The talented data analysts at Rhodium Corp. reported this week that U.S. emissions of greenhouse gases fell nearly two percent last year, even as national economic output rose by 2.4%. This was good news, further evidence of “decoupling” emissions from economic activity, but also bad news, because, says Rhodium, the 1.9% drop in GHG’s was woefully short of the 6.9% annual decrease required from now to 2030 to meet our Paris target of a 50-52% reduction in GHG emissions below 2005 levels.

Here we examine the locus of the good news: the 8% drop in electricity generation in 2023 vs. 2022 that enabled the 2% drop in overall emissions despite rises in emissions from transportation and some other sectors.

Here we examine the locus of the good news: the 8% drop in electricity generation in 2023 vs. 2022 that enabled the 2% drop in overall emissions despite rises in emissions from transportation and some other sectors.

The chart at left seems to reinforce the customary line that the leading driver of reduced U.S. carbon emissions is the switch to gas-fired power generation from coal-fired electricity. Indeed, the 101 TWh increase in gas-fired kilowatt-hours accounted numerically for three-quarters of the 134 TWh drop in coal, showing the close (if inverse) link between the two. Since modern “combined cycle” gas-burning plants emit a whopping 60% less CO2 per kWh than coal-burners, substituting the one for the other is a climate win, even allowing for the greenhouse impacts of methane released in gas drilling and transmission.

What’s missing from this narrative is the role of energy efficiency in suppressing demand for electricity, depicted in the graph’s two right-most bars.

The first bar, showing a gain of 47 TWh labeled as Efficiency, denotes the reduction in total U.S. electricity generation over the first 9 months of 2023 vs. the year-earlier 9-month total. If not for that contraction, either the reduction in coal-fired electricity would have been smaller than the 134 TWh shown, or the increase in gas-fired electricity would have had to be greater than the actual 101 TWh, or a combination of the two. (The other sources — nuclear, hydro, wind and solar — are already producing at their maximum capability.) Power-sector emissions would have been greater in either case.

But the efficiency story doesn’t end there. U.S. economic output wasn’t flat in 2023, it grew by 2.4% over 2022 (per preliminary figures reported by Rhodium). In earlier periods of U.S. history, that economic growth would have required greater electricity production. For most of the last century, the ratio averaged around 2-to-1, i.e., electricity growth was twice as fast as overall GDP growth. From 1975 to around 2005, the relationship was around 1-to-1. Since 2005, in a profound development that few predicted (and which few have acknowledged, other than CTC), U.S. electricity usage has been virtually flat, even as economic activity has risen by more than 40 percent.

But the efficiency story doesn’t end there. U.S. economic output wasn’t flat in 2023, it grew by 2.4% over 2022 (per preliminary figures reported by Rhodium). In earlier periods of U.S. history, that economic growth would have required greater electricity production. For most of the last century, the ratio averaged around 2-to-1, i.e., electricity growth was twice as fast as overall GDP growth. From 1975 to around 2005, the relationship was around 1-to-1. Since 2005, in a profound development that few predicted (and which few have acknowledged, other than CTC), U.S. electricity usage has been virtually flat, even as economic activity has risen by more than 40 percent.

For this post, and in the chart above, I’ve used a 1-to-1 relationship, i.e., I’ve assumed that if not for increased energy efficiency, the 2.4% year-on-year growth in U.S. economic activity would have required a corresponding 2.4% increase in electricity production. Numerically, nearly 80 additional TWh would have been required (calculated as 2.4% of 2022 9-month U.S. electricity production, including rooftop solar, of 3,283,000 TWh). Adding that to the actual decrease in electricity yields the true efficiency figure of 126 TWh shown in the right-most bar.

The biggest enabler of the 2022 drop in coal-fired electricity generation, then, wasn’t increased power production from natural gas, which grew by 101 TWh. It certainly wasn’t solar, which grew by a lot percentage-wise, nearly 15%, but by just 27 TWh in absolute terms. Nor was it the U.S. wind sector, which actually contracted in the first nine months of the year (see first chart, above).

Well-meaning misinformation from Canary Media, Jan. 10. See link to story in text.

Others are spinning the 2023 data differently. Rhodium reports that “coal is playing less and less of a role on the grid, while both natural gas and renewable generators are filling the gap.” True, but it leaves out the vital — I would say central — role played by energy efficiency in constraining U.S. electricity demand so that the increase in gas-burning could be held to 101 TWh.

For sheer distortion it’s hard to top Canary Media’s take, shown at left. While it’s true that “the buildout of renewable energy helped to curb America’s greenhouse gas emissions by 1.9% in 2023,” the actual gain in renewable power output was a sideshow to electricity efficiency. Indeed, netting the 27 TWh increase in solar output by the combined 23 TWh decrease in hydro and wind generation combined leaves almost nothing in the way of net renewables growth.

This suggests updating the adage about victory having a thousand fathers while defeat is an orphan. In climate circles and energy policy, last year’s modest success in reducing emissions has multiple parents: more gas-burning, more solar arrays, more renewables. Meanwhile, the truest parent — increased efficiency in electricity usage — goes unremarked. This inattention is mirrored in policy. The Inflation Reduction Act subsidizes everything from electric cars and heat pumps to battery storage and factories to supply wind turbines and solar cells. It doesn’t, for the most part, subsidize ways to use energy more efficiently.

That’s not deliberate, it’s the nature of energy efficiency, savings and conservation: they involve ways of doing more with less, and they come in a million guises. They can’t be subsidized, but they can be rewarded, by taxing carbon emissions.

We’ve been saying for two decades: Taxes on fossil fuels, levied “upstream” at mines, wells and import docks, raise the value of every personal, corporate and collective action to reduce unnecessary use of energy. There’s no way around taxing carbon.

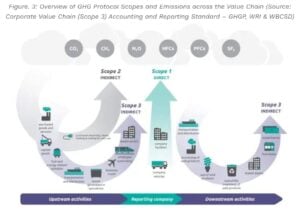

Carbon Footprint

Verra to Launch Scope 3 Standard in 2026: A New Era for Value Chain Carbon Tracking

The post Verra to Launch Scope 3 Standard in 2026: A New Era for Value Chain Carbon Tracking appeared first on Carbon Credits.

Rising global oil prices are driving up demand for electric vehicles (EVs), with Chinese brands emerging as key beneficiaries. Recent spikes in crude prices are driven by heightened tensions in the Middle East and disruptions in the Strait of Hormuz, a critical oil shipping route.

These factors have pushed Brent crude above $100 per barrel and created instability in fuel markets. This has pushed many consumers to rethink fuel costs and consider EV alternatives. Higher fuel prices increase running costs for gasoline and diesel cars, making EV ownership more economical in many markets.

Chinese EVs Gain Speed Abroad

Dealers in countries like Australia and parts of Southeast Asia see growing interest in Chinese EVs. This rise comes as fuel prices increase.

Showrooms selling Chinese new energy vehicles (NEVs) are seeing more test drives, customer inquiries, and rising order volumes. In Australia, the EV market share hit a record high of 11.8% for vehicle sales. Analysts say this jump is partly due to rising petrol prices.

Chinese manufacturers like BYD, GWM, and Chery are rapidly growing abroad. Some dealers see more walk-ins and more customers buying EVs.

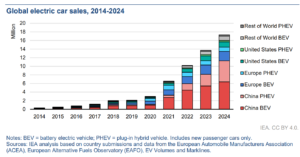

China’s EV industry is now the largest in the world. In 2024, Chinese automakers produced over 12.87 million plug‑in electric vehicles (PEVs), including battery electric (BEV) and plug‑in hybrid models, accounting for nearly 47.5% of total automobile production. That figure marked a strong year‑on‑year rise and underscored China’s industrial scale and export readiness.

By late 2025, more than 51% of all new vehicles sold in China were electric — a major shift from just a few years earlier.

This domestic scale provides an export advantage. Chinese EVs often cost less than similar European and North American models. This helps them succeed in markets where fuel costs hit household budgets hard.

Fuel Costs Drive Behavior Shift

Rising oil prices are a major driver of these sales trends. Global crude prices have fluctuated due to geopolitical tensions. The Strait of Hormuz route carries around 20% of the world’s oil trade. These disruptions pushed crude prices sharply higher in early 2026.

In many countries, higher retail fuel prices translate into more immediate cost pressures for consumers. Reports from countries like Australia show petrol prices over $2.50 per litre. This rise is making consumers think about EVs to lower long-term costs.

Global EV Market Trends and Forecasts

The surge in Chinese EV exports aligns with broader global trends. Major industry forecasts suggest that global sales of battery electric and plug-in hybrid vehicles may top 22 million units by 2025. This could represent about 25% of all new car sales worldwide.

Global electric vehicle sales in 2025 reached nearly 21 million units, including both battery electric vehicles and plug‑in hybrid electric vehicles. This total represents a significant increase, roughly 20 % more than in 2024.

China’s share in this global growth is large. In 2024, Chinese manufacturers made up around 70% of all EV exports. This shows China’s key role in supply chains and manufacturing.

As oil demand growth slows due to EV uptake, some forecasts suggest that EVs could displace millions of barrels of global oil demand each day in the coming decade. By 2030, EV adoption could cut about 5 million barrels per day of oil use, according to major energy outlooks.

Trade Barriers vs Expansion

Despite strong export gains, barriers remain. Some regions have imposed tariffs and trade restrictions on Chinese EVs, and infrastructure gaps in charging networks can slow adoption. For example, tariffs exceeding 100% on certain Chinese EV imports in the U.S. have limited market share there.

However, Chinese OEMs are developing supplier and shipping capacity to support overseas demand. In 2025, China’s electric car makers expanded shipping through roll‑on/roll‑off carriers capable of transporting more than 30,000 vehicles, improving export logistics.

Emerging markets in Southeast Asia, Latin America, and Oceania are also showing rising EV interest. In the Philippines and Vietnam, dealerships see EV orders growing quickly. Some are even doubling their weekly sales, thanks to high fuel costs.

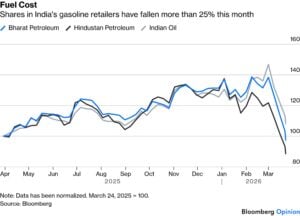

In India, where oil imports make up a big part of the economy, rising petrol costs make running traditional fuel vehicles more expensive. This has helped boost interest in electric vehicles, which are cheaper to operate when fuel is costly. Notably, the share of ICE retailers fell by over 25% in March.

Indian consumers and businesses view EVs as a way to shield against unstable oil prices. This also helps lower fuel costs, supporting the country’s move to electric transport.

What This Means for Energy and Transport Futures

The convergence of high oil prices and strong EV supply from China is creating a feedback loop. Higher fuel costs push consumers to consider EVs more seriously. Chinese manufacturers are well positioned to fill that demand with competitive pricing and large production scale.

The shift could speed up the move from fossil fuel cars to electric vehicles worldwide. This is especially true in price-sensitive and emerging markets. EV adoption also has implications for oil demand trends.

- As battery and charging tech get better and EV markets grow, oil use — especially in transport — might slow down or peak sooner than we thought.

At the same time, governments and industry groups are tracking these shifts closely. Policies that support charging infrastructure, EV incentives, and emissions standards will influence how quickly the global fleet electrifies.

Ultimately, the current oil price shock may have sparked a shift in global automotive markets — one where Chinese EVs take an increasingly central role in transport electrification worldwide.

The post Oil Shock Ignites Chinese EV Export Surge Around the World appeared first on Carbon Credits.

The U.S. is witnessing a surge in utility-scale solar development, driven by growing corporate demand for clean energy. Major tech companies like Meta and Google are securing long-term deals in Texas, combining renewable energy growth with economic and grid benefits.

This trend highlights how corporate commitments are shaping the future of the clean energy transition. Let’s find out.

Zelestra and Meta’s $600 Million Solar Deal

Madrid-based renewable energy firm Zelestra secured a massive $600 million green financing facility, signaling strong investor confidence in utility-scale solar. The funding, backed by Société Générale and HSBC, will support two large solar projects in Texas—Echols Grove (252 MW) and Cedar Range (187 MW).

These projects are not standalone efforts. Instead, they are part of a broader clean energy partnership with Meta, one of the world’s largest corporate renewable energy buyers. Together, they form a portion of a seven-project portfolio totaling 1.2 GW under long-term power purchase agreements (PPAs).

Sybil Milo Cioffi, Zelestra’s U.S. CFO, said:

“This financing marks a significant milestone in the delivery of our largest U.S. solar projects to date. It reflects strong confidence from Societe Generale and HSBC in our strategy and execution capabilities and reinforces our ability to attract first-class capital to support our growth platform in the U.S. market.”

Zelestra is strengthening its presence in the U.S. energy market with innovative solutions for hyperscalers and corporate clients. It is developing around 15 GW of renewable projects across key markets. In February 2026, BloombergNEF ranked Zelestra among the top 10 PPA sellers to U.S. corporations.

Solar Powering Meta’s Climate Strategy

Meta continues to aggressively expand its clean energy footprint. The company has made renewable energy procurement a core part of its climate roadmap—and the numbers clearly reflect that shift.

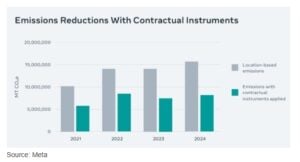

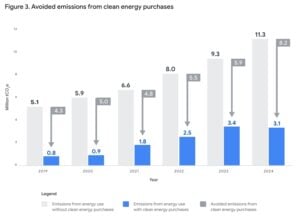

In 2024, Meta reported emissions of 8.2 million metric tonnes of CO₂e after accounting for clean energy contracts. In comparison, its location-based emissions stood at 15.6 million tonnes. This marked a sharp 48% reduction, largely driven by renewable energy purchases.

Moreover, the company has consistently maintained momentum:

- Since 2020, it has matched 100% of its electricity consumption with renewable energy.

- Over the past decade, it has secured more than 15 GW of clean energy globally.

- Overall, renewable energy procurement has helped cut 23.8 million MT CO₂e emissions since 2021.

As a result, Meta cut operational emissions by around 6 million tonnes in 2024 alone. At the same time, it tackled value chain emissions using Energy Attribute Certificates (EACs), reducing Scope 3 emissions by another 1.4 million tonnes.

Most of these deals were concentrated in the U.S., highlighting the country’s growing importance in corporate decarbonization strategies.

Importantly, this collaboration goes beyond just energy supply. It also aims to deliver broader economic benefits, including:

- Local job creation during construction

- Long-term tax revenue for the region

- Continued investment in local infrastructure

David Lillefloren, CEO at Sunraycer, said:

“These agreements with Google represent a significant milestone for Sunraycer and underscore the strength of our development platform. We are proud to support Google’s clean energy objectives while delivering high-quality renewable infrastructure in Texas.”

Additionally, the deal was facilitated through LevelTen Energy’s LEAP process, which simplifies and speeds up PPA execution. This highlights how innovative platforms are now playing a key role in scaling renewable deployment.

“Google’s data centers are long-term investments in the communities we call home,” said Will Conkling, Director of Energy and Power, Google. “This collaboration with Sunraycer will fuel local economic growth while helping to build a more robust and affordable energy future for Texas.”

Google, like Meta, has built a strong clean energy portfolio over time. Since 2010, it has signed over 170 agreements totaling more than 22 GW of capacity worldwide. Its long-term ambition is even more ambitious—achieving 100% carbon-free energy, every hour of every day, by 2030.

Why Texas Is Becoming the Center of Energy Transformation

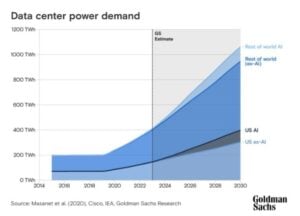

All these developments point to one clear trend—Texas is rapidly becoming a global hub for clean energy and data center growth.

On one hand, the state offers strong solar resources, vast land availability, and a deregulated power market. On the other hand, it is witnessing a surge in electricity demand, especially from data centers and AI-driven workloads.

According to projections from the EIA, U.S. electricity demand could rise by 20% or more by 2030. Data centers are expected to play a major role in this growth. In fact, energy consumption from data centers increased by over 20% between 2020 and 2025.

As a result, energy infrastructure in Texas is facing growing pressure. Rising industrial activity, extreme weather events, and rapid digital expansion are all contributing to grid stress. Yet, at the same time, this demand is driving unprecedented investment in renewable energy.

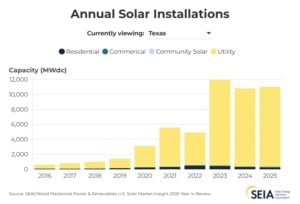

The EIA expects Texas to lead solar expansion in the coming years, accounting for nearly 40% of new solar capacity in the U.S. California will follow closely, and together, the two states will drive almost half of total additions.

Even though the sector has faced temporary slowdowns, the long-term outlook for U.S. solar remains highly positive.

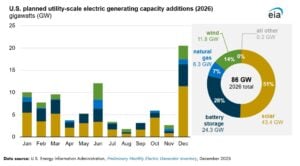

In 2025, the U.S. added 53 GW of new electricity capacity—the highest annual addition since 2002. Notably, wind and utility-scale solar together generated 17% of the country’s electricity, a massive jump from less than 1% two decades ago.

Looking ahead, growth is expected to accelerate again. Developers are planning to add around 86 GW of new capacity in 2026, which could set a new record. Solar alone is projected to account for more than half of this expansion.

Breaking it down further:

- Solar is expected to contribute 51% of new capacity

- Battery storage will make up 28%

- Wind will account for 14%

Utility-scale solar capacity additions could reach 43.4 GW in 2026, marking a 60% increase compared to 2025 levels.

Analysis: Corporate Demand Is Reshaping Energy Markets

Overall, the developments from Zelestra, Meta, Google, and Sunraycer highlight a broader transformation underway in global energy markets.

First, corporate buyers are no longer passive participants. Instead, they are actively shaping energy infrastructure through long-term PPAs. These agreements provide stable revenue for developers while ensuring a clean power supply for companies.

Second, financing is becoming more accessible. Large-scale funding deals, like Zelestra’s $600 million facility, show that banks are increasingly willing to back renewable projects with strong contractual support.

Third, regions like Texas are emerging as strategic energy hubs. The combination of rising electricity demand and favorable renewable conditions is attracting both developers and corporate buyers.

However, challenges remain. Grid reliability, permitting delays, and policy uncertainty could still impact the pace of deployment. Even so, the overall trajectory remains clear.

Clean energy demand is rising fast. Big Tech is leading the charge. And solar power is set to play a central role in meeting future electricity needs.

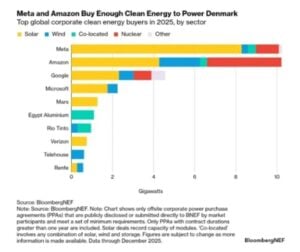

- READ MORE: Meta, Amazon, Google, and Microsoft Dominate Clean Energy Deals as Global Buying Slips in 2025

The post Texas Solar Market Heats Up with Meta and Google Investments appeared first on Carbon Credits.

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?