Lithium, a critical element in modern technology, has become a focal point in discussions about renewable energy and electric vehicles (EVs) due to its importance in batteries. The fluctuating prices of lithium have significant implications for industries and economies worldwide. This article explores the dynamics of lithium pricing, offering insights into historical trends, current market conditions, future predictions, and the key factors that drive its valuation.

Background Information

Lithium is a soft, silvery-white metal belonging to the alkali metal group. It is highly reactive and flammable, making it essential in various industrial applications. Most notably, lithium-ion batteries power everything from smartphones to electric vehicles.

The demand for lithium has surged with the rise of renewable energy technologies and the global push towards reducing carbon emissions. Lithium’s unique properties make it irreplaceable in high-performance batteries, which are pivotal in energy storage solutions and portable electronics.

Lithium is also on several countries’ Critical Minerals lists, such as the U.S., Canada, and Australia.

Historical Lithium Price Trends

Lithium prices have seen dramatic changes over the past decade. From 2010 to 2015, prices remained relatively stable, with minor fluctuations due to steady demand and supply conditions. However, from 2015 onwards, prices began to soar, driven by the booming EV market and increased demand for renewable energy storage solutions.

By 2017, lithium prices had tripled compared to their 2015 levels. This spike was primarily due to the rapid expansion of China’s EV market and increased lithium mining and production investments.

The year 2018 saw prices peaking, but by 2019, an oversupply in the market led to a sharp decline. From 2019 to 2021, prices remained subdued, reflecting a period of market correction and stabilization.

In 2022, however, a record-breaking price rally occurred due to a large supply deficit. Lithium’s largely agreement-based supply model also contributed to this squeeze, sending lithium prices skyrocketing over 5x. This push would continue until midway through the year as China re-implemented full lockdowns nationwide due to rising COVID-19 case numbers, leading to a brief economic slowdown.

While the end of lockdowns coincided with another surge in demand, sending lithium prices to their all-time high of 575,000 CNY (USD 80,000) per tonne, this rally was short-lived. With inflation rates on the rise and EV supply finally overtaking demand, lithium prices plummeted back down in 2023 before stabilizing around the 100,000 CNY (USD 14,000) level, where it continues to trade today.

The past few years have been marked by significant market adjustments. Producers ramped up supply, anticipating continuous high demand, but the market did not grow as quickly as expected.

Consequently, this led to a surplus, driving prices down. Moreover, technological improvements in mining and processing lithium contributed to cost reductions, which also played a role in lowering market prices during this period.

Lithium Price Volatility

One of the main factors contributing to the volatility of lithium prices is that unlike other minerals like gold or copper, the lithium markets are still fairly young and hence the spot market is not very well established. With the recent explosive growth in lithium demand added on top of that, the result is a market sector that’s very much still going through growing pains.

Right now, instead of purchasing contracts for delivery on a spot market most lithium consumers choose to directly sign long-term offtake agreements with lithium miners, securing a guaranteed supply at a fixed price. The current state of the lithium markets has drawn parallels to the iron ore market prior to the 2010s, where pricing would follow an annual benchmark negotiated between miners and steelmakers each year.

In the early 2000s, explosive growth in iron ore demand from China was the catalyst that finally led to change in the iron ore markets. It would take a concerted effort from BHP and other top miners for the iron ore markets to shift towards the spot pricing model it follows today.

Something similar is happening in the lithium markets, with top producer Albemarle having begun holding auctions for its mined lithium since March 2024. These auctions allow buyers to secure pricing that’s more truly reflective of the present supply-demand dynamic, as opposed to being forced to lock in fixed long-term pricing to avoid not having enough supply.

Albemarle plans on holding auctions every two weeks in order to provide more timely and consistent data on lithium pricing.

Albemarle plans on holding auctions every two weeks in order to provide more timely and consistent data on lithium pricing.

The lithium spot market has been seeing increasing activity as well, as shown in the chart above. In conclusion, while lithium prices will likely continue to be volatile for the foreseeable future, there are changes under way that will help stabilize the market as it matures and develops.

Current Market Analysis

As of 2024, lithium prices have stabilized from their major plunge of 2022-2023. The current price is attributed to several factors:

- Increased Demand: The global shift towards electrification and decarbonization has accelerated the demand for lithium-ion batteries. EVs, energy storage systems, and consumer electronics continue to drive this demand. The Paris Agreement and other international efforts to curb carbon emissions have further intensified the focus on lithium as a key resource for achieving climate goals.

- Supply Chain Dynamics: While demand is rising, supply chain disruptions have hindered the steady flow of lithium. These disruptions are caused by geopolitical tensions, logistical challenges, and regulatory hurdles in major lithium-producing countries. For instance, political instability in regions like South America, where a significant portion of lithium is mined, has led to production slowdowns and export restrictions. However, there is still a significant surplus of lithium supply to work through.

- Technological Advancements: Innovations in battery technology, such as solid-state batteries, promise higher efficiency and longer life cycles. These advancements have spurred further investment in lithium production, contributing to the current price dynamics. Additionally, advancements in extraction technologies, such as direct lithium extraction (DLE), are expected to enhance the efficiency and environmental sustainability of lithium production.

The increased focus on domestic production in countries like the United States and Australia is also reshaping the market landscape. Efforts to reduce dependence on imported lithium are driving investments in local mining projects, which, in turn, affect global supply and pricing dynamics.

Future Price Predictions

Looking ahead, the future of lithium prices is shaped by a combination of technological, economic, and geopolitical factors.

Analysts predict that demand for lithium will continue to grow, driven by several key trends:

Analysts predict that demand for lithium will continue to grow, driven by several key trends:

- Expansion of the EV Market: With governments worldwide setting ambitious targets for EV adoption, the demand for lithium is expected to skyrocket. For instance, the European Union aims to phase out internal combustion engine vehicles by 2035, significantly boosting lithium demand. Major automakers are also announcing aggressive plans to electrify their fleets, further driving demand.

- Advancements in Energy Storage: Beyond EVs, the need for efficient energy storage solutions in renewable energy systems will drive lithium demand. Solar and wind energy projects increasingly rely on lithium-ion batteries for energy storage, ensuring a steady demand. The development of grid-scale storage solutions is particularly significant, as it addresses the intermittency issues associated with renewable energy sources.

- Sustainable Mining Practices: The push for sustainable and ethical mining practices may impact the supply side. While this could constrain supply in the short term, it is expected to ensure a stable and environmentally friendly lithium supply in the long run. Innovations in recycling technologies and the development of closed-loop systems are also expected to play a crucial role in meeting future demand sustainably.

Factors Affecting Lithium Prices

Several factors influence lithium prices, creating a complex and dynamic market landscape:

- Supply and Demand Dynamics: The fundamental economics of supply and demand play a crucial role. Any imbalance, such as oversupply or undersupply, directly affects prices. For example, the rapid development of new mining projects can lead to temporary oversupply, depressing prices until demand catches up.

- Geopolitical Factors: Lithium-rich countries, such as Australia, Chile, and Argentina, play a significant role in the global supply chain. Political stability and regulatory policies in these regions can impact lithium prices. Trade policies, tariffs, and international agreements also influence the global flow of lithium and its pricing.

- Technological Developments: Breakthroughs in battery technology can influence lithium demand. For example, the development of alternative battery chemistries could reduce reliance on lithium, affecting its price. Conversely, improvements in lithium extraction and processing technologies can increase supply efficiency and reduce production costs, impacting prices favorably.

- Environmental Regulations: Stricter environmental regulations on mining practices can limit supply and drive up prices. Conversely, advancements in sustainable mining techniques can stabilize prices. The growing emphasis on reducing the environmental footprint of lithium extraction is prompting the industry to adopt greener practices, which may initially increase costs but lead to long-term sustainability.

Key Players in the Lithium Market

The global lithium market is dominated by a few key players who control a significant share of the mined supply. Here are five of the top producers from 2023, who combined for roughly half of total global production:

- Albemarle Corporation: Currently the world’s largest lithium producer, Albemarle operates major lithium mining projects in Australia and the United States. The company has invested heavily in expanding its production capacity to meet rising demand.

- SQM (Sociedad Química y Minera de Chile): Based in Chile, SQM, the world’s second largest producer, is known for its extensive lithium brine operations in the Atacama Desert. The company has leveraged its strategic location and technological expertise to become a dominant player in the market.

- Ganfeng Lithium: A Chinese company, Ganfeng is a major player in the lithium market, with operations spanning from mining to battery production. The company’s vertically integrated business model allows it to control the entire supply chain, ensuring stable supply and competitive pricing.

- Tianqi Lithium: Another Chinese giant, Tianqi, has significant stakes in lithium mining operations globally, including the Greenbushes mine in Australia. The company’s strategic investments and partnerships have positioned it as a key supplier in the global market.

- Arcadium Lithium: A vertically integrated lithium company formed from a merger between American refiner Livent and Australian miner Allkem, Arcadium focuses on high-quality lithium compounds used in batteries and other applications. The company’s commitment to innovation and sustainability has made it a preferred supplier for many high-tech industries.

Challenges and Opportunities

The lithium market faces several challenges and opportunities that will shape its future:

Challenges:

- Environmental Impact: Lithium mining has significant environmental repercussions, including water usage and habitat destruction. Addressing these concerns is crucial for sustainable growth. The industry is under increasing scrutiny to minimize its environmental footprint and adopt greener practices. Expect to see a more pronounced price premium for “green” sustainable lithium once the market matures further.

- Market Volatility: Fluctuations in supply and demand combined with the infancy of the lithium markets can lead to volatile prices, making it challenging for investors and producers to plan long-term strategies. The cyclical nature of commodity markets adds to the unpredictability, requiring robust risk management practices.

- Technological Risks: Dependence on lithium-ion technology poses a risk if alternative battery technologies emerge, potentially reducing lithium demand. The rapid pace of technological innovation necessitates continuous adaptation and investment in research and development.

Opportunities:

- Technological Innovation: Advancements in mining and processing technologies can enhance efficiency and reduce environmental impact. Innovations such as direct lithium extraction (DLE) and improved recycling techniques are expected to revolutionize the industry.

- Strategic Investments: Investing in lithium recycling and alternative sources can diversify supply and stabilize the market. Developing secondary sources of lithium, such as extracting lithium from geothermal brines or recycling used batteries, offers promising avenues for ensuring supply security.

- Global Collaboration: International cooperation on sustainable mining practices and environmental regulations can ensure a stable and ethical lithium supply chain. Collaborative efforts among governments, industry players, and environmental organizations can drive the adoption of best practices and foster a resilient market.

Types of Lithium Companies: Technology, Exploration, Production, Extraction, Refining

The lithium industry comprises various types of companies, each playing a crucial role in the supply chain. These companies can be broadly categorized into technology, exploration, production, extraction, and refining. Understanding the distinct roles and contributions of each type is essential for grasping the complexity of the lithium market.

-

Technology Companies

Role and Contribution: Technology companies are pivotal in the development and advancement of lithium battery technologies. These firms focus on enhancing the performance, efficiency, and safety of lithium-ion batteries. Innovations by technology companies drive the demand for lithium by creating new applications and improving existing ones.

Examples:

- Tesla: Known for its electric vehicles (EVs), Tesla also invests heavily in battery technology through its Gigafactories, which produce lithium-ion batteries for both EVs and energy storage systems.

- Panasonic: Partnering with Tesla, Panasonic manufactures lithium-ion batteries, focusing on improving energy density and reducing costs.

Impact: Technology companies push the boundaries of battery capabilities, influencing the overall demand for high-quality lithium and driving advancements that make renewable energy solutions more viable and efficient.

-

Exploration Companies

Role and Contribution: Exploration companies are responsible for discovering new lithium deposits. These firms conduct geological surveys, drilling, and sampling to identify potential lithium reserves. Exploration is the first step in the lithium supply chain, determining future supply availability.

Examples:

- LiFT Power Corp: An exploration company focused on developing its lithium project in Northwest Territories, Canada, aiming to establish a domestic North American supply of lithium.

Impact: Successful exploration leads to the development of new lithium mines, increasing the global supply of lithium and potentially stabilizing prices. These companies are crucial for ensuring a steady pipeline of lithium resources to meet future demand.

-

Production Companies

Role and Contribution: Production companies are involved in the extraction of lithium from mines and brine sources. They manage the operations of lithium mines and are responsible for bringing raw lithium materials to the market.

Examples:

- Albemarle Corporation: The world’s largest lithium producer in 2023 with operations in Australia and the USA, Albemarle is a key supplier of lithium compounds to various industries.

- SQM (Sociedad Química y Minera de Chile): Operating extensive lithium brine extraction facilities in the Atacama Desert, SQM is a leading global producer of lithium.

Impact: Production companies are the backbone of the lithium supply chain, ensuring that sufficient quantities of lithium are available to meet industrial and consumer needs. Their production capacities and efficiencies directly influence lithium prices and availability.

-

Extraction Companies

Role and Contribution: Extraction companies specialize in the technologies and processes used to extract lithium from raw materials. These firms develop and implement methods for efficiently and sustainably extracting lithium from both hard rock (spodumene) and brine sources.

Examples:

- Standard Lithium: Known for its proprietary extraction technology that aims to streamline the lithium extraction process and increase efficiency.

Impact: Advancements in extraction technology by these companies can significantly lower production costs and environmental impact, making lithium more accessible and sustainable. Efficient extraction processes are essential for meeting growing demand while minimizing ecological footprints.

-

Refining Companies

Role and Contribution: Refining companies are responsible for processing raw lithium materials into high-purity lithium compounds that are suitable for use in batteries and other applications. These companies ensure that the lithium meets stringent quality standards required by technology and battery manufacturers.

Examples:

- Ganfeng Lithium: A vertically integrated company that not only mines lithium but also refines it into battery-grade compounds.

- Tianqi Lithium: Engages in refining lithium to produce battery-grade lithium hydroxide and carbonate, supplying major battery manufacturers.

Impact: Refining companies add value by transforming raw lithium into a usable form, ensuring a consistent supply of high-quality lithium to downstream industries. Their operations are critical for maintaining the supply chain’s integrity and meeting the specifications required for advanced lithium-ion batteries.

Conclusion

Lithium prices are influenced by a myriad of factors, from technological advancements and supply chain dynamics to geopolitical and environmental considerations. The future of lithium pricing looks promising, with growing demand driven by the global shift towards electrification and renewable energy.

However, addressing the challenges of sustainable production and market volatility will be crucial for long-term stability. As the world continues to embrace green technologies, lithium remains a critical component in the journey towards a sustainable future.

References and Further Reading

- Lithium Market Overview and Trends. (2023). International Energy Agency. https://www.iea.org/reports/critical-minerals-market-review-2023/key-market-trends#abstract.

- The Future of Lithium: Supply, Demand, and Prices. (2023). BloombergNEF (https://about.bnef.com/blog/the-future-of-lithium-supply-demand-and-pr)

The post Understanding Lithium Prices: Past, Present, and Future appeared first on Carbon Credits.

ChatGPT developer OpenAI has paused its flagship UK data center project, known as “Stargate UK,” citing high energy costs and regulatory uncertainty. The project was part of a broader £31 billion ($40+ billion) investment plan aimed at expanding artificial intelligence (AI) infrastructure in the country.

The initiative was designed to deploy up to 8,000 GPUs initially, with plans to scale to 31,000 GPUs over time. It was aimed to boost the UK’s “sovereign compute” capacity. This means building local infrastructure to support AI development and reduce reliance on foreign systems.

However, the company has now paused development. An OpenAI spokesperson stated that they:

“…support the government’s ambition to be an AI leader. AI compute is foundational to that goal – we continue to explore Stargate UK and will move forward when the right conditions such as regulation and the cost of energy enable long-term infrastructure investment.”

Energy Costs Are Now a Core Constraint

The main issue is energy. AI data centers require large amounts of electricity to run GPUs and cooling systems.

In the UK, industrial electricity prices are among the highest in developed markets. Recent estimates show costs at around £168 per megawatt-hour, compared to £69 in France and £38 in Texas. This gap creates a major disadvantage for large-scale data center investments.

AI workloads are especially power-intensive. A single large data center can consume as much electricity as tens of thousands of homes. As AI adoption grows, this demand is rising quickly.

Globally, the International Energy Agency estimates that data centers could consume over 1,000 terawatt-hours (TWh) of electricity by 2030, up sharply from about 415 TWh in 2024. This growth is largely driven by AI.

The result is clear. Energy is no longer just a cost. It is a key factor in where AI infrastructure gets built.

Regulation Adds Another Layer of Risk

Energy is only part of the challenge. Regulation is also slowing investment. In the UK, uncertainty around AI rules, especially copyright laws for training data, has created hesitation among companies.

Earlier proposals to allow AI firms to use copyrighted content were withdrawn after backlash. This left companies without clear guidance on compliance.

For large infrastructure projects, this uncertainty increases risk. Data centers require billions in upfront investment. Companies need stable rules before committing capital.

Planning delays and grid connection timelines also add friction. These factors increase both cost and project timelines.

Together, energy costs and regulatory uncertainty create a difficult environment for hyperscale AI infrastructure.

OpenAI’s Global Infrastructure Expands, But More Selectively

Despite the pause, ChatGPT-maker is still expanding globally. The company is investing heavily in AI infrastructure through partnerships with Microsoft, NVIDIA, and Oracle. It is also linked to a much larger $500 billion “Stargate” initiative in the United States, focused on building next-generation AI data centers.

At the same time, the company faces rising costs. Reports suggest OpenAI could lose billions of dollars annually as it scales infrastructure to meet demand.

This reflects a broader industry shift. AI is becoming more like energy or telecom infrastructure. It requires large capital investment, long timelines, and stable operating conditions.

The pause also highlights a deeper issue. AI growth is increasing pressure on energy systems and the environment.

The Hidden Carbon Cost Behind Every AI Query

ChatGPT and similar tools rely on large data centers. These facilities already account for about 1% to 1.5% of global electricity use. Projections for their energy use vary widely due to various factors.

Each individual query may seem small. A typical ChatGPT request can use about 0.3 watt-hours of electricity, which is relatively low. However, usage at scale changes the picture.

ChatGPT now serves hundreds of millions of users. Even small energy use per query adds up quickly. Training models is even more energy-intensive. For example, training GPT-3 required about 1,287 megawatt-hours of electricity and produced roughly 550 metric tons of CO₂.

Newer models are even larger. Some estimates suggest training advanced models like GPT-4 could emit up to 15,000 metric tons of CO₂, depending on the energy source.

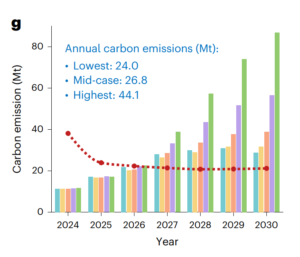

At the system level, the impact is growing fast. AI systems could generate between 32.6 and 79.7 million tons of CO₂ emissions in 2025 alone. By 2030, AI-driven data centers could add 24 to 44 million tons of CO₂ annually.

Looking further ahead, global generative AI emissions could reach up to 245 million tons per year by 2035 if growth continues. These numbers show a clear pattern. Efficiency is improving, but total demand is rising faster.

Big Tech Scrambles to Balance AI Growth and Emissions

OpenAI has not published a detailed standalone net-zero target. However, its operations rely heavily on partners such as Microsoft, which has committed to becoming carbon negative by 2030.

The company has acknowledged that energy use is a real concern. Leadership has pointed to the need for more renewable energy, including nuclear and clean power, to support AI growth.

Across the industry, companies are responding in several ways:

- Improving model efficiency to reduce energy per query

- Investing in renewable energy and long-term power contracts

- Exploring new cooling systems to reduce water and energy use

Efficiency gains are already visible. Some AI systems have reduced energy per query by more than 30 times within a year, showing how quickly technology can improve. Still, total emissions continue to rise because demand is scaling faster than efficiency gains.

The Global AI Infrastructure Race

The pause in the UK highlights a larger trend. AI infrastructure is becoming a global competition shaped by energy, policy, and cost.

Regions with lower energy prices and faster permitting processes have an advantage. The United States and parts of the Middle East are attracting large-scale AI investments due to cheaper power and supportive policies.

At the same time, governments are trying to attract these projects. The UK has pledged billions to support AI growth and improve compute capacity. But this case shows that policy ambition alone is not enough. Companies need reliable energy, clear rules, and predictable costs.

AI’s Next Phase Will Be Decided by Energy, Not Code

The decision by OpenAI does not signal a retreat from AI investment. Instead, it reflects a shift in priorities.

Companies are becoming more selective about where they build infrastructure. They are focusing on locations that offer the right mix of energy access, cost stability, and regulatory clarity.

The UK project may still move forward, but only if conditions improve. For now, the message is clear. The future of AI will not be shaped by technology alone. It will also depend on energy systems, policy frameworks, and long-term investment conditions.

The post OpenAI Hits Pause on $40B UK AI Project: Energy Costs Shake Data Center Economics appeared first on Carbon Credits.

Uranium Energy Corporation (NYSE: UEC) has started production at its Burke Hollow project in South Texas. This is the first new uranium mine to open in the U.S. in over ten years.

The project started production in April 2026 after getting final regulatory approval. This marks a big step for domestic uranium supply. It’s also the world’s newest in-situ recovery (ISR) uranium mine, which shows a move toward less harmful extraction methods.

Burke Hollow was originally discovered in 2012 and spans roughly 20,000 acres, with only about half of the site explored so far. This suggests significant long-term expansion potential as additional wellfields are developed.

The mine’s output will go to UEC’s Hobson Central Processing Plant in Texas. This plant can produce up to 4 million pounds of uranium each year.

A Scalable ISR Platform Expands U.S. Uranium Capacity

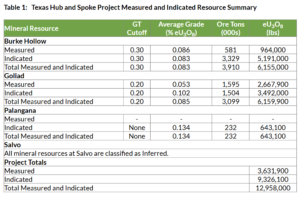

The Burke Hollow launch transforms UEC into a multi-site uranium producer in the United States. The company runs two active ISR production platforms. The second one is at its Christensen Ranch facility in Wyoming; both are shown in the table from UEC.

This “hub-and-spoke” model allows uranium from multiple wellfields to be processed through centralized facilities, improving efficiency and scalability. UEC’s operations in Texas and Wyoming are now active. This gives them a licensed production capacity of about 12 million pounds per year across the U.S.

ISR mining plays a key role in this strategy. Unlike conventional mining, ISR involves circulating solutions underground to dissolve uranium and pump it to the surface. This reduces surface disturbance and can lower environmental impact compared to open-pit or underground mining.

Burke Hollow is the largest ISR uranium discovery in the U.S. in the last ten years. This boosts its long-term value as a domestic resource.

Unhedged Strategy Pays Off as Uranium Prices Rise

UEC’s production launch comes at a time of strong uranium market conditions. The company uses a fully unhedged strategy. This means it sells uranium at current market prices instead of securing long-term contracts.

This approach has recently delivered strong financial results. In early 2026, UEC sold 200,000 pounds of uranium for $101 each. This price was about 25% higher than average market rates. The sale brought in over $20 million in revenue and around $10 million in gross profit.

The strategy allows the company to benefit directly from rising uranium prices, which have been supported by:

- Growing global nuclear energy demand

- Supply constraints in key producing regions

- Increased long-term contracting by utilities

Unhedged exposure raises risk in downturns, but offers more upside in strong markets. UEC is currently taking advantage of this.

Nuclear Energy Growth Is Driving Demand for Uranium

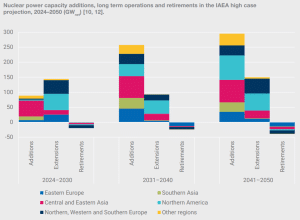

The timing of Burke Hollow’s launch aligns with a broader global shift back toward nuclear energy. Governments are increasingly turning to nuclear power as a reliable, low-carbon energy source.

The International Atomic Energy Agency projects that global nuclear capacity could double by 2050, depending on policy and investment trends. This would require a significant increase in uranium supply.

In the United States, nuclear energy accounts for around 20% of electricity generation. It also produces zero carbon emissions during operations. This makes it a key component of many net-zero strategies.

There are several factors supporting renewed nuclear demand, including:

- Development of small modular reactors (SMRs)

- Extension of existing nuclear plant lifetimes

- Government funding to maintain nuclear capacity

- Rising electricity demand from data centers and electrification

As demand grows, securing a reliable uranium supply becomes increasingly important.

Reducing Import Risk: A Strategic Domestic Supply Push

The Burke Hollow project also addresses a major vulnerability in U.S. energy policy. The country currently imports about 95% of its uranium needs, leaving it exposed to global supply risks.

A large share of uranium production and enrichment capacity is concentrated in a few countries, including Russia and Kazakhstan. This concentration has raised concerns about supply disruptions and geopolitical risk.

By expanding domestic production, UEC is helping to reduce reliance on imports and strengthen the U.S. nuclear fuel supply chain.

The company’s broader strategy includes building a vertically integrated platform covering mining, processing, and, eventually, uranium conversion. This approach aligns with U.S. government efforts to rebuild domestic nuclear fuel capabilities.

Federal programs have allocated billions to boost uranium production and enrichment. This shows how important the sector is.

Two Hubs, One Strategy: Wyoming Supports the Texas Breakthrough

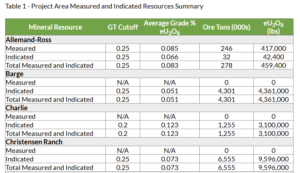

While Burke Hollow is the main focus, UEC’s Christensen Ranch operation in Wyoming remains an important part of its production base.

The Wyoming site has recently received approvals for expanded wellfield development, allowing it to increase output alongside the Texas operation.

Together, the two sites form the foundation of UEC’s dual-hub production model. However, it is the Texas project that marks the first new U.S. uranium mine in over a decade, making it the central milestone in the company’s growth strategy.

Investor Momentum Builds Around Uranium Revival

The restart of U.S. uranium production is drawing strong attention from investors and industry players. Uranium markets have tightened in recent years, driven by rising demand and limited new supply.

UEC’s production launch has already had a positive market impact. The company’s share price rose following the announcement, reflecting investor confidence in its growth strategy.

At the same time, utilities are increasing long-term contracting activity to secure fuel supply. This trend is expected to continue as new nuclear capacity comes online and existing plants extend operations.

Industry forecasts suggest that uranium demand will remain strong through the 2030s, supporting higher prices and increased investment in new production.

Lower Impact Mining, Higher ESG Expectations

The use of ISR mining at Burke Hollow reflects a broader shift toward more sustainable extraction methods. ISR typically reduces land disturbance and avoids large-scale excavation.

However, environmental management remains critical. Key issues include groundwater protection, chemical use, and long-term site restoration.

UEC has emphasized environmental controls and regulatory compliance in its operations. These efforts are important for maintaining social license and meeting ESG expectations.

From a climate perspective, uranium production plays an indirect but important role. Supporting nuclear energy, it helps enable low-carbon electricity generation and reduces reliance on fossil fuels.

The Bottom Line: A Defining Moment for U.S. Uranium Production

The launch of the Burke Hollow mine marks a major milestone for the U.S. uranium sector. It ends a decade-long gap in new mine development and signals renewed momentum in domestic production.

In the short term, it strengthens supply and supports rising uranium markets. In the long term, it highlights the growing role of nuclear energy in global decarbonization strategies.

UEC’s Burke Hollow shows that new uranium projects can advance in today’s market. There are still challenges, like scaling production and handling environmental risks, but progress is possible.

As demand for nuclear energy continues to grow, domestic projects like Burke Hollow will play a key role in shaping the future of energy security and low-carbon power.

The post U.S. Uranium Mining Returns: UEC Launches First New Mine in a Decade appeared first on Carbon Credits.

Carbon Footprint

Carbon Market 2026: Supply Squeeze Pushes Premium Carbon Credit Prices Up, Sylvera Finds

The global carbon market is changing fast in 2026. The latest insights from Sylvera’s State of Carbon Credits report show a clear shift. Volumes are falling, but value is holding steady. This means buyers now focus more on quality than quantity.

Furthermore, the market is splitting into two clear segments. High-quality credits are in demand and sell at higher prices. Older or lower-quality credits are losing interest. This divide is growing stronger and shaping how the market will evolve in the coming years.

Shell’s Sharp Cut Pulls Down Market Volumes

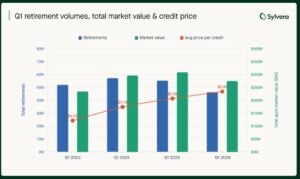

Carbon credit retirements reached 51 million in the first quarter of 2026. This is down from 55.3 million in the same period last year. The total market value also fell slightly to $290 million, compared to $309 million a year ago.

Despite this decline, prices did not weaken. The average price per credit increased to $5.69 from $5.60. This shows that buyers are willing to pay more for credits they trust.

Interestingly, a major reason for the drop in volumes was reduced activity from Shell. The company sharply cut its purchases. It retired just 494,000 credits in Q1 2026, compared to 6.7 million in Q1 2025 and 5.6 million in 2024. This single change had a large impact on the overall market.

Value Now Drives the Market

The carbon market now runs on a simple idea. Value matters more than volume. Buyers want credits that deliver real environmental impact. They prefer projects with clear data, strong verification, and proven results.

High-quality credits now define the market. These credits meet strict standards and often align with compliance systems. Because of this, they command higher prices and stronger demand.

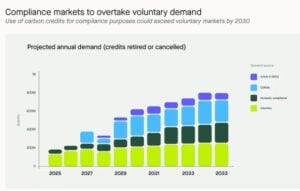

This shift is also linked to the rise of compliance markets. Programs like CORSIA are increasing demand for reliable credits. As a result, voluntary buyers and compliance buyers now compete for the same supply.

Experts expect this trend to grow stronger. Compliance demand could surpass voluntary demand by 2027. This will increase pressure on supply and push premium credit prices higher.

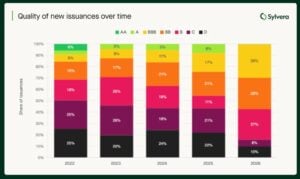

The report highlighted that, investment-grade credits (BBB+) now command an average of $20.10 per credit in Q1 2026, up from $18.10 in Q1 2025, as shown in the image below:

Recap of 2025 Carbon Market

Compliance programs made up 24% of total retirements in 2025. According to Sylvera, this share is rising fast. It is expected to go beyond voluntary demand by 2027. This growth is mainly driven by CORSIA Phase 1 rules and the expansion of domestic carbon markets.

This means compliance demand is set to change the carbon market in a big way. Soon, both voluntary buyers and regulated systems will compete for the same high-quality credits. This is already making supply tighter and more competitive.

At the same time, international trading under Article 6 gained momentum. In 2025, around 20 new bilateral agreements were signed, and the first large-scale carbon credit trades took place. This shows that global carbon transfer systems are now becoming active in practice.

However, the system is also becoming more complex. One key factor is “corresponding adjustments,” which now decide whether a credit is fully acceptable in compliance markets. In addition, countries like China, Japan, Brazil, and Indonesia are building their own domestic carbon systems.

These systems are expected to create strong new demand, but they also add more rules and complexity to the market.

Supply Crunch Becomes the Key Challenge

However, Sylvera has flagged a different scenario for his year. Supply is now the biggest issue in the market. High-quality credits are becoming harder to find. Many credits exist, but not all meet strict requirements.

Furthermore, the main bottleneck is coming from approvals under Article 6. These rules govern international carbon trading. Delays in approvals mean many credits cannot yet enter the market. Now this creates a gap. Supply looks strong on paper, but usable supply remains limited. This shortage keeps prices firm and supports premium credits.

CORSIA Supply Expands, But Not Enough

There has been progress in aviation supply. Eligible credits under CORSIA reached 32.68 million. This is more than double last year’s level.

These credits come from major registries like Verra, Gold Standard, and ART TREES. However, supply still falls short in practice. Not all credits meet full compliance standards. This keeps the market tight and competitive.

Moving on, the question is what’s driving market growth.

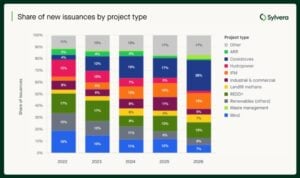

Cookstoves Drive Market Growth

Cookstove projects are growing quickly. Their share increased from 17% in 2025 to 26% in Q1 2026. Africa leads this segment. Around 80% of the supply comes from the region. Most of these projects also meet compliance requirements under CORSIA.

Quality is improving in this category. Developers are moving away from older methods. They now use stronger, data-driven approaches. This shift improves trust and attracts more buyers.

Other projects:

- REDD+ Regains Trust: Forestry projects under REDD+ are making a comeback. Their share of retirements rose to 25% in Q1 2026. These projects faced heavy criticism in the past. However, new rules and better standards are restoring confidence. Updated methodologies have removed weaker credits. This has improved the overall quality of supply. Global policy clarity has also helped. Buyers now have more confidence in using REDD+ credits in compliance markets. This has supported demand.

- Waste management projects: They are growing in importance, and their share reached 10% of total retirements, the highest so far. Landfill methane projects are leading this growth. These projects are easier to measure and verify. They also meet compliance standards. Buyers are now exploring options beyond traditional sectors. Waste projects offer a reliable and practical solution.

New Credit Types Expand the Market

Several new project types are growing fast. They are adding fresh supply and attracting new buyers.

- Clean water projects have seen strong growth in recent years. They now produce millions of credits annually. Marine and mangrove projects are also gaining attention. They offer strong environmental benefits and long-term carbon storage.

- Industrial projects focused on nitrous oxide reduction are expanding as well. These projects are highly measurable and align well with compliance systems. At the same time, regenerative agriculture is growing at the fastest pace. It has moved from almost no activity to millions of credits in a short time.

These new categories are helping the market grow. However, quality remains the key factor that drives demand.

Buyers Shift Toward Better Credits: Regional Analysis

Buyer behavior is changing across regions. The United Kingdom is leading the move toward high-quality credits. Companies are under pressure to show real climate action. This has pushed them to choose better credits.

The United States and Canada are also improving. Buyers prefer projects that meet both voluntary and compliance standards. This supports demand for high-quality supply.

North America Sets the Benchmark

North America sets the benchmark for quality. A large share of its credits meets high rating standards. This strong quality supports higher prices. The average price reached $14.80, the highest globally. Strong domestic demand and strict standards drive this trend.

On the other hand, South America is seeing strong demand but limited new supply. This creates pressure in the market. Prices have slightly declined to $11.50. However, the quality mix is improving. Waste projects are helping fill the gap left by falling forestry supply.

- Europe remains the largest market by volume. However, the quality mix is still uneven. Some buyers continue to use lower-rated credits.

- Japan and South Korea focus on lower-cost options like hydropower. This keeps their share of high-quality credits low. In Latin America, buyers often choose local projects. Limited regulatory pressure keeps the quality demand weaker.

- Africa is moving toward better quality. High-rated supply is increasing, while low-rated supply is falling. As explained before, cookstove projects are the main driver. At the same time, lower-quality forestry projects are declining. This improves the region’s overall market position.

- Asia faces weaker market conditions. Supply has dropped sharply due to fewer renewable energy projects. The average price stands at $5.30, the lowest globally. Demand remains steady but lacks strong growth. This keeps prices under pressure.

Indonesia Stands Out in Asia

Indonesia is a bright spot in the region. Credit prices have risen strongly in the past year. High-quality peatland projects are driving this growth. International deals under Article 6 are also adding value. These factors attract buyers looking for reliable credit.

This shows how strong quality and supportive policies can boost market performance.

Final Take: Quality Defines the Future

The carbon market in 2026 is clear and focused. Quality now drives demand, pricing, and growth. Buyers are becoming more selective. They want credits that are verified, reliable, and compliant.

Supply remains tight, especially for high-quality credits. At the same time, compliance markets are growing. This increases competition and pushes prices higher.

The gap between high- and low-quality credits will continue to widen. In simple terms, the market is no longer about how many credits exist. It is about how good they are.

- READ MORE: Top Carbon Credit Companies to Watch in 2026

The post Carbon Market 2026: Supply Squeeze Pushes Premium Carbon Credit Prices Up, Sylvera Finds appeared first on Carbon Credits.

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits