Critical minerals, including lithium, nickel, cobalt, copper, and rare earths, are essential in the manufacturing of clean energy technologies, spanning from wind turbines to electric vehicles (EVs). Over the last two decades, the annual trade in energy-related critical minerals has surged from $53 billion to $378 billion.

However, US imports of lithium materials and critical minerals, crucial components for EV batteries, saw a decline in 2023 compared to the previous year, per data from S&P Global Market Intelligence. This reflects the subdued demand for EVs.

In 2023, imports of processed and refined lithium totaled 17,130 and 57,210 metric tons, respectively, marking decreases of 2.4% and 20.5% compared to 2022, as reported by Market Intelligence data.

US processed lithium imports saw an uptick in the 4th quarter of 2023 following a rise in the 3rd quarter. However, import levels remained below the record high set in the March quarter of the same year.

The first quarter of 2023 witnessed a record in US imports of lithium-ion batteries as seen in the chart below. This is primarily due to market anticipation of robust EV sales for the year ahead.

Factors Behind US Import Decline of Critical Minerals

Analysts attribute the subdued sales growth in Europe and the US during the second half of 2023 to various factors. These include a higher interest rate environment and a greater price premium for battery electric vehicles compared to internal combustion engine vehicles.

However, there are expectations for an uptick in EV demand in 2024.

According to a February report by S&P Global Mobility, the development of battery-electric vehicle (BEV) sales in the US is expected to continue to grow through 2024. This projection nearly doubles the number of BEV models available by the end of the year compared to 2022.

While it’s true that growth in the global EV market has been decelerating, it’s crucial to maintain the right perspective. In 2021, EV sales more than doubled, experiencing an extraordinary growth rate of nearly 120%.

Remarkably, in January of this year, over 1.1 million EVs were sold worldwide, compared to 660,000 sold during the same period last year, marking a new monthly global sales record. This represents a remarkable 69% year-over-year growth, significantly surpassing the average growth rate observed in the previous year.

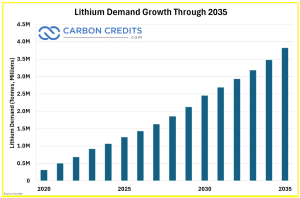

This growth trend in EV sales means lithium production must also keep up.

Trends in US Lithium Imports and Battery Market

In the fourth quarter of 2023, US imports of processed lithium totaled 4,026 metric tons, marking a 6.8% increase year over year. Market Intelligence data reveals that Argentina and Chile contributed 51.6% and 46.1% of these imports, respectively.

Raw lithium undergoes processing and subsequent refinement into chemicals suitable for use as cathode materials and electrolyte solutions in batteries. During the December quarter, the US imported 15,960 metric tons of refined lithium. That represents a 3.5% increase from the 15,426 metric tons imported during the same period in 2022.

Canada accounted for 63.4% of the US imports of refined lithium in the fourth quarter, according to the data.

According to forecasts from Commodity Insights, China would see a decline in its market share in lithium-ion battery production between 2023 and 2030.

Meanwhile, North America’s lithium-ion battery capacity is anticipated to grow at a rate of 22% during this period. The bulk of this growth would take place in the United States, with two projects also slated for Canada.

- READ MORE: Accelerating Lithium Demand and Construction Surge in US and Canada

Additionally, US imports of critical minerals amounted to 612,590 metric tons in 2023. That represents a significant decline of 39.1% year over year.

US Dependency in Critical Mineral Imports

Market Intelligence data further reveals that critical mineral imports totaled 195,805 metric tons in the 4th quarter of 2023. That accounts for a 6.6% increase from the 183,621 metric tons recorded in the fourth quarter of 2022. Notably, Gabon accounted for 47.1% of US imports of critical minerals during the same quarter.

Globally, trade in critical minerals has experienced substantial growth over the past two decades, with an average annual growth rate of 10%. The value of imports has nearly doubled in five years, soaring from $212 billion in 2017 to $378 billion in 2022, according to World Trade Organization data.

Particularly noteworthy is the significant increase in trade in helium and lithium which showed impressive annual growth rates of up to 53% during the same period.

In 2022, China emerged as the largest importer of critical minerals, comprising 33% of the global total. Following China, the European Union accounted for 16%, while Japan and the United States both stood at 11%.

The transition towards a more sustainable future necessitates access to various critical minerals vital for transitioning to the green economy. However, the US currently faces a significant reliance on imported nonfuel minerals, potentially exposing vulnerabilities in the nation’s supply chains.

According to data from the U.S. Geological Survey (USGS), the United States is entirely dependent on imports for at least 12 key minerals identified as critical by the government. Notably, China emerges as the primary source of imports for many of these critical minerals, as well as numerous others.

The graphic illustrates America’s import dependence for 30 key nonfuel minerals, highlighting the primary import sources for each mineral.

The decline in US critical minerals imports amidst EV market fluctuations underscores supply chain complexities. Despite subdued demand in 2023, projections suggest future growth. Global trade in critical minerals surges, emphasizing the need for strategic domestic resource management to secure a stable supply for the green economy.

The post US Imports of Lithium and Critical Minerals Drop Amidst Shifting EV Market appeared first on Carbon Credits.

Carbon Footprint

Thacker Pass Is Being Built: Here Is Why That Is the Best News NILI Investors Have Heard All Year.

Disseminated on behalf of Surge Battery Metals.

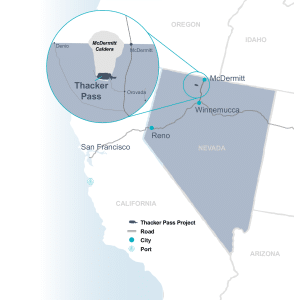

Lithium Americas (LAC) has officially broken ground at Thacker Pass, Nevada. The project is advancing toward its first production target in 2028. LAC CEO Jonathan Evans said in the company’s news release that the project should be mechanically complete by the end of 2026. Commissioning will happen through 2027, with commercial production starting in 2028.

For investors watching Nevada clay lithium, this milestone is more than an update. It’s a market signal that could change the investment landscape.

De-Risking the Clay Lithium Category

For years, clay-based lithium has faced a single recurring objection: “It has never been done at a commercial scale.” Unlike brine or hard-rock lithium, sedimentary clay deposits presented a technological and operational unknown. Investors and lenders were cautious, capital costs were higher, and early-stage projects struggled to secure financing.

Thacker Pass changes that narrative. Once LAC makes battery-grade lithium carbonate from sedimentary clay at a commercial scale, it reduces risks for the whole category. Projects in Nevada now have clear proof that clay-based lithium can be mined and processed effectively.

The historical precedent is instructive. In Chile’s Atacama region, the first brine lithium projects proved the chemistry and cost-effectiveness of large-scale lithium extraction. Later projects attracted capital more easily and on better terms. This created a ripple effect, speeding up the region’s lead in global lithium supply.

Thacker Pass is playing that same role for sedimentary clay. Its success is not just a win for LAC. It marks a key milestone for the whole Nevada clay lithium sector, including the Nevada North Lithium Project (NNLP) of Surge Battery Metals (TSX-V: NILI | OTCQX: NILIF).

Understanding the Technical Landscape

Thacker Pass Phase 1 has lithium levels of 1,500–2,500 ppm. They plan to extract it using sulfuric acid leaching to create battery-grade lithium carbonate. The project is important both geographically and operationally.

It features a large pit, a big processing facility, and integrated infrastructure. This covers access roads, water supply management, and energy sources that meet Nevada’s rules.

While Thacker Pass shows commercial viability, it is crucial to note that NNLP and Thacker Pass are not technically the same. NNLP employs a different beneficiation approach and reagent chemistry to optimize recovery.

NNLP: The Higher-Grade, Next-Generation Project

Thacker Pass shows clay lithium on a large scale. NNLP positions itself as the next evolution of this asset class, with clear geological advantages:

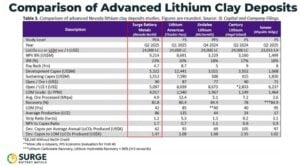

- Grade: NNLP averages 3,010 ppm lithium, significantly higher than Thacker Pass Phase 1 material. Recent drilling results show that step-out drilling found a 31-meter intercept with 4,196 ppm lithium from surface. This gives NNLP a potential extraction advantage.

- Strip Ratio: NNLP’s 1.16:1 strip ratio is among the lowest in the sedimentary clay peer group. This indicates that it has favorable material movement requirements relative to ore recovered.

- Operating Costs: NNLP’s estimated OPEX is US$5,097/t LCE, lower than Thacker Pass guidance of ~US$6,200/t C1. It suggests that it has competitive economic positioning within the peer group.

Both projects produce battery-grade lithium carbonate using sulfuric acid leaching. However, each method is customized for the specific geology of the project. NNLP is not a copy of Thacker Pass. Rather, it is a next-generation clay project designed to leverage lessons learned while improving key parameters.

Moreover, infill drilling showed a steady, thick, high-grade core. It included intercepts like 116 meters at 3,752 ppm Li and 32 meters at 4,521 ppm Li. These results support future resource expansion. They also highlight the project’s scale, quality, and technical readiness as it prepares for a Pre-Feasibility Study.

- SEE MORE: Surge Battery Metals Strengthens Nevada North With High-Grade Expansion and Infill Success

Why Category De-Risking Matters for Investors

In emerging resource sectors, de-risking is often more valuable than the resource itself. Projects that validate a new extraction method or commodity unlock several market advantages:

- Lower financing risk: Investors are more willing to fund projects once proof of concept exists.

- Improved capital terms: Lending rates and equity expectations can improve when technology and economics are validated.

- Accelerated project development: Developers can move faster, reduce contingencies, and focus on optimization rather than proving viability.

Thacker Pass’s progress effectively removes the “first-mover risk” from sedimentary clay projects. NNLP has higher grades, near-surface mineralization, and competitive OPEX. Now, it can be assessed on its own merits, not on doubts about large-scale clay processing.

Strategic Significance in the U.S. Lithium Market

The timing of Thacker Pass’s construction and NNLP’s development aligns with broader policy and market trends. Lithium is a critical input for electric vehicles, grid-scale storage, and advanced defense technologies. The U.S. government has emphasized domestic lithium production as a strategic priority.

In March 2025, President Trump signed an executive order called “Immediate Measures to Increase American Mineral Production.” This order directs federal agencies to speed up permitting and support domestic projects. It also aims to lessen dependence on foreign supply chains for critical minerals.

Projects like Thacker Pass and NNLP benefit from this policy. They provide secure domestic sources that boost the lithium supply chain.

Nevada is central to this strategy. Its clay deposits are among the largest and best in the U.S. They provide a stable base for domestic lithium production, which supports electrification goals and helps reduce reliance on imports.

Thacker Pass’s progress also sends a signal beyond the Nevada clay sector. It demonstrates that investors and capital markets are willing to back sedimentary clay projects at scale. That validation reduces perceived risk for future projects. It also speeds up permitting and development timelines as well as strengthens valuation metrics.

NNLP, with its superior grade and shallower resource, stands to benefit disproportionately. It is no longer constrained by questions of category viability. It can now be evaluated based on its geological quality, operational efficiency, and potential returns.

NNLP’s advantages, combined with the category de-risking effect of Thacker Pass, position it as a next-generation investment opportunity in Nevada’s clay lithium space.

Looking Ahead: Domestic Lithium’s Role in Energy Transition

Lithium demand is set to grow rapidly as electric vehicles, battery storage, and renewable systems expand. Securing a high-quality, domestic supply is critical to maintaining U.S. leadership in clean energy technology.

Thacker Pass proves that commercial-scale sedimentary clay lithium is achievable. NNLP demonstrates the potential for even higher efficiency and superior economics within the same category. Together, these projects show how local resources can support the energy transition while providing compelling investment opportunities.

NNLP’s higher grades, near-surface mineralization, low strip ratio, and competitive OPEX position it as a leading asset within a now-validated category.

For NILI investors, the message is clear: the clay lithium category is no longer theoretical, and NNLP is positioned to capitalize on the proof-of-concept success. The best news of the year is here—and it’s grounded in both science and strategy.

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $90,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: .

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

The post Thacker Pass Is Being Built: Here Is Why That Is the Best News NILI Investors Have Heard All Year. appeared first on Carbon Credits.

Carbon Footprint

Boeing Locks in 40,000 Tons of Soil Carbon Removal with Texas-Based Grassroots Carbon

The aviation industry is under pressure to cut emissions while demand for air travel continues to grow. Against this backdrop, Boeing’s latest agreement with Grassroots Carbon signals a clear shift in how large emitters approach climate action. Instead of relying heavily on traditional offsets, the company is now backing high-quality carbon removal rooted in nature.

This multi-year deal focuses on verified soil carbon removal. It reflects a broader industry trend: moving from compensation to actual carbon removal. More importantly, it connects climate goals with real economic benefits for rural communities.

Boeing’s Shift: From Offsets to Real Carbon Removal

Boeing’s agreement to purchase at least 40,000 metric tons of carbon removal credits marks more than just another sustainability initiative. It shows a deeper transition in its carbon strategy.

Earlier, many companies relied on carbon offsets to balance emissions. However, Boeing has refined its approach. It now follows an “avoid first, remove second” model. This means the company prioritizes cutting emissions directly—through renewable electricity and sustainable aviation fuel—before addressing the remaining footprint.

Targeting Scope 3 Emissions

Still, not all emissions can be eliminated. Business travel, classified under Scope 3 emissions, remains difficult to reduce. This is where carbon removal comes in. By investing in verified soil carbon credits, Boeing aims to tackle these residual emissions more credibly.

At the same time, this approach aligns with growing scrutiny in voluntary carbon markets. Buyers are increasingly looking for durable, science-backed solutions. Soil carbon, when properly measured and maintained, can meet these expectations.

Allison Melia, vice president, Global Enterprise Sustainability, Boeing, said:

“We’re proud to work with Grassroots to accelerate carbon-removal technology that will benefit the entire global aviation industry. Enabling the long-term growth of air travel and supporting our airline customers’ emissions reduction targets are key priorities for Boeing.”

Regenerative Ranching: Turning Soil into a Climate Asset

At the core of this agreement lies regenerative ranching—a land management approach that restores ecosystems while capturing carbon.

Unlike conventional grazing, regenerative systems mimic natural herd movements. Ranchers rotate livestock across pastures. This prevents overgrazing and allows vegetation to recover. As a result, plant roots grow deeper and stronger.

This process plays a critical role in carbon sequestration. Through photosynthesis, grasses absorb carbon dioxide from the atmosphere. They then transfer this carbon into the soil through roots and organic matter. Over time, this builds stable soil carbon that can remain stored for decades.

Additionally, grazing itself can enhance this process. When managed properly, it stimulates plant growth and increases carbon storage below ground. Studies suggest these systems can capture between 1 to 5 tons of CO2 per hectare each year.

However, the benefits go beyond carbon. Healthier soils improve water retention, reduce erosion, and support biodiversity. Ranchers also see improved productivity and greater resilience to climate extremes.

This makes regenerative ranching a rare win-win solution. It supports climate goals while strengthening agricultural systems.

Soil Carbon Credits Are Gaining Credibility

Carbon credits often face criticism for lacking transparency or permanence. However, soil carbon credits are evolving quickly.

In this case, credits are generated by tracking changes in soil carbon over time. Projects establish a baseline and then measure improvements driven by regenerative practices. Each credit corresponds to one metric ton of CO2 removed or avoided.

To ensure credibility, projects use a combination of soil sampling, satellite monitoring, and modeling. Independent verification further strengthens trust. Many of these credits meet standards set by leading registries such as Verra and the Climate Action Reserve.

Durability remains a key question. Soil carbon is considered a long-term storage solution, especially when supported by ongoing land management. In many cases, carbon can remain stored for 25 to 100 years or more.

For corporate buyers, this level of integrity is critical. It allows them to make credible climate claims while supporting real-world impact.

How Grassroots Carbon Is Scaling a Natural Climate Solution

The United States holds a unique advantage in this space. Its grasslands cover roughly 655 million acres—nearly 40% of the country’s land area. These landscapes represent one of the largest untapped carbon sinks.

If managed effectively, they could remove up to 1 billion tons of CO2 equivalent annually. That potential makes soil carbon one of the most scalable nature-based solutions available today.

Grassroots Carbon is working to unlock this opportunity. The company partners with ranchers across more than 2.2 million acres in 22 states. It supports them in adopting regenerative practices while ensuring measurable climate outcomes.

Importantly, the company focuses on scientific rigor. It measures soil carbon directly, often up to one meter deep. Then, independent third parties verify the data using recognized standards. This process ensures that each carbon credit represents real and additional carbon removal.

- The company has already delivered 1.9 million tons of verified carbon removals. A large portion of these credits has been retired by corporate buyers, reflecting strong market demand.

This scale matters. It shows that soil carbon is not just a niche solution. Instead, it can operate at a level relevant to global climate goals.

Supporting Rural Economies

Moving on, regenerative ranching supports rural communities by creating new revenue streams. Ranchers can earn income from carbon credits while improving their land. This reduces financial pressure and encourages long-term stewardship.

Moreover, healthier ecosystems provide broader benefits. Improved soil structure enhances water retention, which is critical in drought-prone areas. Restored grasslands also support wildlife habitats, including bird populations.

Grassroots Carbon works with partners such as conservation groups and research institutions to ensure these outcomes. This collaborative approach strengthens both environmental and social impact.

Aviation’s Broader Climate Challenge

The aviation sector faces one of the toughest decarbonization challenges. Unlike power generation or road transport, it cannot be easily electrified. Aircraft require high-energy-density fuels, which limit near-term options.

Sustainable aviation fuel offers a partial solution. However, supply remains limited, and costs are high. As a result, carbon removal will likely play a growing role in the sector’s strategy.

AlliedOffsets estimates that carbon credit buyers will spend around $2.27 billion per year. Aviation and energy are expected to contribute the most.

- The aviation sector alone has a budget of over $800 million per year, which is about one-third of the total.

Boeing, by supporting soil carbon projects, diversifies its approach to emissions reduction. The biggest advantage is that soil carbon removal is both scalable and immediately deployable. Unlike emerging technologies, it does not require decades of development. Instead, it builds on existing agricultural practices.

At the same time, this move sends a signal to the market. Large buyers can drive demand for high-quality carbon removal. This, in turn, encourages more investment and innovation in the space.

However, scaling this solution will require continued investment, strong verification, and supportive policies. It will also depend on maintaining trust in carbon markets. However, as demand for carbon removal grows, partnerships like this could become a cornerstone of global decarbonization efforts.

The post Boeing Locks in 40,000 Tons of Soil Carbon Removal with Texas-Based Grassroots Carbon appeared first on Carbon Credits.

Tesla has reclaimed the global electric vehicle (EV) sales crown, overtaking BYD in early 2026. In the first quarter of 2026, Tesla delivered 358,023 EVs worldwide. This figure edged out BYD’s 310,389 EV deliveries, giving Tesla back the lead in pure battery electric vehicle (BEV) sales and sending stock slightly upward.

Tesla’s sales in this period rose about 6.3% year‑over‑year, showing a rebound from slower parts of 2025. This shift matters because the EV giant lost the annual global BEV sales lead in 2025.

Last year, BYD’s annual pure electric vehicle sales were higher than Tesla’s, largely due to China’s strong EV demand and policy changes.

The recent growth in Tesla’s sales shows high demand for its main models. The Model Y and Model 3 made up most of the deliveries in Q1 2026.

Battle of the EV Titans: Tesla vs. BYD

Competition between Tesla and BYD has become one of the defining stories in global EV markets.

BYD expanded rapidly over the past few years. It has a broad lineup of EVs and plug‑in hybrids and benefits from strong domestic sales in China. In 2025, BYD reported high sales growth as it strengthened its footprint outside China.

Tesla, by contrast, focuses on a narrower range of pure EVs but scales production efficiently. It has manufacturing plants in the United States, China, and Europe. These facilities help cut costs and serve major markets more quickly.

The rivalry pushes both companies to improve pricing, technology, and production capacity. Tesla’s price cuts in some markets and BYD’s aggressive growth have kept competition tight.

The EV Boom: Markets on Overdrive

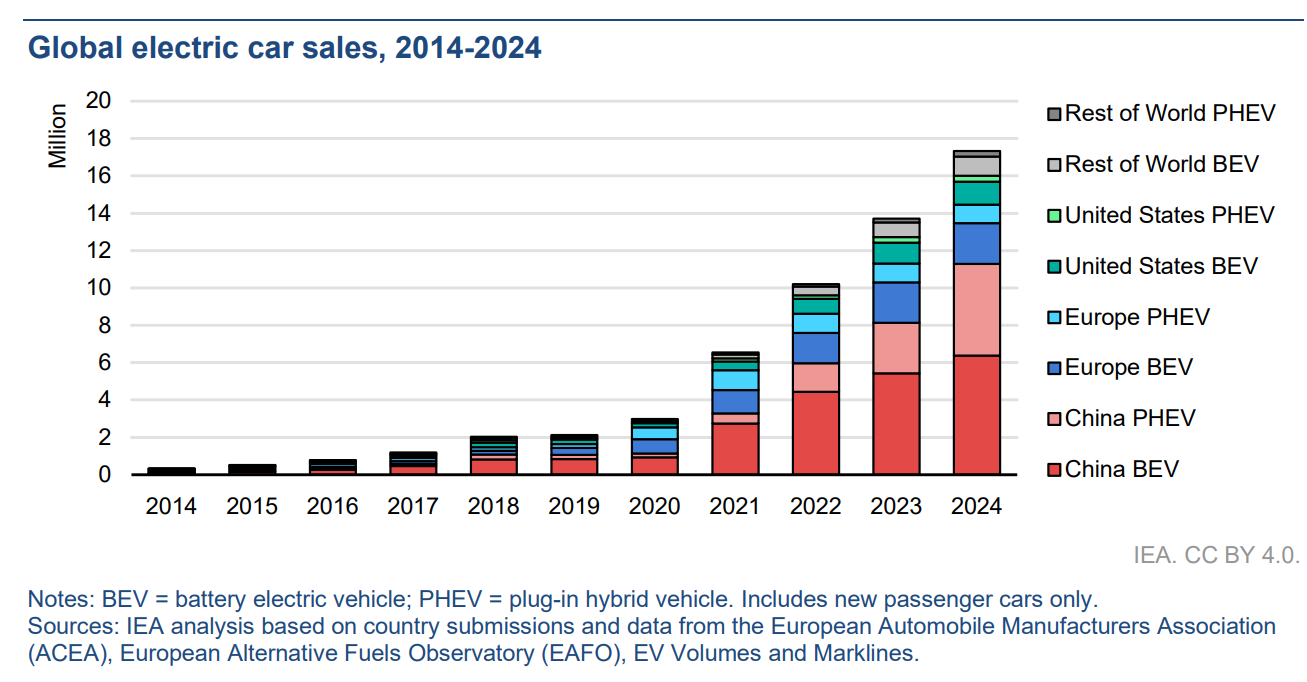

The global EV market keeps growing strongly. According to the International Energy Agency (IEA), electric car sales reached more than 17 million units globally in 2024. EVs made up more than 20% of total new car sales that year — up from earlier levels.

Data from the IEA’s Global EV Outlook 2025 shows that electric light‑duty vehicle sales are expected to reach about 40% of total vehicle sales by 2030 under current policy trends.

The stock of EVs on the road is also growing. The global EV fleet could expand to around 245 million vehicles by 2030 under stated policies.

Growth is strongest in China, Europe, and the United States. China remains the largest EV market, accounting for more than half of global EV sales in recent years.

Battery cost declines also fuel adoption. Average lithium‑ion battery prices have fallen significantly over the past decade, making electric vehicles more affordable. Governments around the world are also boosting EV uptake with incentives and stricter emissions standards.

Tesla’s Playbook: Scale, Tech, and Price Moves

Tesla’s return to the top reflects its focus on production scale and cost efficiency. The company has reduced vehicle prices in key markets to stay competitive. These price cuts helped increase demand, though they also put pressure on profit margins.

Elon Musk’s EV company continues to invest in manufacturing technology. Its “gigafactories” use advanced automation and large casting techniques to reduce production costs. Newer facilities in the U.S. and abroad help Tesla maintain output even as demand shifts.

The company is also developing next‑generation vehicles. These include plans for more affordable EV models designed to attract a wider range of buyers.

Tesla is expanding its energy business as well. This includes battery storage systems and solar products that align with the company’s broader clean energy goals.

Software remains a strength for Tesla. Features like over‑the‑air updates and driver assist systems add value for customers and differentiate Tesla’s vehicles from competitors.

Wall Street Watches, TSLA Reacts

Tesla’s stock, traded as TSLA, has shown volatility in response to sales news.

After Tesla’s delivery numbers in Q1 2026 showed the company regaining the BEV sales lead, its shares saw some short‑term gains. However, the stock has remained volatile. Broader concerns about pricing pressure, excess inventory, and competition have kept investor sentiment cautious.

In early 2026, shares pulled back after production exceeded deliveries and analysts noted weaker-than-expected margins. Tesla produced 408,386 vehicles in Q1 2026 but delivered 358,023, leaving some inventory unsold. This gap contributed to stock pressure.

Despite these swings, Tesla remains one of the highest‑valued automakers in the world. Its market capitalization continues to reflect expectations about future EV adoption and the company’s role in clean energy.

Market watchers note that Tesla’s ability to maintain leadership in BEV sales affects its valuation. Strong delivery figures help support confidence in Tesla’s long‑term strategy, even as competition increases.

Beyond sales and competition, Tesla’s EVs also play a key role in the global effort to reduce carbon emissions and fight climate change.

EVs Fighting Climate Change, One Mile at a Time

Electric vehicles help cut carbon emissions from transport. Road transport is a major source of energy‑related emissions. In recent years, EVs made up more than 20% of global car sales, according to the IEA.

EVs reduce oil demand and lower emissions. The global EV fleet could rise to nearly 245 million vehicles by 2030 under stated policy scenarios, significantly displacing traditional gasoline and diesel cars.

As EV adoption grows, the carbon intensity of the electricity grid becomes more important. EVs charged with cleaner power produce larger net emission benefits.

Even with mixed grid emissions, EVs still reduce lifetime greenhouse gas output compared with internal combustion vehicles.

Governments around the world support EV adoption with stricter fuel standards, tax incentives, and expanded charging networks. These policies help ensure electric vehicles contribute to global decarbonization and climate goals.

Outlook: Growth, Competition, and Innovation

The EV market is expected to grow strongly in the coming years. Demand is supported by climate goals, advancing technology, and consumer interest in cleaner mobility.

Tesla’s return to the top in early 2026 shows that it remains a central player in the electric transition. Its focus on pure electric vehicles, global scale, and continuous innovation continues to fuel its position.

However, the gap between Tesla and competitors like BYD is narrowing. BYD’s strong EV growth, especially in China and expanding export markets, shows that competition remains intense.

Future leadership in the EV industry will depend on cost, technology, charging infrastructure, and the ability to scale production efficiently. Companies that balance these factors well will shape the next phase of the global EV market.

For now, Tesla’s rebound highlights both the rapid growth of the sector and the increasing intensity of competition among the world’s leading EV makers.

The post Tesla Reclaims EV Sales Crown from BYD in Q1 2026, Heating Up the EV Race appeared first on Carbon Credits.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits