When General Motors (GM) committed $625 million to develop Thacker Pass in Nevada, it did more than fund a lithium project. It established a new model for how automakers secure critical minerals, and in doing so, it reshaped how investors should evaluate the next generation of U.S. lithium assets.

This was not a passive investment. It was a fully structured supply chain partnership, combining equity, long-term offtake, and pricing strategy into a single agreement.

For investors watching Nevada’s clay lithium sector, the implication is clear: the first project has been validated – now the market is looking for what comes next.

A Landmark Deal and a New Partnership Model

GM’s $625 million investment in Lithium Americas remains one of the largest commitments by an automaker into upstream battery materials. The structure of the deal matters as much as its size.

GM secured exclusive access to Phase 1 production, locking in long-term supply from Thacker Pass, which is expected to produce around 40,000 tonnes per year of battery-grade lithium carbonate. That output alone could support hundreds of thousands to up to 1 million EVs annually.

More importantly, the agreement evolved into a joint venture structure, with GM ultimately taking a 38% ownership stake in the project while securing long-term offtake rights. This started as a TopCo equity investment but changed into a JV.

John Evans, LAC CEO, said in an interview on the GM agreement:

“They view this as an investment as much as they do a hedge to ensure that they get low-cost lithium. They want to run this JV as a business.”

A key highlight of the Thacker Pass deal is GM’s offtake agreement, which now serves as a template for a world-class OEM arrangement. GM must purchase at least 20% of its North American lithium demand, with the option to increase to 100%.

The floor price is “meaningfully above” the August 2024 low (~$10,000/t) but below current prices (~$21,000/t), as noted by Evans. GM was given an effective discount at higher price levels, lightly structured when prices at that time were at ~$60,000/t.

GM provides rolling three-year forecasts, with the next year’s volume fixed, allowing Lithium Americas to commit remaining volume to third parties. The agreement covers up to three years of contracted volume at a time.

GM Moves Upstream: From Automaker to Lithium Investor

The GM–Thacker Pass agreement highlights a shift in the lithium market. Automakers are moving upstream, directly into mining, to secure supply, manage costs, and reduce geopolitical risk. This approach is driven by both market forces and policy, with the U.S. pushing for domestic sourcing of critical minerals to support EV supply chains.

Key elements of this emerging model include:

Equity participation in the mining project,

Long-term offtake agreements tied to production, and

Structured pricing mechanisms to manage volatility.

Thacker Pass sits at the center of that strategy. It is widely recognized as the largest known lithium resource in the United States, and with construction underway, it is moving from concept to execution.

Breaking the Clay Lithium Barrier

For years, sedimentary clay lithium has carried a persistent discount in the market. Unlike brine operations in South America or hard-rock mining in Australia, clay deposits had never been proven at a commercial scale. The uncertainty around processing, recovery rates, and operating costs limited investor confidence.

Thacker Pass is now changing that, with construction underway, production targeted later this decade, and processing planned using sulfuric acid leaching at an industrial scale. Once operational, it will mark the first large-scale commercial validation of clay lithium extraction.

In resource markets, once a new extraction method is proven, capital follows. Financing improves, development timelines accelerate, and the entire category begins to reprice. This is exactly what happened in Chile’s brine sector decades ago. Clay lithium in Nevada may now be entering a similar phase.

GM’s investment provides a real-world benchmark for what a bankable lithium project looks like in today’s market. It demonstrates that:

OEMs are willing to invest upstream

Long-term offtake agreements can anchor financing

Domestic lithium supply is now a strategic priority

It also answers a key question that has held back the sector: Will major industrial players commit to clay lithium at scale? The answer is now yes.

The Next Project in the Queue: NNLP

With Thacker Pass moving forward, investor focus naturally shifts to the next project capable of attracting similar strategic interest. That brings attention to Surge Battery Metals’ Nevada North Lithium Project (NNLP), a structurally aligned next-tier candidate.

NNLP is not competing with Thacker Pass as a first mover; it is emerging as a next-generation project within a now-validated category.

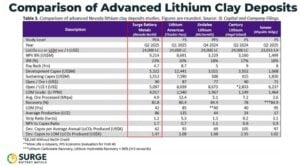

NNLP stands out based on core project metrics that directly impact economics. Its average lithium grade of 3,010 ppm is significantly higher than Thacker Pass Phase 1 material, which ranges from 1,500 to 2,500 ppm. Higher grades typically translate into more efficient recovery and lower processing intensity per tonne.

The project also benefits from near-surface mineralization and a low strip ratio of approximately 1.16:1. This may reduce mining complexity and indicate efficient material movement.

From a cost perspective, NNLP’s estimated operating cost of around $5,243 per tonne LCE compares favorably to LAC’s Thacker Pass guidance of roughly $6,200 per tonne.

Beyond geology, NNLP aligns with the same development framework that defines Thacker Pass. The project has secured a strategic partnership with Evolution Mining, funding up to C$10 million toward the Pre-Feasibility Study (PFS), while Fluor Corporation, the engineering firm involved in Thacker Pass, is leading the PFS at NNLP.

Leadership expertise also matters: Steffen Ball, a key member of the team, previously led battery raw material sourcing strategies at major automakers. These include Nissan North America and Ford Motor Company, aligning with the type of OEM agreements now seen in GM–Thacker Pass.

Scale, Market Tailwinds, and Second-Wave Opportunities

Scale is critical to attract major OEM partners. NNLP outlines a 42-year mine life with average annual production of approximately 86,300 tonnes of lithium carbonate equivalent. That output positions it to support long-term anchor offtake agreements, similar in structure to what GM secured at Thacker Pass.

Market fundamentals continue to support these developments:

Global lithium demand is projected to more than double by 2030.

EV production is scaling rapidly across major markets.

Governments are prioritizing domestic supply chains for critical minerals.

Even with recent lithium price volatility, long-term fundamentals remain intact. GM’s investment reflects a forward-looking strategy: secure supply today to avoid constraints tomorrow.

Thacker Pass carries the burden of being first, proving the process, building infrastructure, and validating the economics of clay lithium. This creates opportunities for projects that follow, like NNLP, which benefit from reduced technical uncertainty, clearer financing pathways, and a market that now understands clay lithium.

First Project Validated, Next Project Poised to Follow

GM’s $625 million investment was not just a bet on one project. It was a commitment to a new supply chain model for lithium—one that integrates mining, manufacturing, and long-term demand into a single structure. Thacker Pass is now proving that model, and NNLP is positioned to fit within it.

With higher grades, favorable mining characteristics, strong development partners, and the right scale, NNLP aligns with the criteria that attracted one of the world’s largest automakers to Nevada clay lithium in the first place.

For investors, the takeaway is straightforward: the first project is being built, the template is established, and the next project in the queue is becoming easier to identify.

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: .

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Image generated with Claude. Why have we juxtaposed a bicycle with balcony solar? Read on.

First it was Plug-In Solar. Then it was Balcony Solar. Now it’s Guerrilla Solar, at least according to Inside Climate News, which yesterday proclaimed that The ‘Guerrilla Solar’ Era Has Arrived.

“It,” of course, is Modular solar panels. They’re the hot new photovoltaic solution: cheap enough to buy at Home Depot, easy to hang or prop to catch maximum rays, and small enough to fit on a balcony (if you’ve got one) and plug into your “home grid.” But, alas, too meager a generator of electricity to be more than a bit player in decarbonizing most U.S. homes.

How do I know? I’ve done the math.

A standard, lower-end 220-watt balcony solar array will produce 337 kilowatt-hours a year, or 28 kWh a month averaged over the course of a year. That’s for a 220W unit measuring 3.5 feet by 3.5 feet. (220W x 1/1000 x 17.5% x 8760 hours per year = 337 kWh. Calculation assumes a 17.5% full-year capacity factor, which is arguably generous for New York, where I live. )

Our balcony solar mashup. Top: an install in Germany. Bottom: Home Depot advert.

A typical U.S. home consumes 10,500 kWh a year, or 28 to 29 kWh per day, says Solartech, drawing on U.S. Energy Information Administration data. That puts a home’s daily power needs on par with a balcony solar unit’s monthly output. In effect, once each month the balcony array gifts a homeowner or renter a bit more than day’s full complement of electricity. And earth’s atmosphere gets the same respite: a 3 percent reduction in carbon emissions caused by the home’s electricity usage.

(The 3 percent figure could also be calculated directly by dividing 337 kWh per year of solar production by 10,500 kWh per year to run the home. For bigger or smaller arrays, just prorate your assumed wattage by my 220W; for 440W, say, double my figures.)

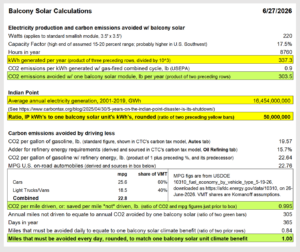

Balcony Solar metrics

Why write about balcony solar if it’s so inconsequential? CTC’s mission includes puncturing would-be climate balloons before they ascend too far. In the same vein, we practice quantification to make clear what does and doesn’t move the climate needle. (More on that further below.)

The best way to depict balcony solar’s climate value is to express it in terms of tangible metrics. We’ve selected two. Both assume the basic, lower-end PV array I assumed at the top: a 3.5 foot-square array whose peak output is 220 watts.

1. It would take 50 million 220W balcony solar units (bsu’s) to restore the climate benefit we destroyed in 2020-2021 when we shut the high-performing Indian Point nuclear power plant 32 miles from Midtown Manhattan.

2. A single person cutting back their driving by a mile a day would provide the same climate benefit over the course of a year as a single 220W bsu.

(Calculations in sidebar. Now you know why we led with images of an urban dweller as cyclist and balcony solar user.)

Yes, it’s dense — as befits a sidebar. The numbers tell a story. Follow the color co-ordination.

Ponder that: It would take fifty million smallish bsu’s to level up to the fossil fuel carbon emissions that Indian Point was keeping at bay by supplying the New York City area year in and year out with abundant carbon-free power. Deploying that many balcony solar units would entail 10 bsu’s for each of the 5 million households in the MTA’s service territory. (The Metropolitan Transportation Authority provides subway, bus and commuter rail transit in the five boroughs and seven suburban counties.) Or, if those same households upgraded to 1100-watt bsu’s, collectively they would still make up only half of the lost Indian Point power.

The second comparison, involving driving, is perhaps trickier to grasp but more interesting, since it relates to people’s behavior. Living differently isn’t part of public discourse, at least not in the USA, and especially when what’s being served up is using less. But “reducing,” as we might call it (remember “Reduce, Reuse, Recycle”? or, “Insulate, then Insolate”?) is just as potent for cutting emissions as switching to renewables — even more so when the reducing means driving less, considering the multitude of benefits that accrue from diminishing cars’ imprints on our communities. Still, staying on topic: driving just one fewer mile per day brings about the same shrinkage in carbon emissions as deploying one 220W solar array.

What Balcony Solar boosters are really saying

To be fair, our friends at Inside Climate News and, yes, The New York Times appear to be trying to modulate their balcony solar enthusiasm.

ICN‘s Dan Gearino, whom we cited up front, said he looked to Germany, the birthplace of balcony solar, to see if the units made sense for U.S. households. His takeaway: “It may make more sense financially to spend the cost of plug-in solar on insulation, air sealing or other basic measures to reduce energy use.” Hooray: insulate before you insolate.

Gearino helpfully interviewed renewables guru (and U.S. emigré) Craig Morris, who currently heads Germany’s plug-in solar trade association, Bundesverband Steckersolar. To Morris, balcony solar’s main advantages are that it provides power without taking up land, and that it affords people a way to “become participants in the transition to clean energy.” Behold, guerrilla solar. That, in turn, bolsters “the political consensus that supports the transition.” But Morris also made clear that widespread adoption of plug-in solar would only meet “about 2 percent of Germany’s electricity demand.”

Morris’s “about 2 percent” feels right for Germany. But not for the U.S., where widespread adoption of virtually any individual carbon alternative seems forever out of reach, and where the energy pie is so much larger — think giant fridges, freezers for beer, steroidal homes bursting with piles of powered toys, not to mention industrial and institutional electricity use that Morris correctly excluded from his figure.

Don’t forget to micro-dose. NYT headline + image for David Wallace-Wells’ guest essay (see text). Image by Rui Pu.

Both Gearino and Morris seem more measured than climate journalist Robinson Meyer, founding editor of Heatmap and frequent contributor to The Times, where he wrote about balcony solar in mid-June.

“New zero-carbon power kits will allow Americans to make their own energy choices,” declares the callout to the print version of Meyer’s NYT guest essay, The Tiny Solar Panel That Could Change America. (The even more expansive print headline invites us to “Forget Roofs. Backyard Solar Is the Next Frontier.”)

Wallace-Wells is of two minds. He calls balcony solar “a small way that apartment- and condo-dwelling Americans can take ownership of their energy choices and cut down their pollution on the margins.” No quarrel there, thanks to his qualifiers “small” and “on the margins.” Earlier, though, he opines that balcony solar units “have the potential to change how Americans understand and consume energy,” But read further and you’ll again see Wallace-Wells cautioning that “Balcony solar will play one small role in [the] drama” of transiting to the new world of clean, abundant energy.

Any such caveats are welcome these days, amid widespread solar hoopla. Still, it doesn’t seem to be in Wallace-Wells’ toolkit — or that of Inside Climate Newsand other mainstream climate journalists — to tutor their audiences as to the true limits of balcony solar and other panaceas. Just like it wasn’t in their field of vision a decade ago to lay out the true stakes of shutting Indian Point as Riverkeeper was singing its siren song.

What’s Next for NY Balcony Solar

Meantime, as Canary Media reported recently (and helpfully), New Yorkers concerned with climate and affordability are waiting for NY Gov. Kathy Hochul to sign the recently passed SUNNY (Solar Up Now New York) Act legalizing balcony and other plug-in solar. It would be head-spinning (and politically suicidal) if she didn’t, given near-universal support ranging from Con Edison to DSA Assembly Member Emily Gallagher, who told Canary Media, “This is the most popular bill I’ve [ever] worked on.”

My guess is that Hochul is waiting for the right moment, and perhaps the right “package,” that can advance and not undercut her push to launch five large new nuclear power plants around the state — one to be built by the public New York Power Authority, the others to be constructed and operated privately. A little bit of math, a la what we offered here a la Indian Point, might help her out.

The governor also must manage the veritable hot potato of her deferred implementation of the landmark 2019 Community Leadership and Climate Protection Act. She might do well to consider jettisoning the act’s unwieldy cap-and-invest centerpiece in favor of a straight-up carbon tax (with the revenues distributed pro rata to the state’s households) in its place. That, far more than balcony (or guerrilla) solar, could blow open the door to the “innovations and technologies we cannot yet imagine” that Wallace-Wells fantasized about in his Times essay.

On 11 June 2026, the Science Based Targets initiative (SBTi) published the most substantial revision of its flagship corporate framework since its introduction. The SBTi Corporate Net-Zero Standard Version 2.0 takes effect on 1 February 2027 and reshapes the way companies approach their net-zero targets.

In a kitchen in rural Kenya, a mother kneels beside a three-stone fire to cook the day’s ugali (a starchy staple food). The flames are open, the smoke is thick, and her youngest child sits close by, breathing it in. This scene plays out in millions of homes every morning, and it is also where a measurable carbon credit can begin.