New Rules: How to Implement and Communicate Climate Strategy for Companies

2023 was a big year for climate action. We saw major announcements of new global governance and regulations across the world:

- In the US, California passed SB-253 Climate Corporate Data Accountability Act and AB-1305 Voluntary carbon market disclosures.

- In Europe, the European Commission released its Proposal for a Directive on Green Claims.

- Globally, new rules for the quality and use of carbon credits were issued ICVCM (The Integrity Council for the Voluntary Carbon Market) and VCMI (The Voluntary Carbon Markets Integrity Initiative), both receiving significant praise from global leaders at the most recent COP28.

At Terrapass, we’re excited by these developments. The world recognizes the need to significantly scale all climate solutions including voluntary carbon markets. For this we must have globally aligned standards. This came together on multiple fronts in 2023.

So, what does this mean for sustainability professionals and everyday consumers?

For everyday consumers this is great news. These regulations ensure that any climate accomplishments promoted by a business will be supported with details that clearly show how those claims were achieved. The rules also ensure that companies are actively working to reduce their own carbon emissions in addition to offsetting their remaining emissions. Please visit Terrapass for more information about your personal or small business carbon footprint.

For sustainability professionals the list of new rules and regulations might seem daunting, but it is also good news. This is a sign of a maturing industry. Policy and consumer experts are contributing their expertise to help make climate action impactful and understandable to both sustainability professionals and everyday customers.

Historically, professional sustainability terms like carbon neutral and net-zero often made their way into marketing and product messaging. Consumer advocates rightly recognized that everyday customers can’t evaluate these phrases on their own. Additionally, vague phrases like green, eco, and sustainable are often used to promote sustainability without any supporting information. Consumer advocates also recognized that customers must be able to see why a product is green. These new regulations in California and Europe ensure that climate communications are always factual and transparent. They ensure that companies can promote their sustainability accomplishments with confidence and that customers have information to evaluate those accomplishments.

New global governance, VCMI in particular, ensures that companies apply sustainability solutions in the most effective way. Terrapass has long promoted the principle of 1. Calculate, 2. Conserve, and 3. Offset in our sustainability guidance to customers. This approach prioritizes:

- First, understand where carbon emissions are in your business,

- Second, disclose your plan to reduce the carbon emissions of your business and regularly report progress, and

- Third, balance your remaining emissions with carbon credits that fund global emission reduction projects.

When companies describe their climate strategy, they sometimes combine these different elements into one term like “carbon neutral.” Phrases like this do reflect an important environmental achievement. However, they hide the distinction between your company’s emission reductions vs. global emission reductions funded through carbon credits. Emission reduction and offsetting must be separate elements of your sustainability strategy and they should also be separate elements of your climate communications. Key elements for your climate communications include:

Steps and priorities:

- Measure your carbon emissions, reduce emissions on a science-based trajectory, and disclose your progress publicly.

- Address your remaining emissions by funding high-quality carbon credits that help reduce greenhouse gases globally.

Tell two different stories in your climate communications:

- Business Emission Reduction: Our carbon footprint was 5,000 mT in 2023, a reduction of 500 mT vs. 2021 and 5% ahead of plan.

- Global Climate Contribution: We purchased 5,000 mT of carbon credits in 2023 to fund global carbon reductions equal to our remaining emissions.

Other considerations:

- Climate communications should be factual, specific and detailed; provide evidence of all environmental claims made.

- Talk about carbon credits as a way to balance your remaining emissions by funding global carbon reduction.

- Talk about carbon credits as a way to support other global sustainability goals (UN SDGs) when applicable.

- Avoid using vague, generic terms like green, eco, climate friendly, sustainable, etc. that are not substantiated.

- Avoid terms that combine your company’s emission reduction and carbon offsetting into one phrase like carbon neutral, climate neutral, etc.

Highlights from each of the new rules and regulations are provided below. Please contact a Terrapass sustainability advisor to help your company navigate its specific needs.

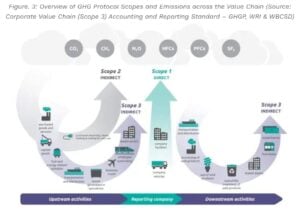

California SB-253 Climate Corporate Data Accountability Act

- For entities with total annual revenues in excess of $1,000,000,000 that do business in California:

- Starting in 2026: Report Scope 1 and Scope 2 greenhouse gas emissions

- Starting in 2027: Report Scope 3 greenhouse gas emissions

- Other requirements:

- For the reporting entity’s prior fiscal year

- Reporting is due annually on a date to be determined by the state board.

- Reporting follows the Greenhouse Gas Protocol

- Reporting entity must obtain an assurance engagement, performed by an independent third-party assurance provider, of the entity’s public disclosure as provided.

California AB-1305 Voluntary Carbon Market Disclosures

- Entities operating in California and making climate-related claims:

- Must publicly disclose information documenting how the claim was determined to be accurate or accomplished, and the measurement of interim progress.

- Applies to claims of net-zero emissions, carbon neutrality or similar, as well as claims of significant reductions in greenhouse gas (“GHG”) emissions,

- Entities operating in California and using voluntary carbon credits to support a climate-related claim.

- Must publicly disclose detailed information related to the credits purchased, the underlying offset projects and any independent verification of the climate-related claims made.

EU Green Claims Directive

- Applies to EU companies and non-EU companies making environmental claims aimed at EU consumers.

- Aims to eliminate greenwashing across EU markets by setting out detailed rules for how companies should market their environmental impacts and performance. It targets “vague, misleading or unfounded information on products’ environmental characteristics. “

- The current list of commercial practices that are banned in the EU is updated to include generic environmental claims – such as ‘environmentally friendly’, ‘natural’, ‘biodegradable’, ‘climate neutral’ or ‘eco’ – unless they can be properly evidenced.

- On the use of carbon credits specifically, the Green Claims Directive allows companies to make “carbon neutral” claims supported by carbon credits, but only if the carbon credits are disclosed correctly:

- Clearly state that carbon credits are being used to offset emissions.

- Disclose sources of emissions and amounts addressed with carbon credits.

- Identify carbon offset project types and distinguish between Reduction and removal offsets (requested, not required)

ICVCM (The Integrity Council for the Voluntary Carbon Market)

- New global quality standards for voluntary carbon credit projects; “regulatory-like”

- Program will be fully implemented over the course of 2023-2024.

- Rules for each carbon credit Category (Methodology/Project Type) were released in June 2023

- CCP-Eligible Programs (Registries) and CCP-Approved Categories (Project Types) will be announced in 2024.

- Not a one-time rule, standards will continuously evolve.

- First revision process for the CCPs in 2025, aimed at implementation starting in 2026.

- ICVCM points to VCMI for guidance on how businesses should use carbon credits.

VCMI (The Voluntary Carbon Markets Integrity Initiative)

- VCMI was established in 2021 to help ensure that voluntary carbon markets make a significant, measurable, and positive contribution to achieving the Paris Agreement goals.

- The VCMI Claims Code addresses market integrity on the demand side by guiding companies on:

- How they can credibly make voluntary use of carbon credits as part of their climate commitments, and

- The associated claims they can make regarding the use of those credits.

- The VCMI program should be followed together with ICVCM rules for high-integrity carbon credits.

Note: The above article provides introductory information only. Every organization must independently evaluate these rules and regulations, and determine specific actions needed for its own compliance.

Brought to you by terrapass.com

Images per Copyright free

Written By Sam Tellen

The post New Rules Tell Companies How to Implement and Communicate Climate Strategy appeared first on Terrapass.

Carbon Footprint

Verra to Launch Scope 3 Standard in 2026: A New Era for Value Chain Carbon Tracking

The post Verra to Launch Scope 3 Standard in 2026: A New Era for Value Chain Carbon Tracking appeared first on Carbon Credits.

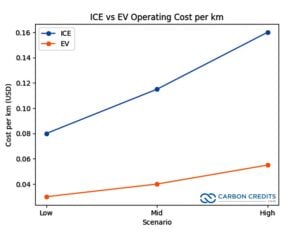

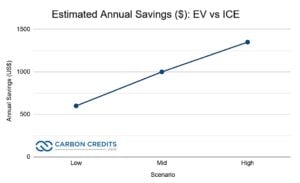

Rising global oil prices are driving up demand for electric vehicles (EVs), with Chinese brands emerging as key beneficiaries. Recent spikes in crude prices are driven by heightened tensions in the Middle East and disruptions in the Strait of Hormuz, a critical oil shipping route.

These factors have pushed Brent crude above $100 per barrel and created instability in fuel markets. This has pushed many consumers to rethink fuel costs and consider EV alternatives. Higher fuel prices increase running costs for gasoline and diesel cars, making EV ownership more economical in many markets.

Chinese EVs Gain Speed Abroad

Dealers in countries like Australia and parts of Southeast Asia see growing interest in Chinese EVs. This rise comes as fuel prices increase.

Showrooms selling Chinese new energy vehicles (NEVs) are seeing more test drives, customer inquiries, and rising order volumes. In Australia, the EV market share hit a record high of 11.8% for vehicle sales. Analysts say this jump is partly due to rising petrol prices.

Chinese manufacturers like BYD, GWM, and Chery are rapidly growing abroad. Some dealers see more walk-ins and more customers buying EVs.

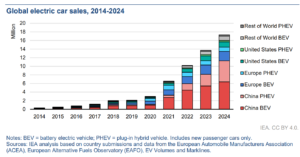

China’s EV industry is now the largest in the world. In 2024, Chinese automakers produced over 12.87 million plug‑in electric vehicles (PEVs), including battery electric (BEV) and plug‑in hybrid models, accounting for nearly 47.5% of total automobile production. That figure marked a strong year‑on‑year rise and underscored China’s industrial scale and export readiness.

By late 2025, more than 51% of all new vehicles sold in China were electric — a major shift from just a few years earlier.

This domestic scale provides an export advantage. Chinese EVs often cost less than similar European and North American models. This helps them succeed in markets where fuel costs hit household budgets hard.

Fuel Costs Drive Behavior Shift

Rising oil prices are a major driver of these sales trends. Global crude prices have fluctuated due to geopolitical tensions. The Strait of Hormuz route carries around 20% of the world’s oil trade. These disruptions pushed crude prices sharply higher in early 2026.

In many countries, higher retail fuel prices translate into more immediate cost pressures for consumers. Reports from countries like Australia show petrol prices over $2.50 per litre. This rise is making consumers think about EVs to lower long-term costs.

Global EV Market Trends and Forecasts

The surge in Chinese EV exports aligns with broader global trends. Major industry forecasts suggest that global sales of battery electric and plug-in hybrid vehicles may top 22 million units by 2025. This could represent about 25% of all new car sales worldwide.

Global electric vehicle sales in 2025 reached nearly 21 million units, including both battery electric vehicles and plug‑in hybrid electric vehicles. This total represents a significant increase, roughly 20 % more than in 2024.

China’s share in this global growth is large. In 2024, Chinese manufacturers made up around 70% of all EV exports. This shows China’s key role in supply chains and manufacturing.

As oil demand growth slows due to EV uptake, some forecasts suggest that EVs could displace millions of barrels of global oil demand each day in the coming decade. By 2030, EV adoption could cut about 5 million barrels per day of oil use, according to major energy outlooks.

Trade Barriers vs Expansion

Despite strong export gains, barriers remain. Some regions have imposed tariffs and trade restrictions on Chinese EVs, and infrastructure gaps in charging networks can slow adoption. For example, tariffs exceeding 100% on certain Chinese EV imports in the U.S. have limited market share there.

However, Chinese OEMs are developing supplier and shipping capacity to support overseas demand. In 2025, China’s electric car makers expanded shipping through roll‑on/roll‑off carriers capable of transporting more than 30,000 vehicles, improving export logistics.

Emerging markets in Southeast Asia, Latin America, and Oceania are also showing rising EV interest. In the Philippines and Vietnam, dealerships see EV orders growing quickly. Some are even doubling their weekly sales, thanks to high fuel costs.

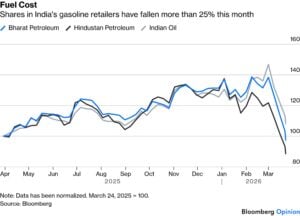

In India, where oil imports make up a big part of the economy, rising petrol costs make running traditional fuel vehicles more expensive. This has helped boost interest in electric vehicles, which are cheaper to operate when fuel is costly. Notably, the share of ICE retailers fell by over 25% in March.

Indian consumers and businesses view EVs as a way to shield against unstable oil prices. This also helps lower fuel costs, supporting the country’s move to electric transport.

What This Means for Energy and Transport Futures

The convergence of high oil prices and strong EV supply from China is creating a feedback loop. Higher fuel costs push consumers to consider EVs more seriously. Chinese manufacturers are well positioned to fill that demand with competitive pricing and large production scale.

The shift could speed up the move from fossil fuel cars to electric vehicles worldwide. This is especially true in price-sensitive and emerging markets. EV adoption also has implications for oil demand trends.

- As battery and charging tech get better and EV markets grow, oil use — especially in transport — might slow down or peak sooner than we thought.

At the same time, governments and industry groups are tracking these shifts closely. Policies that support charging infrastructure, EV incentives, and emissions standards will influence how quickly the global fleet electrifies.

Ultimately, the current oil price shock may have sparked a shift in global automotive markets — one where Chinese EVs take an increasingly central role in transport electrification worldwide.

The post Oil Shock Ignites Chinese EV Export Surge Around the World appeared first on Carbon Credits.

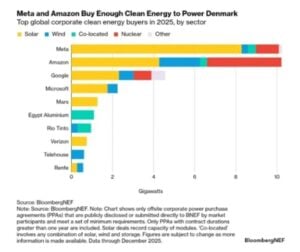

The U.S. is witnessing a surge in utility-scale solar development, driven by growing corporate demand for clean energy. Major tech companies like Meta and Google are securing long-term deals in Texas, combining renewable energy growth with economic and grid benefits.

This trend highlights how corporate commitments are shaping the future of the clean energy transition. Let’s find out.

Zelestra and Meta’s $600 Million Solar Deal

Madrid-based renewable energy firm Zelestra secured a massive $600 million green financing facility, signaling strong investor confidence in utility-scale solar. The funding, backed by Société Générale and HSBC, will support two large solar projects in Texas—Echols Grove (252 MW) and Cedar Range (187 MW).

These projects are not standalone efforts. Instead, they are part of a broader clean energy partnership with Meta, one of the world’s largest corporate renewable energy buyers. Together, they form a portion of a seven-project portfolio totaling 1.2 GW under long-term power purchase agreements (PPAs).

Sybil Milo Cioffi, Zelestra’s U.S. CFO, said:

“This financing marks a significant milestone in the delivery of our largest U.S. solar projects to date. It reflects strong confidence from Societe Generale and HSBC in our strategy and execution capabilities and reinforces our ability to attract first-class capital to support our growth platform in the U.S. market.”

Zelestra is strengthening its presence in the U.S. energy market with innovative solutions for hyperscalers and corporate clients. It is developing around 15 GW of renewable projects across key markets. In February 2026, BloombergNEF ranked Zelestra among the top 10 PPA sellers to U.S. corporations.

Solar Powering Meta’s Climate Strategy

Meta continues to aggressively expand its clean energy footprint. The company has made renewable energy procurement a core part of its climate roadmap—and the numbers clearly reflect that shift.

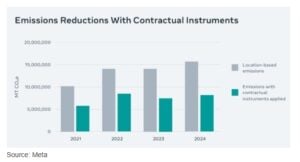

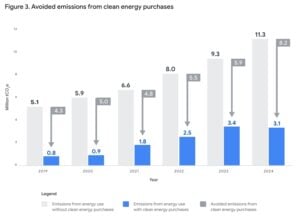

In 2024, Meta reported emissions of 8.2 million metric tonnes of CO₂e after accounting for clean energy contracts. In comparison, its location-based emissions stood at 15.6 million tonnes. This marked a sharp 48% reduction, largely driven by renewable energy purchases.

Moreover, the company has consistently maintained momentum:

- Since 2020, it has matched 100% of its electricity consumption with renewable energy.

- Over the past decade, it has secured more than 15 GW of clean energy globally.

- Overall, renewable energy procurement has helped cut 23.8 million MT CO₂e emissions since 2021.

As a result, Meta cut operational emissions by around 6 million tonnes in 2024 alone. At the same time, it tackled value chain emissions using Energy Attribute Certificates (EACs), reducing Scope 3 emissions by another 1.4 million tonnes.

Most of these deals were concentrated in the U.S., highlighting the country’s growing importance in corporate decarbonization strategies.

Importantly, this collaboration goes beyond just energy supply. It also aims to deliver broader economic benefits, including:

- Local job creation during construction

- Long-term tax revenue for the region

- Continued investment in local infrastructure

David Lillefloren, CEO at Sunraycer, said:

“These agreements with Google represent a significant milestone for Sunraycer and underscore the strength of our development platform. We are proud to support Google’s clean energy objectives while delivering high-quality renewable infrastructure in Texas.”

Additionally, the deal was facilitated through LevelTen Energy’s LEAP process, which simplifies and speeds up PPA execution. This highlights how innovative platforms are now playing a key role in scaling renewable deployment.

“Google’s data centers are long-term investments in the communities we call home,” said Will Conkling, Director of Energy and Power, Google. “This collaboration with Sunraycer will fuel local economic growth while helping to build a more robust and affordable energy future for Texas.”

Google, like Meta, has built a strong clean energy portfolio over time. Since 2010, it has signed over 170 agreements totaling more than 22 GW of capacity worldwide. Its long-term ambition is even more ambitious—achieving 100% carbon-free energy, every hour of every day, by 2030.

Why Texas Is Becoming the Center of Energy Transformation

All these developments point to one clear trend—Texas is rapidly becoming a global hub for clean energy and data center growth.

On one hand, the state offers strong solar resources, vast land availability, and a deregulated power market. On the other hand, it is witnessing a surge in electricity demand, especially from data centers and AI-driven workloads.

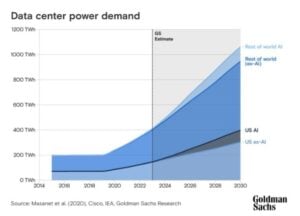

According to projections from the EIA, U.S. electricity demand could rise by 20% or more by 2030. Data centers are expected to play a major role in this growth. In fact, energy consumption from data centers increased by over 20% between 2020 and 2025.

As a result, energy infrastructure in Texas is facing growing pressure. Rising industrial activity, extreme weather events, and rapid digital expansion are all contributing to grid stress. Yet, at the same time, this demand is driving unprecedented investment in renewable energy.

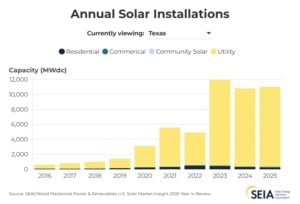

The EIA expects Texas to lead solar expansion in the coming years, accounting for nearly 40% of new solar capacity in the U.S. California will follow closely, and together, the two states will drive almost half of total additions.

Even though the sector has faced temporary slowdowns, the long-term outlook for U.S. solar remains highly positive.

In 2025, the U.S. added 53 GW of new electricity capacity—the highest annual addition since 2002. Notably, wind and utility-scale solar together generated 17% of the country’s electricity, a massive jump from less than 1% two decades ago.

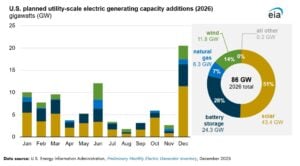

Looking ahead, growth is expected to accelerate again. Developers are planning to add around 86 GW of new capacity in 2026, which could set a new record. Solar alone is projected to account for more than half of this expansion.

Breaking it down further:

- Solar is expected to contribute 51% of new capacity

- Battery storage will make up 28%

- Wind will account for 14%

Utility-scale solar capacity additions could reach 43.4 GW in 2026, marking a 60% increase compared to 2025 levels.

Analysis: Corporate Demand Is Reshaping Energy Markets

Overall, the developments from Zelestra, Meta, Google, and Sunraycer highlight a broader transformation underway in global energy markets.

First, corporate buyers are no longer passive participants. Instead, they are actively shaping energy infrastructure through long-term PPAs. These agreements provide stable revenue for developers while ensuring a clean power supply for companies.

Second, financing is becoming more accessible. Large-scale funding deals, like Zelestra’s $600 million facility, show that banks are increasingly willing to back renewable projects with strong contractual support.

Third, regions like Texas are emerging as strategic energy hubs. The combination of rising electricity demand and favorable renewable conditions is attracting both developers and corporate buyers.

However, challenges remain. Grid reliability, permitting delays, and policy uncertainty could still impact the pace of deployment. Even so, the overall trajectory remains clear.

Clean energy demand is rising fast. Big Tech is leading the charge. And solar power is set to play a central role in meeting future electricity needs.

- READ MORE: Meta, Amazon, Google, and Microsoft Dominate Clean Energy Deals as Global Buying Slips in 2025

The post Texas Solar Market Heats Up with Meta and Google Investments appeared first on Carbon Credits.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?