* Disseminated on behalf of ARMR Sciences Inc.

* For Accredited Investors Only. Offered pursuant to Rule 506(c). Reasonable steps to verify accreditation will be taken before any sale.

PAID ADVERTISEMENT – SPONSORED CONTENT

Artificial intelligence (AI) is helping transform medicine, finance, and logistics. But experts warn it could also be turned against us. With advanced modeling, AI can now generate chemical blueprints at a substantially faster rate than previously available processes. As a result, National security leaders and AI thought leaders (including OpenAI’s Sam Altman), have voiced concerns that adversaries could weaponize AI to design new bioweapons.

The New Threat Landscape

Fentanyl already stands as the deadliest synthetic opioid in U.S. history, responsible for more than 220 deaths every day. But fentanyl itself is only the beginning.

Analogs like carfentanil (100x stronger), xylazine (non-opioid threat), and nitazenes (40x stronger) are beginning to spread, many of which are not reversible with Narcan.

The drug supply is becoming a testing ground for increasingly lethal compounds, some of which could be accelerated by AI-driven chemistry.

This dual challenge – lethal analogs on the street and the potential for AI-designed agents – has led federal agencies, including the Department of Defense and Homeland Security, to classify fentanyl and its cousins as chemical weapons of mass destruction.

The crisis is no longer just a health issue; it is a national security emergency.

ARMR’s Defense Labs Approach

ARMR Sciences is working to position itself to confront this next phase. Its Defense Labs initiative combines AI-powered drug discovery with seven years of Department of Defense–funded science with the goal of building a scalable biodefense platform.

The company’s lead candidate, ARMR-100, designed to train the immune system to block fentanyl before it reaches the brain. In preclinical (animal) studies, ARMR-100 blocked 92% of fentanyl’s entry into the brain and eliminated its addictive behavioral effects (at this stage ARMR-100 is not FDA-approved, human safety and efficacy have not been established, and preclinical results may not predict clinical outcomes).

Unlike reactive tools such as naloxone, ARMR-100 is designed to provide months of protection – a biochemical shield against fentanyl and, eventually, other engineered analogs.

Beyond fentanyl, ARMR plans to develop additional immunotherapies for xylazine, nitazenes, and other emerging threats, creating a portfolio that evolves alongside the risks.

By leveraging AI in its own labs, ARMR seeks to stay ahead of adversaries who might misuse the same technology. And in the battle between innovation and misuse, its proactive biodefense may prove to be America’s strongest shield.

The Scale and the Urgency

With more than 130 million people in the U.S. considered high-risk – from opioid use disorder patients to first responders and military personnel – the potential market is vast.

For policymakers, the message is clear: synthetic opioids are no longer only a health crisis, but a recognized national security threat. Classified alongside terrorism and cyberwarfare, fentanyl and its analogs demand rapid action.

This urgency is creating bipartisan momentum for federal funding, regulatory fast-tracking, and stockpiling of new countermeasures.

Why Investors Should Pay Attention

For investors, we believe that ARMR represents an opportunity to back a company that combines social impact with growth potential. Its model combines biotechnology, AI, and biodefense – a convergence few companies are addressing:

- Seven years of DoD-backed research formed the platform’s foundation

- Lead candidate ARMR-100 blocked 92% of fentanyl from entering the brain in preclinical studies

- A $30M private raise is now open

- A targeted exchange listing in the future

By investing in this round, investors have a chance to support ARMR as it works to build a category-defining role in AI-powered biodefense.

* For Accredited Investors Only. This offering is made pursuant to Rule 506(c) of Regulation D. All purchasers must be accredited investors, and the issuer will take reasonable steps to verify accredited status before any sale. Investing involves high risk, including the potential loss of your entire investment.

* This is a paid advertisement for ARMR’s private offering. Please read the details of the offering at InvestARMR.com for additional information on the company and the risk factors related to the offering.

* For investors from Canada: This advertisement forms part of the issuer’s marketing materials and is incorporated by reference into the issuer’s Offering Memorandum/Private Placement Memorandum under NI 45-106. Investors must receive and review the OM/PPM and execute the prescribed Form 45-106F4 Risk Acknowledgement before subscribing.

DISCLOSURES & DISCLAIMERS

CLIENT CONTENT: Carboncredits.com is not responsible for any content hosted on ARMR Sciences’ sites; it is ARMR Sciences’ responsibility to ensure compliance with applicable laws.

NOT INVESTMENT ADVICE: Content is for educational, informational, and advertising purposes only and should NOT be construed as securities-related offers or solicitations. All content should be considered promotional and subject to disclosed conflicts of interest.

Do NOT rely on this as personalized investment advice. Do your own due diligence.

Carboncredits.com strongly recommends you consult a licensed or registered professional before making any investment decision.

REGULATORY STATUS: Neither Carboncredits.com nor any of its owners or employees is registered as a securities broker-dealer, broker, investment advisor, or IA representative with the U.S. Securities and Exchange Commission, any state securities regulatory authority, or any self-regulatory organization.

CONTENT & COMPENSATION DISCLOSURE: Carboncredits.com has received compensation of thirty thousand dollars from ARMR Sciences for this sponsored content. You should assume we receive compensation as indicated for any purchases through links in this email via affiliate relationships, direct/indirect payments from companies or third parties who may own stock in or have other interests in promoted companies. We may purchase, sell, or hold long or short positions without notice in securities mentioned in this communication.

RESULTS NOT TYPICAL: Past performance and results are unverified and NOT indicative of future results. Results presented are NOT guaranteed as TYPICAL. Market conditions and individual circumstances vary significantly. Actual results will vary widely. Investing in securities is speculative and carries high risk; you may lose some, all, or possibly more than your original investment.

HIGH-RISK: Securities discussed may be highly speculative investments subject to extreme volatility, limited liquidity, and potential total loss. The Securities are suitable only for persons who can afford to lose their entire investment. Furthermore, investors must understand that such investment could be illiquid for an indefinite period of time. No public market currently exists for the securities, and if a public market develops, it may not continue.

DISCLAIMERS & CAUTIONARY STATEMENT: Certain statements in this presentation (the “Presentation”) may be deemed to be “forward-looking statements” within the meaning of Section 27A of the 1933 Securities Act and Section 21E of the Exchange Act of 1934, as amended, and are intended to be covered by the safe harbor provisions for forward-looking statements. Such forward-looking statements can be identified by the use of words such as ”should,” ”may,” ”intends,” ”anticipates,” ”believes,” ”estimates,” ”projects,” ”forecasts,” ”expects,” ”plans,” and ”proposes.” Forward-looking statements, which are based on the current plans, forecasts and expectations of management of ARMR Sciences Inc. (the “Company” or “ARMR Sciences”), are inherently less reliable than historical information. Forward-looking statements are subject to risks and uncertainties, including events and circumstances that may be outside our control.

Although management believes that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from such forward-looking statements. Risks and uncertainties that could cause actual results to differ materially include, without limitation, those risks identified in the Private Placement Memorandum. Forward-looking statements speak only as of the date of the document in which they are contained, and ARMR Sciences Inc. does not undertake any duty to update any forward-looking statements except as may be required by law.

Any forward-looking financial forecasts contained in this Presentation are subject to a number of risks and uncertainties, and actual results may differ materially. You are cautioned not to place undue reliance on such forecasts. No assurances can be given that the future results indicated, whether expressed or implied, will be achieved. While sometimes presented with numerical specificity, all such forecasts are based upon a variety of assumptions that may not be realized, and which are highly variable. Because of the number and range of the assumptions underlying any such forecasts, many of which are subject to significant uncertainties and contingencies that are beyond the reasonable control of the issuing company, many of the assumptions inevitably will not materialize and unanticipated events and circumstances may occur subsequent to the date of any financial forecast.

ARMR Sciences Inc. takes no responsibility for any forecasts contained within the Presentation. None of the information contained in any offering materials should be regarded as a representation by ARMR Sciences Inc. The Company’s forecasts have not been prepared with a view toward public disclosure or compliance with the guidelines of the SEC, the American Institute of Certified Public Accountants or the Public Company Accounting Oversight Board. Independent public accountants have not examined nor compiled any forecasts and have not expressed an opinion or assurance with respect to the figures.

This Presentation also contains estimates and other statistical data made by independent parties and by management relating to market size and other data about our industry. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates.

ARMR Sciences Inc. is currently undertaking a private placement offering of Offered Shares pursuant to Section 4(a)(2) of the 1933 Act and/or Rule 506(c) of Regulation D promulgated thereunder. Investors should consider the investment objectives, risks, and investment time horizon of the Company carefully before investing. The private placement memorandum relating to the offering of Securities will contain this and other information concerning the Company, including risk factors, which should be read carefully before investing.

The Securities are being offered and sold in reliance on exemptions from registration under the 1933 Act. In accordance therewith, you should be aware that (i) the Securities may be sold only to “accredited investors,” as defined in Rule 501 of Regulation D; (ii) the Securities will only be offered in reliance on an exemption from the registration requirements of the Securities Act and will not be required to comply with specific disclosure requirements that apply to registration under the Securities Act; (iii) the United States Securities and Exchange Commission (the “SEC”) will not pass upon the merits of or give its approval to the terms of the Securities or the offering, or the accuracy or completeness of any offering materials; (iv) the Securities will be subject to legal restrictions on transfer and resale and investors should not assume they will be able to resell their securities; and (v) investing in these Securities involves a high degree of risk, and investors should be able to bear the loss of their entire investment. Furthermore, investors must understand that such investment could be illiquid for an indefinite period of time.

The Company is “Testing the Waters” under Regulation A under the Securities Act of 1933. The Company is not under any obligation to make an offering under Regulation A. No money or other consideration is being solicited in connection with the information provided, and if sent in response, will not be accepted. No offer to buy the securities can be accepted and no part of the purchase price can be received until an offering statement on Form 1-A has been filed and until the offering statement is qualified pursuant to Regulation A of the Securities Act of 1933, as amended, and any such offer may be withdrawn or revoked, without obligation or commitment of any kind, at any time before notice of its acceptance given after the qualification date.

The securities offered using Regulation A are highly speculative and involve significant risks. The investment is suitable only for persons who can afford to lose their entire investment. Furthermore, investors must understand that such investment could be illiquid for an indefinite period of time. No public market currently exists for the securities, and if a public market develops following the offering, it may not continue. The Company intends to list its securities on a national exchange and doing so entails significant ongoing corporate obligations including but not limited to disclosure, filing and notification requirements, as well compliance with applicable continued quantitative and qualitative listing standards.

The post AI and Biodefense – Working to Stay Ahead of Synthetic Drug Threats appeared first on Carbon Credits.

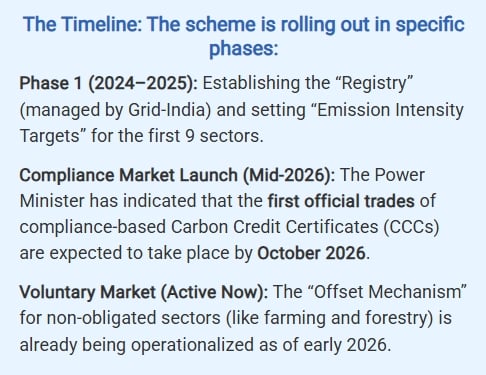

India has taken a major step toward building a working carbon market. The government has launched the Indian Carbon Market Portal, a central digital platform that will support the Carbon Credit Trading Scheme, or CCTS. With this move, India is no longer just designing its carbon market on paper. It is now putting the system into action.

The portal was launched at the International Conference on Carbon Markets, Prakriti 2026, held in New Delhi. Union Power Minister Manohar Lal said formal trading in carbon credit certificates is expected to begin within four months. That timeline makes the launch especially important. It shows that India is moving quickly from policy design to actual market operations.

The new portal will become the main platform for registration, monitoring, reporting, and verification of emissions. In simple terms, it will handle the back-end system needed to run a national carbon market. Companies that want to participate will need to register through the portal before they can trade carbon credits.

From Act to Action: India’s Carbon Market Story

2022: Laying the Foundation

India did not build this market overnight. The foundation was laid in 2022, when Parliament passed amendments to the Energy Conservation Act, 2001. These changes gave the government the legal power to create a carbon market and issue carbon credit certificates. That amendment was the first major sign that India wanted a structured, national system for carbon trading.

2023: Introducing the Carbon Credit Trading Scheme (CCTS)

After that, policymakers worked on the framework needed to turn the idea into reality. In 2023, the government formally introduced the Carbon Credit Trading Scheme. The CCTS created the core structure of the Indian Carbon Market and defined the roles of the institutions that would run it. It also set up the National Steering Committee for the Indian Carbon Market to oversee the framework.

This step mattered because carbon markets need strong governance to work properly. Without clear rules, trusted oversight, and proper measurement systems, trading can lose credibility. India’s approach has been to first build the rules and institutions and then move toward implementation.

Why the Portal Matters for Companies, Offsets, and Climate Goals

This structure fits India’s economy well. The country is still growing fast, and many industries are expanding. So instead of placing a fixed cap on total emissions right away, the system rewards firms that improve carbon efficiency. If a company performs better than its assigned greenhouse gas emission intensity target, it earns carbon credit certificates. If it falls short, it must buy credits from others.

That approach gives the industry some breathing room while still pushing it toward cleaner operations. It also sends a clear financial signal. The lower a company’s emissions intensity, the better its chance of earning value from the market. Over time, this can encourage investments in cleaner fuels, better equipment, energy efficiency, and modern industrial processes.

The compliance market will first cover large industrial units in energy-intensive sectors. These are the industries where emissions are high and where efficiency gains can make a real difference. By focusing first on major emitters, India is trying to create a market that targets the most important sources of industrial emissions.

The Indian Carbon Market Portal is important because it brings all parts of the system together in one place. The Bureau of Energy Efficiency, or BEE, will oversee the portal and the wider market. Through the platform, authorities will assess emissions data, track compliance obligations, and manage the issue and trade of surplus certificates.

That means the portal is not just a registration website. It is the digital backbone of the whole market. It supports the monitoring, reporting, and verification process, often called MRV. This part is critical because carbon markets only work when emissions data is accurate, transparent, and trusted. If the numbers are weak, the market cannot function properly. So the portal plays a central role in building credibility.

Voluntary Carbon Credits Expand India’s Market Reach

Along with the compliance market, India is also developing a voluntary offset market under the CCTS. This part of the system is open to a wider group of projects and participants. It allows eligible climate projects to generate carbon credits that can be traded.

This is an important feature because it expands the market beyond large industrial companies. It gives project developers, clean energy players, and other climate-focused businesses a chance to participate. In turn, that can help bring more investment into low-carbon activities across the economy.

The government has already approved several methodologies for voluntary carbon credit generation. These methodologies set the rules for how emissions reductions are measured and verified. They are essential because credits have value only when buyers trust that the reductions are real.

On March 28, 2025, India’s Ministry of Power approved 8 crediting methodologies for generating voluntary carbon credits, including:

- Renewable Energy

- Green Hydrogen Production

- Industrial Energy Efficiency

- Mangrove Afforestation and Reforestation

Supporting India’s Net Zero Goal

India’s carbon market also supports the country’s wider climate commitments. India has pledged to reduce the emissions intensity of its economy by 45% from 2005 levels by 2030. It has also committed to reaching net zero by 2070. A carbon market can help support both goals by encouraging industries to reduce emissions flexibly and cost-effectively.

At the same time, the market may help Indian companies deal with external carbon rules such as the European Union’s Carbon Border Adjustment Mechanism, or CBAM. As global trade becomes more carbon-conscious, Indian exporters may need stronger emissions data and proof of climate compliance. A domestic carbon market can help improve both.

The launch also fits into a bigger policy trend. India has recently placed more attention on industrial decarbonization, including support for carbon capture, utilisation, and storage in hard-to-abate sectors. This shows that the government is not relying on one solution alone. Instead, it is building a broader climate strategy that combines regulation, technology, finance, and market incentives.

In conclusion, India’s move comes at a time when climate regulation is becoming more important not only at home but also in global trade. A strong domestic carbon market can help Indian industries improve emissions tracking, manage compliance, and prepare for international carbon pricing systems. That gives the portal a much bigger role than just administration. It could become a key tool in India’s low-carbon growth story.

The post India’s Carbon Market Portal Goes Live as Carbon Credit Trading Nears appeared first on Carbon Credits.

Google has taken a major step in reshaping how large energy users interact with the power grid. The company has secured 1 gigawatt (GW) of demand response capacity across its U.S. data center operations with several utility partners. This allows Google to cut or shift electricity use during high demand. It helps stabilize the grid and reduce system costs.

The scale is significant. One gigawatt is roughly enough to power about 750,000 U.S. homes for a year. Demand response helps reduce peak power needs, which can cut grid strain during extreme heat or cold. It also reduces the need for expensive “peaker” plants that run only a few hours per year.

The company noted:

“Demand response enables our data centers to be valuable assets for the power grid. Our ability to shift or reduce our energy demand can help utility companies balance supply and demand and plan for future capacity needs. These agreements create a smart solution to make the electricity systems that serve our data centers more affordable and reliable.”

Demand Response: Turning Data Centers into Flexible Grid Assets

Google’s move reflects a growing challenge. U.S. electricity demand is rising fast. Data centers, especially those running artificial intelligence (AI) and cloud computing, are among the fastest‑growing power loads.

At the same time, building new power supply and grid infrastructure can take five to ten years or more. Google’s strategy bridges this gap by making demand more flexible instead of only increasing supply.

Demand response is a system where large electricity users reduce or shift power use during peak periods. Instead of running at full capacity all the time, facilities adjust operations based on grid conditions. This helps balance supply and demand in real time.

Google applies this by managing its data center workloads. It can delay or shift energy‑intensive tasks, especially machine learning and batch computing, to times when electricity demand is lower. This reduces energy use during peak grid stress without affecting performance.

It also turns data centers into flexible energy assets rather than fixed loads. Traditionally, grids treat demand as constant. Google’s model changes that assumption.

The company has built this system through agreements with multiple U.S. utilities, including:

- Tennessee Valley Authority (TVA)

- Indiana Michigan Power

- Entergy Arkansas

- Minnesota Power

- DTE Energy

These partnerships let grid operators ask Google to cut demand during stressful times, like heat waves or winter peaks. This helps keep the system reliable without just depending on backup generation.

Why Peak Demand Matters for Costs and Reliability

The timing of this move is critical. The U.S. Department of Energy projects that electricity demand could grow 20% or more by 2030, driven by electrification and digital services.

Data centers are a major part of this growth. With AI workloads increasing rapidly, total data center energy use rose over 20% between 2020 and 2025 in the U.S., according to industry studies.

At the same time, grid expansion faces delays. Building new transmission lines or power plants can take years or even decades due to permitting, siting, and cost challenges. Demand response offers a faster solution that can be deployed now.

Google notes that flexible demand can help utilities:

- Balance supply and demand in real time,

- Avoid building rarely used “peaker” plants,

- Reduce stress on transmission systems, and

- Lower wholesale electricity prices during peaks.

Even small flexibility gains can have large system‑wide effects. Research from the Electric Power Research Institute (EPRI) suggests that demand response programs could reduce peak load by 10–20% in many regions, leading to significant savings in infrastructure costs.

This is because peak demand drives infrastructure spending. Power systems are often built to meet only a few hours of extreme demand each year. Reducing those peaks can delay or avoid costly investments in generation and transmission.

Cost Savings and Reliability Gains

Google’s demand response strategy targets two key outcomes: lower costs and improved reliability.

- First, cost reduction. Peak demand periods often coincide with the highest wholesale electricity prices. By lowering demand during those hours, both Google and utilities can save money. These savings can help stabilize electricity prices for businesses and households alike.

- Second, reliability. Power grids face increasing pressure from extreme weather, electrification of transport and buildings, and higher loads from digital infrastructure. Demand response adds flexibility that helps prevent outages when supply is tight.

Google’s system allows it to cut the load quickly when needed. This gives grid operators more tools during tight supply conditions. It also reduces the risk of blackouts and emergency calls for conservation.

Importantly, this approach does not reduce overall energy use over time. Instead, it shifts when energy is used. This makes the system more efficient without limiting long‑term growth in data center activity or other demand.

SEE MORE:

- Google Taps Earth’s Heat in 150MW Geothermal Deal with Ormat Technologies to Power Data Centers

- Google Pledges $50M to Fight Superpollutants by 2030: A Near-Term Climate Game Changer

A Shift in Energy Strategy for Big Tech

Google’s move reflects a broader shift across the technology sector. Large tech companies are no longer just energy consumers. They are becoming active participants in energy systems.

This change is driven by several trends:

- Rapid growth in AI workloads that require large computing resources;

- Rising energy costs that pressure operating margins;

- Corporate climate targets tied to investor and public expectations; and

- Pressure to secure a reliable power supply amid grid uncertainty.

Demand response is now joining renewable energy procurement as a core strategy. Google has already invested heavily in solar, wind, geothermal, and energy storage. The company regularly ranks among the top corporate buyers of renewable energy, which helps avoid emissions.

Other industries have used demand response for years, including manufacturing and heavy industry. However, its use in data centers is still new. The scale of Google’s 1 GW deployment signals that this model could expand quickly and be adopted by other large energy users.

Linking Demand Response to Google’s 24/7 Carbon-Free Goals

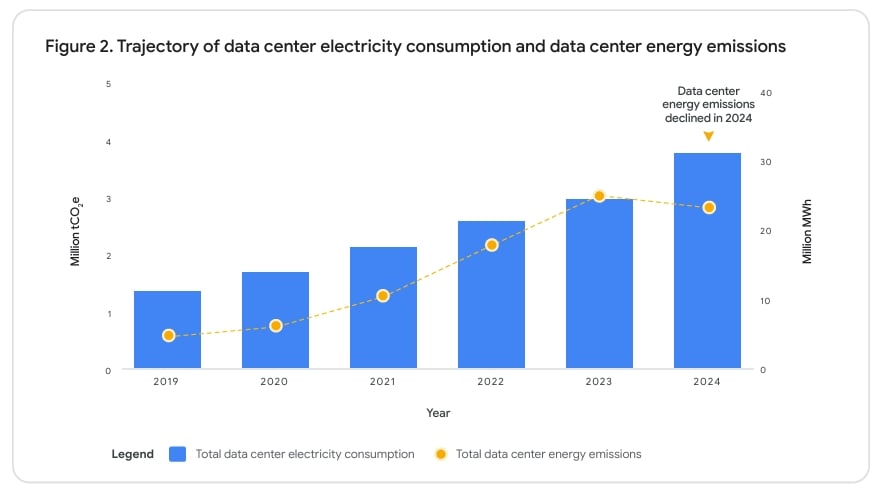

Google’s demand response move also supports its wider clean energy and climate strategy. The company aims to run on 24/7 carbon‑free energy by 2030 and reach net‑zero emissions across its operations and value chain by 2030.

Progress is ongoing. In 2024, Google matched about 66% of its electricity use with carbon‑free energy on an hourly basis, even as power demand rose due to a 27% increase in workload from AI and cloud services.

At the same time, Google added 2.5 GW of new clean energy capacity to the grids serving its operations and cut data center energy emissions by 12% compared with baseline years.

Demand response helps close the remaining gap. By shifting when electricity is used, Google can better match operations with clean energy supply. This improves its ability to run on carbon‑free power every hour of the day.

The Future of Demand Response in AI and Cloud Operations

The demand response market is expected to grow as grids become more complex. Several trends support this outlook.

- Rising demand: U.S. data center growth will drive much of the new electricity use over the next decade. Digital services continue to push the load higher.

- Renewables growth: Wind and solar are cheap but variable, making flexible demand more important for grid stability.

- Grid limits: U.S. interconnection queues include thousands of gigawatts of projects, far more than the grid can handle quickly, causing delays.

Demand response can help manage these constraints. It acts as a “virtual power plant” by reducing demand instead of increasing supply. Studies suggest that flexible demand could unlock large amounts of additional grid capacity and reduce the need for costly transmission upgrades.

This makes demand response one of the fastest and most cost‑effective tools available for grid management.

A Cost-Effective Tool for Modern Grids

As electricity demand continues to grow, this energy model may become more common. Utilities, regulators, and companies are already exploring ways to expand demand‑side flexibility.

In the coming years, the success of these programs will depend on technology, policy support, and market design. However, the direction is clear. Flexible demand is becoming a core part of modern energy systems. Google’s latest move provides a real‑world example of how this transition can work at scale.

The post Google Turns Data Centers Into Grid Assets With 1 GW Flex Power Deal appeared first on Carbon Credits.

Tesla may be getting ready for one of the biggest solar manufacturing moves in America. Reuters reports that the company is looking at buying about $2.9 billion worth of equipment from Chinese suppliers to make solar cells and solar panels in the United States.

If the plan moves forward, it could help Tesla build up to 100 gigawatts of solar manufacturing capacity on American soil by the end of 2028. That is a huge number. It also shows how serious Elon Musk may be about turning solar into a much bigger part of Tesla’s future.

But the report also reveals a bigger problem for the U.S. clean energy sector. Even when companies want to manufacture in America, they still often depend on Chinese tools, machinery, and supply chains to make it happen.

Tesla’s Solar Dream Is Getting Bigger

According to Reuters, Tesla is in talks with several Chinese companies that make solar manufacturing equipment. Suzhou Maxwell Technologies is one of the main names in the discussion. The company is known as the world’s biggest maker of screen-printing equipment used in solar cell production.

Other possible suppliers include Shenzhen S.C New Energy Technology and Laplace Renewable Energy Technology, Reuters said, citing people familiar with the matter.

Some of the equipment may need export approval from China’s commerce ministry before it can be shipped. Reuters reported that the companies were asked to deliver the machinery before autumn, and two sources said the equipment would likely head to Texas.

These details suggest Tesla’s plan is not just an idea or a long-term goal. The company seems to be preparing for a major manufacturing buildout in the U.S. However, the company has not publicly confirmed the reported order. The Chinese suppliers and China’s commerce ministry also did not respond to Reuters’ requests for comment, according to the report.

In January, Musk said solar power could meet all of America’s electricity needs, including rising demand from data centers. Reuters also noted that Tesla job postings said the company wants to deploy 100 GW of “solar manufacturing from raw materials on American soil before the end of 2028.”

The Cost Gap Keeps China in Charge of Solar Supply Chains

After years of heavy investment, China controls most of the world’s solar manufacturing chain. According to Wood Mackenzie, China is expected to hold more than 80% of global polysilicon, wafer, cell, and module manufacturing capacity from 2023 to 2026.

Wood Mac also said a solar module made in China is about 50% cheaper than one made in Europe and 65% cheaper than one made in the United States. That price gap makes it hard for U.S. factories to compete, especially in the early stages.

So even when U.S. companies want to build locally, they still often need Chinese equipment and expertise. Reuters pointed out that the Biden administration excluded solar manufacturing equipment from tariffs in 2024 after U.S. solar companies said they had no real alternative source for the machines needed to launch domestic factories. That exemption has since been extended by the Trump administration.

In other words, America’s solar manufacturing push still depends, at least in part, on Chinese technology.

- READ MORE: Two Solar Stories, Two Different Directions: Why China Builds Faster as the U.S. Hits Pause

Why Tesla May Be Making This Move Now

Tesla’s reported plan is about much more than one company. It highlights a major challenge for the United States as it tries to build a stronger clean energy economy.

U.S. electricity demand is rising again, and solar is growing fast. The Energy Information Administration said U.S. power use hit its second straight record high in 2025. It also expects demand to keep rising in 2026 and 2027.

At the same time, solar is becoming one of the country’s fastest-growing power sources. In its latest outlook, the EIA said utility-scale solar generation in the U.S. is expected to grow from 290 billion kilowatt-hours in 2025 to 424 billion kilowatt-hours by 2027.

The EIA also said nearly 70 GW of new solar capacity is scheduled to come online in 2026 and 2027. That would increase U.S. solar operating capacity by 49% compared with the end of 2025.

Texas Solar Capacity Supports Tesla and SpaceX

Texas is expected to lead much of that growth. Solar generation in the ERCOT grid is forecast to rise from 56 billion kilowatt-hours in 2025 to 106 billion kilowatt-hours by 2027. Battery storage is also growing to help balance solar power throughout the day.

This helps explain why Texas is such an important part of Tesla’s reported plan. The state already plays a big role in Tesla’s manufacturing footprint. It is also one of the hottest solar markets in the country.

For Tesla, building solar equipment or solar products in Texas could support more than just the grid. Reuters said Musk plans to use much of the capacity for Tesla itself, while some could also help power SpaceX satellites.

That would turn solar into a strategic asset across Musk’s wider business empire. It would also tie clean power more closely to Tesla’s long-term growth story, especially as energy demand from artificial intelligence and data infrastructure keeps rising across the country.

Snapshot of US Solar Imports

Even with more local manufacturing, the U.S. solar market still depends heavily on imported parts. Solar Power World reviewed U.S. International Trade Commission data and found that the United States imported 33 GW of silicon solar panels in 2025. It also imported 21 GW of silicon solar cells.

That cell figure is especially important because it shows that U.S. panel assembly is growing faster than domestic cell production. America may be building more panels at home, but it still imports many of the core components needed to make them.

The report said the U.S. has around 50 GW of silicon panel assembly capacity, but less than 5 GW of domestic cell manufacturing output. That means plenty of cells still have to be imported. Notably, most imported cells came from Indonesia and Laos in 2025, while South Korea was also a major supplier.

This is where Tesla could make a difference. If it builds large-scale solar cell and panel manufacturing in the U.S., it could help close one of the biggest gaps in the domestic solar supply chain.

Still, there is an irony here. To reduce America’s dependence on foreign solar products, Tesla may first need to buy Chinese machines.

A Massive Opportunity, But Also a Huge Challenge

If the deal happens, it would be a major win for Chinese solar equipment companies. Many of them have faced weak domestic demand because China has already built too much manufacturing capacity.

For Tesla, the order could lay the foundation for a giant U.S. solar platform. It could support the company’s long-term energy strategy at a time when America needs more electricity, more solar, and more battery storage.

But the challenge is enormous.

Building 100 GW of solar manufacturing capacity in just a few years would be a staggering task. Tesla would need factories, workers, permits, raw materials, logistics, and smooth equipment delivery. It would also need stable trade rules and a supportive policy environment.

The company has already faced supply chain setbacks before. Reuters previously reported that production preparations for the Cybertruck and Semi in the U.S. were disrupted last year after component shipments from China were suspended following higher tariffs on Chinese goods. This history shows how exposed U.S. manufacturing can still be to trade tensions.

If speculations are true, Musk appears to be thinking far beyond electric vehicles, i.e., building a larger clean energy system around solar, batteries, manufacturing, and power demand from new technologies like AI.

For now, Reuters’ report shows a simple reality. The U.S. wants a homegrown solar industry. Tesla may want to help build one. But China still holds many of the tools needed to make that goal real.

The post Is Tesla Building a 100 GW U.S. Solar Giant With Chinese Equipment? appeared first on Carbon Credits.

All This Changed When Trump Came Along

Take a Cool Guess—The Fun Quiz on Renewable Energy and Environmental Sustainability. Today’s Topic: World’s Happiest Countries

Early warning systems are saving lives in Central Asia

-

Climate Change7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?