More than 230 environmental and public-interest groups asked Congress to halt approvals for and construction of new data centers. They want a temporary national moratorium until federal rules address energy use, water needs, local impacts, and emissions. The request came from Food & Water Watch and was signed by national and local groups across the country.

They said that the fast growth of artificial intelligence (AI) and cloud services is putting big new demands on local grids and water systems. They also said current federal rules do not cover the environmental or social impacts linked to data center growth.

Why the Groups Want a Moratorium

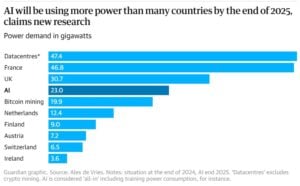

Data centers are using more electricity each year. U.S. data centers consumed an estimated 183 terawatt-hours (TWh) of electricity in 2024. That was about 4% of all U.S. power use. Some national studies project that number could rise to 426 TWh by 2030, which would be about 6.7% to 12% of U.S. electricity, depending on growth rates.

Global data centers used around 415 TWh of electricity in 2024. Analysts expect double-digit annual growth as AI loads increase.

AI-ready data center capacity is projected to grow by about 33% per year from 2023 to 2030 in mid-range market scenarios. Industry groups say global data center capacity could reach over 220 gigawatts (GW) by 2030.

Some groups warn that data center CO₂ emissions might hit 1% of global emissions by 2030. That’s about the same as a mid-size industrial country’s yearly emissions. They say the growth rate is rising faster than the reductions in many other sectors.

An excerpt from their letter reads:

“The rapid expansion of data centers across the United States, driven by the generative artificial intelligence (AI) and crypto boom, presents one of the biggest environmental and social threats of our generation. This expansion is rapidly increasing demand for energy, driving more fossil fuel pollution, straining water resources, and raising electricity prices across the country. All this compounds the significant and concerning impacts AI is having on society, including lost jobs, social instability, and economic concentration.”

When AI Growth Collides With the U.S. Power Grid

Several utilities have linked new power plant plans to data center growth. In Virginia, the largest power company and grid planners see data centers as a key reason for new infrastructure.

In Louisiana, Entergy moved forward with a new gas-plant plan expected to support a large hyperscale data center campus. These cases show how utilities now size new plants with AI-related load in mind.

Some utilities believe these expansions might increase local electricity rates by a few percentage points. This depends on how costs are shared. Regulators in various areas say that extra load can increase distribution and transmission costs. This might lead to higher bills for households.

Several grid operators also report congestion or long waiting lines for new power connections. Northern Virginia, Texas, and parts of the Pacific Northwest now have interconnection queues. In these areas, data center projects make up a large part of the pending requests.

Water Use and Siting Concerns

Water demand is another point of conflict. Many large data centers rely on water-cooled systems. A typical water-cooled data center may use around 1.9 liters of water per kWh. More advanced or dry-cooled facilities may use as little as 0.2 liters per kWh, but these designs are not yet common.

One medium-sized data center can use about 110 million gallons of water per year. Large hyperscale sites can use several hundred million gallons annually, and, in some cases, even more. Global estimates suggest data centers could use over 1 trillion liters of water per year by 2030 if growth continues.

These demands have triggered local resistance. In parts of Arizona, California, and Georgia, community groups have raised concerns about water use during drought periods. In some cases, local governments paused or limited data center approvals. A single campus can use more water each year than some small towns.

Trump Plans Executive Order on AI Regulation

While groups push for limits on new data centers, the White House is also preparing an executive order that would reshape AI policy nationwide, as reported by CNN. President Donald Trump has said he plans to issue an order that would block states from creating their own AI rules.

The administration aims to create one national standard for AI. This way, companies won’t have to deal with different state regulations.

Drafts of the plan say the order may tell federal agencies to challenge state AI laws. This could happen through lawsuits or funding limits if the laws clash with federal policy. Supporters say a unified national rule could help U.S. companies compete globally and reduce compliance costs.

State leaders and consumer protection groups argue the opposite. They say states have a legal right to pass their own rules on privacy, safety, and data use. Some governors argue that an executive order cannot override state laws without action by Congress. Minnesota lawmakers, for example, continue to write their own AI bills focused on deepfakes and child-safety concerns.

The debate adds another layer to the data center issue. AI systems require massive computing power. If AI keeps growing quickly, analysts expect even heavier pressure on local grids and water systems. Advocacy groups say that this makes federal regulation more urgent.

Scale of AI and Hyperscale Build-out

The U.S. is in the middle of a major build-out of hyperscale and AI-optimized data centers. Industry trackers report that hundreds of new hyperscale facilities are planned or already under construction through 2030. Many of these campuses are designed specifically for AI training and inference workloads.

Major cloud and social media companies have sharply increased capital spending to support this build-out. Amazon, Google, Microsoft, Meta, and other major platforms, combined spending on AI chips, data centers, and network upgrades reached hundreds of billions of dollars per year in the mid-2020s. These spending levels signal how fast demand is growing.

Some experts track how major technology firms have changed over time. For example, one big cloud provider said its data center electricity use has more than doubled in the last ten years. This increase happened as its global reach grew. This gives a sense of how long-term trends feed current infrastructure pressures.

AI also adds new layers of demand. Training one large AI model can use millions of kilowatt-hours of electricity. Operating a popular chatbot can require many megawatt-hours per day, especially at peak traffic.

Research shows that processing one billion AI queries uses as much electricity as powering tens of thousands of U.S. homes for a day. This varies with the model’s size and efficiency.

Cities and States Move Faster Than Washington

Local governments have acted faster than federal agencies to respond to public concerns. More than 100 counties and cities have passed temporary moratoria, zoning limits, or new environmental rules since 2023. Examples include parts of Georgia, Oregon, Arizona, and Virginia, where communities plan to evaluate energy and water impacts before approving new projects.

Advocacy groups also argue that federal standards have not kept up. The U.S. does not have national energy-efficiency rules for private data centers. It also does not require detailed, mandatory reporting on energy, water, or emissions for the sector. The groups pushing for a moratorium say Congress must update these policies before more sites break ground.

What the Debate Means for 2026 and Beyond

Congress will review the environmental groups’ request in the coming months. Lawmakers are expected to weigh economic benefits against rising tensions around energy, water, and local resources. At the same time, the White House may release its AI executive order, which could shape how states and companies set their own rules.

With rapid AI growth, rising electricity use, and expanding data center construction, both debates are likely to continue through 2026. Many experts say long-term solutions will require national standards, better reporting, and closer coordination between states, utilities, and federal agencies.

The post Environmental Groups Urge U.S. Congress to Pause Data Center Growth as Federal AI Rule Looms appeared first on Carbon Credits.

Nasdaq has backed one of the first carbon removal credit deals licensed under European Union rules. The project is based in Stockholm and is designed to generate high-quality carbon removal credits under a formal EU framework.

This marks a key shift. For years, carbon markets have relied on voluntary standards with mixed credibility. Now, the European Union has developed a regulated system to define what counts as a valid carbon removal. This move aims to build trust and attract large investors into a market that is still in its early stages.

The deal shows growing interest from major companies. It also reflects rising demand for reliable ways to remove carbon from the atmosphere.

Inside the Stockholm Carbon Removal Project

The removal project is run by Stockholm Exergi. It uses a process called BECCS, or bioenergy with carbon capture and storage. This method burns biomass, such as wood waste and agricultural residues, to produce heat and electricity. At the same time, it captures the carbon dioxide released and stores it underground.

The captured CO₂ will be transported and stored deep beneath the North Sea in rock formations. Over time, it will turn into solid minerals. This makes the carbon removal long-lasting and more secure than many nature-based solutions.

The facility is expected to start operating in 2028. Once active, it will generate carbon removal credits that companies can buy to balance their remaining emissions.

Beccs Stockholm is one of the world’s largest carbon removal projects. In its first ten years, the project could remove about 7.83 million tonnes of CO₂ equivalent. This makes it a key tool for helping the European Union reach climate neutrality by 2050.

The project also aims to scale carbon removal by building a full CCS value chain in Northern Europe and supporting a growing market for negative emissions credits.

This project is important because it is one of the first to follow the EU’s new carbon removal certification rules. These rules define how carbon removal should be measured, verified, and reported. They also aim to reduce risks like double-counting and weak accounting.

EU Certification: Building Trust in a Fragile Market

The European Commission has introduced a framework, also called Carbon Removals and Carbon Farming (CRCF) Regulation, to certify carbon removal activities. This includes technologies like BECCS, direct air capture with carbon storage, and biochar.

The goal is to create a trusted system that investors and companies can rely on. It also established the first EU-wide certification framework for carbon farming and carbon storage in products, not just removals.

Until now, the voluntary carbon market (VCM) has faced criticism. Concerns about transparency and “greenwashing” have made some companies cautious. Many buyers want stronger proof that credits represent real and permanent carbon removal.

The EU framework tries to solve this problem. It sets clear rules for:

- Measuring how much carbon is removed.

- Verifying results through independent checks.

- Ensuring long-term storage of CO₂.

This structure may help standardize the market. It could also make carbon removal credits easier to compare and trade across borders. The Commission states that the goal of having the framework is:

“to build trust in carbon removals and carbon farming while creating a competitive, sustainable, and circular economy.”

Corporate Demand Is Growing—but Still Limited

Large companies are starting to invest in carbon removal. However, the market remains small compared to what is needed.

One major buyer is Microsoft. It currently holds about 35% of all global carbon removal credits, making it a dominant player in the market. In fact, it is responsible for 92% of purchased removal credits in the first half of 2025.

Other companies, including Adyen, a Dutch payments provider, have also joined the Stockholm project. These early buyers aim to secure a future supply of high-quality carbon credits as demand grows.

Ella Douglas, Adyen’s global sustainability lead, said in an interview with the Wall Street Journal:

“This project does exactly that [“catalytic impact” to the VMC] while also building key market infrastructure in collaboration with the European Commission.”

Still, many firms remain cautious. Carbon removal technologies are often expensive and not yet proven at a large scale. Some companies also worry about reputational risks if projects fail to deliver real climate benefits.

This creates a gap. Demand is rising, but the supply of trusted credits is still limited.

- SEE event: Carbon Removal Investment Summit 2026

A Market Set for Rapid Growth

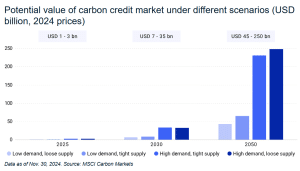

Despite these challenges, the long-term outlook for carbon removal is strong. Estimates suggest the market could reach $250 billion by mid-century, according to MSCI Carbon Markets.

Several factors drive this growth:

- First, global climate targets require large-scale carbon removal. The Intergovernmental Panel on Climate Change estimates that the world may need to remove around 10 billion metric tons of CO₂ per year by 2050 to limit warming.

- Second, many companies have set net-zero goals. These targets often include removing emissions that cannot be avoided, especially in sectors like aviation, shipping, and heavy industry.

- Third, new regulations are pushing companies to disclose and manage emissions more clearly. This increases demand for credible carbon solutions.

However, the current supply falls far short of what is needed. Only a small share of the required carbon removal credits has been developed or sold so far.

Balancing Removal and Emissions Cuts

While carbon removal is gaining attention, experts stress that it cannot replace emissions reductions. Removing carbon from the atmosphere is often more expensive and complex than avoiding emissions in the first place.

Groups like the European Environmental Bureau warn that over-reliance on credits could delay real climate action. They argue that companies should set separate targets for reducing emissions and for removing carbon.

The EU framework reflects this concern. It treats carbon removal as a tool for addressing residual emissions, not as a substitute for cutting pollution at the source. This distinction is important. It helps ensure that carbon markets support, rather than weaken, overall climate goals.

From Concept to Market Infrastructure

The Stockholm project marks a turning point for carbon removal. It shows how rules, strong verification, and corporate backing can bring structure to a fragmented market.

With support from players like Nasdaq, carbon removal is moving closer to becoming a mainstream financial asset. At the same time, the European Union’s certification system is setting the foundation for a more credible and scalable market.

The path ahead remains complex. Technologies must scale. Costs must fall. Trust must grow. But the direction is clear.

Carbon removal is no longer a niche idea. It is becoming a key part of the global climate economy, with the potential to shape investment flows for decades to come.

The post Nasdaq Invests in First EU-Certified Carbon Removal Credits from Stockholm Exergi appeared first on Carbon Credits.

The nuclear energy industry is entering a new phase of transformation. This shift is no longer just about building reactors—it is about building them faster, smarter, and more efficiently.

A recent breakthrough led by the U.S. Department of Energy (DOE), in collaboration with Idaho National Laboratory, Argonne National Laboratory, Microsoft, NVIDIA, Everstar, and Aalo Atomics, highlights that AI tools can streamline the nuclear regulatory process.

AI and DOE’s Genesis Mission: Breaking Bottlenecks in Nuclear Energy Deployment

The work supports President Trump’s Genesis Mission, a national initiative aimed at driving a new era of AI-accelerated innovation and discovery. The mission focuses on using advanced technologies like AI to solve critical national challenges, from energy to healthcare and beyond.

Under the Genesis Mission, DOE recently announced $293 million in competitive funding to tackle twenty-six pressing science and technology challenges, including one dedicated to speeding up nuclear energy deployment.

Rian Bahran, Deputy Assistant Secretary for Nuclear Reactors. said,

“Now is the time to move boldly on AI-accelerated nuclear energy deployment,” “This partnership, combined with the President’s orders, represents more than incremental ‘uplift’ improvements. It has the potential to transform how industry prepares its regulatory submissions and deploys nuclear energy while upholding the highest standards of safety and compliance.”

Simply put, from licensing to construction and operations, AI is now helping eliminate long-standing bottlenecks.

Faster Nuclear Licensing with Advanced Tools

The DOE’s recent announcement is a big step in modernizing nuclear regulation. Normally, preparing licensing documents for nuclear reactors is slow and complicated. It requires reviewing thousands of pages of technical data and making sure everything meets strict rules.

This shows how AI can make nuclear licensing faster and more accurate, helping advanced reactors reach the market sooner. Here’s how AI is simplifying this usually long and complex process.

Kevin Kong, CEO and Founder of Everstar, added:

“Nuclear is poised to solve today’s critical energy challenges,” said “We’re excited to partner with INL to meet the moment, working together to accelerate regulatory review and commercialization.”

Microsoft and NVIDIA Partnership: Building AI Infrastructure for Nuclear Energy

While the DOE demonstration focused on licensing, the broader transformation is being driven by a powerful collaboration between Microsoft and NVIDIA.

Together, they are developing a full-stack AI ecosystem designed specifically for nuclear energy. This platform combines cloud computing, simulation tools, and advanced AI models to streamline every phase of a nuclear project.

Key technologies in this ecosystem include:

- NVIDIA Omniverse for simulation and digital modeling

- NVIDIA CUDA-X and AI Enterprise for high-performance computing

- Microsoft Azure AI for data processing and automation

- Microsoft’s Generative AI tools for permitting and documentation

This integrated system enables developers to manage complex workflows in a unified environment. Instead of working with disconnected tools and datasets, teams can now operate within a single, AI-powered framework.

As a result, nuclear projects become more efficient, transparent, and predictable.

Carmen Krueger, Corporate Vice President, US Federal, Microsoft, further added:

“Our collaborations with DOE, INL, and across the industry are demonstrating how we can effectively bring secure, scalable AI technologies to solve key energy challenges and achieve the broader national and economic security goals envisioned by the Department’s Genesis Mission.”

Aalo Atomics: Cutting Permitting Time and Costs with AI

One of the most compelling real-world examples of AI impact comes from Aalo Atomics.

By leveraging Microsoft’s Generative AI for Permitting solution, Aalo has achieved dramatic improvements in project timelines. The company reported:

- A 92% reduction in permitting time

- Estimated annual savings of $80 million

These results show how AI can address one of the biggest challenges in nuclear development—delays caused by regulatory complexity.

Permitting often takes years and requires extensive documentation. However, AI can automate much of this work, allowing teams to focus on critical decision-making rather than repetitive tasks.

For Aalo, the value goes beyond speed. The technology also improves confidence in project execution by ensuring that all documentation is consistent, complete, and aligned with regulatory expectations.

This video demonstrated further details:

AI-Powered Nuclear Lifecycle: From Design to Operations

The impact of AI is not limited to licensing. It extends across the entire lifecycle of a nuclear plant. In the blog post, written by Darryl Willis, Corporate Vice President, Worldwide Energy and Resources Industry of Microsoft, explained how AI can help nuclear in a broader context.

- Design and Engineering Optimization: AI and digital twins allow engineers to simulate reactor designs in real time. This enables faster iteration and better decision-making. Developers can reuse proven design patterns and instantly evaluate how changes affect performance, safety, and cost.

- Licensing and Permitting Automation: Generative AI handles document drafting, data integration, and gap analysis. It ensures that applications are complete and consistent, reducing delays during regulatory review. This allows experts to focus on safety assessments instead of administrative tasks.

- Construction and Project Delivery: Advanced simulations now include time and cost dimensions. These 4D and 5D models allow developers to track progress, predict delays, and avoid costly rework. AI also enables real-time monitoring, ensuring that construction stays on schedule and within budget.

- Predictive maintenance and Plant Performance: Once a plant is operational, AI continues to add value. Predictive maintenance systems can detect issues early, reducing downtime and improving reliability. Digital twins provide continuous insights into plant performance, helping operators maintain optimal efficiency.

The post AI Solutions from Microsoft and NVIDIA Power DOE’s Nuclear Energy Genesis Mission appeared first on Carbon Credits.

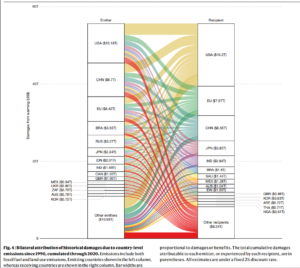

Climate change is not only a physical threat, but it also affects the world’s economy. A major new study published in the journal Nature on March 25, 2026, puts a clear number on this impact. It finds that carbon dioxide (CO₂) emissions from the United States caused about $10.2 trillion in total economic damage worldwide between 1990 and 2020. This makes the U.S. the largest single contributor to climate-related economic loss over that period.

The study shows that emissions slow economic growth in many countries. Rising temperatures cut productivity, lower output, and hurt long-term economic performance around the globe.

Marshall Burke, the lead author of the study, remarked:

“If you warm people up a little bit, we see very clear historical evidence, you grow a little bit less quickly. If you accumulate those effects over 30 years, you just get a really large change by the end of 30 years. It’s like death by a thousand cuts. And you have people being harmed who did not cause the problem, and that feels just fundamentally unfair.”

The researchers focused on carbon dioxide, the most common greenhouse gas. They used data on how temperature affects economic activity and then linked that to how much CO₂ different countries have emitted since 1990. This method links climate science to real economic results, including slower growth, lower productivity, and smaller national outputs.

Counting the Dollars: $10 Trillion in U.S.-Linked Damage

One of the study’s central findings is striking. From 1990 to 2020, U.S. emissions likely caused around $10.2 trillion in global economic damage. This means that warming linked to U.S. emissions has reduced economic production across many countries. The study links these impacts to heat’s long-term effects on labor, agriculture, and overall economic growth.

The damage is not confined to other nations. Roughly 30% of that $10.2 trillion figure is estimated to have occurred within the United States itself. In other words, U.S. emissions have slowed economic growth at home as well as abroad. The remaining impacts are spread across the global economy.

The researchers found that U.S. emissions led to about $500 billion in damage in India and around $330 billion in Brazil during that time. These figures show how carbon released in one area can affect economies far away.

A New Framework for Loss and Damage

The Nature study introduces a new framework for assessing what scientists call “loss and damage.” This term refers to harms that cannot be prevented by reducing emissions or avoided through adaptation alone.

The study uses economic data and climate models. It tracks how temperature changes over the years impact economic output.

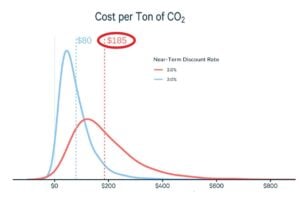

- To put the numbers into context: one tonne of CO₂ emitted in 1990 is estimated to have caused about $180 in global economic damages by 2020.

But that same tonne is projected to cause an additional $1,840 of cumulative damage by 2100, as warming continues and its effects compound over time. This highlights that past emissions still contribute to future economic harm.

The researchers highlight that these estimates focus on economic output, like goods and services. They do not account for all types of climate damage. They do not include costs from loss of life, health impacts, biodiversity collapse, cultural heritage losses, or many kinds of infrastructure damage. These excluded impacts could raise the true total cost of climate change even further.

The Social Cost of Carbon Revisited

This study is part of a broader scientific effort to understand the economic impacts of climate change. Climate and economic models show that rising temperatures are already slowing economic growth. If emissions stay high, this slowdown will get worse in the future.

Analyses by major international institutions and research groups project that climate change could reduce global GDP by a significant percentage by mid-century. This is compared to scenarios with strong mitigation, though exact figures vary by method.

The concept of estimating a “social cost of carbon” (SCC) — a monetary estimate of economic damage per tonne of CO₂ — has been used in policy analysis for years. It helps governments weigh trade-offs in climate policy. For example, they can decide how much to invest in emissions cuts versus adaptation.

However, traditional SCC estimates have been debated. They depend on assumptions about future growth, discount rates, and climate sensitivity. The Nature study advances this approach by tying economic outcomes directly to observed climate impacts.

Economists and climate scientists agree that warming impacts several areas. These include agricultural yields, labor productivity, energy demand, and health outcomes. These effects reduce economic output and increase costs for businesses and governments. The latest research makes these links more explicit by assigning dollar values to the historical impacts of emissions.

Equity and Global Responsibility

The research’s results also highlight important equity questions. Low-income countries often face bigger economic impacts compared to their emissions histories.

For example, nations with warmer climates and more fragile infrastructure may experience greater output losses due to temperature increases. These effects grow over time and can worsen existing development challenges.

At the same time, richer countries with higher historical emissions may take a larger share of responsibility for damage. The Nature study shows it is possible to calculate responsibility in monetary terms. However, turning those numbers into legal or financial obligations is still complex.

Tail Risks and Future Costs

The researchers also point toward the future. It finds that future damages from past emissions are much larger than the losses already accrued.

Since CO₂ remains in the atmosphere for centuries, its warming effects — and the economic damages linked to them — will persist well beyond 2020. This “tail risk” means that the total cost of historical emissions could rise sharply over the rest of this century.

Climate risk is increasingly integrated into economic planning and finance. Governments, businesses, and international institutions are incorporating climate scenarios into investment decisions and risk models.

This includes assessing how rising temperatures may affect infrastructure costs, insurance markets, supply chains, and national budgets. Without strong mitigation and adaptation measures, these economic pressures are expected to grow.

A Shared Reality, Quantified

The Nature study offers a clear and data-based way to think about the economic harms of climate change. Emissions from the United States since 1990 have caused over $10 trillion in global economic damage. This includes harm in the U.S., India, and Brazil.

These findings do not assign legal liability. However, they provide a meaningful picture of how climate change affects the global economy in terms of the social costs of carbon. They show that the costs of climate impacts are measurable and significant.

As the world continues to adapt and respond to climate change, understanding these economic links will be crucial for policymakers, businesses, and communities.

The post $10 Trillion in Carbon Cost? How U.S. Emissions Hit the Global Economy appeared first on Carbon Credits.

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits