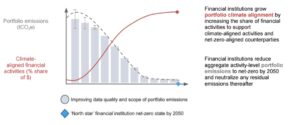

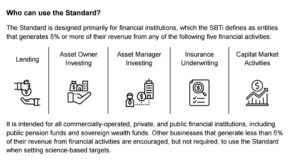

The Science Based Targets initiative (SBTi) has rolled out its first Financial Institutions Net-Zero Standard (FINZ). This framework offers banks, asset managers, insurers, and investors a clear path to aligning their portfolio activities—including lending, underwriting, and investments—with net‑zero emissions by 2050.

The FINZ standard sets clear rules on:

-

Portfolio emissions

-

Fossil fuel finance

-

Deforestation risk, and

-

Reporting

It aims to transform how the finance industry aligns with global climate goals and steers clean capital flows.

Why the New Standard Matters to Climate and Finance

Financial institutions are hugely influential. Their financed emissions—the greenhouse gases tied to the companies they finance—are typically hundreds to thousands of times higher than their own operational emissions.

They account for over 99% of financed emissions through loans, underwriting, and investments. One study found financed emissions can be 750 times greater, and for North American banks that rose to 11,000 times more than their own direct output.

Yet until now, most net‑zero frameworks focused on operational emissions (Scope 1 and 2). The FINZ Standard tackles Scope 3 category 15 emissions—those tied to clients and invested companies. It offers a sector‑specific roadmap for carbon impact across financial services.

Moreover, it strengthens transparency and accountability in financed emissions, including underwriting and capital markets. The UN-backed SBTi aims to drive major reductions. This tool targets not only corporate operations but also global capital markets.

Alberto Carrillo Pineda, SBTi’s Chief Technical Officer, noted:

“Financial Institutions have the ability to play a transformative role in the transition to net-zero. Their influence on the global economy and ability to engage with their portfolios is unparalleled to accelerate the net-zero transition. With its broad applicability and flexibility, this robust, science-based Standard will help financial institutions drive the net-zero transformation all over the world.”

Key Requirements: What FINZ Demands

Here are the major requirements set by the new standard:

Fossil Fuel Finance Phase‑out

Signatories must immediately stop financing new coal and oil field expansion. Financing for new oil and gas projects must also end by 2030. This shift separates general-purpose finance from investment that supports fossil fuel growth.

Portfolio Emissions Targets

Institutions need to measure and set science-based targets. These targets must cover all lending, investment, underwriting, and capital market operations (Scope 3 category 15+). They must align with a 1.5 °C pathway and match the ambition of SBTi’s corporate standard. Public targets and interim milestones are required.

Deforestation and Real Estate Risk Reporting

Banks and asset managers must assess exposure to deforestation and real estate. Those with significant risk must publish mitigation plans. This broadens climate accountability beyond just fossil fuel financing.

Stakeholder Response: Support and Criticism

Over 150 institutions contributed to public consultations, and 33 firms pilot‑tested the standard.

Over 150 financial institutions contributed to public consultations, and 33 firms pilot-tested the draft standard. Also, nearly 135 institutions across six continents have committed to align with FINZ already.

SBTi has validated the most near-term institution targets to date—a nearly 50% increase year-on-year. It also expects more growth under new CEO David Kennedy, with ambitions to scale to 20,000 companies by 2030.

Many praised the approach as both rigorous and practical. The Sustainable Finance Observatory welcomed the initiative’s wider focus. It includes loans, insurance, capital markets, and portfolio investment.

Yet critics highlight a major tension: the delay in phasing out fossil fuel finance until 2030. A recent report found that nearly 95% of bank fossil-fuel financing in 2024 went via general-purpose loans, not project-specific funding—potentially locking in more fossil fuel use this decade.

Some experts argue that progress toward net‑zero demands an immediate cutoff. SBTi believes that slower advocacy could allow more institutions to join in. This might lead to a bigger overall impact.

Major banks like HSBC and Standard Chartered left the SBTi climate approach. They had worries about the new standard’s strictness and how practical it is.

Meanwhile, ING is the first global bank to have validated SBTi targets. It has also promised to stop financing new fossil fuel projects by 2040. It will also cut coal power finance close to zero by 2025.

What It Means for the Carbon Credit Market

The FINZ Standard raises the bar for carbon credit demand. It is also likely to shape the future of the voluntary carbon credit market. Financial institutions are facing stricter rules on financed emissions. So, many will seek verified carbon removal solutions to hit their climate targets.

The SBTi usually doesn’t let carbon offsets replace real emissions cuts but it does see a small role for carbon removals. This is especially true for options like direct air capture or biochar that store carbon long-term.

This creates new demand for high-quality, science-based carbon credits, especially those tied to durable removal projects. Nature-based credits, like forest restoration, may increase in value. This is true if they meet strict verification and permanence standards.

Moreover, financial firms can help fund new carbon projects by investing in climate mitigation. This is especially important in emerging markets, where capital is often hard to find.

Overall, the new standard brings greater credibility to net-zero claims. This could lead to more serious investment in carbon markets. It may focus on removal and insetting instead of just short-term offsets. The standard might also lead buyers to choose credits certified by third-party groups. These should align with international standards like ICVCM and VCMI.

Looking Ahead: Adoption and Market Shifts

The FINZ Standard has been published in July 2025, with a global consultation now closed. It is expected to become mandatory for SBTi‑aligned institutions over the coming years. Here are major development to watch:

- The Financial Institutions Near-Term Criteria (FINT) will stay valid until 2026. New institutions should adopt the FINZ standard now.

- By early 2026, SBTi plans to fully roll out the standard under new CEO David Kennedy. As climate risk grows, it will impact financial stability.

- FINZ might set regulatory standards and change how banks are monitored for climate-related issues.

- Over time, institutions that meet FTIN 1.5 °C‑aligned targets and halt fossil fuel expansion financing will likely enjoy reputational gains and stronger ESG investor support. Conversely, those lagging could face legal, regulatory, and financial scrutiny.

SBTi’s Financial Institutions Net‑Zero Standard is a landmark tool for holding banks and investors accountable for financed emissions. Clear standards on fossil fuel finance, portfolio coverage, and disclosure help align financial flows with net‑zero pathways.

Some critics worry about the slow phase-out of fossil fuel financing. However, many view the new Financial Institutions Net-Zero Standard as a practical method that helps engage institutions and improve climate alignment sooner.

As more firms join, purchase high-quality carbon removals, and report robust financed-emissions targets, the standard could accelerate real emissions cuts. FINZ standard signals a change for those tracking ESG investments, carbon credits, and climate policy. It brings credible, science-based finance and acts as a new tool in the low-carbon market.

The post SBTi Launches Net-Zero Standard to Drive Climate Action in Banking and Finance appeared first on Carbon Credits.

Carbon Footprint

Carbon Market 2026: Supply Squeeze Pushes Premium Carbon Credit Prices Up, Sylvera Finds

The global carbon market is changing fast in 2026. The latest insights from Sylvera’s State of Carbon Credits report show a clear shift. Volumes are falling, but value is holding steady. This means buyers now focus more on quality than quantity.

Furthermore, the market is splitting into two clear segments. High-quality credits are in demand and sell at higher prices. Older or lower-quality credits are losing interest. This divide is growing stronger and shaping how the market will evolve in the coming years.

Shell’s Sharp Cut Pulls Down Market Volumes

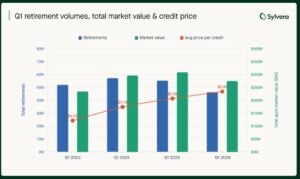

Carbon credit retirements reached 51 million in the first quarter of 2026. This is down from 55.3 million in the same period last year. The total market value also fell slightly to $290 million, compared to $309 million a year ago.

Despite this decline, prices did not weaken. The average price per credit increased to $5.69 from $5.60. This shows that buyers are willing to pay more for credits they trust.

Interestingly, a major reason for the drop in volumes was reduced activity from Shell. The company sharply cut its purchases. It retired just 494,000 credits in Q1 2026, compared to 6.7 million in Q1 2025 and 5.6 million in 2024. This single change had a large impact on the overall market.

Value Now Drives the Market

The carbon market now runs on a simple idea. Value matters more than volume. Buyers want credits that deliver real environmental impact. They prefer projects with clear data, strong verification, and proven results.

High-quality credits now define the market. These credits meet strict standards and often align with compliance systems. Because of this, they command higher prices and stronger demand.

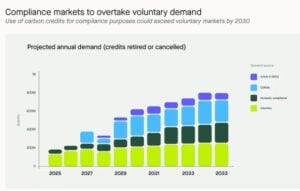

This shift is also linked to the rise of compliance markets. Programs like CORSIA are increasing demand for reliable credits. As a result, voluntary buyers and compliance buyers now compete for the same supply.

Experts expect this trend to grow stronger. Compliance demand could surpass voluntary demand by 2027. This will increase pressure on supply and push premium credit prices higher.

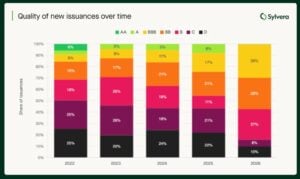

The report highlighted that, investment-grade credits (BBB+) now command an average of $20.10 per credit in Q1 2026, up from $18.10 in Q1 2025, as shown in the image below:

Recap of 2025 Carbon Market

Compliance programs made up 24% of total retirements in 2025. According to Sylvera, this share is rising fast. It is expected to go beyond voluntary demand by 2027. This growth is mainly driven by CORSIA Phase 1 rules and the expansion of domestic carbon markets.

This means compliance demand is set to change the carbon market in a big way. Soon, both voluntary buyers and regulated systems will compete for the same high-quality credits. This is already making supply tighter and more competitive.

At the same time, international trading under Article 6 gained momentum. In 2025, around 20 new bilateral agreements were signed, and the first large-scale carbon credit trades took place. This shows that global carbon transfer systems are now becoming active in practice.

However, the system is also becoming more complex. One key factor is “corresponding adjustments,” which now decide whether a credit is fully acceptable in compliance markets. In addition, countries like China, Japan, Brazil, and Indonesia are building their own domestic carbon systems.

These systems are expected to create strong new demand, but they also add more rules and complexity to the market.

Supply Crunch Becomes the Key Challenge

However, Sylvera has flagged a different scenario for his year. Supply is now the biggest issue in the market. High-quality credits are becoming harder to find. Many credits exist, but not all meet strict requirements.

Furthermore, the main bottleneck is coming from approvals under Article 6. These rules govern international carbon trading. Delays in approvals mean many credits cannot yet enter the market. Now this creates a gap. Supply looks strong on paper, but usable supply remains limited. This shortage keeps prices firm and supports premium credits.

CORSIA Supply Expands, But Not Enough

There has been progress in aviation supply. Eligible credits under CORSIA reached 32.68 million. This is more than double last year’s level.

These credits come from major registries like Verra, Gold Standard, and ART TREES. However, supply still falls short in practice. Not all credits meet full compliance standards. This keeps the market tight and competitive.

Moving on, the question is what’s driving market growth.

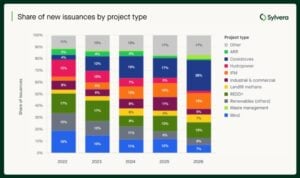

Cookstoves Drive Market Growth

Cookstove projects are growing quickly. Their share increased from 17% in 2025 to 26% in Q1 2026. Africa leads this segment. Around 80% of the supply comes from the region. Most of these projects also meet compliance requirements under CORSIA.

Quality is improving in this category. Developers are moving away from older methods. They now use stronger, data-driven approaches. This shift improves trust and attracts more buyers.

Other projects:

- REDD+ Regains Trust: Forestry projects under REDD+ are making a comeback. Their share of retirements rose to 25% in Q1 2026. These projects faced heavy criticism in the past. However, new rules and better standards are restoring confidence. Updated methodologies have removed weaker credits. This has improved the overall quality of supply. Global policy clarity has also helped. Buyers now have more confidence in using REDD+ credits in compliance markets. This has supported demand.

- Waste management projects: They are growing in importance, and their share reached 10% of total retirements, the highest so far. Landfill methane projects are leading this growth. These projects are easier to measure and verify. They also meet compliance standards. Buyers are now exploring options beyond traditional sectors. Waste projects offer a reliable and practical solution.

New Credit Types Expand the Market

Several new project types are growing fast. They are adding fresh supply and attracting new buyers.

- Clean water projects have seen strong growth in recent years. They now produce millions of credits annually. Marine and mangrove projects are also gaining attention. They offer strong environmental benefits and long-term carbon storage.

- Industrial projects focused on nitrous oxide reduction are expanding as well. These projects are highly measurable and align well with compliance systems. At the same time, regenerative agriculture is growing at the fastest pace. It has moved from almost no activity to millions of credits in a short time.

These new categories are helping the market grow. However, quality remains the key factor that drives demand.

Buyers Shift Toward Better Credits: Regional Analysis

Buyer behavior is changing across regions. The United Kingdom is leading the move toward high-quality credits. Companies are under pressure to show real climate action. This has pushed them to choose better credits.

The United States and Canada are also improving. Buyers prefer projects that meet both voluntary and compliance standards. This supports demand for high-quality supply.

North America Sets the Benchmark

North America sets the benchmark for quality. A large share of its credits meets high rating standards. This strong quality supports higher prices. The average price reached $14.80, the highest globally. Strong domestic demand and strict standards drive this trend.

On the other hand, South America is seeing strong demand but limited new supply. This creates pressure in the market. Prices have slightly declined to $11.50. However, the quality mix is improving. Waste projects are helping fill the gap left by falling forestry supply.

- Europe remains the largest market by volume. However, the quality mix is still uneven. Some buyers continue to use lower-rated credits.

- Japan and South Korea focus on lower-cost options like hydropower. This keeps their share of high-quality credits low. In Latin America, buyers often choose local projects. Limited regulatory pressure keeps the quality demand weaker.

- Africa is moving toward better quality. High-rated supply is increasing, while low-rated supply is falling. As explained before, cookstove projects are the main driver. At the same time, lower-quality forestry projects are declining. This improves the region’s overall market position.

- Asia faces weaker market conditions. Supply has dropped sharply due to fewer renewable energy projects. The average price stands at $5.30, the lowest globally. Demand remains steady but lacks strong growth. This keeps prices under pressure.

Indonesia Stands Out in Asia

Indonesia is a bright spot in the region. Credit prices have risen strongly in the past year. High-quality peatland projects are driving this growth. International deals under Article 6 are also adding value. These factors attract buyers looking for reliable credit.

This shows how strong quality and supportive policies can boost market performance.

Final Take: Quality Defines the Future

The carbon market in 2026 is clear and focused. Quality now drives demand, pricing, and growth. Buyers are becoming more selective. They want credits that are verified, reliable, and compliant.

Supply remains tight, especially for high-quality credits. At the same time, compliance markets are growing. This increases competition and pushes prices higher.

The gap between high- and low-quality credits will continue to widen. In simple terms, the market is no longer about how many credits exist. It is about how good they are.

- READ MORE: Top Carbon Credit Companies to Watch in 2026

The post Carbon Market 2026: Supply Squeeze Pushes Premium Carbon Credit Prices Up, Sylvera Finds appeared first on Carbon Credits.

Carbon Footprint

US and Australia Boost Critical Minerals Support with $3.5B Alliance, Challenging China’s Grip

Australia and the United States have launched a $3.5 billion critical minerals partnership, marking one of the largest bilateral efforts to secure materials essential for clean energy and electric vehicles (EVs).

The agreement focuses on strengthening supply chains for minerals such as lithium, cobalt, nickel, and rare earth elements. These materials are vital for batteries, solar panels, wind turbines, and other low-carbon technologies.

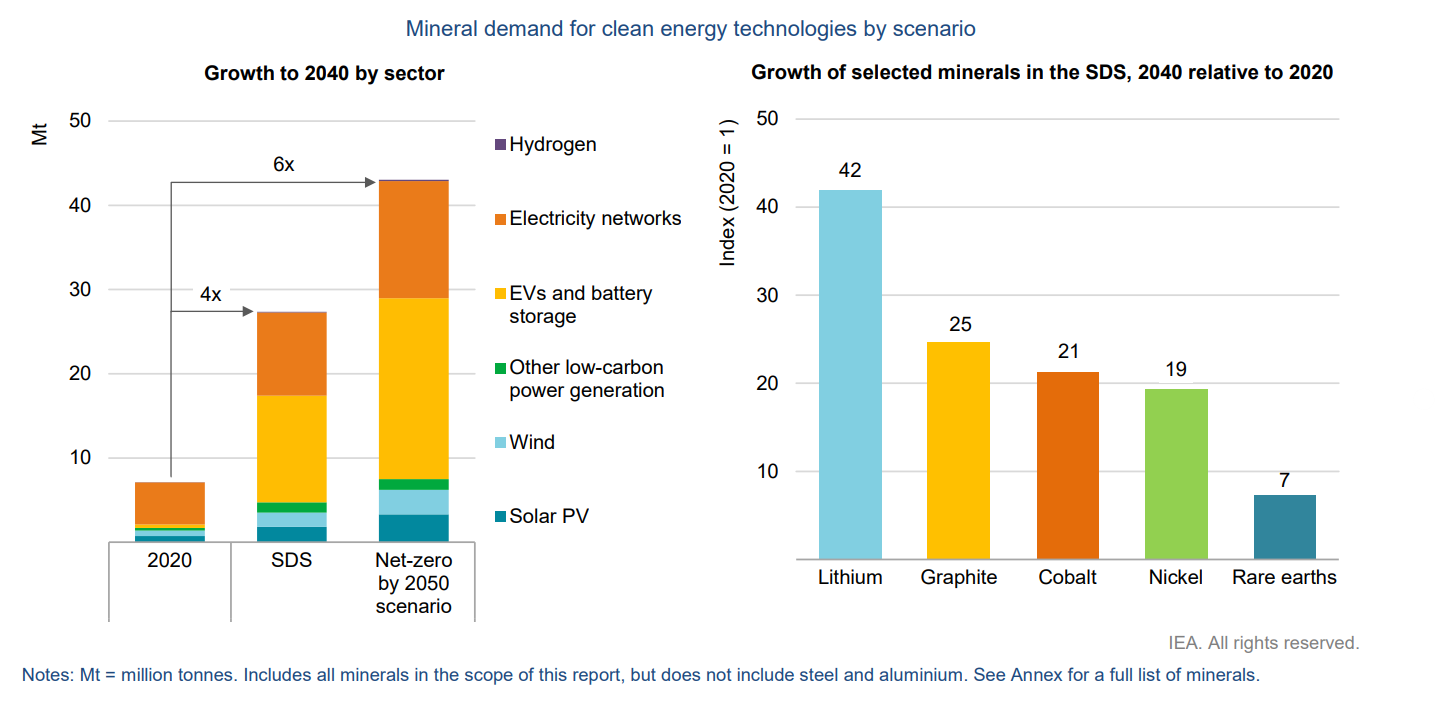

The deal comes as global demand for these minerals rises sharply. The International Energy Agency estimates that demand for critical minerals could quadruple by 2040 under net-zero scenarios. Lithium demand alone could grow more than 40 times by 2040, driven by EV adoption and battery storage.

Australia plays a central role in this supply chain. It currently produces about 55% of the world’s lithium, making it the largest global supplier. However, much of the processing still takes place overseas, creating supply risks for Western economies.

The new partnership aims to address this gap by boosting both extraction and domestic processing capacity.

Billions Back the Full Value Chain—from Mine to Market

The $3.5 billion investment will be deployed over seven years. The United States will give around $2.1 billion. This funding comes from the Defense Production Act and the Infrastructure Investment and Jobs Act. Australia will provide $1.4 billion through national financing programs.

The funding is designed to support the full value chain, from mining to refining to advanced research. The main areas of investment include:

- $1.8 billion for new mining projects and infrastructure upgrades

- $1.2 billion for processing and refining facilities

- $500 million for research, innovation, and sustainable extraction technologies

A key goal is to reduce reliance on external processing markets and build more resilient supply chains. This includes expanding refining capacity for lithium and rare earth elements, which are often processed outside producing countries.

The partnership is also expected to create economic benefits. Government estimates say about 15,000 direct jobs will be created. Additionally, around 30,000 indirect jobs will come from supply chains and related industries.

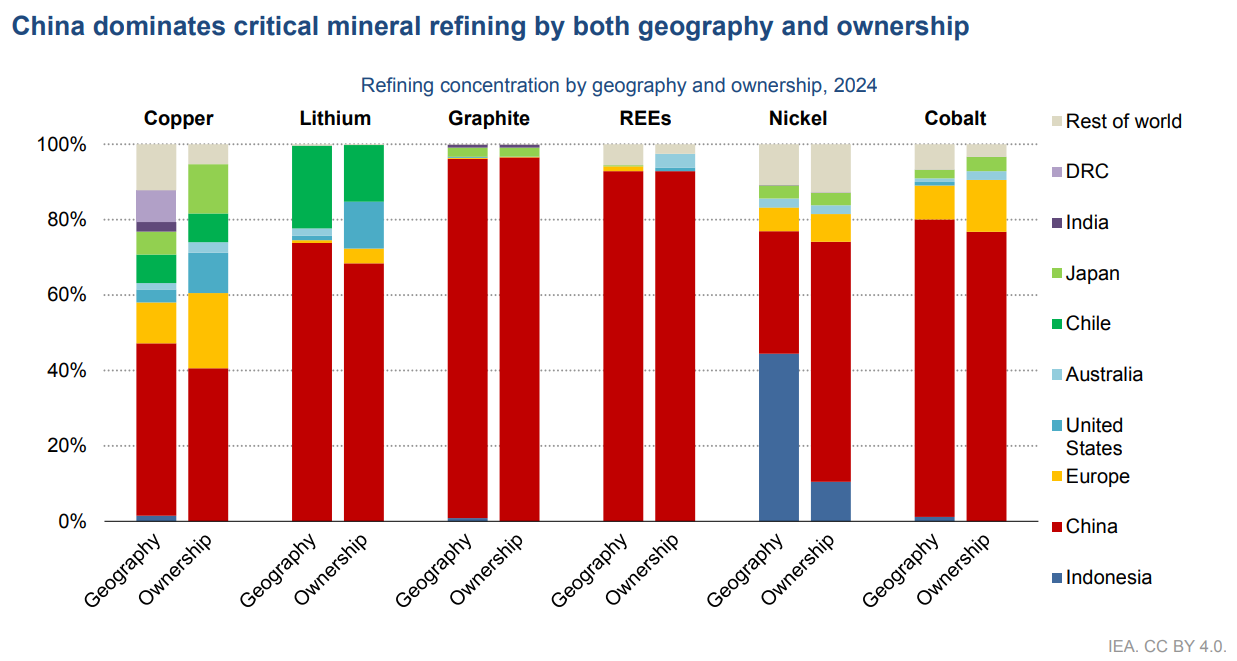

Breaking China’s Grip on Mineral Processing

The agreement reflects growing concern over the concentration of mineral processing in China. Currently, China dominates key parts of the global supply chain.

According to the International Energy Agency:

- China handles about 60% of global lithium processing

- It controls more than 80% of rare earth refining

- It also leads in battery component manufacturing

This dominance creates risks for supply security, pricing, and geopolitical stability. Disruptions in one region can affect global clean energy deployment.

By investing in alternative supply chains, Australia and the United States aim to diversify production and reduce these risks. The partnership could also encourage other countries to develop their own critical minerals strategies.

In addition, the deal may help stabilize prices for key materials. Volatility in lithium and nickel markets has impacted EV production costs. It has also delayed some renewable energy projects in recent years.

Supporting Climate Goals and the Energy Transition

The partnership has direct implications for global climate efforts. Critical minerals are essential for scaling clean energy technologies. Without a reliable supply, the pace of decarbonization could slow.

Battery storage is a key example. Energy storage systems help manage the variability of renewable energy sources like solar and wind. Expanding mineral supply will support the growth of these systems.

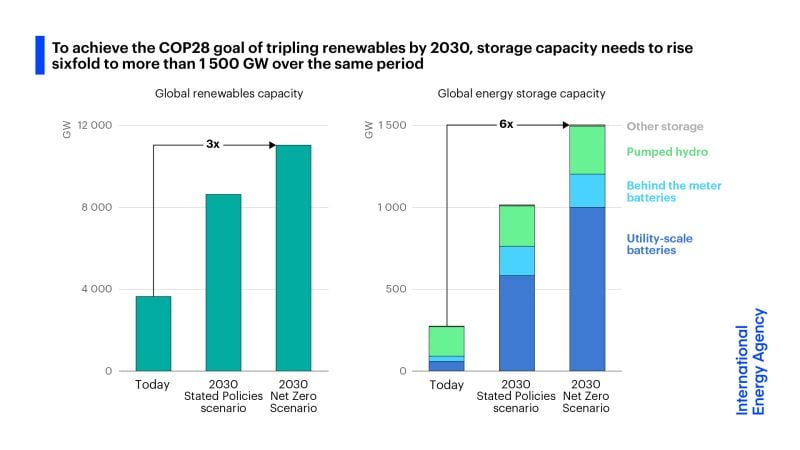

The IEA projects that global battery capacity must increase significantly to meet climate targets. Some estimates suggest energy storage capacity needs to grow more than sixfold by 2030 to stay on track for net-zero emissions.

The US-Australia alliance could help unlock this growth by ensuring stable access to raw materials. This, in turn, may reduce costs for batteries and renewable energy systems over time.

Both countries have also committed to improving environmental standards in mining. This includes reducing emissions, improving water management, and limiting land impacts. These measures are important because mining itself can be carbon-intensive.

Efforts to lower emissions in mineral extraction could also influence carbon accounting frameworks. As supply chains become more transparent, companies may need to track and report emissions linked to raw material sourcing.

ESG, Carbon Markets, and the New Mining Reality

The expansion of critical minerals supply chains is expected to influence carbon markets and ESG strategies.

As mining activity increases, so does the need to manage emissions. This could increase the need for carbon credits in the extractive sector. This is true for projects that cut or offset emissions from mining.

At the same time, improved supply chains for clean technologies may accelerate renewable energy deployment. This could support carbon reduction efforts across multiple sectors, including power generation and transportation.

The partnership may also lead to higher standards for responsible sourcing. Materials produced under strict environmental and social guidelines could command a premium in global markets.

This shift aligns with growing investor focus on ESG performance. Companies face growing pressure to show that their supply chains meet sustainability standards. This includes tracking emissions across Scope 1, 2, and 3 categories.

Over time, these trends could reshape how carbon credits are used. Companies may focus more on cutting emissions directly in their supply chains, rather than just using offsets.

Industry Scrambles to Secure the Next Wave of Supply

The announcement has received strong support from industry players. Major automakers and battery manufacturers are seeking secure and stable supplies of critical minerals. Companies like Tesla, Ford, and General Motors want to source materials from projects tied to the partnership.

Mining firms are also responding. Albemarle Corporation and Pilbara Minerals will likely gain from more investment and quicker project timelines.

Investor interest in the sector is rising as well. Global spending on energy transition minerals is growing rapidly, supported by both public and private capital.

The International Energy Agency reports that investment in critical minerals has increased sharply in recent years. This trend is expected to continue as countries compete to secure supply chains for clean energy technologies.

A Defining Shift in the Global Energy Economy

The $3.5 billion Australia–US critical minerals partnership represents a major step in reshaping global energy supply chains. It addresses a key bottleneck in the transition to a low-carbon economy: access to essential raw materials.

In the short term, the deal may help stabilize supply and reduce risks linked to market concentration. In the long term, it could accelerate the deployment of clean energy technologies and support global climate goals.

For carbon markets, the impact is indirect but important. More minerals can help speed up the use of renewables and energy storage. This, in turn, cuts emissions throughout the economy. At the same time, higher mining activity may drive demand for carbon credits and new emissions reduction strategies within the sector.

The success of the partnership will depend on execution. Expanding mining and processing capacity takes time, investment, and strong environmental oversight.

If these challenges are addressed, the alliance could serve as a model for future international cooperation on critical minerals. It also highlights how energy security, economic policy, and climate action are becoming increasingly connected.

Ultimately, as demand for clean energy continues to grow, securing sustainable and reliable mineral supply chains will remain a key priority for governments and industries worldwide.

The post US and Australia Boost Critical Minerals Support with $3.5B Alliance, Challenging China’s Grip appeared first on Carbon Credits.

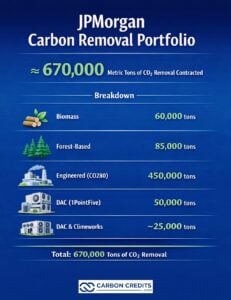

JPMorgan Chase has signed two major carbon removal agreements this month. The first one involves a purchase of 60,000 metric tons of durable carbon dioxide removal (CDR) over ten years from climate startup Graphyte. The deal uses biomass-based technology that converts agricultural and timber waste into stable carbon blocks stored underground.

In parallel, JPMorgan has also secured 85,000 tons of forest-based carbon removal credits through improved forest management projects. These credits, marketed by Anew Climate, come from U.S. forest projects managed by Aurora Sustainable Lands.

They aim to extend harvest cycles, boost forest health, and enhance long-term carbon storage. The approach helps maintain higher carbon stocks in working forests while supporting biodiversity and sustainable timber production.

Taylor Wright, Head of Operational Sustainability at JPMorgan Chase, noted:

“We were excited to add credits from the Little Bear Forestry Project to our carbon removal portfolio. The dynamic baselining provides meaningful evidence that these credits meet a high threshold for quality, supporting our interests as both a buyer and as a steward of market integrity.”

Carbon Removal Still Small, But Growing Fast

The agreements are part of a broader push by the bank to expand its carbon removal portfolio. While the total volume is small compared to global emissions, the deals highlight a shift in corporate climate strategies.

Companies are now focusing more on durable carbon removal, not just emission reductions. JPMorgan’s mix of engineered and nature-based solutions also reflects a growing trend toward portfolio diversification in carbon removal sourcing.

Carbon removal remains a small but critical part of climate action. The United States emits about 5 billion tons of CO₂ per year, showing how limited current removal volumes still are.

However, long-term demand is expected to grow sharply. The Intergovernmental Panel on Climate Change estimates that by 2100, the world might need to remove 100 to 1,000 gigatons of CO₂. By mid-century, annual removal should reach about 10 gigatons per year.

Today’s market is far from that scale. Most carbon removal deals are measured in thousands or hundreds of thousands of tons. But these early contracts are seen as critical. They help build supply, reduce costs, and attract investment into new technologies.

JPMorgan’s latest deals fit this pattern. Together, the 60,000-ton biomass contract and 85,000-ton forest-based agreement provide long-term demand signals across different removal pathways. This helps scale both emerging engineered solutions and more established nature-based approaches.

Turning Waste Into Permanent Carbon Storage

Graphyte’s process, known as “carbon casting,” uses natural carbon capture through plants. Biomass absorbs CO₂ through photosynthesis. The material is then dried, compressed, and sealed to prevent decomposition. This allows the carbon to remain stored for long periods.

The company uses waste materials such as crop residues and timber byproducts. This reduces the need for new land use and lowers overall costs. The process also uses relatively low energy compared to other removal methods.

Projects linked to the JPMorgan deal include facilities in Arkansas and Arizona. These projects also provide added benefits. For example, using forest thinning residues can help reduce wildfire risk and support land restoration.

This reflects a broader trend in carbon markets. Buyers are increasingly looking for projects that deliver both carbon removal and environmental co-benefits. The bank’s forest-based deal reinforces this trend by supporting improved forest management practices that enhance carbon storage while maintaining productive landscapes.

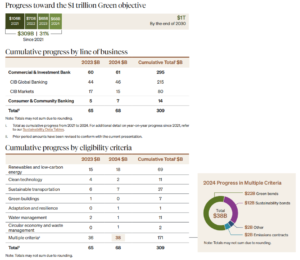

JPMorgan’s $1 Trillion Net Zero Strategy and Climate Finance Push

JPMorgan’s carbon removal investments are part of a wider climate strategy. The bank has committed to facilitating $1 trillion in climate and sustainable development financing by 2030. It has already deployed about $309 billion between 2021 and 2024 toward this goal.

In addition to financing, the bank is building a diversified carbon removal portfolio. Since 2023, it has signed deals to cut hundreds of thousands of tons of CO₂. This includes a plan for up to 800,000 tons of carbon removal through long-term contracts.

The company aims to match its unabated operational emissions with durable carbon removal by 2030.

JPMorgan is also investing in a range of technologies. These include direct air capture, bio-oil sequestration, biomass storage, and forest-based removal. Its latest forest deal shows a continued commitment to high-quality, nature-based removals that meet stricter standards for durability and verification.

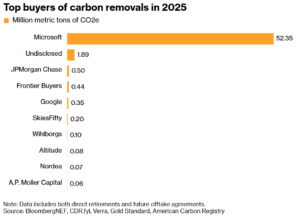

This diversified approach helps reduce risk while supporting different pathways to scale. Compared to many financial institutions, JPMorgan remains an early mover. Most large buyers in carbon removal are still technology companies, particularly Microsoft.

Microsoft Pullback Shakes Market Confidence

However, Microsoft, the largest buyer of carbon removal credits, has reportedly paused new purchases.

The tech giant has played a dominant role in the market. It accounts for up to 90% of global carbon removal purchases and has contracted more than 45 million tons of CO₂ removal to date. In 2025 alone, the company signed agreements for 45 million tons, doubling its 2024 volume and far exceeding any other buyer.

However, reports suggest the company may be adjusting the pace of new deals. This shift does not mean the end of carbon removal demand, but it signals a transition.

The market can no longer rely on a single dominant buyer. In this context, JPMorgan’s continued activity—across both engineered and nature-based deals—shows how new buyers are stepping in to support market stability.

Market Trends: From Cheap Offsets to High-Durability Carbon Credits

The carbon market is evolving quickly. Traditional carbon credits often focus on avoiding emissions, such as protecting forests. However, there is growing demand for removal-based credits that physically take CO₂ out of the atmosphere.

Corporate net-zero goals drive this shift. Many companies now face limits on how much they can reduce emissions directly. Carbon removal is becoming necessary to address remaining emissions.

At the same time, supply remains limited. High-quality removal credits are scarce. This keeps carbon prices high, especially for engineered solutions.

Early buyers like JPMorgan are helping shape the market. Long-term contracts provide price signals and encourage project development. They also help define standards for quality and verification.

Another key trend is the focus on durability. Buyers prefer solutions that store carbon for decades or centuries, rather than short-term offsets.

Early-Stage Market, High-Stakes Growth

Despite growing momentum, carbon removal is still in its early stages. Current volumes are small compared to global needs. Policy support is also limited in many regions.

However, corporate demand is rising. Deals like JPMorgan’s show how private sector investment is driving the market forward.

The combination of long-term contracts, new technologies, and climate finance is expected to accelerate growth. Over time, this could help bring down costs and expand supply.

For now, the focus remains on building scale. Each new agreement adds to a growing pipeline of projects. These projects will play a key role in meeting long-term climate targets.

JPMorgan’s latest purchases may be modest in size. But together, they reflect a larger shift. Carbon removal is moving from early experimentation to a more structured and investable market, supported by a broader mix of buyers and solutions.

The post JPMorgan’s Carbon Bet Marks a Turning Point for the Removal Market appeared first on Carbon Credits.

Iowa Moves to Shield Farmers, Ethanol Plants, From Lawsuits Over Emissions

IEA slashes pre-war oil demand forecast by nearly a billion barrels per day

Humans Just Flew Around the Moon This Week. But Would Babies Born There Ever Truly Feel Gravity? Ask Jellyfish Babies.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits