As artificial intelligence (AI) continues to transform industries and unlock new opportunities, its environmental impact is also a matter of concern. While AI holds immense potential to combat climate change, it paradoxically contributes to the problem it aims to solve. The computational intensity of AI training and deployment leaves a significant carbon footprint. So, what’s the responsible way to savor the benefits of AI without worsening the climate crisis? The answer is Green AI.

So, What Is Green AI?

Green AI is a movement and an innovation that seeks to balance technological advancement with environmental sustainability. Green AI, also referred to as Sustainable AI or Net Zero AI, encompasses practices to reduce the carbon footprint of artificial intelligence technologies. Unlike traditional approaches, Green AI integrates sustainability into every stage of the AI lifecycle, from research and development to deployment and maintenance.

Furthermore, understanding the differences between conventional AI and Green AI is key to addressing this growing challenge.

Traditional AI vs. Green AI: A World of Difference

Traditional AI focuses on achieving unmatched accuracy in tasks like language translation, image recognition, and autonomous driving. While its applications are groundbreaking, this accuracy comes at a cost. Training large-scale AI models often require enormous computational resources, consuming vast amounts of energy.

For example, a nature.com study revealed the carbon footprint of training a single big language model is equal to around 300,000 kg of carbon dioxide emissions. This could be quantified as equivalent to 125 round-trip flights between New York and Beijing, a quantification that laypersons can visualize.

Thus, conventional AI overlooks energy efficiency. It also increases costs for businesses and excludes smaller players from entering the AI landscape. The worst outcome is the damage done to the environment from its carbon footprint, suppressing its potential to mitigate climate change.

In contrast, Green AI prioritizes energy-efficient practices. By focusing on sustainable development and deployment of AI systems, it seeks to minimize environmental harm without compromising innovation. Green AI introduces efficiency as a key metric alongside accuracy. It also advocates solutions that deliver high performance while conserving resources.

AI Powering Innovation but at What Cost?

We projected this study from ScienceDirect to understand the energy appetite of AI solutions. AI is growing rapidly, with bigger data needs and more complex models. However, this doesn’t always lead to equally big improvements in accuracy. While large language models (LLMs) like ChatGPT drive innovation, they come with significant environmental costs. Let’s dig deeper…

AI’s Growing Energy Appetite

The same report explains training GPT-3, for instance, consumed 1287 MWh of electricity and emitted 550 tons of carbon dioxide—comparable to flying 33 times between Australia and the UK.

The energy required for AI isn’t just during training. Using systems like GPT-3 also carries a hefty price. In January 2023 alone, GPT-3 processed 590 million queries, consuming energy equivalent to that of 175,000 people. On a smaller scale, each ChatGPT query uses as much power as running a 5W LED bulb for over an hour.

Fig: CO2 equivalent emissions for training ML models (blue) and of real-life cases (violet). In brackets, the billions of parameters adjusted for each model.

Source: ScienceDirect

Source: ScienceDirect

Deloitte’s recent report, “Powering Artificial Intelligence: A study of AI’s environmental footprint”, revealed the following findings:

- Between 2021 and 2022, data centers accounted for 98% of Meta’s additional electricity use and 72% of Apple’s between 2022 and 2023.

- AI adoption will fuel data center power demand, likely reaching 1,000 terawatt-hours (TWh) by 2030, and potentially climbing to 2,000 TWh by 2050.

- This will account for 3% of global electricity consumption, indicating faster growth than in other uses like electric cars and green hydrogen production.

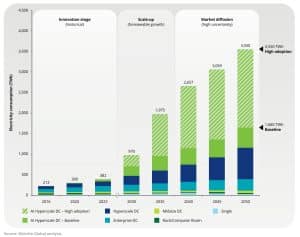

AI Data Centers: Energy Efficient or Energy Waste?

Data centers are the backbone of AI training and deployment, often referred to as the “cloud.” However, they rely on physical infrastructure for computing, processing, storing, and exchanging data. They require massive power and contribute heavily to the energy consumption of tech companies.

Different types of data centers have unique energy demands. Basic computer rooms handle simple tasks, while mid-size and large-scale enterprise data centers manage more complex operations. Hyperscale data centers, owned by tech giants have maximum hardware density and handle massive computational workloads, consuming the most energy.

Within this category, AI hyperscale data centers are emerging as a distinct segment. These centers are specifically built for generative AI and machine learning tasks, requiring high-performance GPUs for model training and inference.

This results in higher server power usage and the need for advanced cooling systems, further increasing energy consumption. Smaller data centers often lack the capacity for these high-demand workloads, driving the growth of AI-focused hyperscale facilities.

Fig: Data centers’ electricity consumption by server type and scenarios

But as they expand, a critical question remains: How sustainable are AI hyperscale data centers in the fight against climate change?

Well, this is where the demand for Green AI garners importance.

Why Green AI Matters?

The environmental cost of AI is no longer a hypothesis, it is palpable all around. Even blockchain technologies like cryptocurrency mining have demonstrated how unchecked digital innovation can lead to unsustainable energy consumption.

Coming straight to the topic, Green AI holds the promise of reversing this trend. For example, AI-powered tools can optimize supply chains, reduce waste, and improve energy grid efficiency. If developed responsibly, AI could become the key driving force behind the global effort to achieve carbon neutrality.

Thus, by combining innovation with sustainability, Green AI can meet the growing demand for computational power while reducing its impact on the environment.

Core Principles of Green AI

This means leveraging AI solutions that are not only effective in optimizing energy use in applications but are also inherently low-energy consumers. It’s crucial to balance AI’s benefits with its environmental impact. It means AI should support sustainability goals and not worsen the problems that it aims to solve.

Energy Efficiency

Green AI encourages the design of algorithms and models that consume less energy. Researchers can achieve this by developing lightweight models or installing techniques like pruning, quantization, and model distillation, which reduce computational requirements.

Hardware Optimization

Using energy-efficient hardware, such as GPUs with higher FLOPS per watt or specialized Tensor Processing Units (TPUs), can significantly cut AI’s energy consumption. Parallelizing tasks across multiple cores also helps reduce training times and emissions, though excessive cores may increase energy use disproportionately.

Another technique is edge computing which means processing data locally to avoid energy-intensive transmissions to cloud or data centers and optimizing resources for IoT (The Internet of Things) devices. Together, these strategies enable powerful AI performance with a smaller environmental footprint.

Data Center Optimization

Adopting renewable energy sources for powering data centers and AI operations is a significant milestone of Green AI. Companies like Google and Microsoft are already leading the charge by transitioning their cloud services to run on clean energy.

To make data centers more energy-efficient, researchers have created algorithms and frameworks that balance server loads, optimize cooling systems, and allocate resources more effectively. All these processes are included in data center optimization that cuts down energy use and emissions.

Transparency and Accessibility

Green AI promotes transparency in reporting the environmental costs of AI projects. Standardized metrics for energy consumption and emissions can help developers and organizations make informed decisions about their AI strategies.

Some of the tools that are used to estimate the carbon footprint of AI technologies are CarbonTracker, CodeCarbon, Green algorithms, and PowerTop.

Additionally, by lowering computational barriers, Green AI fosters inclusivity. Smaller organizations and researchers gain access to advanced tools without burdening themselves with high environmental and financial costs.

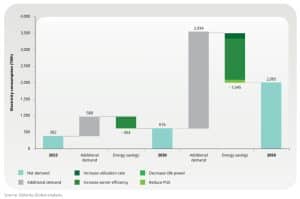

Fig: Achievable electricity demand reduction through energy savings, “High adoption” scenario

Policies Driving Green AI

The United Nations’ Sustainable Development Goals (SDGs) highlight the need for a sustainable future. Goals like Affordable and Clean Energy and Industry, Innovation, and Infrastructure are driving the rise of Green AI. Industry leaders are rethinking data center designs and operations to lower energy consumption and environmental impacts. This shows their eagerness to demonstrate proactive efforts toward sustainability.

While Green AI initiatives are mostly industry-led, some regions are implementing supportive policies. These range from monitoring low-impact data centers to stricter regulations for areas where grid stability is at risk. Thus, balancing these policies can encourage sustainable practices without moving operations to less regulated regions.

Notable policies include:

- European Code of Conduct for Data Centers (EU DC CoC)

- Energy Efficiency Directive (EED)

- Singapore Green Data Centre Roadmap

China has also introduced measures like the Three-Year Action Plan on New Data Centres, while the U.S. lacks federal-level regulations specific to data centers.

Policymakers can amplify these efforts by co-developing standards with industry leaders. Collaborative strategies ensure data centers meet climate goals without compromising growth or grid stability.

Green AI demonstrates that with the right policies and innovations, the tech industry can lead the way to a more sustainable future.

Green AI Takes the Spotlight at COP29

As world leaders convened in Baku, Azerbaijan, for COP29, discussions pointed to the role of AI in promoting environmental sustainability. A Deloitte-hosted panel brought together experts from NVIDIA, Crusoe Energy Systems, EON, and the International Energy Agency (IEA) to explore strategies for reducing AI’s environmental footprint.

Josh Parker, senior director of legal–corporate sustainability at NVIDIA, said,

“We see a very rapid trend toward direct-to-chip liquid cooling, which means water demands in data centers are dropping dramatically right now.”

According to NVIDIA, designing data centers while keeping energy efficiency at the highest priority right from the beginning is very much essential. As AI demands grow, sustainable infrastructure will be critical. Parker highlighted that current data centers are becoming outdated and inefficient.

He added, accelerated computing platforms are 10X more efficient than traditional systems for running workloads. This creates a significant opportunity to cut energy consumption in existing infrastructures.

Accelerated Computing: A Path to Green AI

Parker once again emphasized that accelerated computing represents the most energy-efficient platform for AI and many other applications. Over the past few years, energy efficiency for accelerated computing has improved dramatically, with a 100,000x reduction in energy consumption.

- In just the last two years, energy use for AI inference tasks dropped by 96%, with systems becoming 25x more efficient for the same workload.

Accelerated computing uses GPUs to process tasks faster and more efficiently than traditional CPUs. By handling multiple tasks simultaneously, GPUs reduce the energy required for AI workloads. It’s one of the techniques that come under hardware efficiency and data center optimization.

Furthermore, NVIDIA emphasized the need for energy-efficient infrastructure in data centers. Innovations like liquid-cooled GPUs are transforming cooling methods. Unlike traditional air conditioning, direct-to-chip liquid cooling consumes less power and water while maintaining effective temperature control.

The Bottom Line

Deloitte’s findings have adeptly showcased AI’s potential in driving climate-neutral economies. Green AI strategies focus on minimizing environmental impact by improving hardware design and increasing the use of renewable energy.

Industry leaders are spearheading these efforts, highlighting the effectiveness of sustainable computing practices. The shift toward accelerated computing and energy-efficient design is paving the way for AI to support global climate goals.

As we face a climate crisis, the integration of Green AI principles is no longer optional—it is essential. By redefining how AI solutions are developed, we can harness their power for good while minimizing their environmental toll. The road ahead demands collective effort, innovation, and accountability. Last but not least, Green AI is not just a technological imperative but a moral responsibility to ensure a greener future.

Key Sources:

- A review of green artificial intelligence: Towards a more sustainable future – ScienceDirect

- AI at COP29: Balancing Innovation and Sustainability | NVIDIA Blog

The post Green AI Explained: Fueling Innovation with a Smaller Carbon Footprint appeared first on Carbon Credits.

Carbon Footprint

Carbon Market 2026: Supply Squeeze Pushes Premium Carbon Credit Prices Up, Sylvera Finds

The global carbon market is changing fast in 2026. The latest insights from Sylvera’s State of Carbon Credits report show a clear shift. Volumes are falling, but value is holding steady. This means buyers now focus more on quality than quantity.

Furthermore, the market is splitting into two clear segments. High-quality credits are in demand and sell at higher prices. Older or lower-quality credits are losing interest. This divide is growing stronger and shaping how the market will evolve in the coming years.

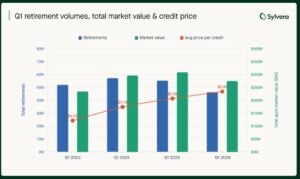

Shell’s Sharp Cut Pulls Down Market Volumes

Carbon credit retirements reached 51 million in the first quarter of 2026. This is down from 55.3 million in the same period last year. The total market value also fell slightly to $290 million, compared to $309 million a year ago.

Despite this decline, prices did not weaken. The average price per credit increased to $5.69 from $5.60. This shows that buyers are willing to pay more for credits they trust.

Interestingly, a major reason for the drop in volumes was reduced activity from Shell. The company sharply cut its purchases. It retired just 494,000 credits in Q1 2026, compared to 6.7 million in Q1 2025 and 5.6 million in 2024. This single change had a large impact on the overall market.

Value Now Drives the Market

The carbon market now runs on a simple idea. Value matters more than volume. Buyers want credits that deliver real environmental impact. They prefer projects with clear data, strong verification, and proven results.

High-quality credits now define the market. These credits meet strict standards and often align with compliance systems. Because of this, they command higher prices and stronger demand.

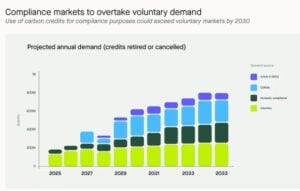

This shift is also linked to the rise of compliance markets. Programs like CORSIA are increasing demand for reliable credits. As a result, voluntary buyers and compliance buyers now compete for the same supply.

Experts expect this trend to grow stronger. Compliance demand could surpass voluntary demand by 2027. This will increase pressure on supply and push premium credit prices higher.

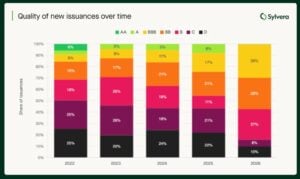

The report highlighted that, investment-grade credits (BBB+) now command an average of $20.10 per credit in Q1 2026, up from $18.10 in Q1 2025, as shown in the image below:

Recap of 2025 Carbon Market

Compliance programs made up 24% of total retirements in 2025. According to Sylvera, this share is rising fast. It is expected to go beyond voluntary demand by 2027. This growth is mainly driven by CORSIA Phase 1 rules and the expansion of domestic carbon markets.

This means compliance demand is set to change the carbon market in a big way. Soon, both voluntary buyers and regulated systems will compete for the same high-quality credits. This is already making supply tighter and more competitive.

At the same time, international trading under Article 6 gained momentum. In 2025, around 20 new bilateral agreements were signed, and the first large-scale carbon credit trades took place. This shows that global carbon transfer systems are now becoming active in practice.

However, the system is also becoming more complex. One key factor is “corresponding adjustments,” which now decide whether a credit is fully acceptable in compliance markets. In addition, countries like China, Japan, Brazil, and Indonesia are building their own domestic carbon systems.

These systems are expected to create strong new demand, but they also add more rules and complexity to the market.

Supply Crunch Becomes the Key Challenge

However, Sylvera has flagged a different scenario for his year. Supply is now the biggest issue in the market. High-quality credits are becoming harder to find. Many credits exist, but not all meet strict requirements.

Furthermore, the main bottleneck is coming from approvals under Article 6. These rules govern international carbon trading. Delays in approvals mean many credits cannot yet enter the market. Now this creates a gap. Supply looks strong on paper, but usable supply remains limited. This shortage keeps prices firm and supports premium credits.

CORSIA Supply Expands, But Not Enough

There has been progress in aviation supply. Eligible credits under CORSIA reached 32.68 million. This is more than double last year’s level.

These credits come from major registries like Verra, Gold Standard, and ART TREES. However, supply still falls short in practice. Not all credits meet full compliance standards. This keeps the market tight and competitive.

Moving on, the question is what’s driving market growth.

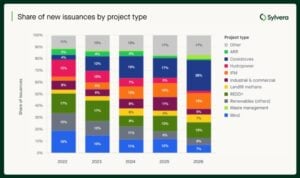

Cookstoves Drive Market Growth

Cookstove projects are growing quickly. Their share increased from 17% in 2025 to 26% in Q1 2026. Africa leads this segment. Around 80% of the supply comes from the region. Most of these projects also meet compliance requirements under CORSIA.

Quality is improving in this category. Developers are moving away from older methods. They now use stronger, data-driven approaches. This shift improves trust and attracts more buyers.

Other projects:

- REDD+ Regains Trust: Forestry projects under REDD+ are making a comeback. Their share of retirements rose to 25% in Q1 2026. These projects faced heavy criticism in the past. However, new rules and better standards are restoring confidence. Updated methodologies have removed weaker credits. This has improved the overall quality of supply. Global policy clarity has also helped. Buyers now have more confidence in using REDD+ credits in compliance markets. This has supported demand.

- Waste management projects: They are growing in importance, and their share reached 10% of total retirements, the highest so far. Landfill methane projects are leading this growth. These projects are easier to measure and verify. They also meet compliance standards. Buyers are now exploring options beyond traditional sectors. Waste projects offer a reliable and practical solution.

New Credit Types Expand the Market

Several new project types are growing fast. They are adding fresh supply and attracting new buyers.

- Clean water projects have seen strong growth in recent years. They now produce millions of credits annually. Marine and mangrove projects are also gaining attention. They offer strong environmental benefits and long-term carbon storage.

- Industrial projects focused on nitrous oxide reduction are expanding as well. These projects are highly measurable and align well with compliance systems. At the same time, regenerative agriculture is growing at the fastest pace. It has moved from almost no activity to millions of credits in a short time.

These new categories are helping the market grow. However, quality remains the key factor that drives demand.

Buyers Shift Toward Better Credits: Regional Analysis

Buyer behavior is changing across regions. The United Kingdom is leading the move toward high-quality credits. Companies are under pressure to show real climate action. This has pushed them to choose better credits.

The United States and Canada are also improving. Buyers prefer projects that meet both voluntary and compliance standards. This supports demand for high-quality supply.

North America Sets the Benchmark

North America sets the benchmark for quality. A large share of its credits meets high rating standards. This strong quality supports higher prices. The average price reached $14.80, the highest globally. Strong domestic demand and strict standards drive this trend.

On the other hand, South America is seeing strong demand but limited new supply. This creates pressure in the market. Prices have slightly declined to $11.50. However, the quality mix is improving. Waste projects are helping fill the gap left by falling forestry supply.

- Europe remains the largest market by volume. However, the quality mix is still uneven. Some buyers continue to use lower-rated credits.

- Japan and South Korea focus on lower-cost options like hydropower. This keeps their share of high-quality credits low. In Latin America, buyers often choose local projects. Limited regulatory pressure keeps the quality demand weaker.

- Africa is moving toward better quality. High-rated supply is increasing, while low-rated supply is falling. As explained before, cookstove projects are the main driver. At the same time, lower-quality forestry projects are declining. This improves the region’s overall market position.

- Asia faces weaker market conditions. Supply has dropped sharply due to fewer renewable energy projects. The average price stands at $5.30, the lowest globally. Demand remains steady but lacks strong growth. This keeps prices under pressure.

Indonesia Stands Out in Asia

Indonesia is a bright spot in the region. Credit prices have risen strongly in the past year. High-quality peatland projects are driving this growth. International deals under Article 6 are also adding value. These factors attract buyers looking for reliable credit.

This shows how strong quality and supportive policies can boost market performance.

Final Take: Quality Defines the Future

The carbon market in 2026 is clear and focused. Quality now drives demand, pricing, and growth. Buyers are becoming more selective. They want credits that are verified, reliable, and compliant.

Supply remains tight, especially for high-quality credits. At the same time, compliance markets are growing. This increases competition and pushes prices higher.

The gap between high- and low-quality credits will continue to widen. In simple terms, the market is no longer about how many credits exist. It is about how good they are.

- READ MORE: Top Carbon Credit Companies to Watch in 2026

The post Carbon Market 2026: Supply Squeeze Pushes Premium Carbon Credit Prices Up, Sylvera Finds appeared first on Carbon Credits.

Carbon Footprint

US and Australia Boost Critical Minerals Support with $3.5B Alliance, Challenging China’s Grip

Australia and the United States have launched a $3.5 billion critical minerals partnership, marking one of the largest bilateral efforts to secure materials essential for clean energy and electric vehicles (EVs).

The agreement focuses on strengthening supply chains for minerals such as lithium, cobalt, nickel, and rare earth elements. These materials are vital for batteries, solar panels, wind turbines, and other low-carbon technologies.

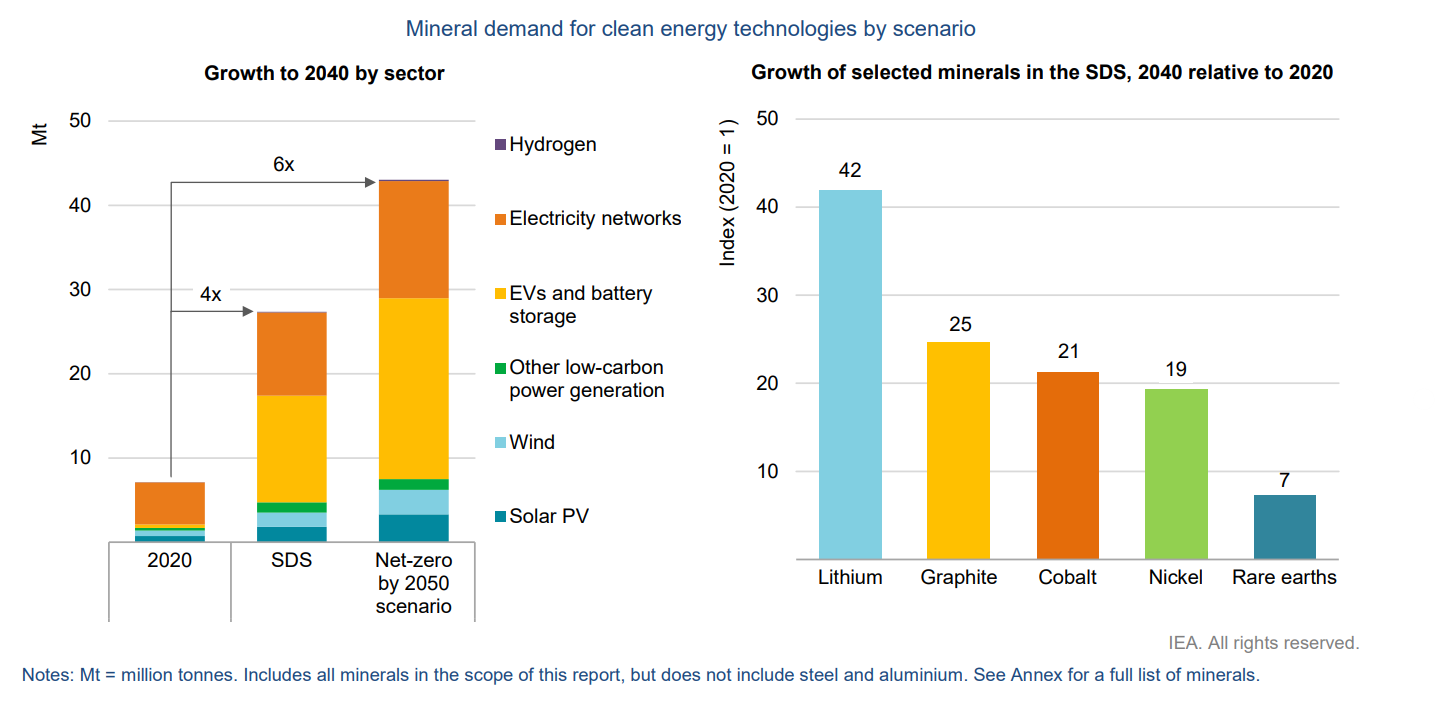

The deal comes as global demand for these minerals rises sharply. The International Energy Agency estimates that demand for critical minerals could quadruple by 2040 under net-zero scenarios. Lithium demand alone could grow more than 40 times by 2040, driven by EV adoption and battery storage.

Australia plays a central role in this supply chain. It currently produces about 55% of the world’s lithium, making it the largest global supplier. However, much of the processing still takes place overseas, creating supply risks for Western economies.

The new partnership aims to address this gap by boosting both extraction and domestic processing capacity.

Billions Back the Full Value Chain—from Mine to Market

The $3.5 billion investment will be deployed over seven years. The United States will give around $2.1 billion. This funding comes from the Defense Production Act and the Infrastructure Investment and Jobs Act. Australia will provide $1.4 billion through national financing programs.

The funding is designed to support the full value chain, from mining to refining to advanced research. The main areas of investment include:

- $1.8 billion for new mining projects and infrastructure upgrades

- $1.2 billion for processing and refining facilities

- $500 million for research, innovation, and sustainable extraction technologies

A key goal is to reduce reliance on external processing markets and build more resilient supply chains. This includes expanding refining capacity for lithium and rare earth elements, which are often processed outside producing countries.

The partnership is also expected to create economic benefits. Government estimates say about 15,000 direct jobs will be created. Additionally, around 30,000 indirect jobs will come from supply chains and related industries.

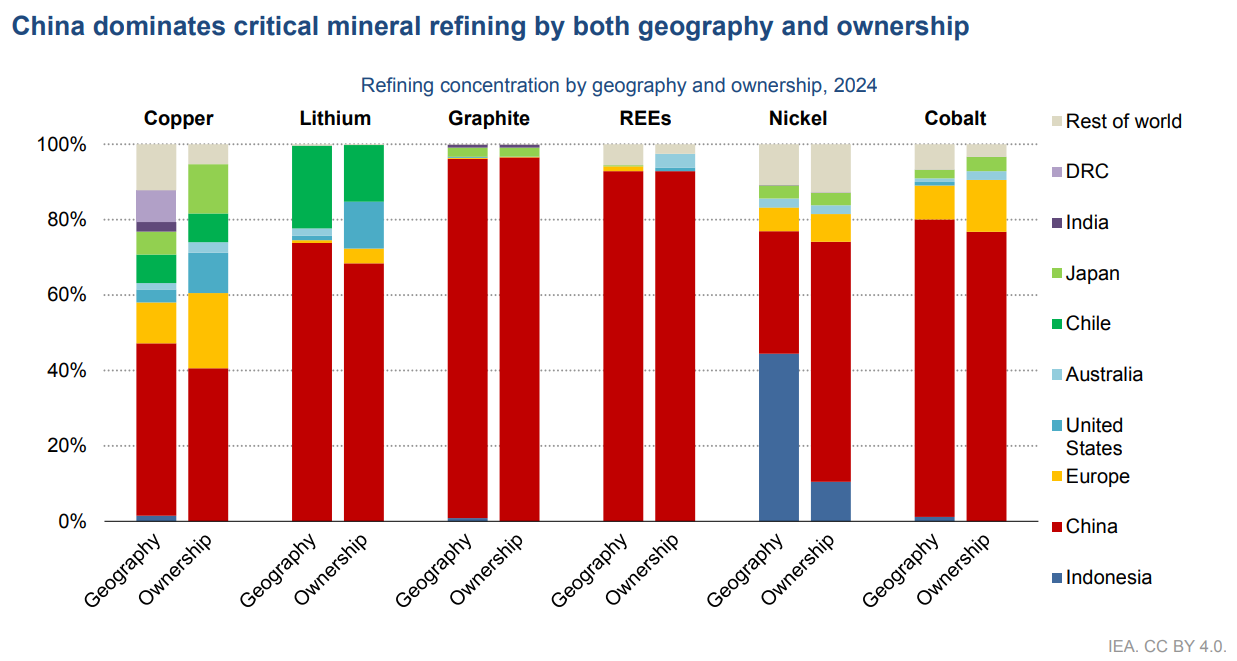

Breaking China’s Grip on Mineral Processing

The agreement reflects growing concern over the concentration of mineral processing in China. Currently, China dominates key parts of the global supply chain.

According to the International Energy Agency:

- China handles about 60% of global lithium processing

- It controls more than 80% of rare earth refining

- It also leads in battery component manufacturing

This dominance creates risks for supply security, pricing, and geopolitical stability. Disruptions in one region can affect global clean energy deployment.

By investing in alternative supply chains, Australia and the United States aim to diversify production and reduce these risks. The partnership could also encourage other countries to develop their own critical minerals strategies.

In addition, the deal may help stabilize prices for key materials. Volatility in lithium and nickel markets has impacted EV production costs. It has also delayed some renewable energy projects in recent years.

Supporting Climate Goals and the Energy Transition

The partnership has direct implications for global climate efforts. Critical minerals are essential for scaling clean energy technologies. Without a reliable supply, the pace of decarbonization could slow.

Battery storage is a key example. Energy storage systems help manage the variability of renewable energy sources like solar and wind. Expanding mineral supply will support the growth of these systems.

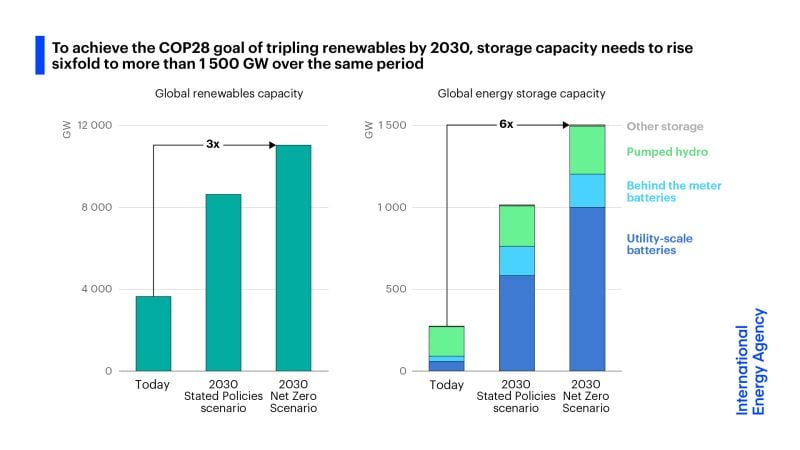

The IEA projects that global battery capacity must increase significantly to meet climate targets. Some estimates suggest energy storage capacity needs to grow more than sixfold by 2030 to stay on track for net-zero emissions.

The US-Australia alliance could help unlock this growth by ensuring stable access to raw materials. This, in turn, may reduce costs for batteries and renewable energy systems over time.

Both countries have also committed to improving environmental standards in mining. This includes reducing emissions, improving water management, and limiting land impacts. These measures are important because mining itself can be carbon-intensive.

Efforts to lower emissions in mineral extraction could also influence carbon accounting frameworks. As supply chains become more transparent, companies may need to track and report emissions linked to raw material sourcing.

ESG, Carbon Markets, and the New Mining Reality

The expansion of critical minerals supply chains is expected to influence carbon markets and ESG strategies.

As mining activity increases, so does the need to manage emissions. This could increase the need for carbon credits in the extractive sector. This is true for projects that cut or offset emissions from mining.

At the same time, improved supply chains for clean technologies may accelerate renewable energy deployment. This could support carbon reduction efforts across multiple sectors, including power generation and transportation.

The partnership may also lead to higher standards for responsible sourcing. Materials produced under strict environmental and social guidelines could command a premium in global markets.

This shift aligns with growing investor focus on ESG performance. Companies face growing pressure to show that their supply chains meet sustainability standards. This includes tracking emissions across Scope 1, 2, and 3 categories.

Over time, these trends could reshape how carbon credits are used. Companies may focus more on cutting emissions directly in their supply chains, rather than just using offsets.

Industry Scrambles to Secure the Next Wave of Supply

The announcement has received strong support from industry players. Major automakers and battery manufacturers are seeking secure and stable supplies of critical minerals. Companies like Tesla, Ford, and General Motors want to source materials from projects tied to the partnership.

Mining firms are also responding. Albemarle Corporation and Pilbara Minerals will likely gain from more investment and quicker project timelines.

Investor interest in the sector is rising as well. Global spending on energy transition minerals is growing rapidly, supported by both public and private capital.

The International Energy Agency reports that investment in critical minerals has increased sharply in recent years. This trend is expected to continue as countries compete to secure supply chains for clean energy technologies.

A Defining Shift in the Global Energy Economy

The $3.5 billion Australia–US critical minerals partnership represents a major step in reshaping global energy supply chains. It addresses a key bottleneck in the transition to a low-carbon economy: access to essential raw materials.

In the short term, the deal may help stabilize supply and reduce risks linked to market concentration. In the long term, it could accelerate the deployment of clean energy technologies and support global climate goals.

For carbon markets, the impact is indirect but important. More minerals can help speed up the use of renewables and energy storage. This, in turn, cuts emissions throughout the economy. At the same time, higher mining activity may drive demand for carbon credits and new emissions reduction strategies within the sector.

The success of the partnership will depend on execution. Expanding mining and processing capacity takes time, investment, and strong environmental oversight.

If these challenges are addressed, the alliance could serve as a model for future international cooperation on critical minerals. It also highlights how energy security, economic policy, and climate action are becoming increasingly connected.

Ultimately, as demand for clean energy continues to grow, securing sustainable and reliable mineral supply chains will remain a key priority for governments and industries worldwide.

The post US and Australia Boost Critical Minerals Support with $3.5B Alliance, Challenging China’s Grip appeared first on Carbon Credits.

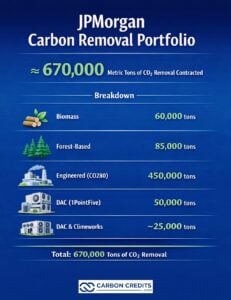

JPMorgan Chase has signed two major carbon removal agreements this month. The first one involves a purchase of 60,000 metric tons of durable carbon dioxide removal (CDR) over ten years from climate startup Graphyte. The deal uses biomass-based technology that converts agricultural and timber waste into stable carbon blocks stored underground.

In parallel, JPMorgan has also secured 85,000 tons of forest-based carbon removal credits through improved forest management projects. These credits, marketed by Anew Climate, come from U.S. forest projects managed by Aurora Sustainable Lands.

They aim to extend harvest cycles, boost forest health, and enhance long-term carbon storage. The approach helps maintain higher carbon stocks in working forests while supporting biodiversity and sustainable timber production.

Taylor Wright, Head of Operational Sustainability at JPMorgan Chase, noted:

“We were excited to add credits from the Little Bear Forestry Project to our carbon removal portfolio. The dynamic baselining provides meaningful evidence that these credits meet a high threshold for quality, supporting our interests as both a buyer and as a steward of market integrity.”

Carbon Removal Still Small, But Growing Fast

The agreements are part of a broader push by the bank to expand its carbon removal portfolio. While the total volume is small compared to global emissions, the deals highlight a shift in corporate climate strategies.

Companies are now focusing more on durable carbon removal, not just emission reductions. JPMorgan’s mix of engineered and nature-based solutions also reflects a growing trend toward portfolio diversification in carbon removal sourcing.

Carbon removal remains a small but critical part of climate action. The United States emits about 5 billion tons of CO₂ per year, showing how limited current removal volumes still are.

However, long-term demand is expected to grow sharply. The Intergovernmental Panel on Climate Change estimates that by 2100, the world might need to remove 100 to 1,000 gigatons of CO₂. By mid-century, annual removal should reach about 10 gigatons per year.

Today’s market is far from that scale. Most carbon removal deals are measured in thousands or hundreds of thousands of tons. But these early contracts are seen as critical. They help build supply, reduce costs, and attract investment into new technologies.

JPMorgan’s latest deals fit this pattern. Together, the 60,000-ton biomass contract and 85,000-ton forest-based agreement provide long-term demand signals across different removal pathways. This helps scale both emerging engineered solutions and more established nature-based approaches.

Turning Waste Into Permanent Carbon Storage

Graphyte’s process, known as “carbon casting,” uses natural carbon capture through plants. Biomass absorbs CO₂ through photosynthesis. The material is then dried, compressed, and sealed to prevent decomposition. This allows the carbon to remain stored for long periods.

The company uses waste materials such as crop residues and timber byproducts. This reduces the need for new land use and lowers overall costs. The process also uses relatively low energy compared to other removal methods.

Projects linked to the JPMorgan deal include facilities in Arkansas and Arizona. These projects also provide added benefits. For example, using forest thinning residues can help reduce wildfire risk and support land restoration.

This reflects a broader trend in carbon markets. Buyers are increasingly looking for projects that deliver both carbon removal and environmental co-benefits. The bank’s forest-based deal reinforces this trend by supporting improved forest management practices that enhance carbon storage while maintaining productive landscapes.

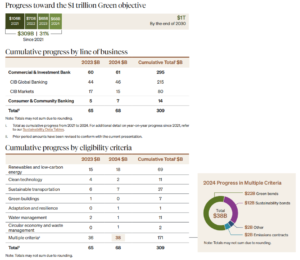

JPMorgan’s $1 Trillion Net Zero Strategy and Climate Finance Push

JPMorgan’s carbon removal investments are part of a wider climate strategy. The bank has committed to facilitating $1 trillion in climate and sustainable development financing by 2030. It has already deployed about $309 billion between 2021 and 2024 toward this goal.

In addition to financing, the bank is building a diversified carbon removal portfolio. Since 2023, it has signed deals to cut hundreds of thousands of tons of CO₂. This includes a plan for up to 800,000 tons of carbon removal through long-term contracts.

The company aims to match its unabated operational emissions with durable carbon removal by 2030.

JPMorgan is also investing in a range of technologies. These include direct air capture, bio-oil sequestration, biomass storage, and forest-based removal. Its latest forest deal shows a continued commitment to high-quality, nature-based removals that meet stricter standards for durability and verification.

This diversified approach helps reduce risk while supporting different pathways to scale. Compared to many financial institutions, JPMorgan remains an early mover. Most large buyers in carbon removal are still technology companies, particularly Microsoft.

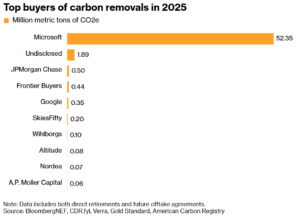

Microsoft Pullback Shakes Market Confidence

However, Microsoft, the largest buyer of carbon removal credits, has reportedly paused new purchases.

The tech giant has played a dominant role in the market. It accounts for up to 90% of global carbon removal purchases and has contracted more than 45 million tons of CO₂ removal to date. In 2025 alone, the company signed agreements for 45 million tons, doubling its 2024 volume and far exceeding any other buyer.

However, reports suggest the company may be adjusting the pace of new deals. This shift does not mean the end of carbon removal demand, but it signals a transition.

The market can no longer rely on a single dominant buyer. In this context, JPMorgan’s continued activity—across both engineered and nature-based deals—shows how new buyers are stepping in to support market stability.

Market Trends: From Cheap Offsets to High-Durability Carbon Credits

The carbon market is evolving quickly. Traditional carbon credits often focus on avoiding emissions, such as protecting forests. However, there is growing demand for removal-based credits that physically take CO₂ out of the atmosphere.

Corporate net-zero goals drive this shift. Many companies now face limits on how much they can reduce emissions directly. Carbon removal is becoming necessary to address remaining emissions.

At the same time, supply remains limited. High-quality removal credits are scarce. This keeps carbon prices high, especially for engineered solutions.

Early buyers like JPMorgan are helping shape the market. Long-term contracts provide price signals and encourage project development. They also help define standards for quality and verification.

Another key trend is the focus on durability. Buyers prefer solutions that store carbon for decades or centuries, rather than short-term offsets.

Early-Stage Market, High-Stakes Growth

Despite growing momentum, carbon removal is still in its early stages. Current volumes are small compared to global needs. Policy support is also limited in many regions.

However, corporate demand is rising. Deals like JPMorgan’s show how private sector investment is driving the market forward.

The combination of long-term contracts, new technologies, and climate finance is expected to accelerate growth. Over time, this could help bring down costs and expand supply.

For now, the focus remains on building scale. Each new agreement adds to a growing pipeline of projects. These projects will play a key role in meeting long-term climate targets.

JPMorgan’s latest purchases may be modest in size. But together, they reflect a larger shift. Carbon removal is moving from early experimentation to a more structured and investable market, supported by a broader mix of buyers and solutions.

The post JPMorgan’s Carbon Bet Marks a Turning Point for the Removal Market appeared first on Carbon Credits.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits