Over the weekend the Washington Spectator published my essay, Diary of a Transit Miracle, recounting the arduous march of NYC congestion pricing from a gleam in a trio of prominent New Yorkers’ eyes at the end of the 1960s, to the verge of startup at the upcoming stroke of midnight June 30, the startup time announced by the MTA last Friday.

Landing page for this post’s original version.

I’m cross-posting it here — the third post on the subject in this space in the past 12 months (following this in December and this post last June) — because the advent of congestion pricing in the U.S. is “a really big deal,” as a number of friends and colleagues have told me in recent weeks. As my new essay makes clear, charging motorists to drive into the heart of Manhattan isn’t just a rejection of unconstrained motordom, it’s a new beachhead in “externality pricing” — social-cost surcharging — of which carbon taxes are the ultimate form.

The essay features two governors, two mayors — one of whom I served a half-century ago as a lowly but admiring data cruncher — a civic “Walter Cronkite,” a Nobel economist, raucous transit activists, a gridlock guru and yours truly, plus a cameo appearance by Robert Moses. It includes footage of the historic 1969 press conference in which Mayor John Lindsay and two distinguished associates enunciated the core idea of using externality pricing to better balance automobiles and mass transit that animated the arduous but ultimately triumphant congestion pricing campaign.

— C.K., April 29, 2024

Diary of a Transit Miracle

A miracle is coming to New York City. Beginning on July 1, and barring a last-minute hitch, motorists will soon pay a hefty $15 to enter the southern half of Manhattan — the area bounded by the Hudson River, the East River and 60th Street.

An anticipated 15 percent or so of drivers will switch to transit, unsnarling roads within the “congestion zone” and routes leading to it. The other 80 or 90 percent will grumble but continue driving. That is by design. The toll bounty, a billion dollars a year, will finance subway enhancements like station elevators and digital signals that will increase train throughput and lure more car trips onto trains.

The result will be faster, smoother commutes, especially for car drivers and taxicab and Uber passengers, who will pay a modest surcharge of $1.25 to $2.50 per trip. Drivers of for-hire vehicles will benefit as well, as lesser gridlock leads to more fares.1

The miracle is three-fold: Winners will vastly outnumber losers; New York will be made healthier, calmer and more prosperous; and that this salutary measure is happening at all, after a half-century of setbacks.

Obstacles to congestion pricing

Congestion pricing, as the policy is known, faced formidable obstacles even beyond the difficulty inherent in asking a group of people to start forking over a billion dollars a year for something that’s always been free.

Congestion pricing also had to contend with: an ingrained pro-motoring ideology that casts any restraint on driving as a betrayal of the American Dream; a general aversion to social-cost surcharges (what economists call “externality pricing”); exasperation over the region’s balkanized and convoluted toll and transit regimes; and, of late, a decline in social solidarity and appeals to the common good.

The advent of congestion pricing in New York is, thus, cause not just for celebration but wonderment. How did this wonky yet radical idea advance to the verge of enactment?

Origins

The trail begins in the waning days of 1969, when newly re-elected mayor John Lindsay recruited two well-regarded New Yorkers to devise a plan to fend off a 50 percent rise in subway and bus fares.

William Vickrey, a Canadian transplant teaching at Columbia and a future Nobel economics laureate, was a protean theorist of externality pricing. New York-bred mediator Theodore Kheel was admired as a civic Walter Cronkite for his plain-spoken common sense.

Lindsay, too often dismissed as a lightweight, understood mass transit as key to loosening automobiles’ spreading chokehold over the city. He had made combating air pollution a pillar of his first term and was fast becoming an exemplar of urban environmentalism. From his municipal engineers, Lindsay knew that technology to clean up tailpipes still lay in the future. A transit fare hike that would add yet more vehicles to city streets imperiled his clean-air agenda.

The triumvirate proposed a suite of motorist fees to preserve the fare. Their program ― higher registration fees and gasoline taxes, a parking garage tax, doubled tolls ― though mild in today’s terms, threatened powerful bureaucracies and their auto allies. Newly dethroned “master-builder” Robert Moses opined that Kheel, in his zeal to save the fare, had “gone berserk over bridge and tunnel tolls.”2 The program went nowhere.

L to R: Kheel, Lindsay, Vickrey. Click arrow to view (please excuse two brief garbled passages toward end).

Moses was right to be alarmed. From a City Hall podium on Dec. 16, 1969, Mayor Lindsay showcased Kheel’s and Vickrey’s respective reports, “A Balanced System of Transportation is a Must” and “A Transit Fare Increase is Costly Revenue.” (Click link in still photo above to view 27-minute video.) The trio propounded a new urban doctrine rebalancing automobiles and public transportation: “Automobiles are strangling our cities… Starving mass transit imposes costs that are difficult to measure, yet real… Correcting the fiscal imbalance between transit and the automobile is key to enhancing our environment and quality of life…”

Their remarks set generations of urbanists on course toward congestion pricing.

Setbacks

Quantifying those precepts became my research agenda 40 years later. In the interim, two creditable attempts to enact congestion pricing crashed and burned.

The central element of Lindsay’s 1973 “transportation control plan” was tolls on the city’s East River bridges, a measure designed to eliminate enough traffic to satisfy federal clean-air standards. Though the plan’s formal demise didn’t come until 1977, in legislation written by liberal lawmakers from Brooklyn and Queens, the toll idea never stood a chance. Electronic tolling was 20 years away, and adding stop-and-go toll booths seemed more likely to compound vehicular exhaust than to cut it.

Three decades later, in 2007, Mayor Michael Bloomberg asked Albany to toll not just the same East River bridges but also the more-trafficked 60th Street “portal” to mid-Manhattan. Predictably, faux-populist legislators saw Bloomberg’s billionaire wealth as an invitation to denounce the congestion fee as an affront to the little guy.

The mayor may have hurt his cause by presenting congestion pricing primarily as a climate and pollution measure. The pollution rationale was no longer compelling in the way it had been in Lindsay’s day, as automotive engineers had slashed rates of toxic vehicle exhaust ten-fold. Appeals tied to global warming also fell flat; remember, congestion pricing contemplated that most drivers would stay in their fossil-fuel burning cars.

This isn’t to say that congestion pricing confers no climate benefits. Rather, the benefits are subtler ones that can be hard to convey to voters, such as making climate-friendly urban living more attractive. A further benefit may come as congestion pricing demonstrates the unique power of externality pricing, as explained below.

From the Rubble

Even as Bloomberg’s toll plan was faltering in Albany, new loci of support were germinating in the city.

Changing times demanded not just the intellectual leadership of think-tanks like the Regional Plan Association and the good-government Straphangers Campaign, but gritty, grassroots transit organizing. Enter the newly-minted Riders Alliance.

2017 subway handbill exemplified new militancy targeting Gov. Andrew Cuomo for failing transit.

As subway service began cratering in 2015, the inevitable result of budget-raiding by a skein of governors, the Alliance posted crowd-sourced photos of stalled trains and jammed platforms alongside demands for improved service from “#CuomosMTA.” Before long, the papers were pointing the finger at the governor not just in “Why Your Commute Is Bad” explainers but in tear-jerkers like the Times’ May 2017 classic, “Money Out of Your Pocket”: New Yorkers Tell of Subway Delay Woes.

The drumbeat was deafening. Cuomo finally blinked. On a Sunday in August 2017, he phoned the Times’ Albany bureau chief and handed him a scoop for the next day’s front page: Cuomo Calls Manhattan Traffic Plan an Idea ‘Whose Time Has Come’.

The “traffic plan” was congestion pricing.

Data Cruncher

Two months later, Cuomo’s staff summoned me to the midtown office of the consulting firm they had retained to “scope” congestion pricing ― essentially, to compute how much revenue tolls could generate. They wanted to see if an Excel spreadsheet model I had constructed and refined over the prior decade could aid their scoping process.

The model was called the Balanced Transportation Analyzer, a name bestowed in 2007 by Ted Kheel.

Ted, in his nineties, had recruited me to determine whether a large enough congestion toll could pay to make city transit free. The idea worked on paper but foundered politically. Nevertheless, Ted saw in my Excel modeling a way to capture phenomena like “rebound effects” (motorists driving more as road space frees up) and “mode switching” between cars, trains, buses and taxicabs, that he and Prof. Vickrey had identified in their 1969 work but lacked the computing ability to quantify.

Ted’s philanthropy enabled me over the next decade to expand, test and update my transportation modeling. With a hundred “tabs” and 160,000 equations, the “BTA” can instantly answer almost any conceivable question about New York congestion pricing, as well as these two central ones: how much revenue it will yield, and how much time will travelers save in lightened traffic and better transit.3

The BTA model aced its 2017 audition and became the computational engine for the congestion pricing legislation the governor’s team enacted into law in 2019. Its impact has been even broader.4 “Having the model helped make the case with the public, journalists, elected officials and others,” Eric McClure, director of the livable-streets advocacy group StreetsPAC, wrote recently, in part by helping congestion pricing proponents push back on opponents’ exaggerated claims of disastrous outcomes and their incessant demands for special treatment. The model may also have influenced the detailed toll design adopted by the MTA board earlier this year, which hewed close to the toll design I had recommended last summer.5

The BTA also provided sustenance during congestion pricing’s seven lean years ― the 2009-2016 period in which the torch was kept lit by a new triumvirate known as “Move NY” ― traffic guru “Gridlock” Sam Schwartz, the very able campaign strategist Alex Matthiessen, and myself. The model helped our team evangelize congestion pricing’s transformative benefits to elected officials and the public. This, I believe, was a key element in mustering the critical mass of support that ultimately swayed not one but two governors.

The Hochul Factor

New York Lieutenant Governor Kathy Hochul’s ascension to governor in August 2021 could have been congestion pricing’s death knell. The toll plan was adrift in the federal bureaucracy, and its latter-day champion Andrew Cuomo had exited in “me-too” disgrace. His successor, from distant Buffalo, wasn’t beholden to New York or congestion pricing.

Hochul, who as governor controls city and regional transit, could have disowned congestion pricing as convoluted, bureaucratic and tainted. Instead, she became a resolute and enthusiastic backer. Her spirited support, both in public and behind the scenes, became the decisive ingredient in shepherding congestion pricing to safety.

Why the new governor went all-in on congestion pricing awaits a future journalist or historian. Had she spurned it, the opprobrium from downstate transit advocates would have been intense; but there doubtless would have been cries of “good riddance” as well. Vickrey, Kheel and Riders Alliance notwithstanding, it’s not clear how closely New Yorkers — including transit users — connect congestion tolls to improved travel and a better city.

What makes Hochul’s embrace especially impressive is that congestion pricing is, in a real sense, an attack on a jealously guarded entitlement: the right to inconvenience others by usurping public space for one’s vehicle. The classic lament about entitlements’ iron grip is that “losers cry louder than winners sing.”6 Yet in this case, it seems, potential losers — actual and aspiring zone-bound drivers — are being out-sung by transit interests seeking, in Kheel’s 1969 words, a better balance between public transportation and automobiles.

Credits and Prospects

Let us now praise Andrew Cuomo’s crafting of the legislation that teed up congestion pricing’s successful run.

Rather than specifying a dollar price for the tolls, or a precise traffic reduction, his 2019 bill established a revenue target: sufficient earnings to bond $15 billion in transit investment — which equates to $1 billion a year to cover debt service. This device trained the public’s focus on the gain from congestion pricing (better transit) instead of the pain (the toll). Equally important, with this deft stroke, any toll exemption that a vocal minority might seek would mathematically trigger higher tolls for everyone else. The effect was vastly heightened scrutiny of requests for carve-outs.

Which cities will follow on New York’s heels? No U.S. urban area comes close to our trifecta of gridlock, transit and wealth. Sprawling Los Angeles or Houston, or even Chicago for that matter, might be better served by more granulated traffic tolls than New York’s all-or-none model.

Perhaps Asia’s megalopolises will be swept up in our wake. In the meantime, my focus will be on the holy grail of externality pricing: taxing carbon emissions. Every economist knows that the surest and fastest way to cut down on a “bad” is by taxing it rather than subsidizing possible alternatives. Yet that approach remains counter-intuitive and even anathema to nearly everyone else.

A huge and important legacy that New York congestion pricing could provide is to prove that intelligently taxing societal harms need not be electoral suicide. This proof could help unlock a treasure-trove of prosperity-enhancing pricing reforms including, most prominently, robust carbon taxing.

The author, a policy analyst based in New York City, worked in Mayor Lindsay’s Environmental Protection Administration in 1972-1974. He met Bill Vickrey in 1991 and worked closely with Ted Kheel from 2007 to 2010.

Endnotes

- The new passenger surcharges of $1.25 for taxicabs and $2.50 for “ride-hails” (principally Ubers) apply to trips touching the congestion zone. These will be partially offset by lower fares owing to shorter wait-time charges due to faster travel speeds.

- Quote is from Moses’ August 23, 1969 guest essay in Newsday, “Is Rubber to Pay for Rails?” (not digitally available).

- The current version of the BTA is publicly available at this link: (18 MB Excel file).

- See Fix NYC Advisory Panel Report, Appendix B, 2019.

- A Congestion Toll New York Can Live With, July 2023, by Charles Komanoff, co-authored with Columbia Business School economist Gernot Wagner.

- As pronounced by University of Michigan economist Joel Slemrod, in Goodbye, My Sweet Deduction, New York Times, by Eduardo Porter and David Leonhardt, Nov. 3, 2005.

Carbon Footprint

Philippines Taps Blue Carbon and Biodiversity Credits to Protect Coasts and Climate

The Philippines is stepping up efforts to protect its coastal ecosystems. The government recently advanced its National Blue Carbon Action Partnership (NBCAP) Roadmap. This plan aims to conserve and restore mangroves, seagrass beds, and tidal marshes. It also explores biodiversity credits — a new market linked to nature conservation.

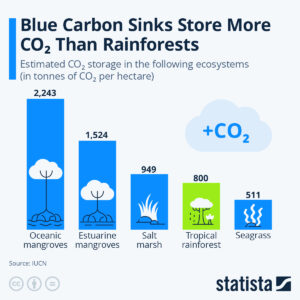

Blue carbon refers to the carbon stored in coastal and marine ecosystems. These habitats can hold large amounts of carbon in plants and soil. Mangroves, for example, store carbon at much higher rates than many land forests. Protecting them reduces greenhouse gases in the atmosphere.

Biodiversity credits are a related concept. They reward actions that protect or restore species and ecosystems. They work alongside carbon credits but focus more on ecosystem health and species diversity. Markets for biodiversity credits are being discussed globally as a complement to carbon markets.

Why the Philippines Is Targeting Blue Carbon

The Philippines is rich in coastal ecosystems. It has more than 327,000 hectares of mangroves along its shores. These areas protect coastlines from storms, support fisheries, and store carbon.

Mangroves and seagrasses also support high levels of biodiversity. Many fish, birds, and marine species depend on these habitats. Restoring these ecosystems helps conserve species and supports local food systems.

The NBCAP Roadmap was handed over to the Department of Environment and Natural Resources (DENR) during the Philippine Mangrove Conference 2026. The roadmap is a strategy to protect blue carbon ecosystems while linking them to climate goals and local livelihoods.

DENR Undersecretary, Atty. Analiza Rebuelta-Teh, remarked during the turnover:

“This Roadmap reflects the Philippines’ strong commitment to advancing blue carbon accounting and delivering tangible impact for coastal communities.”

Edwina Garchitorena, country director of ZSL Philippines, which will oversee its implementation, also commented:

“The handover of the NBCAP Roadmap to the DENR represents a turning point in advancing blue carbon action and strengthening the Philippines’ leadership in coastal conservation in the region.”

The plan highlights four main pillars:

- Science, technology, and innovation.

- Policy and governance.

- Communication and community engagement.

- Finance and sustainable livelihoods.

These pillars aim to strengthen coastal resilience, support community well‑being, and align blue carbon action with national climate commitments.

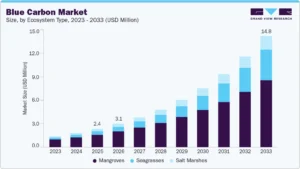

What Blue Carbon Credits Could Mean for Markets

Globally, blue carbon markets are growing. These markets allow coastal restoration projects to sell carbon credits. Projects that preserve or restore mangroves, seagrass meadows, and tidal marshes can generate credits. Buyers pay for these credits to offset emissions.

According to Grand View Research, the global blue carbon market was valued at US$2.42 million in 2025. It is projected to reach US$14.79 million by 2033, growing at a compound annual growth rate (CAGR) of almost 25%.

The Asia Pacific region led the market in 2025, with 39% of global revenue, due to its extensive coastal ecosystems and government support. Within the market, mangroves accounted for 68% of revenue, reflecting their high carbon storage capacity.

Blue carbon credits belong to the voluntary carbon market. Companies purchase these credits to offset emissions they can’t eliminate right now. Buyers are often motivated by sustainability goals and environmental, social, and corporate governance (ESG) standards.

Experts at the UN Environment Programme say these blue habitats can capture carbon 4x faster than forests:

Why Biodiversity Credits Matter: Rewarding Species, Strengthening Ecosystems

Carbon credits aim to cut greenhouse gases. In contrast, biodiversity credits focus on saving species and habitats. These credits reward projects that improve ecosystem health and may be used alongside carbon markets to attract finance for nature.

Biodiversity credits are particularly relevant in the Philippines, one of 17 megadiverse countries. The nation is home to thousands of unique plant and animal species. Supporting biodiversity through market mechanisms can strengthen conservation efforts while also supporting local communities.

Globally, biodiversity credit markets are still developing. Organizations such as the Biodiversity Credit Alliance are creating standards to ensure transparency, equity, and measurable outcomes. They want to link private investment to good environmental outcomes. They also respect the rights of local communities and indigenous peoples.

These markets complement carbon markets. They can support conservation efforts. This boosts ecosystem resilience and protects species while also capturing carbon.

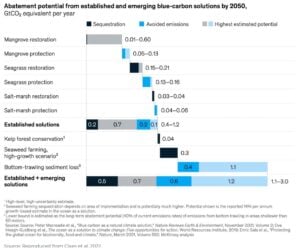

Together with blue carbon credits, they form part of a broader nature-based solution to climate change and biodiversity loss. A report by the Ecosystem Marketplace estimates the potential carbon abatement for every type of blue carbon solution by 2050.

Science, Policy, and Funding: The Roadblocks Ahead

Building blue carbon and biodiversity credit markets is not easy. There are several challenges ahead for the Philippines.

One key challenge is measurement and verification. To sell carbon or biodiversity credits, projects must prove they deliver real and measurable benefits. This requires science‑based methods and monitoring systems.

Another challenge is finance. Case studies reveal that creating a blue carbon action roadmap in the Philippines may need around US$1 million. This funding will help set up essential systems and support initial actions.

Policy frameworks are also needed. Laws and rules must support credit issuance, protect local rights, and ensure fair sharing of benefits. Coordination across government agencies, local communities, and investors will be important.

Stakeholder engagement is key. The NBCAP Roadmap and related forums involve scientists, policymakers, civil society, and private sector partners. This teamwork approach makes sure actions are based on science, inclusive, and fair in the long run.

Looking Ahead: Coastal Conservation as Climate Strategy

Blue carbon and biodiversity credits could provide multiple benefits for the Philippines. Protecting and restoring coastal habitats reduces greenhouse gases, conserves species, and supports local economies. Coastal ecosystems also provide natural defenses against storms and rising seas.

If blue carbon and biodiversity credit markets grow, they could fund coastal conservation at scale while supporting global climate targets. Biodiversity credits could further enhance ecosystem protection by linking nature’s intrinsic value to market mechanisms.

The market also involves climate finance and corporate buyers looking for quality credits. Additionally, international development partners focused on coastal resilience may join in.

For the Philippines, the next few years will be critical. Implementing the NBCAP roadmap, establishing credit systems, and strengthening governance could unlock new opportunities for climate action, sustainable development, and regional leadership in blue carbon finance.

The post Philippines Taps Blue Carbon and Biodiversity Credits to Protect Coasts and Climate appeared first on Carbon Credits.

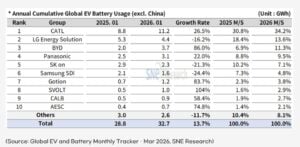

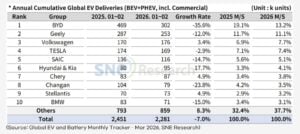

The global electric vehicle (EV) market is gaining speed again. A sharp rise in oil prices, triggered by the recent U.S.–Iran conflict in early 2026, has changed how consumers think about fuel and mobility. What looked like a slow market just months ago is now showing strong signs of recovery.

According to SNE Research’s latest report, this sudden shift in energy markets is pushing EV adoption faster than expected. Rising gasoline costs and uncertainty about future oil supply are driving buyers toward electric cars. As a result, the EV transition is no longer gradual—it is accelerating.

Oil Price Shock Changes Consumer Behavior

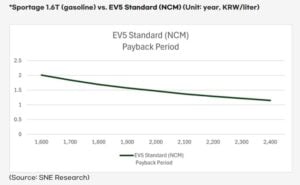

The conflict in the Middle East sent oil markets into turmoil. Gasoline prices jumped quickly, rising from around 1,600–1,700 KRW per liter to as high as 2,200 KRW. This sudden spike acted as a wake-up call for many drivers.

Consumers who once hesitated to switch to EVs are now rethinking their choices. High and unstable fuel prices have made traditional gasoline vehicles less attractive. At the same time, EVs now look more cost-effective and reliable over the long term.

SNE Research noted that even if oil prices stabilize later, the fear of future spikes will remain. This uncertainty is a key driver behind early EV adoption. People no longer want to depend on volatile fuel markets.

EV Growth Forecasts Get a Major Boost

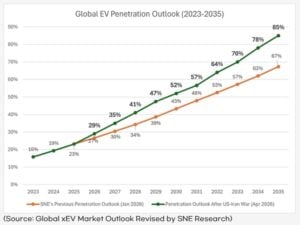

SNE Research has revised its global EV outlook. The firm now expects faster adoption across the decade.

- EV market penetration is projected to reach 29% in 2026, up from an earlier estimate of 27%.

- By 2027, the share could jump to 35%, instead of the previously expected 30%.

- Most importantly, EVs are now expected to cross 50% of new car sales by 2030, earlier than prior forecasts.

The post Global EV Sales Set to Hit 50% by 2030 Amid Oil Shock While CATL Leads Batteries appeared first on Carbon Credits.

Carbon Footprint

AI Data Centers Power Crisis: Massive Energy Demand Threatens Emissions Targets and Latest Delays Signal Market Shift

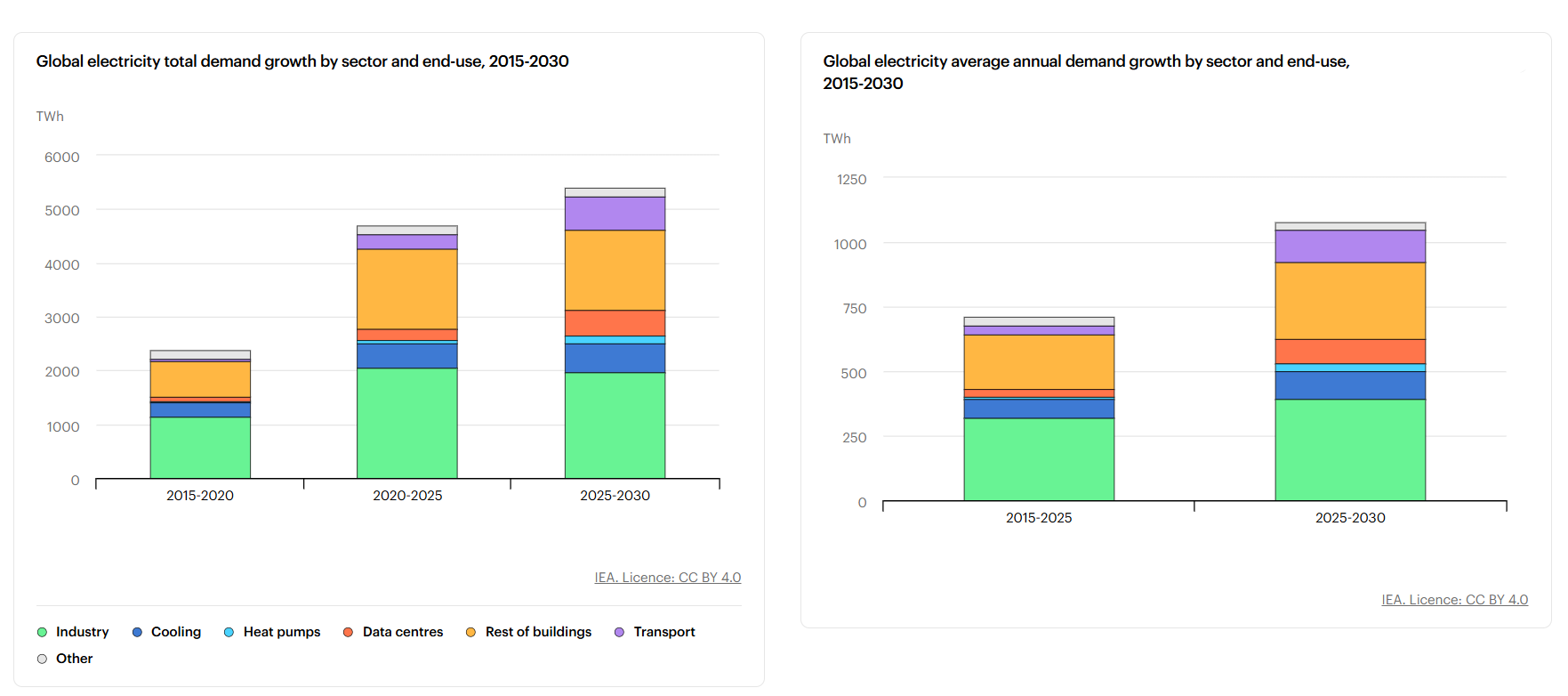

The rapid growth of artificial intelligence (AI) is creating a new challenge for global energy systems. AI data centers now require far more electricity than traditional computing facilities. This surge in demand is putting pressure on power grids and raising concerns about whether climate targets can still be met.

Large AI data centers typically need 100 to 300 megawatts (MW) of continuous power. In contrast, conventional data centers use around 10-50 MW. This makes AI facilities up to 10x more energy-intensive, depending on the scale and workload.

AI Data Centers Are Driving a Sharp Rise in Power Demand

The increase is happening quickly. The International Energy Agency estimates that global data center electricity use reached about 415 terawatt-hours (TWh) in 2024. That number could rise to more than 1,000 TWh by 2026, largely driven by AI applications such as machine learning, cloud computing, and generative models.

At that level, data centers would consume as much electricity as an entire mid-sized country like Japan.

In the United States, the impact is also growing. Data centers could account for 6% to 8% of total electricity demand by 2030, based on utility projections and grid operator estimates. AI is expected to drive most of that increase as companies continue to scale infrastructure to support new applications.

Training large AI models is especially energy-intensive. Some estimates say an advanced model can use millions of kilowatt-hours (kWh) just for training. For instance, training GPT-3 needs roughly 1.287 million kWh, and Google’s PaLM at about 3.4 million kWh. Analytical estimates suggest training newer models like GPT-4 may require between 50 million and over 100 million kWh.

That is equal to the annual electricity use of hundreds of households. When combined with ongoing usage, known as inference, total energy consumption rises even further.

This rapid growth is creating a gap between electricity demand and available supply. It is also raising questions about how the technology sector can expand while staying aligned with global climate goals.

The Grid Bottleneck: Why Data Centers Are Waiting Years for Power

Power demand from AI is rising faster than grid infrastructure can support. Utilities in key regions are now facing a surge in interconnection requests from technology companies building new data centers.

This has led to delays in several major projects. In many cases, developers must wait years before they can secure enough electricity to operate. These delays are becoming more common in established tech hubs where grid capacity is already stretched.

The main constraints include:

- Limited transmission capacity in high-demand areas,

- Slow grid upgrades and long permitting timelines, and

- Regulatory systems not designed for AI-scale demand.

Grid stability is another concern. AI data centers require constant and uninterrupted power. Even short disruptions can affect performance and reliability. This makes it more difficult for utilities to balance supply and demand, especially during peak periods.

In some regions, utilities are struggling to manage the size and concentration of new loads. A single large data center can use as much electricity as a small city. When several projects are planned in the same area, the pressure on local infrastructure increases significantly.

As a result, some companies are rethinking their expansion strategies. Projects may be delayed, scaled down, or moved to new locations where energy is more accessible. These shifts could slow the pace of AI deployment, at least in the short term.

Renewable Energy Growth Faces a Reality Check

Technology companies have made strong commitments to clean energy. Many aim to power their operations with 100% renewable electricity. This is part of their larger environmental, social, and governance (ESG) goals.

For example, Microsoft plans to become carbon negative by 2030, meaning it will remove more carbon than it emits. Google is targeting 24/7 carbon-free energy by 2030, which goes beyond annual matching to ensure clean power is used at all times. Amazon has committed to reaching net-zero carbon emissions by 2040 under its Climate Pledge.

Despite these targets, AI data centers present a difficult challenge. They need reliable electricity around the clock, while renewable energy sources such as wind and solar are not always available. Output can vary depending on weather conditions and time of day.

To maintain stable operations, many facilities rely on a mix of energy sources. This often includes grid electricity, which may still be partly generated from fossil fuels. In some cases, natural gas backup systems are used more frequently than planned.

Battery storage can help balance supply and demand. However, long-duration storage remains expensive and is not yet widely deployed at the scale needed for large AI facilities. This creates both technical and financial barriers.

Thus, there is a growing gap between corporate clean energy goals and real-world energy use. Closing that gap will require faster deployment of renewable energy, improved storage solutions, and more flexible grid systems.

Carbon Credits Use Surge as Tech Tries to Close the Emissions Gap

The mismatch between AI growth and clean energy supply is also affecting carbon markets. Many technology companies are increasing their use of carbon credits to offset emissions linked to data center operations.

According to the World Bank’s State and Trends of Carbon Pricing 2025, carbon pricing now covers over 28% of global emissions. But carbon prices vary widely—from under $10 per ton in some systems to over $100 per ton in stricter markets. This gap is pushing companies toward voluntary carbon markets.

The Ecosystem Marketplace report shows rising demand for high-quality credits, especially carbon removal rather than avoidance credits. But supply is still limited.

Costs are especially high for engineered removals. The IEA estimates that direct air capture (DAC) costs today range from about $600 to over $1,000 per ton of CO₂. It may fall to $100–$300 per ton in the future, but supply is still very small.

Companies are focusing on credits that:

- Deliver verified emissions reductions,

- Support long-term carbon removal, and

- Align with ESG and net-zero commitments.

At the same time, many firms are taking a more active role in energy development. Instead of relying only on offsets, they are investing directly in renewable energy projects. This includes funding new solar and wind farms, as well as entering long-term power purchase agreements.

These investments help secure a dedicated clean energy supply. They also reduce long-term exposure to carbon markets, which can be volatile and subject to changing standards.

Companies Are Adapting Their Energy Strategies: The New AI Energy Playbook

AI companies are changing how they design and operate data centers to manage rising energy demand. Here are some of the key strategies:

- Energy efficiency improvements (new hardware and cooling systems) that reduce data center power use.

- More efficient AI chips, specialized processors, that drive performance gains.

- Advanced cooling systems that cut energy waste and can help cut total power use per workload by 20% to 40%.

- Data center location strategy is shifting, where facilities are built in regions with stronger renewable energy access.

- Infrastructure is becoming more distributed, where firms deploy smaller data centers across multiple locations to balance demand and improve resilience.

- Long-term renewable energy contracts are expanding, which helps companies secure power at stable prices.

A Turning Point for Energy and Climate Goals

The rise of AI is creating both risks and opportunities for the global energy transition. In the short term, increased electricity demand could lead to higher emissions if fossil fuels are used to fill supply gaps.

At the same time, AI is driving major investment in clean energy and infrastructure. The long-term outcome will depend on how quickly clean energy systems can scale.

If renewable supply, storage, and grid capacity keep pace with AI growth, the technology sector could help accelerate the shift to a low-carbon economy. If progress is too slow, however, AI could become a major new source of emissions.

Either way, AI is now a central force shaping global energy demand, infrastructure investment, and the future of carbon markets.

The post AI Data Centers Power Crisis: Massive Energy Demand Threatens Emissions Targets and Latest Delays Signal Market Shift appeared first on Carbon Credits.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits