Surge Battery Metals (TSX-V: NILI | OTCQX: NILIF | FRA: DJ5C) delivered two strong updates from its Nevada North Lithium Project (NNLP) in February 2026. Together, these results confirm expansion potential, reinforce high-grade continuity, and advance technical work needed for the upcoming Pre-Feasibility Study (PFS).

On February 17, Surge reported a major step-out success. The company drilled a 31-meter intercept grading 4,196 ppm lithium from surface in a hole located 640 meters southeast of the existing resource boundary. This intercept sits well above the current resource average grade of 3,010 ppm lithium. The wide step-out confirms that high-grade mineralization extends significantly beyond the defined resource footprint.

Just one week later, on February 25, Surge released the final batch of results from its 2025 core drilling program. These infill holes focused on upgrading inferred resources to higher confidence categories and collecting technical data for the PFS. The results returned some of the strongest intercepts drilled to date.

Together, these two updates strengthen the project’s scale, quality, and development readiness.

Infill Drilling Confirms a Thick, High-Grade Core

The February 25 news highlighted Hole NNL-030 as a standout result. The hole intersected 116 meters, averaging 3,752 ppm lithium. Within that interval, a 32.1-meter zone graded 4,521 ppm lithium. These grades exceed the project’s current average and confirm the presence of a thick, ultra-high-grade core.

Hole NNL-032 also delivered strong results, returning 82.29 meters, averaging 3,664 ppm lithium. Hole NNL-036 intersected 78.63 meters, averaging 3,141 ppm lithium, including a deep 9.4-meter zone grading 4,580 ppm lithium.

These intercepts show both lateral and vertical continuity. They show that high-grade lithium persists across wide widths and at depth. Importantly, most of these zones occur near the surface. Near-surface mineralization reduces stripping requirements and can improve early-year mine economics.

The infill drilling supports resource upgrading efforts. It helps convert Inferred resources into Indicated and Measured categories. Higher confidence categories are critical for mine planning, financing, and permitting.

The results confirm that Nevada North’s high-grade core is consistent, thick, and scalable.

Mr. Greg Reimer, President & Chief Executive Officer and Director of Surge, stated,

“This infill drilling is doing exactly what it was designed to do: upgrade the resource, confirm continuity of some of our best lithium intercepts, and de-risk the early years of a potential mine plan at Nevada North. Coupled with a robust PEA economic profile, we believe Nevada North is strongly positioned as we move forward with the development of our PFS. We look forward to updating the Mineral Resource Estimate as our next key milestone.”

Expansion Beyond the Current Resource Boundary

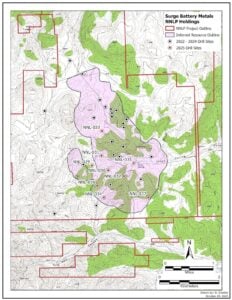

The February 17 step-out result adds a new dimension to the project story. The 31-meter intercept grading 4,196 ppm lithium occurred 640 meters beyond the existing resource area. This large extension demonstrates strong mineral continuity outside the current pit-constrained model.

Step-out drilling is important because it tests the limits of a deposit. A successful 640-meter extension suggests the deposit remains open and may support future resource growth.

Nevada North already hosts a pit-constrained Inferred Resource of 11.24 million tonnes of lithium carbonate equivalent (LCE) grading 3,010 ppm lithium at a 1,250 ppm cutoff. High-grade step-out intercepts increase confidence that future resource updates may expand both tonnage and overall contained lithium.

Highly anomalous soil values and geophysical surveys also suggest the clay horizons could extend even further. The mineralized zone currently spans more than 4,300 meters in strike length and over 1,500 meters in width. Continued drilling could increase the overall scale of the project.

This combination of strong infill and wide step-out success strengthens Nevada North’s long-term growth profile.

Advancing Toward Pre-Feasibility and Permitting

The 2025 drilling program did more than confirm grade. It also collected critical technical data required for the upcoming PFS and environmental permitting.

Hole NNL-035 was strategically positioned near Texas Spring to gather hydrogeological data. The hole successfully installed the Vibrating Wire Piezometers (VWPs) to monitor groundwater conditions. This data will help model basin hydrology and support environmental approvals.

The company also completed detailed geotechnical logging across all holes. High-resolution televiewer surveys mapped fault structures. Representative samples from each rock unit are now undergoing rock strength testing. These tests will help determine safe pit wall angles for future mine planning.

Remarkably, quality control procedures were rigorous. Of the 806 total samples analyzed, 134 were QA/QC samples. Certified reference standards, blanks, and duplicates were systematically inserted.

Standards are performed within acceptable limits. Duplicate samples fell within 10% tolerance. These results confirm strong analytical accuracy and reproducibility.

This technical work reduces development risk. This, in turn, ensures that the PFS is built on high-quality geological and engineering data.

Strategic Upside: By-Products and Strong Economics

In addition to lithium, the infill drilling consistently returned elevated cesium and rubidium values. Cesium reached up to 163 ppm and rubidium up to 349 ppm in association with the lithium core. Surge is evaluating the deportment of these elements in ongoing metallurgical studies.

If recoverable, these critical minerals could add value to the project economics. By-product potential can improve revenue streams and enhance overall project returns.

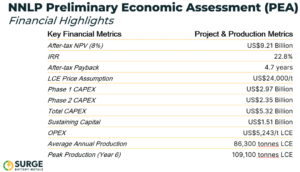

Nevada North already shows strong economic metrics from its Preliminary Economic Assessment. The PEA reports an after-tax NPV (8%) of approximately US$9.17 billion and an after-tax IRR of 22.8% at a lithium price of US$24,000 per tonne LCE. Operating costs are estimated at roughly US$5,243 per tonne LCE.

High grades play a central role in these economics. Thick intervals averaging 3,500–4,500 ppm lithium reduce the tonnage required to produce each unit of lithium. This supports lower operating costs and stronger early cash flow potential.

The joint venture with Evolution Mining also strengthens the project’s development pathway. Evolution is a globally recognized mining company with operational expertise. This partnership adds technical depth and financial strength to the Nevada North project.

A Strengthened Position in the U.S. Lithium Landscape

The United States is working to strengthen its domestic lithium supply chain. Federal incentives and policy measures emphasize secure, locally sourced battery materials. Projects that combine high grade, large scale, and technical readiness are well-positioned in this environment.

Nevada North now demonstrates three key strengths at once:

- Proven high-grade core through infill drilling,

- Expansion potential through 640-meter step-out success, and

- Advancing technical data for PFS and permitting.

These updates reinforce Nevada North as one of the highest-grade lithium clay projects in the United States. They show both growth and de-risking in the same drilling campaign.

As global demand for lithium continues to rise, supply sources with strong grade, scale, and development momentum will stand out. Surge Battery Metals’ recent results highlight meaningful progress on all three fronts.

The company’s Nevada North Lithium Project is not only expanding. It is advancing toward higher confidence resources, improved technical definition, and future development milestones. These combined achievements strengthen Surge’s position within the evolving North American lithium supply chain.

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $50,000 to provide marketing services for a term of two months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2024, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

The post Surge Battery Metals Strengthens Nevada North With High-Grade Expansion and Infill Success appeared first on Carbon Credits.

Carbon Footprint

Philippines Taps Blue Carbon and Biodiversity Credits to Protect Coasts and Climate

The Philippines is stepping up efforts to protect its coastal ecosystems. The government recently advanced its National Blue Carbon Action Partnership (NBCAP) Roadmap. This plan aims to conserve and restore mangroves, seagrass beds, and tidal marshes. It also explores biodiversity credits — a new market linked to nature conservation.

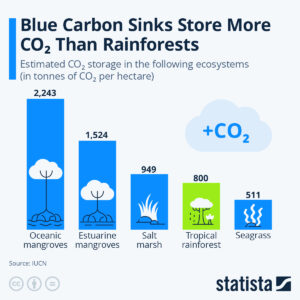

Blue carbon refers to the carbon stored in coastal and marine ecosystems. These habitats can hold large amounts of carbon in plants and soil. Mangroves, for example, store carbon at much higher rates than many land forests. Protecting them reduces greenhouse gases in the atmosphere.

Biodiversity credits are a related concept. They reward actions that protect or restore species and ecosystems. They work alongside carbon credits but focus more on ecosystem health and species diversity. Markets for biodiversity credits are being discussed globally as a complement to carbon markets.

Why the Philippines Is Targeting Blue Carbon

The Philippines is rich in coastal ecosystems. It has more than 327,000 hectares of mangroves along its shores. These areas protect coastlines from storms, support fisheries, and store carbon.

Mangroves and seagrasses also support high levels of biodiversity. Many fish, birds, and marine species depend on these habitats. Restoring these ecosystems helps conserve species and supports local food systems.

The NBCAP Roadmap was handed over to the Department of Environment and Natural Resources (DENR) during the Philippine Mangrove Conference 2026. The roadmap is a strategy to protect blue carbon ecosystems while linking them to climate goals and local livelihoods.

DENR Undersecretary, Atty. Analiza Rebuelta-Teh, remarked during the turnover:

“This Roadmap reflects the Philippines’ strong commitment to advancing blue carbon accounting and delivering tangible impact for coastal communities.”

Edwina Garchitorena, country director of ZSL Philippines, which will oversee its implementation, also commented:

“The handover of the NBCAP Roadmap to the DENR represents a turning point in advancing blue carbon action and strengthening the Philippines’ leadership in coastal conservation in the region.”

The plan highlights four main pillars:

- Science, technology, and innovation.

- Policy and governance.

- Communication and community engagement.

- Finance and sustainable livelihoods.

These pillars aim to strengthen coastal resilience, support community well‑being, and align blue carbon action with national climate commitments.

What Blue Carbon Credits Could Mean for Markets

Globally, blue carbon markets are growing. These markets allow coastal restoration projects to sell carbon credits. Projects that preserve or restore mangroves, seagrass meadows, and tidal marshes can generate credits. Buyers pay for these credits to offset emissions.

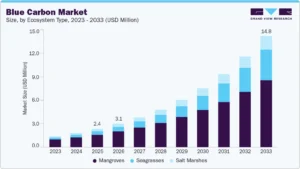

According to Grand View Research, the global blue carbon market was valued at US$2.42 million in 2025. It is projected to reach US$14.79 million by 2033, growing at a compound annual growth rate (CAGR) of almost 25%.

The Asia Pacific region led the market in 2025, with 39% of global revenue, due to its extensive coastal ecosystems and government support. Within the market, mangroves accounted for 68% of revenue, reflecting their high carbon storage capacity.

Blue carbon credits belong to the voluntary carbon market. Companies purchase these credits to offset emissions they can’t eliminate right now. Buyers are often motivated by sustainability goals and environmental, social, and corporate governance (ESG) standards.

Experts at the UN Environment Programme say these blue habitats can capture carbon 4x faster than forests:

Why Biodiversity Credits Matter: Rewarding Species, Strengthening Ecosystems

Carbon credits aim to cut greenhouse gases. In contrast, biodiversity credits focus on saving species and habitats. These credits reward projects that improve ecosystem health and may be used alongside carbon markets to attract finance for nature.

Biodiversity credits are particularly relevant in the Philippines, one of 17 megadiverse countries. The nation is home to thousands of unique plant and animal species. Supporting biodiversity through market mechanisms can strengthen conservation efforts while also supporting local communities.

Globally, biodiversity credit markets are still developing. Organizations such as the Biodiversity Credit Alliance are creating standards to ensure transparency, equity, and measurable outcomes. They want to link private investment to good environmental outcomes. They also respect the rights of local communities and indigenous peoples.

These markets complement carbon markets. They can support conservation efforts. This boosts ecosystem resilience and protects species while also capturing carbon.

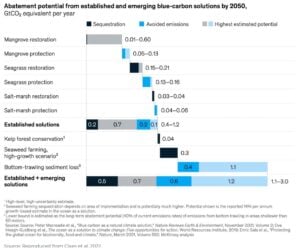

Together with blue carbon credits, they form part of a broader nature-based solution to climate change and biodiversity loss. A report by the Ecosystem Marketplace estimates the potential carbon abatement for every type of blue carbon solution by 2050.

Science, Policy, and Funding: The Roadblocks Ahead

Building blue carbon and biodiversity credit markets is not easy. There are several challenges ahead for the Philippines.

One key challenge is measurement and verification. To sell carbon or biodiversity credits, projects must prove they deliver real and measurable benefits. This requires science‑based methods and monitoring systems.

Another challenge is finance. Case studies reveal that creating a blue carbon action roadmap in the Philippines may need around US$1 million. This funding will help set up essential systems and support initial actions.

Policy frameworks are also needed. Laws and rules must support credit issuance, protect local rights, and ensure fair sharing of benefits. Coordination across government agencies, local communities, and investors will be important.

Stakeholder engagement is key. The NBCAP Roadmap and related forums involve scientists, policymakers, civil society, and private sector partners. This teamwork approach makes sure actions are based on science, inclusive, and fair in the long run.

Looking Ahead: Coastal Conservation as Climate Strategy

Blue carbon and biodiversity credits could provide multiple benefits for the Philippines. Protecting and restoring coastal habitats reduces greenhouse gases, conserves species, and supports local economies. Coastal ecosystems also provide natural defenses against storms and rising seas.

If blue carbon and biodiversity credit markets grow, they could fund coastal conservation at scale while supporting global climate targets. Biodiversity credits could further enhance ecosystem protection by linking nature’s intrinsic value to market mechanisms.

The market also involves climate finance and corporate buyers looking for quality credits. Additionally, international development partners focused on coastal resilience may join in.

For the Philippines, the next few years will be critical. Implementing the NBCAP roadmap, establishing credit systems, and strengthening governance could unlock new opportunities for climate action, sustainable development, and regional leadership in blue carbon finance.

The post Philippines Taps Blue Carbon and Biodiversity Credits to Protect Coasts and Climate appeared first on Carbon Credits.

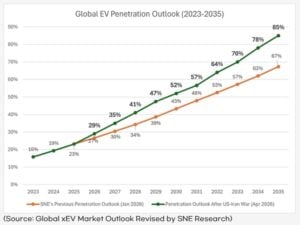

The global electric vehicle (EV) market is gaining speed again. A sharp rise in oil prices, triggered by the recent U.S.–Iran conflict in early 2026, has changed how consumers think about fuel and mobility. What looked like a slow market just months ago is now showing strong signs of recovery.

According to SNE Research’s latest report, this sudden shift in energy markets is pushing EV adoption faster than expected. Rising gasoline costs and uncertainty about future oil supply are driving buyers toward electric cars. As a result, the EV transition is no longer gradual—it is accelerating.

Oil Price Shock Changes Consumer Behavior

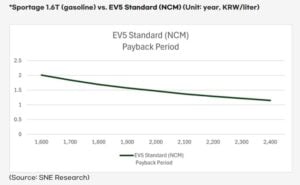

The conflict in the Middle East sent oil markets into turmoil. Gasoline prices jumped quickly, rising from around 1,600–1,700 KRW per liter to as high as 2,200 KRW. This sudden spike acted as a wake-up call for many drivers.

Consumers who once hesitated to switch to EVs are now rethinking their choices. High and unstable fuel prices have made traditional gasoline vehicles less attractive. At the same time, EVs now look more cost-effective and reliable over the long term.

SNE Research noted that even if oil prices stabilize later, the fear of future spikes will remain. This uncertainty is a key driver behind early EV adoption. People no longer want to depend on volatile fuel markets.

EV Growth Forecasts Get a Major Boost

SNE Research has revised its global EV outlook. The firm now expects faster adoption across the decade.

- EV market penetration is projected to reach 29% in 2026, up from an earlier estimate of 27%.

- By 2027, the share could jump to 35%, instead of the previously expected 30%.

- Most importantly, EVs are now expected to cross 50% of new car sales by 2030, earlier than prior forecasts.

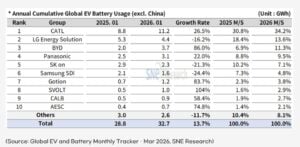

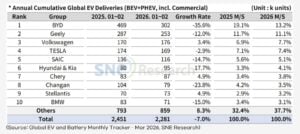

The post Global EV Sales Set to Hit 50% by 2030 Amid Oil Shock While CATL Leads Batteries appeared first on Carbon Credits.

Carbon Footprint

AI Data Centers Power Crisis: Massive Energy Demand Threatens Emissions Targets and Latest Delays Signal Market Shift

The rapid growth of artificial intelligence (AI) is creating a new challenge for global energy systems. AI data centers now require far more electricity than traditional computing facilities. This surge in demand is putting pressure on power grids and raising concerns about whether climate targets can still be met.

Large AI data centers typically need 100 to 300 megawatts (MW) of continuous power. In contrast, conventional data centers use around 10-50 MW. This makes AI facilities up to 10x more energy-intensive, depending on the scale and workload.

AI Data Centers Are Driving a Sharp Rise in Power Demand

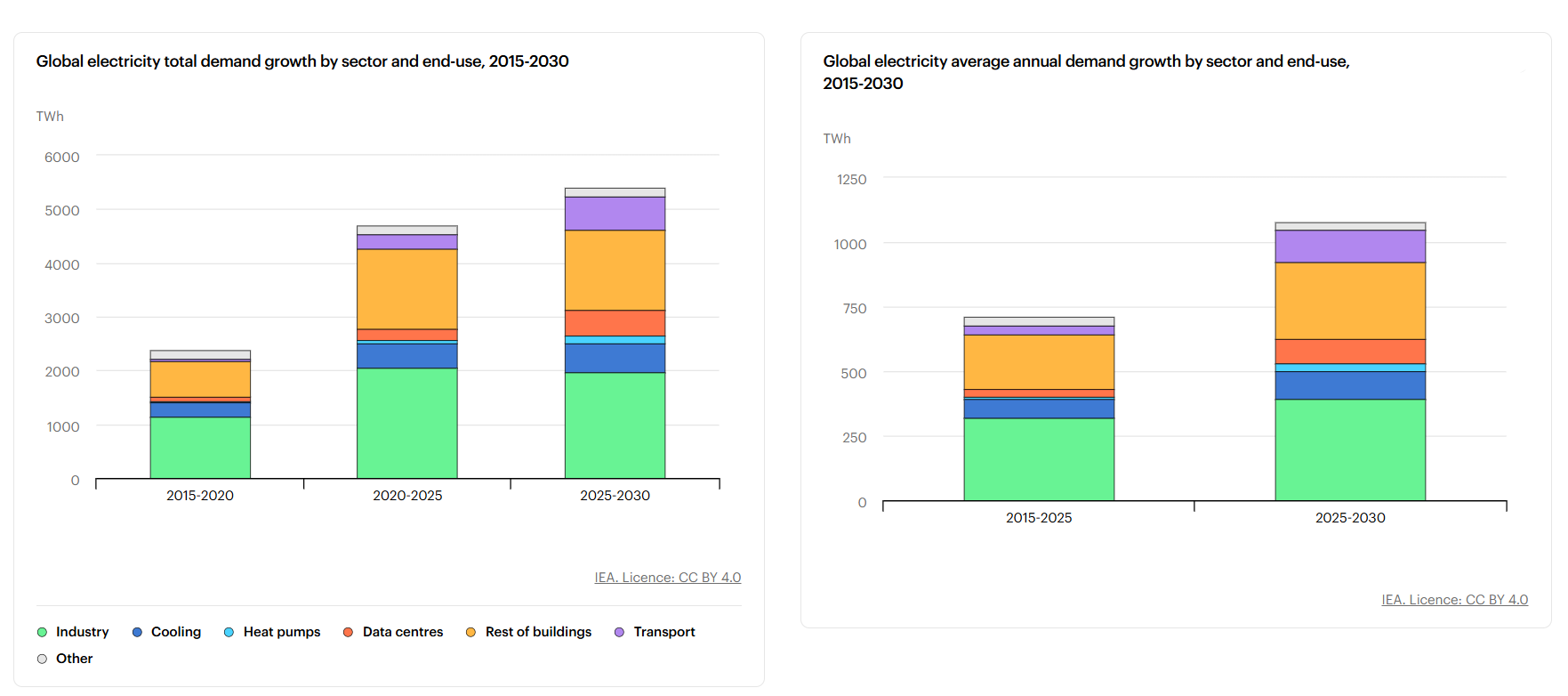

The increase is happening quickly. The International Energy Agency estimates that global data center electricity use reached about 415 terawatt-hours (TWh) in 2024. That number could rise to more than 1,000 TWh by 2026, largely driven by AI applications such as machine learning, cloud computing, and generative models.

At that level, data centers would consume as much electricity as an entire mid-sized country like Japan.

In the United States, the impact is also growing. Data centers could account for 6% to 8% of total electricity demand by 2030, based on utility projections and grid operator estimates. AI is expected to drive most of that increase as companies continue to scale infrastructure to support new applications.

Training large AI models is especially energy-intensive. Some estimates say an advanced model can use millions of kilowatt-hours (kWh) just for training. For instance, training GPT-3 needs roughly 1.287 million kWh, and Google’s PaLM at about 3.4 million kWh. Analytical estimates suggest training newer models like GPT-4 may require between 50 million and over 100 million kWh.

That is equal to the annual electricity use of hundreds of households. When combined with ongoing usage, known as inference, total energy consumption rises even further.

This rapid growth is creating a gap between electricity demand and available supply. It is also raising questions about how the technology sector can expand while staying aligned with global climate goals.

The Grid Bottleneck: Why Data Centers Are Waiting Years for Power

Power demand from AI is rising faster than grid infrastructure can support. Utilities in key regions are now facing a surge in interconnection requests from technology companies building new data centers.

This has led to delays in several major projects. In many cases, developers must wait years before they can secure enough electricity to operate. These delays are becoming more common in established tech hubs where grid capacity is already stretched.

The main constraints include:

- Limited transmission capacity in high-demand areas,

- Slow grid upgrades and long permitting timelines, and

- Regulatory systems not designed for AI-scale demand.

Grid stability is another concern. AI data centers require constant and uninterrupted power. Even short disruptions can affect performance and reliability. This makes it more difficult for utilities to balance supply and demand, especially during peak periods.

In some regions, utilities are struggling to manage the size and concentration of new loads. A single large data center can use as much electricity as a small city. When several projects are planned in the same area, the pressure on local infrastructure increases significantly.

As a result, some companies are rethinking their expansion strategies. Projects may be delayed, scaled down, or moved to new locations where energy is more accessible. These shifts could slow the pace of AI deployment, at least in the short term.

Renewable Energy Growth Faces a Reality Check

Technology companies have made strong commitments to clean energy. Many aim to power their operations with 100% renewable electricity. This is part of their larger environmental, social, and governance (ESG) goals.

For example, Microsoft plans to become carbon negative by 2030, meaning it will remove more carbon than it emits. Google is targeting 24/7 carbon-free energy by 2030, which goes beyond annual matching to ensure clean power is used at all times. Amazon has committed to reaching net-zero carbon emissions by 2040 under its Climate Pledge.

Despite these targets, AI data centers present a difficult challenge. They need reliable electricity around the clock, while renewable energy sources such as wind and solar are not always available. Output can vary depending on weather conditions and time of day.

To maintain stable operations, many facilities rely on a mix of energy sources. This often includes grid electricity, which may still be partly generated from fossil fuels. In some cases, natural gas backup systems are used more frequently than planned.

Battery storage can help balance supply and demand. However, long-duration storage remains expensive and is not yet widely deployed at the scale needed for large AI facilities. This creates both technical and financial barriers.

Thus, there is a growing gap between corporate clean energy goals and real-world energy use. Closing that gap will require faster deployment of renewable energy, improved storage solutions, and more flexible grid systems.

Carbon Credits Use Surge as Tech Tries to Close the Emissions Gap

The mismatch between AI growth and clean energy supply is also affecting carbon markets. Many technology companies are increasing their use of carbon credits to offset emissions linked to data center operations.

According to the World Bank’s State and Trends of Carbon Pricing 2025, carbon pricing now covers over 28% of global emissions. But carbon prices vary widely—from under $10 per ton in some systems to over $100 per ton in stricter markets. This gap is pushing companies toward voluntary carbon markets.

The Ecosystem Marketplace report shows rising demand for high-quality credits, especially carbon removal rather than avoidance credits. But supply is still limited.

Costs are especially high for engineered removals. The IEA estimates that direct air capture (DAC) costs today range from about $600 to over $1,000 per ton of CO₂. It may fall to $100–$300 per ton in the future, but supply is still very small.

Companies are focusing on credits that:

- Deliver verified emissions reductions,

- Support long-term carbon removal, and

- Align with ESG and net-zero commitments.

At the same time, many firms are taking a more active role in energy development. Instead of relying only on offsets, they are investing directly in renewable energy projects. This includes funding new solar and wind farms, as well as entering long-term power purchase agreements.

These investments help secure a dedicated clean energy supply. They also reduce long-term exposure to carbon markets, which can be volatile and subject to changing standards.

Companies Are Adapting Their Energy Strategies: The New AI Energy Playbook

AI companies are changing how they design and operate data centers to manage rising energy demand. Here are some of the key strategies:

- Energy efficiency improvements (new hardware and cooling systems) that reduce data center power use.

- More efficient AI chips, specialized processors, that drive performance gains.

- Advanced cooling systems that cut energy waste and can help cut total power use per workload by 20% to 40%.

- Data center location strategy is shifting, where facilities are built in regions with stronger renewable energy access.

- Infrastructure is becoming more distributed, where firms deploy smaller data centers across multiple locations to balance demand and improve resilience.

- Long-term renewable energy contracts are expanding, which helps companies secure power at stable prices.

A Turning Point for Energy and Climate Goals

The rise of AI is creating both risks and opportunities for the global energy transition. In the short term, increased electricity demand could lead to higher emissions if fossil fuels are used to fill supply gaps.

At the same time, AI is driving major investment in clean energy and infrastructure. The long-term outcome will depend on how quickly clean energy systems can scale.

If renewable supply, storage, and grid capacity keep pace with AI growth, the technology sector could help accelerate the shift to a low-carbon economy. If progress is too slow, however, AI could become a major new source of emissions.

Either way, AI is now a central force shaping global energy demand, infrastructure investment, and the future of carbon markets.

The post AI Data Centers Power Crisis: Massive Energy Demand Threatens Emissions Targets and Latest Delays Signal Market Shift appeared first on Carbon Credits.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits