Carbon dioxide (CO2) emissions from fossil fuels and cement will rise around 0.8% in 2024, reaching a record 37.4bn tonnes of CO2 (GtCO2), according to the 2024 Global Carbon Budget report by the Global Carbon Project.

This is 0.4GtCO2 higher than the previous record, set in 2023.

Total CO2 emissions – including both fossil and land-use emissions – will also set a new record at 41.6GtCO2, reflecting a growth of 2% over 2023 levels.

This is due, in part, to higher than usual land-use emissions driven by extreme wildfire activity in South America.

Despite the increase in 2024, total CO2 emissions have largely plateaued over the past decade, a sign that the world is making some modest progress tackling emissions.

But a flattening of emissions is far from what is needed to bring global emissions down to zero and stabilise global temperatures in-line with Paris Agreement goals.

The 19th edition of the Global Carbon Budget, which is published today, also reveals:

- Emissions emissions are projected to decrease significantly in the EU (down 3.8%) and slightly in the US (down 0.6%) in 2024. They are expected to increase slightly in China (up 0.2%), and increase significantly in India (up 4.6%) and the rest of the world (up 1.6%, including international shipping and aviation).

- Global emissions from coal increased by 0.2% in 2024 compared to 2023, while oil emissions increased 0.9% and gas emissions increased by 2.4%. Emissions from cement and other sources fell by 2.8%.

- Global land-use emissions clocked in at 4.2GtCO2 in 2024. This represents a 0.5GtCO2 increase over 2023 and was primarily driven by wildfire emissions linked to deforestation and forest degradation in South America. Overall, land-use emissions have decreased by around 28% since their peak in the late-1990s, with a particularly large drop in the past decade.

- While the land sink was quite weak in 2023 – leading to speculation that it may be on a path toward collapse – it appears to have largely recovered back to close to its average for the past decade.

- If global emissions remain at current levels, the remaining carbon budget to limit warming to 1.5C (with a 50% chance) will be exhausted in the next six years. Carbon budgets to limit warming to 1.7C and 2C would similarly be used up in 15 and 27 years, respectively.

- The concentration of CO2 in the atmosphere is set to reach 422.5 parts per million (ppm) in 2024, 2.8ppm above 2023 and 52% above pre-industrial levels.

Both global fossil and total CO2 emissions at record levels

The 2024 Global Carbon Budget finds that CO2 emissions from fossil use are projected to rise 0.8% in 2024, reaching a record 37.4GtCO2 – 0.4GtCO2 higher than the previous record, set last year.

Total CO2 emissions, which include land-use change, are also expected to reach record highs at 41.6GtCO2, or 2.0% above the previous record set in 2023.

This large increase was driven both by consistent growth in fossil-fuel emissions and abnormally high land-use emissions in 2024 – due in part to wildfires in South America exacerbated by a strong El Niño event and high temperatures.

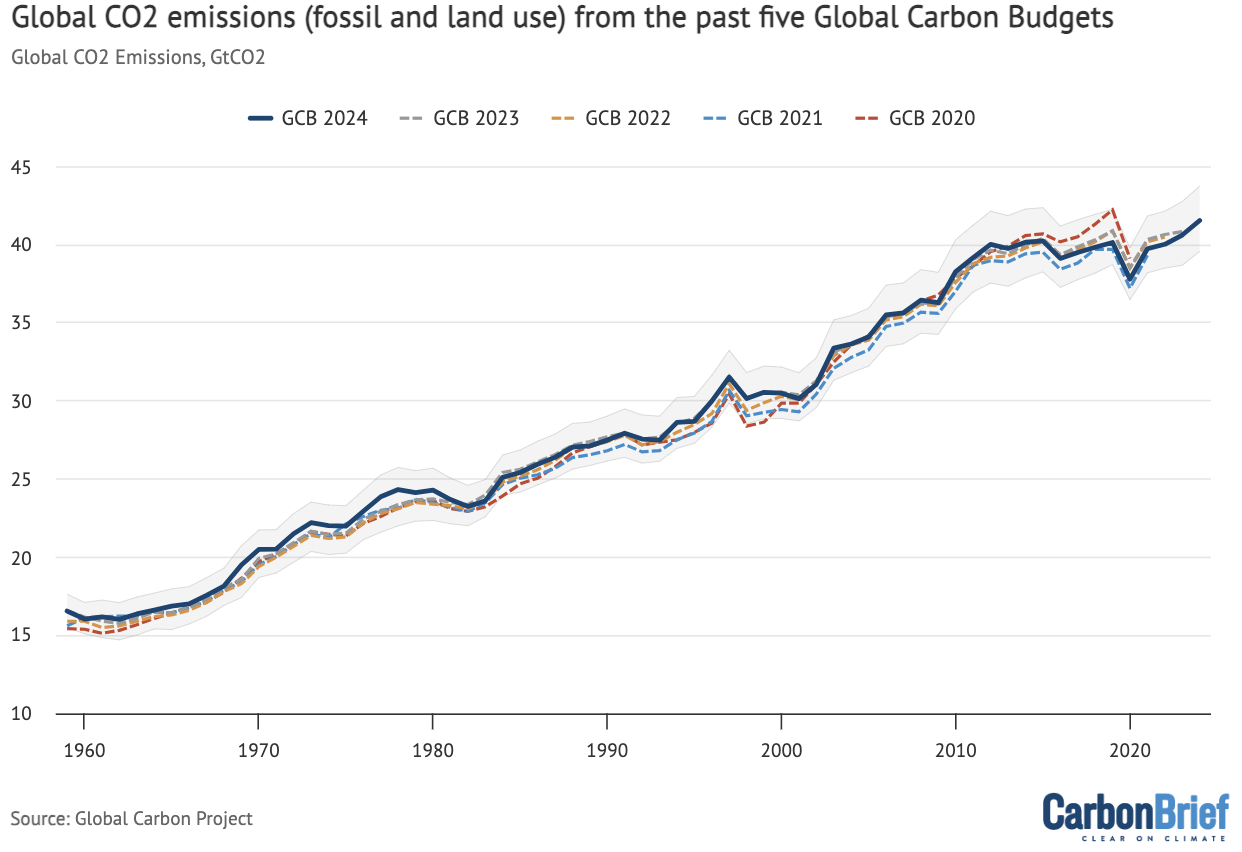

Each year the Global Carbon Budget is updated to include the latest data as well as improvements to modelling sources and sinks, resulting in some year-to-year revisions to the historical record.

The figure below shows the 2024 global CO2 emissions update (dark blue solid line) alongside 2023 (grey dotted) 2022 (yellow dotted), 2021 (bright blue dotted) and 2020 (red dotted). The shaded area indicates the uncertainty around the new 2024 budget.

The 2024 figures are generally quite similar to those in the 2023 Global Carbon Budget, though they show somewhat higher emissions prior to 1980 and slightly lower emissions over the past seven years. Revisions to the data mean that 2023 is no longer a hair below 2019 levels, as was reported by Carbon Brief last year, but rather exceeds them by nearly 0.5GtCO2.

Annual total global CO2 emissions – from fossil and land-use change – between 1959 and 2024 for the 2020, 2021, 2022, 2023 and 2024 versions of the Global Carbon Project’s Global Carbon Budget, in billions of tonnes of CO2 per year (GtCO2). Shaded area shows the estimated one-sigma uncertainty for the 2024 budget. Data from the Global Carbon Project; chart by Carbon Brief.

Total global CO2 emissions have notably plateaued in the past decade (2015-24), growing at only 0.2% per year compared to the 1.9% rate of growth over the previous decade (2005-214) and the longer-term average growth rate of 1.7% between 1959 and 2014.

This apparent flattening is due to declining land-use emissions compensating for continued increases in fossil CO2 emissions. Fossil emissions grew around 0.2GtCO2 per year over the past decade, while land-use emissions decreased by a comparable amount.

However, despite the emissions plateau, there is still no sign of the rapid and deep decrease in CO2 emissions needed to reach net-zero and stabilise global temperatures in-line with Paris Agreement goals.

If global emissions remain at current levels, the remaining carbon budget to limit warming to 1.5C (with a 50% chance) will be exhausted in the next six years. Carbon budgets to limit warming to 1.7C and 2C would similarly be used up in 15 and 27 years, respectively.

Global fossil CO2 emissions also grew more slowly in the past decade (0.7% per year) compared to the previous decade (2.1%). This was driven by the continued decarbonisation of energy systems – including a shift from burning coal to gas and replacing fossil fuels with renewables – as well as slightly weaker global economic growth during the past decade.

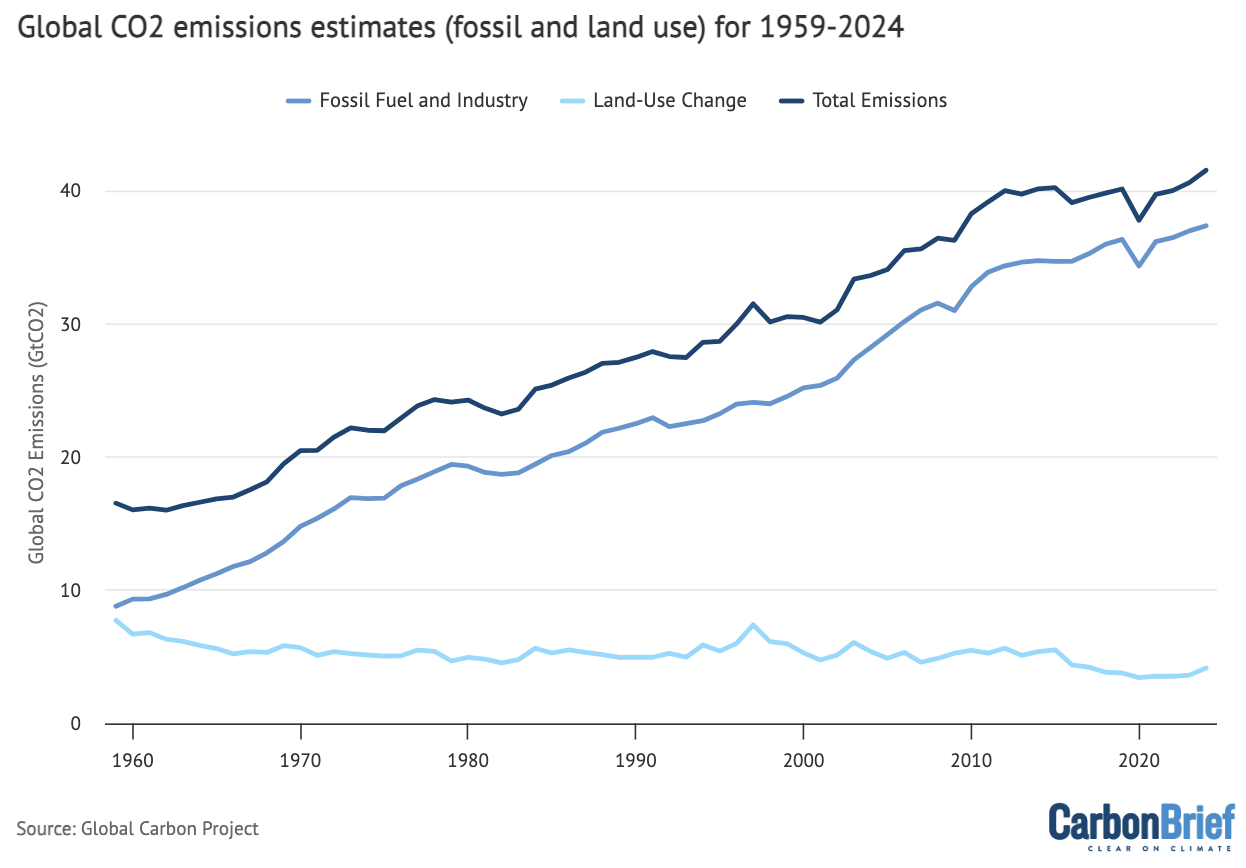

The figure below breaks down global emissions (dark blue line) in the 2024 budget into fossil (mid blue) and land-use (light blue) components. Fossil CO2 emissions represent the bulk of total global emissions in recent years, accounting for approximately 90% of emissions in 2024 (compared to 10% for land use). This represents a large change from the first half of the 20th century, when land-use emissions were approximately the same as fossil emissions.

Global fossil emissions include CO2 emitted from burning coal, oil and gas, as well as the production of cement. However, the Global Carbon Budget also subtracts the cement carbonation sink – CO2 slowly absorbed by cement once it is exposed to the air – from fossil emissions in each year to determine total fossil emissions.

Global CO2 emissions separated out into fossil and land-use change components between 1959 and 2024 from the 2024 Global Carbon Budget. Note that fossil CO2 emissions are inclusive of the cement carbonation sink. Data from the Global Carbon Project; chart by Carbon Brief.

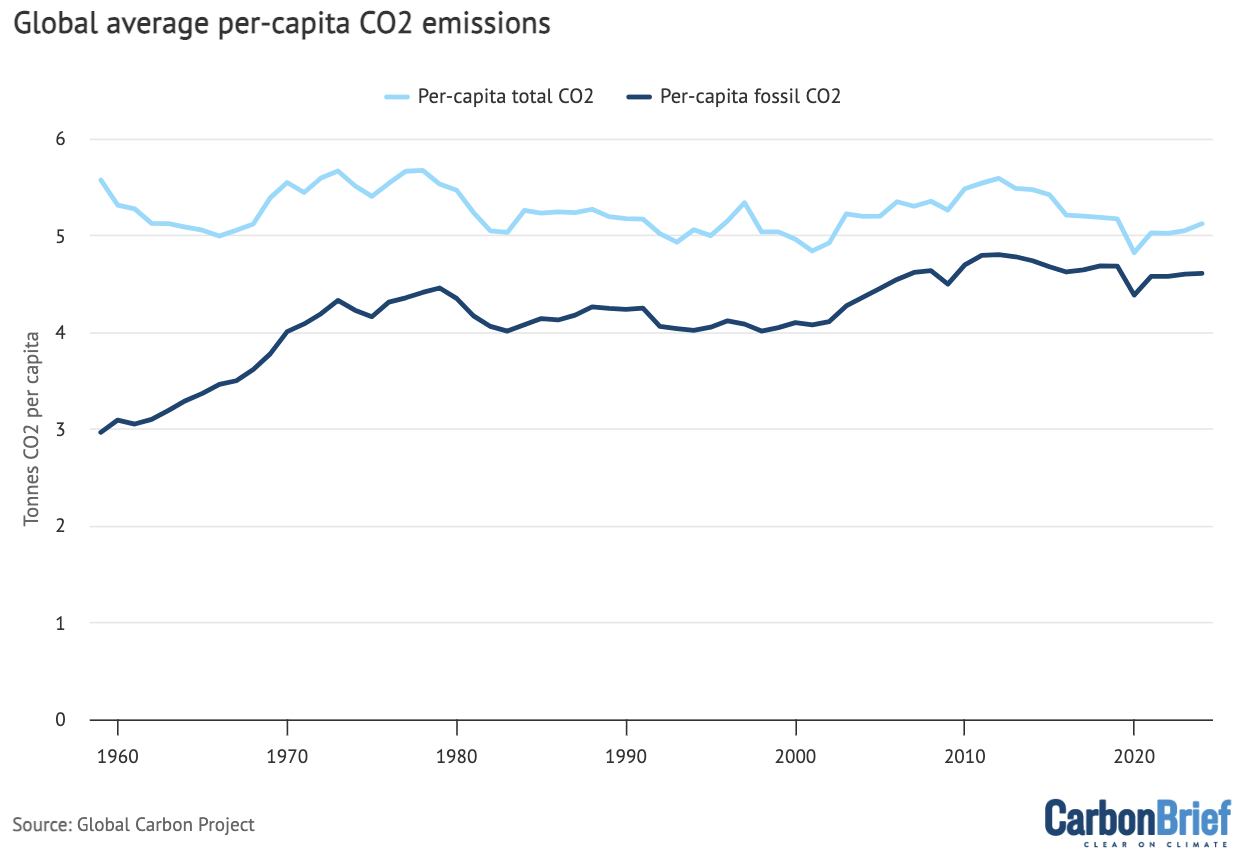

Global emissions can also be expressed on a per-capita basis, as shown in the figure below. While it is ultimately total global emissions that matter for the Earth’s climate – and a global per-capita figure glosses over a lot of variation among and within countries it is noteworthy that global per-capita emissions peaked in 2012 and have been slightly declining in the years since.

Global per-capita CO2 emissions between 1959 and 2024. Note that fossil CO2 emissions are inclusive of the cement carbonation sink. Data from the Global Carbon Project; chart by Carbon Brief.

Land-use emissions trending downward

Global land-use emissions stem from deforestation, degradation, loss of peatlands and harvesting trees for wood. They averaged 4GtCO2 over the past decade (2015-24) and the Global Carbon Budget provides an initial projection for 2024 of 4.2GtCO2.

This represents a 0.5GtCO2 increase over land-use emissions in 2023. This was primarily driven by wildfire emissions linked to deforestation and forest degradation in South America. Drought conditions associated with this year’s El Niño event contributed to the severity of the fires.

Overall, land-use emissions have decreased by around 28% since their peak in the late-1990s, with a particularly large drop in the past decade.

This decline is statistically significant and is due both to decreasing deforestation and increasing levels of reforestation and afforestation globally (though rates of reforestation and afforestation have largely stagnated over the past decade).

This year’s Global Carbon Budget features a number of important improvements to land-use change emissions estimates, including updated estimates of cropland and pasture area in major countries.

Four countries – Brazil, Indonesia, China and the Democratic Republic of the Congo (DRC) – collectively contribute approximately 60% of the global land-use emissions.

The figure below shows changes in emissions over time in these countries, as well as land-use emissions in the rest of the world (grey). Note that Chinese land-use emissions are negative in recent years.

Annual CO2 emissions from land-use change by major emitting countries and the rest of world over 1959-2023. Note that country-level land-use change emissions are not yet available for 2024. Data from the Global Carbon Project; chart by Carbon Brief.

Fossil CO2 in major emitting countries

Global emissions of fossil CO2 – including coal, oil, gas and cement – increased by around 0.8% in 2024, relative to 2023, with an uncertainty range of -0.3% to 1.9%. This represents a new record high and is 2.6% above the 2019 pre-Covid levels.

The figure below shows global CO2 emissions from fossil fuels, divided into emissions from major emitting countries including China (dark blue shading), India (mid blue), the US (light blue), EU (pale blue) and the remainder of the world (grey).

Annual fossil CO2 emissions by major countries and the rest of the world over 1959-2024, excluding the cement carbonation sink as national-level values are not available. Data from the Global Carbon Project; chart by Carbon Brief.

For this year, China represents 32% of global CO2 emissions. Their emissions in 2024 are projected to increase by a relatively small 0.2% (with an uncertainty range of -1.6% to +2%), driven by a small rise in emissions from coal (0.3%) and a large rise in natural gas emissions (8%). Emissions from oil are expected to decrease modestly (-0.8%), while emissions from cement are expected to fall sharply (-8.1%).

The Global Carbon Budget report suggests that Chinese oil emissions have probably already peaked, reflecting the acceleration of vehicle electrification.

India represents 8% of global emissions. In 2024, Indian emissions are projected to increase by 4.6% (with a range from 3.0% to 6.1%), with a 4.5% increase in emissions from coal, a 3.6% increase in emissions from oil, a 11.8% increase in emissions from natural gas and a 4% increase in emissions from cement.

While renewable energy is expanding quickly in India, it remains far slower than the rate of power demand growth as the economy rapidly expands.

The US represents 13% of global emissions this year – though is responsible for a much larger portion of historical emissions and associated atmospheric accumulation of CO2.

US emissions are projected to decrease by 0.6% in 2024 (ranging from -2.9% to +1.7%). This is being driven by a modest decrease in coal emissions (falling 3.5%). Oil emissions are expected to decline by a slight 0.7%, reflecting the rise of electric vehicles, while emissions from gas are expected to increase by 1%.

The EU represents 7% of global emissions. EU emissions are expected to decrease by 3.8% in 2024, driven by a 15.8% decline in coal emissions, a 1.3% decline in natural gas emissions, and a 3.5% decline in cement emissions. EU oil emissions are expected to increase slightly, by 0.2%.

The EU’s overall emissions decline is being driven by a combination of rapid clean energy adoption as well as relatively weak economic growth and high energy prices.

International aviation and shipping (included in the “rest of world” in the figure above) are responsible for 3% of global emissions. They are projected to increase by

7.8% in 2024, but remain below their 2019 pre-pandemic level by 3.5%.

The rest of the world (excluding aviation) represents 38% of global emissions. Emissions are expected to grow by 1.1% in 2024 (ranging from -1.0% to +3.3%), with increases in emissions from coal (0.5%), oil (0.5%), natural gas (2.2%) and cement (2%).

Overall, emissions are projected to decrease in the EU and US in 2024, increase slightly in China, and increase significantly in India and the rest of the world.

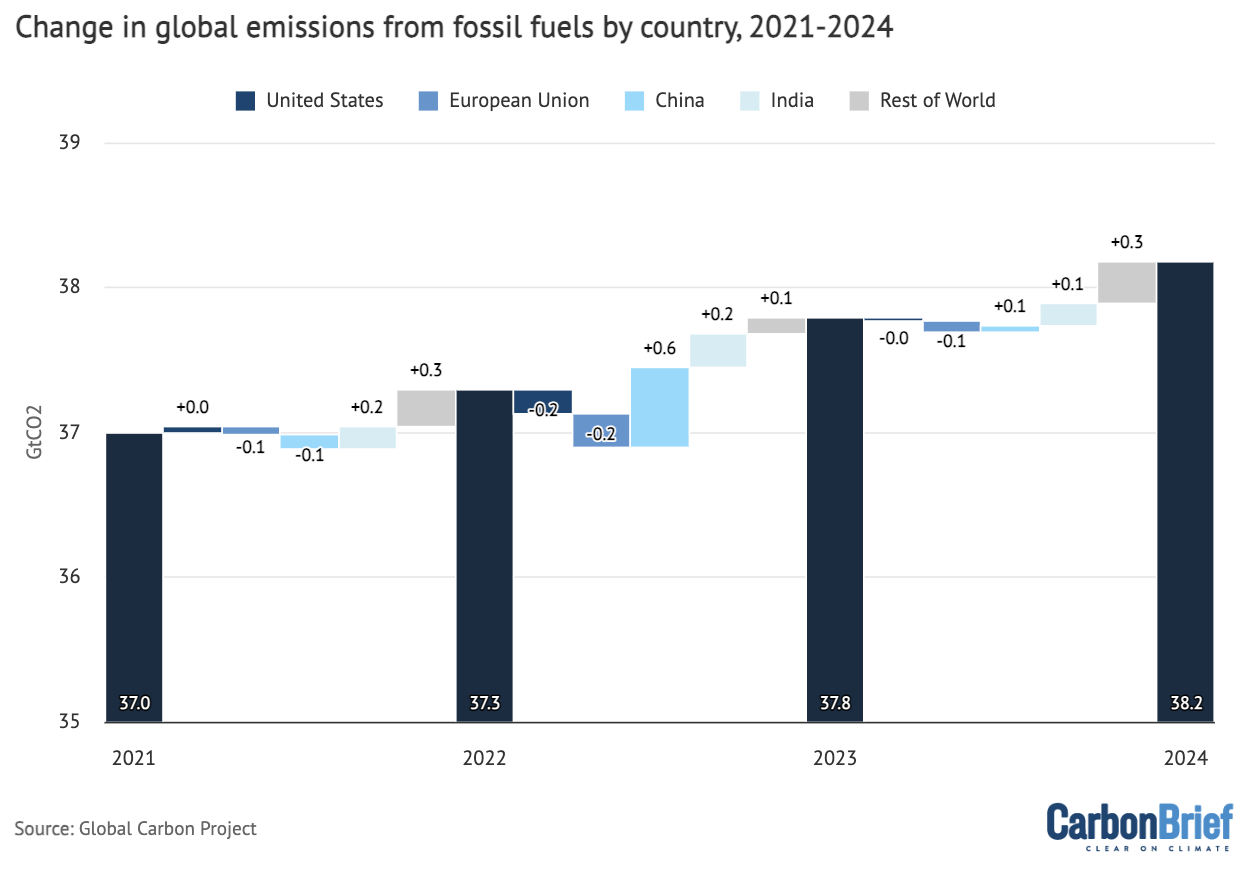

The total emissions for each year between 2021 and 2024, as well as the countries and regions that were responsible for the changes in absolute emissions, are shown in the figure below.

Annual emissions for 2021, 2022, 2023 and estimates for 2024 are shown by the navy blue bars. The smaller bars show the change in emissions between each set of years, broken down by country or region – the US (dark blue), EU (mid blue), China (light blue), India (pale blue) and the rest of the world (grey). Negative values show reductions in emissions, while positive values reflect emission increases.

Annual global CO2 emissions from fossil fuels (navy blue bars) and drivers of changes between years by country (smaller bars), excluding the cement carbonation sink as national-level values are not available. Negative values indicate reductions in emissions. Note that the y-axis does not start at zero. Data from the Global Carbon Project; chart by Carbon Brief.

The Global Carbon Project notes that emissions have declined over the past decade (2014-23) in 22 nations – up from 18 countries during the decade prior to that (2004-13). This decrease comes despite continued domestic economic growth and represents a long-term decoupling of CO2 emissions and the economy.

CO2 emissions decreased in Organisation for Economic Co-operation and Development (OECD) countries by 1.4% per year over the past decade, compared to a decrease of 0.9% per year in the decade prior. Non-OECD countries saw their emissions grow more slowly (1.8%) over the last decade than the prior one (4.9%).

Growth in emissions from coal, oil, and gas

Global fossil-fuel emissions primarily result from the combustion of coal, oil and natural gas. Coal is responsible for more emissions than any other fossil fuel, representing approximately 41% of global fossil CO2 emissions in 2024. Oil is the second largest contributor at 33% of fossil CO2, while gas rounds out the pack at 22%.

These percentages reflect both the amount of each fossil fuel consumed globally, but also differences in CO2 intensities. Coal results in the most CO2 emitted per unit of heat or energy produced, followed by oil and natural gas.

The figure below shows global CO2 emissions from different fuels over time, covering coal (dark blue shading), oil (mid blue) and gas (light blue), as well as cement production (pale blue) and other sources (grey).

While coal emissions increased rapidly in the mid-2000s, it has largely plateaued since 2013. However, coal use increased significantly in 2021 and then slightly in the subsequent three years.

Annual CO2 emissions by fossil fuel over 1959-2024, excluding the cement carbonation sink. Data from the Global Carbon Project; chart by Carbon Brief.

Global emissions from coal increased by 0.2% in 2024 compared to 2023, while oil emissions increased 0.9% and gas emissions increased by 2.4%. Emissions from cement and other sources fell by 3%.

Despite setting a new record this year, global coal use is only 3% above 2013 levels – a full 12 years ago. By contrast, during the 2000s, global coal use grew at a rate of around 4% every single year.

The total emissions for each year between 2021 and 2024 (navy blue bars), as well as the absolute change in emissions for each fuel between years, are shown in the figure below.

Annual global CO2 emissions from fossil fuels (navy blue bars) and drivers of changes between years by fuel, excluding the cement carbonation sink. Negative values indicate reductions in emissions. Note that the y-axis does not start at zero. Data from the Global Carbon Project; chart by Carbon Brief.

Even though they have been increasing over the past four years, global CO2 emissions from oil remain very slightly (0.8%) below the pre-pandemic highs of 2019.

The global carbon budget

Every year, the Global Carbon Project provides an estimate of the overall “global carbon budget”. This is based on estimates of the release of CO2 through human activity and its uptake by the oceans and land, with the remainder adding to atmospheric concentrations of the gas.

(This differs from the commonly used term “remaining carbon budget”, which refers to the amount of CO2 that can be released while keeping warming below global limits of 1.5 or 2C.)

The most recent budget, including estimated values for 2024, is shown in the figure below. Values above zero represent sources of CO2 – from fossil fuels and industry (dark blue shading) and land use (mid blue) – while values below zero represent “carbon sinks” that remove CO2 from the atmosphere. Any CO2 emissions that are not absorbed by the oceans (light grey) or land vegetation (mid grey) accumulate in the atmosphere (dark grey).

Annual global carbon budget of sources and sinks over 1959-2024. Fossil CO2 emissions include the cement carbonation sink. Note that the budget does not fully balance every year due to remaining uncertainties, particularly in sinks. Data from the Global Carbon Project; chart by Carbon Brief.

Over the past decade (2015-24), the world’s oceans have taken up approximately 26.5% of total human emissions, or around 10.6GtCO2 per year. The ocean CO2 sink has been relatively flat since 2016 after growing rapidly over the prior decades, reflecting the plateauing of global emissions during that period.

The land sink takes up around 29% of global emissions, or 11.5GtCO2 per year on average. While the land sink was quite weak in 2023 – leading some to speculate that it may be on a path toward collapse – it appears to have largely recovered back to close to its average level over the past decade in 2024 as El Niño conditions have faded.

Global CO2 emissions from fires were quite high in 2024, around 7GtCO2 over the first 10 months of the year and similar to the above average values in 2023.

This was driven by large emissions in North and South America, particularly in Canada and Brazil. (It is not possible to make a direct comparison between reported fire CO2 emissions and other components of the global carbon budget as they already show up in both parts of the land sink and land-use emissions.)

Overall, the impact of the ongoing emissions from human activity is that atmospheric CO2 continues to increase.

The growth rate of atmospheric CO2 in 2024 is expected to be around 2.76ppm, which is above average compared to the rate of 2.46% over the past decade (2014-23).

The 2024 rise in atmospheric CO2 concentration was the fifth largest over the 1959-2024 period, closely following 2023, 2015, 2016 and 1998 – most of which were strong El Niño years.

Atmospheric CO2 concentrations are set to reach an annual average of 422.5ppm in 2024, representing an increase of 52% above pre-industrial levels of 280ppm.

The post Analysis: Global CO2 emissions will reach new high in 2024 despite slower growth appeared first on Carbon Brief.

Analysis: Global CO2 emissions will reach new high in 2024 despite slower growth

N.C. Gov. Josh Stein wants state lawmakers to rethink tax breaks for data centers. The industry’s opacity makes it difficult to evaluate costs and benefits.

Tax breaks for data centers in North Carolina keep as much as $57 million each year into from state and local government coffers, state figures show, an amount that could balloon to billions of dollars if all the proposed projects are built.

The Global Environment Facility (GEF), a multilateral fund that provides climate and nature finance to developing countries, has raised $3.9 billion from donor governments in its last pledging session ahead of a key fundraising deadline at the end of May.

The amount, which is meant to cover the fund’s activities for the next four years (July 2026-June 2030), falls significantly short of the previous four-year cycle for which the GEF managed to raise $5.3bn from governments. Since then, military and other political priorities have squeezed rich nations’ budgets for climate and development aid.

The facility said in a statement that it expects more pledges ahead of the final replenishment package, which is set for approval at the next GEF Council meeting from May 31 to June 3.

Claude Gascon, interim CEO of the GEF, said that “donor countries have risen to the challenge and made bold commitments towards a more positive future for the planet”. He added that the pledges send a message that “the world is not giving up on nature even in a time of competing priorities”.

-

UK imports of “green” jet fuel linked to Amazon deforestation

A Texas refinery shipping sustainable aviation fuel to Europe has sourced beef tallow with links to a meatpacking firm fined over illegal cattle purchases -

Italy pushes coal exit back after gas prices rise

Analysts say the move sends a negative signal, but its impact will be limited given coal’s marginal role in Italy’s energy mix

Donors under pressure

But Brian O’Donnell, director of the environmental non-profit Campaign for Nature, said the announcement shows “an alarming trend” of donor governments cutting public finance for climate and nature.

“Wealthy nations pledged to increase international nature finance, and yet we are seeing cuts and lower contributions. Investing in nature prevents extinctions and supports livelihoods, security, health, food, clean water and climate,” he said. “Failing to safeguard nature now will result in much larger costs later.”

At COP29 in Baku, developed countries pledged to mobilise $300bn a year in public climate finance by 2035, while at UN biodiversity talks they have also pledged to raise $30bn per year by 2030. Yet several wealthy governments have announced cuts to green finance to increase defense spending, among them most recently the UK.

As for the US, despite Trump’s cuts to international climate finance, Congress approved a $150 million increase in its contribution to the GEF after what was described as the organisation’s “refocus on non-climate priorities like biodiversity, plastics and ocean ecosystems, per US Treasury guidance”.

The facility will only reveal how much each country has pledged when its assembly of 186 member countries meets in early June. The last period’s largest donors were Germany ($575 million), Japan ($451 million), and the US ($425 million).

The GEF has also gone through a change in leadership halfway through its fundraising cycle. Last December, the GEF Council asked former CEO Carlos Manuel Rodriguez to step down effective immediately and appointed Gascon as interim CEO.

Santa Marta conference: fossil fuel transition in an unstable world

New guidelines

As part of the upcoming funding cycle, the GEF has approved a set of guidelines for spending the $3.9bn raised so far, which include allocating 35% of resources for least developed countries and small island states, as well as 20% of the money going to Indigenous people and communities.

Its programs will help countries shift five key systems – nature, food, urban, energy and health – from models that drive degradation to alternatives that protect the planet and support human well-being by integrating the value of nature into production and consumption systems.

The new priorities also include a target to allocate 25% of the GEF’s budget for mobilising private funds through blended finance. This aligns with efforts by wealthy countries to increase contributions from the private sector to international climate finance.

Niels Annen, Germany’s State Secretary for Economic Cooperation and Development, said in a statement that the country’s priorities are “very well reflected” in the GEF’s new spending guidelines, including on “innovative finance for nature and people, better cooperation with the private sector, and stable resources for the most vulnerable countries”.

Aliou Mustafa, of the GEF Indigenous Peoples Advisory Group (IPAG), also welcomed the announcement, adding that “the GEF is strengthening trust and meaningful partnerships with Indigenous Peoples and local communities” by placing them at the “centre of decision-making”.

The post GEF raises $3.9bn ahead of funding deadline, $1bn below previous budget appeared first on Climate Home News.

GEF raises $3.9bn ahead of funding deadline, $1bn below previous budget

Tropical cyclones that rapidly intensify when passing over marine heatwaves can become “supercharged”, increasing the likelihood of high economic losses, a new study finds.

Such storms also have higher rates of rainfall and higher maximum windspeeds, according to the research.

The study, published in Science Advances, looks at the economic damages caused by nearly 800 tropical cyclones that occurred around the world between 1981 and 2023.

It finds that rapidly intensifying tropical cyclones that pass near abnormally warm parts of the ocean produce nearly double – 93% – the economic damages as storms that do not, even when levels of coastal development are taken into account.

One researcher, who was not involved in the study, tells Carbon Brief that the new analysis is a “step forward in understanding how we can better refine our predictions of what might happen in the future” in an increasingly warm world.

As marine heatwaves are projected to become more frequent under future climate change, the authors say that the interactions between storms and these heatwaves “should be given greater consideration in future strategies for climate adaptation and climate preparedness”.

‘Rapid intensification’

Tropical cyclones are rapidly rotating storm systems that form over warm ocean waters, characterised by low pressure at their cores and sustained winds that can reach more than 120 kilometres per hour.

The term “tropical cyclones” encompasses hurricanes, cyclones and typhoons, which are named as such depending on which ocean basin they occur in.

When they make landfall, these storms can cause major damage. They accounted for six of the top 10 disasters between 1900 and 2024 in terms of economic loss, according to the insurance company Aon’s 2025 climate catastrophe insight report.

These economic losses are largely caused by high wind speeds, large amounts of rainfall and damaging storm surges.

Storms can become particularly dangerous through a process called “rapid intensification”.

Rapid intensification is when a storm strengthens considerably in a short period of time. It is defined as an increase in sustained wind speed of at least 30 knots (around 55 kilometres per hour) in a 24-hour period.

There are several factors that can lead to rapid intensification, including warm ocean temperatures, high humidity and low vertical “wind shear” – meaning that the wind speeds higher up in the atmosphere are very similar to the wind speeds near the surface.

Rapid intensification has become more common since the 1980s and is projected to become even more frequent in the future with continued warming. (Although there is uncertainty as to how climate change will impact the frequency of tropical cyclones, the increase in strength and intensification is more clear.)

Marine heatwaves are another type of extreme event that are becoming more frequent due to recent warming. Like their atmospheric counterparts, marine heatwaves are periods of abnormally high ocean temperatures.

Previous research has shown that these marine heatwaves can contribute to a cyclone undergoing rapid intensification. This is because the warm ocean water acts as a “fuel” for a storm, says Dr Hamed Moftakhari, an associate professor of civil engineering at the University of Alabama who was one of the authors of the new study. He explains:

“The entire strength of the tropical cyclone [depends on] how hot the [ocean] surface is. Marine heatwave means we have an abundance of hot water that is like a gas [petrol] station. As you move over that, it’s going to supercharge you.”

However, the authors say, there is no global assessment of how rapid intensification and marine heatwaves interact – or how they contribute to economic damages.

Using the International Best Track Archive for Climate Stewardship (IBTrACS) – a database of tropical cyclone paths and intensities – the researchers identify 1,600 storms that made landfall during the 1981-2023 period, out of a total of 3,464 events.

Of these 1,600 storms, they were able to match 789 individual, land-falling cyclones with economic loss data from the Emergency Events Database (EM-DAT) and other official sources.

Then, using the IBTrACS storm data and ocean-temperature data from the European Centre for Medium-Range Weather Forecasts, the researchers classify each cyclone by whether or not it underwent rapid intensification and if it passed near a recent marine heatwave event before making landfall.

The researchers find that there is a “modest” rise in the number of marine heatwave-influenced tropical cyclones globally since 1981, but with significant regional variations. In particular, they say, there are “clear” upward trends in the north Atlantic Ocean, the north Indian Ocean and the northern hemisphere basin of the eastern Pacific Ocean.

‘Storm characteristics’

The researchers find substantial differences in the characteristics of tropical cyclones that experience rapid intensification and those that do not, as well as between rapidly intensifying storms that occur with marine heatwaves and those that occur without them.

For example, tropical cyclones that do not experience rapid intensification have, on average, maximum wind speeds of around 40 knots (74km/hr), whereas storms that rapidly intensify have an average maximum wind speed of nearly 80 knots (148km/hr).

Of the rapidly intensifying storms, those that are influenced by marine heatwaves maintain higher wind speeds during the days leading up to landfall.

Although the wind speeds are very similar between the two groups once the storms make landfall, the pre-landfall difference still has an impact on a storm’s destructiveness, says Dr Soheil Radfar, a hurricane-hazard modeller at Princeton University. Radfar, who is the lead author of the new study, tells Carbon Brief:

“Hurricane damage starts days before the landfall…Four or five days before a hurricane making landfall, we expect to have high wind speeds and, because of that high wind speed, we expect to have storm surges that impact coastal communities.”

They also find that rapidly intensifying storms have higher peak rainfall than non-rapidly intensifying storms, with marine heatwave-influenced, rapidly intensifying storms exhibiting the highest average rainfall at landfall.

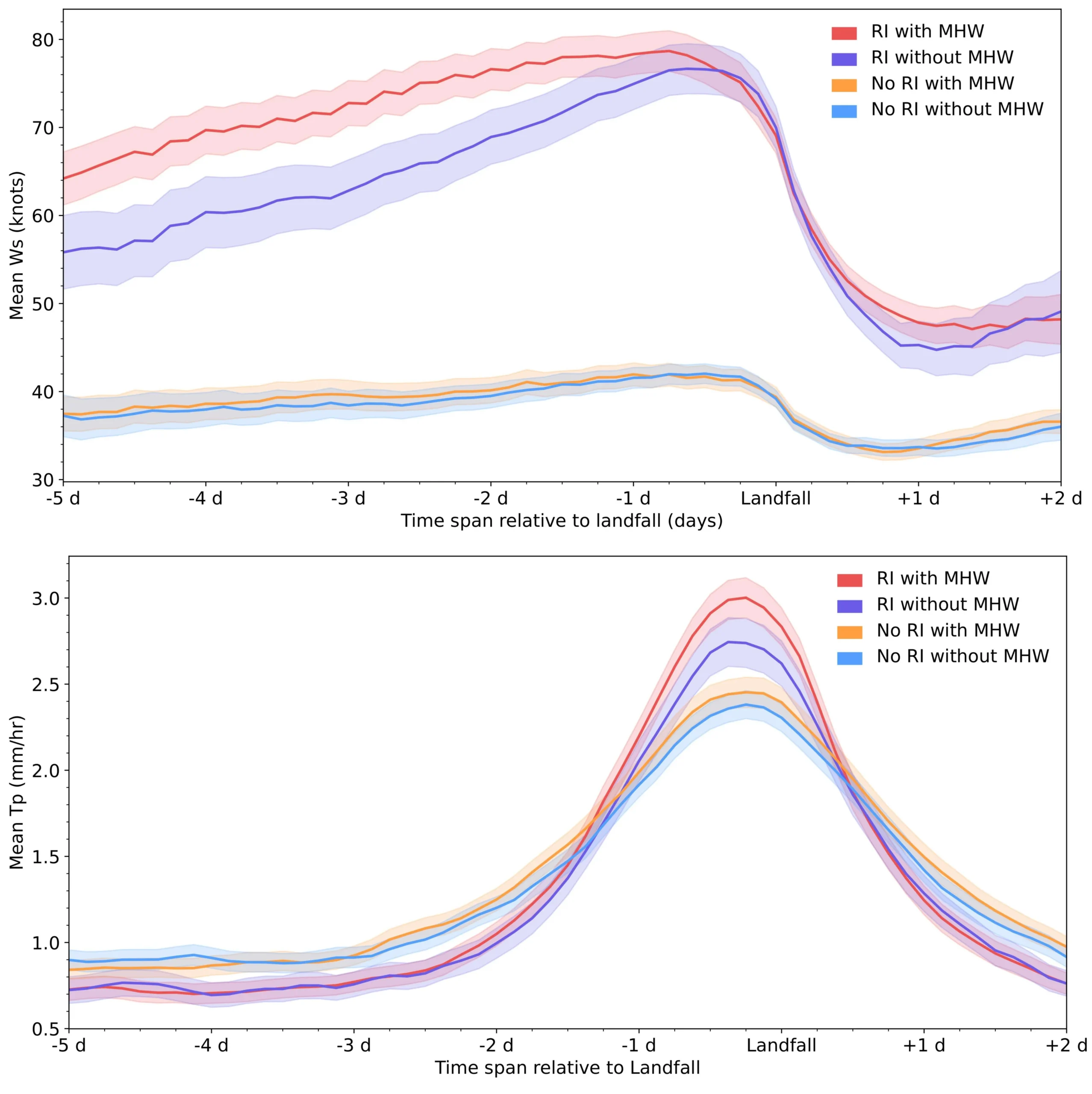

The charts below show the mean sustained wind speed in knots (top) and the mean rainfall in millimetres per hour (bottom) for the tropical cyclones analysed in the study in the five days leading up to and two days following a storm making landfall.

The four lines show storms that: rapidly intensified with the influence of marine heatwaves (red); those that rapidly intensified without marine heatwaves (purple); those that experienced marine heatwaves, but did not rapidly intensify (orange); and those that neither rapidly intensified nor experienced a marine heatwave (blue).

Dr Daneeja Mawren, an ocean and climate consultant at the Mauritius-based Mascarene Environmental Consulting who was not involved in the study, tells Carbon Brief that the new study “helps clarify how marine heatwaves amplify storm characteristics”, such as stronger winds and heavier rainfall. She notes that this “has not been done on a global scale before”.

However, Mawren adds that other factors not considered in the analysis can “make a huge difference” in the rapid intensification of tropical cyclones, including subsurface marine heatwaves and eddies – circular, spinning ocean currents that can trap warm water.

Dr Jonathan Lin, an atmospheric scientist at Cornell University who was also not involved in the study, tells Carbon Brief that, while the intensification found by the study “makes physical sense”, it is inherently limited by the relatively small number of storms that occur. He adds:

“There’s not that many storms, to tease out the physical mechanisms and observational data. So being able to reproduce this kind of work in a physical model would be really important.”

Economic costs

Storm intensity is not the only factor that determines how destructive a given cyclone can be – the economic damages also depend strongly on the population density and the amount of infrastructure development where a storm hits. The study explains:

“A high storm surge in a sparsely populated area may cause less economic damage than a smaller surge in a densely populated, economically important region.”

To account for the differences in development, the researchers use a type of data called “built-up volume”, from the Global Human Settlement Layer. Built-up volume is a quantity derived from satellite data and other high-resolution imagery that combines measurements of building area and average building height in a given area. This can be used as a proxy for the level of development, the authors explain.

By comparing different cyclones that impacted areas with similar built-up volumes, the researchers can analyse how rapid intensification and marine heatwaves contribute to the overall economic damages of a storm.

They find that, even when controlling for levels of coastal development, storms that pass through a marine heatwave during their rapid intensification cause 93% higher economic damages than storms that do not.

They identify 71 marine heatwave-influenced storms that cause more than $1bn (inflation-adjusted across the dataset) in damages, compared to 45 storms that cause those levels of damage without the influence of marine heatwaves.

This quantification of the cyclones’ economic impact is one of the study’s most “important contributions”, says Mawren.

The authors also note that the continued development in coastal regions may increase the likelihood of tropical cyclone damages over time.

Towards forecasting

The study notes that the increased damages caused by marine heatwave-influenced tropical cyclones, along with the projected increases in marine heatwaves, means such storms “should be given greater consideration” in planning for future climate change.

For Radfar and Moftakhari, the new study emphasises the importance of understanding the interactions between extreme events, such as tropical cyclones and marine heatwaves.

Moftakhari notes that extreme events in the future are expected to become both more intense and more complex. This becomes a problem for climate resilience because “we basically design in the future based on what we’ve observed in the past”, he says. This may lead to underestimating potential hazards, he adds.

Mawren agrees, telling Carbon Brief that, in order to “fully capture the intensification potential”, future forecasts and risk assessments must account for marine heatwaves and other ocean phenomena, such as subsurface heat.

Lin adds that the actions needed to reduce storm damages “take on the order of decades to do right”. He tells Carbon Brief:

“All these [planning] decisions have to come by understanding the future uncertainty and so this research is a step forward in understanding how we can better refine our predictions of what might happen in the future.”

The post Marine heatwaves ‘nearly double’ the economic damage caused by tropical cyclones appeared first on Carbon Brief.

Marine heatwaves ‘nearly double’ the economic damage caused by tropical cyclones

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits