A few years ago, many Australians wanted to switch to solar energy, but the cost sometimes didn’t match their expectations.

But today, the landscape has changed dramatically. 2025 is poised to be a pivotal moment for the adoption of renewable energy in Australia. Wondering why?

With a range of generous government rebates and support programs available, particularly in Victoria (VIC) and New South Wales (NSW), going solar has never been more accessible or affordable.

Whether you’re a homeowner, renter, or involved in community housing, these federal and state solar rebates can significantly reduce installation costs, making the transition to solar energy more achievable than ever.

Therefore, in this article, we’ll focus specifically on the types of government rebates available for Solar Panels in VIC & NSW.

We’ll also highlight how these expanded federal incentives, upgraded state schemes, and new battery rebates are helping Australians lower their electricity bills while boosting energy independence.

So, let’s get started!

In this blog post:

-

Federally Available Rebates for Both VIC & NSW

-

VIC Solar Panel Rebates, Grants & Incentives in 2025

-

New South Wales (NSW) Solar Incentives

-

Takeaway Thoughts

Federally Available Rebates for Both VIC & NSW

From the abundant sunshine of Australia, we get around 58 million petajoules of clean, reliable solar energy each year, which is nearly 10,000 times more than we actually need.

So it’s no surprise we’re making the shift to solar in a big way.

To help in this energy transition, the government offers solar rebates through Small-scale Technology Certificates (STCs) under the Renewable Energy Target (RET).

Isn’t it a smart move toward a cleaner, greener future? Surely it is!

So let’s explore the available rebates and incentives further in the following section:

Small-scale Renewable Energy Scheme (SRES) | Solar Rebates via STCs

In this federal SRES, your installer applies for Small-scale Technology Certificates (STCs) when installing solar systems up to 100 kW, delivering an immediate discount on upfront costs.

However, please note that the value depends on your system’s size and geographical location. For example:

- In Victoria, a 6 kW system might yield around $1,748 based on 46 STCs, each at $38.

- In New South Wales, the same system could attract approximately $2,052. These figures typically reduce installation costs by 30% to 40%.

So, what are STCs?

STCs are energy certificates generated by authorized solar retailers. For each megawatt of energy saved by the solar, one STC is generated.

These energy certificates serve as a financial inducement for home and small-business owners to adopt different energy-saving techniques, including solar water heaters and solar panel systems.

Is the homeowner responsible for generating these certificates? Do you get a cheque in the mail in exchange for them? No, that’s not how it works.

The CEC (Clean Energy Council) approved solar retailer with whom you make the deal is responsible for generating these certificates and handing them over to the energy retailers.

The Small-scale Technology Percentage (STP) determines how many STCs the energy provider must submit. The price against each STC is determined by the demand and supply curves of the financial quarter.

What’s in it for you?

Here’s the good part: these Small-scale Technology Certificates (STCs) aren’t just a win for the planet; they’re a win for your wallet, too.

Solar retailers trade these certificates for financial gain, which means they’re motivated to offer you upfront discounts on your system. In the end, you save thousands on installation costs just for choosing to go green.

It’s a simple way to cut your power bills, reduce your carbon footprint, and make the most of Australia’s sunshine all in one move.

STC FAQs For Beginners: Know Before You Apply!

Am I eligible for this rebate?

If you are running a small business or a household with a capacity of 100kW or less, you are eligible.

What’s the price of STC?

The price of STCs depends on the market demand and supply for the quarter. It can range anywhere from $0 to $40 at max.

How can I get it?

Reach out to a CEC-approved solar retailer and use CEC-approved products for the installation, and you will get it. Of course, there are other benchmarks to meet to provide a definitive answer.

Will STC end soon?

Until the year 2030, all solar retailers will generate certificates, and after that, this scheme will come to an end.

Cheaper Home Batteries Program: Federal Battery Rebate

Launched on July 1, 2025, this federal initiative offers approximately 30% off eligible home battery installations, delivered through the SRES framework. However, to become eligible for this battery incentive, you must meet a few criteria.

Here’s the eligibility checklist:

- Your solar battery has a nominal capacity ranging from 5 kWh to 100 kWh.

- The system must be approved by the Clean Energy Council.

- STCs (Small-scale Technology Certificates) are calculated based on the battery’s usable capacity, but can only be claimed for the first 50 kWh of usable capacity.

- The battery must be installed with a new or existing solar PV system.

- Installation done by accredited installers.

- Open to all eligible properties, with a limit of one rebate per property.

Lastly, installation is considered complete once a Certificate of Electrical Compliance is signed, confirming your system meets all relevant state and territory electrical safety rules.

Does This Impact Power Bills?

According to government analysis, households combining solar with battery installations could save up to $2,300 annually, nearly 90% of a typical electricity bill.

In practical terms, the rebate can be up to $372 per usable kWh for systems with a capacity of up to 50 kWh. This ultimately saves thousands of dollars in total for your Aussie homes.

Moreover, in large commercial systems with capacities of 13.5 kWh or more, these typical savings can range from $3,300 to $4,000. The best part is that you can stack this program with state rebates, thereby increasing the total savings.

VIC Solar Panel Rebates, Grants & Incentives in 2025

In addition to the federal rebate, Victorians can enjoy a state rebate that reduces the initial investment cost. Here are the different types of financial incentive schemes available to Victorians at the state level.

Solar Homes Program: Solar Panel Rebates & Interest-free Loans

- Under this solar home program, households can enjoy an upfront rebate of up to $1,400 for rooftop solar PV systems. This rebate covers up to 50% of the cost of the solar installation.

- This financial aid is available to people of various categories, from owner-occupiers, renters, homes under construction, to community housing organizations.

Interest-free Loan in VIC

In addition to the $1,400 off the system, Victorians can enjoy an interest-free loan option facilitated by the state government.

An equal amount of loan will be provided to those who meet all the criteria determined by the state government. You may apply for this matching interest-free loan up to $1,400, repayable over four years with no interest or additional fees.

Here we’ve listed the eligibility criteria for this loan:

- A combined household taxable income of less than $210,000 per year.

- Owner or current occupier of the property of the installation.

- Property valuation of less than 3 million dollars.

- No existing solar PV system.

- Have not taken advantage of the solar homes program in the last 10 years.

In addition to these solar rebates, other energy efficiency schemes can help you upgrade your home with smart and energy-efficient appliances.

For instance, they offer hot water rebates of up to $1,000 for eligible heat pump or solar hot water products. If you opt for an Australian‑made product, eligibility may increase to $1,400.

These energy-efficient homes reduce energy cost, lower carbon emissions, and power your home sustainably.

New South Wales (NSW) Solar Incentives

In NSW, residents also benefit from the SRES or STC scheme, which offers a discount of around 30%. The rebate amount is typically around $2,500 for a 6.6 kW system.

Peak Demand Reduction Scheme (PDRS) | Battery Rebates

- PDRS offers $1,600 to $2,400 off battery installation costs for households with existing solar systems.

- An additional incentive of $250 to $400 is available for connecting the battery to a Virtual Power Plant (VPP). This incentive can often be claimed again after three years.

The PDRS in NSW has increased the battery installation rate compared to before. Many people claim that households with solar and battery setups can save around $1,500 annually under this scheme.

Are there any upcoming rebates available for NSW residents? Let’s check out!

SoAR (Solar for Apartment Residents) Grant

Opening from 1 December 2025, the new Solar for Apartment Residents (SoAR) grant initiative is specifically designed to help NSW communities install rooftop solar systems on multi-unit dwellings.

Here is the detail of the grant:

- Grant Name: Solar for Apartment Residents (SoAR) Grant.

- Coverage: Funds 50% of the cost of a shared solar PV system on eligible apartment buildings and other multi-unit dwellings in NSW.

- Benefit: Helps residents, including renters, lower energy bills and greenhouse gas emissions

- Current Uptake: Fewer than 2% of apartment buildings in NSW currently have solar installed.

- Why It Matters: Rising energy costs and a growing apartment population underscore the need for innovative solar solutions.

- Funding Pool: $25 million total grant funding available.

- Grant Limit: Up to $150,000 per project.

- Funding Partners: Jointly funded by the Australian Government and the NSW Government.

However, the application window opened on 28 February 2025 and will close at 5:00 pm on 1 December 2025, or sooner if the funding is fully allocated. Therefore, act quickly and apply before the portal closes.

Takeaway Thoughts

Not to mention, these government efforts and financial support present a golden opportunity for solar and battery adoption among NSW and Victorian residents.

Additionally, the generous federal incentives combined with state programs significantly reduce upfront costs, empowering households to make the switch.

These combined thoughtful efforts are also contributing to the country meeting its renewable energy targets and achieving net-zero emissions by 2050.

Wanna join this green revolution? It’s high time now!

So, if you have any questions or concerns about the solar rebates and schemes, please don’t hesitate to contact Cyanergy today.

Your Solution Is Just a Click Away

The post What Types of Government Rebates are Available for Solar Panels in VIC & NSW appeared first on Cyanergy.

What Types of Government Rebates are Available for Solar Panels in VIC & NSW

Can’t swear that this is true but hoping so.

Can’t swear that this is true but hoping so.

We must never forget.

The more visibility and the more frequent reminders we can get on this catastrophe in U.S. history the better.

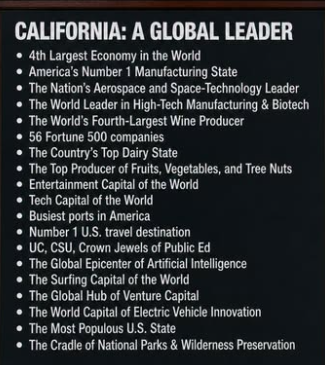

It’s almost funny when we hear that California is a socialist state, or a police state (due to our environmental restrictions), or that people are leaving in droves to go to Texas or Florida. When I come across people who say this, I wonder: have you ever actually been to California?

It’s almost funny when we hear that California is a socialist state, or a police state (due to our environmental restrictions), or that people are leaving in droves to go to Texas or Florida. When I come across people who say this, I wonder: have you ever actually been to California?

Do you know that the garden-variety 3 BR, 2 BA house here lists at about $1.2 million, where, if it were moved to, say, the Midwest, it would be worth perhaps $2500,000? Why do you think that could possibly be? Maybe the law of supply and demand doesn’t apply to the Marxist part of the nation?

Perhaps it’s because Californians are offered fantastic economic opportunities. We develop and implement ideas that improve the lives of everyone on Earth, and that we profit greatly from our undertakings.

Something for the MAGA crowd to consider.

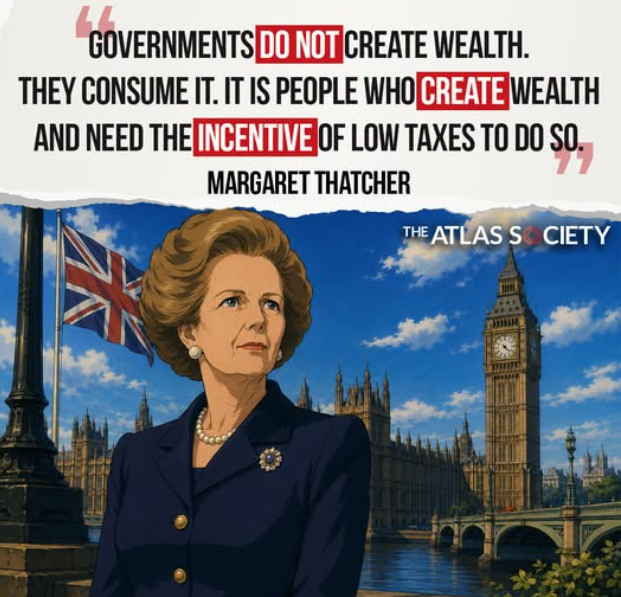

The main way governments create wealth is by educating people so that they can become productive members of society. They also build roads and airports and maintain law and order so that honest businesses can thrive.

The main way governments create wealth is by educating people so that they can become productive members of society. They also build roads and airports and maintain law and order so that honest businesses can thrive.

Anyone living now who believes that Elon Musk and Jeff Bezos are creating wealth for anyone but themselves is a total fool.

A ton of people bought into the concept expressed here in the mid-20th Century, but no semi-intelligent person today believes that tax breaks for billionaires/trillionaires generates a nickel for the common person.

World falling short on 22 of 23 nature targets for 2030, says draft UN report

Climate change is driving a ‘shift’ in childhood malaria risk across Africa

Q&A: What does China’s 15th ‘five-year plan’ for renewables mean for climate change?

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测