Japan is preparing to invest about US$1.3 billion to encourage companies to use clean electricity. This funding will support industries and regions that switch to decarbonized power.

The plan will run over five years, starting in fiscal 2026. It is part of Japan’s broader strategy to reduce reliance on fossil fuels and expand clean energy. This step also aims to help local economies and strengthen long-term investment confidence in clean power.

Where the Funding Will Go

The government will give subsidies to companies that commit to using clean power. Eligible companies must use 100% decarbonized electricity and support regional development. The subsidies can cover as much as 50% of the capital costs. This includes costs for equipment and infrastructure needed to shift from fossil fuels to clean electricity.

Data centers and manufacturing firms are expected to benefit. This policy aims to lower financial barriers for businesses that want to purchase clean power. It also seeks to make these investments more appealing.

Inside Japan’s Green Transformation Strategy

This funding program fits into Japan’s Green Transformation (GX) 2040 Vision. The GX vision aims to connect climate goals with economic growth. Under this strategy, the government and regional partners will create clusters of industry powered by clean electricity.

The clusters will receive financial support and tailored regulatory policies. The goal is to spur innovation and local job creation while reducing carbon emissions. The country is the fifth-largest emitter worldwide.

- Japan also plans to increase the role of nuclear power. Officials aim for nuclear energy to contribute around 20% of electricity by 2040.

SEE MORE: Japan to Restart the World’s Largest Nuclear Power Plant

Meanwhile, the share of renewables is targeted to reach around 40–50%, up from about 26–27% in recent years. These shifts aim to reduce reliance on imported fossil fuels and meet national climate goals.

Pro-growth Carbon Pricing Concept

Japan’s Power Mix: Where Clean Energy Stands Today

Japan’s electricity mix still includes a significant share of fossil fuels. In 2024, renewable sources accounted for about 26.7% of total power generation, up from 25.7% in 2023.

Solar energy made up about 11.4% of electricity, and wind power contributed around 1.1%. Biomass and hydro added smaller shares. Nuclear power contributed roughly 8–9% of electricity in recent years. These changes show gradual growth in clean sources, but Japan still faces work to meet the longer-term goals of major clean energy adoption.

Increasing clean power demand from large corporate users is intended to support faster growth in renewable generation and encourage private and public investment.

Clean Energy Market Trends Shaping Japan’s Power Future

The clean energy market in Japan is growing and showing clear trends. These trends help explain why the new subsidy program matters.

First, Japan’s renewable energy market is expanding steadily. As of 2024, Japan’s renewable energy generation was approximately 247.2 terawatt hours (TWh). Analysts predict this could reach around 355–356 TWh by 2033 or 2034. It may grow at an annual rate of 3.7% to 3.9% until the decade ends.

This trend reflects ongoing investment in renewable capacity from solar, wind, hydro, and biomass.

- In 2025, the renewable energy market is projected to reach around 244.98–256.9 TWh of electricity generation.

- By 2033–2034, the market is forecast to reach approximately 355–356 TWh.

- This implies consistent annual growth of roughly 3.7–3.9% from 2025 into the early 2030s.

Solar energy remains the largest segment of renewables in Japan. It has already surpassed hydroelectric power in terms of generation share. Japan ranks among the top solar power generators in the world, and its solar capacity per unit of land is among the highest for major economies.

The government’s strategic plans predict that solar energy may reach 23% to 29% of the country’s electricity mix by 2040. This would make it the largest renewable source. This would make solar the dominant clean power source in the coming decades.

Wind energy is also on a growth path, though its current share is smaller than solar. Japan’s total wind energy production is expected to reach around 8.92 billion kilowatt hours (kWh) in 2025. It will likely grow at a rate of about 3.3% each year until 2029. These figures indicate a steady rise in wind power capacity and generation, reflecting government support for offshore and onshore wind projects.

Overall, these forecasts show that a cleaner electricity system is emerging in Japan. Renewable generation is rising, and market forecasts show continued expansion through the early 2030s.

Companies and investors are responding to policy incentives, technology improvements, and climate commitments. As demand grows, clean energy production and investment are expected to follow.

Why Clean Power Demand Is the Missing Piece

Clean power demand is a key factor in Japan’s energy transition. Many nations focus first on increasing the clean power supply.

Japan’s new policy adds a demand-side focus. By helping businesses shift to decarbonized electricity, the government hopes to create stable, long-term demand. This, in turn, should encourage utilities and energy producers to build more renewable capacity and invest in grid improvements.

Large corporate users such as data centers, manufacturers, and tech firms can shape electricity markets. If more companies commit to using clean power, utilities can plan new projects with greater certainty. This can lead to lower costs for renewable generation in the long run and faster deployment of new clean energy technologies.

Barriers Japan Still Faces in the Energy Shift

Despite progress, Japan still faces challenges in its clean energy transition. Japan’s heavy reliance on fossil fuel imports has defined its energy landscape for decades. Although the share of fossil fuels in electricity has declined, they still provide a significant portion of Japan’s energy mix.

Japan’s nuclear sector plays a role as well. After the 2011 Fukushima disaster, most nuclear reactors were shut down for safety reasons. In recent years, some reactors have restarted, and the government plans to increase nuclear contribution as part of the energy strategy. However, delays and regulatory challenges remain.

Supply-side challenges also affect renewables. Offshore wind projects can face high costs and long development timelines. Large solar projects sometimes meet local opposition. In this context, encouraging demand growth can help support broader investment and confidence in clean energy expansion.

Expected Economic and Climate Payoff of the New Subsidies

Japan’s new subsidy program is expected to:

- Reduce costs for companies shifting to clean power.

- Boost regional investment around renewable energy hubs.

- Strengthen business confidence in clean energy markets.

- Support job creation in new energy sectors.

- Help reduce greenhouse gas emissions over time.

The government aims to begin accepting applications from companies in 2026. This initiative reflects Japan’s broader effort to align economic growth with climate goals and to support a cleaner, more resilient power system for the future.

The post Japan to Invest US$1.34B on Clean Power to Spur Energy Transition appeared first on Carbon Credits.

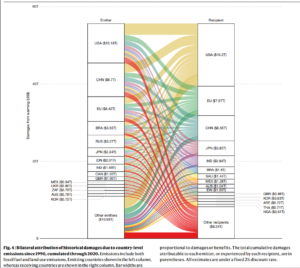

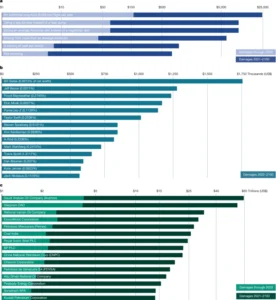

Climate change is not only a physical threat, but it also affects the world’s economy. A major new study published in the journal Nature on March 25, 2026, puts a clear number on this impact. It finds that carbon dioxide (CO₂) emissions from the United States caused about $10.2 trillion in total economic damage worldwide between 1990 and 2020. This makes the U.S. the largest single contributor to climate-related economic loss over that period.

The study shows that emissions slow economic growth in many countries. Rising temperatures cut productivity, lower output, and hurt long-term economic performance around the globe.

Marshall Burke, the lead author of the study, remarked:

“If you warm people up a little bit, we see very clear historical evidence, you grow a little bit less quickly. If you accumulate those effects over 30 years, you just get a really large change by the end of 30 years. It’s like death by a thousand cuts. And you have people being harmed who did not cause the problem, and that feels just fundamentally unfair.”

The researchers focused on carbon dioxide, the most common greenhouse gas. They used data on how temperature affects economic activity and then linked that to how much CO₂ different countries have emitted since 1990. This method links climate science to real economic results, including slower growth, lower productivity, and smaller national outputs.

Counting the Dollars: $10 Trillion in U.S.-Linked Damage

One of the study’s central findings is striking. From 1990 to 2020, U.S. emissions likely caused around $10.2 trillion in global economic damage. This means that warming linked to U.S. emissions has reduced economic production across many countries. The study links these impacts to heat’s long-term effects on labor, agriculture, and overall economic growth.

The damage is not confined to other nations. Roughly 30% of that $10.2 trillion figure is estimated to have occurred within the United States itself. In other words, U.S. emissions have slowed economic growth at home as well as abroad. The remaining impacts are spread across the global economy.

The researchers found that U.S. emissions led to about $500 billion in damage in India and around $330 billion in Brazil during that time. These figures show how carbon released in one area can affect economies far away.

A New Framework for Loss and Damage

The Nature study introduces a new framework for assessing what scientists call “loss and damage.” This term refers to harms that cannot be prevented by reducing emissions or avoided through adaptation alone.

The study uses economic data and climate models. It tracks how temperature changes over the years impact economic output.

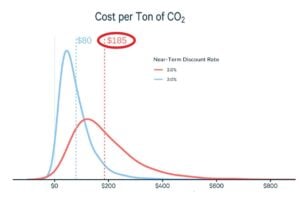

- To put the numbers into context: one tonne of CO₂ emitted in 1990 is estimated to have caused about $180 in global economic damages by 2020.

But that same tonne is projected to cause an additional $1,840 of cumulative damage by 2100, as warming continues and its effects compound over time. This highlights that past emissions still contribute to future economic harm.

The researchers highlight that these estimates focus on economic output, like goods and services. They do not account for all types of climate damage. They do not include costs from loss of life, health impacts, biodiversity collapse, cultural heritage losses, or many kinds of infrastructure damage. These excluded impacts could raise the true total cost of climate change even further.

The Social Cost of Carbon Revisited

This study is part of a broader scientific effort to understand the economic impacts of climate change. Climate and economic models show that rising temperatures are already slowing economic growth. If emissions stay high, this slowdown will get worse in the future.

Analyses by major international institutions and research groups project that climate change could reduce global GDP by a significant percentage by mid-century. This is compared to scenarios with strong mitigation, though exact figures vary by method.

The concept of estimating a “social cost of carbon” (SCC) — a monetary estimate of economic damage per tonne of CO₂ — has been used in policy analysis for years. It helps governments weigh trade-offs in climate policy. For example, they can decide how much to invest in emissions cuts versus adaptation.

However, traditional SCC estimates have been debated. They depend on assumptions about future growth, discount rates, and climate sensitivity. The Nature study advances this approach by tying economic outcomes directly to observed climate impacts.

Economists and climate scientists agree that warming impacts several areas. These include agricultural yields, labor productivity, energy demand, and health outcomes. These effects reduce economic output and increase costs for businesses and governments. The latest research makes these links more explicit by assigning dollar values to the historical impacts of emissions.

Equity and Global Responsibility

The research’s results also highlight important equity questions. Low-income countries often face bigger economic impacts compared to their emissions histories.

For example, nations with warmer climates and more fragile infrastructure may experience greater output losses due to temperature increases. These effects grow over time and can worsen existing development challenges.

At the same time, richer countries with higher historical emissions may take a larger share of responsibility for damage. The Nature study shows it is possible to calculate responsibility in monetary terms. However, turning those numbers into legal or financial obligations is still complex.

Tail Risks and Future Costs

The researchers also point toward the future. It finds that future damages from past emissions are much larger than the losses already accrued.

Since CO₂ remains in the atmosphere for centuries, its warming effects — and the economic damages linked to them — will persist well beyond 2020. This “tail risk” means that the total cost of historical emissions could rise sharply over the rest of this century.

Climate risk is increasingly integrated into economic planning and finance. Governments, businesses, and international institutions are incorporating climate scenarios into investment decisions and risk models.

This includes assessing how rising temperatures may affect infrastructure costs, insurance markets, supply chains, and national budgets. Without strong mitigation and adaptation measures, these economic pressures are expected to grow.

A Shared Reality, Quantified

The Nature study offers a clear and data-based way to think about the economic harms of climate change. Emissions from the United States since 1990 have caused over $10 trillion in global economic damage. This includes harm in the U.S., India, and Brazil.

These findings do not assign legal liability. However, they provide a meaningful picture of how climate change affects the global economy in terms of the social costs of carbon. They show that the costs of climate impacts are measurable and significant.

As the world continues to adapt and respond to climate change, understanding these economic links will be crucial for policymakers, businesses, and communities.

The post $10 Trillion in Carbon Cost? How U.S. Emissions Hit the Global Economy appeared first on Carbon Credits.

Carbon Footprint

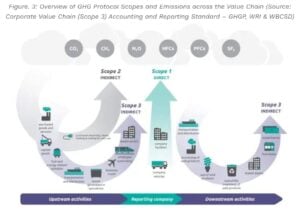

Verra to Launch Scope 3 Standard in 2026: A New Era for Value Chain Carbon Tracking

The post Verra to Launch Scope 3 Standard in 2026: A New Era for Value Chain Carbon Tracking appeared first on Carbon Credits.

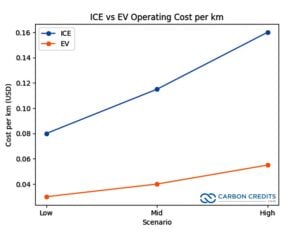

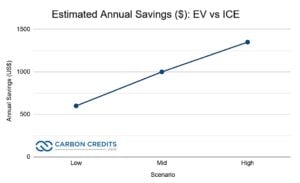

Rising global oil prices are driving up demand for electric vehicles (EVs), with Chinese brands emerging as key beneficiaries. Recent spikes in crude prices are driven by heightened tensions in the Middle East and disruptions in the Strait of Hormuz, a critical oil shipping route.

These factors have pushed Brent crude above $100 per barrel and created instability in fuel markets. This has pushed many consumers to rethink fuel costs and consider EV alternatives. Higher fuel prices increase running costs for gasoline and diesel cars, making EV ownership more economical in many markets.

Chinese EVs Gain Speed Abroad

Dealers in countries like Australia and parts of Southeast Asia see growing interest in Chinese EVs. This rise comes as fuel prices increase.

Showrooms selling Chinese new energy vehicles (NEVs) are seeing more test drives, customer inquiries, and rising order volumes. In Australia, the EV market share hit a record high of 11.8% for vehicle sales. Analysts say this jump is partly due to rising petrol prices.

Chinese manufacturers like BYD, GWM, and Chery are rapidly growing abroad. Some dealers see more walk-ins and more customers buying EVs.

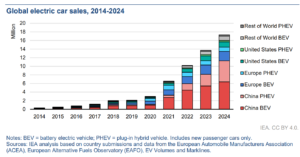

China’s EV industry is now the largest in the world. In 2024, Chinese automakers produced over 12.87 million plug‑in electric vehicles (PEVs), including battery electric (BEV) and plug‑in hybrid models, accounting for nearly 47.5% of total automobile production. That figure marked a strong year‑on‑year rise and underscored China’s industrial scale and export readiness.

By late 2025, more than 51% of all new vehicles sold in China were electric — a major shift from just a few years earlier.

This domestic scale provides an export advantage. Chinese EVs often cost less than similar European and North American models. This helps them succeed in markets where fuel costs hit household budgets hard.

Fuel Costs Drive Behavior Shift

Rising oil prices are a major driver of these sales trends. Global crude prices have fluctuated due to geopolitical tensions. The Strait of Hormuz route carries around 20% of the world’s oil trade. These disruptions pushed crude prices sharply higher in early 2026.

In many countries, higher retail fuel prices translate into more immediate cost pressures for consumers. Reports from countries like Australia show petrol prices over $2.50 per litre. This rise is making consumers think about EVs to lower long-term costs.

Global EV Market Trends and Forecasts

The surge in Chinese EV exports aligns with broader global trends. Major industry forecasts suggest that global sales of battery electric and plug-in hybrid vehicles may top 22 million units by 2025. This could represent about 25% of all new car sales worldwide.

Global electric vehicle sales in 2025 reached nearly 21 million units, including both battery electric vehicles and plug‑in hybrid electric vehicles. This total represents a significant increase, roughly 20 % more than in 2024.

China’s share in this global growth is large. In 2024, Chinese manufacturers made up around 70% of all EV exports. This shows China’s key role in supply chains and manufacturing.

As oil demand growth slows due to EV uptake, some forecasts suggest that EVs could displace millions of barrels of global oil demand each day in the coming decade. By 2030, EV adoption could cut about 5 million barrels per day of oil use, according to major energy outlooks.

Trade Barriers vs Expansion

Despite strong export gains, barriers remain. Some regions have imposed tariffs and trade restrictions on Chinese EVs, and infrastructure gaps in charging networks can slow adoption. For example, tariffs exceeding 100% on certain Chinese EV imports in the U.S. have limited market share there.

However, Chinese OEMs are developing supplier and shipping capacity to support overseas demand. In 2025, China’s electric car makers expanded shipping through roll‑on/roll‑off carriers capable of transporting more than 30,000 vehicles, improving export logistics.

Emerging markets in Southeast Asia, Latin America, and Oceania are also showing rising EV interest. In the Philippines and Vietnam, dealerships see EV orders growing quickly. Some are even doubling their weekly sales, thanks to high fuel costs.

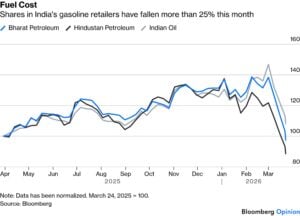

In India, where oil imports make up a big part of the economy, rising petrol costs make running traditional fuel vehicles more expensive. This has helped boost interest in electric vehicles, which are cheaper to operate when fuel is costly. Notably, the share of ICE retailers fell by over 25% in March.

Indian consumers and businesses view EVs as a way to shield against unstable oil prices. This also helps lower fuel costs, supporting the country’s move to electric transport.

What This Means for Energy and Transport Futures

The convergence of high oil prices and strong EV supply from China is creating a feedback loop. Higher fuel costs push consumers to consider EVs more seriously. Chinese manufacturers are well positioned to fill that demand with competitive pricing and large production scale.

The shift could speed up the move from fossil fuel cars to electric vehicles worldwide. This is especially true in price-sensitive and emerging markets. EV adoption also has implications for oil demand trends.

- As battery and charging tech get better and EV markets grow, oil use — especially in transport — might slow down or peak sooner than we thought.

At the same time, governments and industry groups are tracking these shifts closely. Policies that support charging infrastructure, EV incentives, and emissions standards will influence how quickly the global fleet electrifies.

Ultimately, the current oil price shock may have sparked a shift in global automotive markets — one where Chinese EVs take an increasingly central role in transport electrification worldwide.

The post Oil Shock Ignites Chinese EV Export Surge Around the World appeared first on Carbon Credits.

$10 Trillion in Carbon Cost? How U.S. Emissions Hit the Global Economy

Sustainability In Your Ear: Schneider Electric’s Steve Wilhite Maps the Renewable Energy Transition

The West Is Burning Before Summer Even Starts, and It’s No Accident

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits