The UK’s greenhouse gas emissions fell by 2.4% in 2025 to their lowest level in more than 150 years, according to new Carbon Brief analysis.

The biggest factors were gas use falling to a 34-year low and coal use dropping to levels last seen in 1600, when Queen Elizabeth I was on the throne and William Shakespeare was writing Hamlet.

These shifts were helped by record-high UK temperatures, elevated gas prices, the end of coal power in late 2024 and a sharp slowdown in the steel industry.

Other key findings of the analysis include:

- The UK’s greenhouse gas emissions fell to 364m tonnes of carbon dioxide equivalent (MtCO2e) in 2025, the lowest level since 1872.

- Coal use roughly halved, with more than half of this due to the end of coal power and another third due to closures and other issues in the steel industry.

- Gas use fell by 1.5% to the lowest level since 1992, with roughly equal contributions from cuts in heat for buildings and industry, more than offsetting a small rise in gas power.

- Oil use fell by 0.9%, despite rising traffic, helped by more than 700,000 new electric vehicles (EVs), electric vans and plug-in hybrids on the nation’s roads.

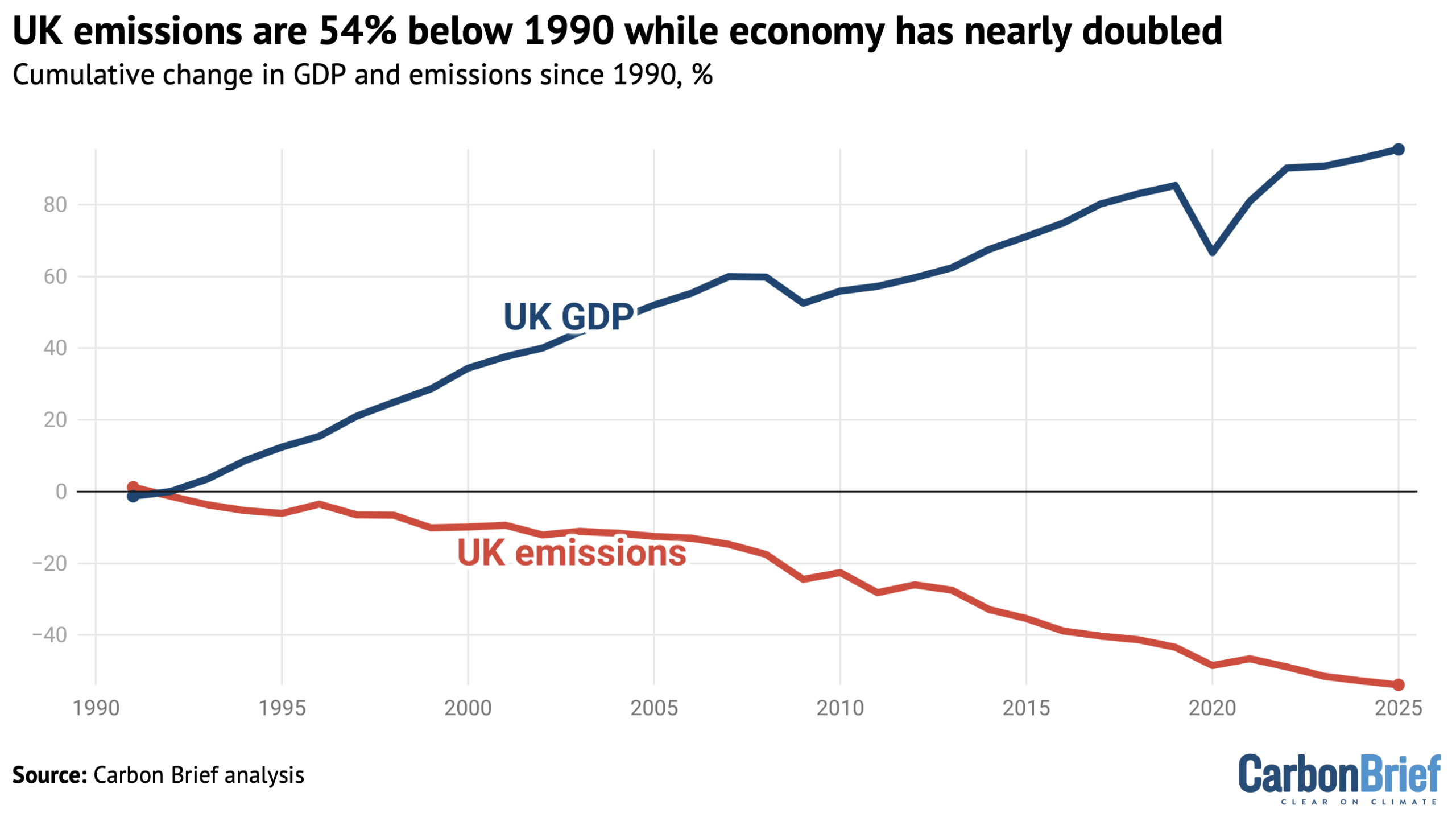

- The UK’s emissions are now 54% below 1990 levels, while its GDP has nearly doubled.

The 2.4% (8.9MtCO2e) fall in emissions in 2025 was only slightly more than half of the 15MtCO2e cut needed each year on average until 2050, to reach the UK’s legally binding net-zero target.

The analysis is the latest in a decade-long series of annual estimates from Carbon Brief, covering emissions during 2024, 2023, 2022, 2020, 2019, 2018, 2017, 2016, 2015 and 2014.

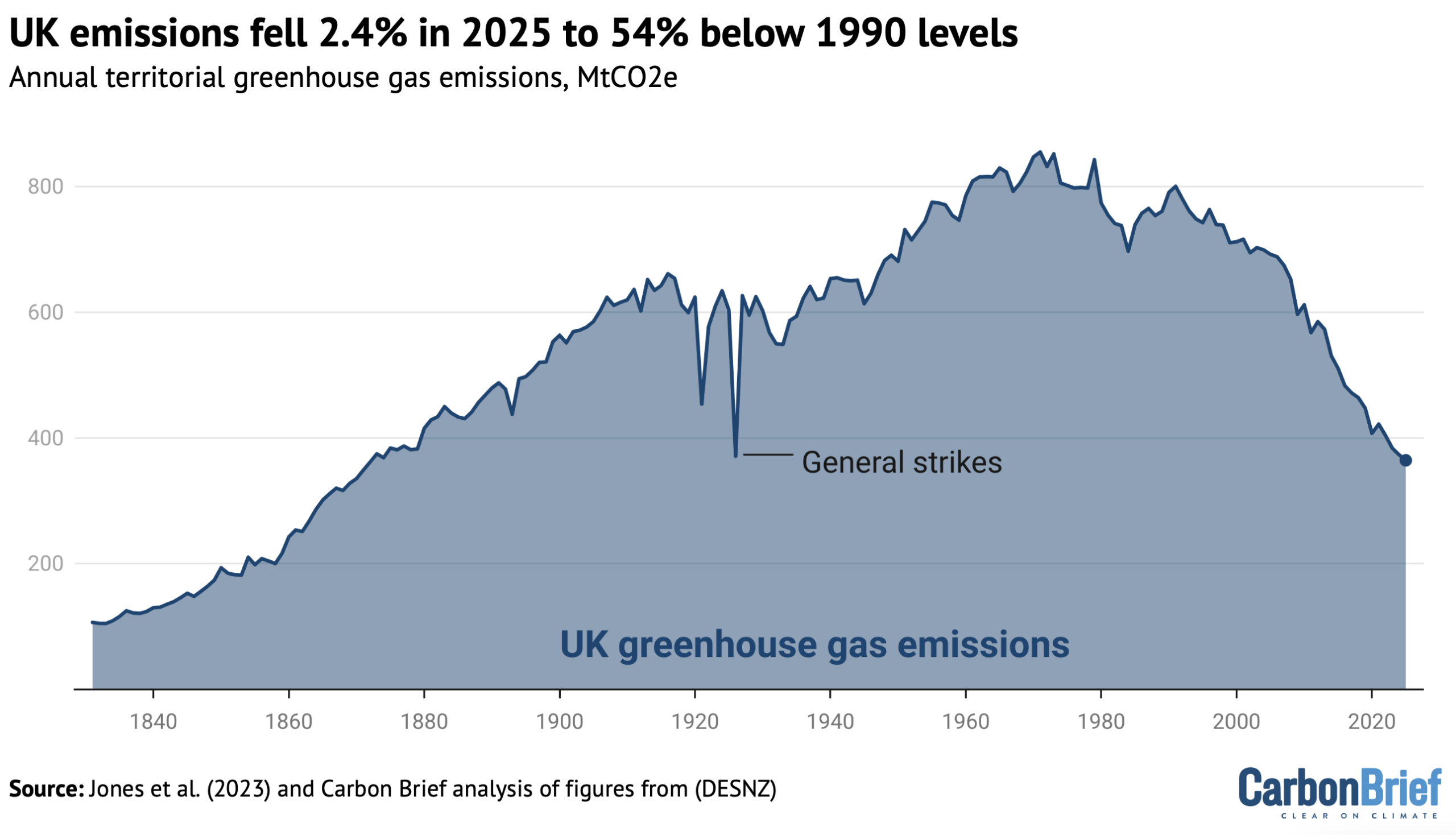

Emissions fall to 150-year low

The UK’s territorial greenhouse gas emissions – those that occur within the country’s borders – have now fallen in 27 of the 36 years since 1990.

(The recent fall in territorial emissions has not been “offset” by a rise in the amount of CO2 embedded in imports, which has stayed relatively constant since around 2008.)

Apart from brief rebounds after the global financial crisis and the Covid-19 lockdowns, UK emissions have fallen every year for the past two decades.

The latest 9MtCO2e (2.4%) reduction takes UK emissions down to 364MtCO2e, according to Carbon Brief’s analysis, which is 54% below 1990 levels.

This is the lowest since 1872, as shown in the figure below.

The latest fall puts UK emissions below the level seen during the 1926 general strike, when the nation’s industrial base was brought to a standstill.

It means that UK emissions are now at sustained lows not seen since Victorian times.

Nevertheless, emissions will need to continue falling in order to meet the UK’s legal climate goals and its net-zero target, which is part of international efforts under the Paris Agreement to stop dangerous warming.

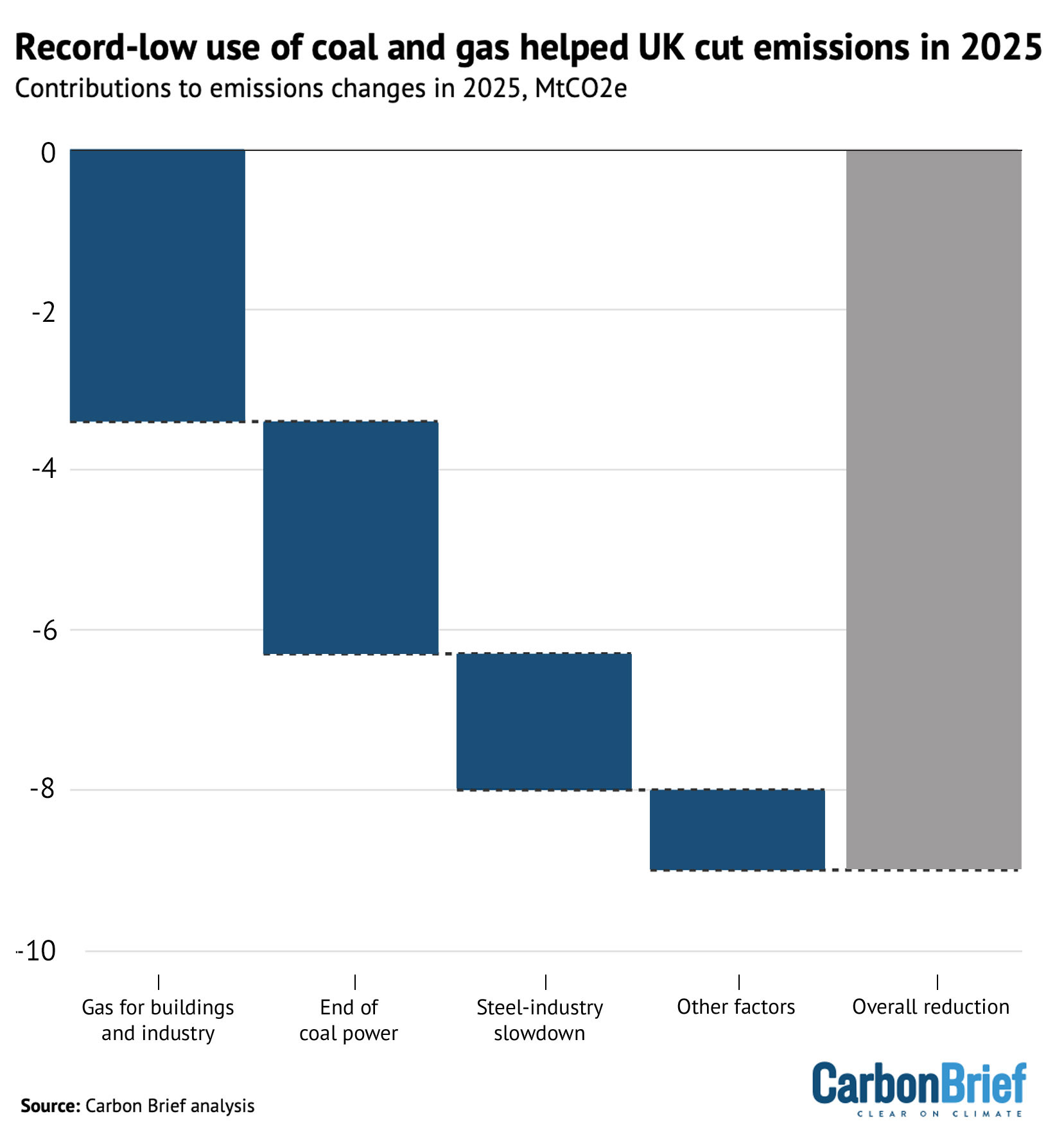

Record lows for coal and gas

The key factors in driving down UK emissions in 2025 were coal and gas use falling to their lowest levels since 1600 and 1992, respectively.

For gas, this was mainly down to lower demand from building heat and from industry, likely at least partly related to record-high temperatures and elevated gas prices. For coal, this was a combination of the end of coal power and a steel-industry slowdown, as shown below.

These were not the only factors driving the change in UK emissions in 2025.

The UK saw record generation from renewable sources, particularly wind and solar, but a further decline in nuclear generation, the end of coal power and an increase in electricity demand for the second year running meant that gas-fired power output also went up slightly.

In the transport sector, demand for oil fell by 0.9% year-on-year, even though traffic levels went up by around 1%, according to provisional figures through to September 2025.

This partly reflects the changing makeup of vehicles on the road.

By 2024, there were 2.8m fewer diesel vehicles than there were in 2019, a trend likely to continue due to falling diesel car sales. In contrast, there are now nearly 3m EVs, plug-in hybrids or electric vans on the nation’s roads, making up 5% of the car fleet overall and 2% of vans.

These electrified vehicles are cutting UK emissions by more than 7MtCO2 every year, according to Carbon Brief analysis, with the 700,000 new EVs in 2025 alone saving nearly 2MtCO2.

Drivers with EVs saved a total of £2m in lower fuel costs in 2025, the analysis shows, as EVs are much more efficient and, therefore, cheaper to run than petrol or diesel vehicles. This amounts to more than £700 per EV per year and more than £1,100 for each electric van.

Despite falling demand for oil-derived fuels and the impact of the growing EV fleet, Carbon Brief estimates that the UK’s oil-related emissions actually increased by 0.2% in 2025. This is largely down to a shift in the amount and type of biofuel blended into diesel and petrol at the pump.

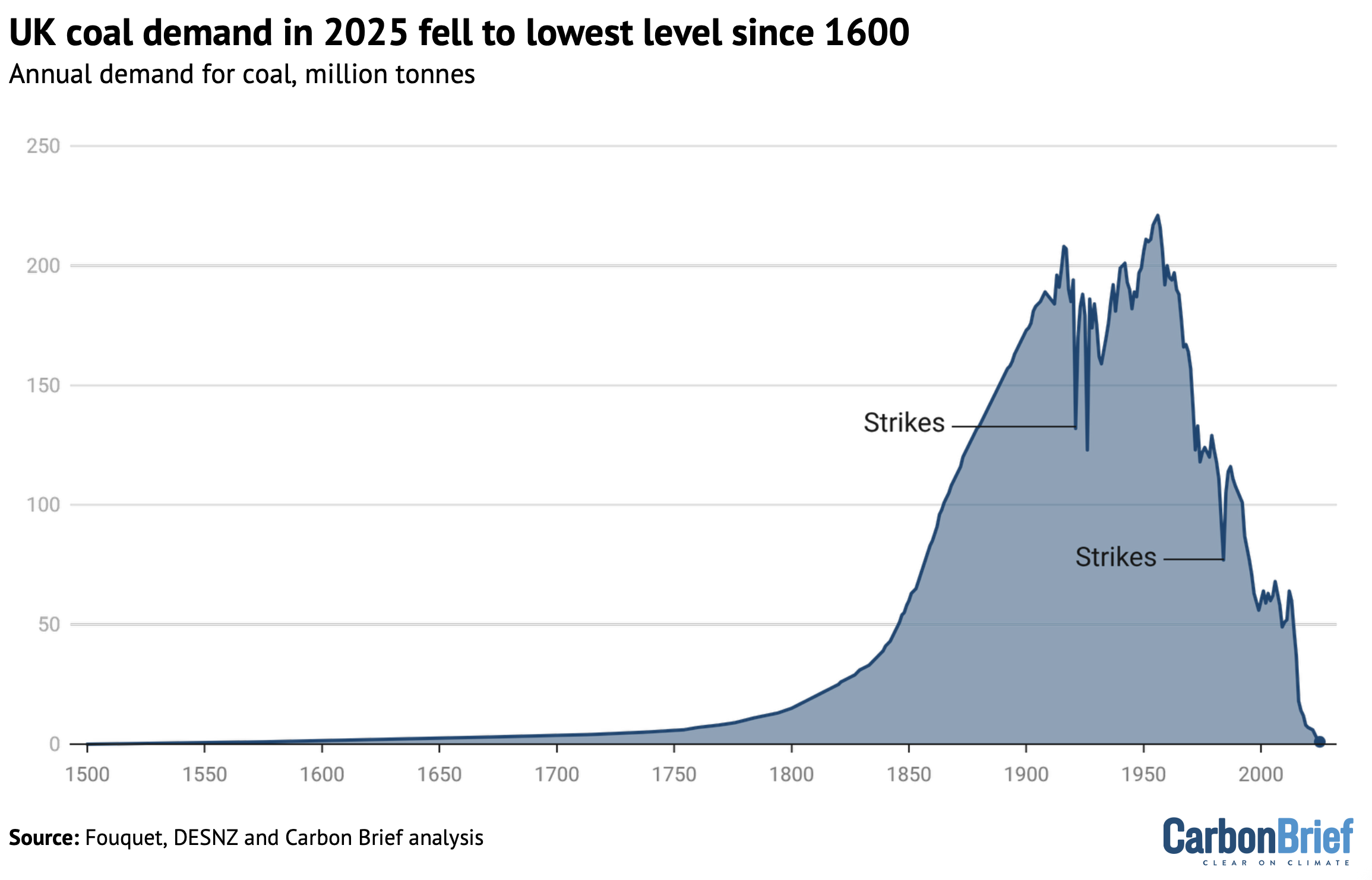

Coal falls to lowest level in 400 years

There have been dramatic declines in UK coal use over the past decade, in particular resulting from the phaseout of coal-fired electricity generation.

UK coal demand fell by another 56% in 2025 to just under 1m tonnes (Mt). This is down 97% from the 37Mt burned in 2015 and is 99.6% below the peak of 221Mt in 1956.

As shown in the figure below, coal demand is now at the lowest level since 1600, when Elizabeth I was the queen of England and Ireland.

(It was during her five-decade reign that coal had become the country’s main source of fuel, following an Elizabethan “energy crisis” triggered by a lack of wood for making charcoal.)

The UK’s last coal-fired power plant, at Ratcliffe-on-Soar in Nottinghamshire, closed down on 30 September 2024. It had run at low levels that year, but still burned some 0.7m tonnes of coal. The end of coal power contributed nearly three-fifths of the fall in demand for the fuel in 2025.

There has also been a marked reduction in UK steel production in recent years, particularly since the closure of two of the nation’s last blast furnaces at Port Talbot in south Wales in 2024.

The last blast furnaces in the country are at the British Steel plant in Scunthorpe in Lincolnshire, which had been due for closure in early 2025 until the government stepped in to keep it open.

The slowdown in coal-based steel production accounts for around a third of the decline in UK coal use in 2025, but only 14% of the drop in the past decade, which was mainly due to coal power.

Globally, the steel industry is facing intense competition in an oversupplied market, with a growing “glut” that has driven down prices. At the same time, the industry in the UK has ageing equipment and expensive electricity, which UK Steel says is largely a result of high gas prices.

The Port Talbot site is being converted to “electric arc furnace” (EAF) steelmaking, which does not rely on coal. The same shift is under discussion for the Scunthorpe site. Analysis from thinktank Green Alliance suggests EAFs would be the cheapest option for both sites.

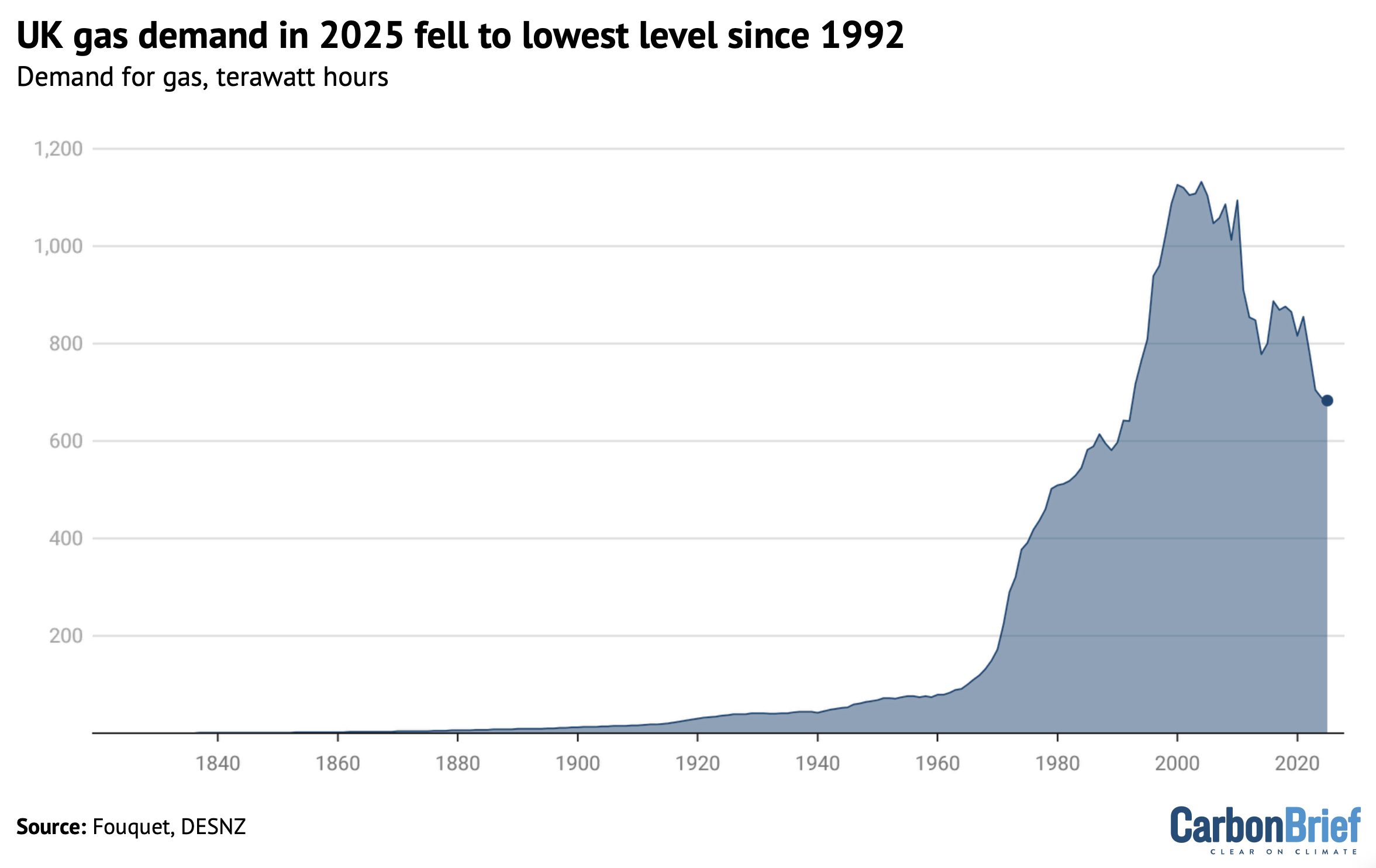

Gas falls to lowest level in 34 years

There have also been dramatic declines in UK demand for gas over the past 15 years. After another 1.5% drop in 2025, gas use is now at the lowest level since 1992, as shown below.

This means gas demand is now similar to when the UK began its “dash for gas” in the early 1990s. Starting in 1991, this period saw a wave of new gas-fired power stations being built. It was triggered by a change in regulations to allow the use of gas to generate electricity, advances in turbine technology, a period of low gas prices and the privatisation of the UK electricity system.

In total, UK gas demand has fallen by nearly two-fifths since 2010. Half of this overall reduction is due to a 50% fall in gas-fired electricity generation, which has been displaced by falling demand and renewable sources. Another third of the overall reduction is from home heating, where demand has dropped due to more efficient gas boilers and improved insulation.

In 2025, the 1.5% reduction in gas use was caused by roughly equal contributions from lower demand for building heat and from industrial users.

This was helped by 2025 being the hottest year on record, with high gas prices likely also a factor.

Gas prices have remained significantly above the levels seen before Russia’s invasion of Ukraine in 2022. At the start of March 2026, UK gas prices roughly doubled as a result of the conflict in the Middle East triggered by the US and Israeli attacks on Iran.

Whereas the UK’s fleet of EVs is already having a significant impact on emissions, domestic heat pump sales remain at relatively low levels, particularly compared with other European nations.

After a 25% year-on-year increase in 2025, there were still only 125,000 heat pump sales in the UK. These new installations will have cut UK emissions by around 0.2MtCO2 in 2025 relative to gas heating, shows Carbon Brief analysis.

By the end of 2025, the UK had a total of around 450,000 domestic heat pumps, generating total savings of roughly 0.7MtCO2 after accounting for the increase in electricity demand.

The 2.3m domestic heat pumps expected by 2030 in the National Energy System Operator’s “future energy scenarios” would save the UK around 4.5MtCO2 per year.

Emissions continue to decouple from growth

In total, UK greenhouse gas emissions in 2025 fell to 54% below 1990 levels, the baseline year for its legally binding climate goals.

Since then, the UK economy has nearly doubled in size, with GDP growing by 95% according to data from the World Bank, as shown in the figure below.

Transport remains the single-largest sector, accounting for around 30% of UK emissions, followed, in order, by buildings, agriculture, industry and electricity generation.

The majority of emissions cuts over recent decades have come in the power sector – formerly, the UK’s largest emitter – as coal has been phased out and renewables have replaced gas.

This is set to change over the next 10-15 years. The rise of EVs is set to make transport the largest source of emissions cuts from now until 2040, according to the Climate Change Committee.

While industrial emissions have also declined significantly since 1990, falling some 74% by 2025, the size of UK manufacturing output has also roughly doubled.

Despite the progress in cutting emissions to date, the UK has a long way to go if it is to meet its climate goals in the future, including the yet-to-be legislated seventh “carbon budget”, covering the years 2038-2042, as well as the 2050 net-zero target.

Emissions would need to fall by 15MtCO2e each year until 2050 on average, in order to meet the net-zero target. Meeting the UK’s 2035 international pledge under the Paris Agreement, a 78% reduction below 1990 levels, emissions would need to fall by 22MtCO2e per year.

These figures can be compared with the 9MtCO2e cut achieved in 2025. Emissions did, in fact, fall by an average of 15MtCO2e per year over the past decade – and by an average of 13MtCO2e per year since the turn of the century.

Methodology

The starting point for Carbon Brief’s analysis of UK greenhouse gas emissions is preliminary government estimates of energy use by fuel. These are published monthly, with the final month of each year appearing in figures published at the end of the following February. The same approach has accurately estimated year-to-year changes in emissions in previous years (see table, below).

Annual change in UK greenhouse gas emissions, %

| Year | Official figures | Carbon Brief | Difference |

|---|---|---|---|

| 2010 | 2.5 | 2.7 | 0.1 |

| 2011 | -7.2 | -7.7 | -0.4 |

| 2012 | 3.1 | 3.6 | 0.6 |

| 2013 | -2.1 | -4.1 | -2.0 |

| 2014 | -7.4 | -7.5 | -0.1 |

| 2015 | -3.8 | -3.7 | 0.0 |

| 2016 | -5.4 | -5.7 | -0.3 |

| 2017 | -2.4 | -2.0 | 0.4 |

| 2018 | -1.6 | -1.7 | -0.1 |

| 2019 | -3.6 | -3.9 | -0.3 |

| 2020 | -8.9 | -8.8 | 0.1 |

| 2021 | 3.6 | 3.5 | -0.1 |

| 2022 | -4.3 | -3.6 | 0.7 |

| 2023 | -5.0 | -5.2 | -0.2 |

| 2024 | -2.7 | -3.0 | -0.3 |

| 2025 | -2.4 |

One large source of uncertainty is the provisional energy use data, which is revised at the end of March each year and often again later on.

Emissions data is also subject to revision in light of improvements in data collection and the methodology used, with major revisions in 2021 and more minor changes in early 2026.

The latest changes to the DESNZ emissions methodology have led to 2% reduction in baseline 1990 emissions, but the impact on recent years is minimal.

This does not affect the UK’s carbon budgets, which are set in terms of tonnes of emissions over a five-year period, rather than a percentage reduction compared with 1990 levels.

The table above applies Carbon Brief’s emissions calculations to the comparable energy use and emissions figures, which may differ from those published previously.

Another source of uncertainty is the fact that Carbon Brief’s approach to estimating the annual change in emissions differs from the methodology used for the government’s own provisional estimates. The government has access to more granular data not available for public use.

Carbon Brief’s analysis takes figures on the amount of energy sourced from coal, oil and gas reported in Energy Trends 1.2. These figures are combined with conversion factors for the CO2 emissions per unit of energy, published annually by the UK government. Conversion factors are available for each fuel type, for example, petrol, diesel, gas and coal for electricity generation.

For oil, the analysis also draws on Energy Trends 3.13, which further breaks down demand according to the subtype of oil, for example, petrol, jet fuel and so on. Similarly, for coal, the analysis draws on Energy Trends 2.6, which breaks down solid fuel use by subtype.

Emissions from each fuel are then estimated from the energy use multiplied by the conversion factor, weighted by the relative proportions for each fuel subtype.

For example, the UK uses roughly 50m tonnes of oil equivalent (Mtoe) in the form of oil products, around half of which is from road diesel. So half the total energy use from oil is combined with the conversion factor for road diesel, another one-fifth for petrol and so on.

Energy use from each fossil fuel subtype is mapped onto the appropriate emissions conversion factor. In some cases, there is no direct read-across, in which case the nearest appropriate substitute is used. For example, energy use listed as “bitumen” is mapped to “processed fuel oils – residual oil”. Similarly, solid fuel used by “other conversion industries” is mapped to “petroleum coke” and “other” solid fuel use is mapped to “coal (domestic)”.

The energy use figures are calculated on an inland consumption basis, meaning they include bunkers consumed in the UK for international transport by air and sea. In contrast, national emissions inventories exclude international aviation and shipping.

The analysis, therefore, estimates and removes the part of oil use that is due to the UK’s share of international aviation. It draws on the UK’s final greenhouse gas emissions inventory, which breaks emissions down by sector and reports the total for domestic aviation.

This domestic emissions figure is compared with the estimated emissions due to jet fuel use overall, based on the appropriate conversion factor. The analysis assumes that domestic aviation’s share of emissions is equivalent to its share of jet fuel energy use.

In addition to estimating CO2 emissions from fossil fuel use, Carbon Brief assumes that CO2 emissions from non-fuel sources, such as land-use change and forestry, are the same as a year earlier. The remaining greenhouse gas emissions are assumed to change in line with the latest government energy and emissions projections.

These assumptions are based on the UK government’s own methodology for preliminary greenhouse gas emissions estimates, published in 2019.

Note that the figures in this article are for emissions within the UK measured according to international guidelines. This means they exclude emissions associated with imported goods, including imported biomass, as well as the UK’s share of international aviation and shipping.

The Office for National Statistics (ONS) has published detailed comparisons between various approaches to calculating UK emissions, on a territorial, consumption, “environmental accounts” or “international accounting” basis.

The UK’s consumption-based CO2 emissions increased between 1990 and 2007. Since then, however, they have fallen by a similar number of tonnes as emissions within the UK.

Bioenergy is a significant source of renewable energy in the UK and its climate benefits are disputed. Contrary to public perception, however, only around one-quarter of bioenergy is imported.

International aviation is considered part of the UK’s carbon budgets and faces the prospect of tighter limits on its CO2 emissions. The international shipping sector has a target to at least halve its emissions by 2050, relative to 2008 levels.

The post Analysis: UK emissions fall 2.4% in 2025 as coal hits 400-year low appeared first on Carbon Brief.

Analysis: UK emissions fall 2.4% in 2025 as coal hits 400-year low

Tucked among forested slopes and pristine valleys in a corner of northeastern India, young villagers have been busy knocking on doors – hoping to convince sceptical elders that graphite mining would bring much-needed jobs to their distant region.

“The youth in our village migrate to cities for work. What’s better than to have jobs near home?” Gollo Doni, a farmer and secretary of the local youth association, told Climate Home News as he and other members in their 20s discussed the latest meetings between locals and representatives of Oil India Limited (OIL), a state company exploring graphite and vanadium reserves in Arunachal Pradesh.

The mining plans in the state, which is home to more than one-third of India’s graphite reserves and the subject of a sovereignty dispute with China, reflect a push by the Indian government to position itself as a leading producer of battery-grade graphite as the mass rollout of batteries for electric vehicles (EVs) and power storage drives demand for the mineral.

-

Warning against ‘consumer club’ as G7 forms critical minerals alliance

G7 countries want to reduce their reliance on China for minerals and protect supplies from geopolitical interests but experts see few benefits for developing nations -

Brazil jostles for rare earths share as US-China rivalry heats up

With the world’s second-largest reserves of rare earths after China, Brazil is catching the eye of US and Chinese companies – spurring the government’s critical minerals policy push -

After another battery startup bankruptcy, can Europe ever cut reliance on China?

Norway’s Morrow Batteries set out to challenge Chinese producers, but a cash crunch forced it to file for bankruptcy in a setback for European ambitions for clean energy sovereignty

An average electric car contains about 60 kg of graphite anode materials, according to the International Energy Agency, and the graphite supply chain is heavily dominated by China, which produces about 80% of the world’s natural graphite and controls more than 90% of global refining.

As Western countries seek to reduce their dependency on China, India’s reserves of graphite and other minerals vital for the switch to clean energy have caught governments’ attention, with Germany signing a critical minerals partnership agreement in January.

Ambitious plans

But hurdles remain to India’s ambitious plans to ramp up critical minerals output, both to position itself as an alternative to China and to meet its own fast-growing needs.

India has a target for 30% of new vehicle sales to be electric by 2030, and demand for EV lithium batteries looks set to surge close to 35-fold between 2023 and 2035, according to S&P Global Mobility, driven by growth in two- and three-wheelers in the country of 1.4 billion people.

Although domestic manufacturing of EV batteries is expanding, the sector remains at an early stage and India depends heavily on imports from China, South Korea and Japan.

At the same time, it wants to get graphite processing off the ground, aiming to turn its reserves of the mineral – which rank among the world’s 10 biggest – into higher value battery-grade supplies.

The energy transition has a rare earth problem: These startups are solving it

With exploration already underway, the next step should be starting discussions about developing processing facilities – including support from foreign partners, said Kaira Rakheja, South Asia energy analyst at the Institute for Energy Economics and Financial Analysis (IEEFA).

“These exploration and extraction projects have a long gestation period. So even if discussions on processing start now, it will still take a while,” she said, noting India’s simultaneous push to create “rare earth corridors” encompassing every step of production.

Hurdles ahead

India’s graphite reserves are mainly of a lower grade, however, making processing for use in battery anodes more complex, while the country is a late entrant.

“We are not a big player in the market and have missed the bus,” said Aditya Ramji, director of the Global South Clean Transportation Centre at the University of California, Davis.

While exploration work is already underway at several sites in Arunachal Pradesh, and at some places in eastern and southern India, production will take at least two years to start, said Tana Tage, director at the Centre for the Earth Sciences and Himalayan Studies, OIL’s local partner and holder of a 10% stake in the Phop project.

A mine would create about 300 jobs and the project’s partners are discussing options for processing the site’s medium- to high-grade graphite locally, Tage added, despite voicing concern about a lack of technological know-how.

“India does not have the large-scale, advanced processing capabilities to achieve the ultra-high purity levels required for EV batteries and clean technologies,” he told Climate Home News.

Diversification drive

Despite such challenges, industry experts say India could benefit from the push to find sources of battery graphite other than China.

“We can’t beat China in this space, but we can still create a space for ourselves in buying and selling, as everyone is looking for a space to diversify,” said Rishabh Jain, fellow at the Council on Energy, Environment and Water, a New Delhi-based think-tank.

India’s government hopes the bilateral memorandum of understanding (MoU) signed with Germany could help.

As well as pledging cooperation on critical minerals exploration, the declaration envisions the exchange of know-how to add value through processing and recycling, facilitating investment and building the supply chain resilience of both countries. That could include identifying joint research projects and facilitating cooperation between industry players.

-

The scramble to stockpile critical minerals could drive up energy transition costs

Researchers warn that uncoordinated stockpiling could push up prices of minerals needed for clean energy technologies and delay their roll out -

Chinese EV brands woo Yemen’s wealthy elite as war prompts solar boom

For the well-off few, buying an EV is the next step in a solar revolution that has helped Yemenis weather years of power outages and high fuel prices -

Recycling could meet half of Europe’s critical mineral needs by 2050

A new report by an EU-funded research project says the bloc could harness its “urban mines” to reduce its dependence on China for energy transition minerals

“India and Germany will work together to mutually strengthen supply chains in the field of critical minerals,” a spokesperson for the German government’s energy strategy said. “We will encourage companies to build strong ties in terms of knowledge sharing, offtake agreements and investments.”

Germany is already supporting several domestic projects focused on converting graphite into battery anode material – valuable experience that could potentially be shared with India, said Rakheja. In return for shared technical expertise, India offers a strong pool of workforce talent and a big market.

“This way, both partners can look beyond China,” she said.

India sets achievable green electricity and emissions intensity targets

The MoU, which is non-binding, is “a good start”, said Svenja Schöneich, a senior advisor at the NGO Germanwatch, adding that it was thin on details, including on how to add value to India’s critical mineral resources.

“The partnership document should figure out the problem of local value creation. It should also consider that it can’t really skip processing through China,” Schöneich said.

An official at India’s Mining Ministry did not respond to requests for comment.

Trade deals and tax breaks

Beyond the five-year German accord, India has implemented numerous policy measures aimed at securing its own supplies of critical minerals and adding value to its mineral exports, for example by signing favourable trade deals. Last year, India’s graphite was granted zero-duty access to the US, just as the tariffs on Chinese graphite imports climbed to a high 160%.

When the government announced the national budget in February, it included a raft of financial measures aimed at kickstarting a plan to process minerals domestically – the details of which are expected to be announced in the coming months.

They included zero customs duty on critical mineral inputs and enhanced tax deductions for exploration, while the government’s production-linked incentive (PLI) scheme allocated the equivalent of $1.87 billion to build domestic battery cell manufacturing.

Before that can happen, progress on new mining – such as the Arunachal Pradesh graphite projects – is vital, Jain said.

“We are in 2026, and looking to move towards a cleaner world. This is the future,” he said.

The state government in Arunachal Pradesh agrees. It called last year for fast-tracked environmental permitting for graphite projects, new infrastructure around mine sites and reforms to avoid legal disputes that could hold the sector back.

Back in the village of Phop, youth association secretary Doni said that while reluctant residents did not raise an objection to OIL’s preliminary exploration licence, he fears a bigger fight ahead.

Tage said up to 3,000 people could ultimately be displaced if the project proceeds, raising questions about whether economic benefits would outweigh the social and environmental costs.

“It has been difficult to make the elders agree to actual mining,” Doni said, as he and other young villagers sipped on sweet tea in a thatched mountain house. “We are trying to convince our elders that mining will not only bring resources for the nation, but bring us jobs here.”

The post India looks to untapped graphite riches for slice of critical minerals boom appeared first on Climate Home News.

India looks to untapped graphite riches for slice of critical minerals boom

Wamuyu Manyara is country director for Trócaire Malawi and Tarcizio Kalaundi is its climate resilience officer.

This week, the Fund for responding to Loss and Damage (FRLD) faces a significant decision that will determine its ability to address the harms being done by climate change.

Discussions on the Fund’s Resource Mobilisation Strategy must get the scale and accessibility of the Fund right. Failure to do so would risk undermining its role to channel finance to countries experiencing loss and damage, and undermine obligations to climate justice and human rights.

This discussion could not come at a more pressing time. As loss and damage (L&D) continues to escalate globally, and as the world teeters perilously close to the Paris Agreement’s critical 1.5C warming limit, the FRLD also faces the very real danger of running out of funding in 2027.

As Nigeria rails at loss and damage “mirage”, fund boss assures money is coming

Experts calculate that in 2025, L&D finance needs for climate-vulnerable countries may have reached USD$937 billion. Last year’s major impacts included a series of extremely destructive cyclones that hit the Philippines, estimated to have caused over $5 billion in losses, while in Jamaica, the losses and damage caused by Hurricane Melissa were estimated at $12.2 billion.

The bill for just one of these disasters would exhaust the Fund’s existing resources many times over. While the costs and human rights violations rack up, almost four years after being agreed at COP27, the FRLD remains critically underfunded.

Pledges to the Fund ($822 million) are just a fraction of 1% of annual loss and damage needs, and only around half of those pledges ($448 million) have been paid into the Fund so far.

Meanwhile, those who have done nothing to cause the climate crisis are facing its worst – and intensifying – impacts and are being left to foot the bill for the damages already incurred, not to mention the severe non-economic costs to communities. It is therefore crucial that the FRLD’s Resource Mobilisation Strategy urgently brings in far more L&D finance.

Contributor conundrum

Many developed states will claim that additional countries should provide L&D finance. This, however, is a distraction – particularly considering the deep abyss between the contributions of developed states that are obligated to pay and their fair share as calculated according to their wealth and historical emissions. Furthermore, some states and regions that are currently not obligated to contribute are already doing so.

Analysis reveals that, even in the highly inequitable scenario where all states including those who have contributed nothing to causing the climate crisis were to pay towards L&D finance, wealthy countries would still be responsible for the vast majority of L&D finance.

The Fund’s Resource Mobilisation Strategy must focus political discussions on the ability of rich and highly polluting states to raise public, grant-based L&D finance that is new and additional to existing climate finance obligations and overseas development assistance.

Developed states have the means to pay and the FRLD should introduce mandatory and progressive mechanisms to make the biggest polluters, including the ultra-rich and fossil fuel corporations, pay for their climate harms.

African impacts

Increasingly unpredictable seasons and more frequent and extreme events are driving food insecurity, malnutrition, displacement and other human rights risks in climate-vulnerable countries, and communities facing these escalating and compounding impacts must be centred in FRLD policies.

In Ethiopia, 2023 saw 24 million people affected by five back-to-back failed rains leading to severe food and water shortages, including a 90% crop loss in drought-affected areas. Eleven million people required food assistance, and over 500,000 people were displaced. Meanwhile, the 2023–24 floods and the 2024 Gofa landslide disrupted or destroyed health facilities, displaced thousands, and led to outbreaks of cholera, malaria, and measles.

Comment: Let’s tax luxury air travel to fund climate adaptation and loss and damage

Today, Somalia is facing one of its most severe drought emergencies in recent history driven by climate extremes. Malnutrition rates continue to exceed projections and previous devastating records, with 1.9 million children in Somalia acutely malnourished.

In Malawi, child stunting had significantly reduced, but climate impacts are now affecting children’s growth and development. Tropical Cyclone Freddy in 2023 was one of the worst on record, causing over 1,200 deaths, displacing half a million people, and causing damages exceeding $500 million. Recovery needs for four major disasters between 2015 and 2023 are estimated at $1.7 billion, equivalent to more than a quarter of Malawi’s 2026-2027 budget.

Funding for communities

Access to community grants in the southern African country, however, has catalysed local responses to L&D that coordinate around immediate and long-term needs and restoring livelihoods.

Direct access to the FRLD for climate-vulnerable countries and communities, with community-centric planning, is essential to ensure that the Fund can respond to the needs of people experiencing the worst impacts of climate change, through prompt and flexible mechanisms that do not hinder recovery options.

Stepping up to fill the FRLD through an ambitious and needs-based Resource Mobilisation Strategy is the bare minimum that wealthy states can and must do. It is, after all, an obligation that flows from the international duties of cooperation and prevention of harm, and from the obligation to provide reparation when harm occurs. Failure to do so would further erode climate justice and human rights for communities on the frontline of loss and damage.

The post The loss and damage fund needs far more finance to deliver climate justice appeared first on Climate Home News.

The loss and damage fund needs far more finance to deliver climate justice

Climate Change

Woodside “SLAPP suit” against climate campaigners an attempt to silence growing opposition to drilling at Scott Reef

SYDNEY, Thursday 9 July 2026 — Greenpeace Australia Pacific has condemned Woodside’s legal pursuit of concerned community members for their 2023 climate protest, calling it an attempt to silence and intimidate growing opposition to plans to drill for oil and gas at Scott Reef.

Woodside has revived litigation against Western Australian community members in the Supreme Court of Western Australia relating to a three-year-old protest to bring attention to the harmful effects of Woodside’s gas expansion on climate and cultural heritage.

It comes as public opposition to Woodside’s plans to drill over 50 gas wells at Scott Reef continues to mount.

David Ritter, CEO at Greenpeace Australia Pacific, said: “In the face of growing opposition to Woodside’s plans to drill over 50 gas wells at Scott Reef, this smacks of Woodside trying to intimidate and bully everyday Australians into submission.

“But the community won’t be silenced on this. Woodside’s plan to drill for gas at the pristine, magnificent Scott Reef, risking precious marine wildlife like turtles and whales, oceans and the climate, is a disaster waiting to happen.

“This SLAPP* suit is part of an alarming global trend of corporate bullies using bad-faith legal tactics to intimidate and silence people exercising their democratic right to protest. Companies like Woodside should not be allowed to use the courts to suppress public participation.

“WA has a proud history of civil protest to establish many of the rights, freedoms and benefits that we now celebrate. The whales that West Australians now love so much would not have been saved without protest. This kind of action by Woodside is intended to silence such protest. A healthy democracy depends on everyday people being free to speak out without fear of corporate intimidation.”

-ENDS-

Notes for editor

*SLAPP stands for “Strategic Lawsuit Against Public Participation”. It is a legal tactic used by powerful corporations, particularly within the fossil fuel industry, to censor, intimidate, and silence critics by burdening them with the high costs of a legal defense until they abandon their environmental advocacy or protests.

Media contact

Lucy Keller on 0491 135 308 or lucy.keller@greenpeace.org

-

Climate Change11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases12 months ago

嘉宾来稿:探究火山喷发如何影响气候预测