Nations are “back on track” to adopt a framework for curbing global shipping emissions, following the latest International Maritime Organization’s (IMO) meeting in London, UK.

The proposed “net-zero framework” had been expected to be approved by countries at the IMO towards the end of 2025.

Instead, the Trump administration was accused of “bully-boy” tactics as the US led a concerted effort to reject the framework, leading to its approval being delayed.

Since then, the US, other fossil-fuel producers and some industry groups have called for the framework to be stripped of its carbon-pricing mechanism, or abandoned entirely.

At the Marine Environment Protection Committee (MEPC84) meeting in London, UK, last week, nations tried once again to reach an agreement on the framework.

Opponents said they were trying to seek consensus, but supporters, such as Brazil, the EU and Pacific islands, pointed out the framework was already a “careful balance of interests”.

Liberia and Panama – “flag states” for a third of the world’s commercial shipping – led a counter-proposal, alongside Argentina, which effectively cut carbon pricing from the framework.

Ultimately, however, the meeting ended with a reconfirmation that delegations are committed to rebuilding consensus on global shipping emissions.

The framework survived the negotiations and the committee will now try to adopt it at its December 2026 meeting.

Below, Carbon Brief explains why the framework has proved so contentious, who the major players have been and what the final outcome was at the latest IMO meeting.

- Why was the net-zero framework delayed last year?

- Why do some countries oppose the net-zero framework?

- What ‘alternative frameworks’ were discussed?

- What do supporters of the net-zero framework want?

- What was the final outcome from the IMO meeting?

Why was the net-zero framework delayed last year?

In April 2025, nations at the IMO had agreed on a “net-zero framework” at their MEPC83 meeting in London, despite the US withdrawing halfway through.

Later that year, in October 2025, they failed to formally adopt the framework after a fraught meeting that saw US negotiators accused of “bully-boy tactics”.

The framework was meant to be a practical set of measures to achieve the global net-zero target for shipping, agreed at the IMO in 2023. The target is significant, as international shipping is responsible for more than 2% of emissions and is not covered by the Paris Agreement.

Following a week of negotiations at the April 2025 meeting, the remaining nations had voted on approving a compromise proposal for an emissions levy – effectively a carbon tax on global shipping – and a credit-trading system.

A majority of nations had agreed to this framework that would have set a lower emissions-intensity reduction target of 4% in 2028, rising to 30% in 2035. It had also included an upper target that would have increased from 17% in 2028 to 43% in 2035.

Ships that failed to lower their emissions intensity in line with these limits would have needed to purchase “remedial units” for $380 per “tier two” unit. This would have fed into a new IMO “net-zero fund”.

Those who met the lower target, but fell short of the more difficult upper target, would have had to pay into the IMO fund, but at the lower rate of $100 per “tier one” unit.

The number of compliant ships had been expected to grow under this framework, reducing the number of vessels reliant on buying units and helping to reduce emissions intensity by over 40%, as the chart below shows.

The purchase of units to comply with the rules had been expected to raise $10-15bn annually in the initial years of the fund, as well as help with the development of zero and near-zero (ZNZ) greenhouse gas fuels and energy sources, according to thinktank IDDRI.

In turn, the fund would have been used to support developing countries to decarbonise shipping.

A clear majority of 80% of the eligible voters – not including those who abstained or the US – approved the framework at the April 2025 meeting.

The 63 countries that voted in favour included the EU, China, India and Brazil, while those that voted against included major fossil-fuel producers, such as Saudi Arabia, Russia and the United Arab Emirates (UAE).

Following this “landmark” agreement, countries had then been expected to formally adopt the framework at the next MEPC session in October 2025.

However, the meeting proved challenging. The US “unequivocally rejected” the proposal and lobbied extensively against adoption, including by threatening governments, individual diplomats and shipping companies with sanctions, visa restrictions, tariffs and port fees.

During the October meeting, the US and its allies pushed for a shift from a “tacit” approval system for the net-zero framework to one that would require explicit acceptance by governments. This would mean it would only come into force if, six months later, two-thirds of nations actively accepted the deal, Climate Home News explained at the time.

Negotiations continued throughout the week before Saudi Arabia called to adjourn the meeting, a move that was passed after it was backed by 57 countries.

As such, the decision on the adoption of the net-zero framework was pushed back by a year.

Among the 63 countries that supported the IMO net-zero framework at MEPC83 in April 2025, 15 supported the adjournment and 10 abstained – showing that some nations that had previously supported the framework had softened on the deal, following lobbying by the US, Saudi Arabia and their allies.

Going into the April 2026 MEPC84 meeting, it was clear that agreement on the framework would not be straightforward. A report ahead of the meeting from University College London (UCL) noted:

“The level of support is noticeably weaker than in April [2025] and likely reflects the effectiveness and efforts made by sides supporting or opposing the net-zero framework over the intervening period.”

In the week ahead of the MEPC84, US IMO delegation lead Wayne Arguin told a meeting that there was a “clear, strong and sizable bloc of countries opposed to the [net-zero framework]” and “no prospect of achieving consensus”, according to Politico.

As the meeting kicked off on 27 April 2026, IMO secretary-general Arsenio Dominguez called on parties to engage in “engage in constructive and pragmatic exchanges”.

Why do some countries oppose the net-zero framework?

A coalition of countries, including the US, Saudi Arabia and various fossil-fuel producers, strongly oppose the IMO net-zero framework that was agreed last year.

They were supported by a wider group of industry bodies and major flag states – countries where many ships are registered – which were instrumental in advancing “alternative frameworks” at the latest meeting. (See: What ‘alternative frameworks’ were discussed?)

Documents submitted ahead of the April 2026 meeting laid out the basis for this opposition, with the US criticising the net-zero framework’s “significant shortcomings”, concluding:

“The most appropriate path forward is to end consideration of the IMO net-zero framework entirely.”

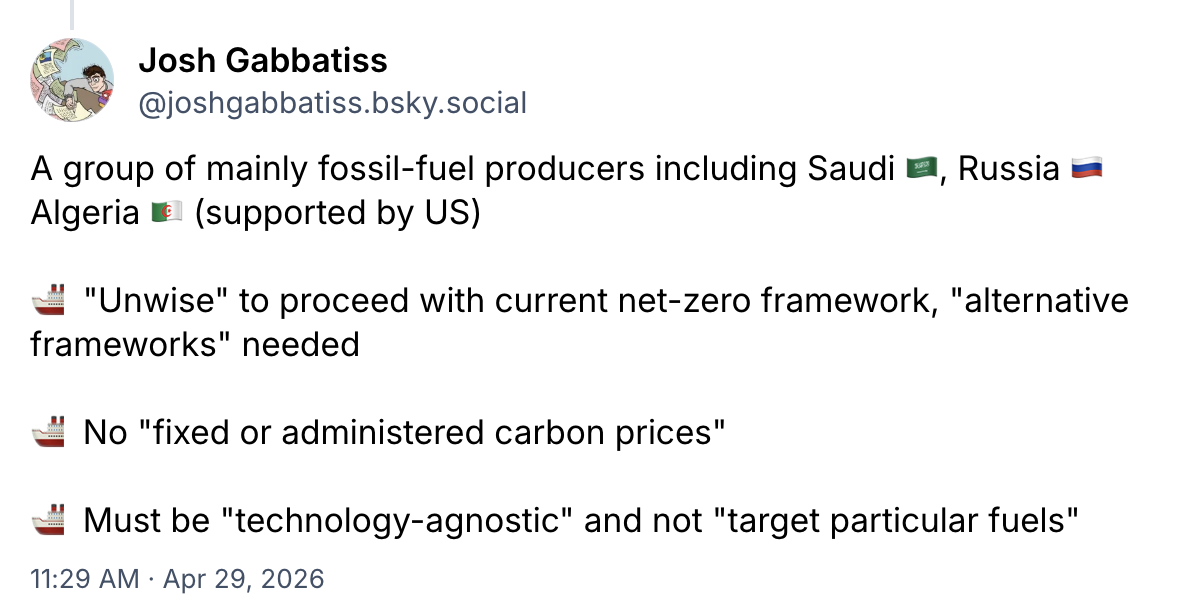

More nuance came in a statement from a group of primarily large fossil-fuel producers, including Saudi Arabia, Russia and Algeria, which was also backed by the US.

It stressed the need for “alternative” frameworks, with an emphasis on achieving consensus, as well as “practicability, equity and trust”. In practice, this meant a system without any carbon pricing, “top-down restrictions” or “international penalties”.

Opposing countries said any outcome should be “technology-neutral”, meaning it should not disadvantage specific fuels, potentially including liquified natural gas (LNG) and other fossil fuels.

These nations also stressed what they claimed were the potential impact of additional net-zero costs on “food and energy security”.

Much of their criticism was based on supposed economic harm that the net-zero framework would cause, particularly in developing countries.

These arguments purported to be about fairness for these countries. Yet some opponents of the framework were also calling for the IMO fund to be abandoned.

If this IMO fund were lost, then developing countries could lose out on a potential source of support for their own maritime decarbonisation, as well as potentially their broader energy transitions.

As well as supporting the fossil-fuel producers’ call for “alternative frameworks”, the UAE filed its own submission questioning the legitimacy of the IMO in establishing a new fund.

The US submission to the IMO stated that the fund would provide “pennies on the dollar compared to the economic hardship” brought about by the framework overall.

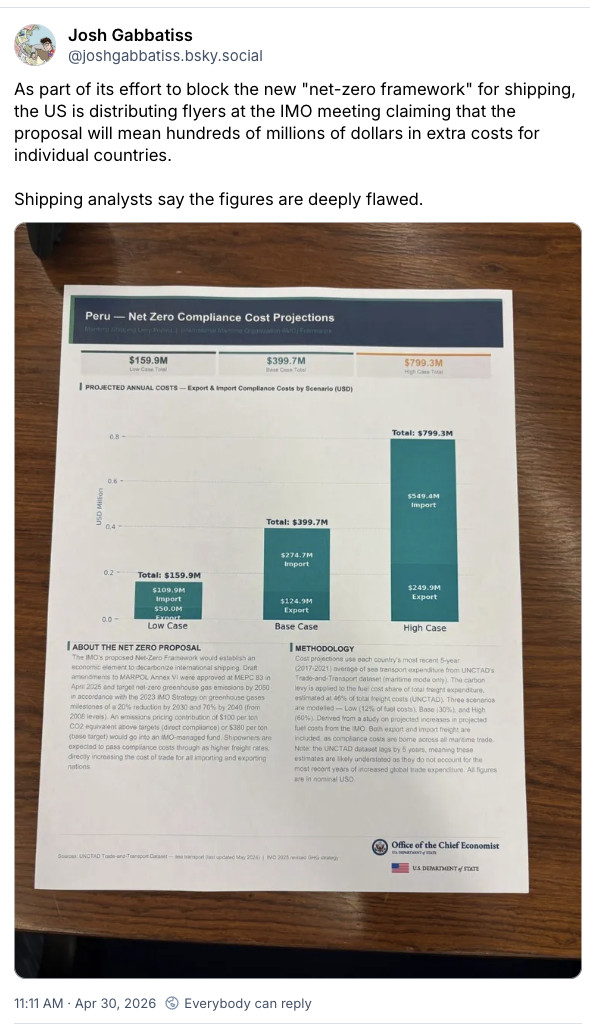

US delegates distributed flyers at the IMO meeting, emphasising the financial burden they claimed the framework would place on developing countries. While low-carbon shipping will come with substantial costs, analysts said the US figures were “not credible”.

Campaigners accused the US of “pretending to care about other countries’ economies”, pointing out that the energy crisis – triggered by the US-led war on Iran – is costing the shipping industry billions.

Moreover, they stated that the Trump administration’s new port entry fees would be a far greater financial burden for the global shipping industry than the mooted net-zero rules.

Analysis by UCL shipping researchers ahead of MEPC84 concluded that the Trump administration would potentially be less able to exert “soft power and influence” at the talks than last year. Additionally, it pointed to a Supreme Court ruling that limited the US’s capacity to impose punitive tariffs.

In practice, the US was less vocal at the talks, choosing to support alternative framework ideas proposed by other IMO members.

What ‘alternative frameworks’ were discussed?

There were two main alternatives to the net-zero framework considered at MEPC84.

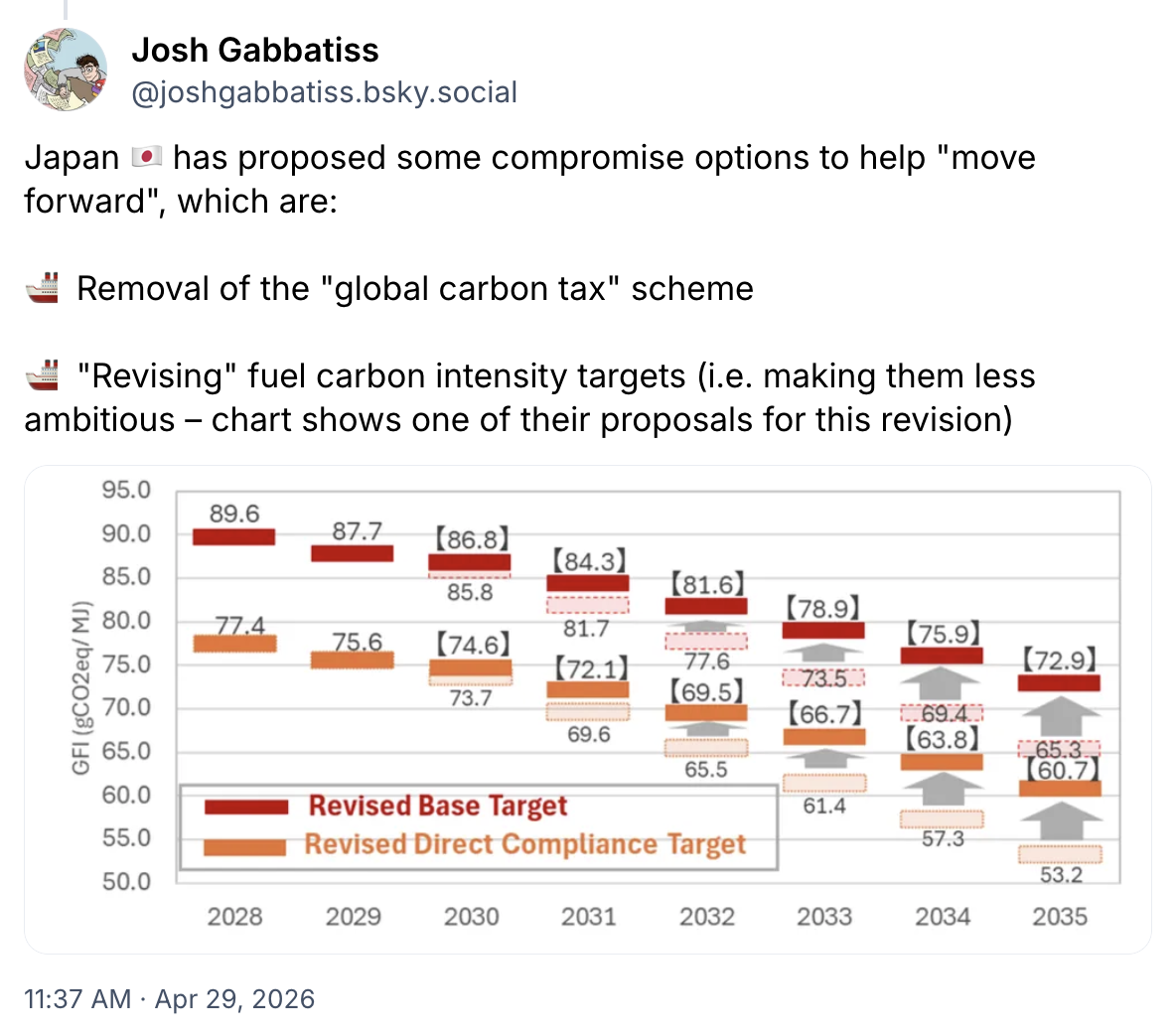

Japan suggested some ideas as a “possible basis for discussion”, which included removing the need for ships to pay into an IMO fund when they fail to meet emissions targets.

It also suggested simply relaxing the emissions targets, in order to make them easier for shipping companies to meet.

The second – and more significant – counter-proposal to the net-zero framework was not submitted by the US or its fossil-fuel producer allies.

Instead, it came from Liberia, Panama and Argentina, three countries that have strong political and historical ties with the US.

This was particularly notable given Liberia and Panama’s status as the top two “flags of convenience”, as shown in the chart below. A third of the world’s commercial shipping is registered in these small states, giving them disproportionate significance within the talks.

Their proposal, offered in the spirit of “consensus‑building”, said that only fuels already considered “commercially viable” should be included in the IMO’s carbon-intensity targets.

The Argentina-Liberia-Panama proposal was dismissed by observers as “business-as-usual”, as it removes incentives to develop clean fuels, any substantial means of enforcement and opportunities to raise funds to help developing countries.

Delaine McCullough, director of the shipping programme at the Ocean Conservancy, tells Carbon Brief:

“By removing the mandatory greenhouse gas price, you take away the ability to provide any kind of rewards or other incentives, and you also take away the regulatory incentive, so you just end up where we are today.”

This was the proposal that the net-zero framework’s most prominent opponents, including the US and the Gulf states, rallied around at MEPC84.

Among those also backing the idea during the talks were some developing countries, such as Ghana, Nigeria and Sierra Leone, that also said they wanted the IMO outcome to provide them with financial support.

This came in spite of the proposal stating there should be “no establishment of an IMO fund”. Speaking on condition of anonymity, a small-island state delegate tells Carbon Brief:

“Many countries that support the Liberia-Panama-Argentina submission also seek support for transition, capacity-building and mitigation of negative impacts. This support will not be available if [that] approach is taken.”

Some delegates questioned the decision by Liberia and Panama to lead this pushback against the net-zero framework. Both nations had previously supported an emissions levy on shipping, which would have been far more ambitious than the framework they now oppose.

Observers noted ties between nations that opposed the framework and parts of the shipping sector – including US-based interests and LNG assets.

Among the industry voices arguing strongly against the net-zero framework have been the American Bureau of Shipping and a group of international shipping companies and registries – including the national registries of Liberia and Panama.

The latter group voiced “significant concerns” and called for “alternative proposals”. Rather than a domestic entity, the Liberian registry that issued this statement is a privately owned US company.

Reflecting on these issues, Prof Tristan Smith, an energy and transport expert at UCL, wrote on LinkedIn:

“Privately owned registries have leverage over their host governments because one angry shipowner’s personal wealth is more than the flag state’s GDP and governments of low-income countries can’t easily take risks with even small volume revenues.”

Major Greek shipowners, including some with US-linked LNG interests, also opposed the net-zero framework, citing the “absence of support from major and influential states representing a significant share of global tonnage”.

Greece itself had reportedly pushed back against the framework behind the scenes, despite the EU’s public, unified position of support.

What do supporters of the net-zero framework want?

There were many vocal supporters of the net-zero framework at MEPC84, including a broad range of developed and developing countries.

Among them were the EU, Brazil, Mexico, Kenya, Pacific island states, Australia and the UK.

Having supported the net-zero framework last April, but voted to postpone its adoption in October, China expressed support for a carbon-pricing system and an IMO fund in a technical submission issued ahead of MEPC84.

The major shipping nation had remained quiet during the US-Saudi disruption in October last year, so its submission was viewed as a positive for backers of the framework.

Colombia, which was simultaneously hosting a global conference on “transitioning away” from fossil fuels, also emerged as a supporter of the net-zero framework.

There has also been support from some sections of the shipping industry, including a large coalition of ports, logistics companies and clean-fuel providers.

Supportive nations pointed out that the net-zero framework was the result of years of talks and already represented what Pacific island states called a “fragile compromise”. They framed it as the “only politically viable option” for hitting the IMO’s net-zero goal.

Pacific islands and around 50 other nations had originally called for a universal carbon levy on shipping. Ultimately, they were forced to accept the net-zero framework as a compromise, but Pacific islands said they would revert to their call for a levy if they felt the framework was being “watered down”.

The demand for a levy was strongly opposed by numerous countries, including some of the current framework’s supporters, such as Brazil and Australia.

In a bid to revive the net-zero framework, a submission by Brazil sought to “dispel any possible potential misunderstandings”, stressing that the approach is “flexible” and “should not be mistaken for a ‘global tax’”.

For example, Brazil notes that the framework “does not exclude any fuels” and that even existing “bunker” fuels and LNG could be used, as long as carbon intensity targets are met. (Ships could, for example, use carbon capture and storage to meet the goals.)

Michael Mbaru, a low-carbon shipping expert for the Kenya climate special envoy, told a briefing ahead of the conference that the net-zero framework was in developing countries’ interests:

“If the global package unravels, pressure grows for more regional and unilateral measures instead, and this is particularly difficult for African and other developing countries, because fragmented regulation raises compliance, complexity [and] transaction costs.”

In response to the Argentina-Liberia-Panama proposal that opponents of the framework had coalesced around, the Solomon Islands pointed out that, in seeking “consensus”, this group was ignoring the numerous parties that wanted more ambition, rather than less. It stated in a submission:

“There is no reason to expect that a new proposal, that differs from the IMO net-zero framework, would find a majority, much less a consensus.”

Nevertheless, supporters of the net-zero framework also acknowledged that there were some areas where greater clarity might help countries to finalise the details.

These areas include clarifying technical considerations such as: how fuel intensity is calculated; addressing the potential impacts of net-zero rules on food security; the governance of the IMO fund; and regulation of sustainable fuel certification schemes.

Given this, there was broad support for more discussions at an extra “intersessional” meeting later this year, in order to hash out these final details before attempting to approve the net-zero framework once more.

What was the final outcome from the IMO meeting?

Ultimately, the IMO’s net-zero framework was agreed and will now be negotiated further in the uutumn, ahead of the next MEPC meeting in December 2026.

The decision, as well as the general willingness to move forward noted by numerous observers, was broadly welcomed. IMO secretary-general Arsenio Dominguez said:

“We are back on track, but we have to rebuild trust. I encourage you to maintain this momentum through your intersessional work and to prepare submissions that can bring the membership together.”

Over the week of negotiations, nearly 100 delegations took to the floor to voice their opinions on the adoption of the net-zero framework.

Of these, over half were in favour of it, including countries like the EU, Brazil, Colombia, Kenya, Tuvalu and others.

Others pushed for reopening the framework for substantial changes, including the US, UAE, Saudi Arabia, Liberia and others.

On Friday 1 May, the discussion turned to the terms of reference for further negotiation and countries agreed to move the net-zero forward as the only option in the final outcome text.

Em Fenton, senior director of climate diplomacy at Opportunity Green, tells Carbon Brief:

“The framework has survived, but survival is not a victory and we cannot end up in a cycle of open-ended negotiations. Taking forward consideration of multiple proposals is only acceptable as a bridge, not a destination.

“We must now look forward to moving towards adoption of the framework later this year in a way that maintains urgency and ambition, and delivers justice and equity for countries on the frontlines of climate impacts.”

The IMO committee agreed to establish an intersessional working group to resolve a number of outstanding concerns and “drive broader convergence on a global measure” ahead of the next MEPC meeting.

Member states will be able to submit new amendments and adjustments to complement those already approved.

The two intersessional meetings will take place in September and November, ahead of MEPC85 in December.

Christiaan De Beukelaer, senior lecturer in culture and climate at the University of Melbourne, tells Carbon Brief:

“The ship is mostly built, though it’s obvious that more work needs doing on its interior. Right now, some are trying to finish the build while others are trying to scuttle it.”

The post Q&A: How countries got the global ‘net-zero’ shipping deal ‘back on track’ appeared first on Carbon Brief.

Q&A: How countries got the global ‘net-zero’ shipping deal ‘back on track’

The United Nations Secretary-General and foreign ministers from the UK, France and Spain have blamed the deadly wildfires engulfing Europe on climate change, using the disaster to renew calls for faster cuts to greenhouse gas emissions.

António Guterres told journalists on Friday that the “climate crisis is in overdrive”, adding that global heat seen so far is just a “warm up act” as a phenomenon known as El Niño intensifies “adding fuel to a planet already on fire”.

A new World Meteorological Organisation (WMO) report published on Friday predicts that the weather pattern will grow into a “strong event” between now and October, increasing the risk of higher than normal temperatures across much of the world and disrupted rainfalls.

“That risks shattering every seasonal record – and driving even more severe effects worldwide,” Guterres said.

El Niño builds on top of an already warming world, driven primarily by the burning of fossil fuels. A WMO scientist, who did not want to be named, told journalists that all the heatwaves and other climate impacts seen so far this year are “before the effects of El Niño are really kicking in at a global scale”.

Fossil fuellling the fires

Fires have broken out across much of Europe but are threatening the most people in the south-west of France near Bordeaux and in Central Spain near Madrid. Nearly a quarter of a million people have been evacuated in France with hundreds of homes destroyed while in Spain 80,000 people have had to leave their homes and at least 13 died in one village.

A scientific study published on Friday by the World Weather Attribution group found that man-made climate change made deadly fires in France twice as likely and those in Spain twenty times more likely. Smaller fires in the UK were not analysed by the study.

UN Climate Change leader Simon Stiell blamed fossil fuels for the fires, as well as storms in Chile and heatwaves in North America and Japan in recent weeks. “The climate alarm is blaring”, he said on Wednesday.

Guterres criticised new fossil fuel production projects and fossil fuel subsidies for causing hardship across the world. Discussing his speech, a senior UN official – who did not want to be named – said the subsidies amounted to trillions of US dollars a year and criticised pension funds and institutional investors, including insurance companies, for continuing to invest in fossil fuel projects.

Asked why world leaders and the public are not prioritising climate action, Guterres said they are distracted by wars in Ukraine, the Middle East, Sudan and elsewhere and sometimes forget “other aspects that are a sometimes even more dangerous threat”.

Also the fossil fuel industry and “some countries” are campaigning to pretend that climate change does not exist, he said, adding that the UN should be more active in “naming the situations as they are and the responsibilties as they are and mobilising the public opinion”.

After meetings in Paris and Madrid earlier in the week, the UK’s new foreign minister Ed Miliband issued joint statements with his French and Spanish counterparts – Jean-Noël Barrot and José Manuel Albares Bueno – calling on the world to reduce its dependence on fossil fuels.

They promised to do more to reduce emissions and protect their people and encouraged other governments to do the same.

The UK-French statement called on governments to publish UN climate plans, known as nationally determined contributions (NDCs), which are aligned with the Paris Agreement’s goal to limit global average temperatures to 1.5C above pre-industrial levels.

According to Climate Action Tracker, only three countries – the UK, Nigeria and Norway – have submitted NDCs with 2035 emissions reduction targets which are compatible with 1.5C. Fifty-two countries – including Egypt, Vietnam and Argentina – have yet to submit an NDC at all.

Defending science

Beyond action on emissions, the ministers also intervened in an ongoing dispute over the timing of the Intergovernmental Panel on Climate Change’s (IPCC)’s next flagship assessment.

Miliband and Barrot’s statement said they “underline the importance” of scientific report feeding into governments’ next global stocktake of progress on climate action in two years’ time, calling it a “critical input” to that process.

The timing of this report has been a contentious issue in government negotiations at the IPCC and at June’s climate talks in Bonn. While a group of nations calling themselves the “friends of science” want the report before the stocktake, others like Saudi Arabia and India have argued that this would make the report of a worse quality and less inclusive of developing countries’ scientists.

Science ‘under attack’ from fossil fuel interests at UN climate talks

The UK-Spanish statement weighed in less explicitly on this issue but said that they “recall the importance of scientific evidence and acknowledge the work of the IPCC in this respect.”

The British and French ministers said they would seek to accelerate reductions of emissions in methane, a particularly potent greenhouse gas, at COP31 in November. They encouraged governments “to work jointly to develop a marketplace for fossil fuels with near-zero methane intensity.”

Methane leaks from oil, gas and coal production are a major contributor to global warming. Over a 20-year period, methane traps around 80 times more heat than carbon dioxide.

The UK and Spanish statement emphasised the importance of supporting the Global South and underlined the need to mobilise sustainable financing “at scale with the challenge we face”. The previous UK government, in which Miliband was energy minister, cut climate finance to developing countries to pay for increases in military spending.

The UK government led by new Prime Minister Andy Burnham has yet to outline any major changes to climate finance in its two weeks in power but has announced it will convert some finance from grants to loans in order to free up money to subsidise bus travel in England.

More adaptation needed

Guterres said that “it is time to stop treating each disaster as an isolated tragedy and recognise the systemic risk that is unfolding before our eyes.” A recent study found that three-quarters of UK media reports about the British June heatwave did not mention climate change.

As well as reducing emissions, the UN Secretary-General called for measures to adapt vulnerable people to extreme heat. Specifically, he said that buildings should be built and retrofitted for extreme heat and that every city and country should have heat-health action plans and early warning systems. Over 250 cities have joined the UN’s ‘beat the heat’ initiative, he said.

The Portuguese diplomat called for governments and employers to do more to protect their workers from heat, criticising global fashion brands for not setting heat standards for the factories that supply them. “No one should have to risk their life to earn a living,” he said.

The post UN chief warns climate crisis “in overdrive” as El Niño threatens to fuel the fire appeared first on Climate Home News.

UN chief warns climate crisis “in overdrive” as El Niño threatens to fuel the fire

Climate Change

‘Ride the wave of momentum’: Australia announces once-in-a-decade Marine Parks Network review

In response to the federal government announcing its once-in-a-decade review of Australia’s Marine Parks Network, the following lines can be attributed to Elle Lawless, Senior Campaigner at Greenpeace Australia Pacific:

“Greenpeace Australia Pacific welcomes today’s announcement that the Albanese Government will review Australia’s Commonwealth Marine Parks Network. This is a rare, once-in-a-decade opportunity to strengthen our marine parks and ban industrial fishing in Australia’s marine protected areas.

“Australians would be appalled to know that more than half of Australia’s Marine Parks Network currently allows for extractive industries, like longlining, bottom trawling and oil and gas mining. These so-called ‘protected’ areas were designed to safeguard our beloved ocean wildlife and underwater ecosystems – that is what Australians expect. Damaging industrial industries should not be given a free pass to trawl, fish, drill or extract from our marine parks.”

“With the first Ocean COP just around the corner, and off the back of Australia’s move to ratify the Global Ocean Treaty earlier this year, the Australian government has a unique opportunity to ride the wave of this momentum and solidify itself as a true global ocean leader.

“Greenpeace Australia Pacific is calling for industrial activities to be banned from our protected waters and for at least 30% of Australia’s ocean to be protected as ocean sanctuaries. This review presents a rare opportunity to create more ocean sanctuaries, true blue havens where ocean life can recover, thrive and repopulate the surrounding waters.”

—ENDS—

‘Ride the wave of momentum’: Australia announces once-in-a-decade Marine Parks Network review

In recent days, prominent climate sceptics and rightwing commentators have shared charts on social media incorrectly implying that Europe is having its “quietest” year for wildfires in 2026.

These include Dr Matthew Wielicki, a former University of Alabama geochemist and self-described “professor in exile”, who was recently appointed by the Trump administration to lead the US Global Change Research Program.

However, these charts paint a misleading picture as they are skewed by encompassing the entirety of Russia in the data – including the vast plains of Siberia.

These charts also use data that include fires that are deliberately lit to manage cropland, which is a declining practice across much of Europe.

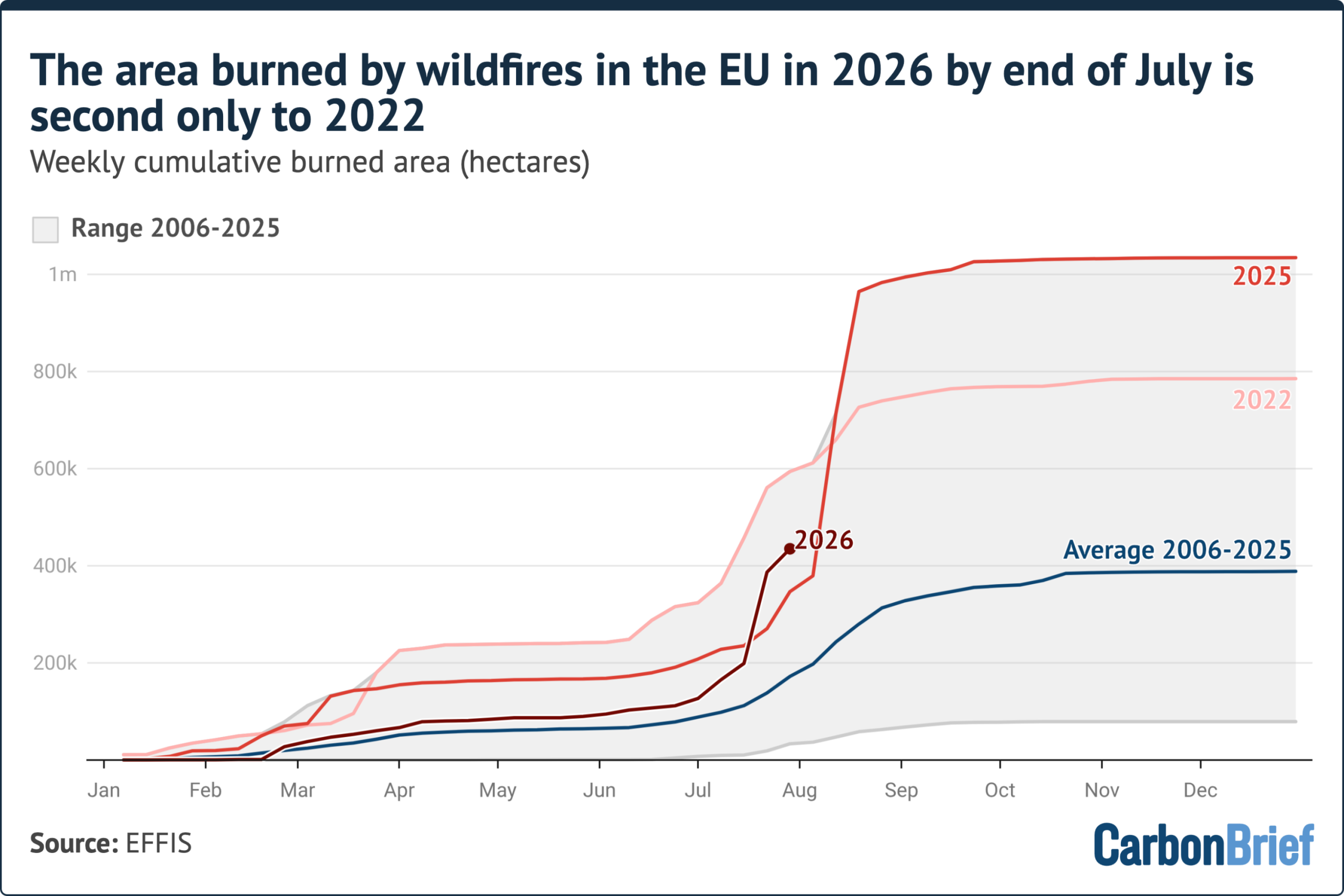

In this factcheck, Carbon Brief shows that the area burned by wildfires across the European Union in 2026 is second only to 2022 for this time of year.

The latest data from the European Forest Fire Information System (EFFIS) also shows that France has set a new modern record for area burned and Spain’s wildfire season is among the worst on record.

The fires have displaced more than a third of a million people across south-western Europe, while an impending heatwave has also raised fears of the fires worsening in the coming days.

‘Quietest year’

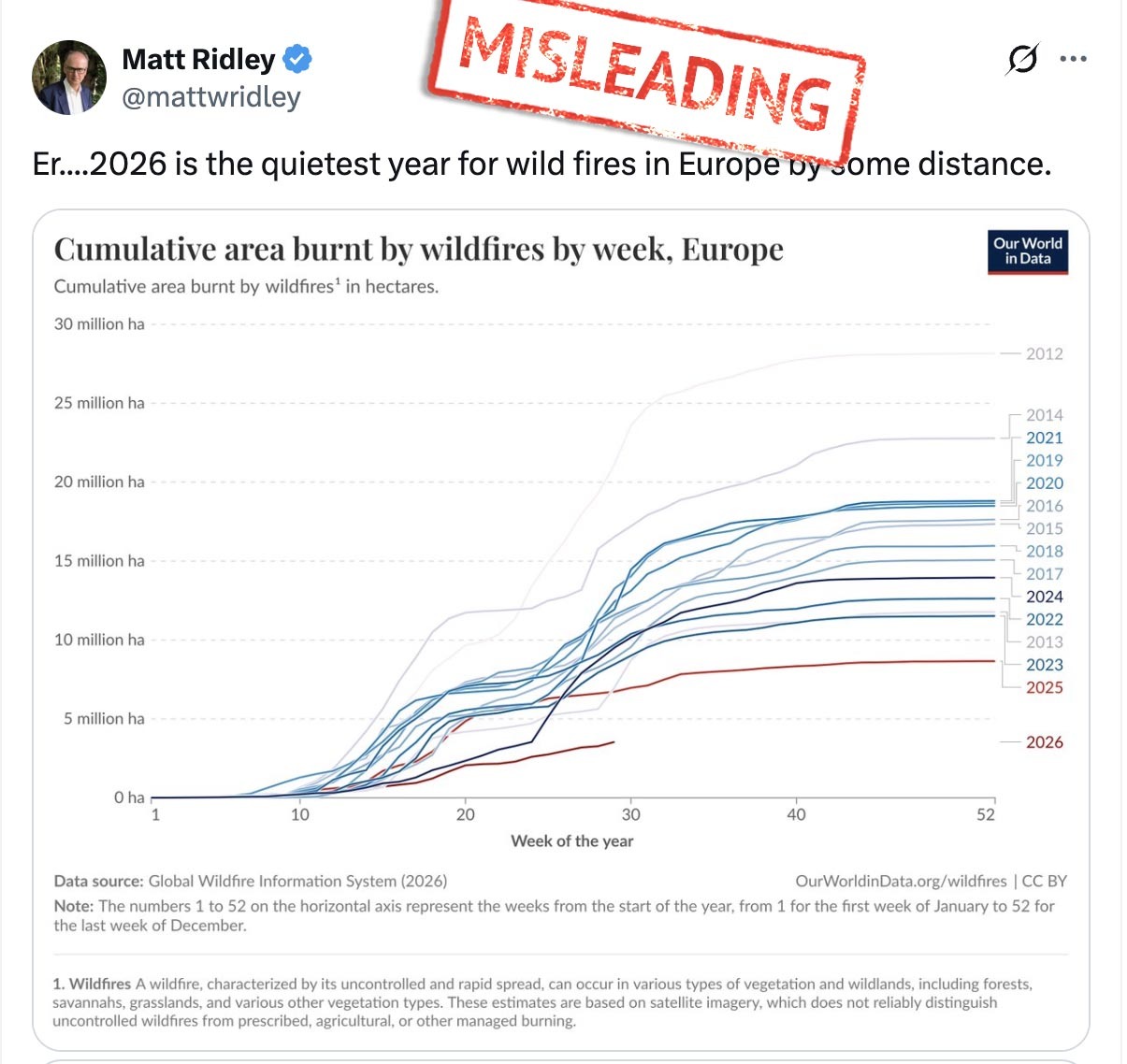

On 27 July, as wildfires raged across multiple European countries, former Conservative peer and climate-sceptic commentator Matt Ridley posted on Twitter that “2026 is the quietest year for wildfires in Europe by some distance”.

Ridley, who sits on the academic advisory council of the Global Warming Policy Foundation (GWPF), a UK-based climate-sceptic lobby group that refuses to reveal the sources of its funding, was responding to an article by Daily Telegraph columnist Tim Stanley.

Stanley’s column, headlined: “Climate change is real – and the right needs to get serious about it”, warned:

“This is no longer a matter of speculation: the wildfires of Europe, pitiless and persistent, are the way we live now.”

Ridley included a chart from Our World In Data, showing the cumulative area burned by wildfires by week for Europe. The chart puts 2026 as having the smallest area for this time of year in a dataset going back to 2012.

Ridley’s post was widely shared by prominent rightwing figures – including Richard Tice, deputy leader of the hard-right, climate-sceptic Reform UK party, former Conservative cabinet minister Jacob Rees-Mogg and multiple commentators.

Separately, Wielicki also shared a chart on Twitter to imply that wildfires in Europe are declining. Wielicki has previously claimed that the “science is not settled on climate change”.

The charts posted by Ridley and Wielicki both use data from the Global Wildfire Information System (GWIS). The GWIS category for “Europe” encompasses all the countries on the continent and includes the whole of Russia.

As a result, Russia accounts for about 74% of the area included in the GWIS definition of “Europe”.

Wildfires in Russia typically account for 80-90% of the burned area in the GWIS Europe dataset. In 2026, fires in Russia are substantially below average. Therefore, including Russia in this comparison creates the false impression that wildfire activity across Europe is unusually low.

Dr Calum Cunningham, a research fellow at the University of Tasmania’s Fire Centre, says that such claims are “highly misleading”, noting that “they rely on aggregating fire activity across an enormous and climatically diverse region”. He tells Carbon Brief:

“A relatively quiet season in Russia can easily mask an exceptionally active season in France or Spain. If the analysis is focused on the regions actually experiencing the current fires, the picture is very different.

“The reality is that western Europe has experienced an extraordinary sequence of climate conditions this year.”

In contrast, the EFFIS provides a subset of wildfire data specifically for the area covered by the 27 nations of the EU, which, therefore, excludes Russia.

Another difference between the two datasets is that GWIS monitors all fires – including those on agricultural land that are intentionally set alight. The burned area as measured by GWIS contains significant cropland area.

By contrast, EFFIS uses land-cover data and other information to filter specifically for forest fires.

Looking at the EU-only data from EFFIS reveals that Europe is far from having its “quietest” year. The bloc’s burned area, as of 29 July, is almost 435,000 hectares (ha) – second only to 2022 for this time of year.

Notably, Wielicki has actually continued to post charts based on GWIS data, even after acknowledging that “includ[ing] all of Russia, including vast areas of Siberia…isn’t a good proxy for Europe”.

French fires

Even looking at EU-wide data misses the scale of this year’s wildfires for some individual countries.

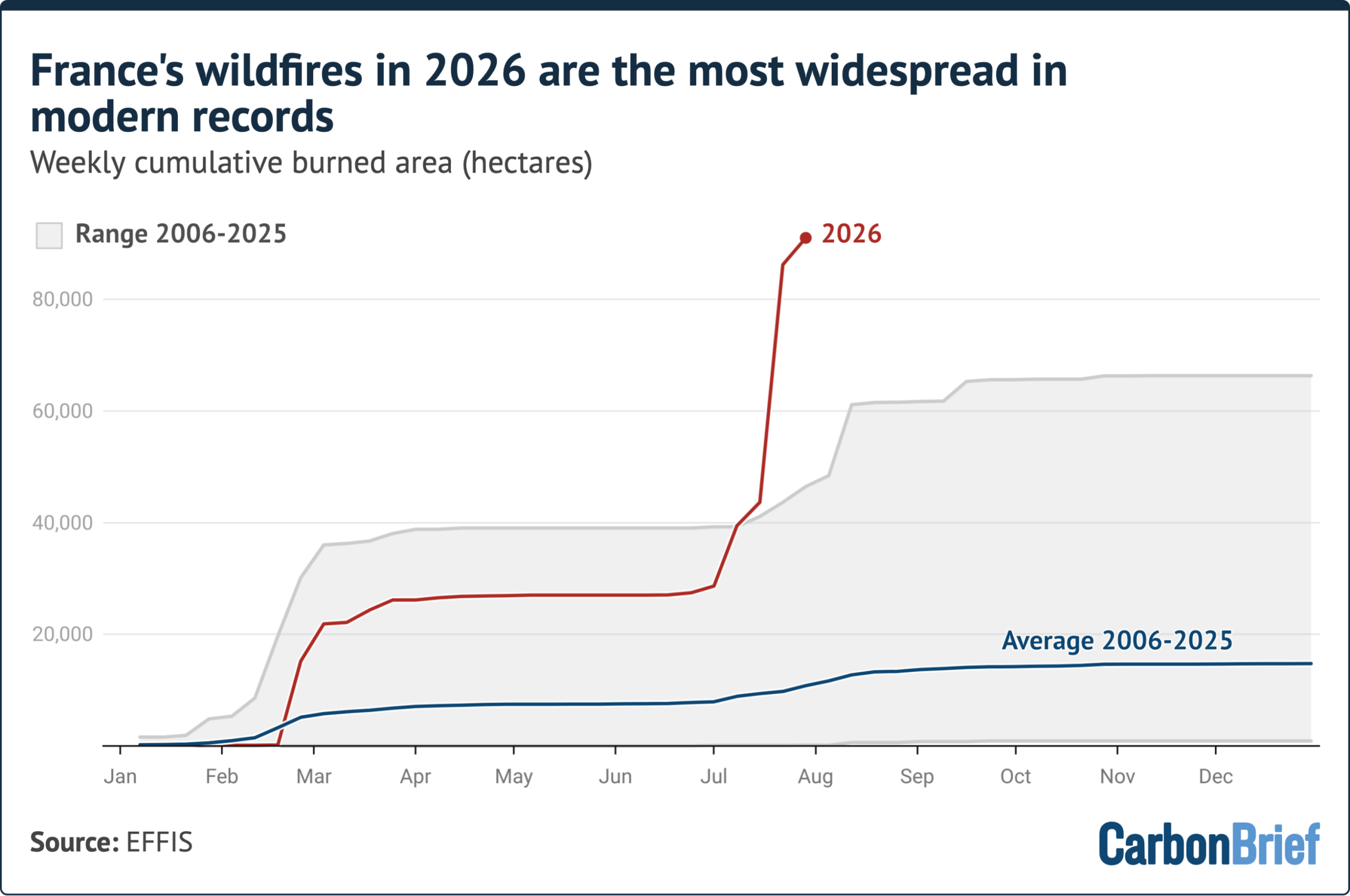

The chart below shows the surge in burned area in France since mid-July.

For much of the first half of the year, the country was having a wildfire season that was only slightly above average in terms of total burned area. However, a notable uptick began in the first week of July.

The third week of the month saw France break its previous cumulative annual record by more than 19,000ha. That gap has widened as the fires continue to burn; as of 29 July, the cumulative burned area in France during 2026 was nearly 24,700ha above the previous record.

The fires in France follow a record-breaking June heatwave that “dried out vegetation across the region, allowing fires to spread quickly”, wrote the New York Times.

On 27 July, French president Emmanuel Macron called a “crisis cabinet meeting” in order to address the fires “ravaging several areas of south-west France”, said France 24.

More than 220,000 people have been evacuated due to the Gironde fire, west of Bordeaux, in “what may be France’s largest peacetime evacuation”, reported the Associated Press.

In the Conversation, Cunningham and two other University of Tasmania researchers write that evacuation orders “protec[t] human lives, but makes it more likely houses and other structures will burn if there’s no one to defend them”. They add:

“There is little doubt climate change has made France and Spain’s wildfires worse. They represent yet another reason to redouble our efforts to tackle climate change and stabilise our climate.”

Central Spain scorched

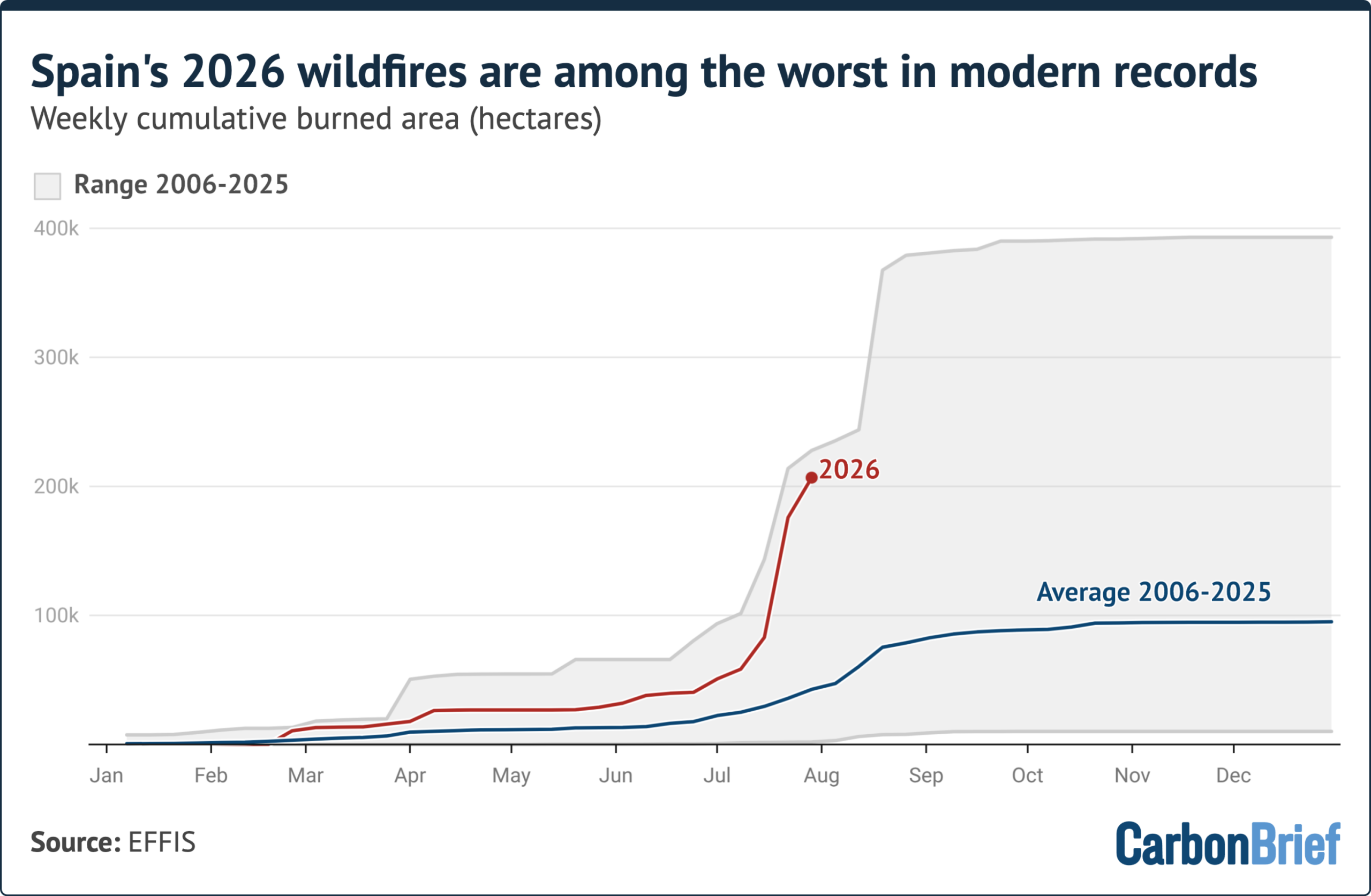

While Spain’s fire season has not broken records in the same way that France’s has, it is on track to be among the worst since EFFIS began reporting data in 2006.

The chart below shows the rapid increase in burned area in Spain since 8 July. The latest data from EFFIS reveal that, as of 29 July, Spain has almost matched its previous record at this point in the year. It is also nearly five times the average area burned for this time of year.

In Spain, the wildfires have been concentrated in the central part of the country, near Madrid.

BBC News reported that the fires outside the capital have burned “an area more than twice as large as the city itself”.

Nearly 90,000 people were forced from their homes in central Spain by the fires, said the Associated Press.

Pedro Sánchez, Spain’s prime minister, called the fires a “painful expression” of climate change.

Meanwhile, the UK, French and Spanish governments have issued joint statements this week in response to the fires. The UK/Spain statement begins:

“This summer’s wildfires demonstrated that climate change was now a national security emergency facing Europe and threatening our way of life.”

Related

The post Factcheck: No, Europe is not having its ‘quietest’ year for wildfires appeared first on Carbon Brief.

Factcheck: No, Europe is not having its ‘quietest’ year for wildfires

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测