Nearly a tenth of global climate finance could be under threat as US president Donald Trump’s aid cuts risk wiping out huge swathes of spending overseas, according to Carbon Brief analysis.

Last year, the US announced that it had increased its climate aid for developing countries roughly seven-fold over the course of Joe Biden’s presidency, reaching $11bn per year.

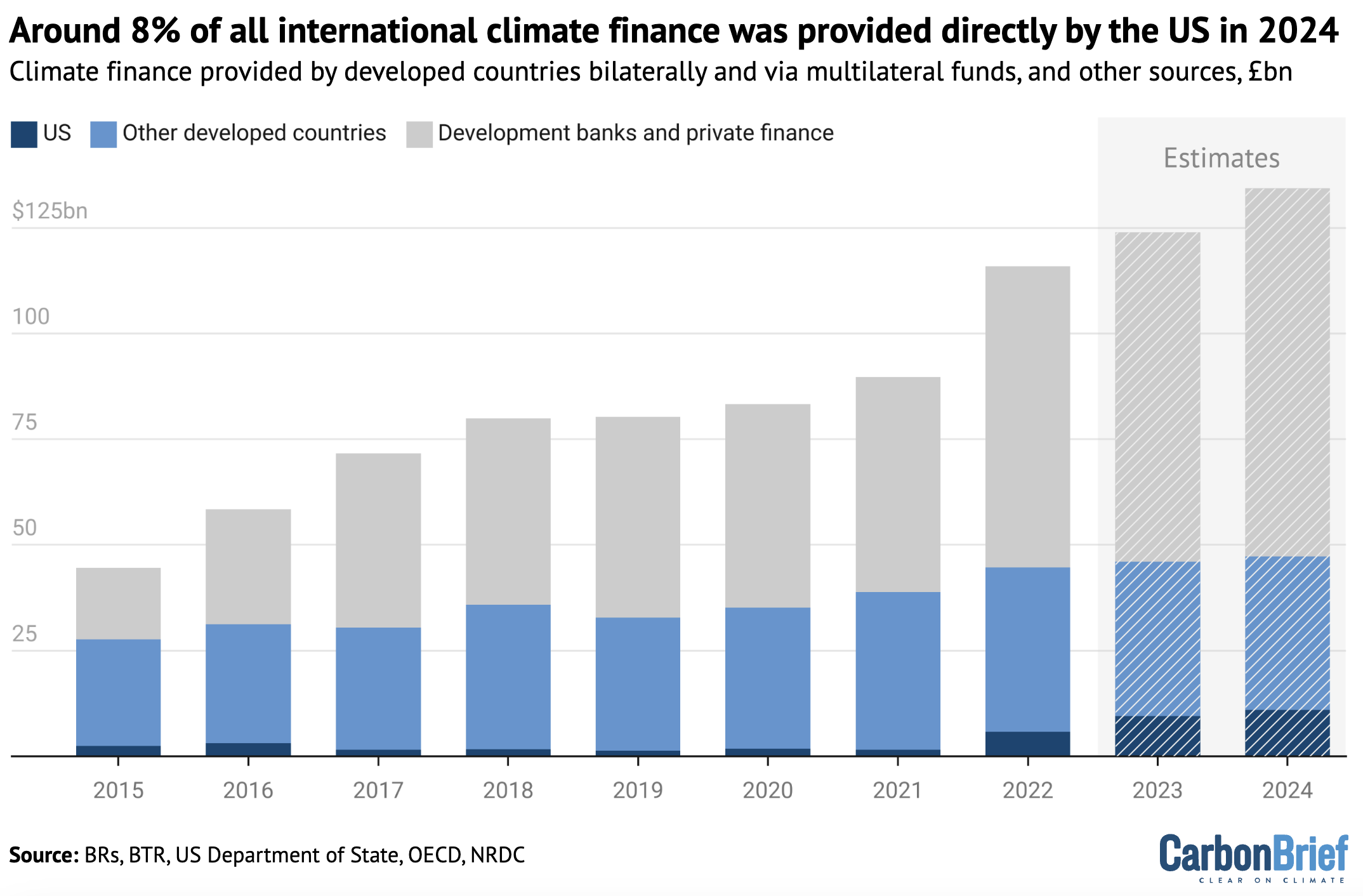

This likely amounts to more than 8% of all international climate finance in 2024.

However, any progress in US climate finance has been thrown into disarray by the new administration.

Trump has halted US foreign aid and threatened to cancel virtually all US Agency for International Development (USAid) projects, with climate funds identified as a prime target.

USAid has provided around a third of US climate finance in recent years, reaching nearly $3bn in 2023, according to Carbon Brief analysis.

Another $4bn of US funding for the UN Green Climate Fund (GCF) has also been cancelled by the president’s administration.

One expert tells Carbon Brief that more climate funds will likely end up on the “cutting block”.

Another warns of an “enormous gulf” to meeting the new global $300bn climate-finance goal nations agreed last year, if the US stops reporting – let alone providing – any official climate finance.

Carbon Brief’s analysis draws together available data to explain how the Trump administration’s cuts endanger global efforts to help developing countries tackle climate change.

- How much did climate finance increase under Biden?

- What are the climate impacts of cutting USAid?

- Are other sources of climate finance at risk?

- Methodology

How much did climate finance increase under Biden?

The US is by far the world’s largest economy and biggest historical emitter of carbon dioxide (CO2).

This means that, while it is the fourth-biggest national provider of international climate finance, its overall share is low relative to the nation’s wealth and responsibility for climate change. As a result, the US has long been seen as a laggard in this area.

The US provides 0.24% of its gross national income (GNI) as aid for developing countries, which includes some climate funding. This is the same share as the Czech Republic, a nation with a per-capita GNI three times smaller.

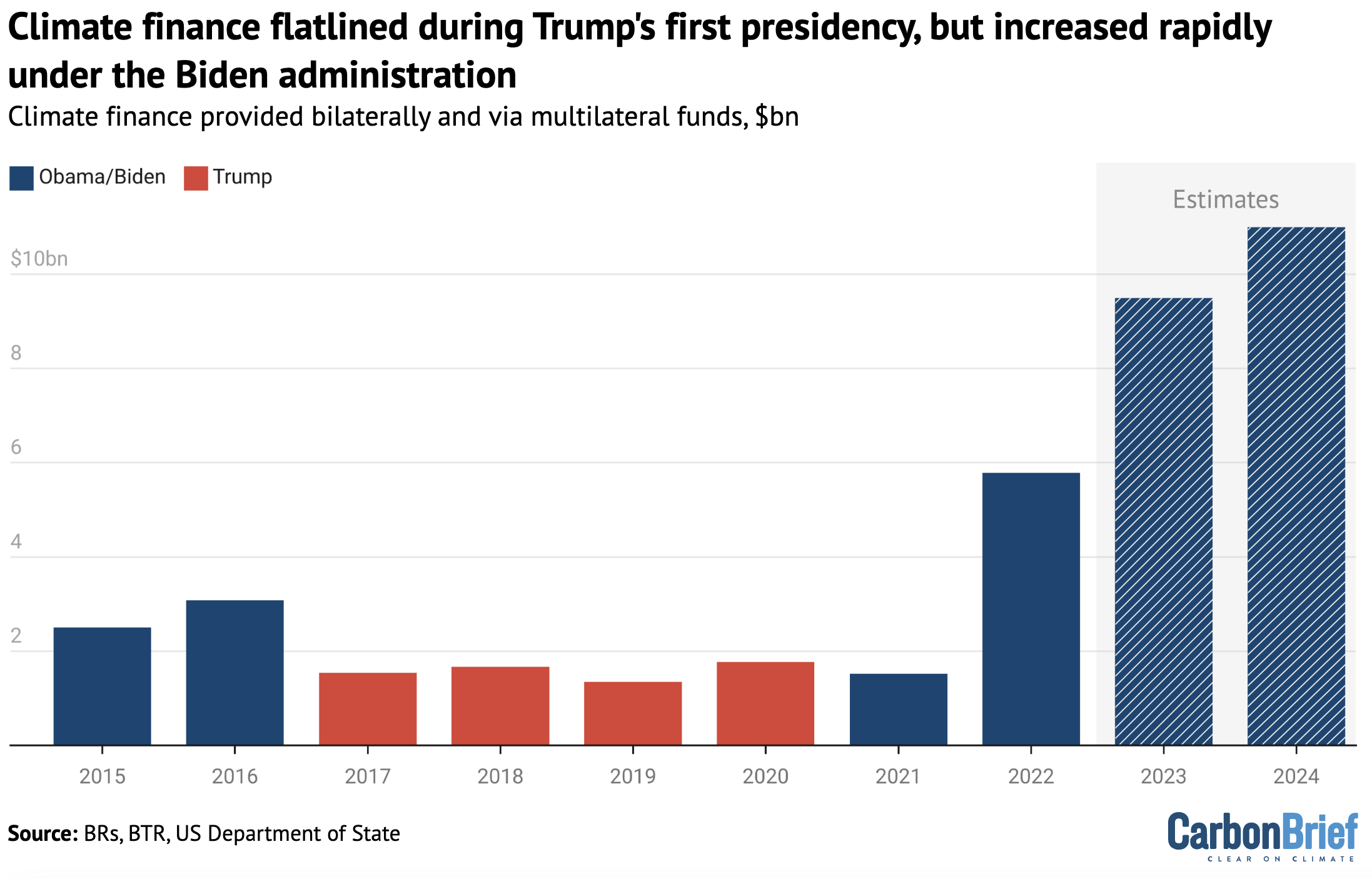

US climate-finance contributions stalled during Trump’s first four-year term as president, when other developed countries were ramping up to meet their target of providing and mobilising $100bn a year for developing countries by 2020.

A shift in focus came when Biden became president in 2021. He established an international climate finance plan to scale up US efforts, in line with US obligations under the Paris Agreement.

Biden also announced that the US would reach $11.4bn in annual climate finance by 2024.

This goal was achieved, according to “preliminary estimates” announced by the US during the COP29 climate summit at the end of 2024. These estimates, which are unlikely to be confirmed by the new administration, are shown in the chart below.

The figures are based predominantly on “bilateral” climate finance reported to the UN. They also include US finance distributed via multilateral climate funds, such as the Global Environment Facility (GEF) and the GCF.

Bilateral climate finance largely comes from aid programmes with climate benefits, such as supporting a geothermal project in the Philippines, investing in “climate-smart” agriculture in Bangladesh, or improving water security in Niger.

The US significantly increased its contribution towards climate finance during the Biden administration. Ramping up relevant US aid projects and multilateral funding helped developed countries to hit the $100bn climate-finance target – albeit two years late in 2022.

The $11bn reported by the US in 2024 would be the equivalent of 21% of all bilateral and multilateral climate fund inputs that year – up from around 4% under the previous Trump presidency. These funds are shown by the blue bars in the figure below.

(Estimates for 2023 and 2024 assume a steady rise in climate finance from sources beyond the US, as official figures beyond then have not been released. See Methodology for more information.)

Even when considering other sources of international climate finance – specifically multilateral development banks (MDBs) and “mobilised” private finance shown in grey in the figure below – the US has contributed a sizable share in recent years.

After lingering around 2% during the last Trump administration, the US share of total climate finance roughly quadrupled to more than 8% in 2024, Carbon Brief analysis suggests.

It is also worth noting that the US, as the biggest shareholder at the World Bank and a major shareholder at other MDBs, can be linked to a large portion of their finance. This contribution is not factored into official US reporting, so it has not been included in this analysis.

Even accounting for MDB contributions, US climate finance spending is still far lower than its “fair share”, based on its historical responsibility for climate change and ability to pay. Some analysts have put the US fair share as high as 40-50% of climate finance overall.

What are the climate impacts of cutting USAid?

Upon taking office for the second time in January 2025, Trump immediately took aim at international aid spending and climate action with a flurry of executive orders.

One order announced plans to withdraw the US from the Paris Agreement and criticised such treaties for “steer[ing] American taxpayer dollars to countries that do not require, or merit, financial assistance”. It also “revoked and rescinded” Biden’s international climate finance plan.

In another executive order, Trump announced a “pause” on US foreign aid “for assessment of programmatic efficiencies and consistency with US foreign policy”.

USAid handles 60% of US foreign aid – more than $43bn in 2023 – while the State Department oversees most of the remainder. Trump says he wants to “close [USAid] down” and his advisor Elon Musk has called it a “criminal organisation”.

Source: Truth Social.

Trump requires the approval of Congress to repurpose USAid funds or, indeed, abolish the agency. His administration’s actions have, therefore, been described as “illegal” and “unconstitutional” by senior Democrats and aid workers.

Yet, despite lawsuits and court orders instructing the administration to lift the pause, it has since stated its intention to eliminate more than 90% of USAid contracts and, more widely, $60bn of US foreign aid.

This would have major implications for US climate finance.

News outlets have reported on the climate-related programmes at risk, sometimes stating that USAid has funded half a billion dollars of climate programmes annually in recent years.

This figure, while based on USAid’s own reporting of its clean energy, climate adaptation and nature projects, is a significant underestimate of its total climate-finance contributions.

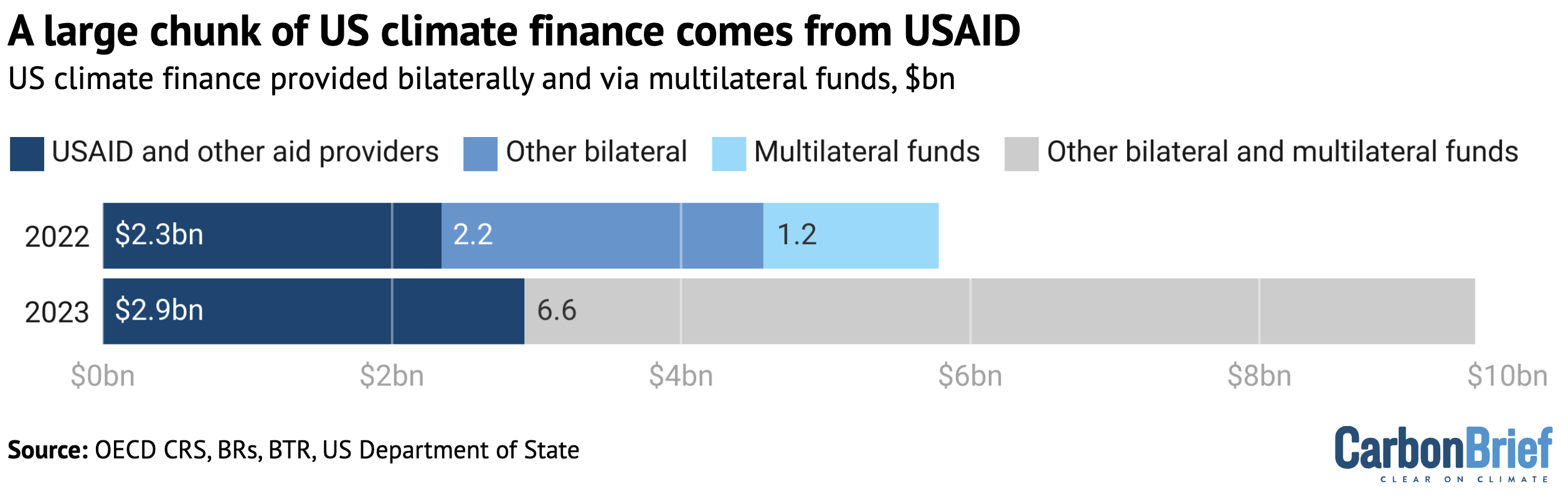

Carbon Brief analysis suggests that USAid contributed $2.8bn of climate finance in 2023, the latest year for which data is available. Other US departments with aid contributions in the OECD database contributed smaller sums, bringing total climate spending up to $2.9bn.

This equates to around a third of US climate finance that year. If a similar share from these departments was counted as climate finance in 2024, it would amount to nearly $4bn, Carbon Brief finds.

(These are estimates based on “climate-related” aid data reported to the OECD. See Methodology for more details.)

Climate-finance experts tell Carbon Brief that these higher figures align with the fact that many aid projects targeting other issues, such as agriculture, have climate components.

Dr Ed Carr, a centre director at Stockholm Environment Institute US who has previously worked at USAid, tells Carbon Brief:

“The way that the Biden administration was doing stuff and the way that [former president Barack] Obama before was doing stuff, [was to] start to weave a degree of climate sensitivity into everything…So, basically, a huge percentage of programmes [are] working on some aspect of climate.”

Unlike many forms of climate finance, USAid projects include lots of grant-based funding, which many developing countries view as preferable to loans and better suited to supporting climate adaptation.

Relevant projects backed by USAid in recent years include support for a food-security programme in Ethiopia, upgrading a dam in Pakistan and protecting water supplies in Peru.

The Trump administration has made it clear that “climate” is one of the issues that it is scrutinising as it assesses aid projects for consistency with what it defines as US interests. A survey sent to grant recipients several weeks after the initial executive order asks:

“Can you confirm this is not a climate or ‘environmental justice’ project or include such elements?”

Are other sources of climate finance at risk?

The remaining billions in climate finance are handled by more than a dozen organisations, distributing grants, loans, development finance and export credits.

Around $1.2bn of US climate finance in 2022 was paid into international funds, including the GEF. This amounts to a fifth of the total US climate finance that year.

The Biden administration did not release a breakdown of how much money went to these funds in 2023 and 2024. However, in 2023 the country paid out $1bn for the GCF alone.

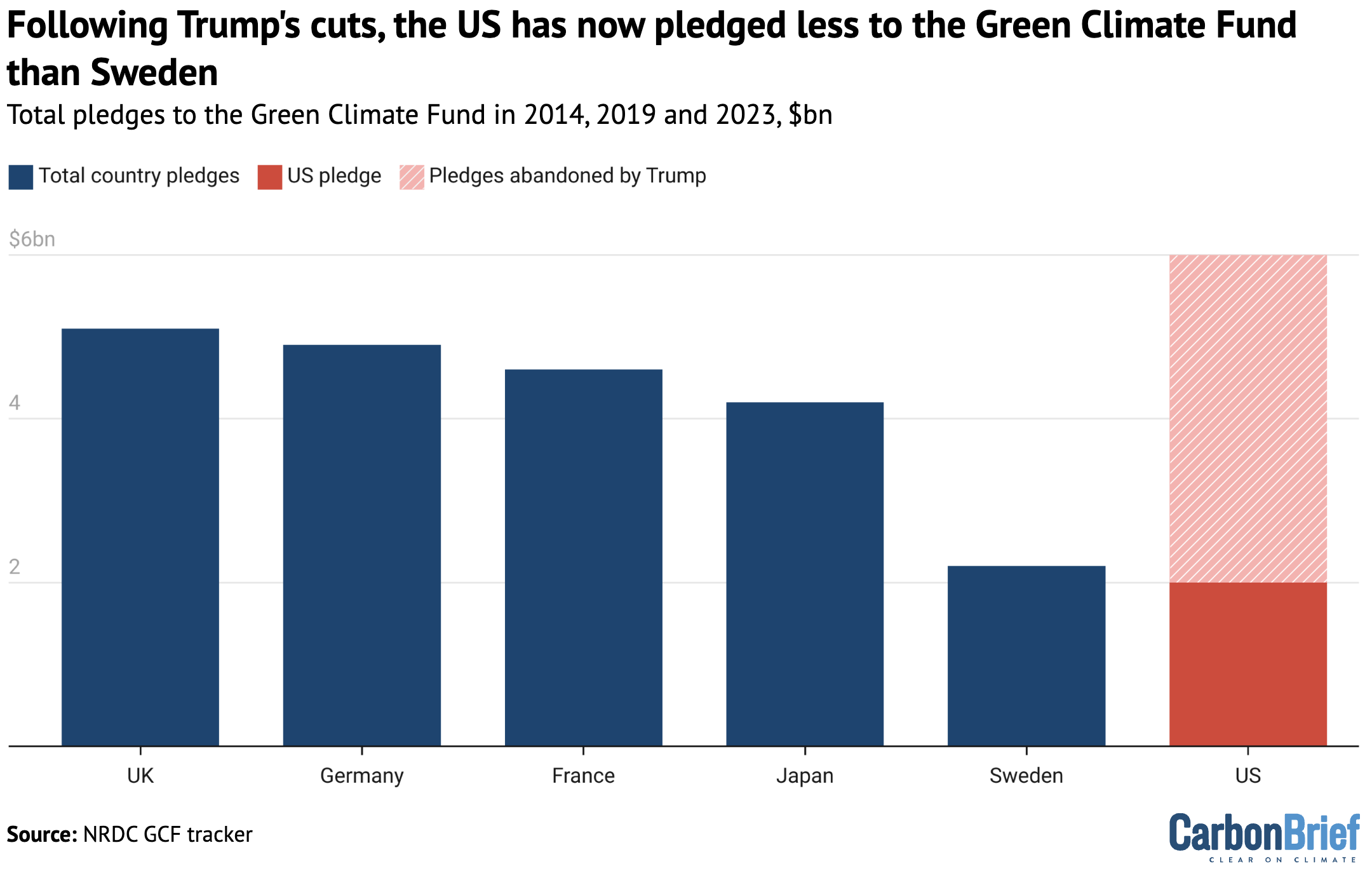

Such funding is also at risk as the new administration pulls away from what the White House calls “international agreements and initiatives that do not reflect our country’s values”. Notably, the US has now cancelled $4bn in funds previously committed to the GCF.

(Biden and Obama pledged $3bn each to the fund. However, neither of them ever delivered more than $1bn of their pledge, leaving $4bn outstanding.)

As the chart below shows, this means the US contribution to the GCF is now lower than that of Sweden – a country with an economy 50 times smaller.

The GCF is not the only specific fund that has been targeted. The US formally ended its involvement in the UN loss and damage fund, which it pledged $17.6m towards in 2023. It has also withdrawn from the Just Energy Transition Partnership initiative, which included at least $56m in grants to help South Africa transition away from coal power.

Another Trump executive order announced a review of “international intergovernmental organisation” membership, including MDBs.

There is an assumption that the US will not give up its considerable power in these banks. However, Trump supporters, including those behind the influential Project 2025, have laid out plans for withdrawing the US from the World Bank.

A large chunk of the remaining US climate finance in recent years has come from the US International Development Finance Corporation (DFC), which committed more than $3.7bn in climate finance in 2024 and a similar amount in 2023. This included loans for a wind power project in Mozambique and a railway to carry critical minerals through Angola.

DFC is a development finance institution that invests in private enterprises and was set up under the first Trump administration. It has so far been insulated from US aid cuts and there has been speculation that it may now play a larger role in US foreign policy.

Leaning more heavily on DFC, as well as the US Export-Import Bank (EXIM), would not be suitable for climate finance, Ritu Bharadwaj, a climate-finance principal researcher at the International Institute for Environment and Development (IIED), tells Carbon Brief:

“If these mechanisms remain intact while grant-based finance is gutted, it signals a shift away from public, needs-based funding toward finance that prioritises US commercial and strategic interests. In other words, what little climate finance remains will likely benefit US corporations first, rather than frontline communities.”

Additionally, even if such organisations are favoured by the new administration, this does not mean their climate projects will be protected. Benjamin Black, Trump’s nominee to lead DFC, wrote a blog post about the corporation in January, stating:

“The Biden administration’s emphasis on virtue-signaling – such as dedicating 40% of [DFC’s] recent commitments to green projects – raises serious concerns.”

Carr tells Carbon Brief that more US climate spending could still end up on the “cutting block”:

“From what we’ve seen so far, it looks to me like they are going to try and root out everything that they see as clearly related to climate.”

He caveats this by noting that some of the money the Biden administration would have counted as climate finance may continue, but not be defined as such.

This highlights the importance of accounting when assessing climate finance. Different governments around the world report different things as climate finance, depending on their priorities and political leanings.

For example, during the last Trump presidency, the US stopped reporting on climate finance to the UN. When calculating progress towards the $100bn goal during this period, the OECD had to estimate US figures based on “provisional data” or averages from previous years.

The Biden administration retrospectively reported the missing data from the Trump years in 2021, resulting in the OECD scaling down a previous estimate.

Clemence Landers, a senior policy fellow at the Center for Global Development (CGD) who previously worked at the US Treasury, tells Carbon Brief that a “very educated guess [is] that there will be no reporting from the US” in the coming years.

The US government website tracking aid has not been updated since December.

If climate finance is not recorded, this could hamper its inclusion in the annual $100bn goal, which lasts until 2025, as well as the $300bn goal that countries agreed on last year at COP29 to replace it, as Landers notes:

“That does leave an enormous gulf in terms of the new global climate-finance target.”

Methodology

Climate-finance reporting practices mean that official data can be difficult to analyse in detail.

In this article, annual US climate-finance figures for the period 2015-2022 are based on those reported by the US government to the UN in biennial reports (BRs) and, for the years 2021 and 2022, its first biennial transparency report (BTR).

These can be considered “official” climate-finance figures. They align with the figures that the US federal government has released and are the ones used to inform the OECD’s assessments of developed countries’ progress towards the $100bn annual target.

The figures only include bilateral climate finance and inputs into multilateral climate funds. MDB shares and private finance mobilised are not covered. Again, this aligns with the “climate-finance” totals quoted in progress reports by the Biden administration.

The climate-finance totals for 2023 and 2024 are based on releases from the US Department of State during the Biden administration. These figures are for the US financial year (FY), which runs from 1 October to 30 September. However, the FY figures are the same as the calendar year numbers reported to the UN for 2021 and 2022, so Carbon Brief assumes the same is true for 2023 and 2024.

Due to the significant time lag in official reporting to the UN, the figures underpinning these totals are not due to be released until 2026. (The previous Trump administration did not report them at all and it is unlikely that the current one will either, now that the US has announced its departure from the Paris Agreement.)

Given this time lag, estimates for total international climate finance in 2023 and 2024 are derived from a joint analysis by the thinktanks Natural Resources Defense Council (NRDC), ODI, Germanwatch and ECCO. This calculated likely totals in 2030, based on existing pledges and planned reforms. Carbon Brief assumes a steady trajectory to the overall $197bn estimated under the thinktanks’ “business-as-usual” scenario, with bilateral finance, specifically, reaching $50bn by 2025.

Climate-finance figures reported to the UN by the US do not include details of the government departments and agencies responsible, making it difficult to determine the share overseen by USAid. The Biden administration also did not report the breakdown between agencies.

This data is reported to the OECD Creditor Reporting System (CRS), which contains figures up to 2023. However, the information in the CRS is not “official” climate finance, but rather “climate-related development finance”, identified as such using Rio Markers. Most countries apply simple coefficients to convert the figures they report to the CRS into their climate-finance submissions to the UN, but the US calculates its climate-finance submissions separately.

Nevertheless, to obtain approximate figures, Carbon Brief has assumed that 100% of CRS projects marked as “principal” climate projects and 50% of the projects marked as “significant”, are climate finance. This aligns with a methodology used by other organisations, such as Oxfam, as well as other nations, including Germany, Japan and Denmark.

However, it is only a rough estimate. Experts that Carbon Brief consulted stressed the uncertainties of climate finance reporting and said the numbers could be higher or lower.

The post Analysis: Nearly a tenth of global climate finance threatened by Trump aid cuts appeared first on Carbon Brief.

Analysis: Nearly a tenth of global climate finance threatened by Trump aid cuts

Britain’s new prime minister announced in his first week that he will cut the cost of public transport and electricity, making lower-emission technologies like bus travel, electric vehicles and heat pumps more affordable for voters. But some of the funding for those policies will come from the budget for international climate finance, the government has said, raising concerns about fairness.

Former Manchester Mayor Andy Burnham took over from Keir Starmer as Labour Party leader and prime minister on Monday, appointing climate advocates Ed Miliband as foreign and development minister and Miatta Fahnbulleh as climate and energy minister.

On Tuesday, Burnham said his government would cut the value added tax (VAT) households and some small businesses pay on their electricity bills from 5% to zero from October 1, saving households £45 ($60) a year.

On Wednesday, he said the maximum fare bus companies in England can charge for a single journey will be reduced from £3 ($4) to £2 ($2.67) from January 1, 2027. The government said the subsidies to achieve this would be mostly funded by switching money set aside for overseas climate finance projects from grants to loans. It did not give further information in its announcement, while the UK’s transport minister told Sky News the plan is still being worked out.

-

Tropical forest protection fund at risk after UK stalls on pledge

The Brazil-led TFFF was launched at COP30 as an innovative financial model to keep rainforests standing, but is still short on startup cash -

UK halves Green Climate Fund contribution, as it spends more on security

After promising £1.6 billion to the UN’s flagship climate fund in 2023, the UK government has now said it will only hand over half as much -

EU, UK lead push for electrification as “powerful weapon” against fossil fuels

A group of dozens of countries seeks to build momentum for a COP31 pledge to electrify 35% of global energy use by 2035 as an alternative to fossil fuels

The floated changes to the climate finance budget were immediately criticised by groups working on climate justice for developing countries, including Bond, the UK network for NGOs, which described the decision as “disappointing”.

“Robbing Peter to pay Paul is not the answer and pitches marginalised communities in the UK against marginalised communities in lower-income and climate-vulnerable countries,” BOND CEO Romilly Greenhill said in a statement. “Climate finance must not worsen the debt burden of countries that are already suffering the worst – and most costly – impacts of a climate crisis they did not cause.”

Hunt for money

Burnham promoted both policies as measures to combat the rising cost of living and “give people breathing space”, with climate campaigners and industry groups noting they are also likely to reduce the UK’s climate-heating emissions by encouraging bus travel and the use of electric vehicles and heating.

But thorny questions remain over how the policies will be paid for. The government said Tuesday’s VAT cut for electricity would be funded by scrapping the previous government’s digital ID programme, but Darren Jones, a former minister involved with that policy, said it had been “unfunded” – a statement that dominated media coverage.

A day later, the government said the new bus fare cap would cost £454 million ($606m). Transport minister Heidi Alexander told Sky News that £54 million would be taken from an under-spend in the budget of the Department for Energy Security and Net Zero (DESNZ) and £400 million would come from changing unspecified international climate finance from grants to loans. The details “still need to be worked through”, she said, adding that the government “had wanted to make an announcement today”.

Mohamed Adow, director of Nairobi-based think-tank Power Shift Africa, said “climate finance was never meant to be a pot of money that governments raid when they need to pay for domestic spending”.

DESNZ had not responded to a request for comment at the time of publication. “We’re not wanting to fleece anyone here, and we actually want to maximise the development potential of this money that is available,” minister Alexander said in her TV interview.

Aside from the controversy over their funding, the policies themselves were widely welcomed by climate campaigners. Jess Ralston, energy lead at the Energy and Climate Intelligence Unit (ECIU), said the tax cut on electricity bills “could help households to switch to electric heat pumps, protecting UK homes from becoming ever more exposed to the whims of Putin and Trump when turning on their gas boiler”.

The last few months have seen global momentum build behind electrification, spurred by the US-Iran war disrupting oil and gas supplies and driving up prices. The Turkish and Australian COP31 presidencies have announced a global target to boost electrification, backed by the European Union, Canada, Philippines, UK and others.

Campaigners call for lower power prices

While reaction to the VAT cut was supportive, some questioned whether £45 a year of savings per household is enough and called for more measures to cut electricity bills.

Friends of the Earth’s energy lead Imogen Dow said those on the lowest incomes should be given cheaper electricity through a “social tariff” and the Institute for Public Policy Research (IPPR) think-tank – which is close to the Labour Party – said levies on energy bills should be shifted to general taxation.

Matthew Paterson, a politics professor at Manchester University, told Climate Home News that the most effective way to reduce electricity bills is to take on the UK’s private electricity companies, while consumer-oriented measures like the VAT cut are “tinkering around the edges”.

Jarrod Birch, head of policy and public affairs for the EV charging industry association Charge UK, said that while the policy would make home-charging cheaper, people who charge their vehicles at public points will still have to pay 20% VAT. The UK’s tax authority is fighting a court ruling that ordered it to reduce the tax motorists pay on public chargers to the current household rate of 5%.

Further measures will be the responsibility of Secretary of State for Energy Security and Net Zero Miatta Fahnbulleh, who is relatively new to politics after a career at left-wing, pro-climate think tanks the IPPR and the New Economics Foundation.

Michael Jacobs, political economy professor at Sheffield University and former adviser to UK Labour prime minister Gordon Brown, said Fahnbulleh would be a “climate advocate” who would continue the “progressive climate agenda” of her predecessor Ed Miliband.

“She’s a very creative policy wonk so I expect there to be lots of policy innovation under her,” he said, “I think she will be looking at new ways to encourage take-up of heat pumps and domestic batteries.”

Aid budget in Miliband’s hands

Despite reports he could be made finance minister, Miliband has been appointed Secretary of State for Foreign and Commonwealth Affairs. Miliband has attended many climate COP meetings over several decades, most recently representing the UK at COP29 and COP30, and has been targeted by the right-wing media for his support for climate action and opposition to new oil and gas drilling in the UK’s part of the North Sea.

In his new role, Miliband will be responsible for the UK’s overseas aid budget including its international climate finance, which the Starmer government had slashed to fund increases in defence spending.

UK cuts support for climate action abroad to fund military instead

Jacobs said he expected Miliband to prioritise climate and development in the UK’s foreign policy and to push Burnham and new finance minister John Healey to reverse Starmer’s aid cuts.

But there are fears Healey could try to cut the aid budget further to fund the military. Healey was a surprise pick for Chancellor of the Exchequer and grabbed headlines when he resigned as Starmer’s defence minister in June over what he saw as insufficient defence spending.

The post Will new UK PM’s green measures at home cause climate finance pain overseas? appeared first on Climate Home News.

Will new UK PM’s green measures at home cause climate finance pain overseas?

AMSTERDAM, Netherlands, 22 July 2026 – Greenpeace Netherlands has launched legal proceedings against a multi-billion-dollar global expansion plan by the biggest meat producer in Australia, JBS, in an escalation of climate litigation against the livestock industry.

Greenpeace petitioned a Dutch court to compel the meat giant to disclose information in order to challenge its business policies in court, including a US$6 billion global expansion, for which almost half is earmarked for Nigeria.

Elizabeth Atieno, Food Campaigner at Greenpeace Africa, said: “JBS’ meat empire expanded hand-in-glove with Amazon destruction, colossal emissions, human rights and corruption scandals, all with barely a semblance of transparency. This is the business model it wants to export to sub-Saharan Africa. JBS promises food security, but its expansion in Nigeria risks causing irreversible environmental damage and the displacement of smallholder farmers to line the pockets of wealthy global elites.

“Nigerians know well from the legacy of companies like Shell the destructive impact wrought by unchecked corporate power. As Greenpeace Africa has argued before the African Court of Human Rights, states with jurisdiction over multinationals must hold those corporate actors accountable – wherever they operate in the world. We welcome this bold legal action: the Netherlands and other European states must not be safe havens for corporations like JBS seeking to evade their responsibilities.”

In light of JBS’ longstanding failure to publish accurate and reliable information on its climate, nature and human rights impacts or its expansion plans, Greenpeace Netherlands views accessing this data as a necessary precursor to formal litigation in order to support its case. The case has the potential to be the first climate litigation of this scale against the livestock industry. This could set a major precedent for future legal challenges against the industrial agriculture sector, a major source of global emissions, particularly of methane, a potent greenhouse gas, responsible for 0.5°C of warming since the Industrial Revolution.[1]

JBS, via its subsidiary JBS Foods Australia, is the largest meat and food processing company in Australia. With a weekly processing capacity of over 50,000 cattle, it accounts for almost a quarter of all beef processing in the country, as well as a significant presence in the lamb, pork and farmed fish markets. [2] In 2022, ABC’s Four Corners accused the company of ‘repeatedly failing to protect its workers from horrific injuries.’ [3]

Marieke Vellekoop, Executive Director at Greenpeace Netherlands, said “In a month where JBS has thrown its flagship environmental commitments onto the scrap heap, JBS’ disdain for basic transparency only adds to the impression that this meat giant has something to hide and is desperate to prevent its expansion plans from going public. We were hoping we wouldn’t have to trouble a judge with this matter, but JBS has left us no choice but to seek our right to information through the Dutch courts.

“JBS appears to believe that despite moving to the Netherlands, our rules do not apply to it. This legal action aims to prove it wrong – and lay the ground for a first major climate and nature lawsuit against the dangerous expansion of the global meat industry.“

At the centre of the dispute is JBS’ planned US$ 2.5 billion investment in industrial livestock production in Nigeria.[2] Civil society groups in Nigeria have raised urgent warnings that the aggressive expansion will threaten local food security, drive regional instability, and accelerate ecological degradation. There is no available evidence that JBS has conducted any impact assessments or community consultations in Nigeria, and local efforts to gather more information via Freedom of Information requests have reportedly been ignored.[3]

The escalation to the courts follows the refusal of JBS, the world’s largest meat company, to comply with a formal disclosure demand delivered by Greenpeace Netherlands in April. The environmental group is utilising new Dutch legislation, which grants parties with a legitimate interest the right to demand access to specific corporate data necessary to build litigation against Dutch companies.[4]

Greenpeace Netherlands’ lawyers allege that JBS’ historic business practices and future expansion plans are inconsistent with the company’s climate and biodiversity obligations and represent a breach of its Dutch duty of care, which requires companies to act in line with international human rights law.[5]

If the court rules in favor of Greenpeace Netherlands, it is entitled to seek the required information in the form of documents and from senior JBS figures under oath, raising the prospect of the Batista brothers being forced to testify in Dutch court. JBS reincorporated as a Dutch entity (JBS N.V.) last year to facilitate a dual listing on the New York Stock Exchange.

In April, JBS was forced to temporarily suspend its first annual general meeting since moving its headquarters to Amsterdam after it was disrupted by dozens of Greenpeace Netherlands activists.

Last week, JBS scrapped two flagship commitments to reach Net Zero emissions by 2040 and eradicate deforestation from its supply chain. It also removed any explicit reference to Indigenous lands from all of its current policies. Greenpeace Netherlands is concerned this indicates JBS is seeking to expand unconstrained by the climate, nature and human rights impacts of its business.

–ENDS–

Notes:

[1] The livestock sector is estimated to be responsible for 31% of global methane emissions (more than oil and gas operations). In comparison to CO2, methane is shorter lived (around 12 years) but has a much stronger ability to trap heat in the atmosphere over its lifetime: it has approximately 80 times more climate impact than CO2 when measured over 20 years. This means that changes in methane emissions have a more rapid effect on the climate than changes in CO2. See Greenpeace Netherlands letter to JBS dated 30 April 2026.

[2] JBS Foods Australia, Our Business

[3] ABC, Australia’s biggest meat company JBS is repeatedly failing to protect its workers from horrific injuries, 25 April 2022

[4] JBS announcement

[5] Experts raise concerns over the risks of industrial animal farming (The Sun Nigeria)

[6] Simplification and modernisation of Dutch evidence law (Fieldfisher)

[7] Greenpeace Netherlands petition to Dutch court available here. Media briefing with further details on JBS expansion plans, including in Nigeria, available here.

Greenpeace launches legal challenge against Australia’s biggest meat company

Climate Change

“Next year is too late for regulations”: Beetaloo Energy’s 2GW gas-powered AI data centre a “disaster proposal” destined to cause climate chaos

SYDNEY, Wednesday 22 July 2026 — Beetaloo Energy has secured land from the NT Government for a massive $40 billion “hyperscale” AI data centre near Darwin, which would be powered by 2 gigawatts (GW) of gas power fracked directly from the Beetaloo basin, prompting calls from Greenpeace for urgent federal legislation.

The proposal marks a dangerous escalation in the AI data centre industry’s expansion, which threatens to entrench fossil fuel infrastructure for decades and put immense pressure on the region’s fragile water resources — while continuing to be unregulated.

Joe Rafalowicz, Head of Climate and Energy at Greenpeace Australia Pacific, said: “This disaster proposal for a 2GW gas-powered AI data centre in the NT is a shocking example of the unchecked expansion of hyperscale data centres in Australia. It is also, critically, more evidence for the urgent need for a moratorium on all new data centres until strong, binding regulations are put in place to protect our communities and climate.

“This proposal mirrors the frenzied, unchecked expansion currently wreaking havoc on communities in the US. We are seeing cowboy data centre operators treat Australia like a playground, steam-rolling ahead with projects that would lock down precious water resources and spike emissions, despite the overwhelming community opposition.

“Every day, more councils, communities and environmental groups are joining Greenpeace’s call for a moratorium on data centres, yet as of today there is still no system of safeguards or rules in place to regulate these companies.

“While Beetaloo Energy and the NT Government prepare to bulldoze ahead with this climate and water disaster, the Prime Minister is asleep at the wheel, promising to legislate a vague set of standards next year.

“Next year is too late, and anything less than mandating data centres cover their own energy demand, and then some, with new renewable energy is not enough.”

-ENDS-

Media contact

Lucy Keller on 0491 135 308 or lucy.keller@greenpeace.org

-

Climate Change11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测