Disseminated on behalf of Alaska Energy Metals Corporation.

The global nickel market enters 2026 after a bruising and uneven year. In 2025, macroeconomic stress, trade disruptions, and deep supply imbalances reshaped pricing and sentiment. Although short-term rallies have returned, the underlying structure of the market remains fragile. As a result, 2026 is shaping up to be a year defined by volatility rather than a sustained recovery.

A Challenging Backdrop from 2025

To understand where nickel is headed, it helps to revisit the environment it emerged from. In 2025, global trade flows came under pressure after the US implemented new tariff policies. These measures disrupted supply chains and dampened confidence across industrial commodities. At the same time, global manufacturing growth slowed, weighing heavily on the broader nonferrous metals complex.

SMM reported highlighted some significant points. Adding to the uncertainty, the US Federal Reserve sent mixed signals throughout the year. Expectations around interest rate cuts shifted repeatedly. Each change altered risk appetite and triggered sharp moves across commodity markets. Nickel, already vulnerable due to oversupply, struggled to attract sustained buying interest.

China attempted to offset some of these pressures. Policymakers rolled out proactive fiscal measures and maintained a moderately accommodative monetary policy. They also focused on boosting domestic demand and diversifying export routes to reduce exposure to trade frictions. In July, China introduced its “anti-involution” policy, aimed at curbing destructive price competition across industries.

Even so, nickel underperformed. While other nonferrous metals showed mixed results, nickel remained constrained by a clear mismatch between supply and demand. Prices trended lower for most of the year. LME nickel opened near $15,365 per tonne and slid to lows around $13,865 per tonne, marking a sharp reset in the price center.

2026 Nickel Price Outlook: A Volatile Start to the New Cycle

Momentum shifted suddenly toward the end of the year. From mid-December, nickel prices began climbing rapidly.

- By early January, LME prices had surged past $18,000 per tonne, the first time in more than a year. In just 12 trading sessions, prices jumped nearly 20%, catching many traders off guard.

Several factors fueled this rebound. Demand signals from China improved modestly, particularly from stainless steel mills and EV battery producers. At the same time, speculative positioning adjusted as supply risks from Indonesia returned to the spotlight.

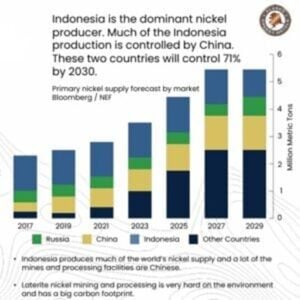

Trading Economics analysis stated that Indonesia, the world’s largest nickel producer, hinted at a potential 34% reduction in output for this year. Meanwhile, Vale temporarily halted operations at its Pomalaa and Bahodopi mines while waiting for regulatory approvals. Although its flagship Sorowako mine continued operating, these pauses added to market caution.

Still, the rally faced clear limits. Inventory levels remained elevated. Combined LME registered and off-warrant stocks jumped nearly 58% last year, reaching more than 367,000 tonnes. In addition, large shadow inventories in Singapore and Kaohsiung continued to hang over the market. As a result, every price spike met resistance.

Price Expectations Remain Capped

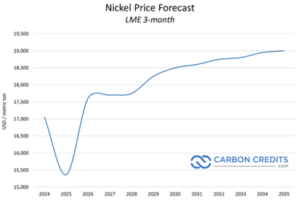

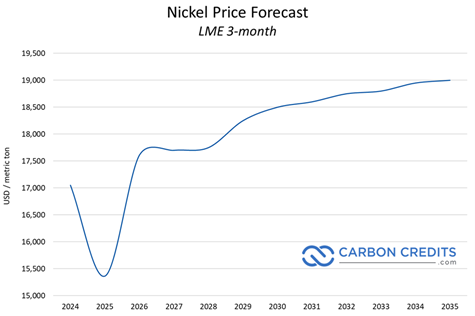

Most analysts expect nickel prices to settle into a narrow band rather than trend sharply higher. Forecasts largely cluster between $15,000 and $16,000 per tonne. Several major institutions attribute the restrained outlook to ongoing surpluses.

- The World Bank’s 2026 nickel price outlook also revealed nickel prices to stay around US$15,500, rising to US$16,000 in 2027.

- Trading Economics data indicated that nickel futures moved back up to nearly $17,800 per tonne, reversing last week’s steep decline as buyers stepped back into the market.

Analysts consider that the differences in price forecasts primarily reflect contrasting views on how strictly Indonesia will enforce production limits and how quickly global manufacturing activity is expected to recover.

- CHECK: LIVE NICKEL PRICES

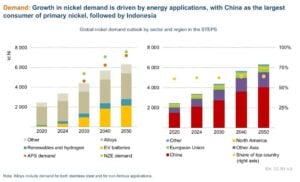

Nickel Demand Drivers Show Modest Growth

- Stainless steel: remains the dominant driver, accounting for about 70% of total demand. Consumption may rise to roughly 2.45 to 2.5 million tonnes. China’s production recovery offers support, while infrastructure projects in emerging markets add incremental demand. Still, no major surge is expected.

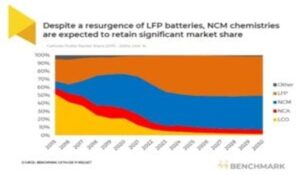

- Battery and EV application: They make up roughly 13% to 15% of demand. Nickel use in this segment could reach up to 500,000 tonnes. High-nickel cathodes continue to support premium EV models.

According to Benchmark Mineral Intelligence, demand for battery-grade nickel is expected to surge, tripling by 2030. This growth will largely be due to mid- and high-performance EVs in Western markets.

Other uses, including alloying, plating, aerospace, and electronics, provide steady but smaller contributions. A broader manufacturing recovery and net-zero investments could lift demand slightly, while faster EV adoption remains the main upside risk.

Supply-Demand Balance Stays Uneven

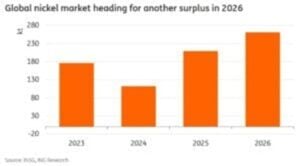

According to SMM, the nickel market will remain oversupplied through the year, remaining between 120,000 and 275,000 tonnes. While short-term rallies may continue, oversupply will remain the dominant force.

On the supply side, Indonesia’s refined nickel output stays high, supported by sunk investments and low operating costs. On the demand side, growth remains steady but unspectacular.

Ewa Manthey, a commodities strategist at London-Based ING Group, explained that the global nickel market is still set to remain oversupplied, with a projected surplus of about 261,000 metric tonnes. As a result, any production cuts would need to be deep and sustained to meaningfully shift market fundamentals.

China’s real estate support policies may provide limited relief for stainless steel consumption. However, a strong housing rebound appears unlikely, and any improvement is expected to be gradual. Similarly, demand from ternary batteries faces structural headwinds. Solid-state batteries remain years away from large-scale commercial use, and near-term battery chemistry trends do not favor a sharp jump in nickel intensity.

As a result, the average price level may drift lower over time. Tightening ore supply could briefly push prices above $16,000 per tonne. However, high inventories and excess capacity will take longer to absorb.

Why Nickel Matters for US Critical Mineral Independence?

Nickel plays a critical role in military-grade alloys, advanced weapons systems, electric vehicle batteries, grid-scale energy storage, and broader clean energy infrastructure. Despite its importance, the United States remains almost entirely dependent on imports for nickel, while China controls much of the global processing and supply chain. This reliance has become a clear strategic risk, one that domestic resources need more exploration.

And this is the reason America’s push to secure its critical mineral supply is gaining real momentum.

Spotlight: Alaska Energy Metals – America’s Nickel Backbone

At the center of this shift is Alaska Energy Metals Corporation (TSX-V: AEMC, OTCQB: AKEMF) and its Eureka deposit, the largest documented nickel resource in the United States. As Washington intensifies efforts to reshore critical supply chains for national security and clean energy goals, AEMC’s Nikolai Project in Alaska is steadily gaining recognition as a strategic domestic asset.

At the same time, the project aligns closely with the Trump administration’s executive orders focused on critical minerals and Alaska resource development. Those directives sought to speed up domestic production, curb reliance on foreign suppliers, and reinforce US security interests.

Against this backdrop, Nikolai stands out as a fully US-based “Sulphide nickel and battery metal project” to meet the country’s metal needs for the energy transition. Significantly, it has two claim blocks: Eureka and Canwell.

Eureka: The Largest Known Nickel Resource in the US

The Eureka deposit is not just large—it is nationally strategic. It hosts nickel alongside copper, cobalt, chromium, iron, and platinum group metals, including platinum and palladium. This metal mix makes Eureka highly relevant for both defense systems and the expanding clean energy economy.

According to the 2025 Mineral Resource Estimate, Eureka contains:

- Indicated Resource of 814 million tonnes grading 0.42% nickel equivalent, representing 5.62 billion pounds of nickel in situ.

- Inferred Resource of 896 million tonnes grading 0.39% nickel equivalent, totaling 9.38 billion pounds of nickel in situ.

Combined, the deposit contains more than 15 billion pounds of nickel, enough to support American demand for decades.

FAST-41 Listing Accelerates the Nikolai Project

A major step forward came when the Nikolai Project was accepted onto the FAST-41 Transparency Dashboard by the Federal Permitting Improvement Steering Council.

- The initial phase focuses on infrastructure upgrades, including rehabilitation and extension of the Rainy Creek Mining Trail, installation of temporary bridges, and development of an on-site camp.

These improvements will lower exploration costs, improve safety, enable better site access, and speed up the transition to advanced exploration and development at Eureka. Just as important, FAST-41 provides transparency, inter-agency coordination, and defined permitting milestones.

Key catalysts ahead

AEMC is entering a phase with several near- and mid-term value drivers. These include a first-pass metallurgical study to assess metal recovery, the potential for a major US Department of Defense grant, completion of a Preliminary Economic Assessment, and continued drilling at the Angliers target. Each step strengthens the investment and strategic case for Eureka.

Nickel Oversupply Overseas, Opportunity in the US

In summary, the nickel market faces another complex year. Structural oversupply, elevated inventories, and cautious demand growth define the landscape. Although policy shifts in Indonesia and short-term demand improvements can trigger sharp rallies, fundamentals continue to cap sustained upside. For now, nickel remains a market driven more by volatility than by balance.

As the US rebuilds its domestic critical mineral supply chain, assets like Eureka are becoming indispensable. With its scale, multi-metal profile, federal permitting support, and alignment with national policy priorities, Alaska Energy Metals Corporation is positioning itself as a key player in America’s push for resource security. In a world increasingly defined by competition for critical metals, Eureka has the potential to become the backbone of the US nickel supply for generations.

READ MORE: Nickel Demand to Triple by 2030: Can the Market Keep Up?

The post Nickel Prices Hit $18,000 in 2026 Amid Global Oversupply, US Boosts Domestic Supply Chain appeared first on Carbon Credits.

Disseminated on behalf of Alaska Energy Metals Corporation

The global nickel market is shifting fast. Years of oversupply pushed nickel prices lower and delayed new mining investments. But recent price gains suggest the cycle may be turning. In early 2026, nickel prices jumped about 18% in a single month, highlighting how sensitive the market is to supply expectations.

For investors, this shift creates a high-risk, high-reward opportunity. Early-stage developers advancing projects today could benefit disproportionately when deficits emerge. Alaska Energy Metals Corporation (AEMC) sits at the center of this narrative, with its Nikolai Nickel Project moving toward a Preliminary Economic Assessment (PEA) in 2026 and growing momentum in the U.S. critical minerals policy landscape.

Nickel Prices Are Rising, and the Market Is Fragile

Nickel’s recent rally reflects growing concerns about future supply. Indonesia dominates global nickel production, and any policy shift there can move prices instantly. Markets reacted strongly to speculation about Indonesian output controls, showing how fragile the supply balance remains.

Despite today’s inventories, analysts warn that the world will need massive investment to meet future demand. Estimates suggest roughly $66 billion in global nickel supply chain investment may be required to avoid shortages later this decade.

This gap creates a structural opportunity. Low prices discourage new mines today, but demand from EVs, grid storage, and stainless steel continues to rise. And companies advancing projects during the downturn could benefit when the cycle flips.

Nikolai Nickel Project: A Strategic U.S. Critical Minerals Asset

AEMC’s flagship Nikolai Nickel Project in Alaska ranks among the largest undeveloped nickel resources in the United States. The project also contains copper, cobalt, chromium, platinum, palladium, and iron, making it a polymetallic critical minerals asset.

This resource mix strengthens the investment case. Nickel and cobalt are essential for batteries. Platinum group metals support hydrogen and industrial applications. Chromium and iron add potential by-product revenue streams.

Thus, domestic critical minerals projects like Nikolai are becoming strategic priorities as governments seek to reduce reliance on foreign supply chains.

New Work Program Accelerates Path to PEA

In October 2025, AEMC closed a $1 million non-brokered private placement, issuing roughly 11.8 million units at $0.085 per unit. Each unit included one common share and one warrant exercisable until October 2030. Insider participation and no finder’s fees signaled management confidence in the project.

The company outlined a focused work program designed to move Nikolai toward economic evaluation:

- Metallurgical studies to produce concentrates

- Hydrometallurgical testing to assess on-site metal production

- Permitting for road extensions and camp upgrades

- Internal economic evaluations for a PEA

- Planning for a 2026 field program and investor outreach

These steps are critical. Metallurgy, infrastructure, and early economics determine whether large deposits can become mines.

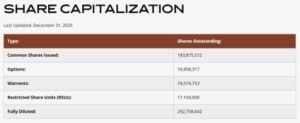

The current share structure shows:

Hydrometallurgy, RecycLiCo, and Lucid Partnership Add Value

AEMC’s Memorandum of Understanding with RecycLiCo Battery Materials adds a downstream processing angle. RecycLiCo’s U.S. subsidiary will test whether its hydrometallurgical technology can refine metals from Nikolai ore.

Alongside, the nickel miner has also signed an MOU with Lucid Group, Inc (NASDAQ: LCID), maker of the world’s most advanced electric vehicles.

AEMC confirmed hydrometallurgical studies as part of its development plan. On-site refining could reduce reliance on foreign smelters, improve margins, and strengthen U.S. supply chain security.

Integrated mining and refining projects often command premium valuations. They also attract government support and strategic partnerships.

Trump-Era Critical Minerals Push Boosts Domestic Projects

U.S. policy momentum around critical minerals accelerated during former President Donald Trump’s administration and continues to influence today’s strategy. Trump’s executive orders declared critical minerals a national security priority and directed federal agencies to support domestic mining, processing, and recycling.

This policy shift led to:

- Funding programs under the Defense Production Act

- Streamlined permitting initiatives

- Federal grants for mining, processing, and battery supply chains

- Public-private partnerships for domestic critical minerals

These initiatives laid the foundation for today’s expanded funding and permitting reforms. Projects like Nikolai align directly with this policy framework, positioning AEMC to benefit from federal incentives, grants, and offtake partnerships.

FAST-41 and Government Engagement Reduce Risk

Nikolai is listed on the U.S. Permitting Council’s FAST-41 Transparency Dashboard. FAST-41 aims to accelerate permitting and improve coordination across federal agencies.

AEMC has also reported ongoing engagement with U.S. government departments regarding Nikolai’s role in domestic supply chains. This alignment matters for investors. Government backing can reduce permitting risk, unlock funding, and attract strategic partners.

Emily Domenech, Permitting Council Executive Director.

“I am excited to welcome the Nikolai Nickel project to the FAST-41 program. We are proud to support more mining projects that will strengthen the U.S. economy and reduce our reliance on foreign nations. I look forward to working with the Alaska Energy Metals Development Corporation to provide a transparent and predictable federal permitting process while achieving President Trump’s vision for American energy dominance.”

2026 PEA: A Major Valuation Catalyst

AEMC has initiated internal scoping studies to evaluate mining rates, sequencing, and economics. Early plans focus on extracting higher-grade near-surface zones first to improve project economics.

The Preliminary Economic Assessment is a major milestone. It converts geological resources into financial metrics like net present value and internal rate of return. Mining equities often re-rate significantly after a credible PEA.

With a PEA targeted for 2026, AEMC could hit this milestone as nickel markets tighten—a powerful combination for valuation.

Valuation Leverage to Nickel Prices

Junior miners offer strong leverage to commodity prices. A 10–20% increase in nickel prices can dramatically improve project economics for bulk tonnage deposits. The recent 18% monthly nickel rally highlights how quickly sentiment can change. If prices stabilize near $18,000–$20,000 per tonne, project valuations could rise sharply.

Key upside catalysts include:

- Sustained nickel price recovery

- Positive metallurgical and hydromet results

- Completion of the PEA

- Permitting and infrastructure progress

- Government funding or strategic partnerships

Each milestone reduces risk and increases valuation multiples.

Macro Tailwinds: EVs, Grid Storage, and Infrastructure

Nickel remains critical for high-energy-density batteries used in premium EVs and heavy-duty applications. Even as lithium iron phosphate batteries grow, nickel-rich chemistries dominate performance segments.

Stainless steel demand also continues to grow with global infrastructure and urbanization. Combined demand growth will strain supply, especially as Indonesian ore grades decline and regulatory pressures increase.

Western governments are pushing to localize critical minerals supply chains. This macro backdrop supports long-term bullish scenarios for domestic nickel developers.

M&A and Strategic Optionality

Large miners, automakers, and battery manufacturers increasingly seek secure North American supply. Nikolai’s scale, polymetallic (high-grade Ni-Cu-PGE massive sulphide mineralization) profile, and location make it a potential joint venture or acquisition target.

Downstream processing partnerships further increase strategic value. Domestic refining capability could attract OEMs, defense contractors, and federal agencies seeking supply security.

This optionality adds upside beyond commodity price appreciation.

Investment Outlook: From Oversupply to Opportunity

The nickel market’s surplus today hides a structural supply challenge. Massive investment is needed to meet electrification demand, yet low prices discourage new projects. This disconnect creates asymmetric opportunities for developers advancing projects during downturns.

AEMC’s Nikolai Nickel Project sits at the intersection of rising demand, domestic supply chain policy, and improving market sentiment. The company has secured financing, launched metallurgical and hydromet studies, engaged government stakeholders, and targeted a 2026 PEA.

Trump-era critical minerals policies and ongoing federal funding programs further strengthen the domestic mining investment thesis. If nickel prices continue to recover and AEMC delivers on technical milestones, the company could see a significant valuation re-rating.

In a world racing to electrify and localize supply chains, domestic nickel developers are becoming strategic assets. AEMC could emerge as one of the most leveraged plays on America’s critical minerals push.

To sum up, AEMC CEO Gregory Beischer commented,

“The cost and time savings for further exploration and development once ground access is established will be quite significant. It is very encouraging to see proactive streamlining and coordination amongst permitting agencies. We are grateful to the Permitting Council for including the Nikolai Nickel project in the FAST-41 program. With Nikolai hosting six Critical Minerals – nickel, cobalt, copper, chromium, platinum and palladium, two of which, nickel and cobalt, are Defense Production Act Title III materials deemed to be in shortfall, we are extremely well aligned with the U.S. national security objective of developing long-lived, domestic sources of metals and minerals essential to the national economy and national defense. Nikolai is a project potentially capable of significantly reducing US nickel and cobalt import dependency and vulnerability.”

- MUST READ: Nickel Prices Hit $18,000 in 2026 Amid Global Oversupply, US Boosts Domestic Supply Chain

Live Nickel Spot Price

Unit: USD/Tonne——Loading Chart…

The post From Oversupply to Opportunity: AEMC’s Nickel Upside in a Tightening Market appeared first on Carbon Credits.

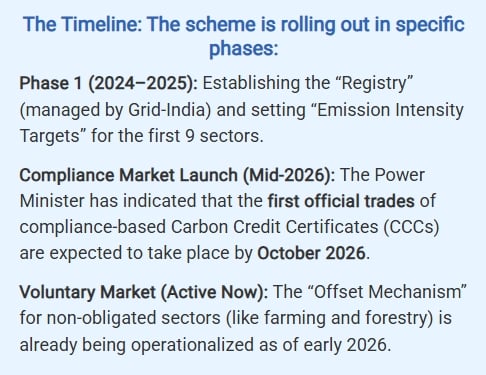

India has taken a major step toward building a working carbon market. The government has launched the Indian Carbon Market Portal, a central digital platform that will support the Carbon Credit Trading Scheme, or CCTS. With this move, India is no longer just designing its carbon market on paper. It is now putting the system into action.

The portal was launched at the International Conference on Carbon Markets, Prakriti 2026, held in New Delhi. Union Power Minister Manohar Lal said formal trading in carbon credit certificates is expected to begin within four months. That timeline makes the launch especially important. It shows that India is moving quickly from policy design to actual market operations.

The new portal will become the main platform for registration, monitoring, reporting, and verification of emissions. In simple terms, it will handle the back-end system needed to run a national carbon market. Companies that want to participate will need to register through the portal before they can trade carbon credits.

From Act to Action: India’s Carbon Market Story

2022: Laying the Foundation

India did not build this market overnight. The foundation was laid in 2022, when Parliament passed amendments to the Energy Conservation Act, 2001. These changes gave the government the legal power to create a carbon market and issue carbon credit certificates. That amendment was the first major sign that India wanted a structured, national system for carbon trading.

2023: Introducing the Carbon Credit Trading Scheme (CCTS)

After that, policymakers worked on the framework needed to turn the idea into reality. In 2023, the government formally introduced the Carbon Credit Trading Scheme. The CCTS created the core structure of the Indian Carbon Market and defined the roles of the institutions that would run it. It also set up the National Steering Committee for the Indian Carbon Market to oversee the framework.

This step mattered because carbon markets need strong governance to work properly. Without clear rules, trusted oversight, and proper measurement systems, trading can lose credibility. India’s approach has been to first build the rules and institutions and then move toward implementation.

Why the Portal Matters for Companies, Offsets, and Climate Goals

This structure fits India’s economy well. The country is still growing fast, and many industries are expanding. So instead of placing a fixed cap on total emissions right away, the system rewards firms that improve carbon efficiency. If a company performs better than its assigned greenhouse gas emission intensity target, it earns carbon credit certificates. If it falls short, it must buy credits from others.

That approach gives the industry some breathing room while still pushing it toward cleaner operations. It also sends a clear financial signal. The lower a company’s emissions intensity, the better its chance of earning value from the market. Over time, this can encourage investments in cleaner fuels, better equipment, energy efficiency, and modern industrial processes.

The compliance market will first cover large industrial units in energy-intensive sectors. These are the industries where emissions are high and where efficiency gains can make a real difference. By focusing first on major emitters, India is trying to create a market that targets the most important sources of industrial emissions.

The Indian Carbon Market Portal is important because it brings all parts of the system together in one place. The Bureau of Energy Efficiency, or BEE, will oversee the portal and the wider market. Through the platform, authorities will assess emissions data, track compliance obligations, and manage the issue and trade of surplus certificates.

That means the portal is not just a registration website. It is the digital backbone of the whole market. It supports the monitoring, reporting, and verification process, often called MRV. This part is critical because carbon markets only work when emissions data is accurate, transparent, and trusted. If the numbers are weak, the market cannot function properly. So the portal plays a central role in building credibility.

Voluntary Carbon Credits Expand India’s Market Reach

Along with the compliance market, India is also developing a voluntary offset market under the CCTS. This part of the system is open to a wider group of projects and participants. It allows eligible climate projects to generate carbon credits that can be traded.

This is an important feature because it expands the market beyond large industrial companies. It gives project developers, clean energy players, and other climate-focused businesses a chance to participate. In turn, that can help bring more investment into low-carbon activities across the economy.

The government has already approved several methodologies for voluntary carbon credit generation. These methodologies set the rules for how emissions reductions are measured and verified. They are essential because credits have value only when buyers trust that the reductions are real.

On March 28, 2025, India’s Ministry of Power approved 8 crediting methodologies for generating voluntary carbon credits, including:

- Renewable Energy

- Green Hydrogen Production

- Industrial Energy Efficiency

- Mangrove Afforestation and Reforestation

Supporting India’s Net Zero Goal

India’s carbon market also supports the country’s wider climate commitments. India has pledged to reduce the emissions intensity of its economy by 45% from 2005 levels by 2030. It has also committed to reaching net zero by 2070. A carbon market can help support both goals by encouraging industries to reduce emissions flexibly and cost-effectively.

At the same time, the market may help Indian companies deal with external carbon rules such as the European Union’s Carbon Border Adjustment Mechanism, or CBAM. As global trade becomes more carbon-conscious, Indian exporters may need stronger emissions data and proof of climate compliance. A domestic carbon market can help improve both.

The launch also fits into a bigger policy trend. India has recently placed more attention on industrial decarbonization, including support for carbon capture, utilisation, and storage in hard-to-abate sectors. This shows that the government is not relying on one solution alone. Instead, it is building a broader climate strategy that combines regulation, technology, finance, and market incentives.

In conclusion, India’s move comes at a time when climate regulation is becoming more important not only at home but also in global trade. A strong domestic carbon market can help Indian industries improve emissions tracking, manage compliance, and prepare for international carbon pricing systems. That gives the portal a much bigger role than just administration. It could become a key tool in India’s low-carbon growth story.

The post India’s Carbon Market Portal Goes Live as Carbon Credit Trading Nears appeared first on Carbon Credits.

Google has taken a major step in reshaping how large energy users interact with the power grid. The company has secured 1 gigawatt (GW) of demand response capacity across its U.S. data center operations with several utility partners. This allows Google to cut or shift electricity use during high demand. It helps stabilize the grid and reduce system costs.

The scale is significant. One gigawatt is roughly enough to power about 750,000 U.S. homes for a year. Demand response helps reduce peak power needs, which can cut grid strain during extreme heat or cold. It also reduces the need for expensive “peaker” plants that run only a few hours per year.

The company noted:

“Demand response enables our data centers to be valuable assets for the power grid. Our ability to shift or reduce our energy demand can help utility companies balance supply and demand and plan for future capacity needs. These agreements create a smart solution to make the electricity systems that serve our data centers more affordable and reliable.”

Demand Response: Turning Data Centers into Flexible Grid Assets

Google’s move reflects a growing challenge. U.S. electricity demand is rising fast. Data centers, especially those running artificial intelligence (AI) and cloud computing, are among the fastest‑growing power loads.

At the same time, building new power supply and grid infrastructure can take five to ten years or more. Google’s strategy bridges this gap by making demand more flexible instead of only increasing supply.

Demand response is a system where large electricity users reduce or shift power use during peak periods. Instead of running at full capacity all the time, facilities adjust operations based on grid conditions. This helps balance supply and demand in real time.

Google applies this by managing its data center workloads. It can delay or shift energy‑intensive tasks, especially machine learning and batch computing, to times when electricity demand is lower. This reduces energy use during peak grid stress without affecting performance.

It also turns data centers into flexible energy assets rather than fixed loads. Traditionally, grids treat demand as constant. Google’s model changes that assumption.

The company has built this system through agreements with multiple U.S. utilities, including:

- Tennessee Valley Authority (TVA)

- Indiana Michigan Power

- Entergy Arkansas

- Minnesota Power

- DTE Energy

These partnerships let grid operators ask Google to cut demand during stressful times, like heat waves or winter peaks. This helps keep the system reliable without just depending on backup generation.

Why Peak Demand Matters for Costs and Reliability

The timing of this move is critical. The U.S. Department of Energy projects that electricity demand could grow 20% or more by 2030, driven by electrification and digital services.

Data centers are a major part of this growth. With AI workloads increasing rapidly, total data center energy use rose over 20% between 2020 and 2025 in the U.S., according to industry studies.

At the same time, grid expansion faces delays. Building new transmission lines or power plants can take years or even decades due to permitting, siting, and cost challenges. Demand response offers a faster solution that can be deployed now.

Google notes that flexible demand can help utilities:

- Balance supply and demand in real time,

- Avoid building rarely used “peaker” plants,

- Reduce stress on transmission systems, and

- Lower wholesale electricity prices during peaks.

Even small flexibility gains can have large system‑wide effects. Research from the Electric Power Research Institute (EPRI) suggests that demand response programs could reduce peak load by 10–20% in many regions, leading to significant savings in infrastructure costs.

This is because peak demand drives infrastructure spending. Power systems are often built to meet only a few hours of extreme demand each year. Reducing those peaks can delay or avoid costly investments in generation and transmission.

Cost Savings and Reliability Gains

Google’s demand response strategy targets two key outcomes: lower costs and improved reliability.

- First, cost reduction. Peak demand periods often coincide with the highest wholesale electricity prices. By lowering demand during those hours, both Google and utilities can save money. These savings can help stabilize electricity prices for businesses and households alike.

- Second, reliability. Power grids face increasing pressure from extreme weather, electrification of transport and buildings, and higher loads from digital infrastructure. Demand response adds flexibility that helps prevent outages when supply is tight.

Google’s system allows it to cut the load quickly when needed. This gives grid operators more tools during tight supply conditions. It also reduces the risk of blackouts and emergency calls for conservation.

Importantly, this approach does not reduce overall energy use over time. Instead, it shifts when energy is used. This makes the system more efficient without limiting long‑term growth in data center activity or other demand.

SEE MORE:

- Google Taps Earth’s Heat in 150MW Geothermal Deal with Ormat Technologies to Power Data Centers

- Google Pledges $50M to Fight Superpollutants by 2030: A Near-Term Climate Game Changer

A Shift in Energy Strategy for Big Tech

Google’s move reflects a broader shift across the technology sector. Large tech companies are no longer just energy consumers. They are becoming active participants in energy systems.

This change is driven by several trends:

- Rapid growth in AI workloads that require large computing resources;

- Rising energy costs that pressure operating margins;

- Corporate climate targets tied to investor and public expectations; and

- Pressure to secure a reliable power supply amid grid uncertainty.

Demand response is now joining renewable energy procurement as a core strategy. Google has already invested heavily in solar, wind, geothermal, and energy storage. The company regularly ranks among the top corporate buyers of renewable energy, which helps avoid emissions.

Other industries have used demand response for years, including manufacturing and heavy industry. However, its use in data centers is still new. The scale of Google’s 1 GW deployment signals that this model could expand quickly and be adopted by other large energy users.

Linking Demand Response to Google’s 24/7 Carbon-Free Goals

Google’s demand response move also supports its wider clean energy and climate strategy. The company aims to run on 24/7 carbon‑free energy by 2030 and reach net‑zero emissions across its operations and value chain by 2030.

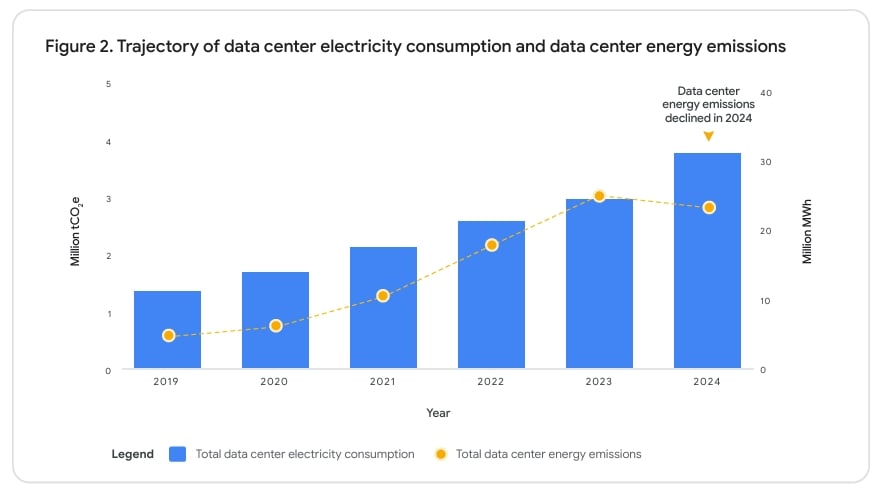

Progress is ongoing. In 2024, Google matched about 66% of its electricity use with carbon‑free energy on an hourly basis, even as power demand rose due to a 27% increase in workload from AI and cloud services.

At the same time, Google added 2.5 GW of new clean energy capacity to the grids serving its operations and cut data center energy emissions by 12% compared with baseline years.

Demand response helps close the remaining gap. By shifting when electricity is used, Google can better match operations with clean energy supply. This improves its ability to run on carbon‑free power every hour of the day.

The Future of Demand Response in AI and Cloud Operations

The demand response market is expected to grow as grids become more complex. Several trends support this outlook.

- Rising demand: U.S. data center growth will drive much of the new electricity use over the next decade. Digital services continue to push the load higher.

- Renewables growth: Wind and solar are cheap but variable, making flexible demand more important for grid stability.

- Grid limits: U.S. interconnection queues include thousands of gigawatts of projects, far more than the grid can handle quickly, causing delays.

Demand response can help manage these constraints. It acts as a “virtual power plant” by reducing demand instead of increasing supply. Studies suggest that flexible demand could unlock large amounts of additional grid capacity and reduce the need for costly transmission upgrades.

This makes demand response one of the fastest and most cost‑effective tools available for grid management.

A Cost-Effective Tool for Modern Grids

As electricity demand continues to grow, this energy model may become more common. Utilities, regulators, and companies are already exploring ways to expand demand‑side flexibility.

In the coming years, the success of these programs will depend on technology, policy support, and market design. However, the direction is clear. Flexible demand is becoming a core part of modern energy systems. Google’s latest move provides a real‑world example of how this transition can work at scale.

The post Google Turns Data Centers Into Grid Assets With 1 GW Flex Power Deal appeared first on Carbon Credits.

-

Climate Change7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?