In a major move, the U.S. Commerce Department announces preliminary anti-dumping duties of 93.5% on imports of Chinese graphite—a key input for electric vehicles (EV) batteries—after finding Chinese companies were selling it at unfairly low prices.

The duties affect up to $347 million in annual imports and could further disrupt U.S. battery supply chains. Analysts warn U.S. EV and battery manufacturers may face higher costs and production delays, while alternative suppliers rush to fill the gap.

The Unsung Hero Driving the EV Boom

Graphite is one of the most important materials used in EV batteries. It forms the anode, or negative electrode, in nearly all lithium-ion batteries—the type used in most EVs today. In fact, over 95% of all EV battery anodes rely on graphite.

Each electric vehicle contains between 50 and 100 kilograms of graphite, making it the largest battery component by mass and volume. The mineral allows lithium ions to move in and out of the battery during charging and discharging. This process helps EVs store energy, achieve long driving ranges, and charge quickly.

Graphite is also stable, durable, and cost-effective. It can handle thousands of charging cycles and helps prevent battery overheating. So far, there is no widely used alternative that offers the same performance at scale. Because of this, graphite is considered essential to the clean energy transition and a key mineral for the global EV industry.

U.S. Dependence on Chinese Graphite

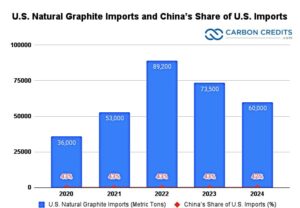

As of 2024, the U.S. imported about 60,000 metric tons of natural graphite, down from roughly 84,000 tons in 2023. China remained the largest supplier, accounting for around 67.6% of all natural graphite imports by value. This is worth roughly $375 million. It represents a slight decrease in volume but still a dominant share of the market.

As the chart shows, China has consistently played a major role in supplying graphite to the U.S., especially in high-purity forms used for EVs. But recent policy changes are reshaping this trade.

Tariff Shock: U.S. Takes Aim at Chinese Graphite

The U.S. government recently declared provisional anti-dumping duties of up to 93.5% on imports of Chinese anode-grade graphite. Officials said Chinese exporters were selling graphite in the U.S. at unfairly low prices, which hurt American manufacturers.

These duties could impact up to $347 million in graphite imports each year. The move is part of a broader effort to support domestic production of critical materials and reduce dependence on foreign sources.

While the tariffs aim to protect U.S. businesses, they could also raise costs for American EV and battery makers. Finding new suppliers—or building up local production—will take time and investment, as analysts warn.

China Strikes Back: Export Curbs Escalate the Conflict

China responded by tightening controls on its own exports of graphite and other critical minerals. In late 2024 and early 2025, China added export licenses for tungsten, molybdenum, tellurium, indium, and bismuth, on top of earlier restrictions for gallium and germanium. These materials are important for electronics, chipmaking, and green energy technologies.

By requiring companies to apply for permission to export these minerals, China aims to protect its national security and gain leverage in trade talks. So far, the approval process has slowed shipments, with more than 60% of applications still waiting for clearance.

Together, these actions show that minerals like graphite are becoming tools in the wider strategic competition between the U.S. and China.

Impacts on the EV and Tech Industry: Who’s Getting Hit the Hardest?

This growing tension is having a ripple effect across industries—especially electric vehicles, batteries, and semiconductors. Here’s how this tension impacts the said industries:

- EV Battery Production: Tariffs and export restrictions could raise the price of battery materials, making EVs more expensive to build. Slower or costlier production may hurt efforts to expand EV use across the U.S.

- Clean Energy Transition: Minerals like graphite, gallium, and rare earths are key to making wind turbines, solar panels, and other low-carbon technologies. Any disruption could delay progress toward climate goals.

- Semiconductors and AI Chips: The U.S. has already limited exports of advanced chip technology to China. In return, China is squeezing supplies of gallium and germanium, which are used in chipmaking. This tit-for-tat adds risk to global electronics supply chains.

Many countries are now rushing to diversify their sources and build resilient supply chains. The U.S., for example, is investing in domestic mining and processing, as well as partnerships with countries like Australia and Canada. But rebuilding this infrastructure will take time—often 3 to 5 years or more.

What’s Next in the Mineral Cold War?

Several key events will shape how this trade conflict evolves. Analysts predicted these major ones to occur.

Final U.S. Decision on Tariffs:

The current graphite duties are provisional. A final ruling is expected by December 5, 2025, and could keep or adjust the tariffs based on further review.

China’s Export Licenses:

As China decides which companies can continue exporting key minerals, delays and uncertainty may persist well into 2026.

Negotiations and Trade-Offs:

There is still room for dialogue. For example, recent reports suggest the U.S. may allow chipmakers like Nvidia to sell some AI chips to China in exchange for cooperation on rare earth exports.

This back-and-forth could continue for years. But both sides are now deeply focused on economic security, especially in strategic industries like batteries, semiconductors, and clean energy.

Beyond Batteries: How Minerals Shape Global Power Plays

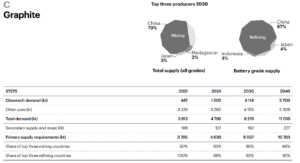

Graphite may seem like just another material, but it plays a big role in shaping the future of transportation and technology. For now, China leads the global market in graphite production and processing, both in 2024 and in 2030, as predicted by the IEA. The U.S., facing a supply risk, is using tariffs and domestic investments to try to close the gap.

At the same time, companies are watching closely. Automakers, battery makers, and tech giants all depend on stable access to key minerals. The next few years will show whether governments can build secure supply chains. Or whether trade tensions will disrupt the path to a cleaner, more connected world.

- FURTHER READING: DOE Supercharges the U.S. Battery and Critical Minerals Industry with $3 Billion Boost

The post US–China Trade Tensions Heat Up Over Graphite and EV Battery Supply Chains appeared first on Carbon Credits.

Most businesses have a clear picture of what happens inside their own operations. They track energy consumption, manage waste, and monitor the emissions produced on-site. What they often cannot see is everything that happens before a product reaches their facility, and everything that happens after it leaves.

![]()

Carbon Footprint

Texas-Based EnergyX’s Project Lonestar™ Signals a Turning Point for U.S. Lithium Supply

Energy Exploration Technologies, Inc. (EnergyX), led by CEO Teague Egan, has moved the United States closer to building a reliable domestic lithium supply chain. The company recently commissioned its Project Lonestar™ lithium demonstration facility in Texas, marking a key milestone in scaling direct lithium extraction (DLE) technologies.

This development comes at a time when lithium demand is rising sharply due to electric vehicles and energy storage systems. At the same time, the U.S. remains heavily dependent on foreign processing, particularly from China.

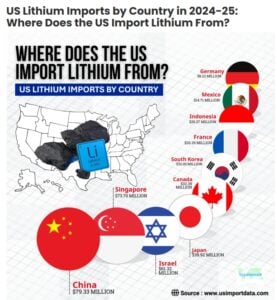

- According to the US import data and Lithium import data of the USA, the total value of US lithium imports reached $432.36 million in 2024, a 9% decline from the previous year.

- The total value of US lithium imports (cells & batteries) accounted for $205.29 million in the first 6 months of 2025.

Against this backdrop, EnergyX’s progress offers both technological validation and strategic value.

From Concept to Reality: How Project Lonestar™ Works

Project Lonestar™ is EnergyX’s first major lithium project in the United States and its second globally. The demonstration plant, located in the Smackover region spanning Texas and Arkansas, is now operational and uses industrial-grade systems rather than small pilot equipment.

- The facility produces around 250 metric tons per year of lithium carbonate equivalent (LCE).

While this output is modest compared to global supply, its importance lies in proving that EnergyX’s proprietary GET-Lit™ technology can efficiently extract lithium from brine. The plant processes locally sourced Smackover brine, a resource that has historically been underutilized despite its lithium potential.

Unlike traditional lithium production, which often relies on hard-rock mining or evaporation ponds, DLE technology directly extracts lithium from brine using advanced filtration and chemical processes. This reduces production time and may lower environmental impact.

- More importantly, the Lonestar™ plant can supply 5 to 25 tons of battery-grade lithium samples to customers.

This allows battery manufacturers to test and validate the material before committing to large-scale supply agreements.

Scaling Up: From Demonstration to Commercial Production

The demonstration plant is only the first phase of a much larger plan. EnergyX aims to scale Project Lonestar™ into a full commercial operation capable of producing 50,000 tonnes of LCE annually across two phases.

- The first phase alone targets 12,500 tonnes per year, which would already place it among the more significant lithium producers in the U.S.

- Significantly, the company has invested approximately $30 million in the demonstration facility, supported in part by a $5 million grant from the U.S. Department of Energy.

- For the full-scale project, EnergyX estimates total capital expenditure at around $1.05 billion.

Cost metrics suggest strong economic potential. The company estimates capital costs at roughly $21,000 per tonne of capacity and operating costs near $3,750 per tonne. If these figures hold at scale, the project could compete effectively with global lithium producers, particularly in a market where cost efficiency is becoming increasingly important.

Teague Egan, Founder & CEO of EnergyX, said,

“Bringing the biggest integrated DLE lithium demonstration plant online in the United States is a foundational milestone for EnergyX and for U.S. domestic lithium production in general. This facility not only validates the performance of our technology on an industrial scale under real-world conditions, but also establishes EnergyX as the lowest cost producer in the U.S. Ultimately this benefits all our customers who need large volumes of lithium for EV and ESS applications, as well as any lithium resource owners looking to implement best-in-class DLE technology whom we are happy to license to.”

Breaking the Bottleneck: Why U.S. Refining Matters

One of the biggest challenges facing the U.S. lithium sector is not resource availability but refining capacity. While lithium deposits exist across the country, most battery-grade lithium chemicals are processed overseas.

China dominates this segment, controlling roughly 70 to 75 percent of global lithium chemical conversion capacity. This concentration creates a structural dependency. Even when lithium is mined in the U.S. or allied countries, it is often shipped abroad for processing before returning as battery materials.

Project Lonestar™ directly addresses this gap. By integrating extraction and refining into a single domestic operation, EnergyX is working to build a complete “brine-to-battery” value chain within the United States. This approach could reduce reliance on foreign processing and improve supply chain resilience.

U.S. Senator Ted Cruz highlighted the project’s importance, noting that domestic lithium production supports both energy security and defense readiness, particularly for applications in advanced battery systems.

- CHECK: LIVE LITHIUM PRICES

The Current Landscape: Limited Supply, Big Ambitions

Investment is flowing into regions such as Nevada, North Carolina, and Arkansas. If even a portion of these reserves is converted into production, the U.S. could significantly reduce its reliance on imported lithium.

Active Resources and Future Potential

At present, U.S. lithium production remains relatively small. The only active large-scale operation is the Silver Peak Mine in Nevada, which produces between 5,000 and 10,000 tonnes of LCE annually, depending on market conditions.

However, several projects are in development that could significantly expand capacity. The Thacker Pass project, for example, is expected to produce around 40,000 tonnes per year in its first phase once operational later in the decade.

In addition, brine-based developments in the Smackover region aim to produce tens of thousands of tonnes annually, with long-term plans exceeding 100,000 tonnes across multiple sites.

These projects indicate a shift from a niche domestic industry to a more substantial production base. Still, timelines remain uncertain due to regulatory and financial challenges.

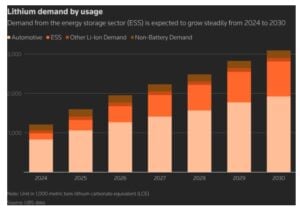

Demand Surge: Batteries Drive the Lithium Boom

The urgency to expand lithium production is driven by rapid growth in battery demand. Electric vehicles, renewable energy storage, and grid modernization are all increasing lithium consumption.

According to S&P Global, U.S. lithium demand is expected to grow at an average rate of 40 percent annually between 2024 and 2029. Canada is projected to see even faster growth, albeit from a smaller base, with demand rising by around 74 percent per year over the same period.

Globally, battery capacity is forecast to approach 4 terawatt-hours by 2030. This expansion highlights lithium’s central role in the clean energy transition. Without sufficient supply, battery production—and by extension, EV adoption—could face constraints.

Why Progress Takes Time

Turning lithium reserves into operational mines and processing facilities is not straightforward. Projects often face long permitting timelines, environmental scrutiny, and legal challenges. Financing can also be difficult, especially in a volatile commodity market.

Local opposition can further complicate development, particularly in areas with high environmental concerns. These factors can delay projects by several years, slowing the pace of expansion.

To address these barriers, the U.S. government is increasing its involvement through funding, policy support, and efforts to streamline permitting. The Department of Energy’s backing of EnergyX reflects a broader strategy to accelerate domestic critical mineral development.

Conclusion: A Strategic Shift in Motion

Project Lonestar™ represents a meaningful step toward reshaping the U.S. lithium landscape. By proving the viability of direct lithium extraction at an industrial scale, EnergyX has laid the groundwork for larger, commercially viable operations.

The project also aligns with national priorities around energy security, supply chain resilience, and clean energy transition. While challenges remain, the combination of technological innovation, government support, and rising demand creates a strong foundation for growth.

As the world moves toward electrification, lithium will remain at the center of the transition. Projects like Lonestar™ show that the United States is beginning to close the gap between resource potential and real-world production—one facility at a time.

The post Texas-Based EnergyX’s Project Lonestar™ Signals a Turning Point for U.S. Lithium Supply appeared first on Carbon Credits.

Carbon Footprint

Canada Doles Out Almost C$29M for CCUS and Renewables as Clean Energy Market Surges

Canada has pledged nearly C$29 million ($21.6 million) to support carbon capture, utilization, and storage (CCUS) and renewable energy projects. The funding aims to back new technologies that reduce greenhouse gas emissions and make clean energy more competitive. This commitment was announced by the Canadian government in late March 2026 as part of ongoing efforts to meet climate goals.

The investment is small compared with Canada’s larger climate budget. But it signals continued federal support for emerging technologies and deployment of clean energy solutions. CCUS is one of several tools that nations are using to curb emissions while keeping energy supplies stable.

What Canada Is Funding? Inside the C$29M Clean Tech Bet

The C$29 million pledge covers a mix of CCUS and renewable energy efforts. It is intended for 12 projects that capture carbon dioxide (CO₂) from industrial emissions. It also supports systems that convert captured CO₂ into usable products or store it underground so it cannot enter the atmosphere.

The Honourable Tim Hodgson, Minister of Energy and Natural Resources, said:

“Canada is scaling up clean energy while strengthening our electricity grid and responsibly growing our conventional energy industry — because competitiveness means doing more than one thing at the same time. We are investing to provide reliable, affordable and clean power across the country that will propel our economic growth, protect affordability for Canadian families and make Canada a low-risk, low-cost, low-carbon energy superpower.”

Carbon capture refers to systems that trap CO₂ from power plants and factories before it is released. The captured gas can be stored deep underground or used in industrial processes, such as making building materials or fuels. Utilization means finding commercial uses for captured CO₂ so that it has economic as well as environmental value.

Renewable energy projects in Canada focus on expanding wind, solar, hydro, and other low‑carbon power sources. As of 2024, about 79 % of Canada’s electricity generation came from low‑carbon sources, with hydropower alone accounting for roughly 55 %. The rest comes from wind, solar, and nuclear energy.

Carbon Capture’s Strategic Role in Net Zero

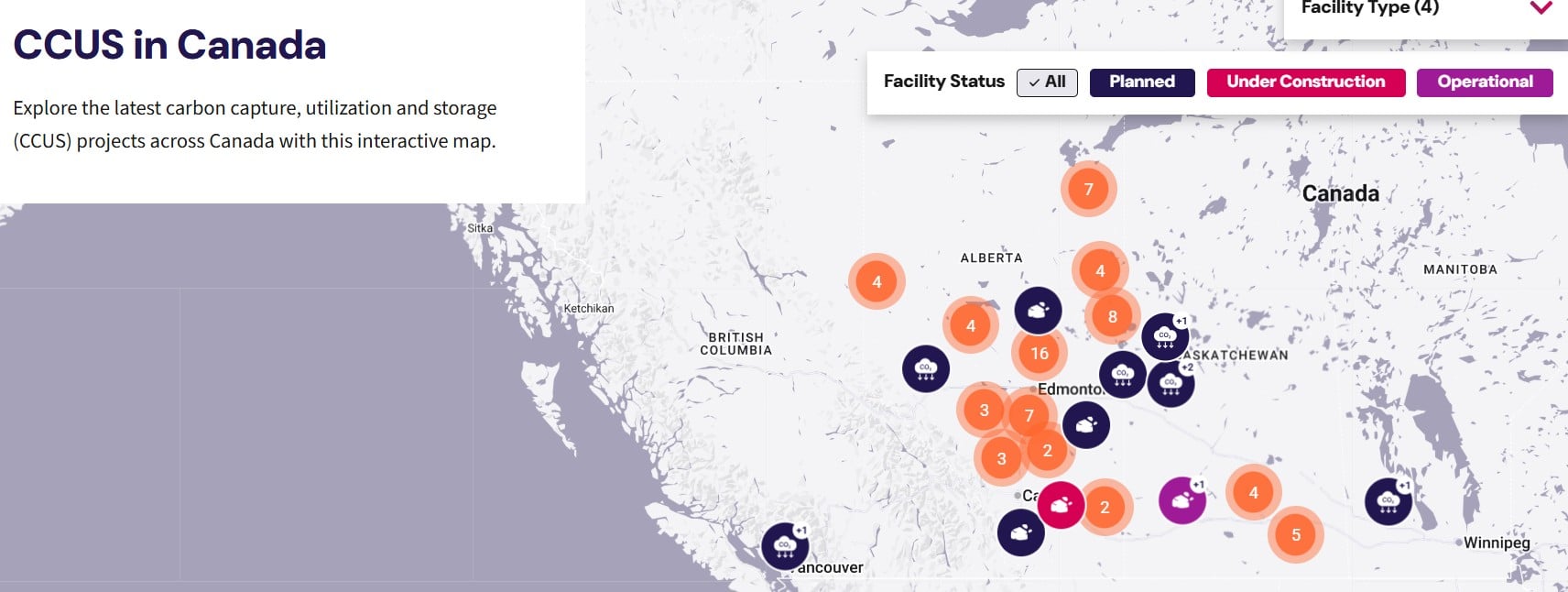

Canada has a strong track record in CCUS deployment. Several large‑scale facilities already operate in the country, especially in Alberta and Saskatchewan.

For example, the Quest Carbon Capture and Storage Project in Alberta captures about one million tonnes of CO₂ per year and stores it deep underground.

Canadian CCUS technology accounts for a notable share of planned global capacity. Canadian projects represent about 11.5 % of planned CCUS storage capacity worldwide.

Notably, Canada’s carbon capture capacity could increase from about 4.4 million tonnes of CO₂ per year to 16.3 million tonnes annually by 2030. However, much larger growth is still necessary to meet net-zero targets by 2050.

CCUS is considered critical for reducing emissions from hard‑to‑decarbonize sectors like heavy industry and oil and gas. It also plays an important role in achieving Canada’s long‑term climate targets, including net-zero emissions by 2050. In these scenarios, CCUS helps bridge gaps that electrification and renewables alone cannot fill.

Canada’s Energy Innovation Program (EIP) is designed to speed up the development of clean energy technologies while keeping the energy system reliable and affordable. It supports early-stage research and development in CCUS.

The program also funds renewable energy demonstration projects that test new ways to generate and integrate clean power, especially those with local benefits. In addition, EIP promotes innovation in electricity systems by supporting new approaches to smart grid regulation and capacity building.

A Power Mix Already Going Green

Renewable energy is another core part of Canada’s climate strategy. Over the last decade, installed renewable capacity has grown steadily. Between 2014 and 2024, Canada’s total renewable energy capacity increased from about 89,773 MW to 110,470 MW.

The federal government has supported renewable projects through multiple funding programs. Earlier initiatives included a $964‑million investment targeting wind, solar, storage, hydro, and other renewable technologies.

Canada has also set decarbonization targets tied to renewables. The country aims for net‑zero electricity by 2035, which supports a broader economy‑wide goal of net‑zero greenhouse gas emissions by 2050.

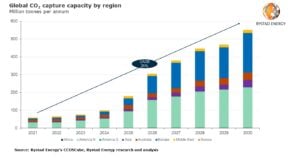

CCUS and Renewables on a Global Rise

Investment in CCUS and renewable energy is rising globally. According to industry forecasts, the global clean energy market — including wind, solar, energy storage, and CCUS — is expected to continue strong growth through 2030 as countries push toward climate targets.

For CCUS specifically, analysts project that global installed capacity could grow fivefold by 2030 as more projects move from demonstration to full deployment. Canada is among several countries with mature CCUS infrastructure and planned expansions.

Renewables continue to be the fastest‑growing energy source globally. International agencies like the International Renewable Energy Agency (IRENA) project that renewable capacity will keep expanding rapidly through the end of the decade, driven by falling technology costs and climate commitments.

The Roadblocks to Scaling Clean Tech

While CCUS has potential, it also faces hurdles. Costs are high, and the technologies are still emerging at scale. Critics argue that CCUS has historically underperformed in some early projects, and that a significant amount of captured CO₂ is used in enhanced oil recovery rather than stored permanently.

Some stakeholders also warn that public funds for CCUS must be carefully targeted to avoid subsidizing continued fossil fuel use rather than meaningful emission cuts. Despite these concerns, many policymakers see CCUS as an essential component of climate strategy if Canada is to meet its 2030 and 2050 goals.

Renewable energy projects also face challenges, including grid integration, siting barriers, and supply chain constraints for equipment like turbines and solar panels. However, continued funding and clear policy signals tend to reduce these barriers over time as markets mature.

Cutting Emissions While Keeping Energy Stable

Canada’s C$29 million commitment fits into a broader pattern of public funding aimed at accelerating clean energy and decarbonization technologies. Larger federal efforts, such as the Net Zero Accelerator Initiative, provide billions of dollars over multiple years for clean tech, including CCUS deployment and industrial decarbonization.

The CCUS market is evolving from pilot projects to commercial opportunities. Meanwhile, renewable energy continues its growth as a mainstream power source. Together, these developments support Canada’s long‑term climate and economic goals.

As the global energy landscape changes, investments in both CCUS and renewables help reduce emissions, create jobs, and build resilience in a low‑carbon economy. Canada’s latest funding pledge reinforces its ongoing role in these key markets.

- READ MORE: Canada Approves First Uranium Mine in 20 Years as Tech Giants Eye Nuclear Fuel for AI Power

The post Canada Doles Out Almost C$29M for CCUS and Renewables as Clean Energy Market Surges appeared first on Carbon Credits.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits