in Rice Farming in the Philippines and Create Carbon Credits

ACR’s Forest Credits Face Tighter Baseline Tests

Same with Gold Standard, ICVCM also granted conditional CCP approval to ACR’s Improved Forest Management (IFM) on Non-Federal US Forestlands v2.0. IFM projects aim to change forest management practices to increase stored carbon or avoid emissions compared with a baseline scenario.

ICVCM explained that v2.0 is an earlier version of an IFM methodology that its Governing Board had already approved in August 2025 (v2.1). For v2.1, ICVCM had set a condition tied to leakage.

- A leakage deduction is needed for projects that cut wood product output by less than 5%. This keeps treatment consistent with projects that exceed that threshold.

For v2.0, ICVCM set two additional conditions. The methodology can earn CCP labeling if:

- A dynamic evaluation of the baseline is verified in line with ACR’s tool for dynamic baseline evaluation (developed with v2.1), and/or

- Removal credits are generated using a specified equation in the methodology (ICVCM references Equation 30).

ICVCM also quantified the immediate impact. It said 2.7 million credits were expected to be immediately eligible for the CCP label out of 13.3 million issued credits under this methodology.

The Integrity Council also stated that past and future removal credits from this method can get CCP labels. Future emission reduction credits can qualify, too, if they use the dynamic baseline evaluation tool.

ACR said the CCP label will soon activate for 2.7 million eligible IFM 2.0 credits in the ACR registry. They linked eligibility to the same baseline evaluation tool.

What CCP Expansion Means for Buyers and Developers

These ICVCM decisions matter because they expand the set of methodologies that can produce credits with the CCP label. For buyers, the label can act as a quick screen when building procurement rules. CCP decisions can influence method evolution for project developers and standards bodies. Conditional approvals often need updates to methods or stricter project tests.

At the same time, the details show that CCP labeling is not automatic. For example, ICVCM’s conditions for the rice methodology mean that some already-issued credits will not qualify. In the IFM case, ICVCM tied eligibility to specific approaches for baselines and the type of credit (removals versus emission reductions).

The approvals expand high-integrity CCP-labeled credits. They also signal growing supply for buyers while enforcing strict standards on baselines, additionality, and verification—shaping voluntary carbon markets toward greater quality and scale.

The post ICVCM Adds New CCP-Approved Carbon Credit Methods for Isometric, Gold Standard and ACR appeared first on Carbon Credits.

Climate change is real, and the evidence is everywhere, from rising sea levels to extreme weather events. While changes in Earth’s climate have occurred naturally over millennia, human activities are now the dominant force behind the current warming trend. Understanding what climate change is, what causes it, and what we can do to stop it is essential for safeguarding our planet and future generations.

Key takeaways

- Human activities, especially burning fossil fuels, are now the dominant driver of climate change, not natural cycles like solar activity.

- Livestock accounts for an estimated 51% of annual global greenhouse gas emissions, while deforestation is the second-largest contributor.

- 2023-2025 was the first three-year period on record to average more than 1.5°C above pre-industrial temperatures.

- Global fossil fuel CO2 emissions hit a record 38.1 billion tonnes in 2025, with no sign yet of a peak.

- Nearly 30% of plant and animal species could be at risk of extinction if global temperatures keep rising.

- Solutions like renewable energy, energy efficiency, carbon offsets, and reduced deforestation can meaningfully slow climate change today.

Climate Change in 2026: The Latest Data

The data keeps confirming the same trend: warming is accelerating, not leveling off. Here’s where things stand as of 2026, based on the most recent findings from NOAA, Copernicus, NASA, and the Global Carbon Project.

2026 climate data snapshot

- Global temperatures: 2025 was the third-warmest year on record, behind 2024 and 2023. The past 11 years (2015–2025) are the 11 warmest ever measured, and 2023–2025 marked the first three-year period to average above 1.5°C over pre-industrial levels.

- CO2 levels: Atmospheric CO2 hit a record monthly high of 430.5 ppm at Mauna Loa in May 2025. Global fossil fuel emissions reached a record 38.1 billion tonnes in 2025, and researchers now say the remaining carbon budget to keep warming under 1.5°C will likely be exhausted before 2030 at current emission rates.

- Extreme weather costs: The U.S. recorded 23 separate billion-dollar weather disasters in 2025, the third-highest annual total on record, costing an estimated $115 billion. The January 2025 Los Angeles wildfires alone caused $61.2 billion in damage, making them the costliest wildfire event in U.S. history.

- Sea level rise: Global mean sea level rose just 0.08 cm in 2025, slowed temporarily by La Niña rainfall patterns, but the long-term rate of sea level rise has more than doubled since 1993, and oceans are up roughly 10 cm (about 4 inches) since satellite records began.

None of this changes the underlying picture: the causes, effects, and solutions below remain the same, they’re just playing out faster and at greater cost each year.

What Is Climate Change?

You’ve likely heard the terms “climate change” and “global warming” used interchangeably. However, they have distinct meanings. Global warming refers specifically to the increase in the planet’s average surface temperature, largely due to greenhouse gas emissions. Climate change, on the other hand, encompasses a broader range of long-term changes in temperature, precipitation, wind patterns, and other aspects of the Earth’s climate system.

Climate change has always been part of Earth’s history, driven by natural interactions between five key systems:

- Atmosphere (air)

- Biosphere (living things)

- Cryosphere (ice and permafrost)

- Hydrosphere (water bodies)

- Lithosphere (Earth’s crust and upper mantle)

Today, the rapid pace and scale of climate change are primarily driven by human activities.

Climate Change (infographic)

What Are the Causes of Climate Change?

Greenhouse Gases

Greenhouse gases (GHGs) trap heat in the Earth’s atmosphere. While some GHGs occur naturally, human activities have sharply increased their concentrations. Major contributors include:

- Carbon dioxide (CO2) – Released by burning fossil fuels, deforestation, and land-use changes.

- Methane (CH4) – Emitted from livestock, landfills, and oil and gas production.

- Nitrous oxide (N2O) – Produced by agricultural activities and fossil fuel combustion.

- Chlorofluorocarbons (CFCs) – Man-made chemicals used in refrigeration and aerosols.

CO2 is the most significant and long-lasting of these gases, making it the primary driver of global warming.

While some of these greenhouse gases, such as water vapor, are naturally occurring, others, such as CFCs, are synthetic. CO2 is released into the atmosphere from both natural and human-made causes and is one of the leading contributors to climate change. CO2 has been increasing at an alarming rate and has the potential to stay in the earth’s atmosphere for thousands of years unless it gets absorbed by the ocean, land, trees, and other sources. As CO2 production has steadily risen, though, the earth’s natural resources to absorb it have also been diminished. This is already occurring in many ways as the earth’s resources are disappearing from things like deforestation. Some studies even predict that plants and soil will be able to absorb less CO2 as the earth continues to warm, possibly accelerating climate change even further.

While some of these greenhouse gases, such as water vapor, are naturally occurring, others, such as CFCs, are synthetic. CO2 is released into the atmosphere from both natural and human-made causes and is one of the leading contributors to climate change. CO2 has been increasing at an alarming rate and has the potential to stay in the earth’s atmosphere for thousands of years unless it gets absorbed by the ocean, land, trees, and other sources. As CO2 production has steadily risen, though, the earth’s natural resources to absorb it have also been diminished. This is already occurring in many ways as the earth’s resources are disappearing from things like deforestation. Some studies even predict that plants and soil will be able to absorb less CO2 as the earth continues to warm, possibly accelerating climate change even further.

Solar Activity

Solar activity, as mentioned above, does play a role in the earth’s climate. While the sun does go through natural cycles, increasing and decreasing the amount of energy that it emits to the earth, it is unlikely that solar activity is a major contributor to global warming or climate change. Since scientists began to measure the sun’s energy hitting our atmosphere, there has not been a measurable upward trend.

Agriculture

There are many significant ways in which agriculture impacts climate change. From deforestation in places like the Amazon to the transportation and livestock that it takes to support agricultural efforts around the world, agriculture is responsible for a significant portion of the world’s greenhouse gas emissions. However, agriculture is also an area that is making tremendous strides to become more sustainable. As productivity increases, less carbon is being emitted to produce more food. Agriculture also has the potential to act as a carbon sink, and could eventually absorb nearly the same amount of CO2 it emits.

Deforestation

Deforestation and climate change often go hand in hand. Not only does climate change increase deforestation by way of wildfires and other extreme weather, but deforestation is also a major contributor to global warming. According to the Earth Day Network, deforestation is the second leading contributor to global greenhouse gasses. Many people and organizations fighting against climate change point to reducing deforestation as one of, if not the most, important issues that must be addressed to slow or prevent climate change.

Human Activity

According to the Environmental Protection Agency, the most significant contributor to climate change in the United States is the burning of fossil fuels for electricity, heat, and transportation. Of these factors, transportation in the form of cars, trucks, ships, trains, and planes emits the largest percentage of CO2, speeding up global warming and remaining a significant cause of climate change.

Livestock

While interconnected to many of the agricultural and deforestation issues we have already touched on, livestock in the form of cattle, sheep, pigs, and poultry play a significant role in climate change. According to one study, “Livestock and Climate Change,” livestock around the world is responsible for 51% of annual global greenhouse gas emissions.

What Are the Immediate Effects of Climate Change?

From melting glaciers to more extreme weather patterns, people everywhere are beginning to take notice of the real impacts of climate change. While some nations around the world are taking action with initiatives such as the Paris Climate Agreement, others are continuing business as usual, pumping millions of tons of carbon into the atmosphere year after year. As the 2026 data above shows, climate change continues to cause extreme weather as well as safety and economic challenges on a global scale, and the costs are climbing every year.

Extreme Weather

Changes to weather are perhaps the most noticeable effect of climate change for the average person, largely because of the financial impact severe weather events can have. In 2025 alone, the U.S. recorded 23 separate billion-dollar weather disasters totaling $115 billion in damages, continuing a run of the three highest years on record (2023, 2024, and 2025). Extreme weather influenced by climate change includes:

- Stronger storms & hurricanes

- Heatwaves

- Wildfires

- More flooding

- Heavier droughts

Safety & Economic Challenges

In 2014 the U.S. Department of Defense released a report that stated climate change posed a severe and immediate threat to national security. According to former Secretary of Defense, Chuck Hagel, rising global temperatures, shifting precipitation patterns, climbing sea levels, and more extreme weather events intensify the challenges of global instability, hunger, poverty, and conflict.

Climate change is also likely to cause continued economic challenges in many parts of the world. Some estimates have the U.S. already spending around $240 billion annually due to human-caused climate change, and the 2025 U.S. billion-dollar disaster total of $115 billion shows those costs remain elevated year after year. Putting an exact number on the real costs of climate change is difficult, though, once you consider the staggering costs of losing natural resources like clean air and water.

What Is the Long-Term Impact of Climate Change?

The long-term impact of climate change could be absolutely devastating to the planet and everyone and everything living on it. If the world continues on its current trajectory, and 2025’s record fossil fuel emissions suggest it is, then we will likely continue to see increasing effects on everyday life.

Health

There are many ways in which climate change could impact people’s health. Depending on age, location, and economic status, climate change is already affecting the health of many and has the potential to impact millions more. According to the Center for Disease Control and Prevention, climate change-related health risks may include:

- Heat-related illness

- Injuries and fatalities from severe weather

- Asthma & cardiovascular disease from air pollution

- Respiratory problems from increased allergens

- Diseases from poor water quality

- Water & food supply insecurities

Negative Impact on Ecosystems

Ecosystems are interconnected webs of living organisms that help support all kinds of plant and biological life. Climate change is already changing seasonal weather patterns and disrupting food distribution for plants and animals throughout the world, potentially causing mass extinction events. Some studies estimate that nearly 30% of plant and animal species are at risk of extinction if global temperatures continue to rise.

Water & Food Resources

Climate change could have a significant impact on food and water supplies. Severe weather and increased temperatures will continue to limit crop productivity and increase the demand for water. With food demand expected to increase by nearly 70% by 2050, the problem will likely only get worse.

Sea Levels Rising

Rising sea levels could have far-reaching effects on coastal cities and habitats. Increasing ocean temperatures and melting ice sheets have steadily contributed to the rise of sea levels on a global scale. Global sea level has risen roughly 10 cm (about 4 inches) since satellite records began in 1993, and the National Oceanic and Atmospheric Administration estimates sea levels will rise by at least 8 inches by 2100, potentially causing increased flooding and a decrease in ocean and wetland habitats.

Shrinking Ice Sheets

While contributing to rising sea levels, shrinking ice sheets present their own set of unique problems, including increased global temperatures and greenhouse gas emissions. Climate change has driven summer melt of the ice sheets covering Greenland and Antarctica to increase by nearly 30% since 1979.

Ocean Acidification

The ocean is one of the main ways in which CO2 gets absorbed. While at first glance that may sound like a net positive, the increasingly human-caused CO2 is pushing the world’s oceans to their limits and causing increased acidity. As pH levels in the ocean decrease, shellfish have difficulty reproducing, and much of the ocean’s food cycle becomes disrupted.

What Are the Solutions for Climate Change?

While the effects of climate change can seem bleak, there is still hope. By taking immediate action to curb climate change, we may never see the worst consequences. Likewise, as the world adopts cleaner, more sustainable energy solutions, there may be millions of new jobs created and billions of dollars of economic benefits. Below are some practical ways you can battle climate change, including:

- Switching to renewable energy (solar, wind, hydro)

- Purchasing Renewable Energy Certificates (RECs) for your home

- Using energy-efficient appliances and insulating buildings

- Offsetting your carbon emissions through verified programs

- Adopting plant-based diets and reducing meat consumption

- Minimizing food waste and single-use plastics

- Protecting and restoring forests and wetlands

- Supporting clean transportation options (EVs, public transit, biking)

Try the Terrapass Flight Carbon Calculator

Traveling by plane? Use the Terrapass Flight Carbon Calculator to estimate your flight emissions and support verified offset projects.

See How Terrapass Can Help Your Business

Companies facing growing pressure to cut emissions, whether from regulation, investors, or customers, can explore Terrapass’s business carbon offset programs to start addressing their footprint today.

Why Climate Change Matters to Everyone

Climate change isn’t just an environmental problem. It’s an everything problem. It touches every aspect of our lives:

- Jobs and the economy: Clean energy sectors are rapidly expanding and could create millions of new jobs worldwide.

- National security: Climate change exacerbates global instability, resource conflicts, and forced migration.

- Public health: Clean air, safe drinking water, and stable food systems are all at risk.

- Justice and equity: Low-income communities and developing nations are often hit hardest despite contributing the least to global emissions.

- Future generations: The choices we make today will shape the legacy we leave behind.

By investing in climate solutions now, we not only avoid catastrophe but also unlock opportunities for innovation, resilience, and shared prosperity.

FAQ: Climate Change

What is climate change?

Climate change refers to long-term shifts in temperature, precipitation, wind patterns, and other aspects of Earth’s climate system, largely driven today by human greenhouse gas emissions.

What is the difference between climate change and global warming?

Global warming specifically means the rise in the planet’s average surface temperature. Climate change is the broader term, covering the shifts in weather patterns, sea levels, and ecosystems that result from it.

What causes climate change?

The main driver is greenhouse gas emissions, especially carbon dioxide from burning fossil fuels, along with deforestation, agriculture, and livestock. Natural factors like solar activity play a much smaller role.

What are the effects of climate change?

Effects include more extreme weather, rising sea levels, shrinking ice sheets, ocean acidification, threats to food and water supplies, and growing risks to public health.

Is climate change getting worse in 2026?

The trend lines are still moving the wrong way. 2025 was the third-warmest year on record, global fossil fuel emissions hit a new record of 38.1 billion tonnes, and 2023–2025 was the first three-year period to average above 1.5°C over pre-industrial levels.

Can climate change be reversed?

It’s generally described as something we can slow and adapt to rather than fully reverse in the near term. Cutting emissions, protecting forests, and shifting to renewable energy can still prevent the worst outcomes.

What can I do to help stop climate change?

Individual actions add up: switching to renewable energy, using energy-efficient appliances, offsetting your carbon emissions, reducing meat consumption, and supporting clean transportation all make a difference.

Brought to you by Terrapass, your trusted partner in carbon offsets and climate education.

Sources:

- Rose, Brian E. “ATM 623: Climate Modeling.” Lecture04 – Climate System Components, atmos.albany.edu.

- “AAAS Reaffirms Statements on Climate Change and Integrity.” American Association for the Advancement of Science, aaas.org.

- “The Causes of Climate Change.” NASA, 6 Sept. 2019, climate.nasa.gov/causes.

- “The Carbon Cycle.” NASA, earthobservatory.nasa.gov/features/CarbonCycle/page5.php.

- Green, Julia K., et al. “Large Influence of Soil Moisture on Long-Term Terrestrial Carbon Uptake.” Nature, vol. 565, no. 7740, 2019, pp. 476–479, nature.com.

- “Is the Sun Causing Global Warming?” NASA, climate.nasa.gov.

- “Agriculture and Greenhouse Gas Emissions.” American Farm Bureau Federation, fb.org.

- “Deforestation and Climate Change.” Earth Day Network, earthday.org/campaigns/reforestation/deforestation-climate-change/.

- “REDD: Protecting Climate, Forests and Livelihoods.” International Institute for Environment and Development, 24 Jan. 2018, iied.org.

- “Sources of Greenhouse Gas Emissions.” EPA, 13 Sept. 2019, epa.gov.

- Goodland, Robert and Anhang, Jeff. “Livestock and Climate Change.” worldwatch.org.

- “Extreme Weather and Climate Change.” Center for Climate and Energy Solutions, 14 Aug. 2019, c2es.org.

- “DoD Releases 2014 Climate Change Adaptation Roadmap.” U.S. Department of Defense, defense.gov.

- “The Economic Case for Climate Action in the United States.” FEUUS, feu-us.org.

- “Climate Change and Public Health.” Centers for Disease Control and Prevention, cdc.gov.

- “Climate Impacts on Ecosystems.” EPA, 22 Dec. 2016, epa.gov.

- Kijne, Jacob W. “Hugh Turral, Jacob Burke and Jean-Marc Faurès: Climate Change, Water and Food Security.” fao.org.

- “Quick Facts on Ice Sheets.” National Snow and Ice Data Center, nsidc.org.

- “Copernicus: 2025 was the third hottest year on record.” Copernicus Climate Change Service, climate.copernicus.eu.

- “Assessing the Global Temperature and Precipitation Analysis in 2025.” NOAA NCEI, ncei.noaa.gov.

- “Fossil Fuel CO2 Emissions Hit Record High in 2025.” Global Carbon Project, globalcarbonbudget.org.

- “2025 in Review: U.S. Billion-Dollar Disasters.” Climate Central, climatecentral.org.

- “NASA Analysis Shows La Niña Limited Sea Level Rise in 2025.” NASA/JPL, jpl.nasa.gov.

The post What Is Climate Change? Causes, Effects & Solutions (2026) appeared first on Terrapass.

We will explore the process of burning fossil fuels and look at why they are burned and what sectors use the energy they supply. Then, we will cover what sort of products and greenhouse gases are released when fossil fuels are burned. Finally, we’ll view alternative energy solutions that are available for energy production.

Key takeaways

- Fossil fuels still supplied about 86% of global energy in 2025, only a slight decline from roughly 87% in 2024.

- Burning fossil fuels releases six main products: carbon dioxide, carbon monoxide, sulfur dioxide, nitrogen oxides, lead, and particulate matter.

- Carbon dioxide accounts for roughly 74% of global greenhouse gas emissions, and burning fossil fuels is the single largest source of it.

- Natural gas is the cleanest-burning fossil fuel, but it’s still primarily methane, a potent greenhouse gas.

- The three adverse effects of burning fossil fuels are air pollution, water pollution, and climate change.

- Renewable energy, nuclear power, and carbon offset programs are all viable ways to reduce reliance on fossil fuels today.

Fossil Fuels in 2026: The Latest Data

Despite years of clean energy investment, fossil fuels haven’t lost much ground yet, they’ve mostly just been joined by more of everything else. Here’s the latest picture, based on the Energy Institute’s 2026 Statistical Review of World Energy and the U.S. Energy Information Administration (EIA).

2026 fossil fuel data snapshot

- Global energy mix: Fossil fuels supplied about 86% of the world’s total energy in 2025, down only slightly from roughly 87% in 2024. Oil provided about a third of global supply, followed by coal and natural gas.

- Coal set a new record: Global coal use hit an all-time high in 2025, even as renewables grew faster in percentage terms, because total global energy demand kept rising alongside it.

- U.S. electricity: About 58% of U.S. utility-scale electricity generation came from fossil fuels in 2025 (down from roughly 60.6% in 2020), with natural gas alone supplying about 41%. Renewables reached nearly 26% of U.S. generation.

- Emissions: Global carbon dioxide emissions from energy rose 1.1% in 2025, with China accounting for roughly 31% of global emissions.

The takeaway: fossil fuel combustion is still growing in absolute terms even as its share of the energy mix inches down, which is why the effects and alternatives covered below remain just as relevant in 2026 as ever.

What Are Fossil Fuels?

Most of the fossil fuels we exploit today are the product of plants and animals that died 540 million to 65 million years ago and were buried in layers of sediment. Over time, the fossils were subjected to increased pressure and heat as the sedimentary rock layers of the earth’s crust continued to develop above them.

Eventually, these fossils turned into kerogen, also known as oil shale. After even more time, the oil shale was subjected to even greater temperatures and ultimately transformed into coal, oil, or natural gas. Fossil fuels consist of energy stores called hydrocarbons that form during exposure to immense heat and pressure.

What Is Fossil Fuel Combustion?

Fossil fuel combustion is the process of burning coal, oil, natural gases, or other fossil fuels to create energy. The use of fossil fuels creates around 80% of the world’s energy. While these fuels are an inexpensive way to produce power, they release large amounts of carbon dioxide and other greenhouse gases when combusted.

Creating electricity through burning fossil fuels utilizes a steam generator to create power. Fossil fuels are burned to heat water in boilers that make large amounts of steam. High pressure from the steam then rotates a turbine in a steam generator and creates power. This power is then transferred into the power supply.

Other forms of fossil fuel combustion come from the transportation sector. Burning fuel to power cars, trucks, and airplanes are all forms of fossil fuel combustion.

What Happens When You Burn Fossil Fuels?

Due to the presence of hydrocarbons, fossil fuels produce a substantial amount of energy per pound when combusted. Hydrocarbon-rich fossil fuels hold a large amount of energy potential that is released in the form of heat when combusted in the presence of oxygen.

However, these hydrocarbons also produce large amounts of carbon dioxide, which contributes to the greenhouse effect and in turn causes global warming. As the hydrocarbon compounds break down during combustion, the carbon dioxide is released alongside the heat energy.

Why Are Fossil Fuels Burned?

Burning fossil fuels creates energy in many different ways for people worldwide. Fossil fuels are responsible for powering the energy sector, transportation sector, and industrial sector.

In the energy sector, people rely on electricity generation for lighting, heating, and cooling in their homes and places of business. As of 2025, about 58% of U.S. utility-scale electricity generation still came from burning fossil fuels, according to the U.S. Energy Information Administration. Natural gas is also commonly used in homes and commercial buildings for heating, cooking, and other needs.

Fossil fuels are also used to power the transportation sector. In 2020, the U.S. transportation sector received 89% of its energy from petroleum fuel sources. People rely on personal vehicles, public transportation, and air travel to get where they need to be. Many of these modes of transportation rely on burning fossil fuels. Fossil fuels also power the transportation of goods around the world. Cargo ships, trucks, and airplanes are often powered with petroleum fuels.

Finally, the industrial sector relies on fossil fuels to create heat for their industrial practices and to create power to manufacture products. The industrial sector uses energy generated by burning fossil fuels to power electrical equipment like motors, lights, computers, and more. The manufacturing industry is responsible for using the most energy within the industrial sector.

What Do Fossil Fuels Release When Burned?

Six products are released due to the burning of fossil fuels. Each of these products affects the environment in different ways.

Carbon Dioxide

Of all the greenhouse gases, carbon dioxide is the most abundant when it comes to human-related emissions. Carbon dioxide is released in large quantities from burning coal, gas, and oil because these fuels are primarily composed of hydrocarbons released in the form of carbon dioxide once combusted. Coal burning is the primary source of carbon dioxide emissions, followed by burning oil, then natural gas.

Carbon Monoxide

Carbon monoxide is released when carbon-based fuel is not completely burned. The primary source of carbon monoxide emissions comes from road vehicles. Non-road vehicles, like boats or construction equipment, also contribute to carbon monoxide emissions.

Sulfur Dioxide

Sulfur dioxide is found in coal and oil. It can be emitted when these fossil fuels are burned and through the process of extracting gasoline from crude oil. When sulfur dioxide dissolves into water vapor and forms sulfuric acid, it interacts with other gases in the air, and sulfates are formed. This can lead to acid rain.

Nitrogen Oxides

Nitrogen oxides are released when fossil fuels are burned at high temperatures in motor vehicles or from other fuel-burning sources in industrial or home settings. Nitrogen dioxide, one common form of nitrogen oxide, creates smog over city centers.

Lead

Lead used to be a more common emission when leaded gasoline was used for vehicles. Today, most lead pollutants can be found in the air around factories that separate metal from ore.

Particulate Matter

Particulate matter is any solid particle or liquid droplet found in the air. Particulate matter is released when fossil fuels are burned and can be found in higher concentrations in regions that burn more fuels, like city centers or power facilities.

Why Is Burning Fossil Fuels a Problem?

The primary issue associated with burning fossil fuels is that the practice releases large quantities of greenhouse gases into the atmosphere. High concentrations of greenhouse gases in the atmosphere increase the global temperature and cause climate change.

Carbon dioxide is the most emitted greenhouse gas, accounting for roughly 74% of global greenhouse gas emissions, according to the Center for Climate and Energy Solutions’ analysis of European Commission emissions data. Burning fossil fuels is the activity responsible for emitting the most carbon dioxide around the world.

As the world continues to rely on fossil fuels for energy production and transportation, carbon emissions will continue to remain high. Global CO2 emissions from energy rose another 1.1% in 2025. If the globe does not mitigate the amounts of carbon dioxide released by burning fossil fuels, then we will continue to see increasing global temperatures and climate change.

What Are 3 Effects of Burning Fossil Fuels?

There are three adverse effects of burning fossil fuels: air pollution, water pollution, and climate change. These effects are caused by the products released when fossil fuels are burned.

Air Pollution

Air pollution occurs when products like sulfur dioxide, carbon monoxide, nitrogen oxides, and particulate matter are released from burning fossil fuels. Air pollution has been found to cause respiratory disease, cardiovascular disease, and cancer. Children, pregnant women, and elderly people are all at higher risk of the negative health effects caused by air pollution.

Water Pollution

Water pollution occurs when sulfur dioxide dissolves into water and creates sulfuric acid. This produces acid rain and can lead to the acidification of freshwater sources like lakes and streams. When these bodies of water become too acidic, life cannot survive in them. Acid rain can also affect local crops and soil acidity levels.

Climate Change

Climate change is a significant threat to ecosystems and human populations worldwide. Carbon dioxide emitted through burning fossil fuels plays a huge role in global warming. As more carbon dioxide is released into the atmosphere, more heat is trapped on earth through the greenhouse effect. Increasing global temperatures can lead to rising sea levels, deforestation, changing climates, and scarcity of food sources.

Which Fossil Fuel Is the Cleanest Burning?

Of the three primary fossil fuels, the cleanest burning fuel is natural gas. Using natural gas to generate energy emits less of all kinds of air pollutants and carbon dioxide than both oil and coal.

While natural gas is cleaner to burn for energy, it consists primarily of methane, a harmful greenhouse gas. Natural gas leaks are a leading cause of methane emissions each year in the United States. What is more, the process of locating natural gas wells and drilling for natural gas can have negative environmental impacts.

What Are Alternatives to Burning Fossil Fuels?

Alternatives to burning fossil fuels include renewable energy sources like hydroelectricity, wind power, and solar energy. Clean energy from nuclear power plants is another alternative to burning fossil fuels.

The benefit of transitioning to clean energy is a significant reduction in emissions. Nuclear energy and renewable energy sources have no emissions, which can slow the effect of climate change around the world.

A switch to entirely renewable energy systems would provide the best alternative to fossil fuels. Fossil fuels are non-renewable, meaning once the natural resource is diminished, we will not be able to continue using it. On the other hand, sustainable energy sources provide us with a supply we can never run out of, meaning increased energy security for future generations.

The Intergovernmental Panel on Climate Change emphasizes that these energy sources are essential for achieving long-term emissions reductions.

Burning Fossil Fuels? Only for the Time Being

Burning fossil fuels provides the majority of global energy. However, this natural resource is not sustainable and releases many harmful emissions when it is burned.

While fossil fuels are cheap and efficient, the globe should move forward to find better solutions on how to create energy. That way, we can avoid the negative effects that come along with burning fossil fuels while still providing the energy our planet relies on.

In the meantime, while the world energy system is still dependent on fossil fuels, you can make a difference by participating in carbon offsetting programs. These programs are designed to mitigate the carbon released from activities that burn fossil fuels.

For example, if you are taking a flight somewhere, you can purchase carbon offset credits that go toward projects that support reducing the amount of carbon in the atmosphere. Visit Terrapass today and view all of our carbon offset programs for individuals and businesses.

FAQ: Burning Fossil Fuels

What happens when you burn fossil fuels?

Burning fossil fuels releases the energy stored in their hydrocarbons as heat, along with six main byproducts: carbon dioxide, carbon monoxide, sulfur dioxide, nitrogen oxides, lead, and particulate matter.

Why are fossil fuels burned in the first place?

They’re burned because they’re an energy-dense, relatively inexpensive way to generate power for electricity, transportation, and industry. Fossil fuels still supplied about 86% of global energy in 2025.

What are the effects of burning fossil fuels?

The three main effects are air pollution, water pollution, and climate change, driven by the carbon dioxide, sulfur dioxide, and other byproducts released during combustion.

Which fossil fuel burns the cleanest?

Natural gas is the cleanest-burning of the three primary fossil fuels, emitting less air pollution and CO2 than coal or oil, though it’s still mostly methane, a potent greenhouse gas.

What are the alternatives to burning fossil fuels?

Renewable sources like solar, wind, and hydroelectric power, along with nuclear energy, are the main zero-emission alternatives. All are considered essential for long-term emissions reductions.

Is the world still relying on fossil fuels in 2026?

Yes. Fossil fuels supplied about 86% of global energy in 2025, and global coal use hit a new record even as renewables grew, because overall energy demand keeps rising.

Brought to you by terrapass.com

The post What Happens When You Burn Fossil Fuels? Effects & Alternatives appeared first on Terrapass.

Key takeaways

- SBTi is the default reference point for corporate climate action: 51% of Fortune Global 500 companies now hold net-zero targets, up from 8% in 2020, and over 11,000 organizations worldwide have SBTi-validated targets.

- Net Zero Standard V2 redefines climate leadership as reducing emissions and mitigating ongoing emissions, not reduction alone.

- The new standard adds flexibility through five-year cycles, a “best efforts” standard, and an Asset Transition Method for companies whose path to net-zero doesn’t fit a straight-line trajectory.

- Voluntary carbon credits are formally recognized for the first time, with reduction and removal credits accepted from 2027, and removals required from 2035.

- Companies with 2030 targets keep using V1 for their current cycle and move to V2 in 2028; companies without targets can start using V2 on February 1, 2027.

Why every business needs to understand the SBTi Net-Zero Standard revision

The Science Based Targets initiative (SBTi) has become the default reference point for credible corporate climate action. Net-zero targets are now held by 51% of Fortune Global 500 (FG500) companies, up dramatically from just 8% in 2020, and more than 11,000 organizations worldwide have set SBTi-validated targets.

However, SBTi’s influence extends well beyond the companies formally participating in the program. Every business in the value chain of an SBTi participant will have to reduce its own carbon emissions, and businesses that aren’t SBTi participants themselves still look to the program for guidance on climate action.

In short, SBTi gives every business a credible blueprint for climate action, and companies that follow its principles can pursue climate action with confidence, whether or not they’re formally part of the program.

How will the Net Zero Standard revision affect business climate action?

SBTi participation is expected to grow. Despite strong target-setting participation among the F500, only 17% of companies use the SBTi Net Zero Standard V1 beyond target setting, largely because its rules have been seen as too rigid to apply in practice. Much of the Net Zero Standard revision has focused on creating more flexibility to enable higher participation. Medium and small businesses will also increasingly feel pressure for climate action, since SBTi mandates that its participants reduce carbon emissions across their value chains.

Net Zero Standard V2 also redefines climate leadership: leading climate action now means reducing emissions and mitigating ongoing emissions. Reducing your own emissions while ignoring the emissions you continue to release along the way is no longer considered leadership. Supporting voluntary carbon projects with high-integrity carbon credits is now backed by the leading authority on corporate climate action.

What lessons shaped the Net Zero Standard V2 revision?

The revision reflects a few learnings about what actually drives climate progress, and how SBTi built those lessons into the new standard.

| Net Zero Standard V1 Learnings | Net Zero Standard V2 Implementation |

|---|---|

| Making real short-term progress is more important and more difficult than making big long-term promises | Focus on short-term climate progress |

| Every company has a different path to net zero that doesn’t always fit generalized net-zero rules | Create asset transition plans based on each company’s unique asset lifecycles and capital planning |

| We need to mitigate our ongoing emissions to keep global carbon emissions in check | Reduce global carbon emissions by financing voluntary carbon projects with high-integrity carbon credits |

What are the key changes between the old and new Net Zero Standard?

Both versions of the standard are grounded in net-zero by 2050. However, the old standard treated climate leadership as simply reducing emissions, expected a long-term commitment to net zero, based emission reduction targets on generalized net-zero goals, revoked status from companies that fell behind on targets, and ignored voluntary carbon projects entirely.

The new standard treats climate leadership as reducing emissions and mitigating ongoing emissions. It shifts the focus to short-term progress through five-year cycles, and it bases emission reduction targets on both the net-zero goal and a company’s own asset decarbonization plan. A new Asset Transition Method lets companies set decarbonization targets through asset plans with committed, verifiable steps; an ambitious but achievable path based on a company’s starting point, financial resources, and technology, with multiple pathways to reflect the unique opportunities and constraints of different industries and companies.

Crucially, the new standard moves to a “best efforts” basis that creates real flexibility on progress against targets. Businesses that miss their targets can keep their status if they’ve used “every lever” within their control, and minimum progress rules will be set out in the SBTi Assurance Manual.

Finally, the new standard formally uses voluntary carbon projects to mitigate ongoing emissions. From 2027 through 2034, this mitigation is recognized, and both carbon reduction and removal credits are accepted. From 2035 forward, mitigation with carbon removal credits becomes required, with durability matching between the removal and the emission it offsets.

| Old Net Zero Standard | New Net Zero Standard |

|---|---|

| Grounded in net-zero by 2050 | Grounded in net-zero by 2050 |

| Climate leadership is reducing emissions | Climate leadership is reducing emissions and mitigating ongoing emissions |

| Make a long-term commitment to net-zero | Focus on short-term progress in 5-year cycles |

| Emission reduction targets are based on net-zero goal |

|

| Businesses who fall behind targets lose status |

|

| Ignores voluntary carbon projects |

|

When does the new Net Zero Standard take effect?

Companies with existing 2030 targets should continue using the old Net Zero Standard for their current cycle, and start using the new Net Zero Standard in 2028 to set targets for the next cycle (2030–2035).

Companies that don’t yet have targets can use the new Net Zero Standard starting February 1, 2027.

What are SBTi’s Category A and Category B companies?

The new Net Zero Standard splits companies into two categories, with different requirements attached to each.

Category A covers large companies from all countries and medium-sized companies from high-income countries. A company from any country qualifies if it meets at least one of: net turnover of €450 million or more, or 1,000 or more full-time employees. A company from a high-income country qualifies if its Scope 1 and 2 emissions are 10,000 tCO2e or more, or if it meets at least two of: balance sheet of €25 million or more, net turnover of €50 million or more, or 250 or more full-time employees.

Category B covers small companies from all countries and medium-sized companies from lower-income countries.

How do Scope 1 targets work under Net Zero Standard V2?

Scope 1 targets aim to transition companies to net-zero direct emissions by 2050 or sooner, and companies can choose from three approaches.

- Absolute emissions reduction follows a straight-line emissions trajectory from the target base year to the net-zero year.

- Emissions intensity reduction lets companies follow sector-specific pathways designed to reflect the reduction opportunities available in sectors like steel, cement, or chemicals.

- Asset transition is designed for companies whose capital stock turnover doesn’t follow a linear or sector pathway. These companies design a transition plan to operate existing assets efficiently and replace them with low-carbon assets, using predetermined milestones.

How do Scope 2 targets work under Net Zero Standard V2?

Scope 2 targets address emissions from purchased electricity through three pathways:

- Reducing electricity consumption,

- Reducing grid consumption by installing onsite or direct-line offsite clean energy generation, and

- Cleaning up the regional grid using market-based tools like PPAs, RECs, and GOs that drive clean energy development.

V2 introduces a dual Scope 2 framework requiring two separate targets, with an overall goal of 100% low-carbon electricity by 2040.

The location-based target addresses the carbon intensity of a company’s physical power use, and requires companies to show that their grid consumption is falling and/or that their physical grid use is getting cleaner; in other words, that their market-based solutions are actually making the grid cleaner.

The market-based (or zero-carbon electricity) target tracks a company’s use of low-carbon power generation contracts and Energy Attribute Certificates. It requires geographical matching of these certificates with electricity consumption based on deliverability regions (grid regions); annual matching is allowed, though hourly matching is encouraged. Category A companies with large electricity loads must report the percentage of their Scope 2 electricity consumption matched with low-carbon attributes on an hourly basis, and there’s an optional recognition framework for companies that meet hourly matching thresholds.

How do Scope 3 targets work under Net Zero Standard V2?

Scope 3 targets share the same 2050-or-sooner net-zero goal, but companies set near-term targets only for material emissions sources in their value chain and areas where they have real influence. Long-term Scope 3 targets are generally not required.

Limited, justified exclusions are allowed for near-term targets, including categories that individually account for less than 5% of total Scope 3 emissions, and activities where a company lacks practical influence, like leased assets it doesn’t operationally control, or the processing of sold products. Optional exclusions are also available in specific categories.

Companies can choose from three approaches to near-term Scope 3 targets:

- An overarching emissions reduction target, which follows a linear contraction of emissions from the base year to residual emissions of 10% or less by 2050 or sooner;

- An overarching supplier/customer alignment target, benchmarked against a growing share of tier 1 suppliers and customers reaching net-zero by 2050 or sooner; or

- A category- or activity-specific target, tailored for companies with concentrated emissions in particular Scope 3 categories or high-emitting activities.

What is “ongoing emissions mitigation” under the new SBTi standard?

This is one of the most significant additions in Net Zero Standard V2. Accelerated climate contributions are needed to help the world achieve climate objectives, limit temperature overshoot, mitigate transition risks, and support the scale-up of climate solutions, and V2 formally recognizes that. Ongoing emissions mitigation runs as a parallel track to companies also reducing their own emissions.

The framework is initially voluntary, with recognition available at three contribution levels to encourage early action.

- Engaged companies address more than 1% of total Scope 1, 2, and 3 emissions.

- Advanced companies address more than 10% of total Scope 1, 2, and 3 emissions, including 100% of Scope 1 and 2 emissions.

- Leadership companies address 100% of total Scope 1, 2, and 3 emissions with a contribution budget of $80/tCO2e.

Carbon credits used for this purpose have to meet certain quality standards. They must be ex-post (issued after the mitigation has actually occurred), independently third-party-assured, emissions reductions or removals, measured in tCO2e, that occur within five years prior to the reporting year. They must be sourced from outside the company’s own value chain. Further minimum criteria will be set to align with high-integrity frameworks, with additional details on the recognition program expected in the second half of 2026.

Starting in 2035, carbon removals become mandatory for Category A companies. From that point, the carbon removal coverage requirement rises linearly from 1% of Scope 1–3 emissions to 100% by a company’s net-zero year. Within that, 10% of long-lived GHG emissions must specifically be covered by durable removals, also rising linearly to 100% by the net-zero year.

How must companies neutralize residual emissions?

At a company’s net-zero target year and thereafter, it must reduce its Scope 1, 2, and 3 emissions to zero or to residual levels, and neutralize all residual emissions using eligible carbon removals. Those removals have to meet two conditions: they must occur within the same reporting period as the residual emissions they’re neutralizing, and long-lived GHGs must be neutralized with long-lived removals, matching the durability of the removal to the atmospheric lifetime of the emission being addressed.

What is the SBTi implementation hierarchy?

Net Zero Standard V2 also lays out how companies should prioritize their actions for credible target delivery, in three tiers.

- Direct actions, at the activity level, are actions that reduce emissions at the source within a company’s own operations and value chain; things like efficiency improvements, fuel switching, and engaging suppliers and customers to reduce their emissions.

- Actions within shared systems, or activity pools that reduce the emissions of shared systems like electricity or gas grids. This includes market instruments that convey low-carbon attributes, such as PPAs, RECs, and GOs, all of which must meet minimum integrity criteria that SBTi will elaborate on in future guidance.

- Sector-level actions relate to the same type of activity occurring in a relevant geography or system, in a way that meaningfully reduces the emissions a company is responsible for.

How Terrapass helps businesses meet the new SBTi standard

As the rules around carbon credits become more rigorous, the quality of the credits behind them matters more than ever. Terrapass has expanded our global network of carbon projects: more project types, locations, prices, ICVCM CCPs, and UN SDGs, spanning super-pollutant destruction, nature-based solutions, and durable removals. We offer Green-e® Climate Certification and we only source from third-party-verified projects on ICVCM-Eligible registries.

We also help clients with impact beyond carbon: EACs, RECs, and GOs including Green-e® Certified credits that support leading renewable energy projects; water credits that support water restoration projects; and custom environmental product needs like RNG and SAF. Wherever your organization is on its sustainability journey, we help clients around the world address climate risk, advance their environmental and social goals, and get the most out of their sustainability budgets.

FAQ: SBTi Net-Zero Standard revision

What is the SBTi Net-Zero Standard?

It’s the framework the Science Based Targets initiative publishes for companies that want validated, credible net-zero targets tied to limiting global warming.

What is changing in the SBTi Net Zero Standard V2 revision?

The biggest changes are more flexibility (five-year cycles and a “best efforts” standard), a new Asset Transition Method for companies whose emissions don’t follow a straight-line path, and formal recognition of voluntary carbon credits for mitigating ongoing emissions.

When do companies need to switch to the new SBTi standard?

If your company already has 2030 targets, you keep using V1 for your current cycle and move to V2 in 2028. If you don’t have targets yet, you can start using V2 as of February 1, 2027.

Can companies use carbon credits to meet SBTi targets?

They can. Under V2, high-integrity carbon reduction and removal credits count toward mitigating ongoing emissions from 2027 through 2034. Starting in 2035, only removal credits count, and they need to be durability-matched to the emissions they offset.

What’s the difference between Category A and Category B companies under SBTi?

Category A is large companies everywhere plus medium-sized companies in high-income countries, based on thresholds like revenue, headcount, or emissions. Category B is small companies everywhere and medium-sized companies in lower-income countries.

What happens if a company misses its SBTi target?

Under the old standard, falling behind could cost a company its SBTi status. Under V2’s “best efforts” approach, a company can hold onto its status as long as it’s used every lever within its control, with minimum progress rules coming in the SBTi Assurance Manual.

Sources: This post is based on Terrapass’s internal analysis of the SBTi Corporate Net-Zero Standard V2.0. Facts and figures were checked against SBTi’s official V2.0 announcement, SBTi’s Corporate Net-Zero Standard V2.0 — Chapter 6: Ongoing Emissions Responsibility, Trellis’s coverage of the standard, Trellis’s reporting on Ongoing Emissions Recognition costs, Sylvera’s analysis of what comes next, Anthesis Group’s Fortune 500 net-zero commitments research, and Climate Impact Partners’ seventh annual FG500 analysis, as reported by CarbonUnits.com.

The post SBTi Net-Zero Standard V2: What the Revision Means for Every Business appeared first on Terrapass.

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy10 months ago

Renewable Energy10 months agoSending Progressive Philanthropist George Soros to Prison?

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits