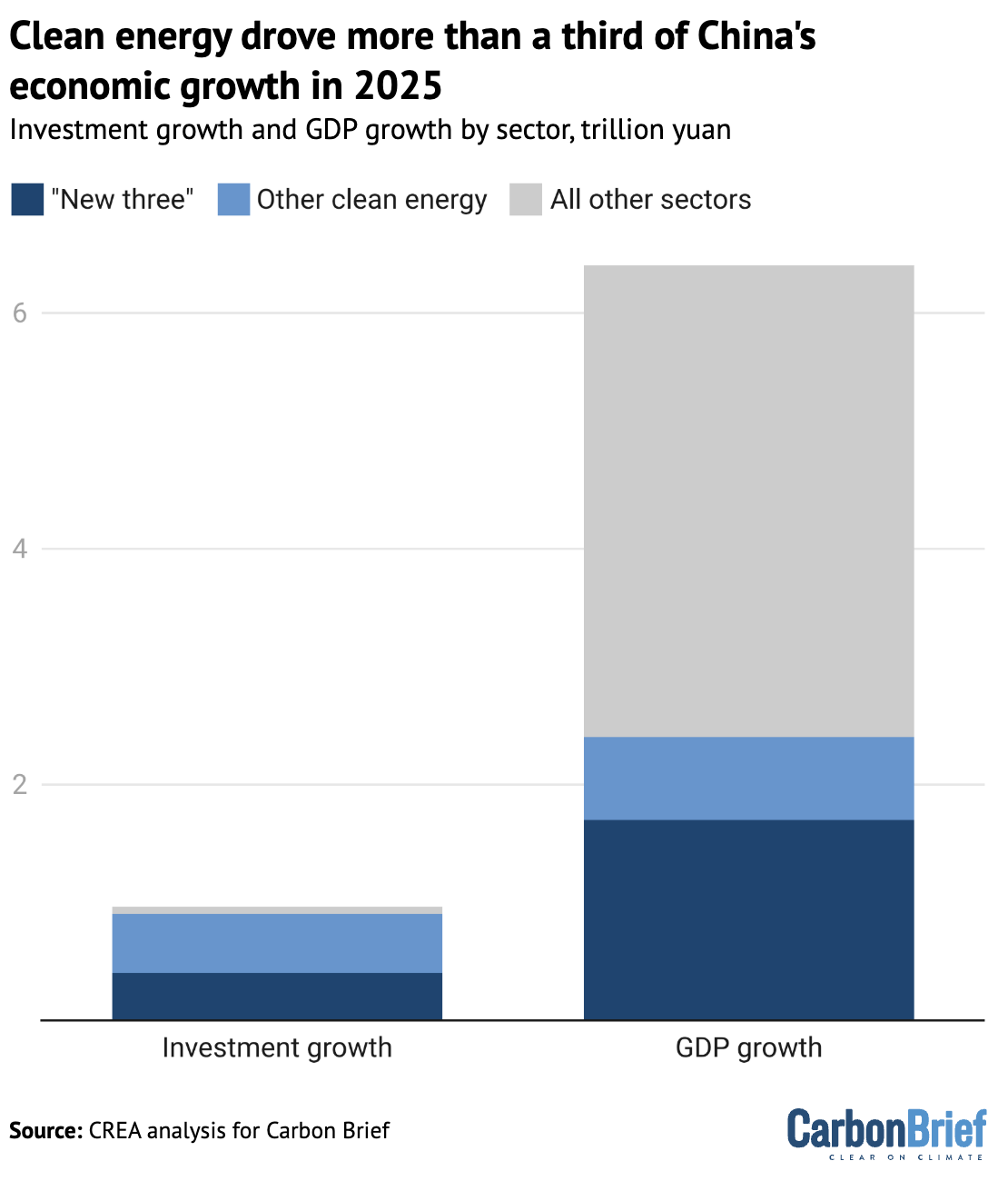

Solar power, electric vehicles (EVs) and other clean-energy technologies drove more than a third of the growth in China’s economy in 2025 – and more than 90% of the rise in investment.

Clean-energy sectors contributed a record 15.4tn yuan ($2.1tn) in 2025, some 11.4% of China’s gross domestic product (GDP) – comparable to the economies of Brazil or Canada.

The new analysis for Carbon Brief, based on official figures, industry data and analyst reports, shows that China’s clean-energy sectors nearly doubled in real value between 2022-25 and – if they were a country – would now be the 8th-largest economy in the world.

Other key findings from the analysis include:

- Without clean-energy sectors, China would have missed its target for GDP growth of “around 5%”, expanding by 3.5% in 2025 instead of the reported 5.0%.

- Clean-energy industries are expanding much more quickly than China’s economy overall, with their annual growth rate accelerating from 12% in 2024 to 18% in 2025.

- The “new three” of EVs, batteries and solar continue to dominate the economic contribution of clean energy in China, generating two-thirds of the value added and attracting more than half of all investment in the sectors.

- China’s investments in clean energy reached 7.2tn yuan ($1.0tn) in 2025, roughly four times the still sizable $260bn put into fossil-fuel extraction and coal power.

- Exports of clean-energy technologies grew rapidly in 2025, but China’s domestic market still far exceeds the export market in value for Chinese firms.

These investments in clean-energy manufacturing represent a large bet on the energy transition in China and overseas, creating an incentive for the government and enterprises to keep the boom going.

However, there is uncertainty about what will happen this year and beyond, particularly for solar power, where growth has slowed in response to a new pricing system and where central government targets have been set far below the recent rate of expansion.

An ongoing slowdown could turn the sectors into a drag on GDP, while worsening industrial “overcapacity” and exacerbating trade tensions.

Yet, even if central government targets in the next five-year plan are modest, those from local governments and state-owned enterprises could still drive significant growth in clean energy.

This article updates analysis previously reported for 2023 and 2024.

Clean-energy sectors outperform wider economy

China’s clean-energy economy continues to grow far more quickly than the wider economy. This means that it is making an outsize contribution to annual economic growth.

The figure below shows that clean-energy technologies drove more than a third of the growth in China’s economy overall in 2025 and more than 90% of the net rise in investment.

In 2022, China’s clean-energy economy was worth an estimated 8.4tn yuan ($1.2tn). By 2025, the sectors had nearly doubled in value to 15.4tn yuan ($2.1tn).

This is comparable to the entire output of Brazil or Canada and positions the Chinese clean-energy industry as the 8th-largest economy in the world. Its value is roughly half the size of the economy of India – the world’s fourth largest – or of the US state of California.

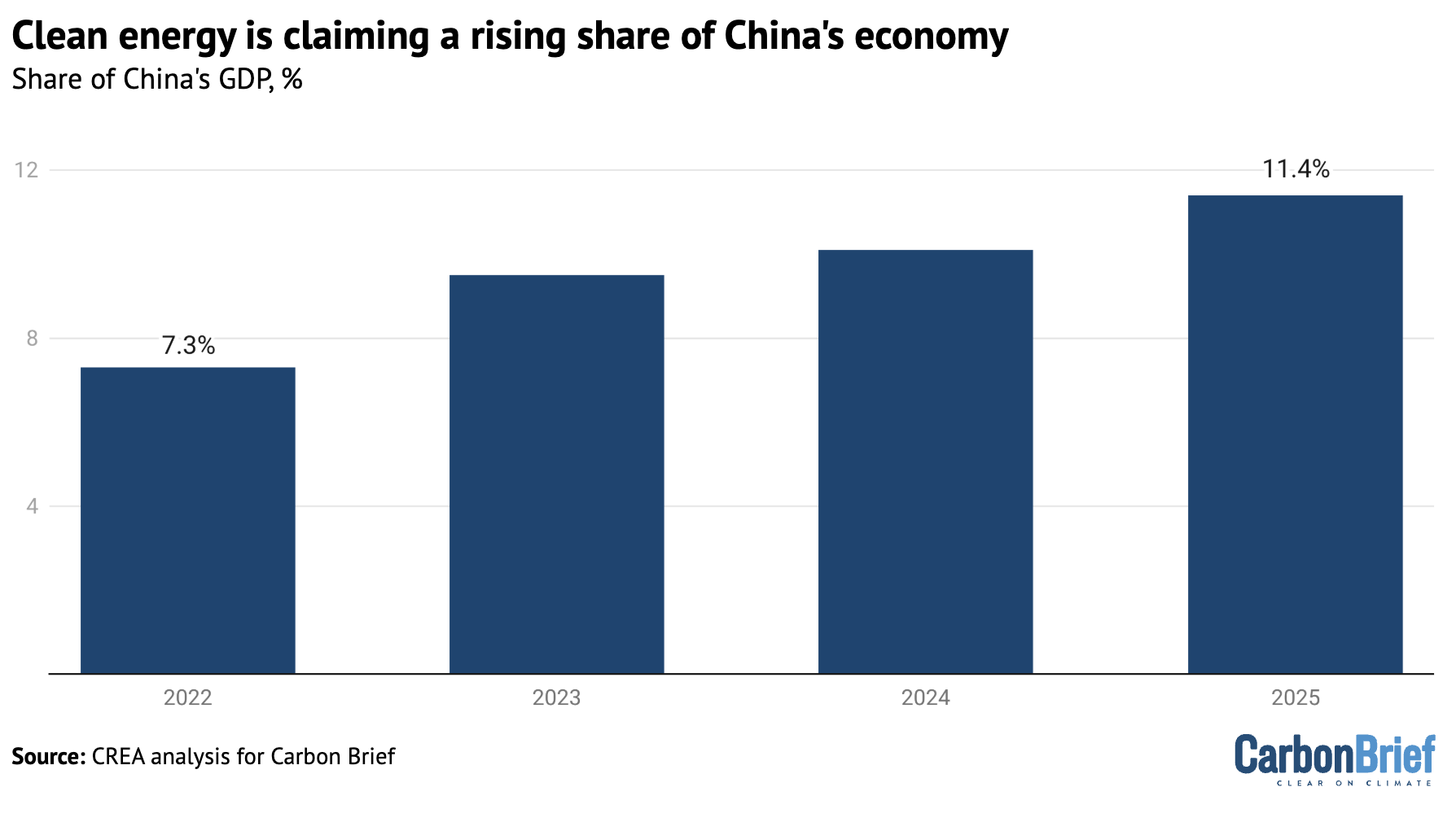

The outperformance of the clean-energy sectors means that they are also claiming a rising share of China’s economy overall, as shown in the figure below.

This share has risen from 7.3% of China’s GDP in 2022 to 11.4% in 2025.

Without clean-energy sectors, China’s GDP would have expanded by 3.5% in 2025 instead of the reported 5.0%, missing the target of “around 5%” growth by a wide margin.

Clean energy thus made a crucial contribution during a challenging year, when promoting economic growth was the foremost aim for policymakers.

The table below includes a detailed breakdown by sector and activity.

| Sector | Activity | Value in 2025, CNY bln | Value in 2025, USD bln | Year-on-year growth | Growth contribution | Value contribution | Value in 2025, CNY trn | Value in 2024, CNY trn | Value in 2023, CNY trn | Value in 2022, CNY trn |

|---|---|---|---|---|---|---|---|---|---|---|

| EVs | Investment: manufacturing capacity | 1,643 | 228 | 18% | 10.4% | 10.7% | 1.6 | 1.4 | 1.2 | 0.9 |

| EVs | Investment: charging infrastructure | 192 | 27 | 58% | 2.9% | 1.2% | 0.192 | 0.122 | 0.1 | 0.08 |

| EVs | Production of vehicles | 3,940 | 548 | 29% | 36.4% | 25.6% | 3.94 | 3.065 | 2.26 | 1.65 |

| Batteries | Investment: battery manufacturing | 277 | 38 | 35% | 3.0% | 1.8% | 0.277 | 0.205 | 0.32 | 0.15 |

| Batteries | Exports: batteries | 724 | 101 | 51% | 10.1% | 4.7% | 0.724 | 0.48 | 0.46 | 0.34 |

| Solar power | Investment: power generation capacity | 1,182 | 164 | 15% | 6.3% | 7.7% | 1.182 | 1.031 | 0.808 | 0.34 |

| Solar power | Investment: manufacturing capacity | 506 | 70 | -23% | -6.5% | 3.3% | 0.506 | 0.662 | 0.95 | 0.51 |

| Solar power | Electricity generation | 491 | 68 | 33% | 5.1% | 3.2% | 0.491 | 0.369 | 0.26 | 0.19 |

| Solar power | Exports of components | 681 | 95 | 21% | 4.9% | 4.4% | 0.681 | 0.562 | 0.5 | 0.35 |

| Wind power | Investment: power generation capacity, onshore | 612 | 85 | 47% | 8.1% | 4.0% | 0.612 | 0.417 | 0.397 | 0.21 |

| Wind power | Investment: power generation capacity, offshore | 96 | 13 | 98% | 2.0% | 0.6% | 0.096 | 0.048 | 0.086 | 0.06 |

| Wind power | Electricity generation | 510 | 71 | 13% | 2.4% | 3.3% | 0.51 | 0.453 | 0.4 | 0.34 |

| Nuclear power | Investment: power generation capacity | 173 | 24 | 18% | 1.1% | 1.1% | 0.17 | 0.15 | 0.09 | 0.07 |

| Nuclear power | Electricity generation | 216 | 30 | 8% | 0.7% | 1.4% | 0.216 | 0.2 | 0.19 | 0.19 |

| Hydropower | Investment: power generation capacity | 54 | 7 | -7% | -0.2% | 0.3% | 0.05 | 0.06 | 0.06 | 0.06 |

| Hydropower | Electricity generation | 582 | 81 | 3% | 0.6% | 3.8% | 0.582 | 0.567 | 0.51 | 0.51 |

| Rail transportation | Investment | 902 | 125 | 6% | 2.1% | 5.8% | 0.902 | 0.851 | 0.764 | 0.714 |

| Rail transportation | Transport of passengers and goods | 1,020 | 142 | 3% | 1.3% | 6.6% | 1.02 | 0.99 | 0.964 | 0.694 |

| Electricity transmission | Investment: transmission capacity | 644 | 90 | 6% | 1.5% | 4.2% | 0.64 | 0.61 | 0.53 | 0.5 |

| Electricity transmission | Transmission of clean power | 52 | 7 | 14% | 0.3% | 0.3% | 0.052 | 0.046 | 0.04 | 0.04 |

| Energy storage | Investment: Pumped hydro | 53 | 7 | 5% | 0.1% | 0.3% | 0.05 | 0.05 | 0.04 | 0.03 |

| Energy storage | Investment: Grid-connected batteries | 232 | 32 | 52% | 3.3% | 1.5% | 0.232 | 0.152 | 0.08 | 0.02 |

| Energy storage | Investment: Electrolysers | 11 | 2 | 29% | 0.1% | 0.1% | 0.011 | 0.009 | 0 | 0 |

| Energy efficiency | Revenue: Energy service companies | 620 | 86 | 17% | 3.8% | 4.0% | 0.62 | 0.528003 | 0.52 | 0.45 |

| Total | Investments | 7,198 | 1001 | 15% | 38.2% | 46.7% | 7.20 | 6.28 | 6.00 | 4.11 |

| Total | Production of goods and services | 8,216 | 1,143 | 22% | 61.8% | 53.3% | 8.22 | 6.73 | 5.58 | 4.32 |

| Total | Total GDP contribution | 15,414 | 2144 | 18% | 100.0% | 100.0% | 15.41 | 13.01 | 11.58 | 8.42 |

EVs and batteries were the largest drivers of GDP growth

In 2024, EVs and solar had been the largest growth drivers. In 2025, it was EVs and batteries, which delivered 44% of the economic impact and more than half of the growth of the clean-energy industries. This was due to strong growth in both output and investment.

The contribution to nominal GDP growth – unadjusted for inflation – was even larger, as EV prices held up year-on-year while the economy as a whole suffered from deflation. Investment in battery manufacturing rebounded after a fall in 2024.

The major contribution of EVs and batteries is illustrated in the figure below, which shows both the overall size of the clean-energy economy and the sectors that added the most to the rise from year to year.

The next largest subsector was clean-power generation, transmission and storage, which made up 40% of the contribution to GDP and 30% of the growth in 2025.

Within the electricity sector, the largest drivers were growth in investment in wind and solar power generation capacity, along with growth in power output from solar and wind, followed by the exports of solar-power equipment and materials.

Investment in solar-panel supply chains, a major growth driver in 2022-23, continued to fall for the second year. This was in line with the government’s efforts to rein in overcapacity and “irrational” price competition in the sector.

Finally, rail transportation was responsible for 12% of the total economic output of the clean-energy sectors, but saw relatively muted growth year-on-year, with revenue up 3% and investment by 6%.

Note that the International Energy Agency (IEA) world energy investment report projected that China invested $627bn in clean energy in 2025, against $257bn in fossil fuels.

For the same sectors as the IEA report, this analysis puts the value of clean-energy investment in 2025 at a significantly more conservative $430bn. The higher figures in this analysis overall are therefore the result of wider sectoral coverage.

Electric vehicles and batteries

EVs and vehicle batteries were again the largest contributors to China’s clean-energy economy in 2025, making up an estimated 44% of value overall.

Of this total, the largest share of both total value and growth came from the production of battery EVs and plug-in hybrids, which expanded 29% year-on-year. This was followed by investment into EV manufacturing, which grew 18%, after slower growth rates in 2024.

Investment in battery manufacturing also rebounded after a drop in 2024, driven by new battery technology and strong demand from both domestic and international markets. Battery manufacturing investment grew by 35% year-on-year to 277bn yuan.

The share of electric vehicles (EVs) will have reached 12% of all vehicles on the road by the end of 2025, up from 9% a year earlier and less than 2% just five years ago.

The share of EVs in the sales of all new vehicles increased to 48%, from 41% in 2024, with passenger cars crossing the 50% threshold. In November, EV sales crossed the 60% mark in total sales and they continue to drive overall automotive sales growth, as shown below.

Electric trucks experienced a breakthrough as their market share rose from 8% in the first nine months of 2024 to 23% in the same period in 2025.

Policy support for EVs continues, for example, with a new policy aiming to nearly double charging infrastructure in the next three years.

Exports grew even faster than the domestic market, but the vast majority of EVs continue to be sold domestically. In 2025, China produced 16.6m EVs, rising 29% year-on-year. While exports accounted for only 21% or 3.4m EVs, they grew by 86% year-on-year. Top export destinations for Chinese EVs were western Europe, the Middle East and Latin America.

The value of batteries exported also grew rapidly by 41% year-on-year, becoming the third largest growth driver of the GDP. Battery exports largely went to western Europe, north America and south-east Asia.

In contrast with deflationary trends in the price of many clean-energy technologies, average EV prices have held up in 2025, with a slight increase in average price of new models, after discounts. This also means that the contribution of the EV industry to nominal GDP growth was even more significant, given that overall producer prices across the economy fell by 2.6%. Battery prices continued to drop.

Clean-power generation

The solar power sector generated 19% of the total value of the clean-energy industries in 2025, adding 2.9tn yuan ($41bn) to the national economy.

Within this, investment in new solar power plants, at 1.2tn yuan ($160bn), was the largest driver, followed by the value of solar technology exports and by the value of the power generated from solar. Investment in manufacturing continued to fall after the wave of capacity additions in 2023, reaching 0.5tn yuan ($72bn), down 23% year-on-year.

In 2025, China achieved another new record of wind and solar capacity additions. The country installed a total of 315GW solar and 119GW wind capacity, adding more solar and two times as much wind as the rest of the world combined.

Clean energy accounted for 90% of investment in power generation, with solar alone covering 50% of that. As a result, non-fossil power made up 42% of total power generation, up from 39% in 2024.

However, a new pricing policy for new solar and wind projects and modest targets for capacity growth have created uncertainty about whether the boom will continue.

Under the new policy, new clean-power generation has to compete on price against existing coal power in markets that place it at a disadvantage in some key ways.

At the same time, the electricity markets themselves are still being introduced and developed, creating investment uncertainty.

Investment in solar power generation increased year-on-year by 15%, but experienced a strong stop-and-go cycle. Developers rushed to finish projects ahead of the new pricing policy coming into force in June and then again towards the end of the year to finalise projects ahead of the end of the current 14th five-year plan.

Investment in the solar sector as a whole was stable year-on-year, with the decline in manufacturing capacity investment balanced by continued growth in power generation capacity additions. This helped shore up the utilisation of manufacturing plants, in line with the government’s aim to reduce “disorderly” price competition.

By late 2025, China’s solar manufacturing capacity reached an estimated 1,200GW per year, well ahead of the global capacity additions of around 650GW in 2025. Manufacturers can now produce far more solar panels than the global market can absorb, with fierce competition leading to historically low profitability.

China’s policymakers have sought to address the issue since mid-2024, warning against “involution”, passing regulations and convening a sector-wide meeting to put pressure on the industry. This is starting to yield results, with losses narrowing in the third quarter of 2025.

The volume of exports of solar panels and components reached a record high in 2025, growing 19% year-on-year. In particular, exports of cells and wafers increased rapidly by 94% and 52%, while panel exports grew only by 4%.

This reflects the growing diversification of solar-supply chains in the face of tariffs and with more countries around the world building out solar panel manufacturing capacity. The nominal value of exports fell 8%, however, due to a fall in average prices and a shift to exporting upstream intermediate products instead of finished panels.

Hydropower, wind and nuclear were responsible for 15% of the total value of the clean-energy sectors in 2025, adding some 2.2tn yuan ($310bn) to China’s GDP in 2025.

Nearly two-thirds of this (1.3tn yuan, $180bn) came from the value of power generation from hydropower, wind and nuclear, with investment in new power generation projects contributing the rest.

Power generation grew 33% from solar, 13% from wind, 3% from hydropower and 8% from nuclear.

Within power generation investment, solar remained the largest segment by value – as shown in the figure below – but wind-power generation projects were the largest contributor to growth, overtaking solar for the first time since 2020.

In particular, offshore wind power capacity investment rebounded as expected, doubling in 2025 after a sharp drop in 2024.

Investment in nuclear projects continued to grow but remains smaller in total terms, at 17bn yuan. Investment in conventional hydropower continued to decline by 7%.

Electricity storage and grids

Electricity transmission and storage were responsible for 6% of the total value of the clean-energy sectors in 2025, accounting for 1.0 tn yuan ($140bn).

The most valuable sub-segment was investment in power grids, growing 6% in 2025 and reaching $90bn. This was followed by investment in energy storage, including pumped hydropower, grid-connected battery storage and hydrogen production.

Investment in grid-connected batteries saw the largest year-on-year growth, increasing by 50%, while investments in electrolysers also grew by 30%. The transmission of clean power increased an estimated 13%, due to rapid growth in clean-power generation.

China’s total electricity storage capacity reached more than 213GW, with battery storage capacity crossing 145GW and pumped hydro storage at 69GW. Some 66GW of battery storage capacity was added in 2025, up 52% year-on-year and accounting for more than 40% of global capacity additions.

Notably, capacity additions accelerated in the second half of the year, with 43GW added, compared with the first half, which saw 23GW of new capacity.

The battery storage market initially slowed after the renewable power pricing policy, which banned storage mandates after May, but this was quickly replaced by a “market-driven boom”. Provincial electricity spot markets, time-of-day tariffs and increasing curtailment of solar power all improved the economics of adding storage.

By the end of 2025, China’s top five solar manufacturers had all entered the battery storage market, making a shift in industry strategy.

Investment in pumped hydropower continued to increase, with 15GW of new capacity permitted in the first half of 2025 alone and 3GW entering operation.

Railways

Rail transportation made up 12% of the GDP contribution of the clean-energy sectors, with revenue from passenger and goods rail transportation the largest source of value. Most growth came from investment in rail infrastructure, which increased 6% year-on-year

The electrification of transport is not limited to EVs, as rail passenger, freight and investment volumes saw continued growth. The total length of China’s high-speed railway network reached 50,000km in 2025, making up more than 70% of the global high-speed total.

Energy efficiency

Investment in energy efficiency rebounded strongly in 2025. Measured by the aggregate turnover of large energy service companies (ESCOs), the market expanded by 17% year-on-year, returning to growth rates last seen during 2016-2020.

Total industry turnover has also recovered to its previous peak in 2021, signalling a clear turnaround after three years of weakness.

Industry projections now anticipate annual turnover reaching 1tn yuan in annual turnover by 2030, a target that had previously been expected to be met by 2025.

China’s ESCO market has evolved into the world’s largest. Investment within China’s ESCO market remains heavily concentrated in the buildings sector, which accounts for around 50% of total activity. Industrial applications make up a further 21%, while energy supply, demand-side flexibility and energy storage together account for approximately 16%.

Implications of China’s clean-energy bet

Ongoing investment of hundreds of billions of dollars into clean-energy manufacturing represents a gigantic economic and financial bet on a continuing global energy transition.

In addition to the domestic investment covered in this article, Chinese firms are making major investments in overseas manufacturing.

The clean-energy industries have played a crucial role in meeting China’s economic targets during the five-year period ending this year, delivering an estimated 40%, 25% and 37% of all GDP growth in 2023, 2024 and 2025, respectively.

However, the developments next year and beyond are unclear, particularly for solar power generation, with the new pricing system for renewable power generation leading to a short-term slowdown and creating major uncertainty, while central government targets have been set far below current rates of clean-electricity additions.

Investment in solar-power generation and solar manufacturing declined in the second half of the year, while investment in generation clocked growth for the full year, showing the risk to the industries under the current power market set-ups that favour coal-fired power.

The reduction in the prices of clean-energy technology has been so dramatic that when the prices for GDP statistics are updated, the sectors’ contribution to real GDP – adjusted for inflation or, in this case deflation – will be revised down.

Nevertheless, the key economic role of the industry creates a strong motivation to keep the clean-energy boom going. A slowdown in the domestic market could also undermine efforts to stem overcapacity and inflame trade tensions by increasing pressure on exports to absorb supply.

A recent CREA survey of experts working on climate and energy issues in China found that the majority believe that economic and geopolitical challenges will make the “dual carbon” goals – and with that, clean-energy industries – only more important.

Local governments and state-owned enterprises will also influence the outlook for the sector. Their previous five-year plans played a key role in creating the gigantic wind and solar power “bases” that substantially exceeded the central government’s level of ambition.

Provincial governments also have a lot of leeway in implementing the new electricity markets and contracting systems for renewable power generation. The new five-year plans, to be published this year, will therefore be of major importance.

About the data

Reported investment expenditure and sales revenue has been used where available. When this is not available, estimates are based on physical volumes – gigawatts of capacity installed, number of vehicles sold – and unit costs or prices.

The contribution to real growth is tracked by adjusting for inflation using 2022-2023 prices.

All calculations and data sources are given in a worksheet.

Estimates include the contribution of clean-energy technologies to the demand for upstream inputs such as metals and chemicals.

This approach shows the contribution of the clean-energy sectors to driving economic activity, also outside the sectors themselves, and is appropriate for estimating how much lower economic growth would have been without growth in these sectors.

Double counting is avoided by only including non-overlapping points in value chains. For example, the value of EV production and investment in battery storage of electricity is included, but not the value of battery production for the domestic market, which is predominantly an input to these activities.

Similarly, the value of solar panels produced for the domestic market is not included, as it makes up a part of the value of solar power generating capacity installed in China. However, the value of solar panel and battery exports is included.

In 2025, there was a major divergence between two different measures of investment. The first, fixed asset investment, reportedly fell by 3.8%, the first drop in 35 years. In contrast, gross capital formation saw the slowest growth in that period but still inched up by 2%.

This analysis uses gross capital formation as the measure of investment, as it is the data point used for GDP accounting. However, the analysis is unable to account for changes in inventories, so the estimate of clean-energy investment is for fixed asset investment in the sectors.

The analysis does not explicitly account for the small and declining role of imports in producing clean-energy goods and services. This means that the results slightly overstate the contribution to GDP but understate the contribution to growth.

For example, one of the most important import dependencies that China has is for advanced computing chips for EVs. The value of the chips in a typical EV is $1,000 and China’s import dependency for these chips is 90%, which suggests that imported chips represent less than 3% of the value of EV production.

The estimates are likely to be conservative in some key respects. For example, Bloomberg New Energy Finance estimates “investment in the energy transition” in China in 2024 at $800bn. This estimate covers a nearly identical list of sectors to ours, but excludes manufacturing – the comparable number from our data is $600bn.

China’s National Bureau of Statistics says that the total value generated by automobile production and sales in 2023 was 11tn yuan. The estimate in this analysis for the value of EV sales in 2023 is 2.3tn yuan, or 20% of the total value of the industry, when EVs already made up 31% of vehicle production and the average selling prices for EVs was slightly higher than for internal combustion engine vehicles.

The post Analysis: Clean energy drove more than a third of China’s GDP growth in 2025 appeared first on Carbon Brief.

Analysis: Clean energy drove more than a third of China’s GDP growth in 2025

The state Senate’s version of the bill offers more opportunities for utilities to profit, leading some observers to question whether the legislation will substantively lower costs for customers.

In its most recent energy affordability legislation, the Maryland Senate has reversed key utility accountability proposals passed by the state House and added new ways for utility companies to earn profit, including by reviving a billion-dollar gas subsidy that requires all ratepayers to cover the cost of running new gas pipelines to housing developments.

Utility Accountability Bills Divide Maryland’s Democratic Leadership

Marcelo Behar is the COP30 Special Envoy for Bioeconomy and co-founder of Ambition Loop Brazil.

Can we be the generation to end the rampant deforestation that is harming the planet’s ecosystems and climate? Back in February, the Brazilian COP30 Presidency opened a call for submissions on its proposed Roadmap for Halting Deforestation and Forest Degradation, which closes today.

What might look like a technical step quickly drew significant attention, with more than 100 responses submitted by governments, civil society organisations, businesses and other stakeholders.

This level of engagement is telling. It reflects both the urgency of the issue and the recognition that this process could shape whether the global goal to end deforestation by 2030 finally moves from ambition to delivery.

As a Brazilian, I see this moment with both pride and realism. Brazil has played a central role in elevating forests on the climate agenda, and the COP30 Presidency has shown leadership in carrying this issue forward far beyond the Belém summit.

COP30 rainforest fund unlikely to make first payments until 2028

But last year also offered a sobering signal. Despite strong efforts from the Brazilian Presidency, the proposed roadmap did not secure consensus in the final outcome of COP30. That outcome underlined a simple truth: while there is broad recognition of the importance of forests, agreeing on how to move forward remains complex. The road ahead is still long and likely uneven.

That is precisely why this moment matters.

Progress on commitments falling short

The world is not short of commitments. Over the past decade, countries have repeatedly pledged to halt and reverse deforestation by 2030. There is a growing body of experience through the REDD+ (Reducing Emissions from Deforestation and Degradation) programme, including the emergence of jurisdictional approaches that are beginning to connect forest protection with finance at scale.

Initiatives such as the Forest and Climate Leaders’ Partnership have helped sustain political attention and cooperation among countries, while national strategies continue to evolve, and Indigenous Peoples and local communities remain at the forefront of protecting forests.

And yet, progress is still falling short.

The gap is not only one of alignment. It is also one of political will – and of having a credible, shared pathway that brings together these efforts in a way that drives implementation at scale.

Civil society is watching this process closely. For many organisations working across climate, nature and conservation, this is not just another initiative – it is a priority. After years of advocating to end deforestation, there is a strong sense that this moment cannot be lost. The expectation is clear: this roadmap must move beyond intention and help unlock real progress.

The opportunity now is to ensure that it does exactly that. This cannot become another report.

Implementation key to roadmap success

A detailed assessment of pathways and challenges, however valuable, will not be enough to change outcomes on the ground. What is needed is an implementation roadmap, one that connects existing commitments, aligns incentives and provides clarity on how to move from ambition to delivery between now and 2030.

The consultation process is an important step. But its value will ultimately be judged by what it produces.

If the roadmap is to succeed, several priorities should guide its development.

-

With no COP30 roadmap, hopes of saving forests hinge on voluntary initiatives

The world is falling short of a target to halt deforestation by 2030, but the “Amazon COP” failed to agree a concrete global plan to save rainforests despite backing by over 80 nations -

Deep in the Amazon, forest protection cash must vie with glitter of illegal gold

The TFFF fund launched at COP30 aims to pay communities to protect the rainforest, but will it be enough? On French Guiana’s border with Brazil, the profits to be had from mining are far higher

First: policy. It must be designed as a tool for implementation. That means going beyond diagnosis to define concrete action: who needs to act, by when, and how progress will be tracked. The solutions are not new, but coordination has been missing.

Second: accountability. It should bring coherence to the existing landscape. The value of a roadmap lies not in creating new commitments, but in connecting what already exists: global targets, REDD+ experience, national action plans, Indigenous leadership and supply chain initiatives. Reducing fragmentation is essential to accelerating delivery.

Early milestones needed

Third: finance. It must be grounded in economic reality. Halting deforestation will not happen without addressing the incentives that underpin it. Aligning public finance, private investment, and market demand with forest protection is not a technical detail; it is the core of the transition.

Fourth: transparency. Legitimacy will depend on openness. A credible roadmap cannot be developed behind closed doors. Governments, Indigenous Peoples and local communities, civil society, business and finance actors all have a role to play and must be able to see how their contributions shape the outcome.

Fifth: urgency. Progress must be visible in 2026. Without early milestones, momentum will fade. By the time climate negotiators gather in Bonn mid-year, the roadmap should have a clear structure, priority actions and growing political backing.

Governments must deliver on the plan

Finally, countries themselves will need to step forward. Last year’s outcome showed that support alone is not enough. Delivering this roadmap will require active political engagement. That means governments that are willing not only to participate in the process, but to help shape and implement it.

Brazil has created an important opening. It has also taken on the responsibility that comes with leadership: to help turn a widely supported idea into something that can deliver in practice.

The commitment to end deforestation by 2030 already exists. What is still needed is a path. And the courage to walk it.

The post How a Brazil-led roadmap can rescue global pledge to halt deforestation appeared first on Climate Home News.

How a Brazil-led roadmap can rescue global pledge to halt deforestation

A US biofuels producer that exports “green” aviation fuel to Britain and the European Union has purchased beef tallow from a Brazilian supply chain tied to illegal deforestation in the Amazon, shipping data and a court document show.

Diamond Green Diesel (DGD), a major provider of sustainable aviation fuel (SAF) and renewable diesel, has sourced hundreds of thousands of tonnes of beef tallow from Brazil, alongside waste fats from other sources, over the last three years, as global demand for biofuel feedstocks soars.

Reporting by Unearthed and nonprofit investigative outlet Repórter Brasil reveals DGD’s connection to a rendering plant that has sourced supplies from a meatpacker fined for buying cattle from an illegally deforested Amazon reserve. A previous investigation by Reuters and Repórter Brasil found DGD had bought animal fat from two other rendering factories linked to supplies of cattle from illegal ranches.

The newly identified factory, Pacífico Indústria e Comércio de Óleos e Proteínas Ltda, which is based in Cacoal, a small city in the far-western Amazon state of Rondônia, has been supplied by Rondônia meatpacker DistriBoi, a 2022 court document shows.

DistriBoi was fined two years ago for illegally purchasing cattle from the state’s Jaci-Paraná conservation reserve, which has been ravaged by illegal ranching.

There is no suggestion that the companies involved were aware of deforestation at farm level. But the findings suggest a traceability gap in the supply chain of feedstocks for sustainable fuels, where cattle by-products are subject to less oversight than the primary commodities of the cattle industry, such as meat and leather.

Pristine rainforest blanketed the Jaci-Paraná reserve when it was created 30 years ago to protect traditional forest activities such as rubber tapping and nut harvesting.

Today, illegal ranching has devoured nearly 80% of its forest cover and it has become a notorious example of the devastation wrought by land grabbers in the world’s largest rainforest.

“The damage to biodiversity has been devastating,” said local Indigenous activist Neidinha Suruí, who featured in the 2025 Emmy Award-winning documentary “O Território”.

“It is sad to see what has been lost,” she said.

Greener air travel?

The “renewable diesel” and sustainable aviation fuel (SAF) that are being exported by DGD – a joint venture between US oil refiner Valero Energy Corp and Texas-based Darling Ingredients – are classed as “green” because they are made from feedstocks classified as waste, including tallow, which consists of fat separated from cattle carcasses.

Many governments and airlines are pinning their hopes for greener flying on SAF made with organic waste materials, including Britain which introduced a compulsory blending requirement last year.

Top green jet fuel producer linked to suspect waste-oil supply chain

Air travel accounts for about 2.5% of global carbon emissions and in contrast to other transport sectors that can be electrified, shrinking aviation’s carbon footprint is much more difficult.

Waste products such as beef tallow and used cooking oil (UCO) are considered the greenest of viable SAF feedstocks on the grounds that they do not create competition with foodstuffs such as soy oil or palm oil, nor increase deforestation pressure.

But there is concern that the global rush to ramp up SAF use could indirectly exacerbate deforestation pressure by increasing demand for feedstocks such as tallow and UCO.

That could increase the profit margins of cattle ranches – including illegal ones – and have other unintended consequences, such as encouraging fraud in supply chains, as Climate Home News has reported.

An investigation published in March by Climate Home News and Swedish broadcaster SVT found that Finnish biofuels giant Neste is sourcing key ingredients for its SAF from an opaque supply chain that enables fresh palm oil to be passed off as used, waste oil.

Because tallow is classified as waste by regulators in markets including the UK and EU, the green fuel industry’s most widely used certification scheme – International Sustainability and Carbon Certification (ISCC) – does not assess whether forests were cleared to rear the cattle that produced it in the first place.

-

Amazon fires threaten initiatives to raise cash for rainforest protection

Brazil’s Tropical Forests Forever Facility (TFFF) and other innovative finance tools will be showcased at COP30, but surging wildfires in the Amazon pose a threat to their success, climate experts warn -

Deep in the Amazon, forest protection cash must vie with glitter of illegal gold

The TFFF fund launched at COP30 aims to pay communities to protect the rainforest, but will it be enough? On French Guiana’s border with Brazil, the profits to be had from mining are far higher -

Funding gap threatens next round of IPCC climate science reports, chair warns

The latest IPCC session in Bangkok was clouded by persistent differences over when its flagship reports should be published and concern over cost-cutting proposals

This allows tallow from cattle to qualify as a sustainable feedstock for green fuels, even if they were raised on illegally deforested land.

“There is clearly an oversight within the rules if the products, in this case animal tallow, are originally coming from deforested land,” said Cian Delaney, a campaign coordinator at the clean transport and energy advocacy group Transport & Environment.

That means government SAF mandates aimed at stemming air travel emissions could help boost the earnings of cattle ranchers linked to illegal deforestation in Brazil, where ranching and other forms of agriculture have been the main driver of forest loss.

Land grabbers clear way for ranchers

Once covered by an unbroken rainforest canopy, Rondônia’s Jaci-Paraná reserve has been decimated by illegal deforestation driven by cattle ranching – a major cause of tree loss in the Amazon.

Land-grabbers have seized – often violently – and cleared more than three-quarters of its forest for pasture, as ranching has steadily advanced into the southern Amazon.

Suruí, the local Indigenous activist, said companies that buy products derived from illegal activities perpetuate environmental crimes in the rainforest.

“If there were no meat processors buying illegally sourced cattle, there would be no land grabbing and no deforestation,” Suruí told Repórter Brasil, which partnered on the new investigation with Unearthed, and a team of journalists supported by JournalismFund Europe.

Lawsuits and linked supply chains

Brazilian President Luiz Inácio Lula da Silva has pledged to end all deforestation in the country by 2030, in part by strengthening environmental enforcement in the world’s biggest rainforest.

In Rondônia, authorities have launched more than 50 lawsuits related to land-grabbing and deforestation in the Jaci-Paraná reserve alone. Local slaughterhouse DistriBoi is named in 31 of the lawsuits, including the 2024 case in which it was fined.

According to the 2022 court document, which concerned an unrelated labour dispute, lawyers for Pacífico refer to DistriBoi as the rendering plant’s “largest supplier of raw materials”.

US-based DGD received almost 15,000 tonnes of tallow from Pacífico from 2023 to 2025 at its Texas refinery, as well as used cooking oil from various countries and sources, according to trade database Panjiva.

Darling Ingredients is also a parent company of Pacífico since its 2022 acquisition of Brazilian rendering company FASA Group.

A spokesperson for Darling Ingredients denied that Pacífico had sourced beef residues from DistriBoi’s Ji-Paraná slaughterhouse – one of two that the meatpacker operates in Rondônia.

“The rendering plant Pacífico does not source any materials from the slaughterhouse Distriboi in Ji-Paraná,” the spokesperson said in an emailed response, without providing evidence or commenting directly on the content of the 2022 court document.

Darling did not respond to a follow-up question about Distriboi’s other slaughterhouse in the region, which, according to cattle transfer documents, has also bought from a farm that has illegally cleared forest within the extractive reserve.

“Our relationships are typically with the slaughterhouse, several levels removed from cattle ranchers. Regardless, we are committed to ensuring our raw materials are deforestation free. We expect our raw material suppliers to abide by our supplier code of conduct. In addition, we are in the process of requiring all [the] raw materials to attest that their material is deforestation free,” the spokesperson said in a statement.

DistriBoi said in an apparent reference to the pending Jaci-Paraná lawsuits that “the matters mentioned … are already under review, including by higher courts”. It has previously denied wrongdoing. The company’s statement did not address a question about its commercial ties to Pacífico.

Valero Energy, the major refiner that co-owns DGD with Darling Ingredients, did not respond to requests for comment, nor did DGD itself.

From slaughterhouse to SAF

In an effort to rein in carbon emissions from air travel, regulators in Britain and the EU have mandated progressively increasing SAF blending quotas in the years ahead, creating a new market for feedstocks including beef tallow.

Brazil’s exports of tallow to the US have risen sharply in recent years, up from less than 10,000 tonnes in 2021 to almost 400,000 tonnes last year, according to Panjiva, reflecting growing demand for biofuels like SAF.

In the UK, Europe’s biggest aviation market by seat capacity, jet fuel was required to contain 2% SAF by the end of 2025, rising to 10% by 2030 and 22% by 2040.

DGD shipped 134,000 tonnes of SAF worth nearly $90 million from Texas to the UK in 2025, according to trade data from Panjiva. The company also exported smaller amounts of renewable diesel to Britain.

The EU received biofuels, including small quantities of SAF, worth over $1.1 billion from DGD’s Texas refinery last year, figures show.

Is the world’s big idea for greener air travel a flight of fancy?

Unearthed’s investigation could not identify which airlines or airports buy DGD’s SAF once it arrives in Britain.

Valero, DGD’s other parent company, is positioning itself as a key player in the transition to lower-carbon fuels in the UK, where it markets its renewable diesel under the Texaco brand.

It has been an active participant in SAF policy discussions and has criticised the government’s planned cap on waste fat sources in SAF, calling them “the world’s most cost-effective production route for SAF” in a submission to parliament.

Helping to cut emissions?

Even tighter oversight over SAF feedstocks is crucial to ensure that blending mandates such as Britain’s are effectively lowering emissions, said Anna Krajinska, a director at Transport & Environment UK.

Forests store vast amounts of carbon; when they are cut down or burned this carbon is released into the atmosphere.

“If there’s tallow coming from land that’s been deforested, then those emissions might be so high that you might not be getting to the greenhouse gas reduction threshold,” Krajinska said.

But as the world’s appetite for flying keeps on growing, some experts say SAF is the only viable means to reduce aviation emissions at present.

Referring to the deforestation links identified in Unearthed’s investigation, Wouter Dewulf, an aviation economist at Belgium’s University of Antwerp, said it “would be important to assess how large this infraction is”.

“I’m quite sure you have aberrations,” Dewulf added. “But biofuels are the best alternative for the moment.”

T&E’s Delaney said there needs to be less opacity and better oversight from regulatory authorities. “Right now, there are just too many blindspots,” he added.

The post UK imports of “green” jet fuel linked to Amazon deforestation appeared first on Climate Home News.

UK imports of “green” jet fuel linked to Amazon deforestation

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits