The past three years have been exceptionally warm globally.

In 2023, global temperatures reached a new high, after they significantly exceeded expectations.

This record was surpassed in 2024 – the first year where average global temperatures were 1.5C above pre-industrial levels.

Now, 2025 is on track to be the second- or third-warmest year on record.

What has caused this apparent acceleration in warming has been subject to a lot of attention in both the media and the scientific community.

Dozens of papers have been published investigating the different factors that could have contributed to these record temperatures.

In 2024, the World Meteorological Organization (WMO) discussed potential drivers for the warmth in a special section of its “state of the global climate” report, while the American Geophysical Union ran a session on the topic at its annual meeting.

In this article, Carbon Brief explores four different factors that have been proposed for the exceptional warmth seen in recent years. These are:

- A strong El Niño event that developed in the latter part of 2023.

- Rapid declines in sulphur dioxide emissions – particularly from international shipping and China.

- An unusual volcanic eruption in Tonga in 2022.

- A stronger-than-expected solar cycle.

Carbon Brief’s analysis finds that a combination of these factors explains most of the unusual warmth observed in 2024 and half of the difference between observed and expected warming in 2023.

However, natural fluctuations in the Earth’s climate may have also played a role in the exceptional temperatures, alongside signs of declining cloud cover that may have implications for the sensitivity of the climate to human-caused emissions.

An unusually warm three years

Between 1970 and 2014, average surface temperatures rose at a fairly steady rate of around 0.18C per decade.

Set against this long-term trend, temperature increases during the period from 2015 to 2022 were on the upper end of what would be expected.

The increases seen in 2023, 2024 and 2025 were well outside of that range.

The high temperatures of the past three years reflect a broader acceleration in the rate of warming over the past decade.

However, the past three years were unusually warm, even when compared to other years in the 2010s and 2020s.

Record-breaking warmth in 2023 meant that it beat the prior warmest year of 2016 by 0.17C – the largest magnitude of a new record in the past 140 years.

The year 2024 then swiftly broke 2023’s record, becoming the first year where average global temperatures exceeded 1.5C above pre-industrial levels.

The 10 months of data available for 2025 indicates that the year is likely to be slightly cooler than 2023 – though it is possible it may tie or be slightly warmer.

The figure below shows global surface temperatures between 1970 and 2025. (The figures for 2025 include uncertainty based on the remaining three months of the year.)

It includes a smoothed average based on temperature data for 1970-2022 that takes into account some acceleration of warming – and then extrapolates that smoothed average forward to 2023-25 to determine what the expected temperature for those years would have been. (This follows the approach used in the WMO’s “state of the global climate 2024” report.)

This approach calculates how much warmer the past three years were than would be expected given the long-term trend in temperatures.

It shows that 2023 was around 0.18C warmer than expected, 2024 was a massive 0.25C warmer and 2025 is likely to be 0.11C warmer.

Researchers have identified a number of potential drivers of unexpected warmth over 2023-25. Here, Carbon Brief looks at the evidence for each one.

A weirdly behaving El Niño event

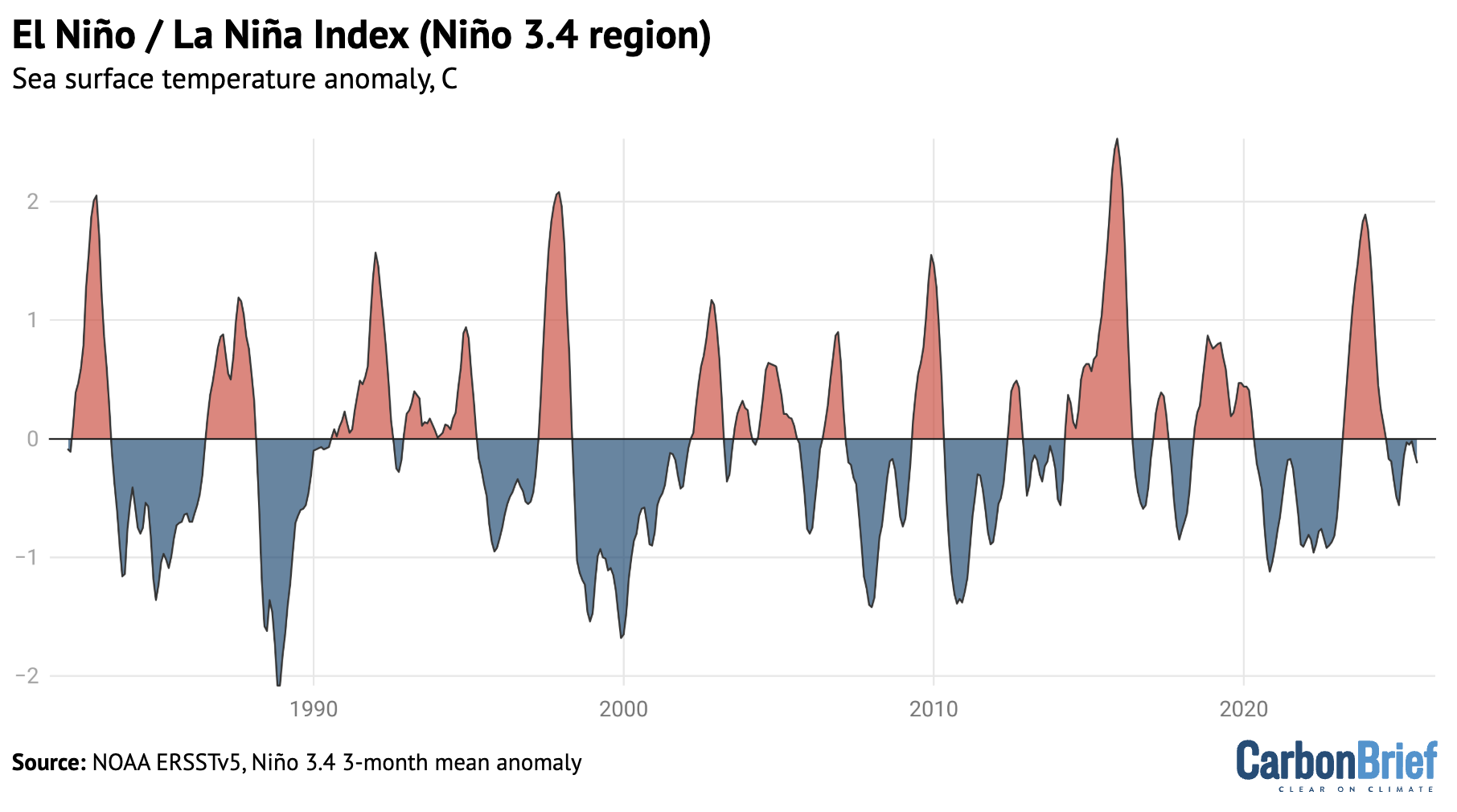

El Niño is a climate pattern of unusually warm sea surface temperatures (SSTs) in the tropical Pacific that naturally occurs every two to seven years. Strong El Niño years generally have warmer global temperatures, with the largest effect generally occurring in the months after El Niño conditions peak (when SSTs reach their highest levels in the tropical Pacific).

A relatively strong El Niño event developed in the latter half of 2023, peaking around November before fading in the spring of 2024.

This event was the fourth-strongest El Niño ever recorded, as measured according to SSTs in the Niño 3.4 region in the central tropical Pacific. However, it was notably weaker than the El Niño events in both 1998 and 2016.

This can be seen in the chart below, which shows the strength of El Niño events (red shading) since the 1980s. (The blue shading indicates La Niña events – the opposite part of the cycle to El Niño, which results in cooler SSTs in the tropical Pacific.)

(It is worth noting that measuring the strength of El Niño events is not entirely straightforward. Other tools used by scientists to monitor changes to El Niño – such as the US National Oceanic and Atmospheric Administration’s (NOAA’s) multivariate ENSO index – show the 2023-24 event was much weaker than indicated in the Niño 3.4 dataset.)

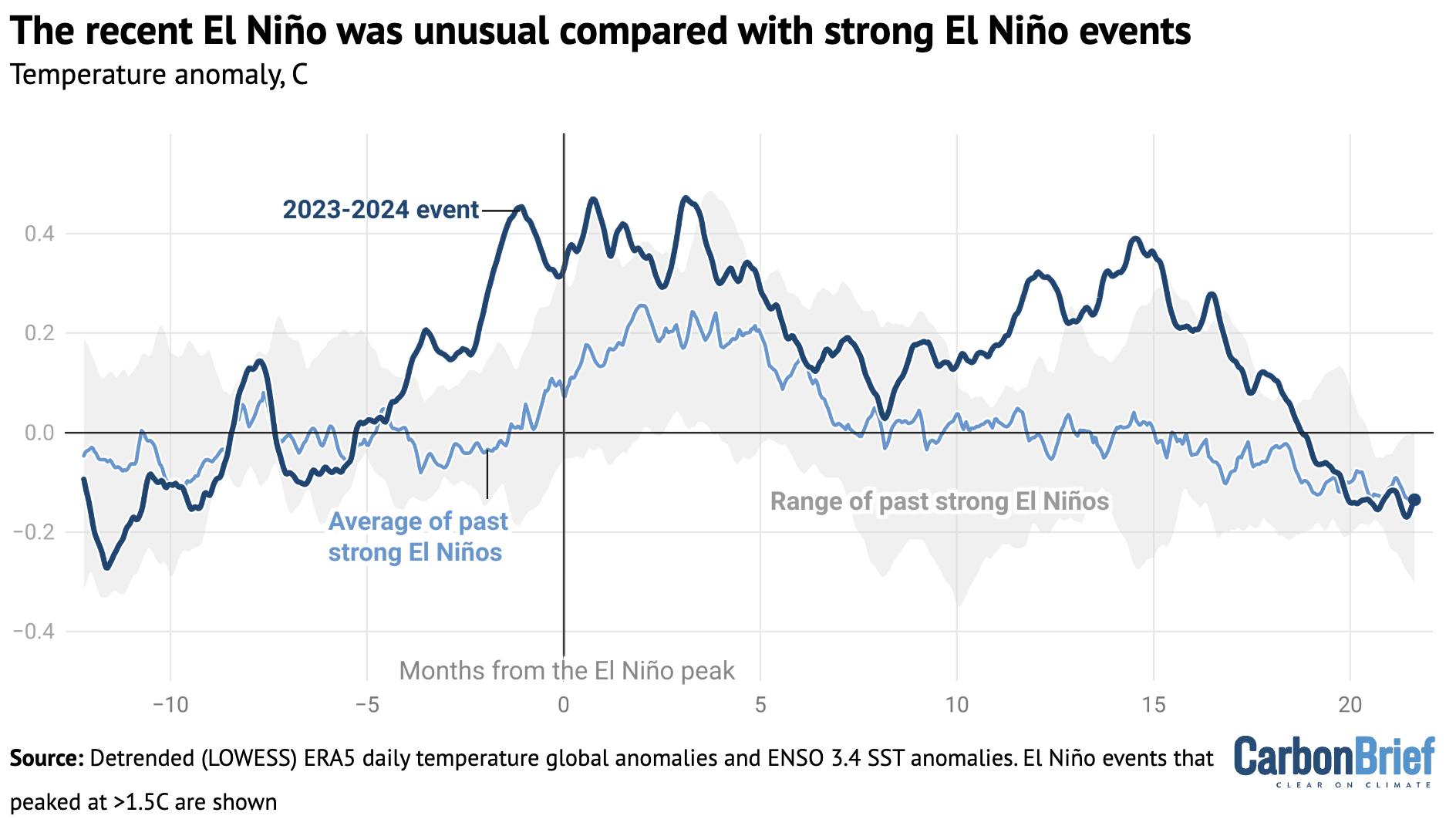

Global surface air temperatures tend to be elevated by around 0.1-0.2C in the six months after the peak of a strong El Niño event – defined here as when SSTs in the Niño 3.4 region reach 1.5C above normal.

The figure below shows the range of global temperature change for the 12 months before and 22 months after the peak of all 10 strong El Niño events since 1950. The light line represents the average of past strong El Niño events, the dark blue line the temperature change observed during the 2023-24 event and the shaded blue area the 5-95th percentile range.

The figure shows the 2023-24 El Niño was quite unusual compared to other strong El Niño events since 1970. Global temperatures rose to around 0.4C above expected levels – which is on the high side of previous El Niños.

The heat also came early, with high temperatures showing up around four months before the El Niño event peaked. This early heat is unlike any other El Niño event in modern history and is one of the reasons why 2023’s global temperatures were so unexpectedly warm.

Global temperatures remained elevated for a full 18 months after the El Niño peaked, well after conditions in the tropical Pacific shifted into neutral conditions – and even after mild La Niña conditions developed at the end of 2024 and into early 2025.

This figure does not explain how much of this unusual heat was actually caused by El Niño, compared to other factors, but it does suggest that El Niño behaviour alone does not fully explain unusually high temperatures in recent years.

Based on the historical relationship between El Niño and global temperatures, Carbon Brief estimates that El Niño contributed a modest 0.013C to 2023 temperatures and a more substantial 0.128C to 2024 temperatures, albeit with large uncertainties. (See “methodology” section at the end for details.)

However, it is possible that this 2023 estimate is too low. There are some suggestions in the literature that 2023-24 El Niño’s early warmth may have been caused by the rapid transition out of a particularly extended La Niña event. There are indications that temperatures have spiked in similar situations further back in the historical temperature record.

Falling sulphur dioxide emissions

Sulphur dioxide (SO2) is an aerosol that is emitted into the lower atmosphere by the burning of coal and oil. It has a powerful climate cooling effect – Carbon Brief analysis shows that global emissions of SO2 have masked about one-third of historical warming.

Global SO2 emissions have declined around 40% over the past 18 years, as countries have increasingly prioritised reducing air pollution, including through the installation of scrubbers at coal plants.

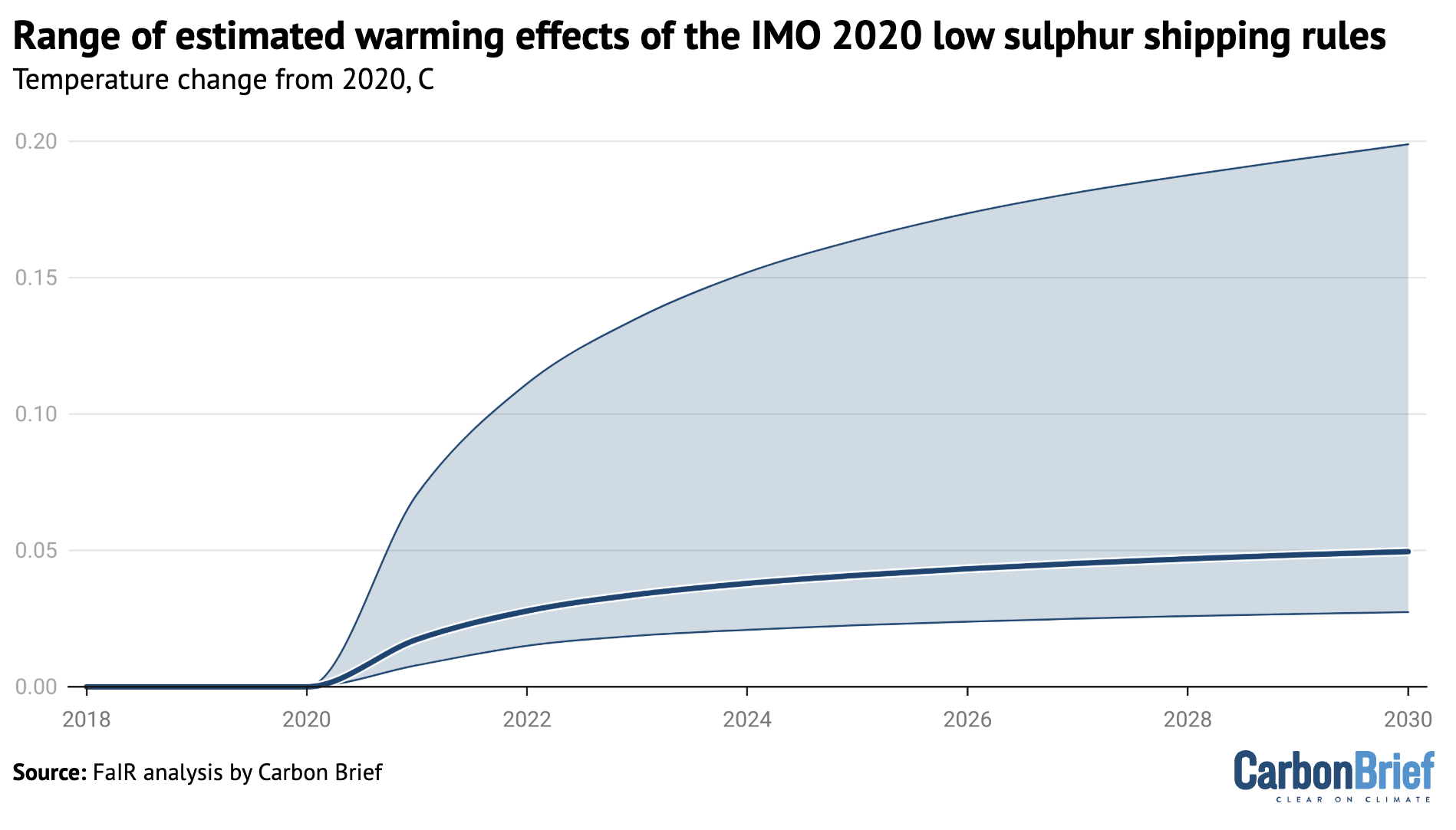

These declines have been particularly concentrated in China, which has seen a 70% decline in SO2 emissions since 2007. In addition, a rule introduced for international shipping in 2020 by the International Maritime Organization (IMO) has resulted in an 80% decline in the sulphur content of shipping fuel used around the world.

The decline of SO2 emissions is shown in the figure below.

Shipping in particular has been suggested as a potential culprit for recent temperatures, given that ships emit SO2 over oceans where the air tends to be cleaner and so emissions have a bigger effect.

Seven of the eight studies that have explored the temperature impact of the IMO regulations have suggested a relatively modest effect, in the range of 0.03-0.08C. However, one study – led by former NASA scientist Dr James Hansen – calculated a much stronger effect of 0.2C that would explain virtually all the unusual warmth of recent years.

The figure below shows Carbon Brief’s estimate of the global average surface temperature changes caused by the low-sulphur shipping fuel rules, using the estimates produced by all eight studies. The central estimate (dark blue line) is relatively low, at around 0.05C, but the uncertainty range (light blue shading) across the studies remains large.

Overall, Carbon Brief’s analysis finds that around 0.04C of warming over 2020-23 and 0.05C of warming over 2020-24 can be attributed to SO2 declines from shipping and other sources.

However, this approach might slightly overstate the effects of SO2 on the exceptional temperatures of the past three years, as shipping and other SO2 declines would have had some effect on 2021 and 2022 as well.

It is also worth noting that the total effects of SO2 declines on global temperatures have been considerably larger and are estimated to be responsible for around one-quarter of all warming since 2007.

However, these SO2 decreases occurred over a long period of time and do not clearly explain the recent spike in temperatures.

An unusual volcanic eruption in Tonga

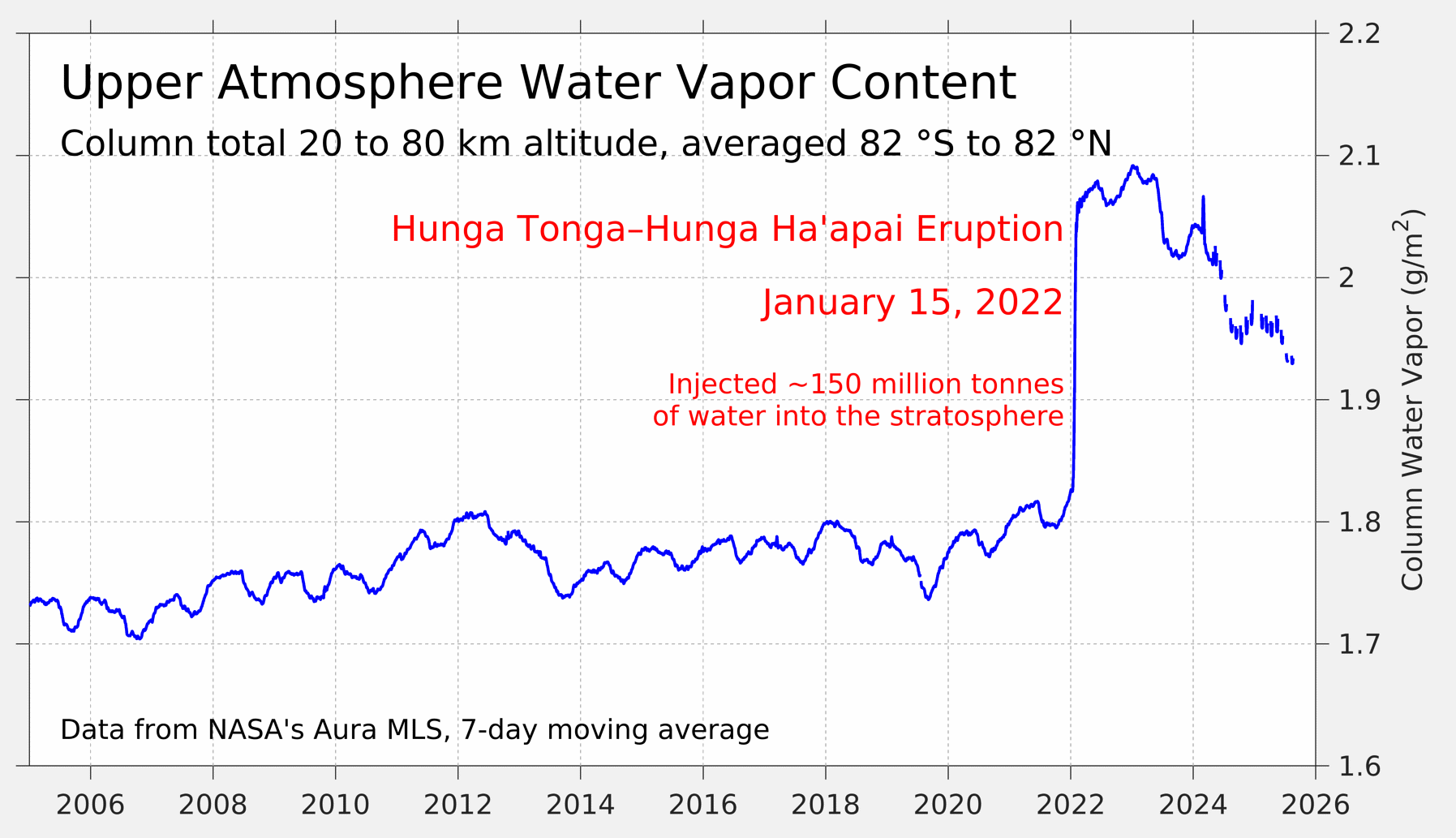

In early 2022, the Hunga Tonga-Hunga Ha’apai underwater volcano erupted spectacularly, sending a plume 55km into the atmosphere. This was by far the most explosive volcanic eruption since Mount Pinatubo erupted in 1991.

This was a highly unusual volcanic eruption, which vaporised vast amounts of sea water and lofted it high into the atmosphere. Overall, around 146m metric tonnes of water vapour ended up in the stratosphere, which is the layer of the atmosphere above the troposphere.

Water vapour is a powerful greenhouse gas. While it is short-lived in the lower atmosphere, it can stick around for years in the stratosphere, where it has a significant warming effect on the climate.

The figure below shows the concentration of water vapour in the stratosphere between 2005 and mid-2025. It shows how the 2022 eruption increased atmospheric concentrations of the greenhouse gas by around 15%. More than half the added water vapour has subsequently fallen out of the upper atmosphere.

Most early studies of the Hunga Tonga-Hunga Ha’apai volcano focused specifically on the effects of stratospheric water vapour. These tended to show strong warming in the lower stratosphere and cooling in the middle-to-upper stratosphere, but only a slight warming effect on global surface temperatures of around 0.05C.

Hunga Tonga-Hunga Ha’apai had much lower sulphur emissions than prior explosive eruptions, such as Pinatubo and El Chichon. However it put 0.5–1.5m tonnes of sulphur into the stratosphere – the most from an eruption since Pinatubo.

Studies that included both sulphur and water vapour effects tend to find that the net effect of the eruption on surface temperatures was slight global cooling, concentrated in the southern hemisphere.

By using the estimates published in a 2024 study published in Geophysical Research Letters, which used the FaIR climate emulator model, Carbon Brief estimates that the Hunga Tonga-Hunga Ha’apai eruption cooled global surface temperatures by -0.01C in 2023 and -0.02C in 2024.

This suggests that the eruption was likely only a minor contributor to recent global surface temperatures.

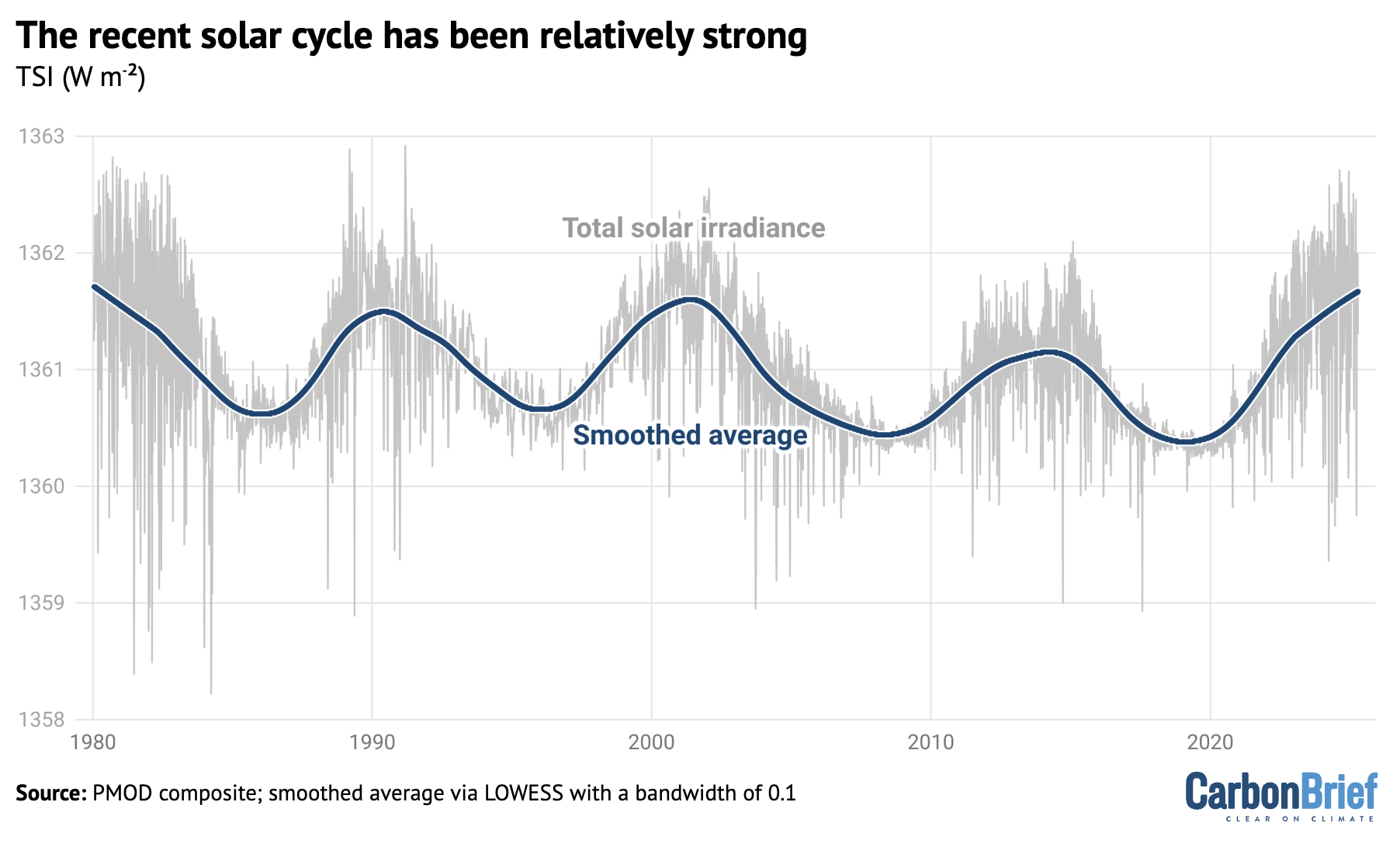

A stronger-than-expected solar cycle

The source of almost all energy on Earth is the sun. Over hundreds of millions of years, variations in solar output have a big impact on the global climate.

Thankfully, over shorter periods of time the sun is remarkably stable, helping keep the Earth’s climate habitable for life. (Big changes – such as ice ages – have more to do with variations in the Earth’s orbit than changes in solar output.)

However, slight changes in solar output do occur – and when they do, they can influence climate change over shorter periods of time. The most important of these is the roughly 11-year solar cycle, which is linked with the sun’s magnetic field and results in changes in the number of sunspots and amount of solar energy reaching Earth.

The figure below shows a best-estimate of changes in total solar irradiance since 1980, based on satellite observations. Total solar irradiance is a measure of the overall amount of solar energy that reaches the top of the Earth’s atmosphere and is measured in watts per metre squared.

The 11-year solar cycle is relatively modest compared to the sun’s total output, varying only a few watts per metre squared between peak and trough – amounting to around 0.01% of solar output. However, these changes can result in variations of up to 0.1C in global temperatures within a decade.

The most recent solar cycle – solar cycle 25 – began around 2020 and has been the strongest solar cycle measured since 1980. It was stronger than most models had anticipated and likely contributed to around 0.04C global warming in 2023 and 0.07C in 2024.

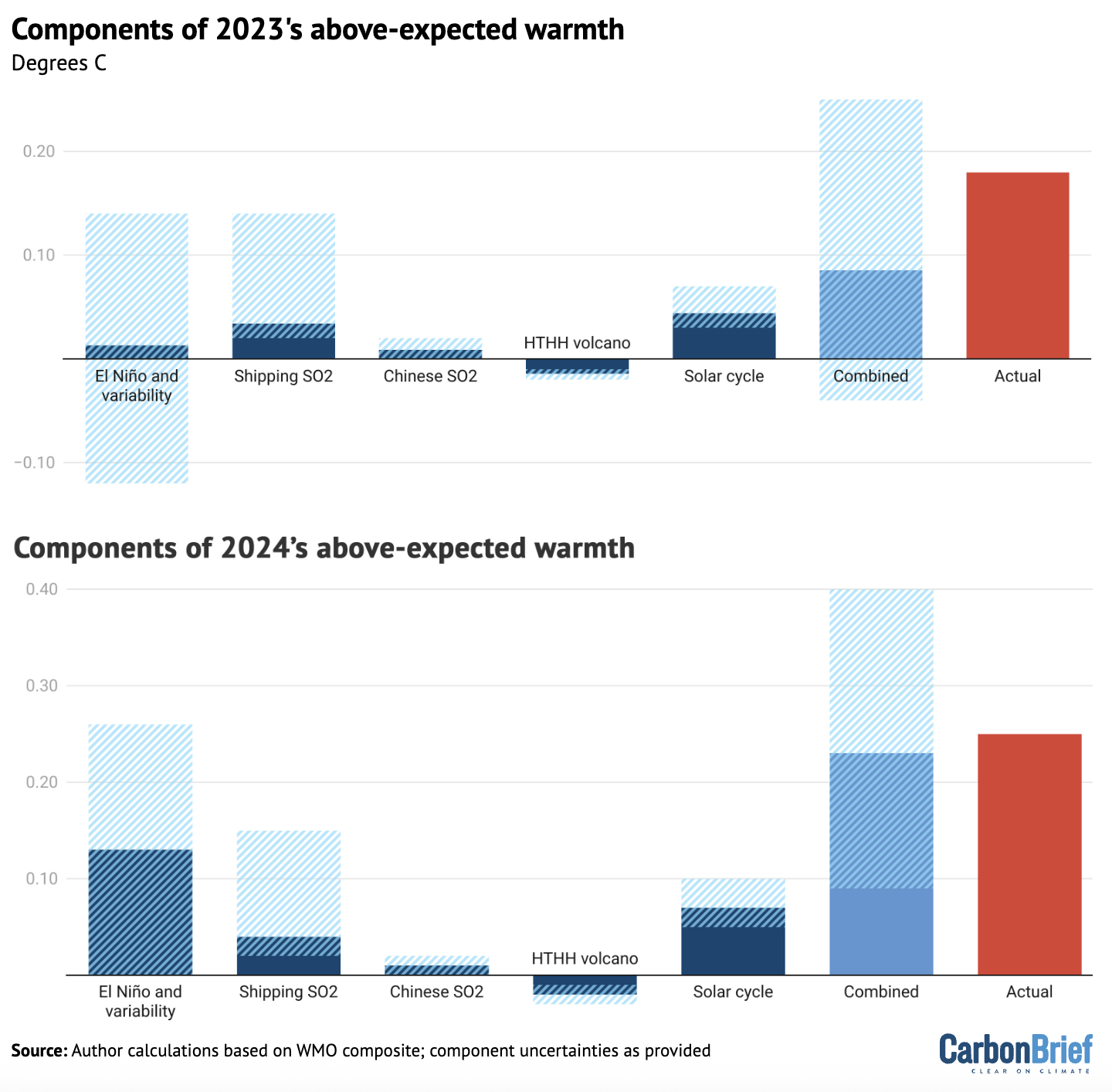

Putting together the drivers

By combining earlier estimates of different factors contributing to 2023 and 2024 global surface temperatures, about half of 2023’s unusual warmth and almost all of 2024’s unusual warmth can be effectively explained.

This is illustrated in the figure below, which shows the five different factors discussed earlier – El Niño, shipping SO2, Chinese SO2, the Hunga Tonga-Hunga Ha’apai volcano and solar cycle changes – along with their respective uncertainties.

The sum of all the factors is shown in the “combined” bar, while the actual warming compared to expectations is shown in red.

The upper chart shows 2023, while the lower one shows 2024.

It is important to note that the first bar includes both El Niño and natural year-to-year variability; the height of the bar reflects the best estimate of El Niño’s effects, while the uncertainty range encompasses year-to-year variability in global temperatures that may be – at least in part – unrelated to El Niño.

The role of natural climate variability

Large natural variability to the Earth’s climate is one of the main reasons why the combined value of the different drivers of expected warmth in 2023 has an uncertainty range that exceeds the observed warming – even though the best-estimate of combined factors only explains half of temperatures.

Or, to put it another way, there is up 0.15C difference in global temperatures year-on-year that cannot be explained solely by El Niño, human-driven global warming, or natural “forcings” – such as volcanoes or variations in solar output.

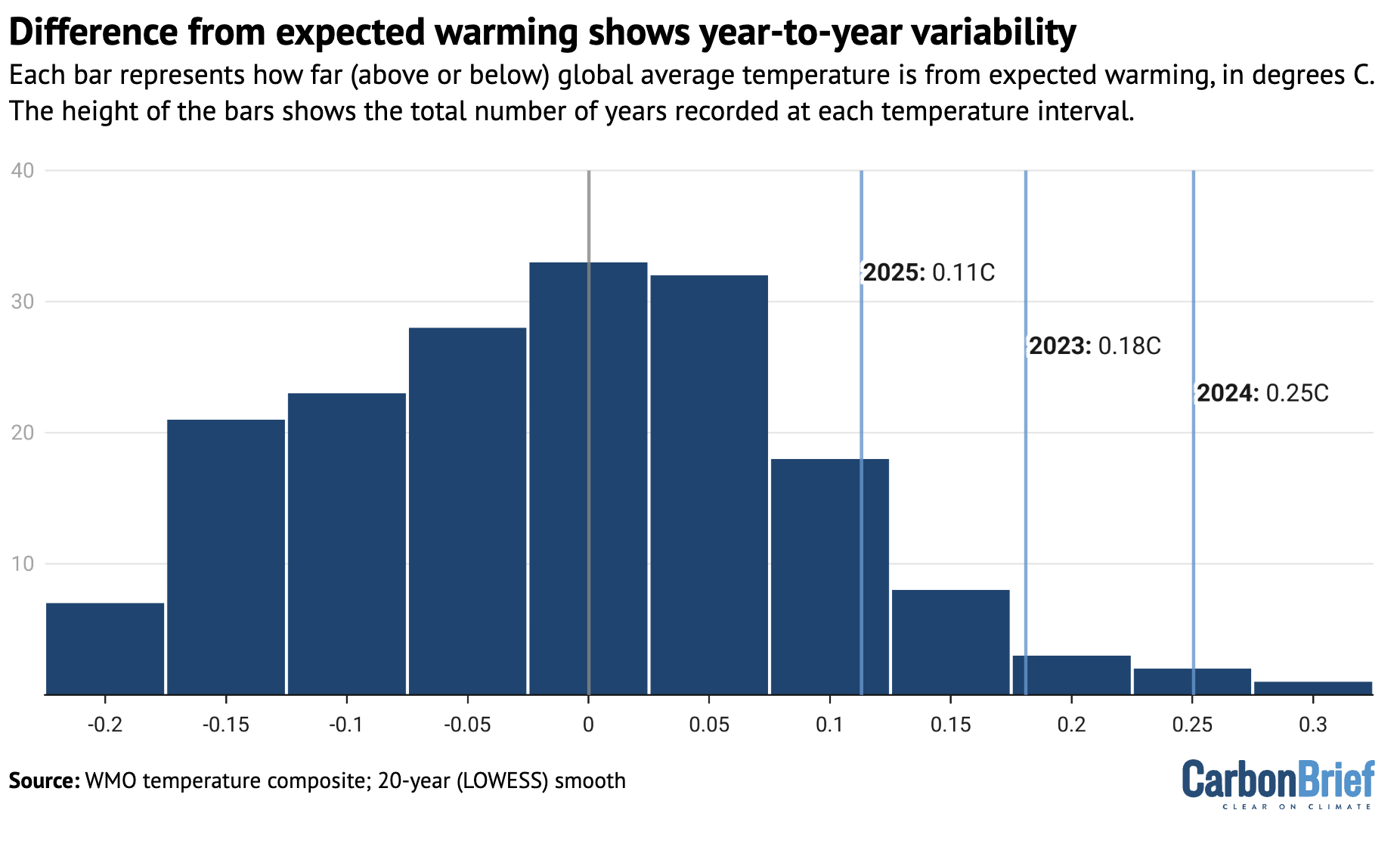

The figure below shows the difference between actual and expected warming in the global temperature record for every year in the form of a histogram. The vertical zero line represents the expectation given long-term global warming and the other vertical lines indicate the warming seen in 2023, 2024 and 2025.

The height of each blue bar represents the number of years over 1850-2024 when the average global temperature was that far (above or below) the expected level of warming.

Based on the range of year-to-year variability, temperatures would be expected to spike as far above the long-term trend as they did in 2023 once every 25 years, on average. The year 2024 would be a one-in-88 year event, whereas 2025 would be a less-unusual, one-in-seven year event.

These likelihoods for the past three years are sensitive to the approach used to determine what the longer-term warming level should be.

In this analysis, Carbon Brief used a local smoothing approach (known as locally estimated scatterplot smoothing) to determine the expected temperatures, following the approach used in the WMO “state of the climate 2024” report.

This approach results in a warming of 1.28C in 2023 and 1.30C in 2024, against which observed temperatures are compared.

Other published estimates put the longer-term warming in 2024 notably higher.

Earlier this year, the scientists behind the “Indicators of Global Climate Change” (IGCC) report estimated that human activity caused 1.36C of recent warming in 2024. They also found a slightly lower overall warming level for 2024 – 1.52C, as opposed to the WMO’s 1.55C – because they looked exclusively at datasets used by IPCC AR6. (This meant estimates from the Copernicus/ECMWF’s ERA5 dataset were not included.)

Based on climate simulations, the IGCC report finds the likelihood of 2024’s warmth to be a one-in-six year event and 2023’s a one-in-four event.

Using the same assumptions as the IGCC, Carbon Brief’s approach calculates that 2024 would be a less-common, one-in-18 year event.

However, the IGCC estimate of current human-induced warming is based on the latest estimates of human and natural factors warming the climate. That means that it already accounts for additional warming from low-sulphur shipping fuel, East Asian aerosols and other factors discussed above.

Therefore, the results from these two analyses are not necessarily inconsistent: natural climate variability (including El Niño) played a key role – but this came in addition to other factors. Natural fluctuations in the Earth’s climate alone would have been unlikely to result in the extreme global temperatures seen in 2023, 2024 and 2025.

A cloudy picture

Even if unusual recent global warmth can be mostly attributed to a combination of El Niño, falling SO2 emissions, the Hunga Tonga-Hunga Ha’apai volcano, solar cycle changes and natural climate variability, there are a number of questions that remain unanswered.

Most important is what the record warmth means for the climate going forward. Is it likely to revert to the long-term average warming level, or does it reflect an acceleration in the underlying rate of warming – and, if so, what might its causes be?

As explained by Carbon Brief in a 2023 article, climate models have suggested that warming will speed up. Some of this acceleration is built into the analysis presented here, which includes a slightly faster rate of warming in recent years than has characterised the period since 1970.

But there are broader questions about what – beyond declining SO2 and other aerosols – is driving this acceleration.

Research recently published in the journal Science offered some potential clues. It found a significant decline in planetary reflectivity – known as albedo – over the past decade, associated with a reduced low-level cloud cover that is unprecedented in the satellite record.

The authors suggest it could be due to a combination of three different factors: natural climate variability, changing SO2 and other aerosol emissions and the effects of global warming on cloud reflectivity.

Natural climate variability seems unlikely to have played a major role in reduced cloud cover, given that it was relatively stable until 2015. However, it is hard to fully rule it out given the relatively short satellite record.

Reductions in SO2 emissions are expected to reduce cloud reflectivity, but the magnitude of the observed cloud reflectivity changes are much larger than models simulate.

Models might be underestimating the impact of aerosols on the climate. But, if this were the case, it would indicate that climate sensitivity might be on the higher end of the range of model estimates, because models that simulate stronger aerosol cooling effects tend to have higher climate sensitivity.

Finally, cloud cover might be changing and becoming less reflective as a result of warming. Cloud responses to climate change are one of the largest drivers of uncertainty in future warming. One of the main reasons that some climate models find a higher climate sensitivity is due to their simulation of less-reflective clouds in a warming world.

The Science study concludes that the 2023 heat “may be here to stay” if the cloud-related albedo decline was not “solely” caused by natural variability. This would also suggest the Earth’s climate sensitivity may be closer to the upper range of current estimates, it notes.

Methodology

Carbon Brief built on work previously published in the IGCC 2024 and WMO state of the global climate 2024 reports that explores the role of different factors in the extreme temperatures in 2023, 2024 and 2025.

The impact of El Niño Southern Oscillation (ENSO) on the temperatures was estimated using a linear regression of the annual mean global temperature anomaly on the Feb/Mar Niño 3.4 index. This resulted in an impact of −0.07C, 0.01C and 0.13C for 2022, 2023 and 2024 respectively (with a 95% confidence interval of ±0.13 ºC).

It is important to note that the uncertainties in the ENSO response estimated here also incorporate other sources of unforced internal (modes of variability in other basins such as AMV), and potentially some forced variability. The bar in the combined figure is labelled “El Niño and variability” to reflect this.

For details on calculations of the temperature impact of shipping and Chinese SO2 declines, see Carbon Brief’s explainer on the climate impact of changing aerosol emissions.

Solar cycle 25 was both slightly earlier and slightly stronger than prior expectations with a total solar irradiance anomaly of 0.97 watts per metre squared in 2023 relative to the mean of the prior 20 years. This resulted in an estimated radiative forcing of approximately 0.17 watts per metre squared and an estimated global surface temperature increase of 0.07C (0.05C to 0.10C) with a one- to two-year lag based on a 2015 study. Thus, the impact on 2023 and 2024 is around 0.04C and 0.07C, respectively (+/- 0.025C). This is a bit higher warming than is given by the FaIR model, as the 2015 study is based on global models that have ozone responses to the UV changes, which amplifies the temperature effects a bit.

The Hunga Tonga-Hunga Haʻapai volcanic eruption added both SO2 and water vapour to the stratosphere (up to 55km in altitude). The rapid oxidation of SO2 to sulphate aerosol dominated the radiative forcing for the first two years after the eruption. As a result, the net radiative forcing at the tropopause was likely negative; −0.04 watts per metre squared and −0.15 watts per metre squared in 2022 and 2023, respectively, implying a temperature impact of -0.02C (-0.01C to -0.03C) calculated using the FaIR model.

The post Analysis: What are the causes of recent record-high global temperatures? appeared first on Carbon Brief.

Analysis: What are the causes of recent record-high global temperatures?

Climate Change

DeBriefed 3 July 2026: US faces scorching Independence Day | Record ocean temperatures | Vietnam’s EV surge

Welcome to Carbon Brief’s DeBriefed.

An essential guide to the week’s key developments relating to climate change.

This week

Heating up

NOT FREE FROM HEAT: “Dangerous, record-breaking” heat altered plans for 4 July celebrations across the US this weekend, reported the Associated Press. New York and Boston hit 100F (37.8C) on Thursday, said the newswire. CNBC reported that temperatures of up to 105F (40.5C) are forecast in central and eastern parts of the country, with “daily, monthly and all-time records possible”.

TEMPERATURES SOAR: Heat that hit western Europe last week spread east to “scorch” Germany, Hungary, Romania, Poland and others, said Bloomberg. Red warnings for extreme heat were issued in a number of nations, noted the outlet, adding that the heat “underscores how climate change is transforming summers in the world’s fastest-warming continent”. The Independent said last month was confirmed to be England’s hottest June on record.

HEAT DEATHS: June’s extreme temperatures caused more than 2,000 excess deaths in Spain and France, reported the Guardian. The countries are bracing for further heat that “could bring temperatures of 44C (111F) over the coming days”, said the newspaper. Deaths in France rose almost 30% at the heatwave “peak” on the week of 22 June, according to Le Monde. Last week’s conditions also led to around 480 excess deaths in the Netherlands, reported Reuters.

BOILING: Global ocean temperatures reached record levels for this time of year, reported NBC News, “fuelling fears of more dangerous heatwaves this summer and fanning concerns over the escalating global climate crisis”. Scientists told the Financial Times that this could lead the world towards “uncharted territory”. The newspaper said global average sea surface temperatures reached 20.96C on 21 June, exceeding June records for 2023 and 2024.

Around the world

- GOAL DROPPED: The World Bank will “abandon” its goal to devote 45% of annual lending resources to climate-related projects, reported Reuters. Carbon Brief explored what it could mean for global climate action.

- FIVE-YEAR PLAN: China plans to invest more than 20tn yuan ($2.9tn) in “key energy projects and new business models” over the next five years, according to International Energy Net.

- DRILLING: The Guardian said UK Labour politicians “urged” the likely next prime minister Andy Burnham to ignore “deluded” calls to develop the Rosebank oil field located in the Atlantic north of Scotland.

- PLASTIC TALKS: Countries and activists feared key issues could be sidelined at “critical” talks on a global treaty to curb plastic pollution in Kenya, said Climate Home News. A treaty could have “important implications” for climate change, reported Carbon Brief in 2024.

- CANADA PIPELINE: Canadian prime minister Mark Carney announced plans to build an oil pipeline to supply Asia with up to 1m barrels per day, reported the Financial Times. Earlier this week, Carney called the previous government’s climate plans “expensive” and “divisive”, said CBC News.

63

The number of UK newspaper editorials calling for more oil and gas extraction in the North Sea so far in 2026, according to Carbon Brief analysis.

Latest climate research

- Including emissions from permafrost thaw raises the likelihood of the Arctic becoming a net-carbon source by more than 50% at 2C of warming | Earth System Dynamics

- Net-zero scenarios relying less on carbon dioxide removals lead to fewer residual emissions, which offers greater health improvements for “non-white and low-income groups” in particular | Nature Climate Change

- Agricultural plots of land in sub-Saharan Africa owned by women face heat impacts 2-2.5 times higher than those owned by men | Nature Sustainability

(For more, see Carbon Brief’s in-depth daily summaries of the top climate news stories on Monday, Tuesday, Wednesday, Thursday and Friday.)

Captured

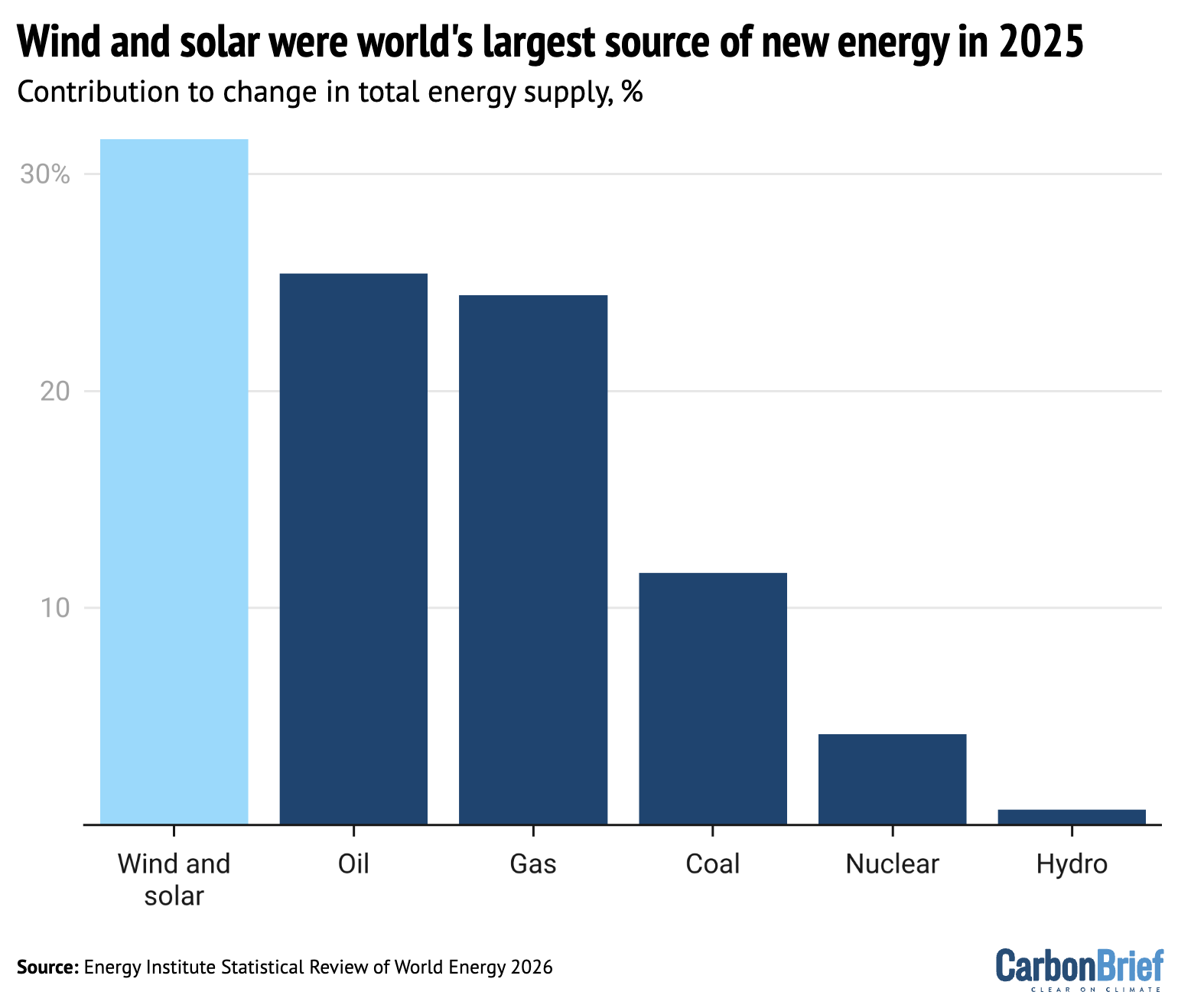

Wind and solar were the world’s largest source of new energy in 2025, according to Carbon Brief analysis of the latest Energy Institute statistical review of world energy. Wind and solar also saw the fastest growth, up by 18% in 2025. Nevertheless, every source of energy – including coal, oil, gas, nuclear and hydro – also reached global all-time highs last year.

Spotlight

Vietnam’s EV surge

Carbon Brief explores the reasons behind soaring electric-vehicle sales in Vietnam.

Motorbikes are a constant fixture on streets across Vietnam. They pollute the air in cities and make crossing the road a feat of endurance.

But, increasingly, people are moving away from petrol-powered vehicles to save money and reduce air pollution.

Sales of electric motorbikes, scooters and mopeds more than doubled in Vietnam last year, according to a recent report from the International Energy Agency (IEA).

This identified that Vietnam has the largest electric vehicle (EV) market in south-east Asia.

Nearly one-in-five of the two-wheeled vehicles sold last year were electric, it noted, in a nation with 102 million people and 77m motorbikes.

This is “particularly impactful” given they are the main mode of transport in Vietnam, said Lam Pham, Asia energy analyst at thinktank Ember. He told Carbon Brief:

“Electrifying road transport is essential for Vietnam to achieve its net-zero target by 2050. Road transport accounted for around 86% of transport-sector emissions in 2022.”

The nation has just 6.8m cars, but this number is also climbing, partly due to EVs, with nearly 40% of new car sales being electric.

This is “above levels seen in most European countries”, noted the IEA. (The UK’s figure is around 30%.)

EV incentives

Fuel costs surged in south-east Asian countries earlier this year after the energy crisis caused by the US-Israel war on Iran.

This “accelerated” discussions from “why use EVs” to “why keep paying more for fuel”, said Dr Tham Nguyen, a lecturer at the Ho Chi Minh City campus of Australia’s Royal Melbourne Institute of Technology (RMIT) University, who has researched Vietnamese public attitudes to EVs.

But the surge is “not driven by fuel prices alone”, noted Pham.

Increased EV sales can also be attributed to a “convergence of affordability, convenience and sustainability”, Nguyen said:

“Vietnamese consumers buy EVs because they see real value with immediate personal benefits, such as cost savings and energy security, alongside long-term environmental gains.”

Government policies have also incentivised sales through registration fee exemptions and tax cuts for EVs.

Another factor is affordable EVs sold by Chinese companies and Vinfast, a Vietnamese manufacturer. The IEA report noted that Vietnam is the only country in south-east Asia with “sizeable” domestic production of accessible EVs.

Vinfast reported a 219% year-on-year increase in orders for electric motorbikes and e-bikes in the first quarter of 2026, but the company has yet to turn a profit.

Pham noted that “growing public awareness of air pollution” has also “dramatically strengthened” public support for EVs.

Future plans

Vietnam’s major cities also have plans to get drivers to go electric or turn to public transport.

The capital city Hanoi announced that it would ban fossil-fuel-powered motorbikes from a central zone this month, but this has been postponed until 2028.

Ho Chi Minh City, the nation’s largest city with more than 9.5 million people, intends to introduce low-emission zones and swap 400,000 petrol-powered motorbikes to electric by 2028.

The city’s green transport plans focus on metro lines, electric buses and e-bikes, explained RMIT associate professor Catherine Earl. She noted that walking and cycling are currently “not popular, accessible or safe for many residents in Ho Chi Minh City’s hot and humid climate”.

Looking ahead, Pham said Vietnam could focus on “purchase subsidies, financing schemes and adequate charging or battery-swapping infrastructure, to ensure lower-income riders, including delivery and ride-hailing drivers, are not negatively affected”.

Watch, read, listen

‘JUST 1%’ OF EMISSIONS: The Guardian debunked arguments that climate actions from smaller countries are “insignificant”.

DRILLING RISKS: Mongabay reported on the possible impacts oil drilling in the Amazon could have on a “little-known reef”.

HEATING UP: The BBC Climate Question podcast discussed the weather pattern El Niño and its links to climate change.

Coming up

- 7-10 July: AI for good global summit, Geneva, Switzerland

- 7-15 July: UN high-level political forum on sustainable development, New York

- 8-10 July: Ninth meeting of the board of the fund for responding to loss and damage, Manila, Philippines

Pick of the jobs

- Green Alliance, senior partnerships officer | Salary: £42,748-£47,346. Location: London

- World Vision, environment and climate action senior adviser | Salary: Unknown. Location: Kenya

- Nature Energy, interim associate or senior editor | Salary: Unknown. Location: London or Milan

- Climate Analytics, senior communications manager – climate policy (maternity cover) | Salary €60,605-€66,880. Location: Berlin

- Carbon Exchange, researcher | Salary: Unknown. Location: Hong Kong

DeBriefed is edited by Daisy Dunne. Please send any tips or feedback to debriefed@carbonbrief.org.

This is an online version of Carbon Brief’s weekly DeBriefed email newsletter. Subscribe for free here.

The post DeBriefed 3 July 2026: US faces scorching Independence Day | Record ocean temperatures | Vietnam’s EV surge appeared first on Carbon Brief.

The World Bank has abandoned a target for 45% of the funding it gives developing countries to be “climate finance”, following months of pressure from the Trump administration in the US.

However, a concerted effort by developed- and developing-country shareholders has seen the bank hold onto its “action plan” for tackling climate change.

The multilateral development bank (MDB) – which is headquartered in Washington DC – is the single largest provider of climate finance globally, distributing $39.2bn in 2025 alone, primarily as loans.

Amid widespread aid cuts by developed countries, the World Bank and other MDBs have previously pledged to significantly scale up their climate finance over the next decade.

Despite scrapping its central target, the bank says it will continue to support the demands of its “clients”, many of which have explicitly stated their need for climate-related investment.

Here, Carbon Brief looks at the likely impact of the World Bank’s policy shift and whether it is – as one expert puts it – “mostly a symbolic victory” for the US.

- How does the World Bank support climate action?

- Why has the World Bank abandoned its climate-finance target?

- Why is the World Bank important for international climate finance?

- How will these changes affect global climate action?

How does the World Bank support climate action?

The World Bank is the oldest and largest MDB. It is tasked by its 189 member governments – the bank’s shareholders – with supporting development projects around the world.

The US is the bank’s largest shareholder, followed, in order, by Japan, China, Germany, France and the UK.

Every year, the bank provides billions of dollars – predominantly as loans – to developing countries.

(One part of the World Bank, the International Development Association – IDA – specifically distributes grants to lower-income nations, as well as lower-interest loans.)

Through its financing, the World Bank also has an important role in “mobilising” private investments in developing countries.

In recent years, the bank has increasingly focused on helping developing countries to cut emissions and adapt their economies for climate change.

The World Bank provided $164bn in what it calls financing with climate “co-benefits” between 2020 and 2025.

The largest share of this funding – roughly one-fifth – went to clean energy and electricity access projects. Smaller shares went to areas such as public transport, water supply and sustainable farming.

As the map below shows, the largest recipients of the bank’s climate funds since 2020 have been emerging economies, such as Turkey ($10.3bn), India ($9bn) and Nigeria ($6.3bn).

Among the largest World Bank projects in recent years are two extensive programmes in India, totalling nearly $3bn, supporting renewables and green hydrogen.

Others include $1.7bn for a Pakistan hydropower project, $926m for Iraq’s railways and $803m to boost “green development” in Colombia.

Despite the bank’s major role in providing climate finance to developing countries, it has faced heavy scrutiny from climate advocates.

In particular, they have noted the dominance of loans that push developing countries further into debt. The World Bank has also been criticised for a lack of transparency around how it classifies projects as “climate-related”, as well as “over-reporting” of climate finance.

Why has the World Bank abandoned its climate-finance target?

When World Bank president Ajay Banga – nominated by former US president Joe Biden – took over the institution in 2023, there were widespread calls for MDB reform.

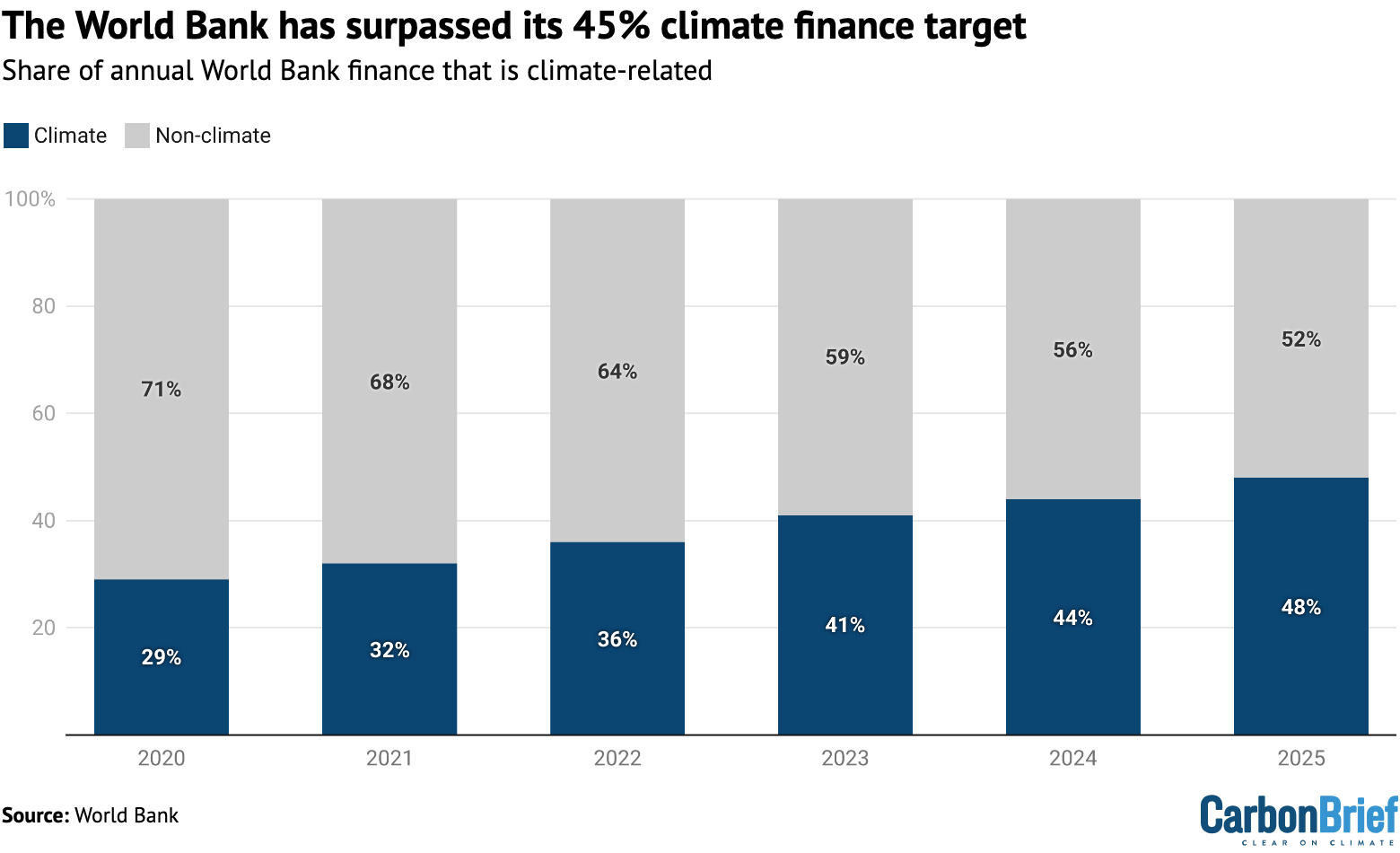

Many of the bank’s shareholders wanted to see billions more dollars being channelled to support climate action. Later that year, Banga announced that the bank would ensure that 45% of the bank’s funding was climate finance by 2025.

This replaced an existing target of 35% for climate finance between 2021 and 2025, which had been set out in the bank’s second climate change action plan (CCAP).

The CCAP is intended to “mainstream” climate action in the bank’s work. With it in place, the World Bank’s climate finance more than doubled from $17.2bn in 2020 to $39.2bn in 2025.

As the chart below shows, this meant the World Bank exceeded its 2025 goal, with climate-related projects making up a 48% share of total funding that year.

When Biden was replaced by Donald Trump as president in 2025, the US administration turned against international cooperation, including climate finance.

However, the US did not walk away from the World Bank, where it exerts considerable power as the largest shareholder.

With the CCAP due to expire in July 2026, the US has spent months pressuring the bank and its shareholders to weaken or abandon the plan altogether.

US Treasury secretary Scott Bessent issued a statement during the 2026 World Bank and International Monetary Fund (IMF) spring meetings in April 2026, in which he called for “jettisoning” the 45% climate-finance target. More broadly, he said:

“We welcome the coming expiration of the CCAP and…expect the bank to immediately shift its myopic focus on climate and financing volumes to one that emphasises high-quality, durable projects.”

This vision involves a push for the World Bank to finance more fossil-fuel projects, including drilling for new gas. (The bank has committed since 2019 to stop funding upstream oil and gas projects.)

The decision on whether to continue with the CCAP was negotiated behind closed doors by the board of directors – representing national shareholders. There were reports of “deep divides”.

A joint statement from 19 of the 25 directors last year affirmed the need for both a plan and a target. The US, Russia, Kuwait and Saudi Arabia all declined to sign up, while Japan and India abstained, according to Reuters.

There were reports of European nations championing a climate plan, bolstered by support from the developing countries that would stand to receive climate finance. The US call to drop the 45% target entirely was reportedly backed by Saudi Arabia and Russia.

Ultimately, the day before the CCAP was due to lapse, the World Bank announced what appeared to be a middle ground. It would drop both the 45% target and the 35% goal it had replaced, while also “extend[ing]” the CCAP.

UK development minister Jenny Chapman told a committee hearing in the House of Commons the next day that this marked a “compromise”. She said:

“It wasn’t clear we were going to get a CCAP at all and a bank without an action plan on climate is a problem for us – so that’s a good outcome.”

Supportive shareholders had been pushing for a one-year extension of the plan. While the World Bank did not initially define the length, Chapman confirmed on LinkedIn that the plan had, in fact, been extended “indefinitely”.

The bank said it would also engage an “independent evaluation group” to assess the CCAP, in line with a board request.

Gaia Larsen, director of climate finance at the World Resources Institute (WRI), tells Carbon Brief that this evaluation will likely be “relatively free from political ideology” and could be “focused on how to make the CCAP more effective”.

Why is the World Bank important for international climate finance?

Under the Paris Agreement, developed countries – including major World Bank shareholders in Europe and elsewhere – are obliged to provide climate finance for developing countries.

This includes a target of $300bn a year by 2035, which is expected to largely come from developed countries. One significant way these nations can contribute to this goal is via their support for MDBs, particularly the World Bank.

The World Bank has described itself as “by far the largest provider of climate finance to developing countries”. Each year, it oversees half of all climate finance from MDBs and far more than any single donor country.

Many developed countries have, therefore, enthusiastically backed the World Bank’s climate efforts, as well as a “bigger” role for MDBs in development more broadly. The bank can lend sums that far exceed the amount of new public finance that individual nations are willing to commit.

This is particularly significant, given many of these nations, including the UK, Germany and France, have announced large cuts to their aid budgets in recent years.

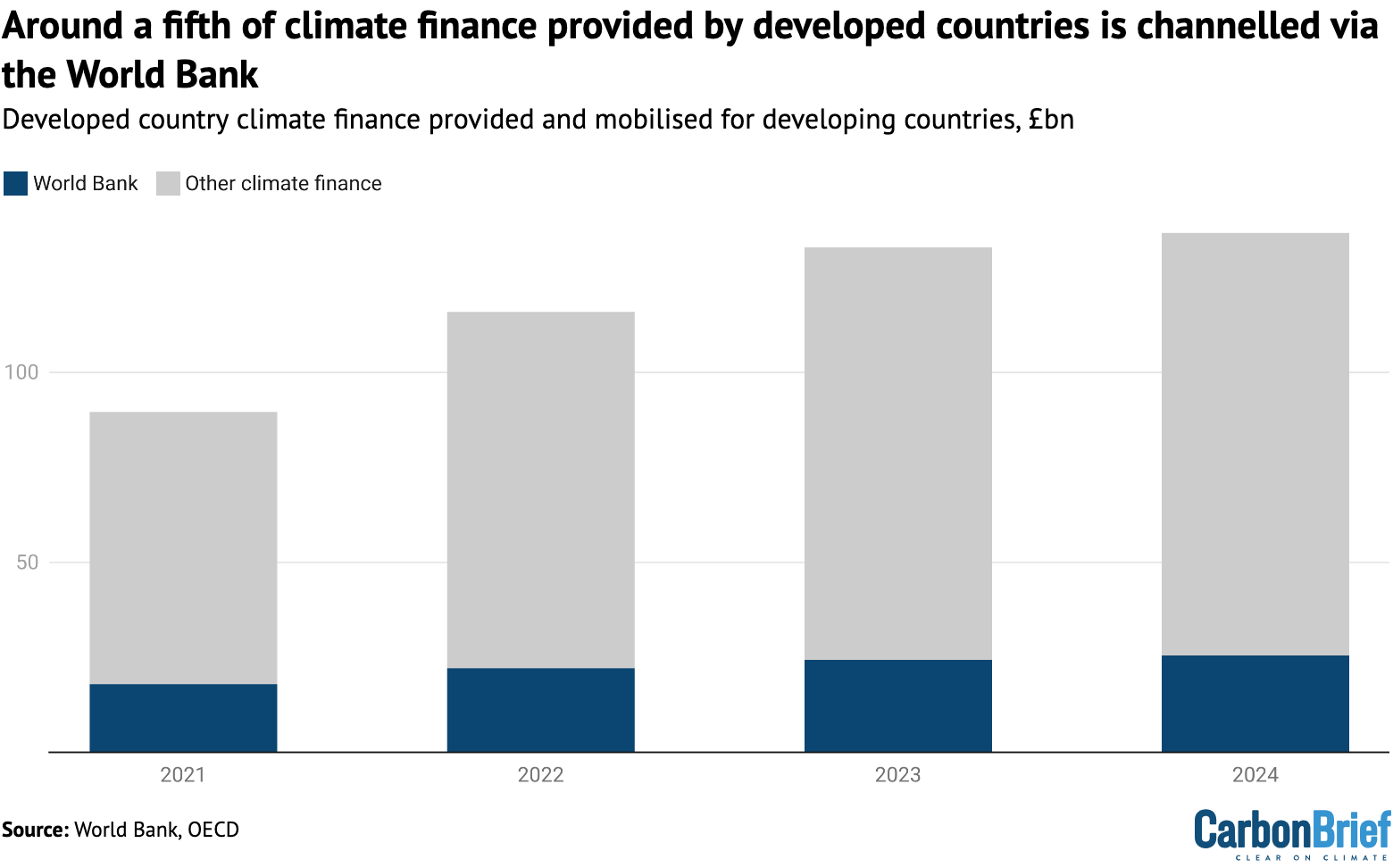

Carbon Brief analysis suggests that roughly a fifth of the international climate finance provided and “mobilised” by developed countries in recent years can be attributed to their World Bank contributions, as the chart below shows.

(This only accounts for the World Bank financing that can be linked to developed-country shares in the bank. Developing countries, such as China, also have significant shares, which are not included in the chart below.)

MDBs – including the World Bank – have committed to providing $120bn in climate finance to developing countries by 2030.

This was set to come from greater shareholder contributions, combined with a programme of reforms to free up capital.

If the World Bank continued to provide half of the MDB total, it would need to increase its climate finance by around 50%, from $39.2bn today to $60bn in 2030.

Therefore, experts see a “key” role for the World Bank in achieving not only the $300bn target, but also the more aspirational $1.3n target that countries agreed as part of the “new collective quantified goal” (NCQG) on climate finance at COP29 in 2024. This includes the private capital it could “unlock” through its lending.

Joe Thwaites, international climate finance director at Natural Resources Defense Council (NRDC), tells Carbon Brief that these “NCQG politics” are “quite important”. He says:

“The maths of the $300bn does not work if the MDBs pull back and so I think that’s why you’re seeing developed countries taking a stand.”

How will these changes affect global climate action?

To date, the World Bank has only released minimal details about its new climate plans. As such, experts say the impact on future climate finance remains uncertain.

Jon Sward, environment project manager at the Bretton Woods Project, tells Carbon Brief:

“They have said they are going to retain all the same processes about climate-finance reporting. So, of course, there is a world in which, actually, climate finance continues to increase like it has been.”

Some of the World Bank’s internal organisations will, in fact, keep their climate-finance goals for the time being. For example, the IDA’s largely grant-based funding retains a 45% target for its current round, which will last until 2028 – the year of the next US presidential election.

However, WRI’s Larsen tells Carbon Brief that the changes, from a bank that was previously a “champion for climate action”, remain significant:

“This reality, reinforced by the elimination of the 45% goal, means that it would not be surprising to see a reduction in climate investments.”

In a statement, the World Bank said its “work on climate is and will remain firmly client driven”, noting that it supports nations undertaking their Paris Agreement climate plans.

Therefore, its climate focus may come down to whether there is demand for climate action from “client” countries receiving finance.

At an April event in discussion with the climate sceptic Bjørn Lomborg, Bessent said that global financial institutions should focus on growth, characterising climate action as an “elite belief”.

The implication from the US Treasury secretary was that recipient countries are not interested in climate action. However, as reported by Devex, a group of World Bank shareholders representing nearly 100 developing countries, wrote a letter that appeared to push back against this framing.

This “G11+” group, led by Brazil and China, said the bank “must remain firmly client-driven”, noting that countries are “following nationally determined pathways toward climate action”. NRDC’s Thwaites tells Carbon Brief:

“It’s one thing for the Europeans to talk about climate…This was the client countries [100 developing countries] saying: ‘No, we want this.’”

Recent research by the ODI thinktank found that 79% of developing-country officials polled wanted to see MDB investment in solar projects, 54% wanted hydropower and 47% wanted wind power. Only 13% wanted investment in gas-power plants.

Rishikesh Ram Bhandary, a senior development researcher at Boston University, has stressed the need for an “enhanced CCAP”, which could be supported by the bank’s new independent evaluation. Among other things, he tells Carbon Brief:

“The bank needs to make a more convincing case about how climate change is being integrated into development priorities rather than competing with them.”

Thwaites says he is hopeful that the outcome is “mostly a symbolic victory for the US”.

However, he says major shareholders from Europe and elsewhere should make it clear to the bank that it is not “the only game in town” when it comes to climate finance. He says:

“If [the World Bank] are going to cave into one shareholder, when the vast majority of the other shareholders are supportive of continuing climate action, they can take their money elsewhere.”

The post Q&A: How will the World Bank’s abandoned finance goal affect climate action? appeared first on Carbon Brief.

Q&A: How will the World Bank’s abandoned finance goal affect climate action?

Rich Wilson is CEO of the Iswe Foundation and co-founder of the Global Citizens’ Assembly.

The numbers are stark. According to the 2026 Global Report on Food Crises, 266 million people across 47 countries experienced high levels of acute food insecurity last year, nearly double the figure recorded a decade ago.

Meanwhile, disruptions to oil, gas and fertiliser flows through the Strait of Hormuz drove a 46% month-on-month spike in urea prices early this year, sending agricultural price indices up 8% and raising the spectre of a global affordability crisis.

This is not a blip. It is a new baseline. The EAT-Lancet Commission concluded that food systems now account for roughly 30% of total greenhouse gas emissions and are the largest single contributor to the climate crisis. The science has been clear for years.

Now some of the solutions to the problem are becoming socially acceptable too.

-

Can giant batteries unlock Africa’s green industrial future?

Battery energy storage systems (BESS) could drive clean tech manufacturing in Africa but shortfalls in finance and data are still limiting deployment at scale

Earlier this year, people from more than 60 countries and territories, selected not by vested interest, but by lottery, spent seven weeks examining the evidence on food and climate for the latest Global Citizens’ Assembly. They heard from scientists, farmers and industry. They worked through 42 hours of structured deliberation, engaging with some difficult trade-offs.

They were not asked to endorse a predetermined conclusion. They were asked an open question: what changes, if any, should we make to how we grow, share and eat food, so that everyone has enough to nourish themselves while tackling the causes and impacts of climate change?

Phase down industrial animal farming

Their answer was unambiguous. They voted to protect forests. They voted to phase down industrial animal food production. They voted for supply chain reform and corporate accountability, explicitly rejecting the idea that the burden of change should fall on individual consumers. All 22 of their Calls to Action passed with over 85% support, a super-majority of randomly selected people from every region of the world, in agreement.

Consider what the assembly was actually being asked to decide. Industrial animal food production is the primary driver of tropical deforestation. Protecting more land as forest and ecosystem means less land available for the expansion of industrial production. That is a real trade-off, with real consequences for real livelihoods. Politicians have spent years avoiding it.

These randomly selected people looked at the evidence, deliberated across time zones and cultures, and chose the forests, with 64% in strong support and a further 20% in favour. People from livestock farming communities voted for change. Not because they were told to. Because deliberation led them there.

We estimate there have now been more than 7,000 citizen participation initiatives worldwide in the last decade. They have been organised because, as our 2025 report: People in the Lead demonstrated, people are now consistently and significantly ahead of politicians on issues ranging from climate to AI governance.

The people know best

What the research consistently shows is that ordinary people, given proper evidence and time, produce recommendations that are more effective and more aligned with public values than what emerges from elected legislatures. The gap in global governance is no longer primarily between science and the public. It is between citizens and their political leaders.

That gap matters for more than procedural reasons. When policy treats people as passive recipients rather than active participants, it leaves out the very actors whose behaviour, trust and consent the transition depends on. Institutions that speak only to other institutions, and negotiate only with state actors and industry lobbies, are missing out on the trust and energy of the people they are supposed to serve.

Governments, left to their own devices, are not moving fast enough to prove that argument wrong. At COP30 in Belém last November, countries failed to agree on a fossil fuel phaseout roadmap, and even full implementation of every submitted national climate plan still leaves the world on course for 2.3 to 2.8C of warming.

Citizens’ track at COP

But the Brazilian presidency grasped something important. Among the conference’s more significant outcomes was the formal launch of a Citizens’ Track within the UNFCCC process, a mechanism for connecting the global participation field to intergovernmental climate negotiations. Türkiye and Australia, who together hold the COP31 presidency in Antalya this November, now have the opportunity to strengthen and institutionalise what Brazil began.

In Guatemala, Indigenous women build climate resilience with old and new farming methods

The question before us is no longer whether citizens can contribute to solving these problems. Across the world, in local food networks, in community assemblies and in participatory planning processes, they already are, quietly generating more ambitious and more legitimate solutions than those emerging from formal diplomatic channels.

What is required now is the political courage to connect people to power. Not to consult citizens and file the results. Not to invite them to observe while the real decisions are made elsewhere. But to recognise the public as partners in perhaps the most consequential governance challenge of our time.

The post As food shocks spread, citizens are showing more leadership than governments appeared first on Climate Home News.

As food shocks spread, citizens are showing more leadership than governments

-

Climate Change11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Renewable Energy8 months ago

Renewable Energy8 months agoSending Progressive Philanthropist George Soros to Prison?

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases12 months ago

嘉宾来稿:探究火山喷发如何影响气候预测